Full Length Research Paper

ABSTRACT

Management accounting in recent times, and perhaps rightly so, has begun to gain recognition as a profession separate and complimentary to financial accounting. Evidence exists to suggest that management accountants are exposed to a unique set of ethical challenges within industry and that a significant high number of management accountants have engaged in unethical practices in performing their jobs. For the accounting profession as a whole, the growing number of corporate failures has created a credibility crisis that requires a deliberate intervention to mitigate. If this is not addressed sooner, the accounting profession stands the risk of losing relevance. Scholarship on ethical issues in accounting practice have either focused mostly on financial accounting or have sought to combine ethical issues for financial and management accounting. Various arguments have been made in recent times of the need to treat ethical issues in behavioural studies as context-specific and therefore separate ethical considerations in management accounting from financial accounting. This study adopts an approach, following various literature, that effective ethics education can help practitioners deal appropriately with ethical issues at the work place, and explores students’ and faculty members’ perceptions on current practices in ethics education. As expected, faculty and students differ significantly on a wide range of issues on ethics education in management accounting. Based on the insights provided from this study, appropriate recommendations have been made to improve ethics education in management accounting.

Key words: Management accounting, ethics education, ethics, accounting scandals.

INTRODUCTION

Even though most research on ethics have focused on general business ethics, rather than ethical issues on functional areas of management (Bampton and Cowton (2002a), research on accounting ethics has gained significant relevance in recent times perhaps owing to concerns around the credibility of organizational reporting vis-à-vis the spectacular corporate scandals and failures (Adkins and Radtke, 2004) as well as concerns about appropriateness of executive mitigating unethical behaviour in business practice (Loeb, 1998) with mixed results (Adkins and Radtke, 2004). Research on ethics has been on the increase, particularly in developed countries (Bampton and Cowton, 2002a).This surge in empirical studies on organizational ethical dilemmas have mostly taken place in developed countries with very few studies about business ethics in developing countries including Africa. Even in developed countries that have experienced phenomenal increase in academic attention to ethical issues, studies have raised concern that ethics education remains on the periphery and in most cases has not been comprehensively integrated into mainstream educational curriculum (Bampton and Cowton, 2002b).

Hopper et al. (2009) and Needles (1976) argue for contextual studies (in line with contingency theory) on behavioural issues to strengthen the generalization power of any given theory. Tsamenyi et al. (2004) and Hopper et al. (2009) call for more empirical studies on behavioural, social and developmental issues in Africa. Tsamenyi et al. (2004) and Hopper et al. (2009) particularly make a compelling case for further empirical studies on management accounting issues in Africa.

Hopper et al. (2009) argue that even though many contextual factors and issues may not be unique to developing countries, developing countries still remain largely distinctive such that it will be wrong to categorise accounting research about developing countries as ‘exotic and irrelevant’ to mainstream accounting studies. Hopper et al. (2009) argue for more research in management accounting in developing countries aimed at fostering understanding that encourages local solutions to local challenges rather than wholesale adoption of western proposed solutions based on alien values. Bampton and Cowton (2002a), and Armstrong (1993) argue that ethics education will be more relevant if it moves a step beyond general business ethics education into purposively-designed ethics curriculum integrated into the various functional areas (or subjects) of management such as management accounting. This may be effective in bridging the gap between ethics theory and relevant business practice and perhaps more helpful in improving general ethical behaviour vis-à-vis, the current trend of significantly high unethical and partially unethical management accountants in business practice (Evan et al., 2001).

Following the scholarly interest in business ethics and accounting ethics education, most business schools, at least in developed countries, have attempted to integrate business ethics into their curriculum (Loeb, 1998), even though the focus seems to be on general business ethics (Cole and Smith, 1995) with an approach to education that treats ethics as peremptory, with a lack of commitment from academics (Gunz and McCutcheon, 1998) resulting in relatively limited discussion of critical ethical issues in the classroom (Adtkins and Radtke, 2004). Duska and Duska (2003) argue for ethics education in accounting. Where research has attempted to explore ethical issues among financial and accounting

practitioners, the focus has been on ethical issues in financial accounting and auditing (Shah, 1996), with very limited literature, albeit evolving, on ethical issues in management accounting (Amstrong, 1985). This skew poses a challenge in that studies on ethical issues in management accounting are equally relevant to general business practice and investor value growth especially following the recent scandals within public and private organizations that provide evidence of laxity in governance, breaches of control systems, and deliberate misreporting of managerial performance in order to earn underserved executive compensation (Armstrong, 1985). Management accountants face significant ethical dilemmas at work. Fisher and Lovell (2000), for instance categorizes 45 ethical issues that management accountants face at the work place.

Because management accounting is integrated into the management process and concerned with supporting managerial decision making around planning, resource accountability and control, competitive strategy, resource allocation and performance evaluation, it may be appropriate to posit that ethical issues in management accounting have a more pronounced effect on resource allocation, investment value, business success and effectiveness. Management accounting is quite distinct in purpose and operational methodology from financial accounting and therefore exposed to varied considerations of ethical issues. Indeed the creation of separate professional bodies of management accountants emphasizes this difference. As an example, financial accountants are governed by an established framework of regulations that perhaps provides a guiding framework for decisions involving ethical concerns. Management accounting on the other hand, has no set of standards or regulations on operational methodology and any efforts at developing a professional code of ethics is affected by this inherent limitation. Management accountants may therefore be more exposed to scenarios requiring ethical considerations on a regular basis than financial accountants; and more worrying, management accounting may probably involve more situations of unethical conduct (due to the absence of standards or regulations) than financial accounting. As well, if education in ethics can mitigate unethical behaviour in organizations (McNeel, 1994) and if this effect is more pronounced if education in ethics moves beyond general business ethics to integrating ethics into specific subjects related to the functional areas of management (Bampton and Cowton, 2002b), then more studies are required about ethics education in management accounting.

Research problem

Studies confirm that accountants lag behind other college graduates in moral development (e.g. Shaub, 1995). As well, the various accounting scandals may have created a credibility crisis for the accounting profession, which remains till today (Adkins and Radtke, 2004) and hopefully studies on ethics education may go a long way to help accountants regain their credibility and re-affirm their relevance.

This study attempts to explore current practices in ethics education in management accounting within the context of a developing country. Specifically, this study explores how ethical issues are integrated into teaching of management accounting in universities in Ghana.

Beyond the explicit relevance of further studies in ethics education in management accounting (Bampton and Cowton, 2002a), and in Africa (Hopper et al., 2009), the choice of management accounting was based on two further reasons. Firstly, this study ties into a broader study on business ethics the researchers are undertaking. Secondly, because management accounting, compared to financial accounting, ties in more easily with general business management (Bampton and Cowton, 2002a), studies on ethics education in management accounting lends itself more easily to borrowing from theoretical prepositions existing in the literature on general business ethics to explain any observations and findings.

This study adds to the growing literature on business ethics by focusing on a scarcely researched subject area (ethics education in management accounting), in Africa. Despite the numerous calls for more empirical studies in Africa, very little of such studies take place. With the attention Africa is receiving from multinational organisations and private investors, following the economic crisis in western economies, relevant empirical studies are required to guide government policy and business decisions.

Africa as a place of inquiry presents an intriguing set of challenges and opportunities. Africa presents an opportunity for new knowledge that, perhaps, may have a greater positive correlation with social development than in advanced countries. If the purpose of research is to promote social development and human progress, then a compelling case arises for continuous empirical studies in Africa.

The rest of the study is organised as follows. The next section discusses the conceptual basis and the existing literature relevant to this study. The third section discusses the research methodology. The fourth section presents the research findings. Section five presents the conclusions of the study, possible limitations of the research and makes recommendations as well as suggestions for future research.

LITERATURE REVIEW AND CONCEPTUAL BASIS

Adkins and Radtke (2004) compare the perception of students to faculty members regarding the relevance of business ethics and accounting ethics education and find that students attach more importance to both business ethics and the goals of accounting ethics education than faculty members. Albrecht and Sack (2000) as well as various accounting professional bodies have emphasized the need for increased discussions of ethical issues in the class room. McNeel (1994) find evidence that ethics education can positively influence moral development especially during business practice.

Stevens et al. (1993) argue that more studies have investigated students’ perception of ethical issues (Cole and Smith, 1995) than faculty members’ perception. Adkins and Radtke (2004) argue that even for the few studies that have compared students’ perception on ethical issues with faculty members’ perception (Stevens et al., 1993; Cole and Smith, 1995), none performs the comparative analysis using matched data based on the same survey instrument.

Stevens et al. (1993) find evidence to suggest that students’ perception on ethical issues are significantly influenced by faculty members especially during student faculty interactions, because most students see faculty members as role models and mentors with more information and awareness on professional ethical standards and recent accounting scandals (Adkins and Radtke, 2004). If students’ perception on ethical issues are heavily influenced by faculty members, then it is safe to posit that if lecturers spend less time engaging students with discussions on ethical issues, students may assume that such issues are either irrelevant in real business practice, or may not be in a position to make the right ethical choices when confronted with real life issues within an organisation.

Various studies confirm that women are generally more ethical and take ethical issues more seriously (Arlow, 1991). Several studies also find that relatively older persons take ethical issues more seriously (Deshpande, 1997).

Research on ethical behaviour in management accounting is still evolving. Mihalek et al. (1987) find evidence to suggest that a significant number of management accountants have engaged in report manipulation due to organizational pressure and inadequate exposure to a code of ethics. Evans et al. (2001) find evidence to suggest that most management accountants, within organizations are dishonest and partially honest rather than totally honest in their reporting behaviour to their superiors. Studies have confirmed that management accountants engaging in budget slacking and/or padding (Hopwood 1972), knowingly attribute managerial failures and other corporate failures to the wrong reasons such as “unforeseen or uncontrollable events” and deliberately delay the submission of reports with the intention to shift stakeholder interest, and, consciously use technical jargons, sophisticated numbers etc, to confuse stakeholders. Various reasons account for this behavioural orientation and include monetary motivation as well as organizational contextual factors, environmental factors and personality traits. Irrespective of the reason, the concerning trend of not totally honest reporting behaviour among management accountants is worrying and may imply that the quality of managerial decision making around competitive strategy and resources allocation are inefficient with direct adverse effect on investor value.

Bampton and Cowton (2002a) study practices around ethics education in management accounting in a developed country (UK) and find a surprisingly low level of ethics education either explicitly or implicitly in management accounting modules. Despite the attempt by Business schools to incorporate ethics education, in some form at least, into the school curriculum, there are still challenges with the methods employed to teach ethics. Saul (1981) for instance argues that efforts at emphasizing relevance for ethics education in Business schools, is more an attempt to impress the external public and not a genuine desire to mainstream ethics education. Kahn (1990) argues that the lack of genuine efforts to mainstream ethics education re-enforces the gap between ‘practical ethics’ and academia. Kahn (1990) argues that whereas traditional academic studies on ethics serve a normative purpose, organizational ethics represents a more contextual study of ethics such that even though equally relevant, are more effective if approached differently. Mintz (1990) finds evidence to suggest that ethics is not appropriately integrated into management accounting courses and leading textbooks do not adequately cover ethics. Hajjawi (2008) finds similar results in Palestine universities.

Several studies have shown a positive relationship between ethics education and ethical behaviour at the work place (Jaffe and Tsimerman, 2005). Jaffe and Tsimerman (2005) argue that the ethical behaviour of future organisational leaders can be positively influenced by comprehensive ethics education of current students because current students made future business leaders.

RESEARCH METHODOLOGY

This study employs a survey method, using self-administered semi-structured questionnaires (with a mix of closed-ended and opened-ended questions) to explore the extent of coverage of ethical issues in management accounting education among universities in Ghana. The use of questionnaires in behavioural studies in financial and management accounting is well documented (Bampton and Cowton, 2002a, Adkins and Radtke, 2004). Concerns about social desirable response bias, that often affects most behavioural studies in accounting, will be mitigated because the questions asked are not personal (Randall and Gibson, 1990). To improve the internal validity of the questionnaire, it was piloted among some PhD students and amended based on suggestions provided.

The issues examined by the questionnaire are broadly grouped into four. The first section explores teaching practices on management accounting in Ghana. This is an attempt to replicate the studies by Bampton and Cowton (2002a) in Ghana. However this study deviates from Bampton and Cowton’s (2002a) in that it measures ethics education from the perspective of both the student and the faculty members, using matched data from the same survey questions. Issues examined include the extent to which management accounting ethics is included in degree courses, whether it is integrated into existing courses or taught separately, which issues are addressed, and challenges faced in management accounting ethics education.

The section after this attempts to measure students’ and faculty members’ perception about the relevance and essence of education in management accounting ethics and borrows from frameworks proposed by Callahan (1980), Loeb (1998), and Adkins and Radtke (2004).

The next section measures demographic data and investigates any significant relationship between demographics and identified trends from section one and section two of the questionnaire. To explain identify trends, this study will draw on theories on general business ethics. The section thereafter attempts to measure students’ and faculty members’ ability at ethical issue recognition and judgment using a scenario construct that investigates manipulation of reports; approving questionable expense sheets, ignoring company policy; granting questionable credit (Sweeney and Costello, 2009).

The questionnaires were addressed to university management accounting lecturers and students. No sampling strategy was applied in selecting faculty members as the population of management accounting lecturers is not large. Questionnaires were delivered by hand (by the researchers or a support assistant) to faculty members, and permission was sought from faculty members to distribute questionnaires to students. Generally, management accounting lecturers were supportive of the research and provided assistance in targeting students studying management accounting. This study was conscious of its ethical responsibility to survey participants and ensured voluntary participation, informed consent, no harm to participants, confidentiality and anonymity of participants as well as privacy to participants. As an example, an introductory page to the questionnaire explained that participation was voluntary, with a brief of the essence of the research, that participation was anonymous and did not request for names or any form of identification. All responses were directly collected from respondents and no student handed over his/her response to a faculty member. Most students had responded to questionnaires before hence could discount the myths that accompany its administration. The findings of this research are presented below.

DATA ANALYSIS AND FINDINGS

There are about 25 tertiary institutions offering a bachelor’s degree in accounting in Ghana. Questionnaires were administered to 20 of these institutions. Twenty faculty members in twenty institutions responded to the questionnaire (a response rate of 100%). In each of the twenty institutions ten questionnaires were administered to management accounting students. In all 200 students were sampled and the response rate was 70%.

80% of the faculty respondents were males whereas 57% of the student respondents were females. 70% of faculty respondents were lecturers, 25% were senior lectures and one (5%) was a teaching assistant. Majority of the student respondents (86%) were less than 22 years old, and 64% were third year undergraduate students. Most faculty respondents (65%) were between the ages of 35 to 50. Very few lecturers and students had practicing experience in management accounting: 70% of faculty members had no such experience compared to

99% for student respondents.

ETHICS COVERAGE IN MANAGEMENT ACCOUNTING

Management accounting is offered as a compulsory module towards the award of a bachelor’s degree in accounting across all the universities sampled. 65% of the universities (13 institutions) offered management accounting in the third year of study (i.e. Level 300); 10% (2 ) offered it as a compulsory course in the third and fourth year, and the remaining 25% offered it as a compulsory module in the final or fourth year (level 400). 50% of two-year postgraduate taught-courses offer management accounting as a compulsory module in the first year and the other 50% offer it as a compulsory module in the second year.

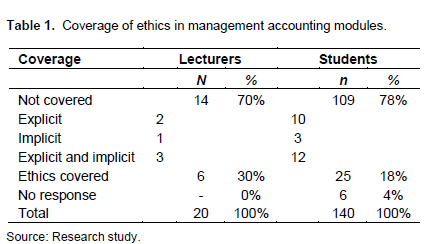

As to the inclusion of ethics, a significant portion of faculty members (70%) and students (78%) indicated that ethics education is not incorporated into management accounting modules. Non response bias will have resulted in a situation where only lecturers who actually incor-porate ethics into management accounting education will have responded. The evidence presented below therefore, does not suggest non response bias because (a) there was a relatively significant number of negative responses and (b) a comparison of early respondents and negative respondents did not reveal any significant differences (Table 1).

The introduction of ethics education in management accounting has been quite recent, mostly between the past two to five years. Only one institution had incorporated ethical issues in the management accounting module for more than five years. Only one faculty member indicated an increasing trend of coverage of ethical issues in management accounting studies (in terms of credit hours dedicated). The other five faculty members incorporating ethics education in management accounting studies mentioned that the trend of coverage had remained unchanged. All faculty members who included ethics education in management accounting studies were optimistic that ethics education in management accounting will increase significantly within the next five academic years because of (a) improvements in the availability of study materials that address ethical issues in, management accounting studies; (b) the growing interest by the accounting and management accounting profession in ethical issues and (c) the growing interest of students in ethical issues.

Various questions were included to measure the seriousness attached to ethics education by the institutions that incorporate ethics education into management accounting studies. These included an exploration of the credit hours dedicated to ethical issues in management accounting studies and the inclusion of ethical issues in module assessments and examinations. The institutions that incorporated ethics education in management accounting studies, dedicated very little time to ethics education (about 8%); citing ‘inadequate time’ (67%) and the existence of a general ethics course (50%) as the main reason(s).86% of students cited the growing disconnect between industry and academia as the main reason for the little or no focus on ethical issues in management accounting; other students(21%) suggested the lack of interest by lecturers., with a few of them (9%) citing the lack of adequate experience by faculty members to deal with ethical issues in management accounting.

Four out of the six faculty members (67%) who incorporated ethics education confirmed that the time allotted to studies of ethical issues in management accounting was inadequate. All students who indicated that ethics education was incorporated agreed with faculty members that the time allotted was very inadequate.

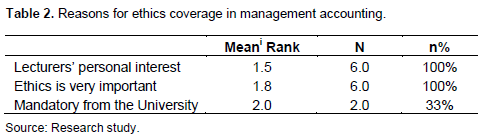

The inclusion of ethical issues in assessments and examinations in management accounting is not consistent. 40% of students indicated that ethical issues were never assessed and 20% of students indicated that it was sometimes assessed. 50% of faculty members sometimes included ethical issues in module assessment but not always and one (1) faculty member has not yet included ethical issues in module assessment but intends to do so in the future. Interestingly, 2 faculty members (33%) indicated that ethical issues are always assessed. Considering the fact that 10 students were sampled from each institution, it was expected that at least 20 students will confirm same. Only ten students from these institutions confirmed this assertion; perhaps suggesting a general challenge by students in identifying ethical issues. Faculty members who included ethics in management accounting teaching provided various reasons for the inclusion (Table 2).

Only two universities mandated the incorporation of ethical issues in management accounting studies. The inclusion of ethical issues in management accounting was mostly as a result of lecturer’s personal interest.

Faculty members who did not include ethics education in management accounting studies suggested that there was no need for a separate focus on ethical issues in management accounting studies (71%), there are no ethical issues peculiar to management accounting studies (64%), inadequate study support materials (64%) and ethics education is adequately covered in other accounting modules (57%).

29% of faculty members who currently do not include ethics education in management accounting will ‘with certainty’ consider including ethics education in future management accounting modules; with 43% undecided and 14% to consider integrating ethics education in management accounting studies depending on (1) the availability of study materials, (2) the revision of the course outlines to make time available and (3) the continuous non-existence of a general ethics course.

Students and faculty members differ significantly on the need for a separate focus on ethical issues peculiar to management accounting studies. A significant number of lecturers (50%) do not consider a separate focus on ethical issues in management accounting as very relevant because they do not perceive that there are ethical issues peculiar to management accounting studies. However 71% of students consider ethics education in management accounting studies as very relevant(very important or quite important), hence requiring a separate focus irrespective of whether there is a general course on ethics or not.

GOALS AND RELEVANCE OF ETHICS EDUCATION

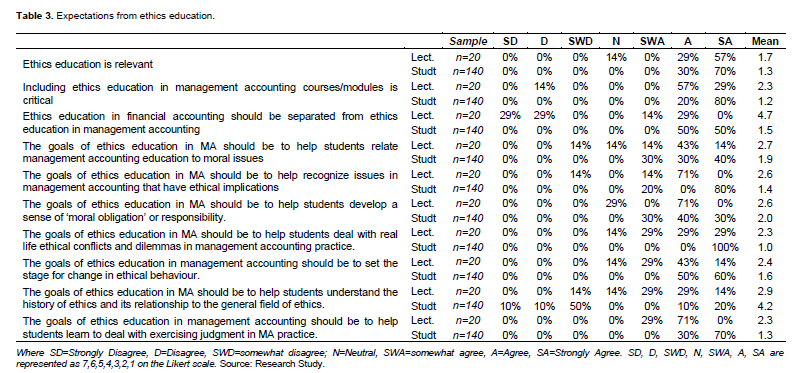

Even though all faculty members and students agreed that ethics can be taught to students, only 30% of lecturers were very convinced (‘absolutely’ and ‘to a great extent’) that ethics education at the tertiary level will help accounting students to solve moral and ethical dilemmas facing the accounting profession. However a significantly more percentage of students (93%) were convinced that ethics education was critical (‘absolutely’ and ‘to a great extent’) in helping students deal with ethical dilemmas at work.

As regards the need for a separate focus on ethical issues in management accounting, students and faculty members differed.50% of faculty members considered it as ‘moderately important’ or only important to ‘some extent’, however 71% of students considered it as ‘very important’ or ‘quite important’. 45% of faculty members prefer a combined ethics course for management and financial accounting and 61% of students prefer a compulsory ethics course integrated into management accounting studies.

Faculty and students also differed on the appropriate level at which ethical issues in management accounting should be discussed. Students generally prefer discussions on ethical issues to start earlier (at level 100) compared to faculty members (at level 300).

There are significant differences between lecturers and students in this study, on the expected outcome of ethics education in management accounting (as seen in Table 3).Whilst most lecturers agreed that ethics education should focus on the history of ethics in accounting vis-à-vis the general fields of ethics, most students disagreed and rather preferred ethics studies to focus on real life ethical conflicts and dilemmas in management accounting practice.

CAPACITY TO IDENTIFY ETHICAL ISSUES

The use of scenarios in ethics studies helps to focus on the most important factors in the decision making by respondents and measure multiple variables simultaneously in a standardized manner across respondents using a precise description of a social situation that makes the decision making situation more real.

Scenarios are widely used in business ethics studies (Randall and Gibson, 1990); Weber (1992) and to be effective as exploratory tools, they must avoid ambiguity (Randall and Gibson, 1990), must be interesting to the participants using precise language to describe real life situations that participants are familiar with and must reflect realistic ethical dilemmas (Weber, 1992) relating to the phenomenon being studied.

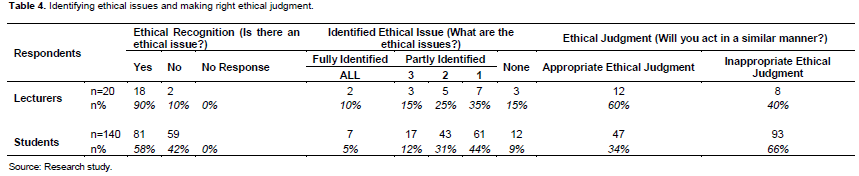

The scenario illustrated practical ethical dilemmas faced by management accountants at the work place and should be familiar to most third year and final year students in management accounting (Flory et al., 1992). The scenario exposed ethical issues about (1) approving a questionable expense report, (2) manipulating company books, (3) bypassing company policy and (4) extending questionable credit which have been identified as the most recurring ethical issues faced by management accountants at the work place. The scenario ended with action decisions taken by a hypothetical management accountant in response to ethical dilemmas. Faculty members and students were asked to identify the existence of ethical issues if any, and whether they agreed with the action decisions of the hypothetical management accountant.

The essence of the scenario was to measure the ability of faculty members and students in recognizing ethical issues and exercising ethical judgments and intentions. This is critical to understanding the capacity of faculty members in appropriately handling ethical discussions in management accounting studies as well as current student’s preparedness to deal with ethical dilemmas at the work place because the ability to recognize ethical issues is critical catalyst to making the right ethical decision.

10% of faculty members and 42% of students could not identify the existence of ethical issues in the scenario presented. Only 10% of faculty members and 5% of students correctly identified all the four ethical issues involved in the scenario. 75% of faculty members and 87% of students could only partially identify the ethical issues involved; with most of them identifying only one ethical issue. The most identified ethical issue was manipulation of company records, bye-passing company policy as well as approving questionable credit. 40% of faculty members and 66% of students suggested they will act in a similar manner as the hypothetical management accountant. Whereas faculty members mostly cited the potential financial benefits to the organisation as a justification for their ethical intentions, students cited the need to be a team player, else the potential fallout with colleagues and management (i.e. work place attrition and job security) who may lose their bonuses if they act otherwise.

DISCUSSION AND IMPLICATIONS

Overall, the focus of ethics education in management accounting studies is very limited; with very few lecturers incorporating ethics education in management accounting studies. Where ethics education was incorporated, it was driven mainly by the personal interest of the lecturer in the subject area (Table 3).

As to the mode of delivery, a combination of explicit and implicit modes of instruction was used but the overall quality and seriousness of the instruction was limited. Specifically, (a) the time allotted to ethics education as part of management accounting studies was significantly low and inadequate; (b) and module assessment did not regularly include ethics issues. Whereas faculty members explained the inadequacy of the time allotted for ethics in management accounting studies to time constraints, and the existence of a general course in ethics, students cited the growing disconnect between academia and practice, lack of faculty interest and lack of adequate experience as the main reason (Table 4).

Most lecturers did not include ethics education in management accounting studies because they did not see the relevance of a separate focus for ethical issues in management accounting studies for the reasons that (a) ethics education was covered in other areas of study and management; (b) there were no ethical issues peculiar to management accounting; and (c) there were inadequate support materials.

Students and faculty members agreed that ethics education is very relevant; that ethics can be taught to tertiary students; but the time allotted for its education is inadequate.

Higher education research has confirmed significant discrepancies between students and faculty members on a lot of issues including perceptions about the effective mode of instruction (Miron, 1988).Students generally prefer a separate focus of ethical issues in management accounting studies irrespective of whether a general course in it exists or not; but lecturers disagree on the relevance of this approach, instead preferring a combined ethics course for financial and management accounting. Even though faculty members agree that ethics can be taught, they are relatively less convinced, compared to students, of the effectiveness of ethics education in helping to solve the moral and ethical dilemmas in accounting practice.

Faculty and students disagree on the most appropriate level to begin such education in management accounting studies. Whereas faculty members prefer ethics education to begin at senior years of tertiary education, students prefer it to begin at relatively earlier levels.

Students and faculty also disagree on what the goals of ethics education in management accounting should be. Students disagree that the goals should be to help students appreciate and understand the history and composition of all aspects of accounting ethics and their relationship to the general field of ethics.

Even though a surprisingly high number of lecturers and students were unable to comprehensively identify ethical issues and make the right ethical judgment in the earlier scenario presented, the situation was more pronounced for students. A relatively higher proportion of students were unable to identify ethical issues and make the right ethical judgment. Considering the fact that faculty members are a critical link in enlightening students on ethical issues, this trend may be disturbing. More-so, a number of studies have suggested that senior level students are relatively more ethical than lower level students (Ludlum et al., 2013), and may qualify as subject-surrogates for ethics studies in the real work environment because no significant difference(s) exists (Ludlum et al., 2013). Holding that to be true, the relatively inability by a significant number of senior level accounting students to identify ethical issues and make the appropriate ethical judgment is worrying and may perhaps confirm the relevance of students’ desire for ethics studies to begin at earlier stages of study.

The results of this study suggest multiple implications for business schools. Given the importance of ethics in the field of accountancy and the growing evidence of the need to improve the mode of instruction of its education in accounting modules, it is impossible to have a holistic view of the effectiveness or otherwise of ethics education, without considering the views of both faculty and students. Examining the perspectives of faculty members as well as students on management accounting ethics education can provide useful insights to guide policy and organizational decisions. Secondly understanding the areas of difference in perceptions may be the starting point to mitigate any discrepancies and help improve accountancy education. Lastly, it is likely that similar discrepancies exist in other areas of study and instruction. Therefore this study provides the impetus for similar studies in other phenomenon.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Adkins N, Radtke RR (2004). Students' and faculty members' perceptions of the importance of business ethics and accounting ethics education: Is there an expectations gap? J. Bus. Ethics. 51(3):279-300. Crossref |

||||

|

Arlow P (1991). Personal characteristics in college students' evaluations of business ethics and corporate social responsibility, J. Bus. Ethics, 10(1):63-69. Crossref |

||||

|

Armstrong P (1985). Changing management control strategies: the role of competition between accountancy and other organisational professions, AOS 10(2):129-148. Crossref |

||||

| Bampton R Cowton CJ (2002a), The teaching of ethics in management accounting: Progress and prospects, Business Ethics: A Eur. Rev. 11(1):52-61. | ||||

|

Bampton R, Cowton CJ (2002b). Pioneering in ethics teaching: The case of management accounting in universities in the British Isles, Teach. Bus. Ethics. 6(3):279-295. Crossref |

||||

| Callahan D (1980), Goals in the teaching of ethics, In Ethics Teaching in Higher Education (pp. 61-80), Springer US. | ||||

|

Cole BC, Smith DL (1995), Effects of ethics instruction on the ethical perceptions of college business students, J. Educ. Bus. 70(6):351-356. Crossref |

||||

|

Deshpande SP (1997), Managers' perception of proper ethical conduct: The effect of sex, age, and level of education, J. Bus. Ethics 16(1):79-85. Crossref |

||||

| Duska RF, Duska B (2003), Accounting Ethics, Malden, Massachusetts: Blackwell Publishing. | ||||

|

Evans III JH, Hannan R, Krishnan R, Moser DV (2001), Honesty in managerial reporting, Account. Rev. 76(4):537-559. Crossref |

||||

| Fisher CM, Lovell A (2000), Accountants' responses to ethical issues at work. Oxford: Chartered Institute of Management Accountants. | ||||

| Flory SM, Phillips Jr TJ, Reidenbach RE, Robin DP (1992). A multidimensional analysis of selected ethical issues in accounting, Account. Rev. pp.284-302. | ||||

|

Gunz S, McCutcheon J (1998), Are academics committed to accounting ethics education? J. Bus. Ethics 17(11):1145-1154. Crossref |

||||

| Hajjawi O (2008), Pioneering in teaching business ethics: The case of management accounting in universities in Palestine, Eur. J. Econ. Finan. Admin. Sci. 14:149-157. | ||||

|

Hopper T, Tsamenyi M, Uddin S, &Wickramasinghe D (2009), Management accounting in less developed countries: what is known and needs knowing, Account. Audit. Accountability J. 22(3):469-514. Crossref |

||||

|

Hopwood AG (1972), An empirical study of the role of accounting data in performance evaluation, Empirical Research in Accounting: Selected Studies, Supplement J. Account. Res. 10:156-82. Crossref |

||||

|

Jaffe ED, Tsimerman A (2005), Business ethics in a transition economy: Will the next Russian generation be any better? J. Bus. Ethics 62(1):87-97. Crossref |

||||

| Kahn WA (1990), Toward an agenda for business ethics research, Acad. Manage. Rev. 15(2):311-328. | ||||

| Loeb S (1998), A separate course in accounting ethics: An example, Adv. Account. Educ. 1:235-250. | ||||

|

Ludlum MP, Moskaloinov S (2004), Right and wrong and cultural diversity: Replication of the 2002 Poll on Business Ethics, J. Educ. Bus. 79(5):294-298. Crossref |

||||

| McNeel SP (1994), College teaching and student moral development, Moral Development in the Professions: Psychol. Appli. Ethics 27:49. | ||||

| Mihalek PH, Rich AJ, Smith CS (1987), Ethics and management accountants, Manage. Account. 69:34-36. | ||||

| Mintz S (1990), Ethics in the management accounting curriculum, Manage. Account. 71(12):51-54. | ||||

|

Miron M (1988), Students' evaluation and instructors' self-evaluation of university instruction, Higher Educ. 17(2):175-181. Crossref |

||||

| Needles BE (1976), Implementing a framework for the international transfer of accounting technology, Int. J. Account. Educ. Res. 12(1). | ||||

|

Randall DM, Gibson AM (1990), Methodology in business ethics research: A review and critical assessment, J. Bus. Ethics 9(6):457-471. Crossref |

||||

|

Saul GK (1981), Business ethics: Where are we going? Acad. Manage. Rev. 6(2):269-276. Crossref |

||||

|

Shah AK (1996), Creative compliance in financial reporting, Account. Organ. Soc. 21(1):23-39. Crossref |

||||

|

Shaub MK (1995), An analysis of the association of traditional demographic variables with the moral reasoning of auditing students and auditors, J. Account. Educ. 12(1):1-26. Crossref |

||||

|

Stevens RE, Harris OJ, Williamson S (1993), A comparison of ethical evaluations of business school faculty and students: A pilot study, J. Bus. Ethics 12(8):611-619. Crossref |

||||

|

Sweeney B, Costello F (2009), Moral intensity and ethical decision-making: An empirical examination of undergraduate accounting and business students, Account. Educ. 18(1):75-97. Crossref |

||||

|

Tsamenyi M, Bennett M, Black J (2004), Perceived purposes of budgets in organizations in a developing country: field study from Ghana, J. Afr. Bus. Stud. 5(1):73-92. Crossref |

||||

|

Weber J (1992), Scenarios in business ethics research: Review, critical assessment, and recommendations, Bus. Ethics Q. 2:137-160. Crossref |

||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0