ABSTRACT

Creative accounting involves the manipulation of company’s records toward a predetermined target. Financial information manipulation is usually aimed at misleading the users of financial reporting through the provision of information that affects their decision making. This study evaluated the effects of creative accounting on investment decision in selected listed manufacturing firms in Nigeria’s real sector for the period of 2007 to 2017. The study was empirically carried out by extracting related data from CBN statistical bulletin and NDIC annual reports for the period on which regression analysis was used. The result revealed a positive but insignificant effect of creative accounting on investment decisions in listed manufacturing firms in Nigeria’s real sector as it reflects in the adjusted R2 of 0.742983 or 74.30%. The study therefore concluded and recommended that proper corporate governance should be applied to ensure that creative accounting is used for stakeholder’s benefits.

Key words: Creative accounting, investment decision, stakeholders’ interest.

Today’s financial accounting reports focus on providing relevant, reliable and timely financial information to stakeholders who use it to make critical financial decisions (Obara and Nangih, 2017). Financial accounting reports are meant to provide financial information so that stakeholders and other users of such information can use it for informed decision. However, current accounting practice allows a degree of choice of policies and professional judgement in determining the methods of measurement, criteria for recognition and even the definition of the accounting entity. The exercise of this choice can involve a deliberate non-disclosure of information and manipulation of accounting figures, thereby making the business appear to be more profitable and financially stronger than it is supposed to be. With this practice, users of accounting information are being misled and this constitutes a threat to corporate investment and growth (Akenbor and Ibanichuka, 2012; Osisioma and Enahoro, 2006).

Nangih (2017) argued that financial statements are signposts which direct users on the path of decision making. Such important reports upon which financial decision are based are expected to be reliable, understandable, comparable, transparent and free of bias.

The manufacturing sector is a critical growth driver for any country. The sector is regarded as a basis for determining a nation’s economic efficiency, notwithstanding there exist gross under-performance of the real sector, particularly manufacturing firms. Firms are expected to meet shareholder’s expectation because shareholders are concerned with firm’s long term survival.

As a way to preserve the value of principal-agent relationship, financial statements may be distorted by directors to achieve a targeted objective (Bowen et al., 2008). However, inadequate or misleading income disclosure may result when income is deliberately and artificially presented (Ashari et al., 1994). Also expenses can be postponed or understated, which has the same effect as misleading income disclosure. Financial statement is arguably the most useful and important to all users especially for the shareholders or investors in decision making process because they can obtain useful information about the effectiveness of the organisation (Khamangy and Sadeeg, 2015).

Creative accounting may lead shareholders and investors to have inadequate information when evaluating organizational effectiveness. The Cadbury saga in Nigeria revealed a significant overstatement of its financial figures over several years. The unpleasant circumstances are similar to Enron’s case in the United States of America, where the company, which rose to the peak as America seventh largest company in just fifteen 15 years, was discovered to have manipulated the company’s profit (Amatorio, 2005). According to Sanusi and Izedomi (2014), the challenge of creative accounting is the conflict of interest among the various stakeholders in business. The conflict is so wide as it is seen in the situation where, management’s interest lies in the payment of less tax and dividends as against the shareholders’ interest of getting more dividend and employees interest of earning better salary and higher profit share all at the same time. However, creative accounting satisfies one group’s interest at the expense of the others.

According to Fizza and Qaiser (2015), corporate governance is expected to be able to control the practices of creative accounting because transparency in the financial reporting is of utmost importance as individual, potential investors, creditors and regulators have to make investment decisions based on corporate published financial reports (Wokukwu, 2015). Aside from corporate governance, the activities of the external auditors should also guide against creative accounting, if done properly. There are both positive and negative perspectives of creative accounting practice. Both the management and the owners of the firm may benefit from creative accounting practice. According to Gabar (2015) and Gaara et al. (2015), the misuse of creative accounting techniques worries users of accounting information as it also affects the reliability on the financial statement.

Several authors have tried to investigate the concept of creative accounting and the various techniques used by management to manipulate financial statements. However, the impact of creative accounting practices on shareholders investing decision has not been given much attention. Moreover, most studies on creative accounting are of foreign origin (Fizza and Qaisar, 2015). It is against this background that this study investigated the effect of creative accounting on investment decision in listed manufacturing firms in Nigeria (Appendix Table 1

This section is made up of conceptual review, theoretical framework and empirical review.

Conceptual review

Creative accounting involves both performance statements and financial positions manipulation. Accounting manipulation is the deliberate alteration and falsification of financial information to satisfy the management with the intention to deceive users either by creating conceivable position of the firm to outsiders or satisfying the expectation of owners of the organisation. According to Paolone and Magazzino (2014), accounting manipulation can be categorised into two separate groups: creative accounting (by maintaining the legitimacy of accounting practices) and accounting fraud (by violating the accounting policy and principles or earnings manipulation). Creative accounting also referred to as income smoothing, earnings management, earning smoothing, financial engineering and cosmetic accounting is one of the emerging issues in financial reporting. Stolowy and Breton (2004) described creative accounting as an assemblage of procedure in order to change the profit by either increasing or decreasing the financial record.

Farlex (2012) defined creative accounting as the practice of recognizing revenue as well as manipulation of expenses in a way that makes a company appear better than it actually is, while still conforming to the Generally Accepted Accounting Principles (GAAP). In support of this definition, Ali et al. (2011) submitted that creative accounting practices are done with the intention of making the financial statements appear better and financially stronger, on one hand, or financially weaker, on the other hand, depending on management’s desire.

Ezeani et al. (2012) posited that creative accounting was responsible for various financial crises and portend a serious challenge to the accounting profession. They further argued that when creative accounting is done with extreme negative intentions, it affects the credibility of financial statements and decisions of its users. This is because the accounting principles and standards are manipulated to hinder the reliability, objectivity and comparability of such statements. Hence decisions based on such financial reports may be misleading and faulty.

Investment decisions

Investment decisions or analysis needs to do with an effective investment of capital (Pandey 2005). Investment decisions concern the distribution and utilization of resources and fund for future returns (Chen, 2013). The choice on whether or not to make investments is based on the investors’ goal; the capacity to finance the investment and how to fund the investment. For a good investment decision, the investor needs to see, completely and correctly understand the possible opportunities of the investment and this investment decision should not be rushed as a bad investment decision can lead companies to bankruptcy (Virlics, 2013). Investment decision cannot be made in a vacuum by relying upon the analysis and complex models, thus investors must be watchful and up to date to achieve the desired goals (Farooq and Sajid, 2015).

Entities owe an obligation to completely reveal matters concerning their activities to help investors in making informed choices (Anaja and Onoja, 2015). Investors are rational beings and they apply financial techniques and plan their investments on risk-return basis (Okere et al., 2018). Corporate organizations have the duty to thoroughly plan and distribute their audited report to investors and different clients. Investment decision includes the dedication of current assets into long term projects for future advantages. Investment decision is extremely crucial and caution must be taken in light of the fact that huge, rare and hard-earned resources are included, permanent in nature, hazardous and have long term suggestion which no investor would need to be stood up to with if negative outcomes happened (Patrick et al., 2017).

Wealth creation in a capitalist economy like Nigeria is based on trust. Investors invest their resources in companies and they produce goods and services to benefit the nation as a whole. Good investment decision is based on information provided by organisations to existing and potential shareholders. Therefore, good information provided is essential to effective growth of capital markets and a productive allocation to economic resources. The investor must have confidence in the financial information provided before they can invest their resources and this is largely dependent on availability of accurate and timely reliable information. It is a matter of great concern to parties who are interested in the financial statements of entities when the system cannot be relied on as a result of creativity and deceitfulness of financial managers to deliver inaccurate information to enable investor evaluate the investment opportunities (Ahmed, 2017).

Investment will lead to increase in employment and development of the economy. This is why it is important to all stakeholders in the development of the Nigerian economy to discourage creative accounting knowing that capital formation process depends largely on investors’ confidence in financial information provided. This should be an issue of great concern to professional accountants, stakeholders and federal government to protect investor from fraudulent firms or individuals who may want to defraud investors to enrich themselves. This will make investors more enlightened and able to guard against losing their investment (Essien and Ntiedo, 2018).

Theoretical framework

Numerous researchers have applied different theories in examining creative accounting. This study is anchored on the legitimate theory, the justification of which is hereby explained:

Legitimacy theory

Legitimacy theory was derived from the concept of organisational legitimacy which was defined by Dowling and Preffer in 1975. Legitimacy theory posited that organisations frequently seek to ensure that they operate within the limits and norms of their respective societies. The legitimacy theory is a device that supports organisations in implementing, developing voluntary social and environmental disclosures in order to accomplish their social contract that enables the recognition of their objectives and the survival in an unstable environment.

Legitimacy theory according to Dowling and Preffer (1975) and Guthrie et al. (2007) is a situation which exists when an entity’s value system is harmonious with the value system of the larger social system of which the entity is a component. Legitimacy theory results from the model of organisational legitimacy. This theory can be seen from two levels: institutional level (concerned with how organisational structures gain support and empowerment by the community at large which eventually make organisations seem natural and meaningful) and organisational level (concerned with how organisations, through their activities and procedures, establish, maintain, extend and protect their legitimacy).

In support of the legitimacy theory, Mousa and Hassan (2015) submitted that it may help to explain the motivations of companies to engage in environmental reporting and also provide a foundation for understanding how and why companies may use external reports to benefit themselves. By extension, the financial statements are expected to notify the stakeholders on the present financial position of the organisation and also determine whether or not the organisation is a going concern.

Therefore, financial statements are prepared to disclose the present position of a company; it reveals if the business is making profit and providing a return on shareholder’s investment. However, prior studies have shown that this is not always the case as creative accounting is sometimes used by companies to manipulate profit figures which distort the true financial health of the company.

Empirical review

Several researches (with only few of them in Nigeria) have been carried out relating to creative accounting, earnings management, incomes smoothening and how it impacts investment decisions.

Ubogu (2019) investigated the effect of creative accounting on shareholders’ wealth in business organization: a case study of selected banks in Delta State. The findings revealed a positive and significant relationship between creative accounting and decision making of an organisation. The study submitted that creative accounting affects shareholders’ wealth and their various investments decisions because it has a great impact on the share prices of the business organisation. The study suggested that only well and legally audited financial statements should be relied on by shareholders in making important decision.

Essien and Ntiedo (2018) examined the extent to which accounting reports and disclosures provides shareholders and other interested parties with reliable information to permit informed investment decisions and true valuation of firms has remained in doubts. Using survey method, the study revealed that accounting creativity contributes 90% to unfair reporting of firm’s operations. Thus, the creativity in those practices is motivated by greed and intention to deceive the public, potential investors and shareholders and increases the rate of enterprise failures at a decreasing rate. However, the study revealed that the many regulations without adequate checks, punishments and rewards creates conducive conditions for creative accounting in providing the opportunity for fantasize and cosmetic financial reporting.

Ahmed (2017) examined the impact of creative accounting techniques on the reliability of financial reporting with particular reference to Saudi auditors and academics using quantitative research design with both primary and secondary data. The finding revealed that the effect of creative accounting cannot be totally eliminated but could be mitigated by proactive corporate governance principles using independent non-executive directors. The study also suggested that statutory auditors can play an effective role in reducing the effect of creative accounting techniques on the reliability of financial reporting.

Umobong and Ironkwe (2016) examined creative accounting and firms’ financial performance using seasonal trading reports. The findings showed that seasonal trading reports had no significant relationship with Return on Assets (ROA), Return on Equity (ROE) and Earnings Per Share (EPS) and not used to manipulate ROA, ROE and EPS. Seasonal trading report had negative relationships with performance variables and they concluded that an increase in seasonal trading report decreases performance. While Nangih (2017) examined empirically the effect of creative accounting practices on the quality of financial statements of oil servicing companies in Nigeria using ordinary least squares regression techniques. Results of the findings revealed that creative accounting practices by oil servicing companies influenced the quality of their financial statements negatively.

Fizza and Qaisar (2015) empirically and essentially investigated the problem of creative accounting in financial reporting. Both descriptive and inferential statistics were used to simplify the results and concluded the findings. The finding revealed that creative accounting plays significant role in financial reporting but has been negatively correlated, which implies that the higher the number of managers involved it, the lower the value of financial information disseminated to investors and other users.

Leyira and Okeoma (2014) examined whether creative accounting and organisational effectiveness has any significant relationship, using correlation statistics, all the hypotheses were found to be statistically significant and positively correlated. However, they found weak evidence of a positive correlation between income smoothing, artificial transaction and market share. Ijeoma (2014) examined the effect of creative accounting on the Nigerian banking industry and attributed the major reason for creative accounting practices in the Nigerian banking industry inflating the operating costs so as to reduce taxable profits. The findings of previous studies lacked consensus, thus showing a research gap which calls for further researches on this topic which motivated this study.

This study adopted ex-post facto research design. The population of the study is all the 66 manufacturing firms listed on the Nigerian Stock Exchange (2017). However, to conduct a meaningful research, ten manufacturing firms were randomly selected based on full data availability. Data were extracted from the annual report for the period of 2007 to 2017. The research objective was achieved using the panel ordinary least square method. The panel data method is widely recommended for it is useful when data is a combination of time-series and cross-sectional features.

Model specifications

This study adapted the econometric model of Umobong and Ibanichuka (2016). The functional relationship between the dependent and independent variable, the disturbance, co-efficient and intercepts for accounting manipulations and financial performance for the purpose of the research is as stated below:

INVD = f (CA, FSIZE) (1)

INVDit = β0 + β1CAit + β2FSIZEit + Uit (2)

Where:

INVD: Investment Decisions

CA: Creative Accounting

FSIZE: Firm Size

Measurement of variable

Dependent variable

Investment Decisions: Natural logarithm of shareholders fund

Independent variable

Creative accounting

The dependent variable in this study is creative accounting. However, based on prior literature, it was observed that the Modified Jones model is the most famous and most frequently used model for detecting earnings management. Based on the nature of the study at hand and the data set available, this study used the OLS regression method to analyse the secondary data. The Modified Jones Model was adopted to determine the unrestricted element of accruals as it is easier to handle earnings via credit sales than cash collections, aside from controlling for endogeneity bias in the creative. Also, it is commonly used for addressing problems relating to management unrestricted behaviours. For the calculation of earnings management, the cash flows statement approach is adopted in this study for the calculation of total accruals.

TA/A(t-1) = β1{1/At-1} + β2 {(Δ in REV- Δ in REC)/At-1) + β3{PPE/At-1} + €it (i)

where:

TAit = Total accruals in year t for firm i

ΔREVit = Revenue in year t less revenues in t-1 for firm I (change in revenue)

ΔRECit = Receivables in year 1 less receivables in year t-1 for firm 1 (change in receivables)

PPEit = Gross property, plant and equipment in year t for firm 1.

Ait-1 = Total assets in year t-1 for firm in year t-1 for firm I (total assets for previous year)

β1, β2, β3 = represents firms’ specific parameters

€ = residual here represents the firm specific discretionary portion of accruals.

However, while the right side of the equation represents the non-discretionary accruals (NDA), the net result for the left side of the equation amounts to the total accruals (TA). Nevertheless, taking the difference between the total accruals and the non-discretionary accruals; it amounts to the discretionary accruals (DA) which is basically used in this study to represent earnings management. Hence, the higher the value of discretionary accruals, the more likely the presence of earning manipulation and vice versa as depicted in equation (ii):

DAi-t = TACit/Ait-1 - αt [1/Ait-1] + α1i [(ΔREV- ΔREC)/Ait-1] + α2i [PPEit/Ait-1] + ϵit (ii)

Control variable

Firm Size: Natural logarithm of total asset of a firm

Data presentation and analysis

This section empirically reviewed the effect creative accounting on investment decision in listed manufacturing firms in Nigeria for the period of 2007 to 2017. The analyses were conducted using E-Views software. The data were analysed using the correlation matrix and the panel OLS and the finding fully discussed.

Descriptive tests

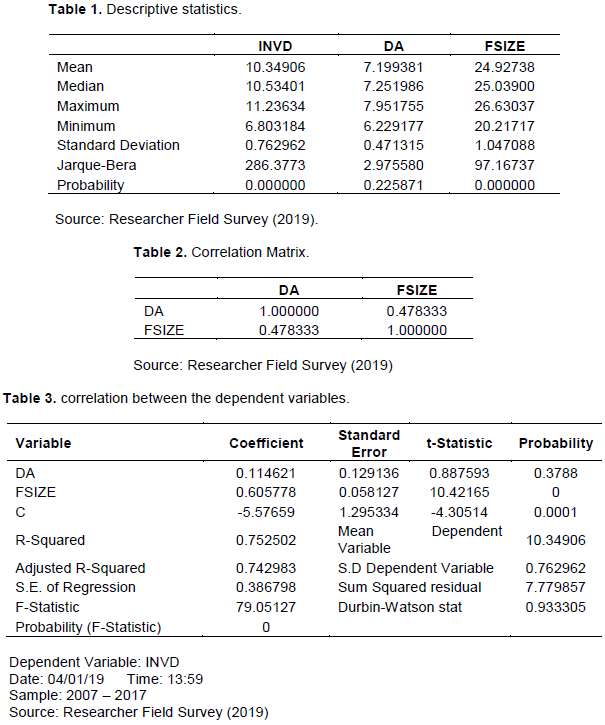

The descriptive statistics is presented for the variables as shown in Table 1. The result revealed that INVD has a mean of 10.34906bn with standard deviation of 0.762962 while the Maximum and minimum values are 11.23634 and 6.803184 respectively. DA has a mean of 7.199381bn with standard deviation of 0.471315, while maximum and minimum values are 7.951755 and 6.229177 respectively. Also FSIZE has a mean of 24.92738bn with standard deviation of 1.047088, while maximum and minimum values are 26.63037 and 20.21717 respectively. The Jacque-Bera statistics shows the normality level of the data set and INVD and FSIZE are significant at 5% level and DA is insignificant at 5% level of significant.

Correlation analysis

Table 2 shows the correlation between the independent variables. It also reveals if there exists multicollinearity between the variables under study. It can be seen that discretionary accrual (DA) has a positive relationship with firm size (FSIZE). Also, in relation to the 80% multicollinearity benchmark by Okere et al (2018), the analysis shows an absence of multicollinearity.

REGRESSION ANALYSIS AND DISCUSSION

A closer examination of the regression result shows that creative accounting has a positive but insignificant relationship with dependent variable (INVD) (t-stat = 0.887593 and p value = 0.3788>0.05) (Table 3). On the other hand, firm size positive sign was equally appropriate but significant to the dependent variable (INVD) (t-stat = 10.42165 and p value = 0.0000<0.05. thus indicating the quantum and quality of investment decisions for the period under review.

Considering the individual coefficient of the explanatory variables, the result that is explicit in the study is that firm size is a strong factor in the determination of investment decision by manufacturing sector in Nigeria. The coefficient of the variable is significant at the 5% level and also has a positive sign/effect indicating that as firm size increases for the manufacturing companies, creative accounting also increases significantly. Firm size has a significant impact on creative accounting. The R-Squared and adjusted R-Squared are 75 and 74%, respectively. This depicts that 74% of changes in the dependent variable can be explained by the independent variables, while the remaining 26% can be explained by factors other than the independent variable. The F-statistics value of 79.05127 at 5% implies that a strong relationship exists between the dependent variable and the independent variables, while the p-val. of 0.0000 also implies a significant effect. Therefore, it can be expressed that there is a significant effect of creative accounting (DA, FSIZE) on investing decisions in listed manufacturing firms in Nigeria. The Durbin Watson of 0.93 reflects presence of positive serial autocorrelation in the data set and this is often present in time series data.

Examining the coefficients, the result revealed that discretionary accruals has a positive but insignificant relationship with investing decisions of listed manufacturing firms in Nigeria. This depicts that a unit change in creative accounting (DA) would bring about a 12% increase in investing decisions by shareholders in listed manufacturing firms in Nigeria. The control variable (FSIZE) has a positive and significant relationship with investing decisions by shareholders in listed manufacturing firms in Nigeria.

Evaluating the analysis, the R-squared and adjusted R-squared are 75 and 74% respectively. This depicts that 74% of changes in the dependent variable can be explained by the independent variables. The F-statistics is 79.05127 and significant at 1, 5 and 10% level. This shows the statistical significance of the model. Therefore, it can be expressed that there is a significant effect of creative accounting (DA, FSIZE) and investing decisions in listed manufacturing firms in Nigeria. The Durbin Watson is 0.93 which shows presence of positive serial autocorrelation in the data set and this is often present in time series data.

Examining the coefficients, it can be seen that discretionary accruals has a positive but insignificant relationship with investing decisions of listed manufacturing firms in Nigeria real sector. This depicts that a unit change in creative accounting (DA) would bring about a 12% increase in investing decisions by shareholders in listed manufacturing firms in Nigeria real sector. The control variable (FSIZE) has a positive and significant relationship with investing decisions by shareholders in listed manufacturing firms in Nigeria real sector.

The results of our findings are consistent with the study of Essien and Ntiedo (2018) on the extent of accounting reports and disclosures provision to shareholders and other interested parties with reliable information could permit informed investment decisions and true valuation of firms which found that creative accounting is euphemism and contributes 90% to the unfair reporting of firm’s operations. In consonant with our study is the work of Ubogu (2019) which further buttressed the point that a positive and significant relationship exists between creative accounting and decision making of an organization as only well and legally audited financial statements should be relied on by shareholders in making important decision. However, Fizza and Qaisar (2015) submitted that creative accounting plays significant role in financial reporting but has been negatively correlated that means more managers involved in it may decrease the value of financial information.

This study examined the effect of creative accounting on investment decision in listed manufacturing firms in Nigeria. Using panel regression analysis, it was discovered that creative accounting has a positive but insignificant effect on investment decision in listed manufacturing firms in Nigeria. This depicts that there are positive benefits of earnings management which is dependent on the motive of management. A company tries to gain greater investors’ confidence by increasing its market share when assessing the financial statement through smoothing of its income.

The following recommendations are made in line with the findings:

(i) There is urgent need for monitoring companies’ activities in order to raise the quality of financial reporting in Nigeria. This can be achieved in determining which accounting manipulation is kept within the limits of legality (creative accounting and which one is violation of accounting principles and policies (Accounting Fraud).

(ii) Emphasis should be placed on the enforcement of code of corporate governance and ethics by entities, through enactment of relevant law by the legislatures. Also all changes in accounting regulations and standards as well as ethical standards by regulatory authorities should be enforced to prevent entities from employing misleading reporting practices of creative accounting (Nag, 2015; Amat and Gowthorpe, 2010).

(iii) Proper internal control mechanisms should be put in place by companies, to check the problem of profit smoothing and other creative accounting practices, which had been responsible for several collapses of companies in Nigeria and beyond.

(iv) The Financial Reporting Council of Nigeria and other regulatory bodies should be more proactive in the discharge of their duties, as this will check negative manipulations of financial information by preparers for selfish gains.

The authors have not declared any conflict of interests.

REFERENCES

|

Ahmed YAI (2017). The impact of creative accounting techniques on the reliability of financial reporting with particular reference to Saudi auditors and academics. International Journal of Economics and Financial Issues 7(2):283-291.

|

|

|

|

Akenbor C, Ibanichuka E (2012). Creative accounting practices in Nigerian banks. An International Multidisciplinary Journal Ethiopia 6(3):23-34.

Crossref

|

|

|

|

|

Ali SSZ, Butt S, Tariq YB (2011). Use or abuse of creative accounting techniques. International Journal of Trade, Economics and Finance 2(6):1-20.

|

|

|

|

|

Amat O, Gowthorpe C (2010). Creative accounting: Nature, incidence and ethical issues. Journal of Economic Literature Classification M4:11-15.

|

|

|

|

|

Amatorio I (2005). Creative accounting nature incidence and ethnic issues. Journal of Economic Literature Classification 2005:1-6.

|

|

|

|

|

Anaja B, Onoja EE (2015). The role of financial statements on investment decision making: a case of United Bank of Africa Plc. European Journal Business, Economics and Accountancy 3(2):12-36.

|

|

|

|

|

Ashari N, Koh H, Tan S, Wong W (1994). Factors affecting income smoothing among listed companies in Singapore. Accounting and Business Research 24(96):291-301.

Crossref

|

|

|

|

|

Bowen RM, Rajgopal S, Venkatachalam, M (2008). Accounting discretion, corporate governance and firm performance. Contemporary Accounting Research 25(2):351-405.

Crossref

|

|

|

|

|

Chen HL (2013). CEO Tenure and R&D Investment: The moderating effect of Board capital. The Journal of Applied Behavioural Science 49(4):437-459.

Crossref

|

|

|

|

|

Dowling J, Preffer, J (1975). Organisational legitimacy: social values and organizational behavior. Pacific Sociological Review 18(1):122-136.

Crossref

|

|

|

|

|

Essien EA, Ntiedo JU (2018). The influence of creative accounting on the credibility of accounting reports. Journal of Financial Reporting and Accounting 16(2):292-310.

Crossref

|

|

|

|

|

Ezeani E, Ogbonna I, Ezemoyih M (2012). The effect of creative accounting on the job performance of accountants (auditors) in reporting financial statement in Nigeria. Kuwait Chapter of Arabian Journal of Business and Management Review 33(845):1-30.

|

|

|

|

|

Farlex (2012). Financial Dictionary. USA. Farlex Inc.

|

|

|

|

|

Fizza T, Qaisar AM (2015). Creative accounting and financial reporting: Model development and empirical testing. International Journal of Economics and Financial Issues 5(2):544-551.

|

|

|

|

|

Farooq A, Sajid M (2015). Factors Affecting Investment Decision Making: Evidence from Equity Fund Managers and Individual Investors in Pakistan. Research Journal of Finance and Accounting 6(9):135-141.

|

|

|

|

|

Gaara OA, Aladah AK, Abotaman M (2015). The effect of financialists' awareness about creative accounting practices on cashflow statement. Managerial Sciences 1:227-246.

|

|

|

|

|

Gabar SN (2015). The impact of creative accounting techniques on the reliability of financial data, field study on some public companies in Iraq. Algary for Managerial and Economics Science Journal, Alkofa University 32:238-264.

|

|

|

|

|

Guthrie J, Cuganesan S, Ward L (2007). Extended performance reporting: evaluating corporate social responsibility and intellectual capital management. Issues in Social and Environmental Accounting 1(1):1-25.

Crossref

|

|

|

|

|

Ijeoma NB (2014). The effect of creative accounting on the Nigerian Banking Industry. International Journal of Managerial Studies and Research 2(10):13-21.

|

|

|

|

|

Khamangy B, Sadeegy M (2015). The real of creative accounting practices in Algerian environment and how to exclude from financial reporting. The Journal of Algerian Enterprises 8:61-78.

|

|

|

|

|

Leyira CM, Okeoma C (2014). The impact of creative accounting on organizational effectiveness: a study of manufacturing firms in Nigeria. British Journal of Economics Management and Trade 10:2107-2122.

Crossref

|

|

|

|

|

Mousa GA, Hassan NT (2015). Legitimacy theory and environmental practices: short notes. International Journal of Business and Statistical Analysis 2(1):41-52.

Crossref

|

|

|

|

|

Nag AK (2015). Is creative accounting ethical: An analysis into pros and cons. Indian Journal of Applied Research 5(2):83-84.

|

|

|

|

|

Nangih E (2017). Nexus between creative accounting practices and financial statements quality in Nigeria: A reflection of oil servicing companies in Port Harcourt metropolis. Journal of Accounting and Financial Management 3(3):64-71.

|

|

|

|

|

Ndebugri H, Tweneboah SE (2017). Analyzing the Critical Effect of Creative Accounting Practice in the Corporate Sector of Ghana. Available at:

View

Crossref

|

|

|

|

|

Obara LC, Nangih E (2017). International Public Sector Accounting Standards (IPSAS) Adoption and Governmental Financial Reporting in Nigeria-An Empirical Investigation. Journal of Advances in Social Science and Humanities 3(01):1-11.

|

|

|

|

|

Okere W, Imeokparia L, Ogunlowore J, Isiaka M (2018). Corporate social responsibility and investment decisions in listed manufacturing firms in Nigeria. Journal of Economics, Management and Trade 21(4):1-12.

Crossref

|

|

|

|

|

Osisioma BC, Enahoro JA (2006). Creative accounting and option of total quality accounting in Nigeria. Journal of Global Accounting 2(1):5-15.

|

|

|

|

|

Pandey IM (2005). What drives the shareholder value? Asian Academy of Management Journal of Accounting and Finance 1(1):105-120.

|

|

|

|

|

Paolone F, Magazzino C (2014). Earnings Manipulation among the Main Industrial Sectors. Evidence from Italy. Economia Aziendale Online 5(4):253-261.

|

|

|

|

|

Patrick ZI, Tavershima A, Eje EB (2017). The effect of financial information on investment decision making by shareholders of Banks in Nigeria. IOSR Journal of Economics and Finance 8(10):20-31.

Crossref

|

|

|

|

|

Sanusi B, Izedonmi PF (2014), Nigerian commercial banks and creative accounting practices. Journal of Mathematical Finance 4:75-83.

Crossref

|

|

|

|

|

Stolowy H, Breton G (2004). Accounts manipulation: A literature review and proposed conceptual framework. Review of Accounting and Finance 3(1):5-92.

Crossref

|

|

|

|

|

Ubogu FE (2019). Effect of creative accounting on shareholders' wealth in business organization: a study of selected banks in Delta State in Nigeria. International Journal of Social Sciences and Humanities Review 2(2):44-62.

|

|

|

|

|

Virlics A (2013). Investment decision making and Risk. Procedia Economics and Finance 6(1):169-177.

Crossref

|

|

|

|

|

Umobong AA, Ibanichuka EAL (2016). Accounting manipulations and firms' financial performance: Evidence from Nigeria. European Journal of Accounting, Auditing and Finance Research 4(10):30-47.

|

|

|

|

|

Wokukwu K (2015), Creative accounting: Unethical accounting and financial practices designed to boost earnings and to meet financial market expectations. Journal of Business and Economics Policy 2(1):39.

|

|