Full Length Research Paper

ABSTRACT

This study examines the relationship between corporate tax avoidance (CTA), earnings management (EM) and corporate social responsibility (CSR) within a context of an emerging economy. The study employs system methods of moments (GMM) and logistic regression to establish whether firms in Ghana manage earnings and avoid tax to finance corporate social responsibility. The results show that almost all the firms sampled have engaged in some management of their earnings and tax during the period. The study also find evidence that an increase in CSR activities is associated with an increase in EM, suggesting that, sampled firms may use CSR as a cover for engaging in opportunistic behaviour such as earnings management. By extension, these results have important policy implications for policy makers in assessing the effectiveness of the tax laws.

Key words: Corporate tax avoidance, corporate social responsibility, earnings management, developing country.

INTRODUCTION

This study examines the relationship between tax avoidance and earnings management, and their joint impact on corporate social responsibility (CSR). Prior researchers analysing the relationship between Earnings Management (EM) and CRS activities (Kim et al., 2012; Lin et al., 2008; Cespa and Cestone, 2007; Garriga and Melé 2004) have explained the relationship mostly relying on the concept of legitimacy and instrumental theories with mixed findings.

Scholtens and Kang (2013) argues that the disclosure of ‘true and fair’ financial earnings is crucial for CSR because it provides outsiders with a basis of trust and confidence regarding the firm’s claims and operations and that a high standard of CSR is to be positively associated with high accounting quality of the firm. Increase in CSR performance and disclosure improves the quality of financial reports leading to increased financial transparency and accountability (Lin et al., 2008). On the other hand, Prior et al. (2008), argue that managers who act in pursuit of private benefits by distorting earnings information will be able to entrench themselves by engaging in CSR and empirically, concluded on a positive association between the level of earnings management and CSR.

Businesses which stress on their CSR activities tend to signal that they are good corporate citizens as well as draw attention away from possible hint that they are engaged in earnings management. As the world economy becomes more integrated, corporations are facing more and more pressure to disclose their CSR information. Similar to Preuss (2010), a noteworthy question to ask is what happens to a firm’s CSR performance in a situation where there are circumstances in which firms engaging in EM can insulate themselves successfully against societal expectations? According to Ball and Shivakumar (2005), one incentive for managing earnings is corporate tax avoidance. Christensen and Murphy (2004) argue that corporate tax avoidance (CTA) is value enhancing to shareholders hence managers are encouraged to employ their best effort to minimising taxes. However, tax avoidance techniques give room for opportunistic management to pursue self-seeking objectives and manage earnings in ways that provide benefits to managers, and that do not benefit shareholders (Desai and Dharmapala, 2009), hence managers managing earnings are more likely to insulate themselves by avoiding more taxes as avoidance offers them shield from shareholder scrutiny. Minimised tax payment leaves excess “after tax” cash flow that can either be distributed as extra dividends or invested in profitable projects. Irrespective of the value-enhancing result of avoidance, the non-payment or refusal of corporations to pay their fair share of taxes has been viewed as socially irresponsible (Christen and Murphy, 2004) hence market will have a negative reaction to stock prices of avoidance firms. According to Hanlon and Slemrod (2009), a company’s stock price declines when there is news about its involvement in tax shelters. However, they noticed that the reaction is small relative to reactions to other corporate misdeeds such as firms managing earnings, firms investigated by the Security and Exchange Commission (SEC) for accounting irregularities, firms sued by their shareholders for improper accounting and firms that restated financial statements (McNichols and Stubben, 2008).

If societal pressure and reaction is low with news of CTA in relation to EM, and there exists complementary techniques for both CTA and EM such that management who avoid taxes can also use those avoidance techniques to manipulate earnings to derive some private benefit (Desai and Dharmapala, 2009), then such compa-nies managing earnings can resort to CTA to insulate themselves successfully against societal reaction to EM. If these firms are able to achieve this complementary effect, what then happens to their CSR performance?

Studies enumerated seem to suggest that both CTA and CSR can provide opportunities for managers of firms to shield their managerial malfeasances, including manipulating earnings (Kim et al., 2011). However the relationship between CTA and CSR has been under-researched (Preuss, 2010) with inconsistent results.

Christensen and Murphy (2004) assert that, companies’ attitude towards CSR legitimately influences their decisions on the extent of and preparedness to reducing their tax liability. This implies that, where firms ethically engage in CSR, such firms are less likely to avoid taxes (Sikka, 2010). That avoidance is considered socially irresponsible as corporate tax payments are perceived as the most fundamental way in which companies engage with broader society, hence considered as part of firms’ CSR. Given the complementary relationship between CTA and EM, then it can be asserted that the reduced avoidance will lead to a reduction in EM. Hence ethically engaging in CSR is expected to reduce both EM and CTA. On the other hand, where CSR is used as a repu-tation management tool, then more avoidance activities leads to more CSR activities (Lanis and Ri, 2010). This position can also be explained from the complementary relationship between CTA and EM. Avoiding more taxes implies managing more taxes. EM has negative implications for the firms reputation hence such firms tend to safeguard their reputation, they will entrench themselves by engaing in more in CSR activities.

Untimately it can be asserted that a company’s attitude towards CSR depends on the relationship between EM and CTA. Although various studies have analysed the variables of interest and have established relationships between them, these relationships have been examined independently in most cases. Prior studies have failed to exploit how the relationship between EM and CTA can jointly impact on the CSR practices of firms or examine the CSR behaviour of firms that manage earnings by avoiding taxes. This study therefore seeks to answer these empirical questions. Do firms that managing earnings by avoiding taxes engage in CSR activities? If so, how does managing earnings by avoiding taxes impact on the corporate social manipulative behaviour of such firms? By providing answers to these research questions, the current study fills the gap by empirically analysing the interaction among CSR, earnings management and tax avoidance, employing a dataset from an emerging economy. Particularly the study test for two main hypotheses: first, corporate tax avoidance increases earnings management. Second, the interaction between earnings management and corporate tax avoidance has an overall impact on CSR. Although no previous study has tested both hypotheses, several studies have analysed the first one contributing to the general understanding of firm tax avoidance and earnings management (Desai and Dharmapala, 2009; Hanlon and Heitzman, 2010; Kim et al., 2011).

The contribution of this study is in two folds: First, it adds to prior literature by examining the CSR performance of firms engaging earning management but insulating itself through tax avoidance practices. It achieves this by empirically analysing the overall impact of the relationship between corporate tax avoidance and earnings management on CSR from the context of a developing country, Ghana, where the capital market is relatively undeveloped. Such a study is relevant within such a context because of the magnitude of problems and harmful effects associated with camouflaging EM activities by engaging in CSR and CTA practices, which can affect the fundamentals of the capital markets in emerging economies and developing countries. Corporate scandals involving high-profile companies such as Enron, WorldCom, Tyco, Yukos, Parmalat, the Big-Four global accounting firms, and major law firms had their root cause in EM and has resulted in increasing advocacy for mechanisms to control excessive opportunistic behaviour amongst corporate management. Additionally, taxation is the main source of government financing in most developing economies.

A study of this type has huge policy implication for the country and Africa at large such economies lose huge amounts of government revenue to schemes put in place by businesses to avoid paying taxes. Secondly, this study specifically focuses on Ghana as the country, besides having a weak capital market, has recently adopted International Financial Reporting Standard coupled with the changes for prudential regulations. A study of this type provides information on the improvement or otherwise of reporting quality of reports prepared using IFRS in a country with a weak capital market. The study also provides information of the pervasion of EM in the corporate world of developing countries. This provides standard setters with a fair idea on the effectiveness of IFRS in improving reporting quality and the role it plays in curtailing managerial manipulative behaviour. In 2011, the Ministry of Trade and Industry in Ghana launched an awarding scheme that seeks to reward socially responsible firms in Ghana. This study therefore provides insight into the subject area from a different perspective. Private and public sector organisations as well as policy and regulatory authorities in Ghana would benefit from having a scientific insight into a CSR, EM and CTA study in Ghana.

The results show the existence and growth of EM among sampled firms. This indicates that sampled firms use flexibility in financial accounting to influence reported earnings. The existence of tax avoidance among sampled firms implies that some private benefit exists for managers engaging in such avoidance activities. There is evidence to suggest that firms in Ghana actively engage in CSR activities. On the relationship between CSR and CTA, the result reveals that firms who engage in CSR activities avoid taxes less. Even though the result is insignificant, the negative coefficient suggests that CSR activities are slightly moved by ethical consideration and sampled firms see avoiding less taxes as one important means by which they can affect society.

LITERATURE REVIEW

This section provides a review of the theoretical literature on the subject matter. The study begins with the theoretical principles underlying CSR, earnings management and tax avoidance. The study then discuss the empirical literature on the variables that affect the relationship of interest.

CSR and earnings management

Although CSR has become an increasingly and widely used term among firms and authorities as well as received much attention by researchers over the last two decades, there has not been a generally accepted definition for the term. According to Carroll (1979) (the most widely accepted definition), “the social responsibility of business encompasses the economic, legal, ethical, and discretionary expectations that society has of organizations at a given point in time”.

This definition suggests that, a socially responsible organization must be profitable (economic responsibility); abide by the laws of society (legal responsibility); do what is right, just and fair (ethical responsibility) and be a good corporate citizen (philanthropic responsibility). Grounded on the four main aspects of CSR suggested by Carroll (1979), Garriga and Melé (2004) categorize theories of CSR into ethical (legitimacy), political, integrative and instrumental theories. Proponents of ethical theories argue that, ‘‘the right thing to do’’ is the ‘‘necessity to contribute to the good of society by doing what is ethically correct.’’ Because business and society are not distinct entities but interwoven, the society expects certain appropriate business behaviour and outcomes from organizations. Firms must therefore accept CSR as an ethical obligation and make it a responsibility to consider the legitimate interests of all stakeholders.

In this regard, the desire for firms to build legitimacy drives the increased attention to social and environmental externalities by companies (Bansal and Roth, 2000). Advocates of political theory of CSR suggest that, a firm needs to consider the community where it operates and seek ways of reinforcing the firm’s proclivity to improve the community in which they operate. Integrative theory of CSR argues that, firms need to integrate social demands into their business because the success of the business operations depends on the society. The instrumental theories of CSR consider economic objectives and view CSR as means of creating shareholders’ wealth hence; any proposed social activity by a firm must be consistent with shareholders wealth creation (Kim et al., 2012).

With the exception of the instrumental theory on CSR, all the other theories of CSR suggest that, it is imperative for firms/managers to be truthful, trustworthy, and ethical in their corporate operations and processes, including their financial reporting practices. If managers engage in CSR based on moral obligations, firms will make responsible decisions; including accounting decisions and maintaining transparency in financial reporting. Thus, the theories that have evolved from Carroll’s definition and subsequent CSR delineation suggest that, CSR activities can result in changes in organizational behaviour, systems and processes including the financial reporting processes.

According to Atkins (2006), what investors mean by “socially responsibility” of a firm is transparency in financial reporting. Firms that provide investors with transparent and reliable financial information are socially responsible firms. It is therefore expected that companies that engage and implement CSR activities to benefit multiple stakeholders will limit manipulation of accounting information that is, earnings management. Other researchers use agency theory to advance an association between CSR and firm’s financial reporting practices due to the perceived opportunistic use of CSR by managers. According to Kim et al. (2012), managers may pursue CSR activities for their own interest instead of the interest of the firm and its stakeholders. Hemingway and Maclagan (2004) contend that, firms adopt CSR to cover up their corporate misconducts. CSR activities are therefore, managerial perquisite that managers use to advance their own career ambitions and personal agenda (McWilliams et al., 2006). CSR motivated by self-interest is likely to misinform stakeholders of the true value and performance of the firm through the manipulation of the accounting information. Engaging in good ethical behaviour is one way through which managers pursue their self- interest and from the opportunistic incentive perspective, managers do this by engaging in opportunistic financial reporting practices that is, earnings management. The extent of which CSR is practiced will possibly determine the quality of accounting information.

Prior literature has concentrated on investigating the relationship between CSR and firm performance, mainly using stakeholder theory (Ruf et al., 2001; Waddock and Graves, 1997). These studies mostly provide evidence of a positive relationship between CSR and firm performance and further conclude that shareholders, the principal stakeholders of firms, benefit when management meet the demand of several other stakeholders. However, these studies have not been able to show the changes that have taken place in organizations because of their engagement in CSR or improvement in CSR activities. Studies that have examined the relationship between firms’ CSR practices and earnings management have provided conflicting results (Choi and Pae, 2011; Hong and Andersen, 2011; Kim et al., 2012). Whereas others document positive relationship between CSR and earnings management, others found a negative relationship or no association at all. Laksmana and Yang (2009) document that, earnings of firms with high corporate citizenship are smooth and more persistent and predictable than those with low corporate citizenship. Their findings also suggest a positive relationship between the quality of earnings and CSR. Hong and Andersen (2011) using USA data conclude that, the more socially responsible firms are, the higher their accrual quality and the lower their activity based earnings management. Utilizing ethical commitment as a proxy for CSR, Choi and Pae (2011) also assert a negative relationship between earnings management and CSR as their results show that, firms with higher level of ethical commitment engage in less earnings management and report more conservatively. Kim et al. (2012) use a larger sample (23,391 firm-year observation) to document that, socially responsible firms are less likely to manage earnings through discretionary accruals and manipulate real operating activities.

Prior et al. (2008) examine whether firms strategically utilize CSR to cover up earnings management using 593 firms (both regulated and unregulated) from 23 different countries. They find a significantly positive relationship between earnings management and CSR in regulated firms, and advance that, the better the CSR activities in a company, the more the company manages its earnings. Using two years of Canadian social investment data and 162 firm years, Gargouri et al. (2010) also report a positive relation between corporate social performance and earnings management. Chih et al. (2008) using 1,653 firms from 46 countries, found out that CSR has a negative relationship with earnings smoothing and positively related to earnings aggressiveness. They, thus, document inconsistent results across the different earnings management proxies they utilized. Kim et al. (2012) suggest that differences in country’s accounting, CSR and investor protection regulations may have compelled the results of Chih et al. (2008) rather than differences in CSR activities. Evidently, the studies on CSR-earnings management relationship have utilized different methodologies, measurement proxies and data from different settings but all in developed economies. Moreover, their results have been inconsistent. Leuz et al. (2003) assert that, the association between CSR and earnings management differs between economies and countries probably due to the different levels of investor protection and CSR legalities of the different countries and economies (Reinhardt et al., 2008).

CSR and tax avoidance

CSR relates firms’ economic objectives to their social responsibilities because firms are to act in an ethical manner, contribute to economic development and improve the quality of life of their stakeholders. Corporate tax payments are conceivably the most fundamental way in which companies engage with broader society, hence considered as part of firms’ CSR. However, Christensen and Murphy (2004) from their informal study of multinationals’ CSR statements, assert that, company directors do not regard tax payment as a part of the CSR agenda.

Recent studies have, however suggested a possible link between tax avoidance and CSR practices. Lanis and Richardson (2011) suggest that, CSR principles could potentially influence the tax aggressiveness of a corporation via the board of directors, as outside directors are more likely to be responsive to the needs of society. Desai and Dharmapala (2006) argue that, CSR could potentially influence tax aggressiveness in terms of how firms account and direct their systems and processes with regards to the welfare of society as a whole. Christensen and Murphy (2004) also assert that, companies’ attitude towards CSR legitimately influences their decisions on the extent of and preparedness to reducing their tax liability. However, the direction of association continues to be a subject of academic and public discourse.

The ethical theory of CSR suggest that, companies in taking an action or by engaging in an activity must not only take into account the economic benefits, but also the other externalized impacts of their actions. For this reason and the fact that taxes are used, in part, for governmental infrastructure and social programs, a firm's strategy to reduce or avoid its taxes (that is, engage in tax avoidance) may benefit shareholders, but may also be at the expense of society (Sikka, 2010). According to Christensen and Murphy (2004), tax avoidance enables companies to enjoy the benefits of corporate citizenship without accepting the costs, cause harmful market distortions and transfer a larger share of the tax burden on to individual tax payers and consumers. Again, tax avoidance practice is an opportunistic way through which firms exploit the implicit contract between the firm and society at the expense of the latter. Tax avoidance practices are thus, costly to society and widely viewed as unethical and irresponsible by the public, society and other stakeholders. In this view, tax avoidance is positively associated with irresponsible CSR activities since it is inconsistent with CSR.

On the other hand, CSR activities are considered as a risk management strategy that a firm uses to enhance its CSR reputation (Hoi et al., 2013). Tax avoidance practices may lead to severe negative sanctions such as loss of firm/executive reputation and increased political/ media pressure when detected (Hanlon and Slemrod, 2009; Wilson, 2009). Accordingly, in order for firms to manage the expected cost associated with tax avoidance practices, firms could manage their reputation by increasing their CSR activities or reduce any irresponsible behaviour (Godfrey, 2005). This connotes that, firms engage in CSR because they employ tax avoidance schemes, which society may consider irresponsible behaviour by firms. Lanis and Richardson (2012) using 408 publicly listed Australian corporations, find a negative association between CSR disclosure levels and effective tax rates that is, firms with more social investment are less likely to be tax aggressive.

They argue that, CSR activities relate to tax avoidance decisions. Hoi et al. (2013) study on the CSR and tax avoidance practices of 2,620 US firms from 2003 to 2009 found out that those firms with excessive irresponsible CSR activities have a higher probability of engaging in tax-sheltering activities and greater discretionary/permanent book-tax differences. They, therefore, suggest that firms with excessive irresponsible CSR activities are more aggressive in avoiding taxes. Watson (2011) examines the relationship between CSR and tax aggressiveness using unrecognized tax benefit (UTB) disclosures and show that, socially irresponsible firms have larger total UTBs than socially conscious firms, indicating greater tax aggressiveness. This evidence suggests that, CSR activities reduce tax avoidance practices of firms. Lanis and Richardson (2012) used a unique sample of 20 Australian corporations accused by the Australian Taxation Office of engaging in tax aggressive activities during 2001 to 2006. Their study shows a positive and statistically significant association between corporate tax aggressiveness and CSR disclosure, thereby confirming legitimacy theory in the context of corporate tax aggressiveness. The inconsistent results of these limited studies, coupled with the over concentration of the studies in developed country and economy setting calls for further studies into this missing link of CSR and tax avoidance.

Tax avoidance and earnings management

Corporate tax avoidance has received much attention over the last two decades and more recently, because of the perceived resurgence in corporate tax avoidance activities (Dyreng et al., 2008). Although, there is widespread interest and concern over the extent, causes and consequences of corporate tax avoidance, there is no universally accepted definition of or constructs for tax avoidance (Hanlon and Heitzman, 2010). Tax avoidance means different things to different people. In the view of Preuss (2010), tax avoidance is a way of promoting the use of complex transactions to provide tax benefits that are inadvertent by the tax laws. Hanlon and Heitzman (2010) define tax avoidance broadly as the reduction of explicit taxes. Their definition reflects all transactions that have any effect on the explicit tax liability of firms, which includes real activities that are tax-favoured, avoidance activities specifically undertaken to reduce taxes, and targeted tax benefits from lobbying activities. Both delineations suggest that, tax avoidance could be strategically planned or consequential from the tax regulations.

However, prior literature have mostly seen tax avoidance behaviour as an outcome of positive book-tax difference1 and low effective tax rates (Kim et al., 2011).

Traditional research view tax avoidance as a value-maximizing activity that transfers wealth from the state to corporate shareholders. Managers of companies assume tax avoidance activities only to reduce corporate tax obligations. Thus, in the view of investors, tax avoidance is value enhancing, and so managers who engage in these activities ought to be motivated and compensated (Kim et al., 2011). While this view also identifies the likely costs associated with tax avoidance such as the potential risk of detection by tax authorities, it overlooks the implications of the agency problems in modern corporations due to separation of ownership and control.

Another view, which incorporates more dimensions of agency problems in firms, has also emerged in recent studies (Chen, 2005; Crocker and Slemrod, 2005; Slemrod, 2004). Slemrod (2004) asserts that, risk-neutral shareholders expect managers to focus on profit maximization, which include opportunities to reduce tax liabilities. However, separation of ownership and control can lead to corporate tax decisions that reflect the private interests of the manager (Hanlon and Heitzman, 2010). In the view of agency theory framework, tax avoidance activities can facilitate managerial opportunism and resource diversion (Chen et al., 2010; Desai and Dharmapala, 2009). Desai and Dharmapala (2009) contend that, tax avoidance activities can provide managers with the tools and justifications to engage in opportunistic behaviours and to pursue activities intended to mislead investors. Moreover, complex and opaque tax avoidance transactions can also increase the latitude for additional ways of rent diversion (Chen et al., 2010; Desai and Dharmapala, 2009) through the manipulation of earnings(Kim et al., 2011). Put in another way, tax avoidance and managerial diversion or opportunistic managerial behaviour can be complementary.

Extant studies have employed different measures for tax avoidance using data from publicly traded firms and tabulated tax returns to shed light on the phenomenon (Hanlon and Shevlin, 2005; Wilson, 2009). These earlier studies focused on annual report measures of avoidance. Others have also examined the stock market consequences of tax avoidance activities under the agency perspective. Desai and Dharmapala (2009) find no relation between tax avoidance and firm value but suggest that, tax avoidance is beneficial in an environment where monitoring and control effectively limit managerial opportunism provided by tax avoidance activities. Hanlon and Slemrod (2009) in their study of market reaction to news about a firm’s involvement in tax shelters, suggest that, investors are concerned about the possible interrelationship between tax shelters, managerial diversion and earnings manipulation as they find a negative market reaction to tax shelter disclosure.

Dhaliwal et al. (2004) study earnings management and GAAP effective tax rates (ETR), a proxy for tax avoidance, and provide evidence that firms lower the projected GAAP ETR from the third to the fourth quarter when the company would otherwise miss the analyst consensus forecast. They further explain that, even though managers lower accrued tax expense to meet analysts’ forecasts, a change in GAAP ETR could also result from tax planning transactions and tax avoidance behaviour. Desai (2003) also provide evidence on specific firms that engage in tax shelters with the sole aim of increasing accounting earnings.

1 Book-tax differences refers to the differences between incomes reported to the capital market and tax authorities.

Dhaliwal et al. (2004) study earnings management and GAAP effective tax rates (ETR), a proxy for tax avoidance, and provide evidence that firms lower the projected GAAP ETR from the third to the fourth quarter when the company would otherwise miss the analyst consensus forecast. They further explain that, even though managers lower accrued tax expense to meet analysts’ forecasts, a change in GAAP ETR could also result from tax planning transactions and tax avoidance behaviour. Desai (2003) also provide evidence on specific firms that engage in tax shelters with the sole aim of increasing accounting earnings.

METHODOLOGY

Data source

The study draws its sample from non-financial firms listed on the Ghana Stock Exchange (GSE) as well as non-listed firms from Ghana Revenue Authority (GRA) database. Series are yearly, covering a sample of 119 firms during the four-year period, 2010 to 2013. Due to the nature of the key variables of the study (CSR, Tax Avoidance and Earnings Management), the study excludes financial institutions due to the peculiar nature of their accruals and their need to meet other reporting requirements. Since the study focuses on tax avoidance, companies that are part of the Ghana Freezone board are excluded from the sample. Freezone companies in Ghana are legally exempted from paying taxes and as a result, the study cannot assess tax avoidance of such companies. Hence, to achieve uniformity, comparability and understandability of data collected and to reduce data distortion to the barest minimum, this study focuses on non-financial firms from GSE and GRA. Following Rohaya et al. (2008), loss-making firms are included in the study as firms’ earnings can be managed either upwards or downwards. This implies that tax avoidance practices may include recording transactions to incur losses. Thus, effective tax rate on loss-making firm is recorded as zero. The zero is then compared with the statutory rate of the year of loss, the difference is recorded as the tax avoidance figure.

Measurement of variables

To measure tax avoidance, the study employs the effective tax rate (ETR) methodology. This method compares the applicable statutory tax rate (STR) of the firms with the ETR. The unexplained excess of the STR over the ETR is considered as tax planning outcome. All things being equal, the wider the gap between the ETR and the STR (that is, STR> ETR), the higher the tax savings from tax planning. The ETR approach has been adopted by previous researchers including Gupta and Newberry (1997) and Rohaya et al. (2008). The strength of the ETR approach lies in the fact that the data required can be accessed without direct correspondence with the firm and the tax authorities.

Inger (2013) used a modified version of the ETR, called cash effective tax rate (CETR). He applied this to assess whether deferred tax expense has the potential of increasing the value of the firm. By this method, one measures the effective tax rate by using tax expenses paid (tax paid in the statement of cash flow) rather than using the total tax expense incurred for the period. This modification, in this study opinion, is suitable for studies that seek to ascertain the effect of the various tax planning components (namely, permanent tax differences, temporary tax differences, net operating losses, and foreign tax (differentials) on firm performance.

This study uses the ETR information to measure firms’ tax avoidance. Noor and Fadzillah (2010) compute the ETR as the total corporate tax expense divided by net profit before tax. This definition suggests that tax planning only seeks to minimize tax burden. Tax avoidance does not only seek to minimize tax burden but also to postpone payment of tax. To cater for the “deferment” objective of tax planning, it is necessary to modify the numerator as total tax expense less deferred tax expense. Thus, this study measures ETR as total corporate tax expense minus deferred tax expense and divide the result by Net profit before corporate tax. The comparable applicable statutory tax rate is arrived at after adjusting for all reliefs and rebates. The Internal Revenue Act, 2000 (Act 592) of Ghana contains reliefs and rebates that have the potential of reducing the general statutory rate of twenty five per cent (25%). It is therefore appropriate to adjust for these reliefs and rebates to enhance drawing of meaningful conclusion on the STR-ETR difference.

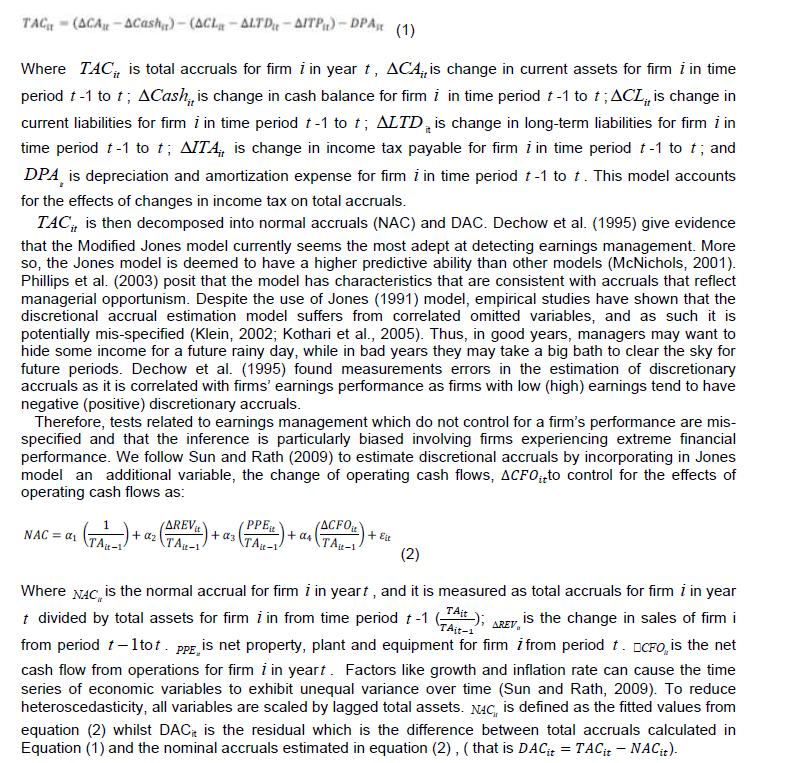

A fundamental element of any test for earnings management is a measure of the discretion the management has over earnings (Healy and Wahlen, 1999). Discretionary accrual (DAC) is, therefore, used as a proxy for earnings management. A widely used measure of earnings management is the ‘Jones model. Jones (1991) proposes the total accruals as a function of changes in revenue and levels of property, plant and equipment. The study employs the following model in estimating total accrual:

Three criteria have been used to measure CSR: expert valuation; content analysis of annual reports and other corporate documents; and performance in controlling pollution (McGuire et al., 1988). Each of these measures has proved difficult since no one standard measure has been agreed upon over the years. Hopkins (2005) however, proffers some means by which CSR can be measured, namely: the set of principles underlying CSR in any organization, the processes of CSR, and the outcome from being socially responsible. For this study, CSR is measured as a dummy variable that takes the value of one when a firm engage or undertakes CSR activities from human resources, environment, energy, fair business practices, community activities and product/consumer, health and safety viewpoint, and zero otherwise.

The study employs a number of additional control variables which prior studies have shown to affect the relationship of interest. The logarithm of total assets is employed as a proxy for firm size. Leverage is total debt scaled by total assets. Asset tangibility measures the physical property of the firm and it is employed as asset structure. Age measures the number of years the firm has been in existence and is used as a proxy for experience. Short-term fund is short-term debt scaled by total assets. Long-term fund is long-term debt scaled by total assets. Equity capital is used as a proxy to measure the degree of capitalization.

Estimation strategy: The dynamic panel model approach

A regression approach, which is the framework for testing the relationship among CSR, tax avoidance and earnings management, is developed. It first analyses whether the CSR increases (or decreases) earnings management. Second, whether the effect of CSR on earnings management and tax avoidance is dependent on the funding sources (equity and leverage) of the firm. The empirical model, which investigates these relationships, is:

EMPIRICAL RESULTS

Descriptive statistics

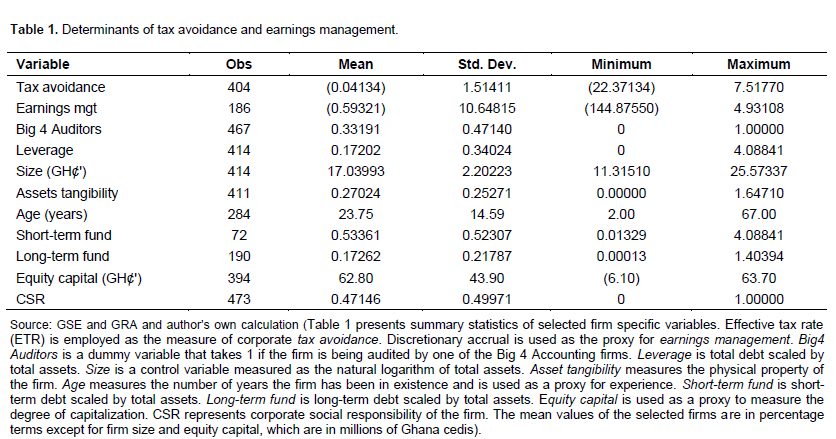

The summary statistics in Table 1 depicts an overall mean of -0.04134 with maximum and minimum values of 7.51770 and -22.37134 respectively for corporate tax avoidance (CTA). This indicates a presence of tax avoidance trait amongst sampled firms. However, it is observed that although there is an indication of tax avoidance, sampled firms do not aggressively engage in it. This is evidenced by the record of negative values for the overall means and minimum value. EM has an overall mean of -0.59321 and a standard deviation of 10.64815. The minimum and maximum values are -144.87550 and 4.93108 respectively.

This also denotes a presence of EM amongst sampled firms. Similar to tax avoidance, although there is a presence of EM among sampled firms, not every firm aggressively engages in the practice of managing earnings. This is also evidenced in the record of negative values for the overall mean and minimum values. A high standard deviation of 10.64815 is observed indicating great variations among firms with respect to their EM behaviours. This may indicate that some firm specific characteristics play important role when it comes to decisions of management to engage in earnings manipulative behaviour. CSR on the other hand has an overall mean of 0.47146 and an overall variation of 0.49971. The variable also has an overall maximum value of 1.00000 with no registered minimum values. These results present evidence of the existence of CSR activities among sampled firms over the sampled period. Unlike CTA and EM, CSR has low maximum value but registers no negative values. This shows that CSR is quite popular among all sampled firms. They may not aggressively engage in it but majority of the firms do undertake some form of CSR activities.

With respect to the control variables, presence of big 4 audit firms registered an overall mean of 0.33191 with a standard deviation of 0.47140. The maximum and minimum values were 1.0000 and 0.0000 respectively. This implies that quite a number of them employ the services of the big 4 audit firms. Leverage has an overall mean of 0.17202 with maximum value of 4.08841 and 0.000 minimum value. Leverage is scaled down by total assets hence the high maximum result indicate that some of the firms are highly geared whiles the low minimum indicates that some firms on the other hand do not use leverage as a source of capital financing. Firm size has an overall mean of 17.03 million cedis with a standard deviation 2.20 million cedis. The maximum and minimum values are 25.57 million cedis and 11.31 million cedis respectively. This indicates that sampled firms were mostly large firms. An overall mean of 23 years with maximum and minimum values of 67 years and 2 years respectively was registered for firm age. The high standard deviation depicts a high disparity of the age distribution of sampled firms. Some firms were as old as 67 years and as new as 2 years. With respect to equity financing, the descriptive indicates that on the average, sampled firms employ equity of about GHS 62.8 million to finance their business with the highest amount of equity being GHS 63.7 million and a minimum of -GHS6.11 million. Similar to the leverage, sampled firms are either aggressively using more equity and less leverage or utilising leverage aggressively and little or no equity.

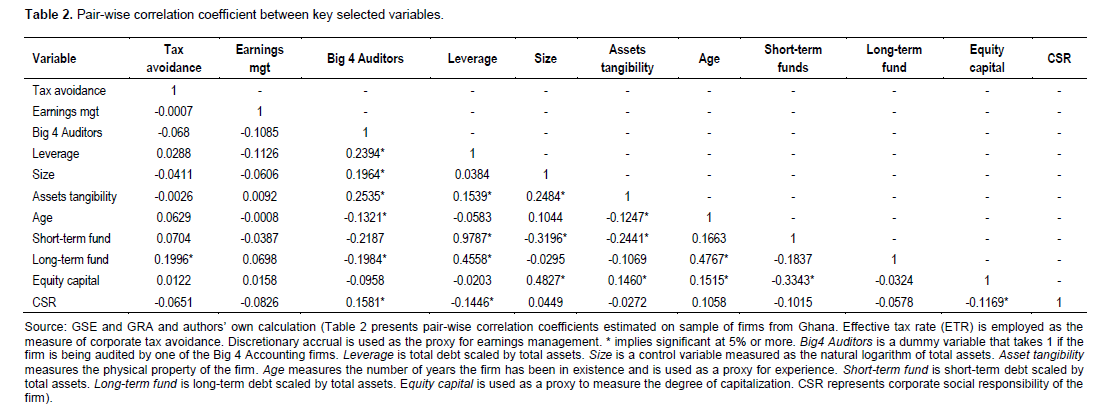

The correlation matrix as depicted in Table 2 shows the relationships among the dependent and independent variables. It shows a negative relationship between EM and tax avoidance. The relationship is however insignificant. The negative relations is contrary to prior findings which indicate a positive and complementary relationship between the two (Desai and Dharmapala, 2009b). CSR also registered a negative insignificant relationship with tax avoidance and a negative insignificant relationship with EM. The negative relationship between CSR and EM is similar to prior findings by Chih et al. (2008) who find a negative relationship between CSR and earnings smoothing. The findings is, however, contrary to prior findings (Kim et al., 2012; Gargouri et al., 2010; Prior et al., 2008) which found a positive relationship between CSR and EM and advance that the better the advancements in CSR activities in a firm.

Evaluation of firm tax avoidance and earnings management

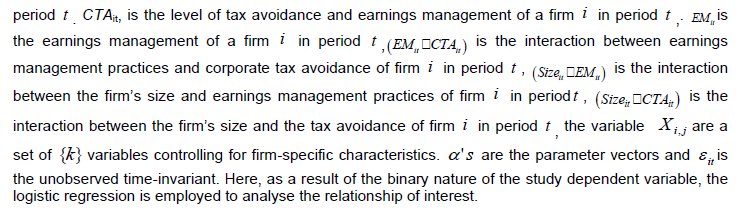

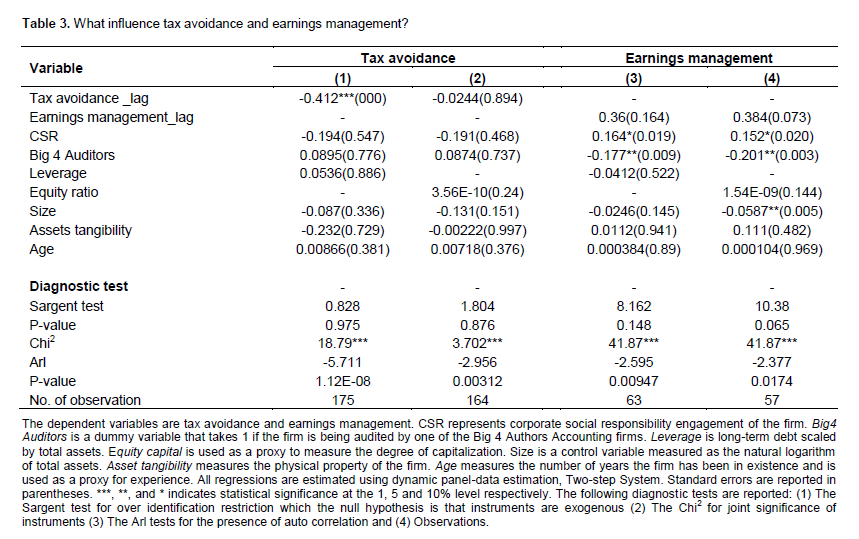

This section analyses how tax avoidance and earnings management are related to the CSR, and the funding strategies of sampled firms in Ghana. Table 3 presents the regression result that has CTA and EM as the dependent variables. The different models relate to different empirical approaches to funding sources (debt and equity) as well as the other explanatory variables. Model 1 and 2 assess the relationship between CSR and CTA while model 3 and 4 assess the relationship between EM and CSR. All regressions are estimated using dynamic panel-data estimation, Two-step System GMM, Windmeijer-correct standard error, small-sample adjustments, and orthogonal deviation.

On the relationship between CTA and CSR, the results indicate that CSR has a negative relationship with CTA. However, the relationship is considered statistically insignificant. The negative relationship indicates that firms who engage in CSR activities avoid less taxes. The regression results, therefore, confirm the provisions of the ethical theory of CSR, which suggests that companies in taking action should not consider only the economic benefits but also the other externalised impacts of their actions. Corporate tax payments has, therefore, been considered as the most fundamental way in which companies engage with the broader society (Christensen and Murphy, 2004). Christensen and Murphy (2004) argue that tax avoidance allows firms to benefit from society without accepting costs and thus, provides an opportunistic way through which firms exploit the implicit contract between the firm and society. Hence, increased avoidance can therefore be associated with irresponsible CSR and vice versa. An instance is where firms knowing the negative consequence of aggressive avoidance behaviours try to enhance their reputation by increasing CSR activities and reducing irresponsible behaviour (Godfrey, 2005). Thus, the regression output revealing a negative relationship implies that sampled firms’ CSR activities are slightly moved by ethical consideration, acknowledging that one important means they can affect society is by avoiding less taxes.

The negative relationship is confirmed when leverage which is a control in the first model is removed and equity variable introduced in the second model. However, the insignificance of the negative relationship reduces with the introduction of equity. Leverage has a positive insignificant relationship with CTA in model 1, so does Equity in model 2. The relationship between CSR and CTA remains the same even when leverage and equity are switched in models 1 and 2. This may imply that the relationship between CSR and CTA remains negative irrespective of capital structure. Thus, firms’ capital structure plays little role when it comes to the relationship between CSR and CTA. The result also indicates a significant negative relationship between CTA of the previous year and CTA of the current year. This implies that when firms are aggressively avoiding taxes in a current year, they are less likely to avoid more taxes in the subsequent year.

The result on the relation between EM and CSR is also depicted by model 3 and 4 in Table 3. The results indicate that CSR has a positive relationship with EM. The positive relationship is statistically significant at 10%. The result implies that increased CSR activities are associated with increased EM. This finding is consistent with the findings of prior researchers (Kim et al., 2012; Gargouri et al., 2010; Prior et al., 2008) who found a positive significant relationship between CSR and EM and advance that the better the advancements in CSR activities in a firm, the more the firm engages in EM. This assertion can be explained by the agency theory, which suggests that managers opportunistically use CSR as a cover up for their corporate misconducts (Kim et al., 2012; McWilliams et al., 2006; Hemingway and Maclagan, 2004). Prior researchers contend that managers may pursue CSR for their own self-interest at the detriment of the firm and its stakeholders.

The result is however contrary to the findings of Chih et al. (2008) who found a negative relationship between CSR and earnings smoothing. Their results indicate on the contrary that, increased CSR activities are associated with less earnings smoothing. This, thus, implies that sampled firms may use CSR as a cover for engaging in opportunistic behaviour such as earnings management. This may provide explanation for the insignificant level of the negative relationship between CSR and tax avoidance. The results imply that sampled firms may have more incentives to cover up their opportunistic behaviours and corporate misconducts with their CSR activities than they will have for ethical reasons.

The positive relationship remains significant when leverage in model 3 is replaced with equity in model 4. Leverage has a positive insignificant relationship with EM in model 3, whiles Equity has a positive but insignificant relationship with EM in model 4. The relationship between CSR and EM remains the same even when leverage and equity are switched in models 3 and 4. This may imply that the relationship between CSR and EM remains positive irrespective of capital structure thus the capital plays little role when it comes to the relationship between CSR and EM. The result also indicates a positive relationship between EM of previous year and EM of the current year. The positive relations become significant in model 4. This implies that the success of the manipulative activities of previous years have a positive impact on the manipulative behaviour of management in the current period. Firm size was also found to have a negative relationship with EM and this relationship becomes significant in model 4. The negative relationship implies that bigger firms are less likely to engage in EM. This is consistent with prior findings that large firms are less likely to engage in earnings management due to more scrutiny by investors and financial analyst (Zhou and Elder, 2002). It is, however, inconsistent with other findings such as the findings of Lobo and Zhou (2006) which suggest that larger firms may be more inclined to manage their earnings because of the complexity of their operations, which makes it difficult for users to detect misstatements.

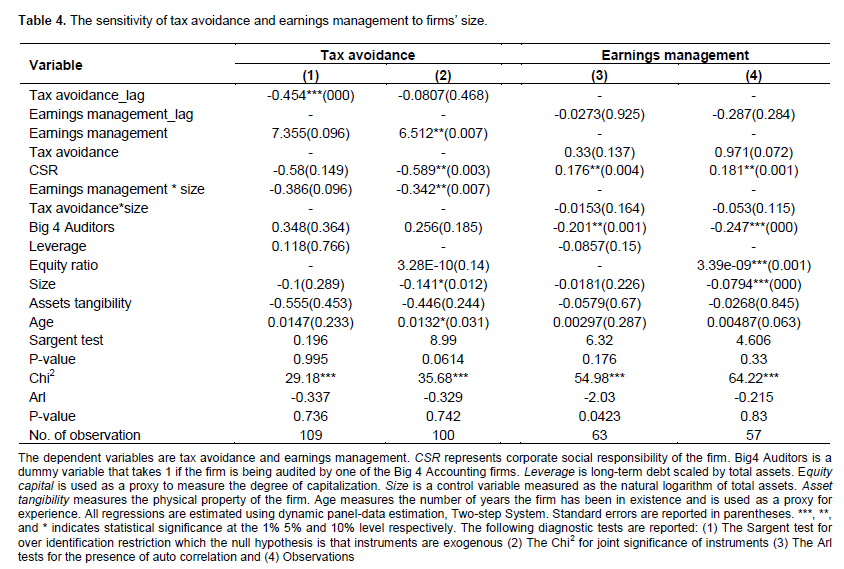

Table 4 analyses the relation between CTA and EM and the interaction of size with the funding source. Similar to Table 3, Table 4 is made up of 4 models. In models 1 and 2, CTA is the dependent variable while models 3 and 4 have EM as the dependent variable. In models 1 and 2, with tax avoidance as the dependent variable, it is found that EM has a positive significant relationship with CTA. The positive significant relationship is maintained when EM is used as the independent variable as presented in models 1 and 2. The positive relationship between CTA and EM in all 4 models implies that increased manipulative activities results in more avoidance activities and vice versa. This is consistent with the link between EM and CTA as revealed by prior researchers such as (Desai and Dharmapala, 2006a; Desai and Dharmapala, 2009b, 2007). They argue that avoidance and manipulative techniques are complementary and are bundled together such that increases in one activity results in increases in another. This relationship can be explained by the agency theory, which also asserts that individuals are self-interested people who seek to maximise their interest at any point. This means that managers will seek their self-interest at the expense of shareholders resulting in conflict of interest between managers and shareholders. The conflict of interest can lead managers into taking such corporate tax decisions that reflect their private interests (Scholtens and Kang, 2013; Prior et al., 2008; Slemrod, 2004). Both models control for CSR and the results re-affirms the relationship as analysed in Table 3.

The relationship between CTA and EM remains positive with the introduction of the interaction term between firm size and EM and between firm size and CTA. When interaction between firm size and EM is introduced into model 2 along with equity financing, the relationship between EM and CTA changes from insignificantly positive to significantly positive. Firm size has a negative relationship with tax avoidance. This implies that bigger firms are less likely to engage in avoidance activities. Since bigger firms engage less in avoidance activities, then it may stand to reason that any attempt to manage earnings will be done through other means other than through engaging in more avoidance activities. This observation is contrary to claims that CTA and EM have complimentary techniques as it indicates that firms can engage in EM without necessarily avoiding more taxes. The negative relationship between CSR and CTA is maintained when EM is introduced into the model 1 and in model 2. The positive relationship between CSR and EM is also maintained in model 3 and 4 when tax avoidance is introduced into the models. Firm size also has a negative relationship with EM. In model 3 the relationship is insignificant. The negative relationship however turns significant in model 4 when the interaction term between firm size and CTA is introduced in model 2. The interaction between firm size and CTA also has a negative insignificant relationship with EM. The interaction result reveals that those big firms who engage less in tax avoidance are less likely to use avoidance techniques to manage earnings.

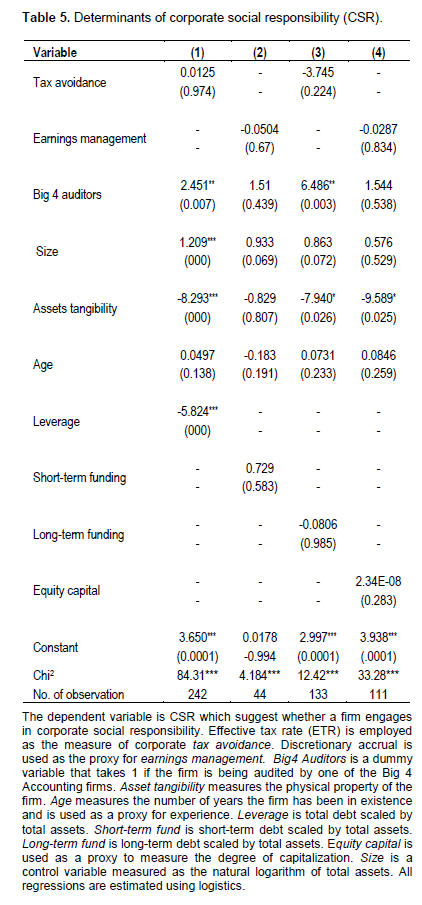

After analysing the relationship between the CTA and EM on one hand and CSR and the funding sources of firms on the other, next is a consideration of how CSR is affected by the CTA and EM. Table 5 analyses the relationship between CTA, EM and CSR with CSR serving as the dependent variable in all 4 models. We are interested in establishing whether firms in Ghana manipulate earnings and avoid tax in order to finance and engage in CSR. Here, the logistic regression is employed to analyse the relationship of interest. The results show that the relationship between CTA and CSR is positive in model 1, but the relationship changes to negative when long-term debt financing is introduced in model 4 and the insignificance improves. This means that the relationship is more negative than positive confirming the relationship as examined in Table 3. The relationship between EM and CSR however turns negative which is contrary to the results of Table 3 where the relationship is seen to be positive. The relationship remains negative with the introduction of equity variable into the relationship in model 4. The negative relationship implies that EM activities results in less CSR. This relationship though has a different direction from that of the relationship in Table 3. Both results can be interpreted that firms that engage in EM use CSR as a cover up, otherwise they will not engage less in responsible CSR when they are engaged in EM activities.

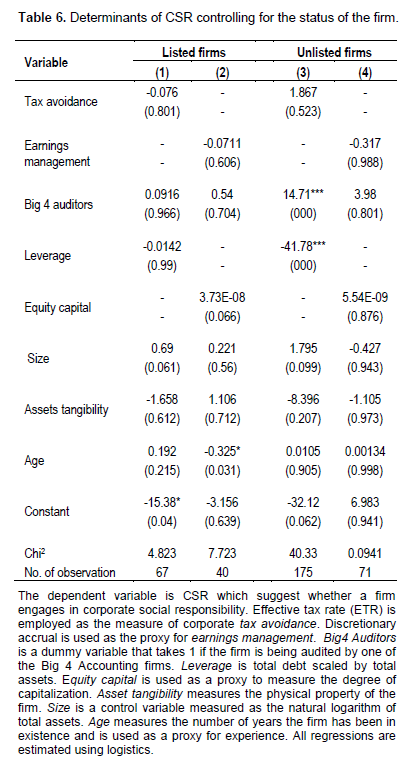

Table 6 explores the relationship between CTA, EM and CSR as it pertains to listed and non-listed firms. When the sample was separated into listed and non-listed firms, the result on the relationship between CSR and CTA remains a negative relationship for listed firms but becomes positive for non-listed firms. This implies that listed firms are less likely to engage in avoidance activities and engage more in ethical CSR. Non-listed firms on the other hand have more incentives to engage more in CTA and use CSR as a cover up. On the relationship between EM and CSR, the results reveal a negative relationship for both listed and non-listed firms. This implies that for both firms, an increase in manipulative behaviours does lead to increases in CSR activities. This indicates that although firms, irrespective of their status, either listed or non-listed engage in EM activities, they may not necessarily resort to CSR as a cover up. They are likely to engage in other activities as cover up if need be and not necessarily resort to CSR. Generally, it can be asserted from the insignificance of the relationships among CTA, EM and CSR that CTA and EM do not have any statistically significant impact on CSR. This result ultimately contradicts claims that firms engage in CSR as cover up for their manipulative behaviour (Kim et al., 2012; McWilliams et al., 2006; Hemingway and Maclagan, 2004).

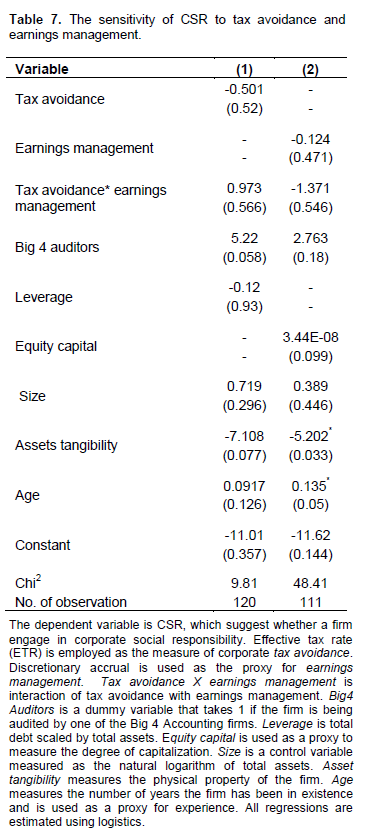

The sensitivity CSR to tax avoidance and earnings management

Table 7 analyses the overall impact of the interaction between CTA and EM on CSR. Model 1 analyses the relationship between CTA and CSR, the relationship remains negative with the introduction of the interaction between CTA and EM. The interaction between CTA and EM has a positive influence on CSR. This implies that although those who engage in less CTA are more likely to engage in CSR, when these firms avoid more taxes as a way of manipulating earnings, they are likely to resort more to CSR as a cover up and divert public attention away from their corporate misconduct (Hemingway and Maclagan, 2004). Model 2 analyses the relationship between EM and CSR, the relationship is negative and remains negative with the introduction of the interaction between CTA and EM. The relationship between the interaction term and CSR is also negative. This implies that firms that engage in more earnings management engage less in responsible CSR.

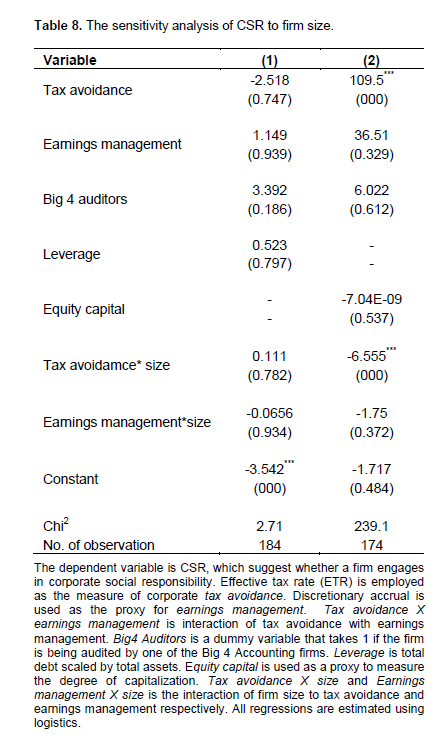

Table 8 on other hand, analyses the relationship between CTA and EM and CSR and introduces the interaction between firm size and CTA and then the interaction between firm size and EM in models 1 and 2. The relationship between both interaction terms and CSR is positive. This is similar to the results in Table 2. The interaction result reveals that those big firms who engage less in tax avoidance are less likely to use avoidance techniques to manage earnings. The same can be said for the relationship between the interaction between firm size and EM and CSR, which implies that bigger firms that engage in earnings management are less likely to resort to CSR as cover up for their corporate misdeeds.

CONCLUSION

The study investigates the relationship between CTA and EM, the relationship between CSR and EM, and how EM activities and tax avoidance practices jointly influence corporate social behaviour. The study draws its sample from non-financial firms listed on the GSE as well as non-listed firms from GRA database. The study employs system methods of moments (GMM) and logistic regression to establish whether firms in Ghana manage earnings and avoid tax to finance CSR.

The results show the existence and growth of EM among sampled firms. This indicates that sampled firms use flexibility in financial accounting to influence reported earnings. The existence of tax avoidance among sampled firms implies that some private benefit exists for managers engaging in such avoidance activities. There is evidence to suggest that firms in Ghana actively engage in CSR activities. On the relationship between CSR and CTA, the result reveals a statistically insignificant negative relationship, which implies that firms who engage in CSR activities avoid taxes less. Even though the result is insignificant, the negative coefficient suggests that CSR activities are slightly moved by ethical consideration and sampled firms see avoiding less taxes as one important means by which they can affect society. The result also shows that increased CSR activities are associated with increased EM. This suggests that sampled firms may use CSR as a cover for engaging in opportunistic behaviour such as earnings management.

Additionally, a positive significant relationship is found between EM and CTA. This implies that increased manipulative activities results in more avoidance activities and vice versa. This suggests that although firms wish to undertake CSR for ethical reasons, CSR provides more leverage when it is used as a cover up for managerial opportunistic behaviours. Our results also reveals that firm size has a negative relationship with tax avoidance implying that bigger firms are less likely to engage in avoidance activities. Firm size also has a negative relationship with EM. The study suggests that those big firms who engage less in tax avoidance are less likely to use avoidance techniques to manage earnings. When the sample was separated into listed and non-listed firms, the result on the relationship between CSR and CTA remains a negative relationship for listed firms but becomes positive for non-listed firms. This implies that listed firms are less likely to engage in avoidance activities and engage more in ethical CSR. Non-listed firms on the other hand have more incentives to engage more in corporate tax avoidance and use CSR as a cover up.

On overall impact of the interaction between CTA and EM on CSR, the study reveals that although sampled firms who engage in less CTA are more likely to engage in CSR, when these firms avoid taxes more, as a way of manipulating earnings, they are likely to resort more to CSR. This they do to cover up and to divert public attention away from their corporate misconducts than for ethical reasons. The study also reveals that bigger firms that engage in EM are less likely to resort to CSR as cover up for their corporate misdeeds.

These results give rise to two public policy implications: First, the study is important because it is conducted in the context of a developing country where the capital market is relatively undeveloped and taxation is the main source of government financing. Such a study is relevant because of the magnitude of problems and harmful effects associated with EM, CSR and CTA practices, which can affect the fundamentals of the capital markets in emerging economies and developing countries. Secondly, the recent changes in financial reporting standards, coupled with the calls for prudential regulations in Ghana have increased the effect of perception and reporting behaviour of firms.

This study therefore provides insight into the subject area from a different perspective. Private and public sector organisations as well as policy and regulatory authorities in Ghana would benefit from having a scientific insight into a CSR, EM and CTA study in Ghana.

CONFLICT OF INTERESTS

The authors have no any conflict of interest issues related to this paper.

ACKNOWLEDGEMENT

The authors would also like to thank the University of Ghana for funding this research.

REFERENCES

|

Alvarez J, Arellano M (2003). The time series and cross-section asymptotics of dynamic panel data estimators. Econometrica 1121-1159. |

|

|

Atkins B (2006). Is Corporate Social Responsibility Responsible? Directorship. (accessed 06-12-14). |

|

|

Bansal P, Roth K (2000). Why companies go green: A model of ecological responsiveness. Neo-empiricism: inductive research methodologies. Acad. Manag. J. 43(4):717-736. |

|

|

Ball R, Shivakumar L (2005). Earnings quality in UK private firms: comparative loss recognition timeliness. J. Account. Econ. 39(1):83-128. |

|

|

Blundell R, Bond S (1998). Initial conditions and moment restrictions in dynamic panel data models. J. Econ. 87(1):115-143. |

|

|

Carroll AB (1979). A Three-Dimensional Conceptual Model of Corporate Performance. Acad. Manage. Rev. 4(4):497-505. |

|

|

Cespa G, Cestone G (2007). Corporate social responsibility and managerial entrenchment. J. Econ. Manage. Strategy 16(3):741-771. |

|

|

Chen KP (2005). Internal Control versus External Manipulation: A Model of Corporate Income Tax Evasion. Rand. J. Econ. 36(1):151-164. |

|

|

Chen X, Chen S, Cheng Q, Terry S (2010). Are family firms more tax aggressive than non-family firms? J. Fin. Econ. 95(1):41-61. |

|

|

Chih HL, Shen CH, Kang FC (2008). Corporate social responsibility, investor protection, and earnings management: Some international evidence. J. Bus. Ethics 79(1-2):179-198. |

|

|

Choi TH, Pae J (2011). Business ethics and financial reporting quality: evidence from Korea. J. Bus. Ethics 103(3):403-427. |

|

|

Christensen J, Murphy R (2004). The social irresponsibility of corporate tax avoidance: Taking CSR to the bottom line. Development 47(3):37-44. |

|

|

Crocker KJ, Slemrod J (2005). Corporate tax evasion with agency costs. J. Public Econ. 89(9/10):1593-1610. |

|

|

Dechow PM, Sloan RG, Sweeney AP (1995). Detecting earnings management. Account. Rev. 193-225. |

|

|

Desai MA (2003). The divergence between book income and tax income. Tax Policy. Econ. 17:169-206. |

|

|

Desai MA, Dharmapala D (2006). CSR and taxation: The missing link. Leading Perspectives (Winter) 4(5). |

|

|

Desai MA, Dharmapala D (2007). Taxes and portfolio choice: evidence from JGTRRA's treatment of international dividends. National Bureau of Economic Research. |

|

|

Desai MA, Dharmapala D (2009). Earnings Management, Corporate Tax Shelters, and Book-Tax Alignment. Natl. Tax. J. 62(1):169-186. |

|

|

Dhaliwal DS, Gleason CA and Mills LF. (2004) Lastâ€Chance Earnings Management: Using the Tax Expense to Meet Analysts' Forecasts. Contemp. Account. Res. 21(2):431-459. |

|

|

Dyreng SD, Hanlon M, Maydew EL (2008). Long-run corporate tax avoidance. Account. Rev. 83(1):61-82. |

|

|

Gargouri RM, Shabou R, Francoeur C (2010). The relationship between corporate social performance and earnings management. Can. J Adm. Sci. 27:320-334. |

|

|

Garriga E, Melé D (2004). Corporate Social Responsibility Theories: Mapping the Territory. J. Bus. Ethics 53(1/2):51-71. |

|

|

Godfrey PC (2005). The relationship between corporate philanthropy and shareholder wealth: A risk management perspective, Acad. Manage. Rev. 30(4):777-798. |

|

|

Gupta S, Newberry K (1997). Determinants of the Variability of Corporate Effective Tax Rates: Evidence from Longitudinal Data. J. Account. Public. Policy 16: 1-34. |

|

|

Hanlon M, Heitzman S (2010). A review of tax research. J. Account. Econ. 50(2/3):127-178. |

|

|

Hanlon M, Shevlin T (2005). Book tax conformity for corporate income: an introduction to the issues. Tax Policy Econ. 19:101-134. |

|

|

Hanlon M, Slemrod J (2009). What does tax aggressiveness signal?: evidence from stock price reactions to news about tax shelter involvement. J. Public. Econ. 93(1/2):126-141. |

|

|

Healy PM, Wahlen JM (1999). A review of the earnings management literature and its implications for standard setting. Account. Horiz. 13(4):365-383. |

|

|

Hemingway CA, Maclagan PW (2004). Managers' Personal Values as Drivers of Corporate Social Responsibility. J. Bus. Ethics. 50(1):33-44. |

|

|

Hoi CK, Wu Q and Zhang H. (2013) Is corporate social responsibility (CSR) associated with tax avoidance? Evidence from irresponsible CSR activities. Account. Rev. 88(6):2025-2059. |

|

|

Hong Y, Andersen ML (2011). The relationship between corporate social responsibility and earnings management: An exploratory study. J. Bus. Ethics. 104(4):461-471. |

|

|

Hopkins M (2005). Measurement of corporate social responsibility. Int. J. Manag. Decis. Mak. 6(3-4): 213-231. |

|

|

Inger KK (2013). Relative valuation of alternative methods of tax avoidance. J. Am. Tax. Assoc. 36(1):27-55. |

|

|

Jones JJ (1991). Earnings management during import relief investigations. J. Account. Res. pp. 193-228. |

|

|

Kim JB, Li Y, Zhang L (2011). Corporate tax avoidance and stock price crash risk: Firm-level analysis. J. Financial. Econ. 100(3):639-662. |

|

|

Kim Y, Park MS, Wier B (2012). Is earnings quality associated with corporate social responsibility? Account. Rev. 87(3): 761-796. |

|

|

Klein A (2002). Audit committee, board of director characteristics, and earnings management. J. Account. Econ. 33(3):375-400. |

|

|

Kothari SP, Leone AJ, Wasley CE (2005). Performance matched discretionary accrual measures. J. Account. Econ. 39(1):163-197. |

|

|

Laksmana I, Yang YW (2009). Corporate citizenship and earnings attributes. Adv. Account. 25(1):40-48. |

|

|

Lanis R, Richardson G (2011). The effect of board of director composition on corporate tax aggressiveness. J. Account. Public Policy 30(1):50-70. |

|

|

Lanis R, Richardson G (2012). Corporate social responsibility and tax aggressiveness: An empirical analysis. J. Account. Public. Pol. 31(1):86-108. |

|

|

Leuz C, Nanda D, Wysocki PD (2003). Earnings management and investor protection: an international comparison. J. Fin. Econ. 69(3):505-527. |

|

|

Lin C, Yang H, Liou D (2008).The impact of corporate social responsibility on financial performance: evidence from business in Taiwan. Technol. Soc. 30:1-8. |

|

|

Lobo GJ, Zhou J (2006). Did conservatism in financial reporting increase after the Sarbanes-Oxley Act? Initial evidence. Account. Horiz. 20(1):57-73. |

|

|

McGuire JB, Sundgren A, Schneeweis T (1988). Corporate social responsibility and firm financial performance. Acad. Manage. J. 31(4):854-872. |

|

|

McNichols MF (2001). Research design issues in earnings management studies. J. Account. Public Policy 19(4):313-345. |

|

|

McNichols MF, Stubben S (2008). Does Earnings Management Affect Firms' Investment Decisions? Account. Rev. Forthcoming. |

|

|

McWilliams A, Siegel DS, Wright PM (2006). Introduction by Guest Editors Corporate Social Responsibility: International Perspectives. J. Bus. Strategy 23(1):1. |

|

|

Murphy K (2004). The Role of Trust in Nurturing Compliance: A Study of Accused Tax Avoiders. Law. Hum. Behav. 28(2):187-209. |

|

|

Noor RM, Fadzillah NSM (2010). Corporate tax planning: a study on corporate effective tax rates of Malaysian listed companies. Int. J. Trade. Econ. Fin. 1(2):189. |

|

|

Phillips J, Pincus M, Rego SO (2003). Earnings management: New evidence based on deferred tax expense. Account. Rev. 78(2):491-521. |

|

|

Preuss L (2010).Tax avoidance and corporate social responsibility: You can't do both, or can you? Corp. Gov. 10(4):365-374. |

|

|

Prior D, Surroca J, Tribó JA (2008). Are socially responsible managers really ethical? Exploring the relationship between earnings management and corporate social responsibility. Corporate Governance: An Int. Rev. 16(3):160-177. |

|

|

Reinhardt FL, Stavins RN, Vietor RHK (2008). Corporate social responsibility through an economic lens. Rev. Environ. Econ. Policy 2(2):219-239. |

|

|

Rohaya MN, Nor'Azam M, Barjoyai B (2008). Corporate effective tax rates: A study on Malaysian public listed companies. |

|

|

Roodman D (2009). A note on the theme of too many instruments*. Oxford Bull. Econ. Stat. 71(1):135-158. |

|

|

Ruf BM, Muralidhar K, Brown RM, Janney JJ, Paul K (2001). An Empirical Investigation of the Relationship between Change in Corporate Social Performance and Financial Performance: A Stakeholder Theory Perspective. J. Bus. Ethics 32(2):143-156. |

|

|

Scholtens B, Kang FC (2013). Corporate social responsibility and earnings management: Evidence from Asian economies. Corp. Soc. Rep. Environ. Manag. 20(2):95-112. |

|

|

Sikka P (2010) Smoke and mirrors: Corporate social responsibility and tax avoidance. Account. Forum. Elsevier. pp. 153-168. |

|

|

Slemrod J (2004). The economics of corporate tax selfishness. Natl. Tax. J. 57(4):877-899. |

|

|

Sun L, Rath S (2009). An empirical analysis of earnings management in Australia. Intl. J. Hum. Soc. Sci. 4(14):1069-1085. |

|

|

Waddock SA, Graves SB (1997). The Corporate Social Performance-Financial Performance Link. Strategic Manage. J. 18(4):303-319. |

|

|

Watson L (2011). Corporate social responsibility and tax aggressiveness: An examination of unrecognized tax benefits. 2011 American Taxation Association Midyear Meeting Paper: New Faculty/Doctoral Student Research Session. |

|

|

Wilson RJ. (2009) An examination of corporate tax shelter participants. The Account. Rev. 84(3): 969-999. |

|

|

Windmeijer F (2005). A finite sample correction for the variance of linear efficient two-step GMM estimators. J. Econ. 126(1):25-51. |

|

|

Zhou J, Elder R (2002). Audit firm size, industry specialization and earnings management by initial public offering firms. Syracuse University, Syracuse, NY and SUNY-Binghamton, Bingharnton, NY, Working Paper. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0