ABSTRACT

Investors’ curiosity on the worth of their investment could be resolved with the availability of sufficient information in predicting their returns and security. Several studies linked dividend payout to the performance of manufacturing firms in Nigeria but a few considered information as a signal to performance not necessarily to dividend. This paper examined the usefulness of accounting information in predicting the investors return especially dividend payout. Ex-post facto design was adopted using secondary data obtained from annual reports and accounts of 36 selected manufacturing firms for a period of 20 years (1997-2016). The results of the regression (fixed effects) analysis carried out revealed that lagged dividend, leverage and sales growth have significant positive effect on dividend payout while earnings per share, operating cash-flow and firm size influences dividend payout ratio negatively with the exemption of asset utilization ratio with insignificant effect. It is evident that accounting information is useful to investors’ in predicting the returns on their investment and dividend payout. Investors should look beyond past dividend in forecasting expected returns but several factors as presented in the financial statements in taking informed investment decisions.

Key words: Accounting information, lagged dividend, asset utilization, returns prediction, investment.

The two key fundamental qualities of good accounting information are to be relevant and faithfully presented. Information is said to be relevant when it possesses predictive and confirmatory features. Relevant and well-presented information enables the users to make crucial decision by examining the past, present and able to forecast the future occurrences through it (ICAN, 2014). One of the key users of financial statements is the investors; they are keen on information relating to their principal and the yearly yielded returns. However, accounting information is expected to serve as a guide in predicting the returns on their investment in a firm.

Prior to 1968, at early development of modern corporations, investors were not driven by the returns (Scott, 1912). Dividend was introduced by East India Company in 1700 and it became pronounced due to its effect on the market price of stocks (Frankfurter et al., 2003). Nwidobie (2016) asserted that, investors perceived dividend as an indication of good corporate performance and thus encourages potential investors to invest in highly-dividend paying firms.

The board of directors is saddled with the responsibility of determining the proportion of earnings to be paid as dividend viz-a-viz the portion to plough back. It is a crucial decision and several factors as investors’ expectation, availability of liquid fund, growth and investment opportunities, perception of general public in respect to firm size and its long existence, as well as ability to generate fund through other source aside plough back profit, are paramount in determining the dividend payout ratio in a firm.

Several propositions have been made on dividend ranging from dividend irrelevance theory to dividend supremacy theory. Dividend was proclaimed to be the only reason for firm’s existence (Graham and Dodd, 1934). Walter (1963) and Gordon (1963) asserted that, in an environment with economic and political instability coupled with fluctuating exchange rate, hyper-inflation, high interest rate, and market deregulations, investors would prefer having their returns in form of immediate cash than capital gains. According to Lintner (1956) signaling model, dwindling returns is a signal of firm’s unproductivity to the investors; therefore, managers tend to sustain dividend payment once it is initiated. On the contrary, Miller and Modigliani (1961) propounded that in a perfect capital market where rational investors operate, investors should be indifferent to dividend policy when corporate and individual taxes are the same.

Appropriation of earnings to returns and retained profit has been the major challenge faced by the firms. Ozoani (1998) proposed that dividend should be least to consider in earnings appropriation; that firms should focus on funding viable growth and investment opportunities and distribute the residuals, if any, as returns to investors. Investors see dividend as a link to hidden information about firm’s prospective profit and stability. Due to several controversies on dividend among various theorists on the investors’ response to dividend policy, the policy cannot assume to rest on dividend theories but on firm’s overall system behaviour.

However, looking at the dividend patterns of Nigerian firms, it still reflects the puzzle model of Black (1976) without specific pattern of dividend payment. There has been inconsistency in the pattern of dividend payment, thus the researcher is curious to know how the decision about the dividend payout ratio is derived by listed manufacturing firms in Nigeria.

Underpinning theories

This paper is anchored on Lintner’s signaling theory, agency cost of free cash-flow hypothesis, Marris growth model, pecking order theory and normative stakeholders’ theory.

Lintner (1956) propounded signaling hypothesis which stated that managers are often unwilling to cut dividend when it is introduced with the notion that it is an avenue of conveying hidden information of the firm to the investors. Also, it is believed that investors perceived dividend payment as evidence of good corporate performance. Fama and Miller (1971) opined that managers tend to be efficient when distributing excess cash flow as returns to shareholders rather than investing it in unprofitable investment opportunities. Agency cost theory postulated that shareholders usually quest for more returns when perceived that a firm has excess cash flow, thus reducing redundant fund in the care of the managers to avoid misappropriations. In contrast, pecking order hypothesis by Donaldson (1961) posited that firms rely mostly on internally generated funds in financing growth opportunities rather than distributing it as dividends; and could only opt for debt when investment opportunities exceeded their internal finance capacity. Marris (1964) asserted that firms with greater growth projects possibly have high retention ratio and pay low dividend to shareholders in the short-run but due to the returns on such investment, thus turn high-dividend paying firms in the long-run. Conclusively, normative stakeholders’ theory propounded by Freeman and Evan (1990) posited that investors should consider several factors which could impair or being impaired by manager’s decision in projecting returns on their investment in a firm.

Empirical review

Earnings as determinant of dividend payout

The study of Okoro et al. (2018) reported an insignificant positive relationship between earnings and dividend payout of Nigerian firms. In the same market, Kajola et al. (2015), Rihanat et al. (2016), Sanyaolu et al. (2017), Uwuigbe (2013), and Uwuigbe et al. (2012) found that earnings significantly and positively influence dividend decision while Morakinyo et al. (2018) and Okpara (2010) revealed a significant negative relationship between earnings and dividend payout. Studies carried out in other countries reported mixed results of earnings effect on dividend payout. In India, Gangil and Nathani (2018), Kumar and Sujit (2018), Ganesh and Suresh (2018), Nishant and Ramesh (2015), Acharya et al. (2012),n and Pandey and Ashvini (2016) discovered a significant positive relationship between earnings and dividend payout; Singhania and Gupta (2012) obtained an insignificant relationship while Brahmaiah (2018) reported a significant negative effect of earnings on dividend yield. Al-Najjar and Kilincarslan (2018) study revealed a significant positive effect of earnings on dividend payout of Turkish firms, similar results were obtained in the studies of Jaara et al. (2018) in Jordan; Gwahula and Mnyavanu (2018) in Tanzania, Lestari (2018), Fitri et al. (2016), Pangemanan et al. (2015), and Ahmad and Wardani (2014) in Indonesia, and Yusniliyana and Suhaiza (2016) in Malaysia. On the other hand, results obtained by Nkrumah et al. (2018), Nadeem et al. (2018), and Mahdzan et al. (2016) revealed insignificant positive relationship; while Yong and Mazlina (2016) obtained an insignificant negative effect of earnings on dividend payout of Malaysian firms.

Lagged dividend as determinant of dividend payout

Lestari (2018), Jaara et al. (2018), Nadeem et al. (2018), Okoro et al. (2018), Fitri et al. (2016), Adhikari (2015), Rihanat et al. (2017), and Yensu and Adusei (2016) reported a significant positive relationship between past dividend and current dividend; their findings are in accordance with Lintner’s (1956) signaling hypothesis. Lagged dividend has insignificant positive effect on dividend payout (Yusniliyana and Suhaiza, 2016). While the study of Brahmaiah (2018) reported an insignificant negative relationship between past dividend and current dividend, the result of the study conducted in Nigeria during stock market crisis in 2009 by Musa revealed a significant negative relationship between past dividend and current dividend pattern.

Leverage as determinant of dividend payout

The reports of Kumar and Sujit (2018), Jaara et al. (2018), Nkrumah et al. (2018), Gul et al. (2012), Gwahula and Mnyavanu (2018), Tahir and Mushtaq (2016), and Mahdzan et al. (2016) showed that leverage has significant negative effect on dividend payout. Similarly, Okoro et al. (2018), Nadeem et al. (2018), and Morakinyo et al. (2018) reported negative but insignificant relationship between leverage and dividend decision. On the contrary, the studies of Brahmaiah (2018), Pandey and Ashvini (2016), and Sindhu et al. (2018) revealed that leverage significantly influence firm’s ability to pay dividend positively while Lestari (2018), Gangil and Nathani (2018), and Yong and Mazlina (2016) obtained an insignificant positive relationship between leverage and dividend payout.

Growth as determinant of dividend payout

Gwahula and Mnyavanu (2018) discovered that a growing firm has low propensity to pay dividend. The report corroborated the findings of Kumar and Sujit (2018), Gangil and Nathani (2018), Fitri et al. (2016), Sanyaolu et al. (2017) and Rihanat et al. (2016), who discovered a significant negative relationship between firms growth and dividend decision. Similar but insignificant findings were reported by Lestari (2018), Nadeem et al. (2018) and Mahdzan et al. (2016). On the contrary, Nkrumah et al. (2018) and Yusniliyana and Suhaiza (2016) obtained an insignificant positive relationship between growth and dividend decision; while Tahir and Mushtaq (2016) discovered that growth has significant positive effect on dividend payout.

Firm size as determinant of dividend payout

The proportion of distributable profits payable to investors as returns is directly related to the firm’s size. Larger firms have tendency to pay higher dividends (Kumar and Sujit, 2018; Jaara et al., 2018; Morakinyo et al., 2018; Yensu and Adusei, 2016; Tahir and Mushtaq, 2016; Yong and Mazlina, 2016; Al-Najjar and Kilincarslan, 2018; Sindhu et al., 2016; Nguri and Jagongo, 2017). Similar but insignificant results were obtained by Gwahula and Mnyavanu (2018), Rihanat et al. (2016) and Sindhu (2014) while Gangil and Nathan (2018), Brahmaiah (2018), and Okoro et al. (2018), reported an insignificant negative relationship between firm size and dividend decision. On the contrary, Mahdzan et al. (2016), Lestari (2018) and Bushra and Mizra (2015) concluded that the larger the firm, the lower the propensity to pay dividend.

Agency cost as determinant of dividend payout

Kumar and Sujit (2018) and Nishant and Ramesh (2015) reported that dividend decision is positively and significantly influenced by the agency cost. On the other hand, the result of Mahdzan et al. (2016) and Bushra and Mirza (2015) study showed an insignificant negative relationship between agency cost and dividend decision while Matthias et al. (2013) revealed that agency cost has significant negative effect on dividend payout.

Operating cash-flow as determinant of dividend payout

The result of the study carried out by Lestari (2018), Al-Taleb (2012) and Imran (2011) revealed that cash-flow exerts a significant negative influence on firm propensity to pay dividend. Similarly, DemirgüneÅŸ (2015) and Soodur et al. (2016) found negative but insignificant relationship between cash-flow and dividend payout. On the contrary, Musa (2009), Nishant and Ramesh (2015), Rihanat et al. (2016), and Wasike and Ambrose (2015) concluded that cash-flow and dividend payout are directly and significantly related while Yusniliyana and Suhaiza (2016) and Al-Najjar and Kilincarslan (2018), and Echchabi and Azouzi (2016) reported an insignificant positive relationship between cash-flow and dividend decision.

This research is a reflection of causal-effect relationship between accounting ratios and dividend payout ratio of listed firms in Nigeria (manufacturing sector with the exclusion of ICT and agricultural firms). The study is an expost-facto research. Seven hundred and twenty (720) year-observations of firms were considered, being twenty (20) years of study of thirty-six (36) selected listed manufacturing firms (2007-2016). Data used in this study was obtained from the audited and reported annual reports and accounts of the selected firms within the time frame of the study.

Understanding the dividend pattern of a firm is very important to the investors, therefore this paper sought to examine the influence of accounting information in predicting the dividend payout ratio of selected manufacturing firms in Nigeria. This study developed its model from the modified model of Okoro et al. (2018) as:

DPR = α0 + α1Dit-1 + α2EPSit + α3AURit + α4LEVit + α5OCFit + α6FSit + α7FGit + εit

where DPR = Dividend Payout Ratio; LLD = Natural logarithm of preceding year dividend; EPS = Earnings per Share; AUR = Asset Utilization Ratio; LEV = Leverage; OCF = Operating Cash flow; FS = Natural logarithm of Total Assets; and FG = Firm’s Growth.

The original model of Okoro et al. (2018):

DPO = α0 + β1MV-1 + β2PROF + β3LEV + β4SIZE + β5PDO-1 + µ;

where DPO = Dividend Payout; MV = Market Value; PROF = Profitability, SIZE = Firm Size; PDO = Preceding Dividend Payout; was modified to suit the purpose of the current study and in accordance with the underpinning theories.

Three-staged procedural estimation analysis was carried out to investigate the relationship between accounting information and dividend payout ratio of listed firms in Nigeria (manufacturing sector). Nature of association among the series in the distribution was examined at first stage using correlational matrix and variance inflation factor tests. This was done to affirm the appropriateness of the combinations of the variables in the model. Pooled ordinary least square, fixed effects model and random effects model of analysis were conducted for the main analysis; while diagnostics tests, which are: serial-correlation, cross-sectional dependence and heteroskedasticity tests were carried out at the third stage to establish if: the residuals and the beta-factor of each variables in the model are uncorrelated; the residuals in the model across firms are unrelated; and there exist a constant variations among the residuals of the model within the time frame.

The individual influence and joint effects of explanatory variables on dividend payout was evaluated using t-tests and F-test at 90% confidence level, while coefficient of determination was used to examine the extent to which accounting information affects dividend payout. The analysis was carried out with the aid of Stata/IC 11.0.

Pre-estimation analysis

The pre-estimation tests were carried out to examine the appropriateness of the series in the distribution and ensure healthy association among the explanatory variables. The results of the tests are shown in Tables 1 to 3, respectively.

Descriptive statistics

The result of the preliminary analysis shown in Table 1 depicts the features of the series in the distribution and ensures the appropriateness.

Interpretation

The standard deviation, skewness and kurtosis values of the size (0.81, 0.17 and 2.4) reveal that firms operating in Nigerian manufacturing industry are relatively equal in asset capacity and evenly spread within the time frame. The skewness and kurtosis values of DPR and lagged dividend showed that dividend is averagely spread over the years; while there are periods of non-payment, there were also instances of almost 100% appropriation of earnings to dividend. Earnings reported in most of the periods are positively and widely dispersed from the mean value and there are periods of reported losses as indicated in the minimum value of -466.34.

Negative shareholders fund were reported in few periods resulting to minimum value of financial risk of -89.34. The minimum, maximum, standard deviation and skewness of the operating cash flow indicated that reported cash flow from operating activities over the period are widely below the mean value. Standard deviation of agency cost as measured as ratio of sales to total assets of 0.62 showed that assets are averagely transformed to sales; it is an indication of management efficiency. Over the years, the industry experienced minimum percentage decrease in sales of -90.7, maximum increase of 233.24 with an average increase of 13.05. The probability of the skewness and kurtosis revealed that all the series are trending, which is expected in a panel data due to heterogeneity of the firms which constitute the panel.

Multicolinearity test

A non-causal effect association among the variables was tested using Pearson correlation matrix; this is to know whether there is multicolinearity problem among the series. Variance inflation factor test was also conducted confirming the result of the correlation test.

The result of the Pearson correlation test shown in Table 2 reveals that there exist positive associations among lagged dividend, earnings per share, operating cash-flow, firm size and growth. The nature of association aligned with Lintner’s signaling theory, agency costs of free cash-flow hypothesis and Marris growth maximization theory. On the other hand, financial risk is negatively associated with lagged dividend, earnings per share, agency cost and size; this is in accordance with pecking order theory and agency cost theory. It was also discovered that agency cost and size are negatively associated; this is a signal of agency problem, managers of large firms tend to have more resources in use thus leading to inefficient utilization. All the correlation coefficients depicted in the Table 2 with the least and highest value of -0.14 and 0.56 being lower than the threshold of 0.8 is an indication that the combinations of the variables are appropriate.

Variance inflation factor test results showed the highest value of 1.79 which is below the threshold of 10 as presented in Table 3 corroborated the result of the correlation matrix that there is no multicolinearity problem among the series in the distribution.

Regression results

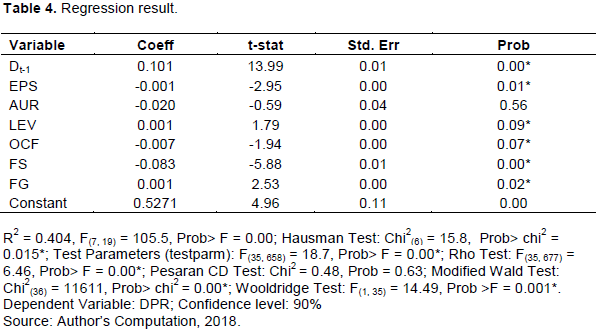

Based on the result of the Hausman and diagnostic tests conducted which reflect that fixed effects is the most appropriate analysis method but due to the results of the Modified Wald Test and Wooldridge Test which revealed that there exists an econometric problem in the model (heteroskedasticity and serial correlation problem), the standard errors of the model was adjusted with Driscoll-Kraay to correct the errors in the model and thus, the fixed effects regression with Driscoll-Kraay standard errors was used to estimate the effect of Dt-1, EPS, AUR, LEV, OCF, FS and FG on DPR and the results are presented in Table 4.

The results presented in Table 4 reveal the strength and importance of each of the accounting information measures in predicting the dividend payout. The result of the regression analysis shows that lagged dividend, leverage and sales growth have significant direct relationship with dividend payout while earnings per share, change in operating cash-flow and firm size affect dividend decision negatively. The study also discovered that asset utilization ratio has insignificant negative relationship with dividend payout ratio.

The significant positive effect of past dividend on dividend payout ratio reported in this study aligned with signaling hypothesis of Lintner (1956). The finding corroborated the reports of studies conducted in Nigeria by Rihanat et al. (2017) and Okoro et al. (2018). Also, by Lestari (2018) and Fitri et al. (2016) in Indonesia, Jaara et al. (2018) in Jordan; Nadeem et al. (2018) in Pakistan; Adhikari (2015) in Nepal, and Yensu and Adusei (2016) using African countries. The result negates the findings of Musa (2009) carried out in Nigeria. The contrast between the findings of this study and Musa (2009) could be as a result of the timing of the research. The negative relationship between dividend payout and past dividend might be based on the occurrence of global financial market crisis that hit Nigeria economy in 2008.

It was observed that Nigerian manufacturing firms have high retention ratio which could have been the cause of significant negative relationship between earnings and dividend payout ratio. This implies that as earnings increase, the appropriated profit to the investors as returns reduces. The significant negative effect of EPS on dividend payout is in consonance with pecking order theory that stated that managers maximize the use of their earnings in financing growth opportunities rather than borrowing or issuing fresh stock, thus having high retention policy. The findings also aligned with the reports of Morakinyo et al. (2018), Okpara (2010), and Brahmaiah (2018) who also obtained a significant negative relationship between earnings and dividend decision.

The asset utilization ratio with β-value of -0.02 and ρ-value of 0.56 indicates a statistically insignificant negative relationship between asset utilization ratio and dividend payout ratio. This negates the conceptual belief that a high yielded return is a function of efficient utilization of assets by the management. This result corroborated the reports of Mahdzan et al. (2016) and Bushra and Mirza (2015). These findings point to inefficient or under-utilization of assets in Nigerian listed manufacturing firms or indication of presence of agency problem whereby managers tend to trade-off shareholders return to shield their self-interest.

The significant positive effects of leverage and sales growth aligned with the postulations of Donaldson (1961) pecking order theory and Marris (1964) growth maximization theory. Donaldson believed that a firm tends to opt for debt when its growth and investment opportunities exceed its internal finance capacity while Marris asserted that returns generated from such investment would lead to more profits in the long run and high dividend payments. The report of this study on relationship between leverage and dividend decision supported the findings of Brahmaiah (2018), Pandey and Ashvini (2016), and Sindhu et al. (2018). Similarly, the significant positive effect of sales growth on dividend payout as reported in this study corroborated the report of Tahir and Mushtaq (2016).

The coefficient of the percentage change in operating cash flow of -0.007 with ρ-value of 0.07 implies that firms with high operating cash flow tend to low propensity to pay dividend. This result negates the postulation of Fama and Miller (1971) agency cost of free cash flow hypothesis but aligned with the reports of Lestari (2018), Al-Taleb (2012) and Imran (2011). The negative mean value of -313.86 is an indication that Nigerian listed firms actually experienced high percentage reduction in their operating cash flows over the years, and this could be the result of the negative relationship between percentage change in operating cash flow and dividend payout.

This study also discovered that larger firms tend to low propensity to pay dividend as reflected in the negative coefficient of firm size of -0.083 with ρ-value of 0.00. This means that firm size has significant negative effect on dividend payout ratio of listed manufacturing firms in Nigeria. The result corroborated with the findings of Mahdzan et al. (2016), Lestari (2018) and Bushra and Mizra (2015).

The coefficient of determination measured by adjusted R2 of 40.4% reflect the combined influence of earnings, past dividend, asset utilization ratio, leverage, size, sales growth and operating cash flow on dividend payout ratio. This implies that 40.4% variation in dividend payout ratio of Nigerian listed manufacturing firms is explained by the accounting information.

CONCLUSION AND RECOMMENDATION

The study investigated the predictive power of accounting information on shareholders returns using earnings, past dividend, asset utilization ratio, firm size, sales growth, leverage and operating cash flow as measure of accounting information and dividend payout ratio as dependent variable. It was observed that accounting information is useful to investors in forecasting the returns on their investment.

Generally, it is expected that larger and highly profitable firms should be highly rewarding in terms of returns to their shareholders but the reports of this study negate the conceptual beliefs. Based on the findings of this study, it is opined that investors should critically evaluate all relevant contents of accounting information within their reach in examining the returns as well as security of their investments in a firm.

The authors have not declared any conflict of interest.

REFERENCES

|

Acharya PN, Biswasroy PK, Mahapatra RP (2012). Determinants of corporate dividend policy: A study of Sensex included companies. Indian Journal of Finance 6(4):35-43.

|

|

|

|

Adhikari N (2015). Determinants of corporate dividend payout in Nepal. NRB Economic Review 1(1):53-74.

|

|

|

|

|

Ahmad GN, Wardani VK (2014). The effect of fundamental factor to dividend policy: Evidence in Indonesia Stock Exchange. International Journal of Business and Commerce 4(02):14-25.

|

|

|

|

|

Al-Najjar B, Kilincarslan E (2018). Revisiting firm-specific determinants of dividend policy: evidence from Turkey. Economic Issues 23(1):3-34.

|

|

|

|

|

Al-Taleb G (2012). Measurement of impact agency costs level of firms on dividend and leverage policy: An empirical study. Interdisciplinary Journal of Contemporary Research Business 3(10):234-243.

|

|

|

|

|

Black F (1976). The dividend puzzle. Journal of Portfolio Management 2(2):5-8.

Crossref

|

|

|

|

|

Brahmaiah B (2018). Determinants of corporate dividend policy in India: a dynamic panel data analysis. Academy of Accounting and Financial Studies Journal 22(2):1-13.

|

|

|

|

|

Bushra A, Mirza N (2015). The determinants of corporate dividend policy in Pakistan. The Lahore Journal of Economics 20(2/Winter):77-98.

|

|

|

|

|

DemirgüneÅŸ K (2015). Determinants of target dividend payout ratio: a panel autoregressive distributed lag analysis. International Journal of Economics and Financial Issues 5(2):418-426.

|

|

|

|

|

Donaldson G (1961). Corporate debt capacity: A study of corporate debt policy and the determination of corporate debt capacity. Division of Research, Harvard Graduate School of Business Administration. (Reprinted in 2000; Washing DC, USA: Beard Books).

|

|

|

|

|

Echchabi A, Azouzi D (2016). Determinants of dividend payout ratios in Tunisia: Insights in light of the Jasmine revolution. Journal of Accounting, Finance and Auditing Studies 2(1):1-13.

|

|

|

|

|

Fama EF, Miller MH (1971). The Theory of Finance. New York: Holt, Rinehart and Winston.

|

|

|

|

|

Fitri RR, Hosen MN, Muhari S (2016). Analysis of factors that impact dividend payout ratio on listed companies at Jakarta Islamic Index. International Journal of Academic Research in Accounting, Finance and Management Sciences 6(2):87-97.

|

|

|

|

|

Frankfurter G, Wood BG, Wansley J (2003). Dividend Policy: Theory and Practice. Imprint of Elsevier science, San Diego CA, USA: Academic Press.

|

|

|

|

|

Freeman RE, Evan WM (1990). Corporate governance: A stakeholder interpretation. Journal of Behaviour Economics 19(1):337-359.

Crossref

|

|

|

|

|

Ganesh S, Suresh M (2018). Dividend payout determinants: Indian Companies. International Journal of Pure and Applied Mathematics 118(18):1529-1537.

|

|

|

|

|

Gangil R, Nathani N (2018). Determinants of dividend policy: A study of FMCG sector in India. IOSR Journal of Business and Management (IOSR-JBM) 20(2/1):40-46.

|

|

|

|

|

Gordon MJ (1963). Optimal investment and financing policy. The Journal of Finance 18(2):264-272.

|

|

|

|

|

Graham B, Dodd DL (1934). Security Analysis. New York: Whittlesey House.

|

|

|

|

|

Gul S, Mughal S, Shabir N, Bukhari SA (2012). The determinants of corporate dividend policy: An investigation of Pakistani Banking Industry. European Journal of Business and Management 4(12):1-5.

|

|

|

|

|

Gwahula R, Mnyavanu W (2018). Determinants of dividend payout of Commercial Banks Listed at Dar Es Salaam Stock Exchange (DSE). Account and Financial Management Journal 3(06):1571-1580.

|

|

|

|

|

ICAN (2014). Financial Accounting. 2014 Annual Report & Financial Statements. Available at:

View

|

|

|

|

|

Imran K (2011). Determinants of dividend payout policy: a case of Pakistan Engineering Sector. The Romanian Economic Journal 14(41):47-60.

|

|

|

|

|

Jaara B, Alashhab H, Jaara OO (2018). The determinants of dividend policy for non-financial companies in Jordan. International Journal of Economics and Financial Issues 8(2):198-209.

|

|

|

|

|

Kajola SO, Desu AA, Agbanike TF (2015). Factors influencing dividend payout policy decisions of Nigerian listed firms. International Journal of Economics, Commerce and Management 3(6):539-557.

|

|

|

|

|

Kumar BR, Sujit KS (2018). Determinants of dividends among Indian firms-An empirical study. Cogent Economics and Finance 6(1):1423895.

Crossref

|

|

|

|

|

Lestari HS (2018). Determinants of corporate dividend policy in Indonesia. The 4th International Seminar on Sustainable Urban Development IOP Conf. Series: Earth and Environmental Science 106(2018):1-7.

Crossref

|

|

|

|

|

Lintner J (1956). Distribution of incomes of corporations among dividends, retained earnings, and taxes. American Economic Review 46(1):97-113.

|

|

|

|

|

Mahdzan NS, Zainudin R, Shahri NK (2016). Interindustry dividend policy determinants in the context of an emerging market. Economic Research‑Ekonomska Istraživanja: Routledge, Tayloir and Francis Group 29(1):250‑262.

|

|

|

|

|

Marris R (1964). The Economic Theory of Managerial Capitalism. London WC: Palgrave Macmillan and Company Limited

Crossref

|

|

|

|

|

Matthias N, Nyema W, Bariyima K (2013). Determinants of dividend policy: Evidence from listed firms in the African stock exchanges. Panoeconomicus 60(6):725-741.

Crossref

|

|

|

|

|

Miller MH, Modigliani F (1961). Dividend policy, growth and the valuation of shares. Journal of Business 34(1):411-433.

Crossref

|

|

|

|

|

Morakinyo FO, David JO, Adeleke EO, Omojola SO (2018). Determinants of dividend policy of listed deposit money banks in Nigeria. World Journal of Finance and Investment Research (International Institute of Academic Research and Development) 3(1):25-40.

|

|

|

|

|

Musa FI (2009). The dividend policy of firms quoted on the Nigerian stock exchange: An empirical analysis. African Journal of Business Management 3(10):555-566.

|

|

|

|

|

Nadeem N, Bashir A, Usman M (2018). Determinants of dividend policy of Banks: Evidence from Pakistan. The Pakistan Journal of Social Issues Special Issue (June):19-27. Available at: View

|

|

|

|

|

Nguri JM, Jagongo AO (2017). Determinants of dividend payout ratio for profitable non- financial companies listed in Nairobi Securities Exchange in Kenya. International Journal of Research and Current Development 2(2):86-93.

|

|

|

|

|

Nishant BL, Ramesh CD (2015). Determinants of dividend payout ratio: Evidence from Indian companies. Macrothink Institute: Business and Economic Research 5(2):217-241.

|

|

|

|

|

Nkrumah ENK, Ofori DN, Anaba OA, Serwah AL (2018). Determinants of dividend policy among banks listed on the Ghana Stock Exchange. Research Journal of Finance and Accounting 9(4):11-19.

|

|

|

|

|

Nwidobie BM (2016). Corporate governance practices and dividend policies of quoted firms in Nigeria. International Journal of Asian Social Science 6(3):212-223.

Crossref

|

|

|

|

|

Okoro CO, Ezeabasili V, Alajekwu UB (2018). Analysis of the determinants of dividend payout of consumer goods companies in NIGERIA. Annals of Spiru Haret University Economic Series, ICCS 1(2018):141-166.

Crossref

|

|

|

|

|

Okpara GC (2010). A diagnosis of the determinant of dividend pay-out policy in Nigeria: A factor analytical approach. American Journal of Scientific Research 8(1):57-67.

|

|

|

|

|

Ozoani GC (1998). Basic of Financial Management and Analysis. Enugu: Veamark Publishers.

|

|

|

|

|

Pandey SN, Ashvini N (2016). A study on determinants of dividend policy: Empirical evidence from FMCG sector in India. Pacific Business Review International 1(1):135-141.

|

|

|

|

|

Pangemanan SS, Kaligis N, Oratmangun S (2015). The characteristics of dividend payers from banking sectors in Indonesia. Research Journal of Finance and Accounting 6(6):248-252.

|

|

|

|

|

Rihanat IA, Nur AA, Woei-Chyuan W (2016). Dividend Payment Behaviour and its Determinants: The Nigerian Evidence. African Development Review 28(1):53-63.

Crossref

|

|

|

|

|

Sanyaolu WA, Onifade HO, Ajulo OB (2017). Determinants of dividend policy in Nigerian manufacturing firms. Research Journal of Finance and Accounting 8(6):105-111.

|

|

|

|

|

Scott WR (1912). The Constitution and Finance of English, Scottish, and Irish Joint Stock Companies to 1720. Cambridge: Cambridge University Press.

|

|

|

|

|

Sindhu IM, Shujahat HH, Ehtasham U (2016). Impact of ownership structure on dividend payout in Pakistani non-financial sector. Cogent Business and Management 3(1):1272815.

Crossref

|

|

|

|

|

Sindhu IM (2014). Relationship between free cash flow and dividend: Moderating role of firm size. Research Journal of Finance and Accounting 5(5):16-23.

|

|

|

|

|

Singhania M, Gupta A (2012). Determinants of corporate dividend policy: A Tobit model approach. Vision 16(3):153-162.

Crossref

|

|

|

|

|

Soodur SAK, Maunick D, Sewak S (2016). Determinants of the dividend policy of companies listed on the stock exchange of Mauritius. Proceedings of the Fifth Asia-Pacific Conference on Global Business, Economics, Finance and Social Sciences (AP16 Mauritius Conference) ISBN - 978-1-943579-38-9 Ebene-Mauritius, January 21-23.

|

|

|

|

|

Tahir M, Mushtaq M (2016). Determinants of dividend payout: evidence from listed oil and gas companies of Pakistan. The Journal of Asian Finance, Economics and Business 3(4):25-37.

|

|

|

|

|

Uwuigbe OR (2013). Determinants of dividend policy: a study of selected listed firms in Nigeria. Change and Leadership 17(1):107-119.

|

|

|

|

|

Uwuigbe U, Jafaru J, Ajayi A (2012). Dividend policy and firm performance: A study of listed firms in Nigeria. Accounting and Management Information Systems 11(3):442-454.

|

|

|

|

|

Walter JE (1963). Dividend policy: Its influence on the value of the enterprise. Journal of Finance 18(1):280-291.

Crossref

|

|

|

|

|

Wasike WTA, Ambrose J (2015). Determinants of dividend policy in Kenya. International Journal of Arts and Entrepreneurship 4(11):71-80.

|

|

|

|

|

Yensu J, Adusei C (2016). Dividend policy decision across African Countries. International Journal of Economics and Finance 8(6):63-77.

Crossref

|

|

|

|

|

Yong T, Mazlina M (2016). Determinants of dividend payout ratio: evidence from Malaysian public listed firms. Journal of Applied Environmental and Biological Sciences 6(1):48-54.

|

|

|

|

|

Yusniliyana Y, Suhaiza I (2016). Determinants of dividend policy of public listed companies in Malaysia. Review of International Business and Strategy 26(1):88-99.

Crossref

|

|