ABSTRACT

This study examines the impact of intellectual capital (IC) on financial performance of listed Nigerian food products companies for five year period 2010 to 2014 by adopting Pulic model of IC known as value added intellectual coefficient (VAIC). Regression models are used to test the hypotheses of the study where the results show that there was positive significant influence of IC on financial performance. Specifically, the results showed that structural capital (SC) and capital employed (CE) influence the financial performance of Nigerian food products companies. Based on the resource-based theory, the results prove that companies can enhance financial performance by emphasising on IC especially in food products companies.

Key words: Intellectual capital, VAIC, financial performance, Nigeria.

The word “capital” has been in existence since the middle ages. It has been used by many renowned economists, who always refer to it as special meaning in their theories. However, no layperson has any real trouble knowing basically what the word stands for. In every speech, capital and money are interchangeable (Hudson, 1993). Fathi et al. (2013) opines that, in business language denotes any means that will deliver future cash flows. The most surely understood resource sorts are tangible in nature. Tangible capital refers to the touchable assets both financial and non-financial of the organizations. Currently, intangible assets are other types of assets besides tangible (Berry, 2004). This includes the aptitudes of the workforce and its association, which are progressively getting to be important towards deciding future profits as economies of the world are transforming from manufacturing base towards knowledge-based economic activity.

Drucker (1993) indicates that knowledge-based economic activity is the superior to land, labour and capital. Scholarly capital or known as intellectual capital (IC) is recognized as a strategic asset which gives competitive advantages by driving associations for superior performance in the current learning based economies (Kalkan, Bozkurt and Arman, 2014). Roos and Roos (1997) viewed IC as “the sum of the knowledge of its members and the practical translation of this knowledge into brands, trademarks, and processes” IC as defined by Bontis (1998a) and Choudhury (2010) is the total knowledge that is surrounded in the personnel, organizational routines and network relationships of an organization. It contains three components: human capital (HC) structural capital (SC) and capital employed (CE) (Mariya and Shakina, 2014).

HC is the generic term for the competences, skills, trainings and motivation of the employees (Anuonye, 2015). Then SC comprises of all the non-human storehouses of knowledge in organisations including databases, organisational charts, process manuals, strategies, routines and anything that has a higher value than its material value to the company (Bontis, 2000a), while CE on the other word comprises of all the financial and non-financial assets of the organization (Kamath, 2007). The definition of IC has been introduced by Kalkan et al. (2014) to include knowledge, information and experience. Durham and Kennedy (1997) defines IC as the relationship of the firm’s market value and the book value. Pulic (1998) opines that IC includes three items:

1. Human capital, which consists of knowledge, training and competence.

2. Structural capital which consists of the routines, procedures, systems, culture and database and

3. Capital employed which speaks of the value of the assets that add to an organization's capacity to create income furthermore known as operating assets.

Pulic (1998) has introduced an efficiency model that monitors and measure the value creation known as value added intellectual coefficient (VAIC). In Nigeria, research on IC and financial performance is skewed to other industries of the economy especially banks with little focus on the food product companies despite its contribution to the Nigerian economy. For example, Honeywell Flour Mills Plc., a market leader in the Nigerian food industry, posted N1.4bn as profit before tax (PBT) and N1.1bn as profit after tax (PAT) where N3.14million goes to government account as tax for the financial year ended 31 March 2015 (Thisday, 2015).

Similarly, on 31 March, 2015 Flour Mills of Nigeria Plc. (FMN) posted a profit after tax (PAT) of N8.5 billion at a growth rate of 58% compared with N5.37 billion in 2014 respectively, where Nigerian economy received over N3bn as revenue from only two out of twelve companies under food products sub-sector (Business Day, 2015). Hence, food products companies are very important to the Nigerian economy. Food products companies are a sub-sector under consumer goods industry with market capitalization of N244,493b (Nigerian stock exchange, 2013). Interestingly, foreign investors recently picked interest in food products companies in Nigeria where Kellogg Company, an American multinational food manufacturing organization headquartered in Battle Creek, Michigan, United States will invest $450 million (N89, 659, 327, 003.63) (Thisday, 2015). Thus, at the end of 2015, market capitalization of food products companies in Nigeria will rise up to N334, 152, 327, 003 .63 ($1, 677, 109, 924.64). Thus, there is need for empirical studies on food product companies in Nigeria more particularly on IC due to the current knowledge-based contribution in the economies.

In this modern world of economy, the power of globalization has come into existence so speedily due to the fact that information and communication technology (ICT) and knowledge become the most precious assets of the firms. Transformation into modern world of technology has necessitated for the urgent need to look and find out intellectual means in a company’s financial reports (Salman et al., 2012). Therefore, IC has been recognized as the bedrock for achievement of organizational goals (Pulic, 1998). An extensive recognition of IC as a medium of competitive advantage resulted in the new strategies of monitoring the activities need in the company to achieve a maximum productivity from IC (Salman et al., 2012; Maditinos et al., 2011; Makki and Lodhi, 2008).

Hence, old-fashioned accounting and measurement systems seem to be inappropriate and imbalanced in the new economic world where competitive advantage is driven by ICT and IC. This is because, old fashioned accounting does not reflect the true picture about the company and may mislead investors and other relevant stakeholders to make appropriate choices when making economic decisions (Brooking, 1996). Due to the knowledge-based economy, all companies around the world depend heavily on IC to achieve a concept of going concern and increase their productivity (Ahangar, 2011).

Prior studies on food products companies in other areas other than IC are many, for example Broring and Cloutier (2008) analyse value-creation in the functional foods and nutraceutical industry in Canada. Likewise, the study of Nezakati et al. (2011) examines the Market Value Coverage in Fast Food Products Industries. In Nigeria, Ademola and Kemisola (2014) studied the effect of working capital management on market value of quoted food products and beverages manufacturing companies. However, the study related to IC in food products companies is limited. Therefore, this study attempt to fill the aforementioned lacunas which aims at examining the impact of IC components on financial performance of listed Nigerian food products companies ranging from the 2010 to 2014 periods by using VAIC model.

It is also pertinent to carry out an empirical study to examine IC components to test any effect of IC components on financial performance of food products firms in Nigeria. This is because, it will stimulate the food products companies in Nigeria to be ready and able to face the new challenges posed by ICT, liberalization and globalization that translated into the increasing entering of foreign food products companies. Finally, the study reveals that IC has a positive and significant influence on the financial performance of food products companies, where both SC and CE as components of IC has a positive and significant influence on the financial performance of foods products companies in Nigeria.

Professor Inman is the first person that used IC at Western Ontario University in 1956 (Hudson, 1993). IC stands as knowledge resources that organization use to attain its goals. Therefore, the success or otherwise of the organization depends on creating, discovering, capturing, disseminating and measuring knowledge. In other word, organizations should increase the productivity of their organizational learning. This is because learning is an ongoing, never-ending and always changing process based on the changing of the market. It is the foundation of adaptability and innovation and in the last two and half decades, the importance of IC has been understood tremendously specifically in developing and developed countries (Salman and Dandago, 2013). Fathi et al. (2013) and Akpinar & Akdemir, (2002) maintain that IC in the millennium as fewer people will do physical work and more people will do intelligence work. Garcia-Ayuso (2003) taken together the research efforts led in the course of recent decades gave convincing evidence that:

1. IC are fundamental sources of competitive advantages that must be recognized, measured and controlled keeping in mind the end goal to guarantee the proficient management of corporation.

2. There is a consistent relationship between most IC investments and subsequent earnings and worth creation in business enterprise

3. IC is nowadays the principal drivers of growth and competitiveness in our social orders and their measurement is essential for the configuration and implementation of public policies

Prior literature has used VAIC in order to evaluate the relationship between IC and firm performance. For example, Berzkalne and Zelgalve (2014) examine the influence of IC on company performance, where the mixed results were detected. Almost all the prior studies on IC over the last two decades for example (Anuonye, 2015; Lina, 2014;

Sledzik, 2013; Kamal et al., 2011, Zeghal and Maaloul, 2010) are mostly concentrated on banking and financial sectors and neglect other sectors, food product companies inclusive. Still they do not reach any agreement on the role of firm’s performance. This is because of the inconsistent results in studies conducted in different countries. It is clear from the literature that, IC is an asset of the organization and an increase in IC ought to increase the worth and profitability of the organization also. The mixed and inconclusive results in the subject of IC and its impact on firms performance is topical and requires more research especially in food products companies due to scarce empirical studies in this sector. Also Kujansivu & Lonnqvist, (2007) do not find clear evidence of the relationship between IC and company performance of Finland companies

It is noted that, companies in Nigeria, still use traditional accounting models in the measurement and reporting systems. This is because, most of the reported IC drivers are expressed in narrative and qualitative instead of in quantitative or fiscal terms with this style, financial performance will never be measured and reported genuinely to concerned parties (Salman and Dandago, 2013). VAIC was developed by Pulic (1998), which monitors and measures the value creation efficiency in the company according to accounting-based figures. The VAIC model is intended to measure the extent to which a company produces added value based on intellectual (capital) resources (Stahle et al., 2011). A simple computation of VAIC model is as follows:

1. HC is interpreted as employee expenses and HC is calculated by dividing added value (VA) with HC: HC = VA/HC.

2. SC is the difference between produced VA and HC or VAHC is calculated by dividing SC with VA: VA-HC/VA

3. CE is interpreted as financial capital and is calculated by dividing VA with CE: VA/CE, thus:

It has been revealed that a significant number of the associations between IC and firm performance are conducted via VAIC. Among these studies include the study of Fathi et al. (2013) where the relationship between IC and financial performance in Tehran Stock Exchange for the period of ten years were examined. The study found mixed associations between IC components and firm performance where there is significant positive relationship between SC with return on assets (ROA), return on equity (ROE), and growth revenues (GR). Similarly, the study found a significant positive relationship between HC, CE with ROA and ROE, but no significant relationship between HC, CE with GR.

In the same vein, Berzkalne and Zelgalve (2014) examined the impact of IC on company value for three different countries which included Estonia, Latvia and Lithuania by using Tobin’s Q method from the period of 2005 to 2011. The results were mixed regarding relationship between VAIC and company value for the three countries. This is because the results showed that there was positive relationship between CE, HC with company value in Latvia and Lithuania while no significant relationship between SC and company value in the two countries. In the case of Estonia, there was no significant correlation between VAIC, its components and company value. Also, Abdulsalam et al. (2011) measured the IC efficiency of the Kuwaiti Banks (commercial and non-commercial) from the periods of 1997 to 2006, where value added stood as dependent variables while CE and HC are independent variables.

The result showed a mixed relationship between IC components and performance of Kuwaiti Banks. The results showed a significant relationship between VA and CE while a negative relationship between VA and HC was noticed. Additionally, Lina (2014) in her study associated the IC components towards the company performance, where the listed companies in Indonesian Stock Exchange were examined between the periods of 2009 to 2011. Result showed that HC and SC had no influence towards company performance while CE had a significant a relationship with company performance. Thus, the study found mixed result too. However, the study of Mehri et al. (2013) on the relationship between IC and financial performance industries in Malaysia, reported a positive significant relationship. In the same vein, the study of Dadashinasab and Sofian (2014) investigated the effect of IC on high IC firm financial performance with moderating role of dynamic capability for the periods of 2000 to 2011.

The study proved that there is positive and significant relationship between HC, SC and CE with firm financial performance. Additionally, in Pakistan, Amin , Aslam and Makki (2014) associated IC and financial performance of pharmaceutical firms. The results of the study showed significant positive impact of IC on financial performance. Conversely, Salman et al. (2012) examined the influence of IC components on financial performance of Nigerian manufacturing sector and found a positive result between IC and ROA as financial performance. Similarly, Khan et al. (2012) studied the impact of intellectual capital on financial performance of banks in Pakistan. The results showed that intellectual capital has significant effect on the financial performance of banks. In line with this, Khan et al. (2012) and Tseng and Goo (2005) examined the IC and corporate value of Taiwanese manufacturing firms. The outcome of the study showed a positive relationship between IC and corporate value.

Similarly, the study of Maditinos et al. (2011) and Laing et al. (2010) in Athens and Australia on empirical relation of IC efficiency based on HC efficiency showed a significant and positive relation with financial performance. A study by Al-Shubiri (2013) on the impact of value added intellectual coefficient components on financial health in Jordanian industrial sector from 2005 to 2011 indicated a significant impact of human, employed element and IC as a whole on financial health as productivity and profitability. Unlike the study of Najibullah (2005) that investigated the value creation efficiency of IC with market valuation and financial performance of 22 Bangladesh Banks listed on Dhaka Stock Exchange. The result proved mixed. This is because, on market valuation where Market to book value (M/B) served as dependent variables, results showed that VAIC is significantly related with M/B.

In the same vein, HC and CE are significantly related with M/B. But SC is not significantly related with M/B. For dependent variable financial performance, which consider ROE, ROA, GR, and EP found in the correlation analysis, value VAIC was not significantly related with the dependent variables of financial performance except GR while HC, CE and SC on the financial performance of the banks, it showed that CE were significantly related with ROE and ROA. The other two components (HC and SC) were found not to be significantly related with ROE and ROA. However, HC was found to be significantly related with GR, and SC was found to be significantly related with EP. Similarly, Yusuf (2013) conducted an empirical research on the association between HC and financial performance in Nigerian banks. The study found that efficient utilization of HC did not have any significant impact on the ROE of banks.

Likewise, the study of Djamil et al. (2013) related IC with firm’s stock return of listed companies in Indonesia. The results still revealed that IC did not affect the current stock return. But it however, contributed to stock growth. Firer and Williams (2003) revealed absences of relationship among IC and financial performance in South African companies. But Makki and Lodhi (2008) revealed the presence of positive relationship among IC and firms’ productivity. Again, Chen et al. (2005) in Taiwan determined positive impact on market value and financial performance. Unlike the study by Musibah and Alfattani (2013) that examined and ascertained the effects of IC on corporate social responsibility (CSR) for Islamic Banks sector for the period of five years, 2007 to 2011, which showed negative influence of IC on CSR of Islamic Banks.

Additionally, Sledzik (2013) investigated the influence of IC performance of Polish banks through the application of VAIC model where 20 banks were observed from 2005 to 2009.

The study, due to the financial crisis, observed a significant decrease of the VAIC ratio in the banking sector in Polish. Al-Musali and Ismail (2014) examined the impact of IC on financial performance during 2008 to 2010 of listed banks in Saudi Arabia via VAIC model. The results showed a positive association between IC and performance of Saudi banks. Additionally, Anuonye (2015) determined the impact of IC on quoted insurance companies in Nigeria by using earnings per share model (EPS). The study concluded that IC had a positive association with EPS. Arslan and Zaman (2014) determined the relationship between IC firms’ financial returns of oil sector in Pakistan from 2007 to 2011, and found positive relationship between IC components and ROI, ROE and EPS as financial performance. Equally, Rehman et al. (2012) determined IC with corporate performance of Pakistan banking sector where the results showed a positive association.

Similarly, Deep and Narwal (2014) analysed IC with financial performance of Indian textile for 10 years ranging from 2002 to 2012. The result showed a positive association between IC and financial performance. In the same vein, recently, Bharathi (2015) found a positive association between IC and market value of Indian firms from 2008 to 2013. Despite this, there are number of empirical studies conducted in the area of IC around the world over the past two decades, in various industries across the economies. However, the agreements are yet to be reached on the significance of IC on firm’s performance. This is because of the diverse and inconsistent evidences in studies carried out from different economies. In addition, it is seems from the literature that IC is an asset of the company and an increase in IC should increase the value of the company as well. The mixed and inconclusive results on IC and its impact on firm’s performance therefore, are topical and require more research.

Hypothesis development

Intellectual capital and financial performance

Financial performance in relation to IC connotes notable actions or achievements which accrue to an enterprise as a result of IC measurement and application (Anuonye, 2015). The traditional monetary bookkeeping is unable to look at the real value of the firm where it only measures physical assets (Lina, 2014). Prior studies keep up that IC makes value for the organization (Fathi et al., 2013). For instance, the investigation of Gan and Saleh (2008) examined the relationship in the middle of IC and firm execution, and they found that IC significantly affected profitability and productivity of the firm. In the same vein, the study of Al-Musali and Ismail (2014) proved an IC and its consequence on financial performance of Saudi Arabian banks where they revealed that IC was positively connected with banks’ financial performance. Additionally, Chen et al. (2005) found that IC had a significant influence on profitability. Therefore, based on the findings of the previous studies, it is hypothesized that:

H1: Intellectual capital influences the companies’ financial performance.

Structural capital

Muhammad & Ismail, (2009) opined that structural capital as a competitive intelligence, formulas, information system, patents, policies and others which resulted from products or systems the company has created over a period of time Bontis (2000) conducted a study on IC and business performance, and revealed that IC had a positive association with business execution regardless of industry. Maditinos et al. (2010) carried out another study to confirm findings of Bontis (2000), the findings revealed a positive relationship of structural capital and firm performance. In his study, Appuhami (2007) found a positive relation between structural capital and firm performance. Hence, in the light of the aforementioned findings, the following hypothesis is derived:

H2: Structural capital influences the companies’ financial performance

Capital employed

Capital utilized is regarded as the strongest predictor of execution (Choudhury, 2010). Accordingly, Lina (2014) opined that a strong linkage between capital utilized backings that information tied up in relationship among representatives, customers, suppliers, cooperation accomplices and so forth tends to prompt process and create developments, better critical thinking which tends to increase generation and administration conveyance effectiveness and in addition customer satisfaction. Appuhami and Bhuyan (2015) also established a positive relationship between capital employed and capital gains on shares of listed companies in Thailand stock market. Also, Khalique et al. (2011) conducted a research on the relationship of IC with the organisational performance of commercial banks in Islamabad, Pakistan. The results showed that relational capital (or capital employed) has positive relationship with organisational performance. Though many studies found the relationship between capital employed and business performance but the result is mixed and inconclusive. This component of IC still makes up a reasonable linkage with business performance. Thus, the hypothesis related to capital employed is formulated as follows:

H3: Capital Employed influences the companies’ financial performance.

Population and sample size

The population of this study comprises of all the Nigerian food product companies under consumer goods companies quoted on the Nigerian Stock Exchange (NSE) as at 2013 fact book. Availability and accuracy of the data is very crucial for studies of this nature. Therefore, the study came up with some filters in order to generate accurate analysis. Firstly, only those firms which have been in operation for at least five years after being listed in the Nigerian Stock Exchange as at 31 December, 2014 will be selected. Secondly, annual reports of the company with relevant data to the study must be available at the Nigerian Stock Exchange. Firms that did not meet any of these criteria were excluded. This is in line with the study of Kurawa and Kabara (2014). Upon applying the two filters, six companies qualified as the working population of the study which also serves as sample size.

Data collection

Data was collected from the period of 2010 to 2014 fiscal year financial statement of the sampled firms. The sample of the data was generated only from the Nigeria food products companies. As explained earlier, this study adopts VAIC Model developed by Pulic (1998). The model has been used by many researchers as it provides relatively unique estimation of the measurement of IC with examples drawn from Berzkalne and Zelgalve (2014), Musibah and Alfattani (2013) and Yusuf (2013). The study utilized secondary source of data. The hypotheses tested in this study using secondary data from the sample size of the firm’s annual reports. Five years (2010 to 2014) data of the sampled companies were gathered from the Thomson Routers Data Stream and their annual reports. This is because the periods are the recent periods that would provide an up-to-date information about the impact of IC on financial performance of food products companies in Nigeria. The data collected that are relevant to the study includes total sales, total assets, total salaries, total expenses, net income, total debts and total intangible assets.

Measures of variables

Measurement of a variable is essentially the process of assigning numbers to that variable of the study (Lee Abbott and McKinney, 2012). In scientific research, variables must be measured (Graziano and Micheal, 1993). Thus, measurement of the variables in the theoretical framework is a part and parcel of scientific research and a crucial aspect of research design (Sekaran and Roger, 2013). Leedy and Ormrod (2010) opined that unless the variables are measured in some means the researcher will not be able to test the hypotheses and eventually to find answers to research questions. In this study, financial performance which is measured by ROA is the dependent variable that reflects the efficiency of firm in utilizing total assets, and holding constant firm’s financial policy. It also provides information about the value added to the company that leads to better performance of that company.

Prior studies like Lina (2014), Salman et al. (2012) and Dadashinasab and Sofian (2014) used ROA as a measure of financial performance while other studies like Bharathi (2015), Fathi et al. (2013), Djamil et al. (2013) and Chan (2011) used ROA in addition to other measures such as ROE, M/B and GR for determining financial performance. ROA = Net income/ Total Assets.In this study IC components are independent variables which includes human, structural and capital employed (Sekeran and Roger, 2013). The current study adopts VAIC technique developed by Pulic (1998). This is because, VAIC technique is distinctive due to easy availability of audited financial data and it is also less criticized model compared to other models as well as the most recent model among them. Additionally, VAIC has been adopted in several studies to examine the relationship between IC and firms performance (Clarke et al., 2011; Maditinos et al., 2011; Anne-Laure and Nick, 2013).

Applying firm size as the control variable in this study is stimulated by the way that it has been discovered to be connected with organizations with distinguishing attributes. The firms’ size has an influence of IC on organization performance (Nimtrakoon, 2015; Ong et al., 2011; Chan, 2011). Prior studies that measured the sizes of the characteristic logarithm of sales and size measured by common logarithm of total assets of the organization include Iavorskyi (2013), Pouraghajan and Malekian (2012) and Chinaemerem and Anthony (2012). Leverage as a debt proportion is characterized by whole of long-term debt of the firm or degree of risk (liabilities) as a rate of aggregate assets. It asserts that the debt proportion has an influence on all the financial performance of the firm.

Research model

In line with the prior studies carried out by Asare et al. (2013) and Ahangar (2011), the current study developed two models. The first model is to associate VAIC with ROA while the second model associates SC and CE with ROA individually. Therefore, the regression equations of this study are as follows:

Where:

ROA = Return on assets,

VAIC = Value added intellectual capital, VASC= value added structural capital, VACE = value added Capital employed, SIZE = Size of the firm,

LEV = leverage,

i = firm =1-6

t = period t = 2010-2014

β = Beta

Ô = error term

Data analysis and results

From the onset, descriptive statistics have been adopted to represent the general condition of the designated variables for this study. Diagnostic tests have also been carried out. These include normality and multi-collinearity test. Under multi-collinearity test, correlation and variance inflation factor were assessed to determine the level of associations between the independent variables of the study. Consequently, multiple regression has been employed to examine the influence of IC, SC and CE on companies’ financial performance.

Descriptive statistics

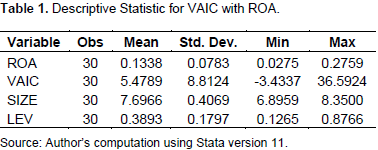

Descriptive statistics merely presents the statistical attributes of the variables in the model of the study is represented in Table 1. From Table 1 ROA show a mean value of 0.1338 and maximum of 28%, this implies that on average shareholders of food product companies earned 13% ROA. The standard deviation of 0.0783 indicates insignificant dispersion among the companies. For VAIC the mean value is 5.4789, the minimum value is -3.4337 and the maximum value is 36.5924. The value of standard deviation of VAIC is 8.8124. This implies that on average shareholders of food product companies earned less than 3% ROA. For ROA, the mean value is 0.1338 which indicates that ROA is low to minimum value of 0.0275 and the maximum is 0.2759, where standard deviation is 0.0783 for the overall firms in this study. The mean value of size of the study measured by the natural logarithm of total assets was 7.6966 and its minimum value was 6.8959 while the maximum value is 8.3500. The standard deviation is 0.4069, which suggests a relatively high level of dispersion in the total assets among the sampled firms.

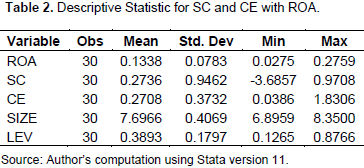

While for leverage, it has a minimum value of 0.1265 and maximum value is 0.8766 while standard deviation is 0.1797 (Table 2). Table 2 presents the descriptive results of variables in model 2. The results reveal that the mean value of SC is 0.2736; this means that SC tends to be very low because the minimum value is -3.6857 and the maximum is 0.9708 while its standard deviation is 0.9462. The mean value of CE is 0.2708 while the minimum value is 0.3857 and maximum value is 1.8306. The standard deviation is low that is, 0.3732. For ROA, the mean value is 0.1338 which indicates that ROA is low to minimum value of 0.0275 and the maximum is 0.2759, while standard deviation is 0.0783 for the overall firms in this study. The mean value of size was 7.6966 and its minimum value was 6.8959 while the maximum value 8.3500. The standard deviation is 0.4069. For leverage, it has a minimum value of 0.1265 and maximum value is 0.8766 while standard deviation is 0.1797.

Diagnostic test

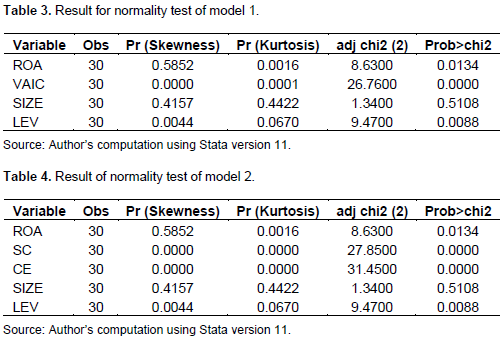

Before analysing the data, the assumption of psychometric characteristic was confirmed. Thus, to ensure the trustworthiness and quality of the generated data for the study and before running the data for multiple regression analysis, there are number of key expectations related with the multiple regression analysis. Hair et al. (2006) reveals that there are number of assumptions that need to be met to ensure that a model in which the actual errors in prediction are as a result of the real absence of a relationship or an association among the variables of the study which is caused by some peculiarities of the data not accommodated by the regression procedure. Thus, normality and multi-collinearity tests are considered for this study. This is in line with the study of Kurawa and Kabara (2014). As the name implies, normality, being the fundamental postulation in data analysis, refers to the shape of the data distribution for an individual metric variable and its correspondence to the normal distribution (Almusali, 2009; Hair et al., 2006). Based on the guidelines projected by Kline (2005) of severe non-normality “skewness > 3; kurtosis > 10”, values in Table 3 for model 1 and Table 4 for model 2 dropped within the cut-off point and could be regarded as normal for further analyses of the study.

Multi-collinearity test

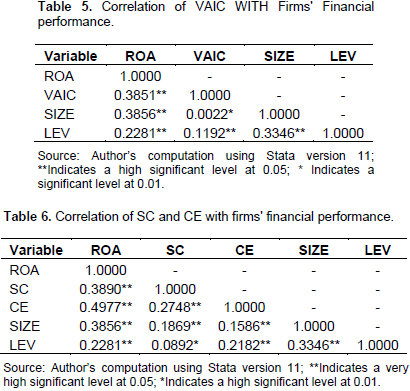

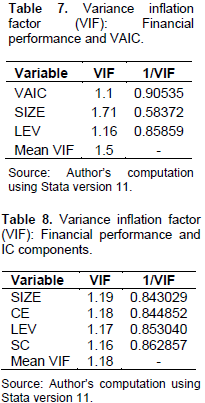

After observing the normality of the data, there is a need to diagnose whether the independent variables of the study are correlated with each other; such association among the variables is termed as multi-collinearity. Najibullah (2005) stated that multi-collinearity is the degree in which a variable can be described by the other variables of the same study. Multi-collinearity is the problem which affects the data of the study negatively therefore, it is crucial to prevent the data by detecting and correcting multi-collinearity problem before analysing the data (Hair et al., 2006). As mentioned earlier, in order to check the multi-collinearity, the study applied correlation coefficient and variance inflation factor (VIF) diagnostic tests. Correlation analysis is the first analysis carried out in order to examine whether any association exists between the independent variables of the study in question. Hair et al. (2006) projected that a threshold value of 0.9 and high among the independent variables as collinearity. Based on this projection, Table 5 and Table 6 for model 1 and 2 respectively indicate vividly that multi-collinearity is not a problem for the data of this study.

As shown in Table 5 of model 1, the values of VAIC, SIZE and LEV against each other does not exceed 0.9 while Table 6 of model 2 the values of SC, CE, SIZE and LEV against each other are all less than 0.9. Absence of multi-collinearity of correlation analysis is not a surety that the data of the study is free from multi-collinearity totally (Hair et al., 2006). Therefore, the study again applied VIF analysis to examine the existence of multi-collinearity in the data. Kline (2005) mentioned that VIF value of less than 10 indicates an absence of multi- collinearity. Thus, the values appear in Tables 7 and 8 for both model 1 and model 2 indicating non-existence of multi-collinearity whereby the value for VAIC, SIZE and LEV in Table 7 of model 1 are less than 10. Likewise, the VIF values for all variables in Table 8 of model 2 are also less than 10. Therefore, the data can be considered appropriate for analysis.

Regression analysis

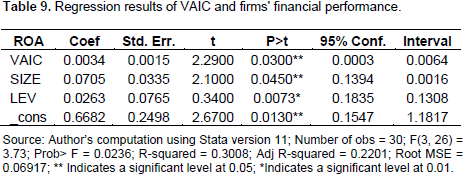

Hair et al. (2006) opined that regression analysis is a linear combination of weighted independent variables collectively used in the study to project the weight of dependent variable. In presenting the results of the regression analysis, the explanatory power (R square) of the regression models and the standardised regression coefficients (β) are presented. The study regresses the dependent variable (ROA) with the overall independent variable (VAIC), and then associates’ dependent variable (ROA) with individual components of IC that is SC and CE. This is consistence with the study of Fathi et al. (2013), Mehri et al. (2013) and Chan (2011) (Table 9). Tables 9 present the results of model 1 of the study:

The results show that the coefficients on VAIC are positively significant concerning their association with financial performance. This indicates that VAIC has an influence on firm’s financial performance. This situation implies that food products companies in Nigeria with greater IC perform better in terms of return on assets. Table 9 also shows that the coefficient of determinations that is “adjusted R-square” value is 0.2201 indicating that the variables considered in the model accounts for about 22% change in the dependent variable (ROA). In appraising the first model, based on the regression result in Table 9, it is suggested that VAIC positively influences firms’ financial performance. This can be justified with the positive “t” value of 2.2900 and P>|t| 0.0300. Likewise, the results reveal a positive coefficient of 0.0015 which proves that an increase in VAIC by one more unit increases financial performance by 0.0015 times. This result is consistent with the findings of Fathi et al. (2013) which reveals that VAIC associated positively with ROA among listed firms in Iran.

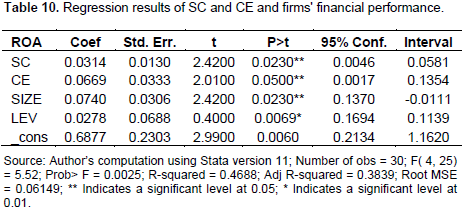

Similarly, the relationship between firms’ size and ROA is positive and significant. This can be justified with the positive “t” value of 2.1000 and P>|t| 0.0450. Similarly, the results show positive coefficient of 0.0705 which attest that, an increase in size by one more unit, other independent variables remaining constant increases the financial performance of Nigerian food Products Company by 0.0705. This result is consistent with the findings of Chan (2011). In addition, the relationship between leverage and ROA is also positively significant at 5% where “t” value of 0.3400P>|t| 0.0073. Equally, the results reveal a positive coefficient of 0.0263 proves that, an increase in leverage by one more unit, other independent variables remaining constant, increases financial performance by 0.0263. The result is consistence with the study of Salman et al. (2012) (Table 10). Table 10 shows the results of model 2:

The results show that ROA is related with SC and CE, suggesting that the IC components of structural capital and capital employed have influence on firm’s financial performance. Table 10 presents the value of adjusted R square of model 2 for SC and CE is 0.3839 which reveal that the two components of IC describe 38% variability in firms’ financial performance. In analysing the model 2, as shown in Table 10, the results show that the relationship between ROA and SC is positively significant. This can be explained by observing the positive “t” value of 2.4200 and P>|t| 0.0230 at 5%. Likewise, the results reveal a positive coefficient of 0.0314 which indicating that, an increase in SC by one more unit, other independent variables remaining constant increases financial performance by 0.0314. This implies that, SC has a significant positive influence on ROA. This result is consistent with the findings of Fathi et al. (2013) and Bharathi (2015) which revealed that SC associated positively with ROA among listed firms in Iran and India respectively.

In the same vein, the relationship between CE and ROA is positively significant at 5% level of significance. This can be justified through the positive “t” value of 2.0100 and P>|t| 0.0500. It has been also validated by the positive coefficient of 0.0669 which means that, an increase in CE by one more unit, other independent variables remaining constant increases the firms’ financial performance by 0.0669. This implies that, CE has a positive and significant influence on ROA. Similarly, under this model, relationship between size and ROA is positive and significant at 5% level of significance, this can be explained by observing the positive “t” value of 2.4200 and P>|t| 0.0230, whichshows that positive coefficient of 0.0740 attests that, an increase in size by one more unit, other independent variables remaining constant, increase the financial performance of Nigerian food products by 0.0740. This is also in line with the findings of Chan (2011) in Hong Kong.

Again, the relationship between leverage and ROA is positively significant at 1% level of significance where “t” value of 0.4000 while P>|t| 0.0069. Similarly, the results reveal a positive coefficient of 0.0278 which shows that, an increase in leverage by one more unit, other independent variables remaining constant increases financial performance by 0.0278. A possible explanation for these results is that, food products firms in Nigeria are trying to increase their performance through the employment of more capital and placing high efforts in utilizing its structural capital more especially in the current contemporary world of information technology and knowledge-based environment. This is in consistent with the study of (Bornemann, Knapp, Schneider, and Sixl, 1999). Overall, it can be said that these findings answered research questions since it shows that VAIC and its components that is, SC and CE contribute significantly to firms’ financial performance. By observing the results of the study, aim and objectives of the study are also attained.

IC, SC and CE has been hypothesised to influence the financial performance (ROA) of listed food products companies in Nigeria. The empirical results provide evidences for the three hypotheses relating to IC and firm’s financial performance. The results also show that adjusted R-square in model 2 that comprises of components of IC (SC and CE) has higher explanatory power of 38% as compared to that in model 1 where the adjusted R-squared is 22%. These findings are corroborated by the study of Bharathi (2015) which is associated IC with financial performance and valuation of firms in India. For the findings in relations to the two control variables used in the study, firm leverage and firm size, the results from the two models suggest that firm leverage is positively associated with the financial performance of the food products of the companies in Nigeria.

This positive and significant association appears to suggest that based on the Nigerian investors in this recent time tends to value food products companies’ more than other companies. Secondly the positive relationship appears to suggest that Nigerian government moves from mono economy to diversified economy where food products and other agricultural companies are getting more attention from the government (Esu and Udonwa, 2015; Abogan, Akinola, and Baruwa, 2014; Onodugo, Ikpe and Oluchukwu, 2013). Results also indicate that firm size is positively associated with financial performance of food products companies. Thus, it appears to suggest that in Nigeria, companies with a larger market capitalisation may tend to be more productive in terms of the revenue generated per unit of asset invested.

The study reveals that IC has a positive and significant influence on the financial performance of food products companies. In relations to SC and CE as components of IC the study proves that:

1. SC has a positive and significant influence on ROA in model 2 suggesting the enhancement in financial performance via the instalments of SC facilities. This can be achieved by providing the employees with best possible technologies and well-talented business strategies in carrying out their work or excellent chain of command in the firms.

2. The results show that CE is also significant and has positive influence on financial performances. This signifies that increasing and maintaining the financial and non-financial capital contributes greatly in improving the profitability and productivity of the Nigerian food products companies.

It is hoped that this study has depicted the genuineness of the IC development condition in one of the most affluent countries in Africa that is and the study does not only contribute to the knowledge of IC research in Nigeria, but also highlights the requirement for local policy makers, business leaders and governments to pay more attention to the cultivation of IC as a strategic asset to sustain in a knowledge-based economy.

The study finally offers the following recommendations:

1. There is a need to have a separate department called IC department in all organization (both public and private), so that clear and proper records of all components of IC could be kept by the organization.

2. There is also need for policy makers and standard setters to include IC components in the harmonised International Financial Reporting Standard and other local GAAPs due to its relevance to business organizations.

3. In order to have an IC managers and up-to-date accountants there is a need to introduce IC in the modern syllabus of higher institutions of learning.

4. There is need for the Nigeria’s three tiers of governments (federal, state and local) to invest more in intangible assets besides investing in traditional factors of production.

IMPLICATION OF THE FINDINGS

This study reveals that apart from traditional factors of production, under contemporary world of knowledge-based economy, IC has a positive and significant influence on financial performance of food products companies in Nigeria. Therefore, these results have an implication to: policy makers, researchers, managers, potential and existing shareholders, academics, accounting regulators and others. The implications of the findings can be divided into two aspects; theoretical and practical. For theoretical the implications can be summarised as:

1. The results of this study could be useful to academics and researchers studying IC and firm’s financial performance worldwide. The findings of this study will motivate them to investigate further towards the development of IC, especially to gather evidences from other industries and regions.

2. Due to the tremendous development in IT and knowledge-based business context, the results suggest that a course related to the management of IC can be introduced to develop a well-equipped IC manager in order to reduce the economic recession effects in the world and unnecessary liquidations of companies.

While the practical implications are:

1. The results of this research would alert the directors and managers of companies to consider the effectiveness of IC towards increasing financial performance of Nigerian food products companies. It is hoped that the results will provide IC for the firm more than tangible and physical assets to increase firm value.

2. The findings of this study would provide hints to food products companies which face the difficulty in leveraging and managing the intangible assets corresponding to the globalization era of technology and knowledge-based economy.

3. The findings would also remind the accounting regulators, standard setters to incorporate and emphasize the management of IC in the accounting standard especially in IFRS applied in Nigeria and local GAAPs.

As discussed earlier, study proves the influence of IC in the performance of the Nigerian food products companies. However, the study has some limitations as follows:

1. Unavailability of required data during this study. Thus, it necessitates the study to use the available data at hand to carry out this research work.

2. The selected firms are confined to only firms listed in Nigerian Stock Exchange (NSE).

3. This research only uses data for five years. Study with longer period of data may provide different findings and more stable.

4. The study uses only one variable (ROA) to measure the financial performance of one of the most important sub-sector in the consumer industry in Nigeria

SUGGESTIONS FOR FUTURE RESEARCH

The findings of the present study offer opportunities for further investigations. Therefore, future researchers could investigate the following areas of study:

1. Analysis in the present study draws on data from Nigeria only and from subsector (food products) within consumer industry reliant on IC. Thus, future research could use data from different nations and different industries, reliance on IC in order to provide further evidence on the impact of IC on firm’s financial performance.

2. Studies can also be carried out on consumer industry in Nigeria by using more than one measurement of firm’s financial performance such as return on equity (ROE), assets turn over (ATO) market-to book value ratio (M/B) to investigate the impact of IC.

The author has not declared any conflict of interests.

REFERENCES

|

Abdulsalam F, Al-Qaheri H, Al-Khayyat R (2011). The Intellectual Capital Performance of Kuwaiti Banks: An Application of VAIC Model. iBusiness 3(1):88-96.

|

|

|

|

Abogan OP, Akinola EB, Baruwa OI (2014). Non-oil export and economic growth in Nigeria (1980-2011). J. Res. Econ. Int. Finance. 3(1):1-11.

|

|

|

|

|

Ademola OJ, Kemisola OC (2014). Working capital management and profitability of selected quoted food and beverages manufacturing firms in Nigeria. European J. Accounting Auditing Finance. 2(3:10-21.

|

|

|

|

|

Ahangar RG (2011). The relationship between intellectual capital and financial performance: An empirical investigation in an Iranian company. Afr. J. Bus. Manage. 5(1):88-95.

|

|

|

|

|

Akpinar AT, Akdemir A (2002). Intellectual Capital. Dspace.Xmu.Edu.Cn. pp. 332-340.

|

|

|

|

|

Al-Musali MAK, Ismail KNIK (2014). Intellectual capital and its effect on financial performance of banks: evidence from Saudi Arabia. Procedia – Soc. Behav. Sci. 164(164):201-207.

Crossref

|

|

|

|

|

Almusali MAKM (2009). The influence of intellectual capitalon financial performance of banks listed in Bahrain.

|

|

|

|

|

Al-shubiri FN (2013). The impact of value added intellectual coefficient components on financial health. Rev. Int. Comparative Manage. 14(962):459-472.

|

|

|

|

|

Amin S, Aslam S, Makki MAM (2014). Intellectual capital and performance of pharmaceutical firms in Pakistan. Pak. J. Soc. Sci. 34(2):433-450. Retrieved from

View.

|

|

|

|

|

Anne-Laure M, Nick B (2013). Intellectual capital and performance within the banking sector of Luxembourg and Belgium. J. Intell. Capital 14(2):286-309.

Crossref

|

|

|

|

|

Anuonye NB (2015). Intellectual capital measurement: using the earnings per share model of quoted insurance companies in Nigeria. Int. Bus. Manage. 10(1):88-98.

|

|

|

|

|

Appuhami BA (2007). The impact of intellectual capital on investors' capital gains on shares: An empirical investigation of Thai banking, finance & insurance sector. Int. Manage. Rev. 3(2):14-25.

|

|

|

|

|

Appuhami R, Bhuyan M (2015). Examining the influence of corporate governance on intellectual capital efficiency Evidence from top service firms in Australia. J. Intell. Capital 30(4/5):347-372.

|

|

|

|

|

Arslan M, Zaman R (2014). Intellectual performance: A study of oil and gas sector of Pakistan. Int. Letters Soc. Humanistic Sci. 43:125-140.

Crossref

|

|

|

|

|

Asare N, Simpson SNY, Onumah JM (2013). Exploring the disclosure of intellectual capital in Ghana: Evidence from listed companies. J. Account. Market. 2(3).

Crossref

|

|

|

|

|

Barney J (1991). Firm resources and sustained competitive advantage. J. Manage. 17(1):99-120.

Crossref

|

|

|

|

|

Berry J (2004). Tangible strategies for intangible assets: How to manage and measure your company's brand, patents. Intellectual property and other services of value. Mcgraw-Hills Publishers company, New York.

|

|

|

|

|

Berzkalne I, Zelgalve E (2014). Intellectual Capital and Company Value. Proc. – Soc. Behav. Sci. 110:887-896.

Crossref

|

|

|

|

|

Bharathi KG (2015). Impact of intellectual capital on financial performance and market valuation of firms in India. Int. Lett. Soc. Humanistic Sci. 48:107-122.

Crossref

|

|

|

|

|

Bontis N (1998a). Intellectual capita: An exploratory study that develops measures and models. Manage. Decision 36(2):63-76.

Crossref

|

|

|

|

|

Bontis N (2000b). Intellectual capital and business performance in Malaysian industries. J. Intellect. Capital. 1(1):85-100.

Crossref

|

|

|

|

|

Bornemann M, Knapp A, Schneider U, Sixl K I (1999). Measuring and reporting intellectual capital: Experience, issues, and prospects. Int. Symposium. pp. 1-34.

|

|

|

|

|

Brooking A (1996). Intellectual capital. London: International Thomson Business Press.

|

|

|

|

|

Broring S, Cloutier LM (2008). Value-creation in new product development within converging value chains: An analysis in the functional foods and nutraceutical industry. Brit. Food J. 110(1):76-97.

Crossref

|

|

|

|

|

Business Day (2015). Honeywell posts N1.4bn profit. Business Day.

|

|

|

|

|

Chan KH (2011). Impact of intellectual capital on organisational performance: An empirical study of companies in the Hang Seng Index. Learn. Org. 16(1):22-39.

Crossref

|

|

|

|

|

Chen MC, Cheng SJ, Hwang Y (2005). An empirical investigation of the relationship between intellectual capital and firms' market value and financial performance. J. Intellect. Capital. 6(2):159-176.

Crossref

|

|

|

|

|

Chinaemerem OC, Anthony O (2012). Impact of capital structure on the financial performance of Nigerian firms. Arabian J. Bus. Manage. Rev. 1(12):43-61.

Crossref

|

|

|

|

|

Choudhury J (2010). Performance impact of intellectual capital: A study of Indian IT Sector. Int. J. Bus. Manage. 5(9):72-80.

Crossref

|

|

|

|

|

Clarke M, Seng D, Whiting RH (2011). Intellectual capital and firm performance in Australia. J. Intellect. Capital. 12(4):505-530.

Crossref

|

|

|

|

|

Dadashinasab M, Sofian S (2014). The impact of intellectual capital on firm financial performance by moderating of dynamic capability. Asian Soc. Sci. 10(17):93-100.

Crossref

|

|

|

|

|

Deep R, Narwal KP (2014). Intellectual capital and its association with financial performance: A study of Indian textile sector. Int. J. Manage. Bus. Res. 4(1):43-54.

|

|

|

|

|

Djamil AB, Razafindrambinina D, Tandeans C (2013). The impact of intellectual capital on a firm's stock return: Evidence from Indonesia. J. Bus. Stud. Quart. 5(2):176-183.

|

|

|

|

|

Drucker PF (1993). Post-capitalsit society. Engstrom, T. E. J., Westnes, P., & Westnes, New York: Harpercollins Publishers Inc.

|

|

|

|

|

Durham K, Kennedy B (1997). Intellectual capital: Realizing your company's true value by finding its hidden brainpower. Res. Technol. Manage. 40(5):59.

|

|

|

|

|

Esu GE, Udonwa U (2015). Economic diversification and economic growth: Evidence from Nigeria. J. Econ. Sustain. Dev. 6(16):56-69.

|

|

|

|

|

Fathi S, Farahmand S, Khorasani M (2013). Impact of intellectual capital on financial performance. Int. J. Acad. Res. Econ. Manage.

|

|

|

|

|

Sci. 2(1):6-18.

|

|

|

|

|

Firer S, Williams SM (2003). Intellectual capital and traditionalmeasures of corporate performance. J. Intellect. Capital. 4(3):348-360.

Crossref

|

|

|

|

|

Gan K, Saleh Z (2008). Intellectual capital and corporate performance of technology-intensive companies: Malaysia evidence. Asian J. Bus. Account. 1(1):113-130.

|

|

|

|

|

Garcia-Ayuso M (2003). Intangibles: Lessons from the past and a look into the future. J. Intellect. Capital. 4(4):597-604.

Crossref

|

|

|

|

|

Graziano AM, Micheal RL (1993). Research methods: Process of inquiry. Harpercollins College Publishers.

|

|

|

|

|

Hair J, Joseph F. Hair, Black B, Babin B, Anderson RE, Tatham RL (2006). Multivarate data analysis. (S. Katie & S. Kelly, Eds.) (Six edition). United States of America: Pearson Education Inc.

|

|

|

|

|

Hudson WJ (1993). Intellectual capital: How to build it, enhance it use it. United States of America: John Willey & Sons Inc.

|

|

|

|

|

Iavorskyi M (2013). The Impact of Capital Structure on Firm Performance: Evidence From Ukraine. Master of Finance Economics Thesis, Kyviv School of Economics.

|

|

|

|

|

Kalkan A, Bozkurt OC, Arman M (2014). The impacts of intellectual capital, innovation and organizational strategy on firm performance. Procedia – Social and Behavioral Sciences, 150, 700–707.

Crossref

|

|

|

|

|

Kamal MHM, Mat RC, Rahim NA, Husin N, Ismail I (2011). Intellectual capital and firm performance of commercial banks in Malaysia. Asian Econ. Financial Rev. 2(4):577-590.

|

|

|

|

|

Kamath GB (2007). The intellectual capital performance of Indian banking sector. J. Intellect. Capital. 8(1).

|

|

|

|

|

Khalique M, Shaari JA, Isa AH (2011). Relationship of intellectual capital with the organizational performance of commercial banks in Islamabad, Pakistan.

|

|

|

|

|

Khan FA, Khan RAG, Khan MA (2012). Impact of intellectual capital on financial performance of banks in Pakistan: Corporate restructuring and its effect on employee morale and performance. Int. J. Bus. Behav. Sci. 2(6):22-30.

|

|

|

|

|

Kline RB (2005). Principles and Practice of Structural Equation Modelling. New York: Guilford Publications.

|

|

|

|

|

Kujansivu P, Lonnqvist A (2007). Investigating the value and efficiency of intellectual capital. J. Intellect. Capital. 8(2):272-287.

Crossref

|

|

|

|

|

Kurawa JM, Kabara AS (2014). Impact of corporate governance on voluntary disclosure by firms in the downstream sector of the Nigerian petroleum industry. In Proceedings of World Business Research Conference (1–19).

|

|

|

|

|

Laing G, Dunn J, Hughes-Lucas S (2010). Applying the VAICTM model to Australian hotels. J. Intellect. Capital. 11(3):269–-283.

Crossref

|

|

|

|

|

Lee AM, McKinney J (2012). Understanding and Applying Research Design, John Wiley & Sons, Inc., Hoboken, NJ, USA.

|

|

|

|

|

Leedy PD, Ormrod JE (2010). Practical research planning and design. Pearson Education Inc.

|

|

|

|

|

Lina AS (2014). The influence of intellectual capital components towards the company performance. J. Manage 14(1):125-140.

|

|

|

|

|

Luthy D (2008). Intellectual capital and its measurement. InProceedings of the Asian Pacific Interdisciplinary Research in Accounting Conference (APIRA), Osaka, Japan 1998 Aug 4. pp. 16-17.

|

|

|

|

|

Maditinos D, Chatzoudes D, Tsairidis C, Theriou G (2011). The impact of intellectual capital on firms' market value and financial performance. J. Intellect. Capital. 12(1):132-151.

Crossref

|

|

|

|

|

Maditinos D, Sevic Z, Tsairidis C (2010). Intellectual capital and business performance: An empirical study for the Greek Listed Companies. Eur. Res. Stud. XIII(3):145-167.

|

|

|

|

|

Makki MAM, Lodhi SA (2008). Impact of intellectual capital efficiency on profitability (A case study of LSE25 companies). Lahore J. Econ. 2(13):81-98.

|

|

|

|

|

Mariya AM, Shakina EA (2014). Article information: J. Intellect. Capital. 15(2):206-226.

|

|

|

|

|

Mehri M, Umar MS, Saeidi P, Hekmat RK, Naslmosavi S (2013). Intellectual capital and firm performance of high intangible intensive industries: Malaysia evidence. Asian Soc. Sci. 9(9):146-155.

Crossref

|

|

|

|

|

Muhammad NMN, Ismail MK A (2009). Intellectual capital efficiency and firm's performance: Study on Malaysian financial sectors. Int. J. Econ. Finance 1(2):206-212.

Crossref

|

|

|

|

|

Musibah AS, Alfattani WSBWY (2013). Impact of intellectual capital on corporate social responsibility evidence from Islamic banking sector in GCC. Int. J. Finance Account. 2(6):307-311.

|

|

|

|

|

Najibullah S (2005). An empirical investigation of the relationship between intellectual capital and firms' market value and financial performance. J. Intellect. Capital. P1-20.

|

|

|

|

|

Nezakati H, Ali NA, Mansouri S, Ang SH (2011). Adapting elements of market value coverage in adoption and diffusion of innovations - fast food industries (preliminary study). Aust. J. Basic Appl. Sci. 5(9):1271-1276.

|

|

|

|

|

Nigerian Stock Exchange (2013). NSE FACTBOOK

|

|

|

|

|

Nimtrakoon S (2015). The relationship between intellectual capital, firm's market value and financial performance: Empirical evidence from the ASEAN. J. Intell. Capital. 16(3):587-618.

Crossref

|

|

|

|

|

Okpala PO, Chidi OC (2010). Human capital accounting and its relevance to stock, investment decisions in Nigeria. Eur. J. Econ. Finance Admin. Sci. 21(21):64-76.

|

|

|

|

|

Ong TS, Yeoh LY, Teh BH (2011).Intellectual capital efficiency in Malaysian food and beverage industry. Int. J. Bus. Behav. Sci. 1(1).

|

|

|

|

|

Onodugo V, Ikpe M, Oluchukwu A (2013). Non-oil export and economic growth in Nigeria: A time series econometric model. Int. J. Bus. Manage. Res. 3(2):115-124.

|

|

|

|

|

Pouraghajan A, Malekian E (2012). The relationship between capital structure and firm performance evaluation measures: Evidence from the Tehran Stock Exchange. Int. J. Bus. Commerce. 1(9):166-81.

|

|

|

|

|

Pulic A (1998). 2nd McMaster world congress on measuring and managing intellectual capital by the Austrian team for intellectual potential. In Measuring the performance of intellectual potential in knowledge economy. pp. 1-20.

|

|

|

|

|

Rehman WU, Rehman HU Usman M, Asghar N (2012). A link of intellectual capital performance with corporate performance: Comparative study from banking sector in Pakistan. Int. J. Bus. Soc. Sci. 3(12):313-321.

|

|

|

|

|

Roos G, Roos J (1997). Measuring your company's intellectual performance. Int. J. Strat. Manage. 30(3):413-426.

|

|

|

|

|

Salman RT, Mansor M, Babatunde AD, Tayib M (2012). Impact of intellectual capital on return on asset in Nigerian manufacturing companies. Interdiscipl. J. Res. Bus. 2(4):21-30.

|

|

|

|

|

Salman RT, Dandago KI (2013). Intellectual capital disclosure in financial reports of Nigerian companies. In Intellectual capital disclosure in financial reports of Nigerian companies. pp. 1-17.

|

|

|

|

|

Sekaran U, Roger B (2013). Research Methods for Business. India: John Wiley & Sons Ltd. Service, F. I. R: Information circular: No: 9701 (1997).

|

|

|

|

|

Sledzik K (2013). The intellectual capital performance of polish banks: An application of VAICTM model. Financial Internet Quart. 9(2):92-100.

|

|

|

|

|

Stahle P, Stahle S, Aho S (2011). Value added intellectual coefficient (VAIC): acritical analysis. J. Intellectual Capital. 12(4):531-551.

Crossref

|

|

|

|

|

Thisday (2015). Honeywell holds AGM, posts N1.4bn profit. Thisday pp.

|

|

|

|

|

Tseng CY, Goo YJJ (2005). Intellectual capital and corporate value in an emerging economy: Empirical study of Taiwanese manufacturers. R and D Manage. 35(2):187-201.

Crossref

|

|

|

|

|

Xu D, Huo B, Sun L (2014). Relationships between intra-organizational resources, supply chain integration and business performance. Ind. Manage. Data Syst. 114(8):1186-1206.

Crossref

|

|

|

|

|

Yusuf I (2013). The relationship between human capital efficiency and financial performance: An empirical investigation of quoted Nigerian banks. Res. J. Finance Account. 4(4):148-155.

|

|

|

|

|

Zeghal D, Maaloul A (2010). Analysing value added as an indicator of intellectual capital and its consequences on company performance. J. Intell. Capital. 11(1):39-60.

Crossref

|

|