ABSTRACT

This paper explains the trade-offs between the relevance and faithful representation of accounting information analyzed in the contexts of the cash-basis, accrual-basis, and fair value accounting methods used to prepare financial statements for Generally Accepted Accounting Principles (GAAP) and tax reporting. Discussion of the role of the relevance and faithful representation of accounting information is generally separate from any discussion of the trade-offs between cash-basis, accrual-basis, and fair value accounting methods, and the different needs and priorities of the users of GAAP and tax reporting information. The study contributes to the literature by suggesting how the importance of relevance and faithful representation differs between GAAP reporting and tax reporting, and how the allowable accounting methods for GAAP and tax reporting align with the differing emphasis on relevance and faithful representation. We review the reporting requirements established by regulators in light of these trade-offs and discuss how the needs of external users of the reporting information shape the allowable accounting methods for GAAP and tax reporting.

Key words: Relevance, faithful representation, cash-basis, accrual-basis, fair value, GAAP, tax reporting.

The purpose of this paper is to discuss the trade-offs inherent in three competing financial reporting systems - cash-basis accounting, accrual-basis accounting, and fair value accounting - and the implications of the trade-offs in light of the requirements established for GAAP (financial) and tax reporting. To the researchers’ knowledge, this study is the first to demonstrate how the importance of relevance and faithful representation differs between GAAP and tax reporting, and how the allowable accounting methods emphasize the different needs and priorities of the users of accounting information.

The conceptual framework developed by the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) states that the primary objective of financial reporting is to provide financial information that is useful to investors and creditors for making investment and lending decisions. According to the FASB, useful information has two fundamental qualities - relevance and faithful representation. Accounting information is considered relevant if it would make a difference in a business decision. For such information to be relevant, it must possess predictive value (providing accurate expectations about the future) or confirmatory value (confirming or correcting prior expectations). Consequently, accounting information is deemed relevant if it provides helpful information about past events or potential future events. Furthermore, accounting information has faithful representation if it accurately depicts the actual events that occurred, including providing information that is complete (without important omissions), neutral (not biased), free from error, and verifiable.

Under cash-basis accounting, companies record revenue and expenses at the time money is received or paid out (related to their operating activities). Cash-basis is largely appealing due to its simplicity, but it can result in misleading financial statements, as it does not record business activities (such as sales) as they happen – the activity is only recorded as cash changes hands. Cash-basis accounting is considered to be low in relevance, but high in faithful representation. Using fair value accounting, companies measure and report the value of assets and liabilities using the actual or estimated fair market price of the assets and liabilities. Changes in asset or liability values are recorded as unrealized gains or losses, increasing or reducing net income, comprehensive income, and/or equity. Fair value accounting is considered high in relevance, and low in faithful representation. Using accrual-basis accounting, transactions are recorded in the periods in which the events occur, even if cash is not exchanged, following the revenue and expense recognition principles. Accrual-basis accounting is considered to be a middle ground for both relevance and faithful representation; as it is more relevant than cash-basis accounting (but less than fair value), and has more faithful representation than fair value (but less than cash-basis accounting).

The qualitative characteristics of accounting information, relevancy and faithful representation, allow those who analyze and use this information to make well informed decisions. We suggest that financial reporting emphasizes relevance: under current GAAP, companies are allowed to report (with few exceptions) using accrual-basis accounting and fair value methods, which are ranked as high and medium in relevance. The external users benefit from the increase in information that is useful for decision making and relies on auditors to verify that the information presented in the financial statements is accurate and free from errors. The focus for financial reporting is on allowing companies to use accounting methods that provide external users with the information they need to make decisions. We also suggest that tax reporting emphasizes faithful representation. Under current tax regulations, companies are allowed to report (with few exceptions) using cash and accrual accounting methods, which are ranked as high and medium in faithful representation. The primary external user for tax reporting is the Internal Revenue Service (IRS). The IRS likely believes there is no benefit to allowing taxpayers increased subjectivity (bias and errors) in their tax reporting. Instead, the focus is on allowing companies to use verifiable, accurate, and easy to audit accounting methods for this reporting.

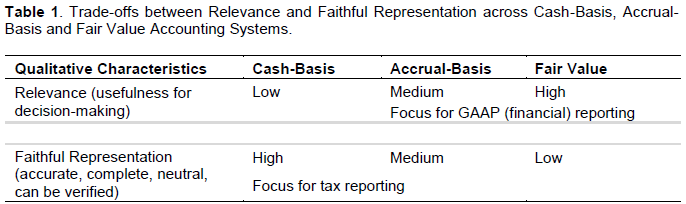

Table 1 illustrates the trade-offs between the relevance and faithful representation of accounting information in the context of the three competing financial reporting systems and importance for GAAP and tax reporting. The information suggests that accrual accounting avoids the extremes, providing users with information that is neither low in relevance nor low in faithful representation and is therefore a frequently used method for both GAAP and tax reporting.

ACCOUNTING METHODS AND RELATED LITERATURE

Cash basis

With cash-basis accounting, revenues are recorded when cash is received from customers in the ordinary course of business, whether it’s after the sale of a product or after a service is provided. Cash flows received from parties other than customers (such as, money borrowed from a bank) would not be considered revenue under a cash-basis system since these cash flows are helping finance the business rather than resulting from day-to-day operations. Expenses under a cash-basis system are recorded when there are cash outflows (that help to generate cash inflows from customers). For example, a manufacturing facility’s cash purchase of equipment would be recorded as an expense under a cash-basis system. The focus of cash accounting is on cash flows; cash receipts, cash payments, and cash surpluses or deficits (Tickell, 2010).

Accrual basis

Using accrual-basis accounting, revenues are recorded only when they are earned, when the goods or services have been provided to customers, and not when cash is received from customers.

Therefore, accrual accounting can provide information on the impact of transactions where cash has not yet been received or paid (Public Sector Committee, 2002). Expenses are recorded under an accrual accounting model only when they are incurred and not when cash has been paid (to employees, vendors, etc.). Under accrual accounting, the transaction is recognized on the date the income is earned or the expense is incurred (Tickell, 2010). For example, monthly rent expense would be recorded at the end of each month, and not when the rent payment is actually made. The historical cost principle is used in accrual accounting, and fixed assets are recorded at their original cost on the balance sheet, and generally depreciated (and subject to impairment). Accrual accounting focuses on revenues, expenses and profits or losses, and enables informed decision making (Tickell, 2010).

Fair value

Fair value accounting is focused on the balance sheet and uses current market values as the basis for reporting certain assets and liabilities. Therefore, fair value accounting modifies the historical cost of assets and liabilities and adjusts them upwards or downwards to their current market values. Fair value is the estimated price at which an asset can be sold, or a liability settled in an orderly transaction to a third party under current market conditions and focuses on the exit price (the price at which an asset can be sold, not the price at which the asset can be purchased; Corporate Finance Institute, 2020).

Under SFAS 157, companies classify their fair-valued assets into three categories: Levels 1, 2, and 3, based on the asset’s liquidity and/or valuation input reliability, and determine the values of the assets accordingly (AICPA; Bragg, 2020). Under fair value accounting, gains or losses from any changes in the value of assets or liabilities are reported in the period in which they occur. An increase in asset value or a decrease in liability value adds to net income or other comprehensive income, and a decrease in asset value or an increase in liability value reduces net income or other comprehensive income.

The usefulness of accounting information, and the use of various accounting methods, has developed into several streams of accounting literature. The seminal article by Ball and Brown (1968) demonstrated the relation between stock returns and earnings. Building on this idea, other studies have examined the faithful representation (or reliability) of accounting information in the context of the ability of current earnings to predict future earnings (Bandyopadhyay, et al., 2010; Kirschenheiter, 1997; Richardson et al., 2005), and whether a high degree of conservatism indicates high quality financial statements (Basu, 1997; Ball et al., 2000; Ball and Shivakumar, 2005; Barth et al., 2008; Chen et al., 2010).

Other studies have shown the links between financial reporting and firm value. For example, researchers have examined whether value relevance, the ability of information that is presented by financial statements to capture and summarize firm value, has increased or decreased over time, examining differences between countries, before and after the adoption of new accounting standards (such as IFRS) and changes in regulations (such as the Sarbanes-Oxley Act), and whether firm characteristics that mediate the relation (Khanagha, 2011; Perera and Thrikawala, 2010; Core et al., 2003; Marquardt and Wiedman, 2004; Kargin, 2013; Iatridis, 2010; Papadatos and Bellas, 2011). Other research streams have studied the historical development of accounting methods. For example, Georgiou and Jack (2011) examine the historical roots of fair value accounting and conclude that no accounting basis has become fully institutionalized to the exclusion of others, resulting in an acceptance of mixed measurements in financial reporting.

This study builds upon these studies and shows that the importance of relevance and faithful representation for GAAP and tax reporting differs, and describe how cash-basis, accrual-basis and fair value accounting methods allowed under each reporting system reinforce the differences.

CASH-BASIS AND ACCRUAL-BASIS ACCOUNTING

The benefits of accrual-basis accounting

Accrual accounting generally results in more relevant income statements, providing information that is better for decision making, compared with a cash-basis system, as expenses are better matched with the revenues that these expenses helped to generate with the accrual accounting method. In Appendix A we provide a numerical example. Without this matching, the net income of companies using cash-basis accounting generally has a larger variance, making it more difficult for investors and lenders to forecast future income or cash flows. Financial statement users may be concerned to see large losses in years when fixed assets are purchased.

Following these “big bath” years, the company is likely to report artificially high book income, which may be very attractive to investors and lenders and may generate unrealistic expectations for future profitability. For tax purposes, a net loss reported in asset purchase years would create a net operating loss (NOL), and that would eliminate taxes due in that year, and could be used to reduce taxable income in future years. Although not ideal for highly relevant financial reporting, cash-basis accounting may be ideal from a tax perspective as it alleviates some pressure on the business cash-flow, which can be a crucial factor in the initial years of an entity.

Just as accrual-basis income statements will generally provide more relevant information to financial statement users than cash-basis income statements, the same thing can be said for the superiority of accrual-basis balance sheets relative to cash-basis balance sheets. For example, significant resources (or claims on resources) are not reflected on a cash-basis balance sheet. Examples include accounts receivable, accounts payable, and fixed assets. Without reflecting receivables and payables and other significant resources and claims on resources, a cash-basis balance sheet may not be very relevant for financial statement users’ decision making.

Accrual-basis balance sheets, which show company resources and claims on those resources, provide more relevant information. For example, a bank would have less difficulty making a good lending decision using an accrual-basis balance sheet that contains information concerning receivables and payables. Interestingly, for small companies (companies with under $250,000 in assets), the IRS does not require balance sheet information to be reported with a company’s tax return. It is likely that the IRS knows many of these small companies are using cash-basis accounting, and the balance sheet would not be very informative.

The benefits of cash-basis accounting

In order to obtain the more relevant income statements with accrual accounting (that match expenses with the revenues generated by those expenses), faithful representation is oftentimes sacrificed with the use of estimates. For example, the annual allocated cost of equipment (depreciation expense) depends on two estimates: useful life and salvage value. If and when either of the estimates are adjusted, (for example, as new information is obtained), the company will change the future depreciation charges. This loss of faithful representation (or reliability) with respect to estimates inherent to the accrual accounting method is a stark contrast to the cash-basis model in which estimates are not needed to complete the financial statements. The lack of estimates makes cash-basis information very easy to verify, and the most faithfully represented of all three accounting methods.

Cash-basis may be potentially advantageous for tax reporting, as companies have some flexibility regarding the exact timing of the cash receipts and disbursements. For example, companies can reduce taxable income in the current year by waiting to send out invoices for goods delivered or services rendered until the start of the following year. Alternately, companies can increase current-year deductions by prepaying certain expenses, like insurance or rent. Using the “12-Month Rule,” a substantial amount of those prepaid expenses can be reported on the current year tax return in order to increase deductions, and reduce taxable income reported to the IRS.

Summary

While the cash-basis method has higher faithful representation than the accrual-basis method, most users of financial statements would agree that the increase in relevance from the use of accrual accounting is worth the sacrifice in faithful representation. The accrual method generally provides a better “report card” of how well a company is doing because of better matching of revenues and expenses, lower variance in net income, and more complete balance sheets (reflecting receivables and payables, etc.) compared with a cash-basis accounting system.

ACCRUAL ACCOUNTING AND FAIR VALUE ACCOUNTING

The benefits of fair value accounting

Fair value income statements provide more relevant information for decision makers compared with accrual-basis income statements, and in Appendix B, the study provides a numerical example. The example demonstrates that with rising replacement costs, fair value income statements provide more conservative net income figures compared with accrual accounting income statements. However, just because the fair value income statements are more conservative (than the accrual accounting statements) does not always mean they help users to make well informed decisions.

The fair value method also provides more relevant data on the balance sheet, compared with the cash and accrual-basis methods. For example, the fair value method would report land on a company’s balance sheet each year based on the appraised value of the land, whereas with accrual-basis, a company’s balance sheet would reflect the original (historical) cost of this land (even if this cost was incurred many years ago).

The study provides an example in Appendix C illustrating the high relevance of fair value balance sheets, compared to accrual-basis balance sheets. In our example in Appendix C, the ending retained earnings using fair value is equal to the cash balance available to either grow the business or pay dividends. Thus, the fair value method yields retained earnings that more accurately portrays how much “better off” the Company is in terms its “true economic profit”. By showing a “true economic profit,” the fair value income statement and balance sheet is highly relevant. Accrual-basis balance sheets, on the other hand, result in a mismatch between retained earnings and cash. Since the cumulative earnings under the accrual model does not agree with the incremental assets available to grow the business and/or pay dividends, the relevance of accrual accounting income statements is said to only be “moderate”. Indeed, the accrual accounting method seems to overstate earnings relative to the “true” economic profit that is reflected in the fair value method.

The benefits of accrual accounting

One drawback of the fair value method is that it can be highly subjective when measuring financial statement accounts. This is especially concerning when active markets do not exist for company assets and liabilities (Level 2 and 3 assets), and the fair value is estimated, opening up the possibility of intentional or unintentional errors in accounting estimates. Due to the subjective nature of fair value accounting and the estimates often involved, fair value accounting is considered to have the lowest level of faithful representation.

In other words, shifting to more relevant fair value data in the balance sheet can oftentimes only be attained by sacrificing faithful representation. Faithful representation is reduced any time a company is not able to perfectly forecast the factors used in determining its estimates. For example, in fair value accounting, the increased purchase price of a replacement asset needs to be accurately allocated to changes in technology, inflation, and/or supply/demand considerations. With these unknowns, the estimation process for the replacement cost depreciation determinations can be quite subjective, and determining which assumptions are correct and how to make the assumptions is very challenging. For example, it can be very subjective determining how much of the increase in an asset’s replacement price is due to improved technology and how much is due to inflationary pressures.

Additionally, it can be quite subjective determining how much more effective (or productive) a replacement asset will be, and whether there will be a related reduction in annual repairs and maintenance. It could turn out that part of the increase in the purchase price of a replacement asset would not be inflationary in nature but would instead reflect expected product improvements. The complexity of making estimates for replacement cost depreciation is just one area that requires a significant number of estimates.

Both GAAP and IFRS are increasing the use of the fair value method to report balance sheet assets (at this point the IFRS has adopted it more broadly).

One example is revaluation, where GAAP and IFRS allow the value of a fixed asset that was originally recorded using historical cost, to be adjusted downward to reflect the fair market value. However, only IFRS permits assets that have been written down to be reversed, where the value is restored to the historical cost or above, and in some cases IFRS allows depreciation based on revaluation of assets, which is not permitted under GAAP. The main advantage of fair value accounting is that if done at regular intervals and without management bias, fair market balance sheets show assets at their true market value, providing highly relevant information to users, and a more accurate financial picture of a company than either the cash or accrual-basis methods.

The IRS allows only a few items to be reported at fair value for tax purposes, likely to prevent the temptation to report biased estimates on the tax return in order to reduce a company’s tax liability. For example, businesses may report the fair value of charitable contributions as a deduction on their tax returns (this depends on the type of property donated, and for qualifying donations; many require an independent appraisal of the fair value). Further, depending on the type of entity and financial reporting requirements, the balance sheet reported on the tax return may include fair value amounts (for example, when reporting investments).

The fair value method is closely linked with estimations. If performed on a regular basis and without management bias, the estimations result in financial statements that are highly relevant. Unfortunately, the extent and subjectivity of estimations suggest that fair value financial statements have the lowest level of faithful representation out of the three methods.

To the authors’ knowledge, they are the first to demonstrate how the importance of relevance and faithful representation differs between GAAP and tax reporting, and how the allowable accounting methods emphasize the different needs and priorities of the users of accounting information. We highlight trade-offs between the two fundamental qualities of useful accounting information in the context of the fair value, accrual-basis, and cash basis accounting methods. The accounting information prepared for GAAP and tax reporting is presumed to be useful for external users. “To be useful, financial information must not only represent relevant phenomena, but it must also faithfully represent the phenomena that it purports to represent” (Conceptual Framework, 2010, A34). Publically traded companies are required to follow U.S. GAAP, suggesting that regulators view highly relevant financial statements as essential for external users, and therefore allow (with few exceptions) companies to report using accrual-basis and fair value methods. Fair values have played a role in U.S. GAAP for more than 50 years; however, accounting standards that require or permit fair value accounting have increased considerably in the last two decades (Ryan, 2008). A recent publication from KPMG states “The use of fair value measurement for financial reporting continues on an upward trajectory and presents significant challenges, requiring judgment and interpretation” (KPMG, 2017, page 3). Fair value accounting has been blamed for multiple stock market crises, including the Wall Street crash of 1929 and the 2008 financial crisis (Ramanna, 2013). However, relying on the idea that financial markets are efficient and that prevailing prices are reliable measures of value most relevant to financial statement users, regulators continue to allow companies to use fair value accounting for reporting a specific set of assets, including certain financial assets and liabilities, asset retirement obligations, derivatives and intangible assets acquired in a business combination (Chung et al., 2016). It appears that regulators believe that allowing accounting methods that increase relevance (accrual-basis and fair value) for external users is the priority, as potential decreases in faithful representation may be mitigated with a high-quality audit.

Tax reporting has few external users – with the IRS being the most significant. As the primary user of tax reporting, the IRS requirements concerning accounting methods are likely focused on limiting the subjectivity (bias and errors) allowed in tax reporting, and allowing companies to use verifiable, accurate, and easy to audit accounting methods. According to Fellow and Kelaher (1991), although the accrual accounting concept is simple to understand, it can be difficult to implement. Therefore, allowing cash-basis accounting (appealing due to simplicity) may lessen the burden of accrual accounting for small taxpayers. As tax information is generally used exclusively for the purposes of collecting tax revenue, and is generally not used by outside parties for lending and investment decisions, it appears that the IRS is willing to sacrifice relevance in order to prioritize obtaining tax reporting information that is high in faithful representation. As tax law is ultimately established by US Presidents and Congress, the study concludes that these branches of the US government have also more highly valued faithful representation compared with relevance.

Regulators have undoubtedly considered the trade-offs between accounting methods when establishing both financial and tax reporting requirements for companies in the U.S. As we suggest, the importance of relevance and faithful representation differs between GAAP and tax reporting, as a result of the different needs and priorities of the external users of this information. However, these needs are not static, and in recent decades regulators have modified the reporting requirements to allow, and in some cases even require, components of the cash-basis, accrual-basis, and fair value accounting methods for both GAAP and tax reporting.

Future research in this area can continue to analyze the trade-offs between fair value, accrual-basis, and cash-basis accounting for financial and tax reporting, in light of changing regulations and reporting environments. For example, recent news articles suggest that the Biden administration may eliminate the basis step-up rule (The New York Times, 2021). Currently, when an individual inherits property, their basis in the property is “stepped-up” to the current fair market value, so an immediate sale of that property would not be subject to capital gains tax. Eliminating the step-up could increase taxes for individuals inheriting property that had appreciated in value and would require information regarding the original owners cost basis in the property. In addition, future studies could also examine how the increase in digital information available to individuals and regulators impacts reporting requirements for financial statement and tax purposes, and how the ease with which fair market value and cost basis information can be gathered affects the relevance and faithful representation of fair value, accrual-basis, and cash-basis accounting methods.

These intriguing ideas are left for future studies.

The authors have not declared any conflict of interest.

REFERENCES

|

AICPA Media Center? (2020). FAQs About Fair Value Accounting, AICPA.org, Available at:

View

|

|

|

|

Ball R, Brown P (1968). An empirical evaluation of accounting income numbers. Journal of Accounting Research pp. 159-178.

Crossref

|

|

|

|

|

Ball R, Kothari SP, Robin A (2000). The effect of international institutional factors on properties of accounting earnings. Journal of Accounting and Economics 29(1):1-51.

Crossref

|

|

|

|

|

Ball R, Shivakumar L (2005). Earnings quality in UK private firms: comparative loss recognition timeliness. Journal of Accounting and Economics 39(1):83-128.

Crossref

|

|

|

|

|

Bandyopadhyay SP, Huang AG, Wirjanto TS (2010). The accrual volatility anomaly. Unpublished Manuscript, University of Waterloo.

|

|

|

|

|

Barth ME, Landsman WR, Lang MH (2008). International accounting standards and accounting quality. Journal of Accounting Research 46(3):467-498.

Crossref

|

|

|

|

|

Basu S (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics 24(1):3-37.

Crossref

|

|

|

|

|

Bragg S (2020). Fair value accounting, Accounting tools, December 13, Available at:

View

|

|

|

|

|

Chen H, Tang Q, Jiang Y, Lin Z (2010). The role of international financial reporting standards in accounting quality: Evidence from the European Union. Journal of international financial management and accounting 21(3):220-278.

Crossref

|

|

|

|

|

Chung SG, Lee C, Mitra S (2016). Fair Value Accounting and Reliability, The Problem with Level 3 Estimates, CPA Journal, July, Available at:

View

|

|

|

|

|

|

|

Conceptual Framework for Financial Reporting (2010). September. Available at:

View

|

|

|

|

|

Core J, Guay W, VanBuskirk A (2003). Market valuations in the new economy: an investigation of what has changed. Journal of Accounting and Economics 34:43-67.

Crossref

|

|

|

|

|

Corporate Finance Institute (CFI) (2020). Fair Value; The actual value of a product, stock, or security, that is agreed upon by both the seller and the buyer, Available at:

View

|

|

|

|

|

Fellow K, Kelaher M (1991). Managing the government the corporate way. Australian Accountant 61(3):20.

|

|

|

|

|

Georgiou O, Jack L (2011). In pursuit of legitimacy: A history behind fair value accounting. The British Accounting Review 43:311-323.

Crossref

|

|

|

|

|

Iatridis G (2010). International Financial Reporting Standards and the quality of financial statement information. International Review of Financial Analysis 19(3):193-204.

Crossref

|

|

|

|

|

Kargin S (2013). The impact of IFRS on the value relevance of accounting information: Evidence from Turkish firms. International Journal of Economics and Finance 5(4):71-80.

Crossref

|

|

|

|

|

Khanagha JB (2011). Value relevance of accounting information in the United Arab Emirates. International Journal of Economics and Financial Issues 1(2):33-45.

|

|

|

|

|

Kirschenheiter M (1997). Information quality and correlated signals. Journal of Accounting Research 35(1):43-59.

Crossref

|

|

|

|

|

KPMG (2017). Fair Value Measurement; Questions and answers; US GAAP and IFRS, December, Available at:

View

|

|

|

|

|

Marquardt CA, Wiedman CI (2004). The effect of earnings management on the value relevance of accounting information. Journal of Business Finance and Accounting 31(3-4):297-332.

Crossref

|

|

|

|

|

Papadatos K, Bellas A (2011). The value relevance of accounting information under Greek and International Financial Reporting Standards: the influence of firm-specific characteristics. International Research Journal of Finance and Economics (76):6.

|

|

|

|

|

Perera RAAS, Thrikawala SS (2010). An Empirical Study of the Relevance of Accounting Information on Investors decisions.

|

|

|

|

|

Public Sector Committee (2002). Transition to the accrual basis of accounting: Guidance for governments and government entities. New York: International Federation of Accountants.

|

|

|

|

|

Ramanna K (2013). Why "Fair Value" Is the Rule, Harvard Business Review, Available at:

View.

|

|

|

|

|

Richardson SA, Sloan RG, Soliman MT, Tuna I (2005). Accrual reliability, earnings persistence and stock prices. Journal of Accounting and Economics 39(3):437-485.

Crossref

|

|

|

|

|

Ryan SG (2008). Fair Value Accounting: Understanding the Issues Raised by the Credit Crunch. White paper commissioned for the Council of Institutional Investors, Available at:

View

|

|

|

|

|

The New York Times (2021). The Estate Tax May Change Under Biden, Affecting Far More People. Available at:

View

|

|

|

|

|

Tickell G (2010). Cash To Accrual Accounting: One Nation's Dilemma. International Business and Economics Research Journal 9(11):71-78.

Crossref

|

|