Full Length Research Paper

ABSTRACT

This paper deals with enhanced relationship participation in an international context. The purpose of this paper is to present insight into the essentials for implementing a Tax Control Framework (TCF) and to present incentives to participate in an enhanced relationship. First, the relevant guidance for implementing a TCF is described. Second, based on a survey with tax directors of the largest Dutch multinational organizations quoted on the Dutch stock exchange incentives for participating in an enhanced relationship are investigated. Performing an analysis on the results identifies two important incentives for organizations to participate in an enhanced relationship.

Key words: Controlling, corporate governance, enhanced relationship, Tax, OECD, internal control

INTRODUCTION

Tax compliance and tax accounting are radically changing in most countries worldwide as part of an initiative of the Organization for Economic Co-operation and Development (OECD). Information notes published by the OECD stimulate the implementation of risk concentrated tax authorities resulting in an “enhanced relationship”. The aim is that companies organize their tax structure risk base (OECD, 2010), comparable with the overall internal control systems emphasized after the Enron failure. The tax structure should give tax authorities insight into the largest tax risks. Based on the OECD initiative countries all over the world implemented enhanced relationship policies in their national regulations (Bakker and Kloosterhof, 2010). In 2005 the Dutch tax authorities introduced a version of the tax based regulation proposed by the OECD, “horizontal monitoring”.

From the year 2007 horizontal monitoring is official policy in the Netherlands (Belastingdienst, 2008; Van Daelen and Van der Elst, 2010). Horizontal monitoring changes the relation of the tax authorities and companies. On one hand, the tax authority has to stimulate an environment of trust and close cooperation. On the other hand companies are expected to contact the tax authorities whenever there is ambiguity about the tax obligation resulting from activities.

The advantage for the tax authorities is a better allocation of resources as it can focus on the organizations and/ or parts of organizations with the highest perceived risk. The advantage for companies is a Less intensive tax investigation by the tax authorities at year end (Kemp and Verbakel, 2010). To reach these advantages the tax authorities needs insight into the risks of companies. To fulfill this requirement the Dutch tax authorities obliged companies who want to participate in horizontal monitoring to set up a Tax Control Framework (TCF).

However, only limited Dutch guidance for a TCF is available; the Dutch Tax Authorities have no mandatory framework. The OECD offers some general guidance. Besides, well known models are present from controlling process other than tax, for example COSO and COBIT. A TCF model fulfilling the requirements of the OECD, COSO, COBIT and the Dutch Tax Authorities is the Tax Management Maturity Model (T3M). This model identifies tax risks in six specific tax related subjects: Business and (Tax) environment, Business operations, Tax Operations, Tax Risk Management, Monitoring/Testing and Tax assurance. These broad areas are divided into more specific factors which are the fundaments for the judgment of a subject.

This paper focuses on the fundaments for implementing a TCF and the main incentives for companies to participate in an enhanced relationship. First, relevant TCF guidance will be stated. As a TCF should fulfill requirements by relevant authorities, understanding this requirements is important. The question that will be answered is what guidance is in place by the OECD, Dutch tax authorities, COSO and COBIT for implementing a TCF? Second, focusing on practitioners in Dutch multinational firms answer will be given to the research question what are the main incentives for multinationals to participate in an enhanced relationship? Specifically, the focus will be on three possible incentives: effect on the business environment, new rules and policies in the short term, and the Netherlands as a tax haven.

This paper continues with the scientific relevance. Then the relevant TCF guidance from the OECD, the Dutch tax authorities, and controlling models will be discussed. The last part of this paper focuses on the results and analysis of a survey with Dutch multinationals quoted on the largest Dutch stock exchanges.

Scientific relevance

Enhanced relationships[1] are regularly discussed in the scientific literature (eSimonis, 2008; De Groot and Van de Enden, 2010). However, the (international) guidelines existing for a TCF have been rarely discussed in the literature. Tax controlling - and a TCF as a part of it - is a portion of the organization’s corporate governance. So, research on the implementation of a TCF is rewarding for the controlling literature as well for company’s best practices. The first important contribution of this paper to the literature is the creation of a universal guideline for the development of a TCF. The Dutch focus of this paper could be easily changed to another country focus by replacing the Dutch tax law factors by other countries’ tax laws factors.

The second important contribution of this paper is the focus on practitioners. An enhanced relationship could not be entirely based on theoretical concepts, but practitioners should contribute to enhanced relationship policies as this will overcome problems not recognized when focusing solely on theories. Only limited research concerning an enhanced relationship focused on practitioners (Freedman et al., 2009).

The survey results presented in this paper show companies’ incentives for participating in an enhanced relationship. As willingness by companies to participate in an enhanced relationship is essential for the success of this policy, this paper exposes important insights for further implementation of enhanced relationship laws and regulations worldwide.

Guidance

OECD

The OECD introduced the concept of an enhanced relationship. After years of discussion with the member states and the draft of many papers 35 economies signed in 2006 the Seoul declaration (OECD, 2006): the commitment for cooperation on efficient and international orientated tax authorities. In 2008 this commitment has been followed up by the Cape Town Communiqué (OECD, 2008). Representatives of 45 economies discussed the application of risk management to taxes. Understanding the risk management of companies gives the tax authorities the possibility to allocate their resources to parts of organizations with higher risks (less effective risk management) and companies not in control for their taxes at all.

In the years after Cape Town the OECD introduced reports giving participating economies high-level input for enhanced relationship implementation (OECD, 2010; 2011; 2012). The main guidance consists of four aspects: real-time contact with companies about tax issues, focus on tax related processes, make tax compliance easier, and stimulate a good cooperation between the tax authorities and companies and their stakeholders.

Dutch tax authorities obliged implementing a TCF for horizontal monitoring participation but supported the interpretation of a TCF only with limited guidance (Belastingdienst, 2008). The horizontal monitoring documentation published by the Dutch tax authorities states that practitioners have to develop a TCF from their own knowledge and experience. Limited guidance is given in this documentation by referencing COSO as possible tool for implementing a TCF.

COSO (ERM)[2]

COSO is a model developed to support companies in setting their internal control frameworks (COSO, 2004). It consists of four company goals. These goals are linked to four organizational levels and eight risk and control components. Besides the model COSO publishes additional reports which can be used by practitioners as best practice: the reports anticipate on new challenges companies encounter (e.g. COSO, 2009). So, usage of the COSO model requires also the application of the COSO reports.

COBIT

Information technology (IT) has a great impact on the functioning of most organizations. The processes concerning IT (IT governance) should be in control. A model supporting this purpose is COBIT[3] developed by ISACA[4]. COBIT consists of five principles which are the fundaments of the model: meeting stakeholder needs, covering the enterprise end-to-end, applying a single integrated framework, enabling a holistic approach, and separating governance from management. This leads to the practical implementation by the “key areas” defined in COBIT: plan, build, run, monitor, and governance.

Combining the guidance given in the sections above creates a framework for implementing a TCF. This framework can be easily internationally implemented, as only the guidance of the Dutch tax authorities has to be replaced to make it fit for other countries than the Netherlands. As mentioned before, a model fulfilling the (international) requirements for setting a TCF is the Tax Management Maturity Model (Colon, 2012).

Large multinationals

This part of the paper contains findings of a survey with tax directors of large multinationals. The results of the survey are further analyzed to find the incentives that are the most important for large multinationals to participate in an enhanced relationship. First the hypotheses will be rationalized, which form the input for our survey. Second the analysis and results will be discussed. Research on enhanced relationship with surveys is very limited. In the paper is referenced Freedman et al. (2009). The only relevant survey in relation to enhanced relationships is our focus. In this research the UK practice has been examined. As there is limited relevant research specific for an enhanced relationship, hypotheses are framed partly by (indirect) related literature and commons sense. Considering the limited research with surveys specific for enhanced relationships, it is not possible to add more relevant literature and we consider literature that is only very limited not as value adding.

Hypotheses

Organizational goals are not only limited to the interest of shareholders. Organizations have to consider the interests of all the stakeholders. Corporate social responsibility (CSR) has an important impact on modern societies. A description of CSR is (Jones et al., 2009): the integration of social, economic, ethical and environment considerations into the organizational strategy and operational activities. So transparency about taxes is also a part of this description.

Not every society organizations’ operations require the same strictness of CSR. The strictness of CSR could be an incentive for organizations to settle in a specific country. Of importance is the perception of the relevant society: does the society perceive the organization in performing their activities regarding CSR. Specific for taxes, this could entail an in-control statement for the TCF (De Groot and Van der Enden, 2010). However, it is important for companies to consider an enhanced relationship relevant for their business. If companies consider an enhanced relationship as positive for their business one could expect them to be more positive in the implementation of an enhanced relationship.

Hypothesis 1

The perception of a better business environment by an enhanced relationship is positively related to the willingness to participate in an enhanced relationship.

Not every company implements the same level of CSR. Some companies are more prepared to implement high level CSR than others. Currently an enhanced relationship is no obligation. However, when companies expect new compliance rules to be applied in the near future, companies have to consider how this impacts their activities. For an enhanced relationship this could mean that companies are more willing to participate immediately.

Hypothesis 2

The expectation of a short term (five years) international obligation to participate in an enhanced relationship is positively related to the willingness to participate in an enhanced relationship.

Some companies present themselves to the society as part of their CSR policy. If companies could be expected to be more society concerned regardless of the reputational effects and possible higher profits,

companies are expected to be more willing to pay taxes. Following this rationale, companies of the opinion that taxes can easily be avoided should be more convenient with an enhanced relationship as these present them-selves more positively than relative less paying companies.

Hypothesis 3

The perception of the Netherlands as a tax haven is positively related to the willingness to participate in an enhanced relationship.

[1] As mentioned the Dutch form of a “enhanced relationship” is “horizontal monitoring”. For the ease of reading in this paper the term “enhanced relationship” is used when the Dutch form is concerned.

[2] Committee of Sponsoring Organizations of the Treadway Commission (Enterprise Risk Management). For a detailed background see: www.coso.org

[3] Control Objectives for Information and related Technology

[4] Information Systems Audit and Control Association

METHOD

The assumed relations will be tested by a survey with a selection of companies. The selection of companies is limited to Dutch multinationals quoted on the largest Dutch stock exchanges (AEX and Midkap). No difference was made to industry or the quotation on only the Dutch or also other stock exchanges. The Dutch multinationals quoted on the Dutch stock exchanges concern the most relevant sample as the Dutch tax authorities focused initially on the these companies before implementing enhanced relationships at other companies. Therefore these companies have more experience with an enhanced relationship than other companies in the Netherlands. For the selected companies a survey had been sent to the company’s tax director. The relevant period of the survey is March to May 2012. The operational numbers are extracted from the relevant annual reports (2012). The sample is states of twenty companies.

Measures

Dependent variable - The measure for the willingness to participate in an enhanced relationship has been measured by a number given by the tax directors scaled from one to five (one is no willingness and five is the opposite).

Independent variables - The effect on the business environment has been determined by questioning respondents considering an enhanced relationship to be negative (one), with no effect (two) or positive (three) for the business environment.

The expectation that an enhanced relationship will be an obligation on the short term (five years) has been measured on a five point scale (five is an enhanced relationship is highly expected). Respondents were questioned to consider the short term obligation of an enhanced relationship in an international context.

The perception of the Netherlands as a tax haven has been EU centered. The tax directors were questioned to consider the taxes in comparison to the other EU member states. Number one indicates low tax avoidance while five indicates that the Netherlands is considered as a tax haven.

In addition, a control variable has been put into the sample to exclude the possible impact of other factors on the hypotheses. As larger companies have a larger impact on their environment; more pressure exists on a company to have more CSR. This possible impact has to be excluded. So, a control variable for the number of employees of a company has been adopted. The number of employees is measured by a logarithm of the actual number of employees.

Method of analysis

Relations will be considered by using SPSS. In SPSS the relations are tested with linear regression. With this method the relations between the first three mentioned independent variables and the dependent variable as described above (conform the hypotheses formulated above) are tested.

RESULTS

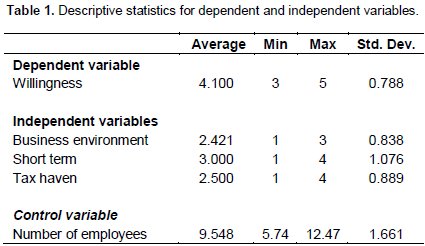

The descriptive statistics (Table 1) show no indication for an exceptional sample. The willingness for an enhanced relationship (4.100 out of 5) is high in the sample. Besides, an enhanced relationship is considered to be positive for the business environment (2.421 out of 3). The perception of an enhanced relationship obligation in the short term and the perception of the Netherlands as a tax haven are neither considered to be positive or negative by the tax directors (3.000 and 2.500 out of 5 respectively). The number of employees in the sample is considered to be high (9.548 after using a logarithm) compared to other research, for example Gallo and Christensen (2011) who found an average of 2.28. However, this is plausible as our sample consists only of the largest Dutch multinationals.

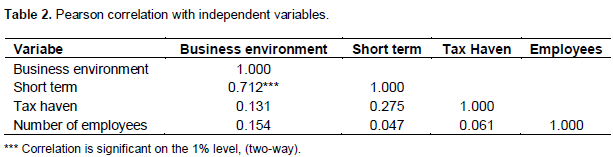

The Pearson correlation (Table 2) shows only one notable outcome. Tax directors who are of the opinion that an enhanced relationship is positive for the business environment are expecting an enhanced relationship to be obliged in the short term. So, based on this finding, logically, it could be expected that these variables are either or neither related to the willingness to participate in an enhanced relationship. No other correlations were found in the sample.

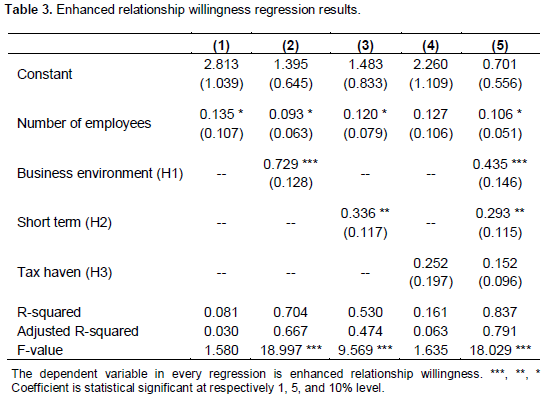

Hypothesis 1 suggested a relation between the perceived (positive) effect on the business environment and the willingness to participate in an enhanced relationship. The regression results (Table 3) presented a significant relation on 1% level (coefficient of 0.729). Based on the sample the perceived effect on the business environment is a major incentive for companies to participate in an enhanced relationship. Hypothesis 1 is accepted.

Hypothesis 2 suggested a relationship between the obligation to participate in an enhanced relationship in the short term (less than five years) and the willingness to participate in an enhanced relationship. The regression results presented a significant relation on 5% level (coefficient 0.336). Based on the sample the perception of the short term obligation of an enhanced relationship is an incentive for companies to participate in an enhanced relationship. Hypothesis 2 is accepted.

Hypothesis 3 suggested a relationship between the perception of the Netherlands as a tax haven and the willingness to participate in an enhanced relationship. The regression results presented no significant relation for this hypothesis. Based on the sample the perception of the Netherlands as a tax haven is no incentive for companies to participate in an enhanced relationship. Hypothesis 3 is rejected.

DISCUSSION

The first part of this paper discussed relevant guidelines for implementing a TCF. International guidelines were described and Dutch guidelines for an enhanced relation-ship were mentioned. It was noticed that the Dutch guidelines stated could easily be replaced by another national guideline for having a universal framework for implementing TCF. Important contributions to the literature have been made by giving an overview of the relevant literature usable universally. For every company implementing a TCF, the guideline mentioned is the basis for implementation.

The second part of this paper presented the analysis of a survey with tax directors employed at Dutch multi-nationals quoted on the largest Dutch stock exchanges. Two important incentives influencing the willingness of companies to participate in an enhanced relationship has been identified: a (perceived) positive impact on the business environment and the expectation that an enhanced relationship will be an obligation in the short term (less than five years). This finding is very important for tax authorities and scholars. For the tax authorities the fundamental has been put for a tax policy stimulating large multinationals to participate in an enhanced relationship. Future regulations should focus more on the benefits for companies to stimulate participation in an enhanced relationship. First we recommend that a financial incentive be given to companies, for example, by lower compliance cost for government regulations charged to companies. Second, we recommend that a reputation incentive be put in place, for example, by obliging the disclosure of the state of the TCF in the annual report. For scholars an important insight has been presented: not a purely theoretical approach has been used for the explanation why an enhanced relationship is or is not a success in a country; but with this paper the beginning of an understanding of company perception/ motivation towards an enhanced relationship has been presented.

This paper has limitations giving possibilities to further scientific research. First, as this paper is limited to the relevant framework for an enhanced relationship in the Netherlands, further investigation could focus on another country or identify the differences between the national guidelines to build further on a (international) framework for a TCF. Second, this paper focused only on a limited amount of incentives influencing the willingness of companies to participate in an enhanced relationship. Additional incentives could be the topic of further research. Besides, the context could also be chanced; this paper focused on the largest organizations, while it is possible smaller organizations or organizations in other countries would give other outcomes. Third, the sample in this paper is small (2o). A small sample is very sensitive for movement in the outcome of one or more items limiting the generalization of this paper. Further research could be focused on overcoming this limitation

CONCLUSION

This paper presented the relevant guideline for imple-menting a TCF with a focus on the Netherlands. Besides, this paper identified two important incentives for companies to participate in an enhanced relationship: the perception of a positive effect on the business environment and the expectation that an enhanced relationship will be an obligation in the short term.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Bakker A, Kloosterhof S (2010). Tax Risk Management: From Risk to Opportunity. Amsterdam: International Bureau of Fiscal Documentation. |

|

|

|

|

|

Belastingdienst (2008). Tax Control Framework: van risicogericht naar "in control": het werk verandert'. Policy paper Belastingdienst. available at www.belastingdienst.nl, http://download.belastingdienst.nl/belastingdienst/docs/tax_control_framework_dv4011z1pl.pdf, last accessed on 30 September 2013. |

|

|

|

|

|

Colon DW (2012). Toetsing van het Tax Management Maturity Model en horizontaal toezicht bereidheid in Nederland. Working paper University of Groningen. |

|

|

|

|

|

COSO (2004). Enterprise Risk Management: Integrated Framework. Committee of Sponsoring Organizations of the Treadway Commission. |

|

|

|

|

|

COSO (2009). Strengthening Enterprise Risk Management for Strategic Advantage. Committee of Sponsoring Organizations of the Treadway Commission. |

|

|

|

|

|

Daelen M, van Elst, C van der (2010). Risk Management and Corporate Governance. Edgard Elgar, Cheltenham. |

|

|

|

|

|

Freedman J, Loomer G, Vella J (2009). Corporate Tax Risk and Tax Avoidance: New Approaches' Bri. Tax Rev. (1):74-116. |

|

|

|

|

|

Gallo P, Cristensen L (2011), Firm Size Matters: An Empirical Investigation of Organizational Size and Ownership on Sustainability- Related Behaviors. Bus. Soc. 50(2):315-349. |

|

|

|

|

|

Groot J, Enden E, van der (2010). Verantwoording over interne beheersing onder Horizontaal toezicht. Weekblad voor Fiscaal Recht 6851:375-382. |

|

|

|

|

|

Kemp J, Verbakel R (2010). Knelpunten van horizontaal toezicht bij middelgrote ondernemingen. Weekblad voor Fiscaal Recht 6844:124-130. |

|

|

|

|

|

Organisation for Economic Co-operation and Development, (2006). Seoul Declaration. OECD declaration. |

|

|

|

|

|

Organisation for Economic Co-operation and Development, (2008). Cape Town Communique. OECD communique. |

|

|

|

|

|

Organisation for Economic Co-operation and Development, (2010). Tax Compliance and Tax Accounting Systems. Information note OECD. |

|

|

|

|

|

Organisation for Economic Co-operation and Development, (2011). Tackling Aggressive Tax Planning Through Improved Transparency and Disclosure. Information note OECD. |

|

|

|

|

|

Organisation for Economic Co-operation and Development, (2012). Right from the start: Influencing the Compliance Environment for Small and Medium Enterprises. Information note OECD. |

|

|

|

|

|

Simone L, Sansing R, Seidman J (2011). When are Enhanced Relationship Tax Compliance Programs Mutually Beneficial? Working paper SSRN. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0