Full Length Research Paper

ABSTRACT

Taxation has gained considerable attention in the past few year and lot of studies have been done on tax evasion and tax compliance. This study assesses the level of tax and identifies factors that shape tax morale in Mauritius. A self-developed questionnaire was distributed to 250 randomly respondents and a logistic regression analysis was used to analyse data collected. A high degree of tax morale is required to achieve high level of tax compliance. The result shows that socio-demographic and socio economic factors have an impact on tax morale and it can be seen that social norm, fairness and equity, trust in government and in tax authority are determinants that shape tax morale. The findings are in line with that some authors who found out that that there is a positive correlation between inequity and tax evasion. The study recommended that population should be educated, tax system should be simplified, government should be fair and tax authority should respect the population.

Key words: Tax evasion, logit model, cross sectional regression, tax morale.

INTRODUCTION

In the 1990s, the concept of tax morale has started to attract attention of researchers. Researchers have tried to analyse why lots of people pay their taxes, despite the fact that fines and probability of audit are low. A special survey has shown that based on the expected utility concept, traditional theories predict a lesser tax compliance. Based on such finding, new research has been conducted to find new factors that influence tax morale. The first finding on tax morale was by German scholars centred on Gunter Schmolders. These authors claimed that the traditional point of view of analysing tax is biased. The question about tax morale is rather why people do not cheat.

In some countries, the level of detection and penalty is so low that taxpayers would evade tax if they were rational but they still comply with paying their taxes. Many authors have argued that tax morale has been a motivating factor for taxpayers to pay taxes and has also contributed to a high degree of tax compliance. Erard and Feinstein (1994) have integrated moral sentiments into the rational model to explain the actual behaviour of taxpayers. Furthermore, Andreoni et al. (1998) pointed out that implementing moral and social dynamic to the traditional model is largely an undeveloped area of research.

Tax compliance is not only based on tax rates, probability of detection, and enforcement but also on the willingness of individual to either evade or comply with tax law. Therefore, it is important to analyse the concept of tax morale. Tax morale is defined as an “intrinsic motivation” to pay tax rather than a legal obligation. In other word, it can be said that, it is a moral obligation to pay tax and to contribute to the general welfare of the society (Torgler, 2003; Torgler, 2004b; Torgler and Schneider, 2009). It is said that a high level of tax morale will result in a relatively high tax compliance.

Research objectives

The goal of this study is to assess the level of tax morale in Mauritius. This study is conducted to identify the various determinants of tax morale. Lot of studies has been done on tax evasion and tax compliance but not on tax morale. Morality can affect tax compliance. The perception of what is good and bad in Mauritius culture will have a large influence in deciding whether to evade or not. The objective of this study is also to find ways and develop policies to improve tax morale and tax compliance as according to the population, Mauritius is highly corrupted The relationship between tax morale, tax evasion and tax compliance will also be examinable in this study.

LITERATURE REVIEW

Tax evasion

Based on the economic crime model, Allingham and Sandmo (1972) presented a formal model, in which self-interested taxpayers evade tax by underreporting their income so as to maximize expected utility or individuals pay their taxes because they fear of being caught. This model has been criticized by many authors. In some countries, tax compliance is high even though the probability of detection and penalty rate is low. Torgler et al. (2010) stated that the problem with this model is that the actual deterrence level is estimated to be too low to explain the high level of tax compliance, Researchers like Lewis (1982), Pommerehne and Frey (1992) and Pommerehne et al. (1994), Frey and Feld (2002) and Torgler (2001a, 2002) try to link high degree of tax compliance with tax morale. Tax morale can be the solution to explain why people do not cheat despite penalty and the probability of detection being low.

It is argued by many authors that factors such as socio-economic and socio- demographic factors, perception of fairness, trust in government and tax authority and the equitable exchange between taxpayers and government can have an effect on tax morale.

Tax morale, socio-economic and socio- demographic factors

Tittle (1980) stated that “older people have higher tax morale as they are sensible to sanction as they have developed greater social incentives over the years”. Social psychologists have also found that males have a relatively lower tax morale than females. Education is another factor that can influence tax morale. Educated people might be more compliant because they are in a better position to understand why it is important to comply with tax law and they are supposed to know the benefits of tax contribution to the society. However, they may be less compliant, as they have knowledge about tax evasion and avoidance and might know how the government uses the tax revenues. In Switzerland and the United States, married people have higher tax morale than non-married people. Strümpel (1969) assessed the level of tax morale among self-employed workers in Europe and found that self-employers have lower levels of tax morale than employees. Empirical findings stated that religiosity has an effect on tax morale in Great Britain, West Germany, United States, and Canada and it has a significant positive effect on tax morale.

Factors that shaped tax morale

Schwartz and Orleans (1967) conducted an experiment and found that moral norms have a stronger influence on taxpayers rather than punishment threats. Guilt, shame, duty and fear are the four sentiments that can affect tax morale. It can be seen that social norm, fairness and equity, trust in government and in tax authority have an effect on tax morale which contribute in tax compliance. Alm et al. (1999) argued that “as long as people believe that tax compliance is a social norm”, individuals will have a positive attitude toward tax compliance. The violation of social norms will induce internal effects such as guilt and remorse, and an external and social effect such as gossip and ostracism.

Grasmick and Bursick (1990) interviewed 355 individuals and he found that the expected guilt associated with tax evasion served as a much greater constraint than sanctions. The degree to which individuals will feel a sense of guilt or shame will depend on the extent to which individuals will believe that tax compliance is a social norm. Scholz and Pinney (1995) argued that individuals rely on heuristics to develop subjective evaluations of risk as the probability of being caught is uncertain.

Spicer (1974) and Song and Yarbrough (1978) have conducted a study on the relationship between tax evasion and perceived inequalities in tax system and they found that there is a positive correlation between inequity and tax evasion. Taxpayers will see tax evasion as a re-establishment of fairness, if the terms of trade between the state and the taxpayers are not fair. Spicer and Lundtstedt (1976) argued that taxpayers will feel cheated if they feel that the tax revenues is not spent well. Smith (1992) and Stalams (1991) indicated that positive actions and appropriate use of tax revenues will raise tax morale as those positive actions will encourage taxpayers to have a positive attitudes and commitment toward tax system. Findings stated that there is a positive relationship between trust and tax morale. More trust in the state, tax authority and legal system will enhance tax morale. Empirical evidences stated that there is a positive relationship between perceived public spending and tax morale. Thibaut et al. (1974) concluded that tax compliance will be high if taxes are paid back in the form of public services. Frey and Feld (2002) argued that tax morale will be higher, if tax officer treat taxpayers with respect. Alm and Torgler (2006) found that tax morale will increase if taxpayers are treated with respect by the tax authority

Institutions such as federalism and direct democracy can have an impact on tax morale. Empirical findings showed that institutional factors increased tax morale. Feld and Frey (2002b) analysed how tax officers treat taxpayers in Switzerland, and found that taxpayer in areas with more direct participation rights have a higher tax morale as tax authorities are more respectfully and less suspicious about underreporting income compared to areas with less direct democracy.

Analysis of tax morale in different countries

East and West Germany was used to analyse the effect of different cultures and social norms on tax morale. In East Germany, the age group from 65 and above had the highest tax morale. Thus, this supports the assumption that elder people have a higher tax morale than younger people. In both East and West Germany, education had a negative impact on tax morale. Females were less than males. In East Germany, singles individual had lower tax morale than married people compared to West Germany and in East Germany, only self-employers had lower tax morale than full time employees.

Asia has different cultures such as Hinduism, Islam and Buddhism. Religion can have an impact on tax morale. Furnham (1981) found in an empirical analysis that “a higher degree of protestant work ethic leads to more opposition to taxation”. In India, Muslims and people with religion reports have generated higher tax morale than Hindus and people without religion has shown a significant reduction in tax morale. In japan, they found that an increase in the level of satisfaction has resulted in an increase in individuals’ perception that tax evasion is unjustifiable. Thus, trust in legal system and the satisfaction of the efficiency of tax administration has increased tax morale.

Spain has significantly lower tax morale than in the Unites States. Trust in the government and parliaments have an effect on tax morale. Moreover, socio- economic factors can also influence tax morale.

METHODOLOGY

The technique used for collecting the data was a self-developed questionnaire, containing items of diverse formats: multiple choice, dichotomous answers like “Yes” and “No”, self-assessment items measured on the 5-point Likert scale, and open-ended questions.

Respondents were chosen through the quota sampling method with regards to specific level of education, that is, those having at least secondary qualification. Moreover, sampling frame was divided into non-overlapping strata for example ethnicity, age, gender and employment which is named as stratified sampling technique. This technique helps to categorize the respondents faster as well as having approximately an equal number of individuals from each group. Also, this method allows each unit of the population to have equal chance of being chosen and in addition due to time and monetary constraints.

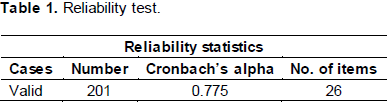

A sample size of 300 respondents was deemed to be sufficient for the survey due to time constraints. However, only 250 results were collected which represents approximately 93% response rate. The sampling population for this research is composed of Mauritians adults that are aged 18 years old or elder. The questionnaire was circulated to individuals having different age groups and diverse professional backgrounds. This study used cross-sectional survey design. Reliability test is use to know whether our survey on the analysis of tax morale is reliable or not.

As shown in Table 1, the Cronbach alpha coefficient of 0.775 is greater than 0.7, therefore we can say that survey questionnaire is reliable and that further analysis can be conducted. “Statistical Package for the Social Sciences” (SPSS 16.0) for windows and Stata was used to analyse collected data. Tables, bar charts and pie was used to illustrate the results.

DATA ANALYSIS

Data preliminary

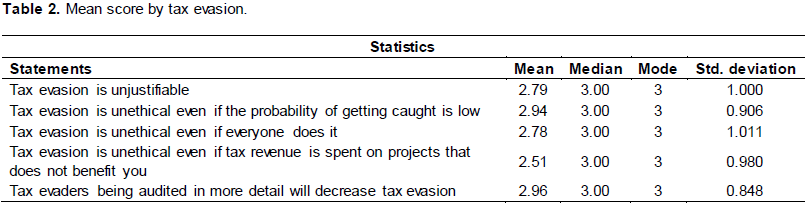

Table 2 shows the descriptive (mean, median. mode and standard deviations). At a mean value of 2.79, participants see tax evasion as unjustifiable. Furthermore, respondents seen to agree with the statements that tax evasion is unethical even if everyone does it or if the probability of getting is low or if tax revenue is not spent on projects that does not benefit them with mean score of 2.94, 2.78 and 2.51 respectively.

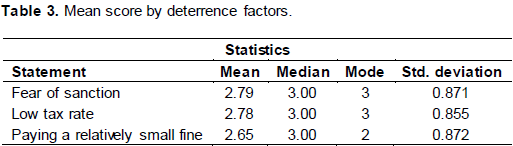

Table 3 shows the descriptive (mean, median. Mode and standard deviations) for deterrence factors. On 4 Likert scale, the mean value for all variables are more than half of the point scale (that is, 2). Most respondents said that the fear of sanction, low tax rate and paying a relatively small fine are factors that highly motivate them to pay their tax with mean score of 2.79, 2.78 and 2.65 respectively.

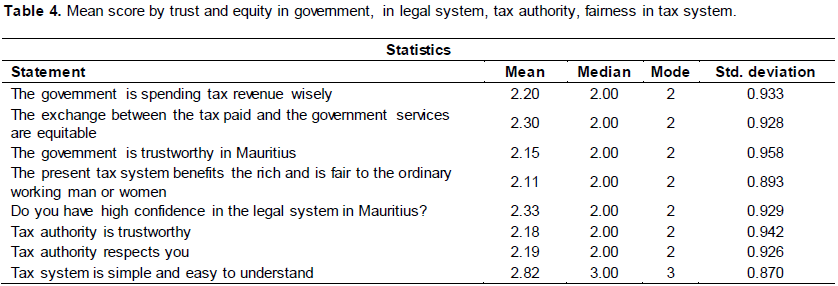

Table 4 shows the descriptive (mean, median. mode and standard deviations) for trust in government and tax authority, equity and fairness of tax system. On a 4 Likert scale, the mean value for all variables are more than half of the point scale. The mean score for trust in government, equity, fairness in tax system, confidence in legal system, trust in tax authority, respect by tax authority and complexity of tax system are 2.15, 2.30, 2.11, 2.33, 2.18, 2.19 and 2.82 respectively

Chi-square test

Tax evasion and tax morale

H0: There is no correlation between tax evasion and tax morale

H1: There is a correlation between tax evasion and tax morale

The p value of 0.000 is less than the significance level of

0.01, therefore we accept H1. It can be observed that there is a positive correlation, that is an increase in the perception that tax evasion is unjustifiable will result to an increase in tax morale.

Equity and tax morale

H0: There is no correlation between equity and tax morale

H1: There is a correlation between equity and tax morale

P- value of 0.000 is less than the significance level of 0.01, therefore H1 is accepted. We can conclude that there is a positive correlation between equity and tax morale.

Trust and tax morale

H0: There is no relationship between trust and tax morale H1: There is a relationship between trust and tax morale

We can accept H1 as the p- value of 0.000 is less than the significance level of 0.01. we can observe that there is a positive relationship between trust and tax morale.

Fairness in tax system and tax morale

H0: There is no correlation between fairness in tax system and tax morale

H1: There is a correlation between fairness in tax system and tax morale

The P-value of 0.000 is significant, therefore we reject H0. We can determine that there is a positive correlation between fairness in tax system and tax morale.

Confidence in legal system and tax morale

H0: There is no correlation between confidence in legal system and tax morale

H1: There is a correlation between confidence in legal system and tax morale

P-value of 0.000 is less than the significance level of

0.01, therefore we accept H1. We can conclude that an increase in confidence in legal system will result in an increase in tax morale.

Tax authority and tax morale

H0: There is no relationship between trust in tax authority and tax morale

H1: There is a relationship between trust in tax authority and tax morale

We can accept H1 as the p-value of 0.000 is significant. we can observe that there is a positive relationship between tax morale and trust in tax authority.

Factor analysis

Respondents were asked if they have a moral obligation to pay tax. The variables used for this factor analysis are age, gender, marital status, tax evasion, moral sentiments, social norms, civic duty, preferences, equity, trust in government, fair in tax system, confidence in legal system, trust in tax authority and respects. Stata was used to generate the iteartion principal factor analysis with 14 variables. The variance of the initial factor is the highest variance with an eigenvalue of the 3.42245. The consequent highest variance is 1.09258 and the variances will continue to decrease. Factor 8 has a negative eigenvalue which indicates that the matrix is not of full rank, which means that though there are 14 variables, the dimensionality of the measures is less. The difference is defined as changes between the eigenvalue. The proportion discloses the percentage of the variance which accounts for each factor and the cumulative combines the proportion of variance gathered.

Logistic regression analysis

Ln Pi 1−Pi = α +β1 (x1) +β2 (x2) + β3 (x3) +β4 (x4) +β5 (x5) +β6 (x6) + β7(x7) + β8(x8) + β9(x9) + β10(x10) + β11(x11) + β12(x12) + β13(x13) + β14(x14) + β15x15) + β16(x16) + ε

Dependent variable: Ln Pi 1−Pi is taken as Y and Y=1, indicates that people have a moral obligation to pay tax, 0 indicate that people do not have a moral obligation to pay tax.

Explanatory variables: x = hypothesized to influence probabilities of independent variables

ß = coefficients of the explanatory variables;

ε = stochastic disturbance term

1. X1 = Age

2. X2 = Gender

3. X3 = Marital status

4. X4 = Tax evasion is unjustifiable

5. X5 = Social norms

6. X6 = Civic duty

7. X7 = Government spending based on taxpayers’ preferences

8. X8 = Moral sentiment

9. X9 = Government spending is wise

10. X10 = Equity and fairness by the government

11. X11 = Complexity in tax system

12. X12 = Trust in government

13. X13 = Fair tax system

14. X14 = Confidence in legal and tax system

15. X15 = Trust in tax authority

16. X16 = Respect by the tax officer

ε = all other factors

Based on this, the logistic regression of attitudinal determinants used in the model is:

log(p/1-p) = b0 + b1*age + b2*gender + b3*Marital status + b4*Tax evasion +b5*social norms + b6*Civic duty +b7*Preferences+ b8*Moral sentiment+ b9*wise+ b10*Equity+ b11*complexity+ b12*trust+ b13*faire+ b14*confidence+ b15* tax authority+ b16*respect where p is the probability that taxpayers would not cheat even if they have a chance to.

Independent variables

Demographics

Demographic factors such as age, gender, religion, church attendance, income, marital status and employment has been analysed to determine whether those factors affect tax morale in Mauritius.

Morale sentiments and social norms

Respondents were asked, if a false income declaration will generate anxiety, guilt and shame and if they believe that tax payment is a social norm. They were also asked if paying their tax is a civic duty for them.

Attitude toward tax evasion

A range of independent variables has been examined to evaluate perception of tax evasion. In several studies, authors mentioned that tax evasion has a negative correlation with tax morale. Thus, the correlation between tax morale and tax evasion will be analysed in this study.

Attitude toward government

Individuals were asked if they trust the government and if they were equitable toward them. Perception of fairness toward government was also evaluated so as to know, if the government is wasting their money. Tax spending based on their preferences was also a concern for this study.

Attitude toward legal and tax system

Diverse independent variables have been used to evaluate the attitude toward tax system such as the perception of fair tax system, the level of confidence they have in the legal system, the level of complexity in the tax system and they were questioned if the tax rate is high or not

Attitude toward tax authority

Different variables such as respect and fairness have been used to examine the attitude toward tax authority. MRA is the legal tax institution in Mauritius. Trust in MRA will help in analysing tax morale among taxpayers.

Error term

Error terms are variables which are not included in the regression analysis but still have an influential effect on the decision of taxpayers. Those variables are factors that cannot be control due to their nature such as corruption, money laundering, black market, discrimination and so on.

Data analysis

Iteration 0: log pseudolikelihood = -106.88694

Iteration 1: log pseudolikelihood = -64.1757

Iteration 2: log pseudolikelihood = -52.936387

Iteration 3: log pseudolikelihood = -51.86815

Iteration 4: log pseudolikelihood = -51.857085

Iteration 5: log pseudolikelihood = -51.857078

Iteration 6: log pseudolikelihood = -51.857078

Logistic regression Number of obs = 201

Wald chi2 (16) = 47.15

Prob > chi2 = 0.0001

Log pseudolikelihood = -51.857078 Pseudo R2 = 0.5148

Robust

Significance Level at 1%: **

Significance Level at 5%: *

Expressed in terms of the variables used, the logistic regression equation is:

log(p/1-p) = -6.232957 –0.136597* age– 0.859374*gender + 0.1878442*marital status + 1.077683* tax evasion + 1.441351*social norms – 0.879632*moral sentiment – 0.5075426*civic duty –0.5075426*preferences – 0.4475051*wise + 0.82141*equity – 0.3642315*complexity + 0.9854554*trust + 0.8310607*fair + 1.17121*confidence + 0.793781*tax authority – 0.1759994*respects

Significant parameter estimates

The logistic regression model will help to analyse the degree of tax morale among taxpayers. The significant factor that influence tax morale are explained as follows:

Tax evasion: The variable “tax evasion “has been statistically significant at p-value 0.01 established whether participants consider tax evasion as unjustifiable. It is more likely shown that for a one-unit increase in the perception that tax evasion as unjustifiable, there will be

a 1.077683 increase in the log of the odds of tax morale. Thus, there is a negative correlation between tax evasion and tax morale.

Social norms: The variable “social norm” tested whether taxpayers believe that tax payment is a social norm. An increase in the belief that tax payment is a social by one unit, will have a 1.441351 positive effect in the log of the odds of the dependent variable. The most people believe that tax compliance is a social norm, the higher will be tax morale. Alm and Torgler, (2003) argued that “as long as people believe that tax compliance is a social norm”, individuals will have a positive attitude toward tax compliance. The p-value of 0.01 is significant considering all other factors constant.

Equitable: This independent variable has a significant relationship of 0.82141-unit which will result in a positive change in the log of the odds with the criterion variable assuming other factors remaining constant. The variable is significant with a p value of 0.022. The respondents were asked whether the exchange between the tax paid and government spending were equitable. Spicer and Lundtstedt (1978) argued that taxpayers will feel cheated if they feel that the tax revenues are not spent well. There is a direct relationship between equity and tax morale. Taxpayers are more willing to pay tax if the amount paid and government spending are equitable.

Trust on the government: This factor tests the trustworthy of the government. The positive coefficient of 0.9854554 demonstrates a positive relationship between trust on the government and tax morale. Respondents will not have the moral obligation to pay tax if they do not trust the government, tax evasion can be a self-defence for them. The value is significant at the p-value of 0.01 assuming all other predictors remaining constant. In Unites states and Spain, they found that trust has a positive impact on tax morale.

Fair tax system: The degree of fairness in the tax system was tested and for one-unit increase in the belief that tax system is fair, the log odds of tax morale will be increase by 0.8310607 for the p-value being significant at 0.05 level of significance considering all factor constant. There is a direct relationship between fairness and tax morale. The higher the fairness of tax system, the higher will be tax morale.

Confidence in the legal system: Respondents were asked to rate their confidence level in the legal system.

The parameter estimate for the factor confidence in the legal system describes that a one-unit increase in the predictor variable, will result in an increase in the log-odd of tax morale by 2.073314 for a significant p-value at 0.05 level of significance considering other predictors constant. There is a positive correlation between confidence in legal system and tax morale. The higher the confidence in the legal system, the higher will be tax morale.

Constant: The value -6.232957 is the expected value of the log-odds of TM when all of the predictor variables are equal to zero. The variable was expected to test other factors such as corruption, black marketing and other illegal activities.

However, other variables are moral sentiment and civic duty. Government spending based on taxpayers’ preferences, complexity of tax system, confidence in the legal system, and respect by tax authority was insignificant in the logistic regression.

Socio demographic and tax morale

Social psychologists have found that females have higher tax morale than males. In India, they found that females have higher tax morale than males. However, we have found that in Mauritius, females have a lower tax morale than males. Empirical analysis from Switzerland and the United States shows that married people have higher tax morale than non-married people. We have observed that our analysis is in line with previous empirical findings that is married people have a higher tax morale than single people. Tittle (1980) argued that elder people have a higher tax morale as they are subtle to sanction and they have developed greater social incentives overtime. We have that in Mauritius, older people have higher tax morale than the young people as said by Tittle (1980). Studies stated that educated person are in a better position to understand why it is important to comply with law and the benefit of tax contribution of tax to society.

However, they can be less compliant because they have a better knowledge of tax evasion and are aware of government wastage. Highly educated people have a higher tax morale as they are less likely to cheat even if they have a chance to. In Asian countries, they found that self-employers are less compliant than full- time employees. In India, they observed that part timer employees, retired people and students had higher tax morale and self –employers had a lower tax morale compared to full-time individuals. In Mauritius, part- time employees, self-employees, unemployed and retired have a higher tax morale than student and full- time employees. Furnham (1981) found in an empirical analysis that “a higher degree of protestant work ethic leads to more opposition to taxation”. We have found that people who attend religious services more frequently have a higher tax morale than those who attend religious services less frequently or never.

Perception of tax evasion

We have observed that taxpayers will pay their tax despite the fact that the probability of getting caught is low. The concept of reciprocal said that if many people does not pay tax; therefore, citizen will not feel oblige to pay tax. Thus tax morale will decrease if everyone perceives tax evasion justifiable. However, in Mauritius, we have observed that tax morale is high as a large amount of people perceived tax evasion as unjustifiable even if everyone evades tax. Tax morale is high even though government spending is not spent on project that benefit them. Government spending based on individual’s preferences can improve tax morale in Mauritius.

Motivational factors to pay tax

Deterrence factors

we can observe that in Mauritius, it seems that enforcement and sanction have an impact on tax compliance. The higher the fear of sanction, the higher will be tax compliance. A lower tax rate and a lower fine rate will motivate them to pay tax. However, a low tax rate, enforcement and fines is not considered as tax morale as people pay tax because people are afraid of sanctions and not because of a moral duty to pay tax.

Civic duty

Some taxpayers are not self-centred. They are also interested in the welfare of the general society. Tax payment can be a civic duty for some taxpayers. A sense of civic duty is developed when citizens are involved in political decision making and thus this will enhance tax morale. We can observe that the Mauritian society have a high tax morale as tax payment is a civic duty for them.

They contribute to the welfare of the society.

Government spending based on our preferences

42.3% citizens have a low level of motivation even if the government spending is based on their preferences and 57.5% are highly motivated to pay tax if government spending is based on their preferences. We can conclude that government spending based on individual’s preferences can improve tax morale in Mauritius.

Factors that will improve tax morale

Moral sentiment

Studies stated that a false declaration will generate anxiety, guilt or shame if caught. Grasmick and Bursick (1990) found that guilt and shame is a much greater restriction than sanctions. Respondents were asked if a false declaration will generate anxiety, guilty or shame if caught. The level of shame and guilt is high in Mauritius thus people will be less likely to evade. We can conclude that tax morale is high in Mauritius.

Positive action by the state

Smith (1992) and Stalams (1991) indicate that positive action and appropriate uses of tax revenue will increase tax morale. Results show that an increase in positive action by the state and a fair use of tax revenue will increase tax morale in the perspective of Mauritian.

Trust in government

Trust in the government is a statistically significant to tax morale. Participates were asked whether more trust in government will increase tax morale. We have concluded that trust in government will increase tax morale.

Fairness in tax system

Several studies have indicated that if taxpayers believe that tax system is unfair, the moral cost will decrease leading to a fall in tax morale. Participants were asked if fairness in tax system will increase tax morale. We can observe that in Mauritius, a fair tax system will increase tax morale

Respect

People were asked whether they would voluntarily pay their tax if tax authority respect them more. And we conclude that more respect by the tax authority will increase tax morale which is in line with Frey and Feld (2002) and Alm and Torgler (2006) who argued that tax morale will be higher if tax officer treat taxpayers with respect.

CONCLUSION

The assessment of tax morale has been an academic research in most countries. Tax compliance is important for the development of the economy. It can be seen that there is a direct relationship between tax morale and tax compliance.

In this study, we can determine that deterrence factors such as sanction, fines, tax rates and probability of detection influence tax compliance decision, however, we can conclude that the willingness of each individual to comply with the tax law is also a function of tax compliance.

The study empirical findings indicate that equity, social norms, attitude toward tax evasion, trust in government and authority, fairness in tax system and confidence in legal system have a significant impact on tax morale. It can be concluded that tax morale will increase if trust, equity, fairness and social norms increase. Moreover, a rise in tax evasion will fall in tax morale. Some of our result is in line with previous empirical finding

In Mauritius, it can be said that the population thinks that the government is not trustworthy and that it does not spend tax revenues wisely. They also do not think that the MRA can be trusted and it is also true that the MRA does not respect the people. Moreover, the population perceives the Mauritian tax system as unfair. It has also been found that the exchange between the performed government services and tax paid were not equitable. Mauritius is highly corrupted therefore; the population does not trust the government.

RECOMMENDATION

Based on the findings in this study, we hereby make recommendation that will increase tax morale as it has been concluded that not only deterrence increase tax compliance but tax morale also can increase tax compliance. Government should take tax morale into consideration as this study has proved that tax morale has an effect on tax compliance. Policies should be developed to increase tax morale.

1. Most participants have agreed with the statement that tax evaders being audited in a more detailed manner will decrease tax evasion. The government can increase audit rate in order to decrease tax evasion. Moreover, deterrence factors have proved to be an effective way to increase tax compliance therefore, the government can implement more deterrence policy to increase tax compliance.

2. It is imperative to educate young people on the important of the role of taxes and their contribution to the welfare of the population. Future taxpayers should know about their rights and duties with regards to tax.

3. If individuals believe that there is corruption in public institution and among tax officials, the willingness to pay taxes will decrease, thus lowering tax morale. Most participants have stated that tax system is not simple and it is difficult to understand. (appendix) Simplifying tax system and increase the transparency of tax policy can positively influence attitudes of individuals towards taxes. This is a way to improve tax morale.

4. Continuous training is needed in order to improve the efficiency and help in carrying their work in a professional manner. This will help in increasing population’s trust towards them which will result in an increase in tax morale.

5. Government should introduce policies that make people believe that tax payment is a social norm. A positive attitude toward tax payment will help in improving tax compliance and this can be done by trying to sensitize people and by a reduction in government wastage. Government should spend tax revenues on activities such as health and safety, education, infrastructures and road. Moreover, they should create employment and reduce inequality distribution in income and wealth. This will result in an increase in trust in the government leading to an improvement in tax morale.

LIMITATION OF STUDY

It was time consuming to collect and analyse responses. It was costly. Some people do not have a good knowledge on taxation therefore, they do not understand the questions properly so there is biased in responses. Responds from age group above 60 was difficult to obtain because it was an online survey. They are not updated with new technology. The answers might be biased.

People were asked if they would cheat if they had a chance to. This question might be sensitive in nature that might discourage them from participating in the survey. Furthermore, a high level of honesty might be observed in the survey as people are afraid of legal actions even though they were assured than all information was strictly confidential.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Alm J, McClelland GH, Schulze WD (1999). Changing the social norm of tax compliance by voting. Kyklos 52:141-171. |

|

|

Alm J, Torgler B (July 2003). Culture Differences and Tax Morale in the United States and in Europe" CREMA Working Paper No. 2004-14. |

|

|

Alm J, Torgler B (2006). Culture differences and tax morale in the United States and in Europe. J. Economic Psychol. 27(2):224-246. |

|

|

Erard B, Feinstein JS (1994). Honesty and Evasion in the Tax Compliance Game, RAND J. Econ. The RAND Corporation. 25(1):1-19, Spring. |

|

|

Feld LP, Frey BS (2002b) Trust breeds trust: How taxpayers are treated". Forthcoming in: Economics of Governance P 3. |

|

|

Furnham A (1981). The protestant work ethic, human values and attitudes towards taxation, J. Econ. Psychol. 3:113-128. |

|

|

Grasmick HG, Bursik RJ (1990). Conscience, Significant Others and Rational Choice. Law. Soc. Rev. 34:837-861. |

|

|

Pommerehne WW, Frey BS (1992). The Effects of Tax Administration on Tax Morale, Discussion Paper Series II:191, University of Konstanz. |

|

|

Pommerehne WW, Hart A, Frey BS (1994). Tax morale, tax evasion and the choice of policy instruments in different political systems, Public Finance 49:52-69. |

|

|

Scholz JT, Pinney N (1995). Duty, Fear, and Tax Compliance: The Heuristic Basis of Citizenship Behavior. Am. J. Polit. Sci. 39:490-512. |

|

|

Smith KW (1992). "Reciprocity and Fairness: Positive Incentives for Tax Compliance", in: J.Slemrod (ed.), Why People Pay Taxes. Tax Compliance and Enforcement. Ann Arbor: University of Michigan Press: pp. 223-258. |

|

|

Smith KW, Stalans LJ (1991). Encouraging tax compliance with positive incentives: a conceptual framework and research directions". Law Soc. Rev. 13:35:53. |

|

|

Song YD, Yarbrough TE (1978). Tax ethics and taxpayer attitudes: A survey. Public Adm. Rev. 38(5):442-452. |

|

|

Spicer M (1974). A behavioral model of income tax evasion. Unpublished Ph.D. thesis, Ohio State University. |

|

|

Spicer MW Lundstedt SB (1976). Understanding tax evasion", Public Finance 31(2):295-305. |

|

|

Thibaut J, Friedland N, Walker L (1974). Compliance with rules: Some social determinants. J. Personal. Soc. Psychol. 30:792-801. |

|

|

Torgler B (2002). Speaking to Theorists and Searching for facts: Tax Morale and Tax Compliance in Experiments. J. Econ. Surv. pp. 658-670. |

|

|

Torgler B (2003). Tax morale: Theory and Empirical Analysis of tax compliance, der Universität Basel zur Erlangung der Würde eines Doktors der Staatswissenschaften, pp.80-94, 432-446, 540-557. |

|

|

Torgler B (2004b). Tax morale in Asian countries. J. Asian. Econ. pp. 238 -261. |

|

|

Torgler B, Schneider F (2009). The impact of tax morale and institutional quality on the shadow economy.J. Econ. Psychol. 30(2):228-245. |

|

|

Torgler B (2002). Speaking to Theorists and Searching for facts: Tax Morale and Tax Compliance in Experiments, J. Econ. Survey, pp. 658-670. |

|

|

Torgler B (2001a). What Do We Know about Tax Morale and Tax Compliance?" International Review of Economics and Business (RISEC) 48:395-419. |

|

|

Torgler B (2003). Tax morale: Theory and Empirical Analysis of tax compliance, der Universität Basel zur Erlangung der Würde eines Doktors der Staatswissenschaften, pp.80-94, 432-446, 540-557 |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0