ABSTRACT

Loss of biodiversity threatens the world's ecosystem and tropical forests provide the last hope of sustainability. Environmental accounting focuses on sustainable production and development generates data and employs methodologies for valuing natural resources. Thus, by providing these accounting realities conservation is not only encouraged but becomes a critical necessity. This study aimed to evaluate the potential roles of environmental accounting in conserving biodiversity in tropical forests. Specifically, it is aimed to estimate the rate of deforestation and evaluate its effect on biodiversity for accounting purposes. The study was conducted in the Forest Reserves of Osun State, Nigeria through a survey of communities around the Forest Reserves to obtain the Contingent Values of biodiversity. Data on rates of deforestation were obtained from records of the Forestry Management Department of the Ministry of Environment in Osun State, Nigeria. These data were analyzed using the LOGIT regression Model and the amounts of WTP was aggregated and extrapolated to obtain the total value of biodiversity losses in the Forest Reserves. Results showed a per capita annual cost of 25USD resulting to over 2,824,408.125 USD as the lost value or depreciation of biodiversity in the study area. This depreciation cost is tremendous requiring urgent attention to conservation. It was concluded that the emergence of environmental accounting tools has significant consequence on biodiversity preservation because what is counted is what is valued and what is valued is what is treasured. This calls for policy and stringent action towards conservation of forest resources.

Key words: Biodiversity, environmental accounting, deforestation, depreciation.

Background to the study

The significance of tropical forests in the world’s ecosystem cannot be overemphasized. It has been adjudged to be the last hope for sustainability of the earth. As Cuckston (2013), quoting Lindsey 2007), puts it, tropical forests contain about half of the species on earth. Biodiversity can be described as the variety of life on earth, that is, the number of species of plants, animals and microorganisms as well as the enormous diversity of genes in these species, the various ecosystems on the planet such as the deserts, rainforests and coral reefs are all part of biologically diverse earth (Shah, 2012). Cuckston (2013) further emphasizes that the biological diversity of trees, shrubs, animals and micro-organisms exists as a highly complex interconnected web of life and death comprising the tropical forest ecosystems.

The International Union for Conservation of Nature-IUCN (2011) indicates that the activities of man have fostered the degradation of forests so that an average of 100 species is lost daily. Tropical forests are of global importance, as they store and process large quantities of carbon via photosynthesis and respiration, approximately six times as much carbon as humans release into the atmosphere through fossil fuel use, and houses between one-half and two-thirds of the world's species (Groombridge and Jenkins, 2002). Thus, small changes within the tropical forest biome can potentially lead to major global impacts on both the rate and magnitude of climate change and the conservation of biodiversity.

Among the causes of biodiversity loss are land use changes, pollution, changes in atmospheric CO2 concentrations, changes in the nitrogen cycle and acid rain, climate alterations, and the introduction of exotic species, all coincident to human population growth. The primary factor is land conversion and not climate change or nitrogen problems because growth in rainforests is usually limited more by low phosphorus levels than by nitrogen insufficiency. The diversity in tropical forests reduces the effects of introducing exotic species than in temperate areas because there is so much that newcomers have difficulty becoming established. In effect, the chief cause of biodiversity loss is deforestation. The Inter Academy Partnership (IAP) (2010), observes that carbon is assimilated in the forest canopy and is stored in trees, roots and soils; a process that is a function of complex biodiversity. However, deforestation and over-exploitation in tropical regions are major contributors to the sixth global mass extinction event. The loss of this store of genetic diversity will compromise the capacity of all life on earth to adapt to human-induced climate change.

The critical issue is that as vital as biodiversity is, its values are quite controvertible. Yet, as observed by Sukhdav (2008), the lack of valuation is an underlying cause of degradation of ecosystems and loss of biodiversity. As can be observed, nations are assessed on the basis of GDP growth or lack of it, yet the GDP, as it is known, does not capture many vital aspects of national wealth, especially nature’s endowment like the biomass. In his assessment, Cuckston (2013), the exclusion of primary forests from Clean Development Mechanism (CDM) is largely due to accounting difficulties encountered in designing Reducing Emissions through Deforestation and Degradation (REDD) projects. Rather than merely estimating carbon taken up as a result of new plantations, REDD was supposed to provide a means of determining emissions that could have taken place in the absence of existing trees by constructing an accounting model to reflect the ecosystem services of forests through carbon sequestration. The concern is to begin to construct accounting models that will not only value biodiversity aright but integrate the values into accounting framework.

Statement of the problem

It is widely acknowledged that there is no solution to climate change without concrete efforts towards conservation of forest biodiversity, which by extension is to slow down deforestation. The benefits associated with such efforts are as varied as watershed protection, tourism revenues, and existence values for species preservation (Dixon and Sherman, 1994). The focus of recent works is on the benefits estimation to the exclusion of costs estimation (Kramer, 2014). Environmental accounting seeks to identify cost elements, measure impacts, monetization of impacts and integration of values in financial reports for the benefits of policy makers. There are a number of challenges traceable to environmental accounting efforts in the direction of biodiversity loss arising substantially from methodologies and measurements.

As observed by Kramer (2014), attention has focused on calculating and accruing benefits of biodiversity conservation in an accounting process, largely because of the need to convince policy makers and program managers that conservation investments can earn economic returns. Although these returns could be largely intangible, beset by methodological challenges, especially the non-market benefits of complex ecosystems. This paper explored the solution to the cost elements to be integrated for accounting purposes adopting the TEEB framework which relies on the amount the society is willing to pay for the services provided by the ecosystem.

Research questions

The following questions were raised to guide this study:

1. What is the rate of deforestation? What is the relationship between deforestation and biodiversity loss? 2. What is the value of biodiversity loss in forest reserves of Osun State, Nigeria?

3. What is the full cost of biodiversity conservation?

4. Can the identified costs be integrated into the accounts?

Research objectives

The main objective of this paper is to evaluate the roles of environmental accounting in conserving biodiversity in tropical forests. Accordingly, the specific objectives are:

1. To estimate the rate of deforestation and evaluate its effect on biodiversity;

2. To determine the value of biodiversity loss in the forest reserves of Osun state;

3. To estimate the full (environmental) cost of biodiversity conservation in the forest reserves of Osun State, Nigeria for accounting purposes; and,

4. To evolve a model for integrating the costs of biodiversity conservation into accounts.

Hypotheses

The following hypotheses were proposed for this study. They are all stated in null form.

Hypothesis I: There is no relationship between deforestation and biodiversity loss.

Hypothesis II: There is no difference in the perceptions of stakeholders on the value of biodiversity loss in the forest reserves of Osun State, Nigeria.

The study area

The study area is the forest reserves of Osun State, located in the south-western Nigeria, Osun State and lies between 7 and 8° 30' North (7 - 8° 30’ N) and longitude 4° and 50° East (4 - 50° E) having a population of three million, four hundred and twenty-three thousand, five hundred and twenty-five people (3,423,525) by 2006 Census (Figures 1 and 2) (Alamu, 2008; National Population Commission, 2007). The state had eleven legacy forest reserves which fell within her boundaries, after she was carved out of the then Oyo state. Only eight of these reserves are still in existence.

Five forest reserves were surveyed. The local population around the five forest reserves (that is, 5 km radius of the forest) is estimated at 300,000. The sample size is 390 computed as follows:

Where, n = sample size; p = level of precision anticipated in respect of the research problem. Since there is no precedence 50% is selected. q = 1-p; ME= Margin of Error that can be tolerated in this research is 5%. Z = the alpha value is determined by calculating 1-confidence level, 1- 0.95 = 0.05 to estimate the critical value given as 1-(alpha/2), that is, 0.975. The value is 1.96, that is, n = [(1.96)2*0.5*0.5 + (0.05)2] / (0.05)2; n = 0.9629/0.0025 = 385.16.

The variables for this study are:

1. Size and changes in forest reserves of Osun state (1992-2015) to depict the rate of deforestation

2. Biodiversity loss due to deforestation

3. Socioeconomic characteristics of respondents

5. Willingness to Pay for Biodiversity (dichotomous choice)

6. Mean Amount of Willingness to Pay for biodiversity

Data analysis was done as follows:

1. Trends of forest size changes, timber harvesting and tree regeneration were calculated and the t-test was used to test the degree of association between them;

2. LOGIT regression model was adopted to determine WTP in determining the value of biodiversity;

3. The mean value of WTP was computed as per capita value of biodiversity in the forest reserves;

4. An extrapolation of the mean WTP to determine accounting value to reflect in the books.

Model specification

1. To measure the Willingness To Pay (WTP) for biodiversity in the forest reserves, the following models were used.

2. The LOGIT regression model analyzes the dichotomous choice between “Yes” and “No” of the WTP and is mathematically expressed as:

Where, P(BDV)is the probability of a respondent showing a WTP; X1 = Gender of respondents; X2 = Marital Status of respondents; X3 = State of origin of respondents; X4 = Education of respondents Xs = Size of farm of respondents; X6 = Annual Income of respondents; X7 = Age of respondents; X8 = Size of family of respondents; X9 = Distance from Forest Reserves.

To determine the appropriate value for biodiversity in Osun State, Nigeria the mean amount of WTP is regarded as per capita valuation of watershed services in the state and thus is extrapolated over the entire population for full values to be obtained:

VBDV refers to the value of biodiversity; X(WTPBDV) is the mean amount of Willingness to Pay for biodiversity. POPosun is the population of Osun state by 2006 Census.

Modeling value for integration into annual accounts

The last step involves the computation of the annualized cost using the rate of deforestation as a factor for annual depreciation of forest environmental services. The rate of deforestation in Osun State Forest reserves is 3.3%.

Annualized Cost (BIODIVERSITY LOSS)) = VBDeV* RDEFORESTATION

Analysis of trends and rates of deforestation in the forest reserves of Osun State, Nigeria

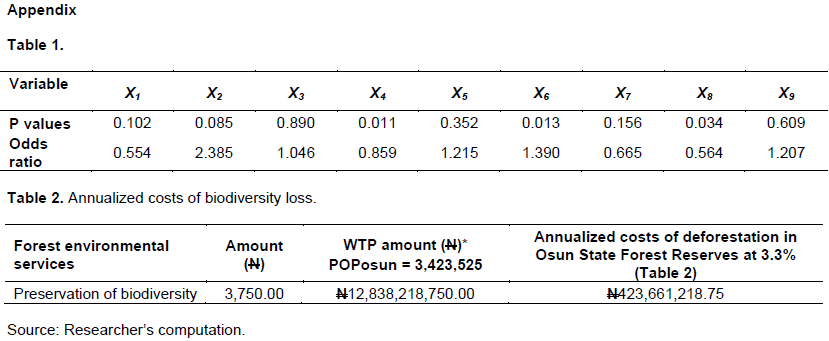

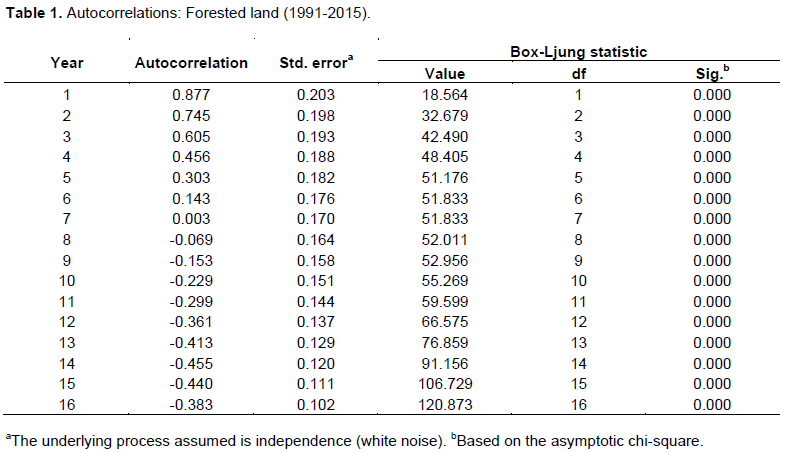

The data available in respect of forest cover at inception of Osun State, Nigeria in 1991 and subsequent years to 2015 show the status of the forest reserves from year to year giving effect to the various changes occurring over the years. These were plotted in Figure 3 with a trend line showing the linearity of the phenomenon of deforestation. The principal forest conversions were reflected alongside the cumulative effects of unsustainable logging. The data on trend of deforestation comprised of forest land cover over the 25-year period that Osun state has existed. The trend was subjected to time series analysis through a 5-year moving averages (autocorrelation). The results were indicative of the rate of forest cover loss over the years, with an average rate of decline at 0.383 forest depreciation with an annual rate of (120.873/16 = 5.7558; 5.7558/120.873 = 0.0476) (Table 1). All the years show p-values that were significant at 1, 5 and 10% levels of significance indicating that deforestation is prevalent in Osun state and at the present stands at 38.3% of the legacy forest reserves with annual growth rate 4.76%.

The trends of deforestation in the forest reserves of Osun State, Nigeria

Butler (2010) in a study with mongabay.com, hinted that Nigeria has the highest deforestation rate in the world. Although Brazil has the largest area of deforested land and Congo has the heaviest consumption of bush-meat, threatening wildlife, Nigeria’s rate is much higher than any other country. The finding of this study showed that whereas the rate of national deforestation in Nigeria was reported as 1.8% per annum (Salami, 2009), through remote sensing and the Nig-Sat1, a study on Osun state forests showed an average rate of deforestation of 3.1% per annum (Olatunji, 2005).

The implications of deforestation are divers but its prevalence is equally worrisome. Among the most threatened tropical rain forest are those in Africa, with Togo, Congo and Nigeria being at worst risk. It would seem that the Kuznet’s hypothesis is playing out because most of the regions at risks are developing countries. It should be recalled that the Kuznet’s hypothesis argues that environmental concerns only become predominant after basic economic growth are resolved (Pasternak and Schlissel, 2001).

Desertification is known to result from deforestation especially in the fragile lands (expunge WPF). When considered with the attendant climate change, it is apparent that every effort to stop desertification is worthwhile. No other approach has been more suitable than afforestation or curbing of deforestation. Recently, it was reported that Nigeria loses about $6 billion annually to deforestation (Butler 2010). At the present rate of deforestation there would be nothing left in the next six to ten years.

FAO, reports Nigeria as having the world's highest deforestation rate of primary forests. She has lost more than half of its primary forest in the last five years. Causes cited are logging, subsistence agriculture, and the collection of fuel wood. Almost 90% of West Africa's rainforest has been destroyed (Csupomona.edu2011.on http://www.csupomona.edu/~admckettrick/ projects/ag101_project/html/size.html). Schmidt (2012) observed that the global cost of deforestation transcends the costs of financial system collapse and these costs were calculated from the perceived costs of losing the services that forests provide. Yet it is impossible to accrue such costs without initially ascertaining the level and rate of deforestation.

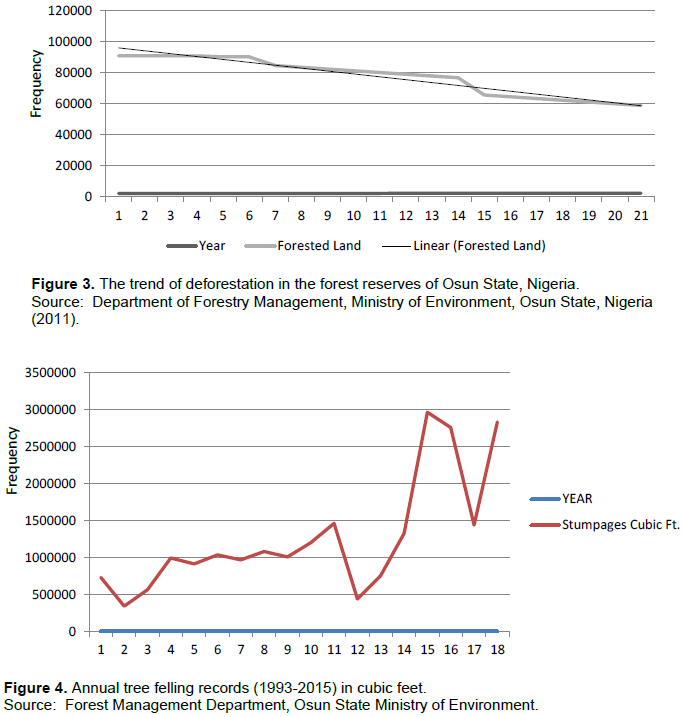

The records of tree felling for the period under review show that although some troughs are noticeable in the curve there is a continuous rise in the volume of tree felled from year to year. When this record is juxtaposed with those of regeneration, the sustainability of current practice can be determined. Also it points to the possible consequences of current practices on the long run.

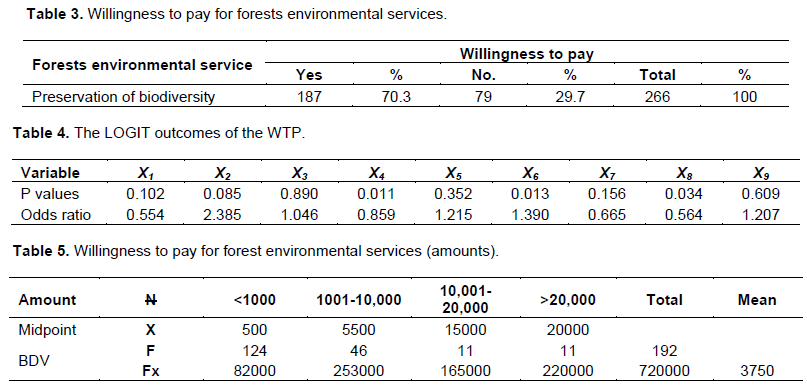

Data on forests regeneration (1993-2015)

Forest regeneration cover activities involved with raising tree seedlings, silviculture and establishment of plantations- whether directly or through collaborative Desertification is known to result from deforestation efforts (Tungyei agro-forestry system). Whereas it is possible to determine the volume of timber felled, the hectares achieved in rehabilitating, renewing or rejuvenating the forests is reckoned here. Thus in comparing tree felling to tree planting, the relativity of the trends could be studied.

The present record shows a steady decline in tree planting efforts (Figure 5). This constitutes an issue of grave concern especially with regards to sustainability of the forests. Besides, it would seem apparent that consumption has largely outstripped regeneration. This would easily be interpreted to mean that whereas tree felling was growing, tree planting was declining giving room to deforestation in the forest reserves.

Analysis of the gap between forest regeneration and timber harvests (Logging) in the forest reserves of Osun State, Nigeria

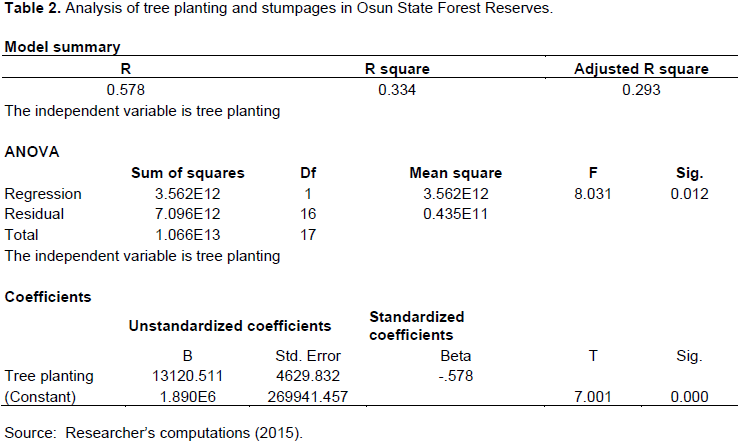

The study produced data that show the pattern of tree planting which is expected to guide harvesting activities to achieve sustainability. The relationship between tree planting and harvesting (logging) is a pointer to level of deforestation and its prevalence within the controlled areas. The data in respect of tree planting were obtained from Forestry Regeneration Department of Osun State Ministry of Environment; while, data relating to timber harvests (stumpages) were obtained from the Forestry Management Department of Osun State Ministry of Environment. Test of significance is carried out using the ANOVA and Student t-test. Results show Fcal as 8.031 and the p-value was 0.012 and this is significant at 0.05 level of significance. Thus the null hypothesis that there is no significant relationship between tree planting and tree felling in the Forest reserves of Osun State, Nigeria is upheld. The tcal was -2.834, R = 0.578 and R2 at 0.334 which implies that regeneration can only explain about 33.4% of tree felled showing a progressive gap of about 66.6% of tree harvest (Table 2).

As observed by Akande (2012), “the current rate of forest depletion in Nigeria implies that the forest base may be incapable of providing adequate biomass supply for the livelihoods of future generations.” This is an issue for ecological footprint accounting.

The issue of deforestation was more graphic as it was examined by Salami (2009), through remote sensing and the Nig-Sat1. It was estimated that the rate of deforestation was about 1.8% per annum; here the rate of removal of the canopy was the basis of estimation. A closer study on Osun state forests showed an average rate of deforestation of 3.1% per annum (Olatunji, 2005). The efforts of United States of America at supporting nations in addressing the emissions problem through REDD (Reducing Emissions through Deforestation and Degradation) was reviewed by Butkiewicz (2011), and it showed that Nigeria alongside Democratic Republic of the Congo had the worst cases in Africa and behind Brazil and Indonesia.

The prevalence of deforestation was said to be worsened by corruption as previous efforts to intervene had only made corrupt politicians and officials richer to the detriment of the environment. Indeed, Kinver (2012) stated that tropical forests are the richest source of biodiversity but have been on steady decline, Nigeria is not exempted from this trend. The results of this study corroborate these previous findings. In addition, the sustainable yield has been flagrantly abused. The theory states that tree felling should be harmonized with regeneration efforts such that the net effects of harvesting is more than compensated for by regeneration (Fisher, 1904; Hotelling, 1925; Thampapilai and Uhlin, 1997; Bishop and Woodward, 2002; Chapman,1999; Forest Australia,2007). Lange (2003) explained that “estimating the volume and cost of deforestation and forest degradation has been a major motivation for forest accounting, especially in developing countries.” So, the determination of the gap between tree planting and tree felling will help explain the prevalence of deforestation for meaningful accounting process.

A contingent valuation of the environmental impacts of deforestation in Osun State Forest Reserves

Sangare (2006) observed that methods were developed in order to find a solution to fundamental asymmetry of

treatment between manufactured goods and natural goods. These methods were attempts to find an ‘approximate’ value for natural goods through the creation of a fictitious market where the marginal Willingness to Pay (WTP) is analogous to price and then total WTP is analogous to consumer surplus (Luenberger, 2006).

WTP for biodiversity

The equation line is used for determining the probability and significance of the WTP for BDV. The outcome variable, z, is the willingness to pay for biodiversity. As stated earlier, the independent variables are X1 to X9. Thus, the expanded equation is given as:

Computation of the annualized costs of biodiversity loss in Osun State forest reserves for accounting purposes is given in Appendix Table 2.

CONCLUSION AND RECOMMENDATIONS

The study was conducted on the declining forest reserves and its ecosystems. The phenomenon of deforestation and its consequence on biodiversity was examined. Attempt was made to evaluate the biodiversity loss prevalent in the forest reserves. These values were construed for accounting purposes and formed into a framework that is akin to accounting depreciation values. It was concluded that deforestation had significant effects on biodiversity loss and that the values derived from contingent valuation provides needed value for accounting purposes. It was recommended that biodiversity loss should be adequately accounted for. Accounting systems and frameworks should be developed to cater for this purpose through collaboration with other fields to achieve synergy in achieving precise values.

The author has not declared any conflict of interests.

REFERENCES

|

Akande JA (2012). The Bastion of Green Advocacy: Our Forests, Our Welfare. MaidenInaugural Lecture. Bowen University, Iwo. P 38.

|

|

|

|

Alamu LO (2008) Evaluation of Log Conversion Efficiency of Band Saws in Osun State Sawmills, in New Era Res. J. Engin. Sci. Technol. P 119.

|

|

|

|

|

Bishop RC, Woodward RT (2002) Sustainability, Economy and Environment, in D. Chapman (ed.) Environmental Economics: Theory, Application and Policy. Addison- Wesley. P 373.

|

|

|

|

|

Butkiewicz JL (2011). Institutions and the Impact of Government Spending on Growth,"(with HalitYanikkaya), J. Appl. Econ. XIV(2):319-341.

Crossref

|

|

|

|

|

Butler RA (2010). World Deforestation Rates and Forest Cover Statistics in

View

|

|

|

|

|

Chapman D (1999). Environmental Economics: Theory, Application and Policy Addison-Wesley. P 85.

|

|

|

|

|

Csupomona.edu2011.View

|

|

|

|

|

Cuckston T (2013). Bringing Tropical Forest Biodiversity Conservation into Financial Accounting Calculation. Accounting, Auditing and Accountability Journal. Emerald Group Publishing Limited. 26(5):688-690.

|

|

|

|

|

Dixon JA, Margulis S (1994). Integrating the Environment into Development Policy Making In Making Development Sustainable, Ismail Serageldin and Andrew Steer (eds.), World Bank. pp. 21-24.

|

|

|

|

|

Fisher I (1904). Precedents for Defining Capital. Quart. J. Econ. P 18.

Crossref

|

|

|

|

|

Forest Australia (2007). Sustainable Yield and Australia's Forests on Forests Australia- Fast Forest Facts.htm of the Department of Agriculture, Fishery and Forestry.

|

|

|

|

|

Groombridge B, Jenkins M (2002). World Atlas of Biodiversity, University of California Press, Ewing, NJ.

|

|

|

|

|

Hotelling H (1925). A General Mathematical Theory of Depreciation. J. Am. Stat. Asso. 20:151, 340.

|

|

|

|

|

Inter Academy Partnership (IAP)(2010). IAP Statement on Tropical Forests and Climate Change.

|

|

|

|

|

Kinver M (2012). Protected Tropical Forests Biodiversity Declining" in BBC News on

View

|

|

|

|

|

Kramer R (2014). Slowing Tropical Forest Biodiversity Loss: Cost and Compensation Considerations.

|

|

|

|

|

Lange G (2003). Policy Applications of Environmental Accounting" in Environmental Economics Series Paper No. 88 of the World Bank Environment Department. Washington: The International Bank for Reconstruction and Development/ THE WORLD BANK. pp. 3-6.

|

|

|

|

|

Luenberger DG (2006). Information Science. Economics and Business. Princeton University Press, ebook.

|

|

|

|

|

National Population Commission (2007). Nigeria Population Estimates. Federal Office of Statistics.

|

|

|

|

|

Olatunji TE (2005). Environmental accounting as a means of promoting sustainable forestry operations in Osun State. J. Bus. Manage. 3(1):129-131.

|

|

|

|

|

Pasternak D, Schlissel A (2001). Combating Desertification with Plants. Springer Science and Business Media New York.

Crossref

|

|

|

|

|

Shah A (2012). Global Issues: Ecological Disturbances. Available from:

View

|

|

|

|

|

Salami AT (2009). Space Applications and Ecological Haemorrhage: The Nigerian Experience, In Inaugural Lecture Series 220.ObafemiAwolowo University Press Limited, Ile-Ife. pp. 9, 13, 21, 31, 40.

|

|

|

|

|

Sangare M (2006). Ivorian Forest Conservation in the Generalized Poverty Context: An Application Of The CVMto the Case of National Park of Taï. A Proposal Submitted to the Ivorian Government on the Valuation of Conservation Efforts at Tai National Park. pp. 11-15.

|

|

|

|

|

Sukhdav P (2008). The Economics of Ecosystem and Biodiversity (TEEB): An Interim Report. Germany: European Communities.

|

|

|

|

|

Schmidt GA (2012). Climate sensitivity - How sensitive is Earth's climate to CO2? PAGES news. 20(1).

|

|

|

|

|

Thampapillai DJ, Uhlin H (1997). Environmental Capital and Sustainable Income: Basic Concept and Empirical Tests. In Cambridge J. Econ. 21(3):379-394.

Crossref

|

|

|

|

|

The International Union for Conservation of Nature-IUCN (2011). International Union for Conservation of Nature: forest facts and figures.

|

|

APPENDIX