Full Length Research Paper

ABSTRACT

This work aimed at assessing the non- financial measures of performance of deposit money banks in Nigeria. The population of the study comprised the entire 21 banks listed on the Nigerian stock exchange as at December, 2013. The study employed expos - factor research design; data were collected from a sample of nine (9) deposits money banks. Content analysis method was employed, with the use of scoring and grading method. The study concluded that Nigerian deposit money banks (dmbs) disclose some part of non-financial measure of performance in their annual report, also the study found out deposit money banks disclosed voluntary information in their annual report. It was recommended that steps should be taken by the Federal Reporting Council Of Nigeria (FRCN), Securities Exchange Commission (SEC), Nigerian Stock Exchange (NSE) and other regulatory bodies to ensure full compliance with relevant international financial reporting standards/international accounting standards (IFRS/IAS) accounting disclosure requirements. And to make sure that Nigerian deposit money banks are disclosing financials and non-financial measures in their annual report for better decision making by their users. Lastly, given the importance of performance evaluation for managers, stockholders and investors, it is suggested that the Nigerian Stock Exchange (Nse) and the Central Bank Of Nigeria (CBN) should issue a policy guideline regarding the adoption of balance scorecard (BSC) as performance assessment technique for the nigerian deposit money banks.

Key words: Non-financial, voluntary disclosure, performance, deposit money banks.

INTRODUCTION

Good corporate reporting plays an important role in helping to restore the trust and confident of owners of companies in the companies’financial reports. Companies and organisations need to communicate more vividly, openly and effectively with the owners on how the operations of their companies are going. On their part, stakeholders are demanding greater transparency in reporting strategy, higher return on their investment and vibrant turnover and competitive advantage.To monitor and ensure the achievement of the above demands of the organizational stakeholders, a performance measurement system needs to be devised. Performance measurement systems play a vital role in developing strategy, evaluating the achievement of organizational goals and objectives (Kaplan and Norton, 2001).Inadequacies in financial performance measures have led to innovations in financial reporting ranging from disclosure of non-financial indicators of "intangible assets" and "intellectual capital" to "balanced scorecards" of integrated financial and non-financial measures. Most banks and financial institutions are struggling to go further beyond the application of financial measures by integrating the non-financial measures.

Therefore, non-financial measures arise as the result of limitations of financial performance measures and the rising prominence of intangible assets (Niven, 2006; Drury, 2004; Kaplan and Norton, 1996).

Organisations that are moving towards integrated reporting could develop a well competitive advantage which can secure capital and credit, help in the war for talent, and build strong business relationships. Stake-holders will gain a better understanding of the quality and sustainability of performance through insight into external influences, strategic priorities and the dynamics of the chosen business model (Armin and Werner, 2012).

When there is return, there shall be an investment which, in turn, brings about economic growth. On the other hand, poor banking performance has a negative repercussion on the economic growth and development. Poor performance can lead to runs, failures and crises. Banking crisis could entail financial crisis which in turn brings the economic meltdown as happened in USA in 2007 (Marshall, 2009). Several measures of performance exist, which include the use of ratios (ROI, ROCE), and CAMEL. All these measure are historical in nature and lack futuristic outlook (Kaplan and Norton 1996).

As such, the introduction of BSC approach to performance management will achieve a balance between, short and long run objectives. Although there have been several studies on the BSC as performance measure-ment of Deposit money Banks, most of the studies were carried out in different countries.

The objective of this study is to access how deposit money banks in Nigeria disclosed non- financial mea-sures of performance in their annual reports and account.

Corporate Reporting

Globalization brings about changing’s from one aspect to the other. For an organisation to be competitive it needs to adopt global changes. Performance measurement can be financial or non-financial. Traditional performance measurement systems, which rely on financial measures only, do not fit today's business environment (Umar and Olatunde, 2011). As such, to succeed in the business, both the performance measure should be used together (Kaplan and Norton, 1996). They believed that if companies were to improve the management of their intangible assets, they had to integrate the measurement of intangible assets into their management system.

As a result of failure of traditional performance measurement systems based on financial measures to integrate all those factors critical in contributing to the rapid development ofbusiness excellence,people started agitating for a multi-dimensional performance measures and as such the BSC was seen as the most suitable tool to integrate financial and non-financial performance measures in an integral management control system (Atkinson et al., 1997; Hoque and James, 2000; Simons, 2000; Malina and Selto, 2001; and Bisbe and Otley, 2004). Moreover, Kaplan and Norton (2001) emphasised on the need to use multi-dimensional performance measures in the service sector such as banking sector.

There are attempts to carry some of these studies in developingcountrieslikeNigeria.Inaresearch conducted by Umar and Olatunde (2011) on performance evaluation of consolidated banks using non-financial measures, multiple regressions were used. They found out that performance of banks increase as they adopt non-financial measures.

Esther (2013) in her contribution conducted a research on Strategic decision making, balanced scorecard profitability, issues and challenges. She found that inherent benefits of applying the balanced scorecard as against the nonspecific approach of appraising employee performance will enhance profitability.

Moyin and Michael (2014) conducted a study on Performance Measurement Systems in the Financial Service Industry: A Comparative Analysis of Nigeria and United Kingdom Banks, they found out that the PMS adopted in the Nigerian banking industry are more traditional in nature, while UK banks use innovative PMS. Also, the three most common PMS in the two banking industries are the balanced scorecard, Performance dashboards, and financial measures.

Brancato (1995) and Fisher (1995)indicate that many firms believe that financial measures are too historical and ‘‘backward-looking,’’ lack predictive ability to explain future performance, reward short-term or incorrect behavior, provide little information on root causes or solutions to problems, give inadequate consideration and difficult to quantify ‘‘intangible’’ assets such as intellectual capital.

As a result, many firms are supplementing financial metrics with a diverse set of non-financial performance measures that are believed to provide better information on strategic progress and success. Non-financial performance measures provide managers with timely information center on the causes and drivers of success and can be used to design integrated evaluation systems (Kaplan and Norton, 1996; Banker et al., 2000).

Such leading indicators are especially necessary for performance measurement and management compensation when current managerial actions influence the firm’s long-term financial return but are not reflected in the contemporaneous accounting measures. Examples refer todelaying costly maintenance activities at the expense of the future availability of the machinery and, therefore, a lower future financial return. The use of non-financial performance measures in compensation schemes is limited by the fact that it is often problematic to relate non-financial data to accounting performance (Hofmann, 2001).

METHODOLOGY

Research design is the blueprint for fulfilling research objectives and answering research questions. In other words, it is a master plan specifying the methods and procedures for collecting and analyzing the needed information. In addition, it must ensure that the information collected is appropriate for solving a problem under study. Content analyses of the annual report were used for the study. Each annual report will scrutinize and scored as a disclosure index based on the checklist design by the researcher. This can help theresearchertogatherinformation foransweringthe research questions.

The population of the study consists of all DMB’s quoted on Nigerian stock exchange as at December, 2013. A total of twenty-one (21) banks were listed in the Nigerian Stock Exchange.

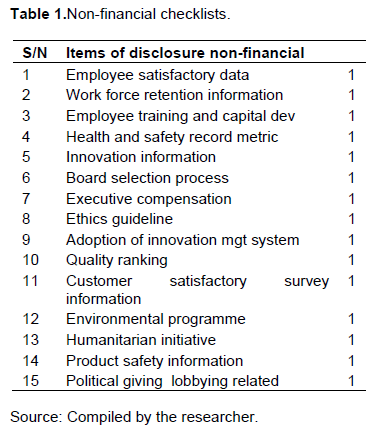

Based on that, the researcher picked 9 Banks which represent 40% of the population as sample of the DMBs in Nigeria. The selection of the sample will be based on data available. A filter was used to filter the population. Any DMBs that do not have full annual report of those years under study will be filtered out. Based on that, most of the banks published abridge financial statement; thosethat filled the criteria of full annual report from the population were selected as sample.The researcher adopted some index based on the variable under study. The researcher used 1-14 index for non-financial measures, these indexes will be used in the content analyses of annual report of DMBs. This is shown in Table 1. This was adopted from the work of Hoff and Wood (2008) and Umar and Olatunde (2011) with some modifications.

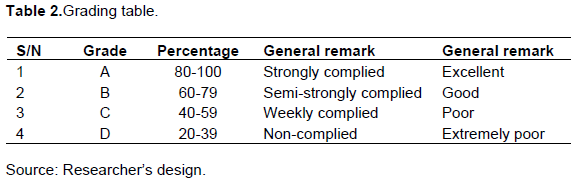

A range were prepared from 0 - 100%, impliedly any of the requirement shown in Table 2 disclosed by a Firm in its annual report and account fall between the range. After that, the DMBswillbe graded, where a company score 145 into 145, it will be graded an ‘A’ and has strongly applied the requirement. But, if a DMBs scores ‘0’ is graded as not having applied the requirement of the standard. The NUC university examination grading systems were used as seen in Kantudu (2006) and Barde (2009) with some modifications.

Data analysis and presentation

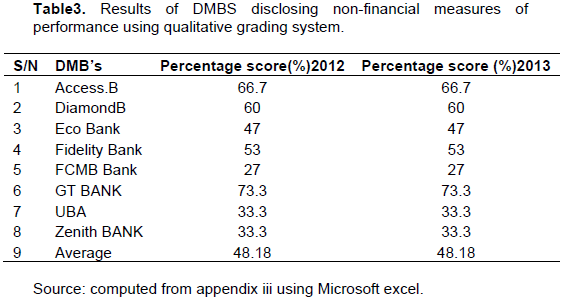

Data collected (Appendix I) show the various degrees to which individual DMBs in the industry comply with the disclosure checklist of non-financial for the 2-year period under observation. The result differ greatly form firm to firm with no firm guaranteeing 100% level of compliance. It is expected that firms that comply in full will have an annual score of 100% and be graded an ‘A’. A look at individual firms shows the following results (Table 3).

GT bank Nigeria plc. has a high score of 73.3% in year 2012 and still maintained it’s position in year 2013. Theses indicate that the level of compliance is more than average and the DMB can be score an ‘A’ which indicated a strongly disclose (Table 2).

Access bank followed by having a percentage of 66.7% in both the two years under study. These also can be graded as ‘B’ semi strongly disclosed.Followed by Diamond bank and Fidelity which fall under grade ‘B’ having 60% and 53% respectively and narrate as semi strongly disclosure.

After that, Eco bank score 47% followed by Skye with 40%, Zenith bank 33.3% and UBA with 33.3%, all of them graded as ‘C’ weakly disclosure. Lastly is FCMB with 27% disclosure, having a grade of ‘D’ and very weak disclosure.

The outcome of our assessment reveals a 55% application of this requirement which by our grading falls within the range of semi strong. The overall result shows the application of the non-financial measure of performance on the average to be 48.18%, which by our criteria falls within the weak range (Table 2). In a nutshell, we can accept our null hypothesis which says that, Nigerian DMBs do not use non-financial measure in measuring their performance. Notwithstanding, this is the overall average score, but if individual DMB are considered, some use non-financial measure in a strongly disclosed form as shown in Table 3.

METHODOLOGY

Research design is the blueprint for fulfilling research objectives and answering research questions. In other words, it is a master plan specifying the methods and procedures for collecting and analyzing the needed information. In addition, it must ensure that the information collected is appropriate for solving a problem under study. Content analyses of the annual report were used for the study. Each annual report will scrutinize and scored as a disclosure index based on the checklist design by the researcher. This can help theresearchertogatherinformation foransweringthe research questions.

The population of the study consists of all DMB’s quoted on Nigerian stock exchange as at December, 2013. A total of twenty-one (21) banks were listed in the Nigerian Stock Exchange.

Based on that, the researcher picked 9 Banks which represent 40% of the population as sample of the DMBs in Nigeria. The selection of the sample will be based on data available. A filter was used to filter the population. Any DMBs that do not have full annual report of those years under study will be filtered out. Based on that, most of the banks published abridge financial statement; thosethat filled the criteria of full annual report from the population were selected as sample.The researcher adopted some index based on the variable under study. The researcher used 1-14 index for non-financial measures, these indexes will be used in the content analyses of annual report of DMBs. This is shown in Table 1. This was adopted from the work of Hoff and Wood (2008) and Umar and Olatunde (2011) with some modifications.

A range were prepared from 0 - 100%, impliedly any of the requirement shown in Table 2 disclosed by a Firm in its annual report and account fall between the range. After that, the DMBswillbe graded, where a company score 145 into 145, it will be graded an ‘A’ and has strongly applied the requirement. But, if a DMBs scores ‘0’ is graded as not having applied the requirement of the standard. The NUC university examination grading systems were used as seen in Kantudu (2006) and Barde (2009) with some modifications.

Data analysis and presentation

Data collected (Appendix I) show the various degrees to which individual DMBs in the industry comply with the disclosure checklist of non-financial for the 2-year period under observation. The result differ greatly form firm to firm with no firm guaranteeing 100% level of compliance. It is expected that firms that comply in full will have an annual score of 100% and be graded an ‘A’. A look at individual firms shows the following results (Table 3).

GT bank Nigeria plc. has a high score of 73.3% in year 2012 and still maintained it’s position in year 2013. Theses indicate that the level of compliance is more than average and the DMB can be score an ‘A’ which indicated a strongly disclose (Table 2).

Access bank followed by having a percentage of 66.7% in both the two years under study. These also can be graded as ‘B’ semi strongly disclosed.Followed by Diamond bank and Fidelity which fall under grade ‘B’ having 60% and 53% respectively and narrate as semi strongly disclosure.

After that, Eco bank score 47% followed by Skye with 40%, Zenith bank 33.3% and UBA with 33.3%, all of them graded as ‘C’ weakly disclosure. Lastly is FCMB with 27% disclosure, having a grade of ‘D’ and very weak disclosure.

The outcome of our assessment reveals a 55% application of this requirement which by our grading falls within the range of semi strong. The overall result shows the application of the non-financial measure of performance on the average to be 48.18%, which by our criteria falls within the weak range (Table 2). In a nutshell, we can accept our null hypothesis which says that, Nigerian DMBs do not use non-financial measure in measuring their performance. Notwithstanding, this is the overall average score, but if individual DMB are considered, some use non-financial measure in a strongly disclosed form as shown in Table 3.

CONCLUSION AND RECOMMENDATIONS

This study assesses the performance reporting structure and performance of DMBs in Nigeria. The extent of disclosure compliance with voluntary and non-financial measure of performance is measured using a self-disclosure compliance index, scoring and grading.

Based on the findings of this study the following conclusions are drawn:

It has been established that DMBs use some of the non-financial measure in reporting their performance, their low usage can be as a result of Central Bank of Nigeria as the apex financial institution is empowered to supervise banking sector, which usually emphasizes financial performance rather than blending the two measures. It is recommended that Nigeria needs to adoptBalanced Scored Budget perspectives toachieve her aspiration to be among the top 20th economies of the world by the year 2020. Key indicator of performance and growth is the embediment of budget discipline at all the tiers of government, thus money spent must be justified and satisfied by all the established budgetary and budget monitoring organs. Balanced Scorecard of Budget preposition not only aligns strategy and objectives but also stipulates performance measures necessary to evaluate strategic visions or mission statements.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

| Atkinson AA, Balakrishan R, Booth P, Cote JM, Groot T, Malmi T, Roberts H, Uliana E (1997): New Directions in Management Accounting Research. J. Manage. Account. Res. Vol. 9. | ||||

|

Banker RD, Potter G, Srinivasan D (2000). An empirical investigation of an incentive plan that includes nonfinancial performance measures. The Accounting Review. http://dx.doi.org/10.2308/accr.2000.75.1.65 |

||||

| Barde IM (2009). An Evaluation Of Accounting Information Disclosure In The Nigerian Oil Marketing Industry. Ph. D. Dissertation, Bayero University, Kano, Department of Accounting. | ||||

|

Bisbe J, Otley D (2004). The Effects of the Interactive Use of Management Control Systems on Product Innovation. Account. Organ. Soc. 29(8):709-737. DOI: 10.1016/j.aos.2003.10.010 http://dx.doi.org/10.1016/j.aos.2003.10.010 |

||||

| Brancato CK (1995). New Corporate Performance Measures, New York: Conference Board. | ||||

| Drury C (2004). Management and Cost Accounting (6th Ed.). London, Book Power. | ||||

| Esther A (2013). Strategic decision making, balanced Scorecard Profitability: Issues and Challenges. Int. J. Accounting Res. Vol. 1. | ||||

| Fisher J (1995). Use of nonfinancial performance measures. In: S. M. Young (Ed.), Readings in management accounting. Englewood Cliffs, NJ: Prentice Hall. | ||||

| Hoffman ML (2001). A comprehensive theory of prosocial moral development. Stipek D, Bohart A (EDs.), Constructive and destructive behavior. | ||||

|

Hoque Z, James W (2000). "Linking Balanced Scorecard Measures to Size and Market Factors: Impact on Organizational Performance. Journal of Management Accounting. http://dx.doi.org/10.2308/jmar.2000.12.1.1 |

||||

|

Kaplan RS, Norton DP (2001). Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part 1. Accounting Horizons. http://dx.doi.org/10.2308/acch.2001.15.2.147 http://dx.doi.org/10.2308/acch.2001.15.1.87 |

||||

| Kaplan RS, Norton DP (1996). Using the Balanced Scorecard as a Strategic Management System. Harvard Bus. Rev. Vol. 74. | ||||

|

Kohli AK, Jawaorski A (1996). Market orientation: Review, Refinement and road map: J. Market. Focused Manage. 1(2):119-135. http://dx.doi.org/10.1007/BF00128686 |

||||

| Malin MA, Selto FH (2001). Communicating and Controlling Strategy: An Empirical Study of the Effectiveness of the Balanced Scorecard, J. Manage. Account. Res. 13:47-91.http://dx.doi.org/10.2308/jmar | ||||

| Marshall J (2009). The financial crisis in the US: key events, causes and responses, Research Paper, http://www.parliament.uk | ||||

| Niven P (2006). Driving Focus and Alignment with the Balanced Scorecard. J. Qual. Participation 28(4):21-25. Academic Search Premier Database. | ||||

| Norton D (2001), Beware: The Unbalanced Scorecard. Balanced Scorecard Report, The Institute of Management Accountants, Montvale, NJ, March. | ||||

| Simons R (2000). Performance Measurement & Control Systems for Implementing Strategy: Text & Cases. Englewood Cliffs, New York, Prentice-Hall, Inc. | ||||

| Umar G, Olatund, OJ (2011) 'Performance Evaluation of Consolidated Banks in Nigeria by Using Non-Financial Measures' Interdisciplinary Journal of Research in Business, Vol.1. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0