Full Length Research Paper

ABSTRACT

The aim of the article is to identify canonical correlations among performance indicators calculated from a base of accounting statements prepared in accordance with United States Generally Accepted Accounting Principles (US GAAP), Brazilian accounting standards (BR GAAP) and International Financial Reporting Standards (IFRS). Descriptive research with a quantitative approach was carried out. A research sample of 50 companies was selected, including 17 Brazilian companies listed on the Bovespa’s Board of Corporate Governance and 33 English companies listed on the London Stock Exchange, all of which trade American Depositary Receipts on the New York Stock Exchange. The results demonstrate divergence between companies and indicators in relation to differences calculated in performance indicators as well as statistically significant canonical correlations in both groups researched. The performance indicators of Brazilian and English companies were not affected in any significant way, despite divergences between BR GAAP and US GAAP and between IFRS and US GAAP. However, stands out as the main limitation that no company listed on Bovespa was found in the lists of European stock exchanges, which was necessary in order to verify the differences in these companies’ indicators in the conversion of their accounting statements from BR GAAP to US GAAP and IFRS. This required the adoption of an alternative (i.e., canonical correlations). The main implication of this study is that the impact of IFRS adoption by Brazilian companies may be less than the expected, in terms of improvement of accounting quality and cost of adoption. The article advances research on a comparative study of the financial disclosures made according to Brazilian, American and international accounting standards, supported by an analysis of performance indicators calculated from accounting statements prepared from and based on these standards.

Key words: Performance indicators, accounting statements, BR GAAP, US GAAP, IFRS, canonical correlations.

INTRODUCTION

The separation between capital and management has brought asymmetric information problems, which in this study are analysed from an external investor perspective. The differences between what is shown to foreign and domestic investors can be configured as an asymmetric information problem within the scope of Agency Theory.

The publication of audited accounting statements is one example of how accounting information functions as a reducer of information asymmetry. Therefore, accounting plays an important role in the reduction of information asymmetry in the context of Agency Theory. However, it also confronts information asymmetry problems in its financial disclosures from the perspective of the accounting standards of other countries.

Disclosure and the harmonisation of accounting standards have been the objects of several studies over the past few years. Various international bodies have issued accounting standards, such as the Financial Accounting Standards Board (FASB), the Federation des Experts Comptables Europeens and the Confederation of Asian and Pacific Accountants. However, the one that stands out in terms of harmonization is the International Accounting Standards Board (IASB), which has been aligning accounting standards with the objective of eliminating information asymmetry in accounting.

The intention of this article is to advance research in this direction by means of a comparative study of the financial disclosures made according to Brazilian, American and international accounting standards. To this end, we analyse performance indicators calculated from accounting statements prepared from and based on these standards. The study seeks to identify the differences between the performance indicators of Brazilian companies, calculated based on the accounting statements provided to the São Paulo Stock Exchange (BOVESPA) and New York Stock Exchange (NYSE), and those of English companies calculated based on accounting statements sent to the London Stock Exchange (LSE) and to the NYSE.

Therefore, this study refers to firms of two countries (Brazil and England) based on three accounting statements (BR GAAP, US GAAP and IFRS). The choice of these two countries is a result of their contextual differences in terms of legal systems, importance of capital markets, investor protection mechanisms and quality of accounting education in addition to the characteristics of the accounting regulations in each country. These factors may contribute to a comparison of the differences between the information highlighted by companies based on local accounting standards and International Financial Reporting Standards (IFRS) in relation to performance indicators.

Brazil can be characterised by a legal system based on code law, with developing capital markets and rule-based accounting standards, while England has a legal system predicated on common law, strong capital markets and principles-based accounting standards. Thus, one can identify which of these two contexts presents greater information asymmetry between what companies evidenced to local stakeholders (local GAAPs) and to external stakeholders (IFRS).

Moreover, no studies have applied canonical correlation analysis to examine the differences in accounting information using performance indicators calculated on financial statements prepared based on different sets of accounting standards, in this case, BR GAAP, US GAAP and IFRS. This analysis can help determine the gain in accounting information quality through the adoption of IASB standards.

The use of canonical correlation analysis in this case is indicated by providing a broader perspective of the effects of different sets of accounting standards in relation to companies’ performance indicators, which would not occur if the analysis were carried out by pairs, indicator by indicator.

Significant canonical correlations between the differences in the performance indicators of Brazilian and English companies would mean that the international accounting convergence process does not offer significant improvements to accounting information quality in relation to the disclosure of Brazilian companies. In this case, efforts towards convergence might be useless.

Put another way, the absence of canonical correlations between these differences could represent an opportunity to improve accounting information quality in Brazilian companies through the adoption of IASB standards.

Based on this, the following research question was designed: Are there statistically significant canonical correlations between performance indicators calculated from a base in accounting statements prepared according to BR GAAP and US GAAP and to IFRS and US GAAP? Therefore, the objective of the article is to identify canonical correlations between performance indicators calculated from a base in accounting statements prepared according to Brazilian and American accounting standards and to International and American accounting standards.

The article is structured as seven topics, starting with the introduction to the study. This is followed by a theoretical inquiry into the efforts made towards the harmonisation of accounting standards, the principal divergences in accounting standards on an international scale and performance indicators calculated from a base in accounting statements. Evidence of the method and procedures used in the research is then given. This is followed by a presentation of the results of the research, highlighting canonical correlations between the investigated performance indicators calculated from the three accounting standards. Finally, the conclusions of the research are presented.

Harmonisation of accounting standards and accounting quality

Several studies have examined the convergence of international accounting standards and the impact on accounting information quality. There are many approaches being used for that, such as earnings management, timely loss recognition and value relevance.

Since the 1980s, several international studies have sought to identify the quantitative impact of international accounting differences in different countries as well as interpret their causes using economic and cultural approaches (Gray, 1980, 1988; Weetman and Gray, 1990, 1991). Gray (1980) showed the tendency for companies in France and West Germany to be relatively conservative in earnings measurement compared with UK companies. Weetmann and Gray (1990) also found more conservative bias in earnings measurement under US GAAP compared with UK principles.

The adoption of IFRS by European Union countries since 2005 has increased international accounting convergence studies. Bartov et al. (2005) compared international and US standards and concluded that IFRS is a high quality set of accounting standards that is equivalent to US GAAP in terms of value relevance. Barth et al. (2008) examined whether the application of International Accounting Standards (IAS) was associated with higher accounting quality. They found that applying IAS generally leads to higher quality of accounting amounts. Daske et al. (2008) analyzed the effects of market liquidity, cost of capital, and Tobin´s q in 26 countries using a sample of firms that were mandated to adopt IFRS. Their results show increases in market liquidity, decrease in firm´s cost of capital, and increase in equity valuations.

On the other hand, Holthausen (2009) pointed out several factors that impact the financial reporting outcomes beyond the adoption of IFRS, as incentives, enforcement, ownership structure, and market and legal forces. Dechow et al. (2010) discussed the causes of various measures of earnings qualities have been used by researchers lately. They pointed out that the quality of earnings is a function of the firm´s fundamental performance, what is one area for future work.

More recently, Barth et al. (2012) examined whether application of IFRS by non-US firms results in accounting amounts comparable to those resulting from application of US GAAP by US firms. They concluded although application of IFRS has improved financial reporting comparability with US firms, significant differences remain.

Previous research tends to indicate that the adoption of IFRS has improved the quality of accounting information. The differences observed among accounting systems and the impact of IFRS adoption may be related to institutional factors such as the legal system (Ball et al., 2000), capital market development (Ding et al., 2007; Jeanjean and Stolowy, 2008), the country's economic development (Kang and Pang, 2005) and differences between local accounting standards and IFRS (Barth et al., 2008).

Leuz (2003) examined companies trading in Germany’s New Market in 1999 and 2000. He found no differences in information asymmetry between companies using IAS and those using US GAAP. Bartov et al. (2005) also found no significant difference in the value relevance of US GAAP and IFRS.

Ball et al. (2000) found differences in the timeliness of the reporting of losses and conservatism based on whether companies are from a common law or code law country. Considering Brazil to be a code law country and England and the US as common law countries, we expect there to be no correlation between differences in performance indicators, when comparing BR GAAP with US GAAP and IFRS with US GAAP, which may mean higher or lower information asymmetry in the financial statements of Brazilian companies.

Lang et al. (2006) compared reconciled earnings for non-US companies with the earnings of US companies from 1991 to 2002. They found that companies from countries with weaker investor protection have less informative and more managed earnings, which can mean a lower quality of accounting information. Ali and Hwang (2000), Ball et al. (2000) and Hung (2001) all showed that in countries such as that, accounting quality and transparency are lower.

Nobes (1998) and Radebaugh et al. (2006) pointed out that differences in accounting systems exist because accounting needs differ among nations. Therefore, it would be expected that there is no correlation between differences in the performance indicators of Brazilian and English companies.

Bae et al. (2008) identified 21 key items to measure the compliance of local accounting standards to IASB standards, analysing the differences in 49 countries. They found that the UK has greater compliance between local accounting standards and IASB standards (of the 21 items analysed, only one was divergent). By contrast, Brazil had 12 differences from IASB standards. These results reinforced the expectation of no correlation between differences in the performance indicators of Brazilian and British companies when comparing BR GAAP with US GAAP and IFRS with US GAAP.

Thus, the following research hypotheses were formulated and tested by means of statistical analysis:

H1: There is statistically significant canonical correlation between the performance indicators of Brazilian companies, calculated based on BR GAAP and US GAAP.

H2: There is a statistically significant canonical correlation between the performance indicators of English companies, calculated based on IFRS and US GAAP.

There being no evidence to reject H1 and H2, it could be concluded that the differences between Brazilian and American accounting standards are similar to the differences between American and international accounting standards. It can then be inferred whether. Brazilian accounting standards are more or less adequate compared with American standards and international accounting standards.

Principal divergences in accounting standards on an international scale

Most studies of differences in international accounting standards point in the same direction, attributing such differences to the legal characteristics and systems of each country. Commenting on the probable motivations for different accounting practices in member countries of the European Community, Castro (1998) listed the following motives: cultural influence, level of governmental control, structure of property and amassing of capital and peculiarity in accounting principles.

According to Weffort (2005), the causes of different accounting practices can be classified as the characteristics and necessities of the users and preparers of information, the way that the society is organised, cultural aspects and external factors. This can be accompanied by asymmetric information. Depending on their locations, users can have different impressions of the same company. Table 1 shows the principal differences between the recommendations of the IASB, the FASB and the Brazilian Accounting Standards for the recognition and measurement of differences in the valuation of company resources.

The divergences presented in Table 1 can influence the value constants of accounting statements. The same company can present different compositions of assets and liabilities and divergent results when analysing its accounting statements sent to different markets or countries. These differences end up altering the values of performance indicators, which are calculated from these statements.

In conclusion, a company can present very different indicators of liquidity, indebtedness or profitability depending on the statements analysed. However, the calculation of performance indicators is part of the analysis of accounting statements, which seeks to extract this information from reports on the economic and financial situations of organisations.

RESEARCH METHOD AND PROCEDURES

The research carried out here is characterised as descriptive research. In this sense, this research sought to analyse the performance indicators of Brazilian and English companies for verifying the existence of canonical correlations between them.

In relation to its approach to the problem, research can be characterised as quantitative. This comparability of information is what allows for the quantitative analysis of data. Therefore, in order to apply it, the existence of a set of more or less comparable elements is indispensable.

The research population is composed of 81 Brazilian companies listed at Levels 1 and 2 in the New Market of Corporate Governance of Bovespa (www.bovespa.com.br) in January 2007 and 1,306 English companies (not necessarily made up of English capital but listed on the LSE) (www.londonstockexchange.com) in January 2007.

Initially, the intention was to compare Brazilian companies listed on Bovespa with those on a European stock exchange. However, no company listed on Bovespa was found on the lists of European stock exchanges. The intention was also to verify the differences in the indicators of these companies in the conversion of their statements from BR GAAP to US GAAP and IFRS. Since only companies that negotiate their shares on European stock exchanges were identified, which do not need to convert their statements into IFRS, this approach was compromised and the study took advantage of this second alternative.

In Brazil, companies listed at the Levels of Corporate Governance of Bovespa were selected, because they were considered to possess greater commitment to information transparency, thus transmitting greater reliability. In the case of English companies, we opted to use companies listed on the LSE as it has the greatest number of companies listed that need to publish accounting statements elaborated from a base in IFRS.

The sample selected for the research was of the intentional type in which, according to Richardson (1999), the elements of the sample are intentionally related according to the characteristics prescribed in the plan and hypotheses of the research. The criterion used was that sample companies negotiate American Depositary Receipts (ADRs) on the NYSE. Based on this, 17 Brazilian companies listed at the Bovespa Governance levels were selected along with 33 English companies listed on the LSE, making a total sample of 50 companies.

Data were collected by means of accounting reports sent to Bovespa, to the LSE and to the NYSE by the companies in the sample. Based on these reports, various economic and financial indicators related to the theoretical foundation of the work were calculated (Table 2).

Performance indicators were calculated based on the accounting statements of the Brazilian companies for 2005, sent to Bovespa and to the NYSE. Percentage differences were then taken between the indicators of the accounting statements sent to Bovespa and those sent to the NYSE. An identical procedure was then applied to the English companies, based on accounting statements sent to the LSE and NYSE. These performance indicators were chosen because they are the most important accounting indicators according Brazilian literature (used by analysts and investors from Brazil (Iudícibus, 1998; Assaf, 2002).

Moreover, the existence of canonical correlations between the performance indicators of both groups was analysed (Bovespa and NYSE; LSE and NYSE). Canonical regression was developed by Bartlett (1938) as an extension of the canonical correlation analysis of Hotteling (1935, 1936). Whereas canonical correlation analysis focuses on “correlation between linear combinations of two sets of variables, canonical regression deals with the estimation of a regression equation that corresponds to the largest, or first, canonical correlation” (Estrella, 2007, p. 724). This correlation measures the degree of association that exists between two sets of variables (here, the secondary indicators of BR GAAP and US GAAP, IFRS and US GAAP). Thus, the regression is a generalisation of a multiple linear regression, or this is a particular case of the primary.

In the matrices  and

and  we have the table of the 17 Brazilian companies and their seven respective accounting indicators. The matrices

we have the table of the 17 Brazilian companies and their seven respective accounting indicators. The matrices  and

and  contain the table of the 33 English companies and their seven accounting indicators.

contain the table of the 33 English companies and their seven accounting indicators.

Concerning statistical inference, there is a test to verify whether the matrices X, Y, W and Z are correlated among themselves. However, this test is only applied when the vectors are normal multivariates. When multivariate normality is valid, it is also possible to construct statistical tests to evaluate the significance of canonical variables. As the software used in the article was the 5.1 version of Statgraphics, these tests were already conducted by default. Correlation and determination were effected through the use of the following formulas:

where SQ(model) denotes the sum of the squares referent to the model of regression adjusted to the data and SQTotal is the sum of the squares in their totality.One limitation of this research is that no company listed on Bovespa was found in the lists of European stock exchanges, which was necessary in order to verify the differences in these companies’ indicators in the conversion of their accounting statements from BR GAAP to US GAAP and IFRS.

Another limitation results from the performance indicators chosen, since the results cannot be the same if the indicators differ from those selected. However, this is something that a future study with other research strategies can address.

Description and analysis of data

There were percentage differences in the performance indicators of Brazilian companies calculated based on the statements sent to Bovespa and the NYSE. Similarly, there were also percentage differences in the performance indicators of English companies based on the statements sent to the LSE and to the NYSE. Moreover, the existence of canonical correlations between performance indicators was assessed for both groups (Bovespa and NYSE, LSE and NYSE).

Percentage differences in performance indicators according to Brazilian standards

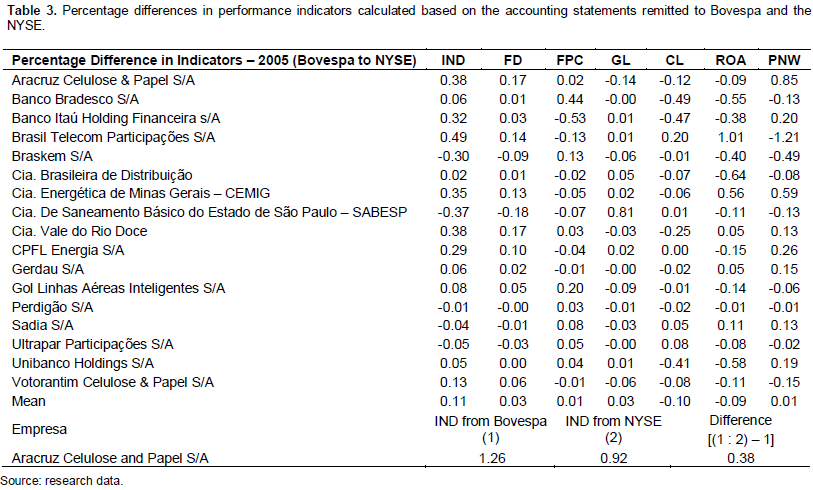

Performance indicators were calculated based on the 2005 accounting statements of Brazilian companies remitted to Bovespa and to the NYSE. Later, percentage differences between the accounting statement indicators remitted to Bovespa and those sent to the NYSE were recorded. These differences are presented in Table 3, which were calculated this way.

Table 3 demonstrates that the percentage variations in the performance indicators are heterogeneous; there are positive and negative variations. Furthermore, some companies have significant differences in particular indicators and irrelevant ones in other indicators. For example, Aracruz Celulose S/A has a positive variation in PNW of 85%. In other words, this indicator, calculated according to the accounting statements remitted to the NYSE, is 85% higher than the indicator calculated based on the statements sent to Bovespa. On the other hand, Brasil Telecom Participações S/A presented a negative variation of 121% in this same indicator. Perdigão and Ultrapar had minimum variations of approximately 1 and 2%, respectively.

Percentage differences in performance indicators according to IFRS

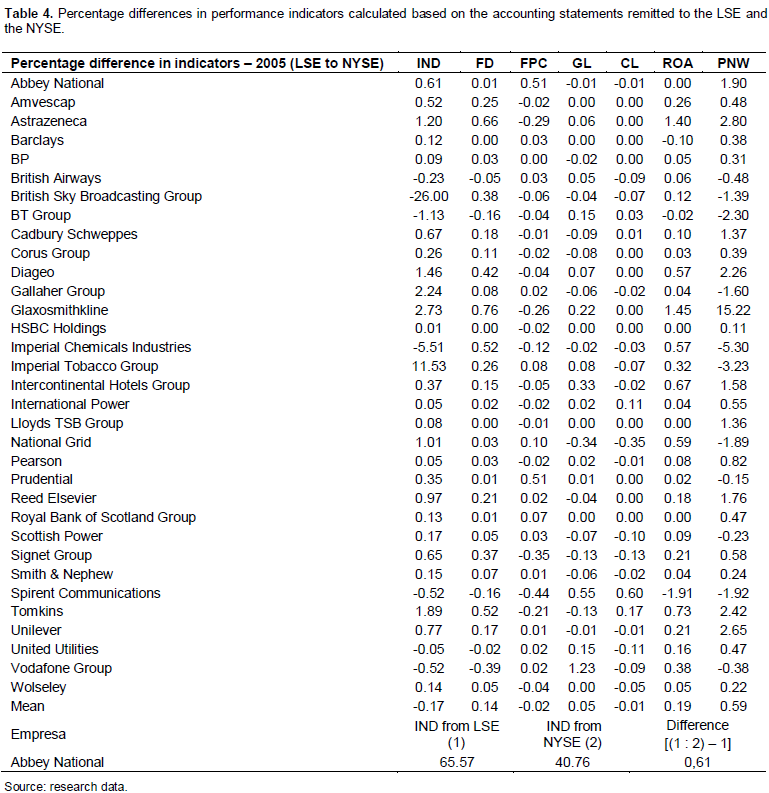

The performance indicators for English companies were calculated based on their 2005 accounting statements sent to the LSE and the NYSE. Later, percentage differences between the accounting statements indicators sent to the LSE and remitted to the NYSE and those sent to the NYSE were recorded. These differences are presented in Table 4, which were calculated this way.

The percentage differences in performance indicators calculated based on IFRS in relation those based on US GAAP seem to be significant or not depending on the indicator and company analysed. For example, for the PNW indicator, we observe positive differences of 1,522% for Glaxosmithkline and 280% for Astrazeneca. On the other hand, we can also see negative differences of 530% for Imperial Chemicals and 323% for Imperial Tobacco. This heterogeneity of differences can also be seen in the other indicators. Depending on the company and indicator analysed, there may or may not be significant distortions.

Analysis of canonical correlations between the calculated performance indicators

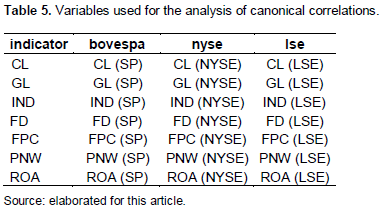

In order to carry out a global analysis of the impact of the divergences in accounting standards on a company’s performance indicators, we analysed canonical correlations. The indicators calculated based on accounting statements prepared according to the standards of countries whose stock exchanges were used in the study were used as variables, as seen in Table 5.

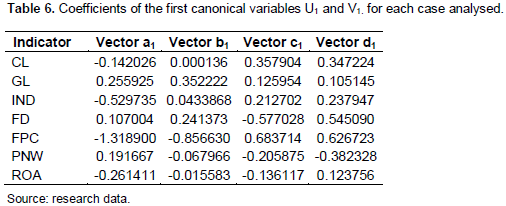

Using the statistical software Statgraphics (version 5.1), the coefficients of the first canonical variables U1 and V1 were determined for each case analysed, as demon-strated in Table 6.

Table 6 presents four vectors: a1, b1, c1 and d1, with i = 1, 2, ..., 7 (“i” is an indicator of its sub-index). The vectors a1 and b1 (with i = 1, 2, ..., 7) establish the relationship between Bovespa (called SP) and the NYSE. The values listed in the a1 and b1 vector columns are the coefficients of each variable (CL, GL, IND, FD, FPC, PNW, ROA). The c1 and d1 vectors (where i = 1, 2, ..., 7) establish the relation between the NYSE and the LSE. The values listed in the c1 and d1 vector columns are the coefficients of each variable (CL, GL, IND, FD, FPC, PNW, ROA).

The canonical regression is also known as “first correlation” because it organises crossed regressions between the analysed variables (Timm, 2002). Therefore, it is possible to establish seven regression equations between each of the indicators analysed. However, there is no reason for analysing them all because only the first regression is important, since it has the highest correlation coefficient.

If the equation was calculated with the values of CL, GL, IND, FD, FPC, PNW and ROA for a company listed in Bovespa, the values were multiplied by each of their related coefficients, added (or subtracted, if they were negative), and then the same carried out for the NYSE, the result between U1 and V1 would be similar. Thus, this creates a relation that sets a cloud of data to another cloud of data. Thus, the first canonical variables were described between the values of Bovespa and the NYSE:

U1(SP) = -0.1420265 CL(SP) + 0.255925 GL(SP) + …-0.261411 ROA(SP)

and

V1(NYSE) = 0.000136 CL(NYSE) + 0.352222 GL(NYSE) +... – 0.0155833 ROA(NYSE)

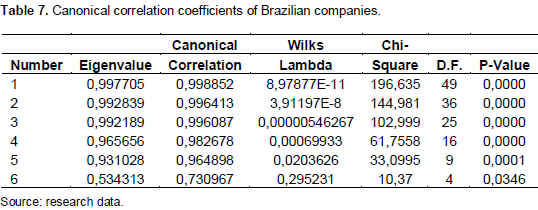

The coefficient of canonical correlation between these two groups of data is 99.88% (Table 7). Therefore, the performance indicators calculated based on accounting statements elaborated in BR GAAP are strongly related to those calculated from accounting statements elaborated in US GAAP.

Using an identical procedure, and taking the data between the NYSE and the LSE, we arrive at the following:

U1 = 0.0357904 CL(NYSE) + 0.125954 GL(NYSE) + ... – 0.136117 ROA(NYSE)

and

V1 = 0.347224 CL(LSE) + 0.105145 GL(LSE) + ... + 0.123756 ROA(LSE)

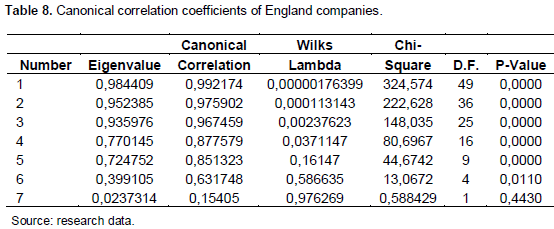

In this case, the coefficient of canonical correlation (also high) reached 99.22% (Table 8), which shows that a strong relationship exists between the indicators calculated from accounting statements prepared in IFRS and US GAAP.

CONCLUSIONS

The objective of the article was to identify canonical correlations between performance indicators calculated based on three accounting systems (Brazilian, American and international). In terms of the global analysis of the impact of the divergences in accounting standards on companies’ performance indicators, we found correlation coefficients of 99.88 and 99.22%, respectively, in the two related groups (BR GAAP and US GAAP, and IFRS and US GAAP). This indicates a strong relationship between the performance indicators calculated from accounting statements elaborated in BR GAAP and those calculated from accounting statements elaborated in US GAAP. It also shows a strong relationship between the indicators calculated from accounting statements prepared in IFRS and US GAAP.

The influence on performance indicators due to divergences between international and American accounting standards was greater than that observed between Brazilian and American accounting standards. These minor differences can be explained by turning to the historical origins of the sample countries. In Brazil, there has been a strong influence from Anglo-American audit firms, which came to the country bringing a strong tradition of audit procedures and manuals and the habit of training companies on accounting standards and procedures. These aspects have given the accounting procedures adopted in Brazil certain similarities to those established in US GAAP.

Concerning the research hypotheses formulated, the hypothesis H1and H2 are accepted based on the presented statistical analysis. H1 presupposed statistically significant canonical correlations between performance indicators based on BR GAAP and US GAAP of Brazilian companies. H2 did the same between performance indicators based on IFRS and US GAAP of English companies.

It can be concluded that, in a general way, the performance indicators of Brazilian and English companies are not affected in a significant way, despite divergences between Brazilian and American accounting standards and between international and American accounting standards. Therefore, the main implication of this study is that the impact of IFRS adoption by Brazilian companies may be less than the expected, in terms of improvement of accounting quality and cost of adoption. By comparing the canonical correlations of the sampled Brazilian and English companies, it can be stated that the relationship of the indicators calculated from accounting statements converted from BR GAAP to US GAAP is greater than those converted from IFRS to US GAAP. Therefore, based on the sample researched and performance indicators considered, greater divergences are noted between international standards and American standards than between Brazilian accounting standards and American standards.

However, the results of this research cannot be generalised, as they only relate to the sample of Bovespa and LSE companies surveyed and the considered indicators. The canonical correlations presented could have been affected by the length of samples, which when extended may increase or decrease the effects of the differences between accounting standards. The performance indicators selected may also have influenced the research findings, since relating the financial statements of groups of accounts depends on the consequences of applying different accounting standards. It is thus still necessary to consider that each company may present larger or smaller values in accounting amounts that are more or less affected by differences in accounting standards. Moreover, the value relevance and importance of any performance measures can differ from Brazil to England due to various factors, including the differences in the underlying accounting methods. Another limitation of our study is related to the year 2005 that may not be ideal, since this is the first year of mandatory adoption of IFRS in EU.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Ali A, Hwang L (2000). Country-specific factors related to financial reporting and the value relevance of accounting data. J. Account. Res. 38(1):1-21. |

|

|

|

|

|

Assaf NA (2002). Estrutura e análise de balanços: um enfoque econômico-financeiro (7a. ed.). São Paulo: Atlas. |

|

|

|

|

|

Bae K-H, Tan H, Welker M (2008). International GAAP differences: the impact of foreign analysts. Account. Rev. 83(3):593-628. |

|

|

|

|

|

Ball R, Kothari S, Robin A (2000). The effect of international institutional factors on properties of accounting earnings. J. Account. Econ. 29(1):1-51. |

|

|

|

|

|

Barth ME, Landsman WR, Lang MH (2008). International Accounting standards and accounting quality. J. Account. Res. 46(3):467-498. |

|

|

|

|

|

Barth ME, Landsman WR, Lang MH, Williams C (2012). Are IFRS-based and US GAAP-based accounting amounts comparable? J. Account.Econ. 54(1):68-93. |

|

|

|

|

|

Bartlett MS (1938). Further aspects of the theory of multiple correlation. Proceedings of the Cambridge Philosophical Society. 34:33-40. |

|

|

|

|

|

Bartov E, Goldberg SR, Kim M (2005). Comparative value relevance among German, US, and International Accounting Standards: a German stock market perspective. J. Account. Audit. Financ. 20(2):95-119. |

|

|

|

|

|

Bolsa de Valores de São Paulo (BOVESPA) (2007). Available as of January 3th, 2007, at http://www.bovespa.com.br/principal.asp. |

|

|

|

|

|

Castro NJL (1998). Contribuição ao estudo da prática harmonizada da contabilidade da União Européia. Tese de doutorado não-publicada, Universidade de São Paulo, São Paulo, Brasil. |

|

|

|

|

|

Daske H, Hail L, Leuz C, Verdi R (2008). Mandatory IFRS reporting around the world: early evidence on the economic consequences. J. Account. Res. 46 (5):1085-1142. |

|

|

|

|

|

Dechow P, Ge W, Schrand C (2010). Understanding earnings quality: a review of the proxies, their determinants and their consequences. J. Account.Econ. 50(2-3):344-401. |

|

|

|

|

|

Ding Y, Hope O-K, Jeanjean S, Stolowy H (2007). Differences between domestic accounting standards and IAS: measurement, determinants and implications. J. Account. Public Policy 26(1):1-38. |

|

|

|

|

|

Estrella A (2007). Generalized canonical regression. Econ. J. 115(505):722-744. |

|

|

|

|

|

Financial Accounting Standards Board (FASB). SFAS 2 Accounting for Research and Development Costs, Available as of April 20th, 2008. |

|

|

|

|

|

Financial Accounting Standards Board (FASB), SFAS 13 Accounting for Leases, Available as of April 20th, 2008. |

|

|

|

|

|

Financial Accounting Standards Board (FASB), SFAS 87 Employers' Accounting for Pensions, Available as of April 20th, 2008. |

|

|

|

|

|

Financial Accounting Standards Board (FASB), SFAS 88 Employers' Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination Benefits, Available as of April 20th, 2008. |

|

|

|

|

|

Financial Accounting Standards Board (FASB), SFAS 133 Accounting for Derivative Instruments and Hedging Activities, June 1998, Available as of April 20th, 2008. |

|

|

|

|

|

Financial Accounting Standards Board (FASB), SFAS 142 Goodwill and Other Intangible Assets, Available as of April 20th, 2008. |

|

|

|

|

|

Generally Accepted Accounting Principles in the United States, Accounting Principles Board (APB) Opinion 22 - Disclosure of Accounting Policies, Available as of April 20th, 2008. |

|

|

|

|

|

Gray SJ (1980). The impact of international accounting differences from a security analysis perspective: some european evidence. J. Account. Res. Oxford. 18(1):64-76. |

|

|

|

|

|

Gray SJ (1988). Towards a theory of cultural influence on the development of accounting systems internationally. Abacus, Sidney. 24(1):1-15. |

|

|

|

|

|

Holthausen R (2009). Accounting standards, financial reporting outcomes, and enforcement. J Account. Res. 47 (2), 447-458. |

|

|

|

|

|

Hotteling H (1935). The most predictable criterion. J. Educ. Psycol. 26(2):139-142. |

|

|

|

|

|

Hotteling H (1936). Relations between two sets of variates. Biometrika. 28(3-4):321-377. |

|

|

|

|

|

Hung M (2001). Accounting standards and value relevance of earnings: an international Analysis. J. Account. Econ. 30(3):401-420. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 1 Presentation of Financial Statements, Available as of April 20th, 2008. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 16 Property, Plant and Equipment, Available as of April 20th, 2008. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 17 Accounting for Leases, Available as of April 20th, 2008. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 19 Employee benefits, Available as of April 20th, 2008. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 38 Intangible Assets, Available as of April 20th, 2008. |

|

|

|

|

|

International Accounting Standard Board (IASB), IAS 39 Financial Instruments: Recognition and Measurement, Available as of April 20th, 2008. |

|

|

|

|

|

Iudícibus Sde. (1998). Análise de balanços (7a. ed.). São Paulo: Atlas. |

|

|

|

|

|

Jeanjean T, Stolowy H (2008). Do accounting matters? An exploratory analysis of earnings management before and after IFRS adoption. J. Account. Public Policy 27(6):480-494. |

|

|

|

|

|

Kang T, Pang YH (2005). Economic development and the value-relevance of accounting information – a disclosure transparency perspective. Rev. Account. Financ. 4(1):5-31. |

|

|

|

|

|

Lang M, Wilson W, Raedy J (2006). Earnings management and cross-listing: are reconciled earnings comparable to US earnings? J. Account. Econ. 42(1-2):255-284. |

|

|

|

|

|

Leuz, C. (2003). IAS Versus US GAAP: Information asymmetry-based evidenced from Germany's new market. J. Account. Res. 41(3):445-472. |

|

|

|

|

|

London Stock Exchange (LSE). List companies. Available as of January 5th, 2007. |

|

|

|

|

|

Niyama JK (2005). Contabilidade internacional. São Paulo: Atlas. |

|

|

|

|

|

Nobes C (1998). Towards a general model of the reasons for international differences in financial reporting. Abacus 34(2):162-187. |

|

|

|

|

|

PriceWaterhouseCoopers (PWC). Semelhanças e diferenças IFRS x USGAAP x práticas contábeis adotadas no Brasil. Available as of November 21th, 2006, at http://www.pwc.com.br. |

|

|

|

|

|

Radebaugh L, Gray S, Black E (2006). International accounting and multinational enterprises (4a ed.). New Jersey: John Wiley & Sons. |

|

|

|

|

|

Richardson RJ (1999). Pesquisa social: métodos e técnicas (3a. ed.). São Paulo: Atlas. |

|

|

|

|

|

Timm NH (2002). Applied multivariate analysis. New York: Springer Verlag. |

|

|

|

|

|

Weetman P, Gray SJ (1990). International financial analysis and comparative corporate performance: the impact of UK versus US Accounting principles on earnings. J. Int. Finan. Manage. Account. 2(2):111-130. |

|

|

|

|

|

Weetman P, Gray SJ (1991). A comparative international analysis of the impact of accounting principals on profits: the USA versus the UK, Sweden and the Netherlands. Account. Bus. Res. Kingston. 21(83):363-379. |

|

|

|

|

|

Weffort EFJ (2005). O Brasil e a harmonização contábil internacional: influências dos sistemas jurídico e educacional, da cultura e do mercado. São Paulo: Atlas. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0