Full Length Research Paper

ABSTRACT

Even though Africa has constantly emphasized the need to reduce deficit financing through mobilization of more internal revenues, this has not been achieved. Perhaps encouraging voluntary tax compliance can improve internal revenue mobilization. This study explores the relationship between ethical orientation and tax compliance and finds that ethical persons are generally more tax compliant than unethical persons but are more influenced by considerations of tax rate and withholding positions compared to unethical persons. The findings of this study differ from Reckers et al. in a number of ways and contribute to the literature by providing a possible explanation of the cause(s) of tax non- compliance.

Key words: Taxation, non-compliance, ethics, tax rate, withholding position.

Abbreviation: JEL: H26; H27; H71.INTRODUCTION

Ghana practices a self-assessment system where, essentially, tax payers are legally obligated to declare their estimated tax liabilities (following prescribed formats) and settle the tax due accordingly (Terkper, 1995). Based on a risk management model and evidences provided on self-assessment forms, the Ghana Revenue Authority (GRA), which is the state body responsible for tax collection), may request for evidence or perform an audit to confirm submissions by tax payers. Following the opportunity to self-declare tax liabilities, self-assessments systems typically over compensate with higher penalties for default and under declarations, compared to other tax assessment systems.

The study aims to investigate the effects, if any, of individual ethical attitudes on tax compliance behavior. Bearing in mind the hypothesis that individual ethical attitudes influence choices on tax compliance behavior, then perhaps a good case is made for its inclusion in behavioral decision making models.

Tax collection has been a challenge for most low income countries and Ghana is no exception (Terkper, 1995). In Ghana, following the recent trend of excessive deficit financing and its attendant inflationary and other adverse pressures, the government of Ghana, pressured by various civil society groups have acknowledged the need to increase state sources of revenue especially from tax collection (Osei and Quartey, 2005). A focus of these efforts has been widening the tax net to cover previously untaxed segments, sectors and persons especially in the informal sector but as well in the formal sector. Also, government has heightened its efforts to stamp out tax evasion and enforce voluntary compliance through a complex set of carrot and stick approaches involving tax amnesties, penalties, concessions for voluntary disclosure, and public awareness campaigns.

In Africa, most evasion of taxes is mostly by individual and self-employed persons relative to organizations and institutions (Goerke, 2014); perhaps due to the fact that African economies are cash economies with a high number of small scale businesses within the informal sector (Delaney, 2013). Individuals exhibit diverse behaviors in tax compliance (Alm et al., 1992).

Concerns about and research on deterioration in voluntary compliance are as old as the institution of taxation itself. In recent times, studies about tax compliance has focused on the behavioral issues, particularly the development of models that can help predict the likelihood of tax evasion by tax payers and/or the decision making model that various tax payer groups use in guiding their decision on tax compliance behavior. Clotfelter (1983) confirms that, in most cases tax noncompliance increases with the tax rate and often non compliances decisions by a tax payer are interdependent.

Whereas it may seem obvious that individual differences, especially on ethical values may be an important element in decision making models on predicting tax compliance behavior, most decision making models on tax compliance have excluded considerations on individual ethical propensities (Reckers et al., 1994; Bobek and Hatfield, 2003). Rather, most studies have focused on the implications of tax rates and tax-payers consideration of the effects of their decisions (prospect framing theory) in making compliance decisions. Reckers et al. (1994) argue that the results of research into decision making models on tax compliance behavior are mostly inconclusive, perhaps due to the exclusion of personal ethical considerations of tax payers. Where efforts have been made to consider the effects of ethics in tax compliance behavior, the focus has been on general ethical considerations and social norms rather than individual ethical orientations of taxpayers (Henderson and Kaplan, 2005).

Admittedly, studies in other countries have confirmed that ethical considerations affect tax compliance behaviors (Henderson & Kaplan, 2005; Reckers et al., 1994). However, none of these studies, so far, has taken place in Ghana. Considering the fact that ethical considerations can be significantly influenced by culture (Collins and Plumlee, 1991; Alm et al., 1995), a study of the relationship between individual ethical attitudes and culture within the Ghanaian environment is equally relevant and adds to the growing body of literature on ethics. As well, it supports the need for a critical mass of literature relevant for theorization. The rest of the study is organized as follows; the next part reviews the related literature for ethics and behavioral studies on tax compliance; the following parts discuss the research methodology; results and conclusions respectively.

TAX COMPLIANCE BEHAVIOR AND ETHICS

Wenzel (2005) defines tax ethics as “one’s belief that there is a moral imperative that one should be honest in one’s tax dealings”.

Blasi (1980); Tooke and Ickes (1988) explored the relationship between ethical beliefs and behavioral choices and suggest that ethical behaviors tend to be contextual and case specific (Henderson and Kaplan, 2005). Haan (1975); Arrington and Reckors (1985), and Henderson and Kaplan (2005) argue that, to provide credible analysis, measures of ethical beliefs must be situation specific. Therefore, even though studies in other social disciplines have explored and confirmed that personal ethical considerations affect decision matrixes, the findings of such studies cannot be automatically assumed to hold in behavioral studies on tax compliance.

Following on from the deterrence theory and the classical economic theory of rational utility maximizing behavior, Smith and Kinsey (1987); Carroll (1992; 1987) suggest that tax payers do a cost-benefit-analysis of noncompliance by comparing the value of the marginal satisfaction from the monetary rewards of noncompliance with the potential cost and/or risk of sanctions (and other disutility) from non-compliance. This traditional economic model of decision making, suggests that tax payers choices are made solely from a perspective of self-interest (Hodgson, 1988). Therefore, the ‘rational pursuit’ of self-interest allows tax payers to consider taxation as a cost that they must avoid or reduce and hence a taxpayer is likely to evade tax unless the likelihood that he will be caught and the severity of punishment makes evasion an unattractive option (Wenzel, 2005). Proponents of this theory therefore argue that deterrence is an effective means of enforcing tax compliance (Allingham and Sandmo, 1972; Cowell and Gordon, 1988; Andreoni et al., 1998). Alm et al. (1992) and Henderson and Kaplan (2005) have however criticized the deterrence theory as being narrow and limited in its explanation power of the generally wide level of compliance among various taxpayers particularly as tax audits, and penalties for tax evasion, as well as the cost of other detection mechanisms are generally very low. Indeed studies on the impact of audit probabilities on tax compliance have provided weak and inconclusive results (Fischer et al., 1992; Slemrod et al., 2001; Spicer and Thomas, 1982; Mason and Calvin, 1978, Song and Yarbrough, 1978, Spicer and Lundstedt, 1976 and Wärneryd and Walerud, 1982). Evidence of the relationship between penalties (such as fines) and tax compliance also provides inconsistent results (Fischer et al., 1992; Park and Hyun, 2003; Friedland et al., 1978).

Wenzel (2005) and Henderson and Kaplan (2005) find that tax compliance is influenced by a complex mix of individual ethical propensities and other social norms (James et al., 2001; Tyler, 1990).

Etzioni (1988) proposes that ethical considerations and values are an interference with a moderating effect on the classical economic decision-making model of self-interest utility maximization. Scholz (1985) however contends that individual utility functions necessarily incorporate considerations of social responsibility as well as self-interested goals. Either-way ethical values affect the decision making process and can affect tax compliance decisions by causing tax payers to avoid non-compliance and illegal avoidance practices (Baldry, 1987, Jackson and Milliron, 1986; Trivedi et al., 2003).

Carroll (1987); Smith (1990); and Etzoini (1988) argue that an individuals’ ethical propensity affects tax compliance behavior by providing a broad framework of possibilities and boundaries from which choices can be made (Grasmick and Bursik, 1990; Reckers et al., 1994; Sheffrin and Triest, 1992). Therefore high ethical values affect the decision making process by limiting choices available to the tax payer as well as the process to be used to achieve a given outcome (Reckers et al., 1994) and hence may override a ‘rational’ consideration of self-interest utility maximization.

Kohlberg (1976) argues that each individual has a different set of ethical values. Therefore not all tax payers will view tax evasion with a high sense of morality (Reckers et al, 1994; Henderson and Kaplan 2005). Accepting Kohlberg’s (1976) proposal that individuals have different ethical propensities, tax payers can be assumed to differ on an ‘honesty characteristics’ and can be grouped into different categories (Clotfelter, 1983).

Hessing et al. (1992) for instance identify three types of tax payers; tax payers who never evade tax; tax payers who will occasionally try to evade tax; and tax payers who will regularly try to evade tax. Clotfelter (1983) confirms that evidence exists that some tax payers never evade tax.

Smith (1990) suggests that perhaps, compared to traditional economic considerations based on the deterrence theory, evidence exist to suggest that personal ethical values have a stronger effect on tax compliance behavior. Therefore, compared to deterrence factors, individual ethical beliefs have been confirmed to have a relatively more significantly verifiable relationship with tax compliance (Etzioni, 1988).

Effect of tax rate, income levels and outcome framing on tax compliance

Findings about the effect of tax rate on tax compliance have been mixed (Reckers et al, 1994). Clotfelter (1983) finds a positive relationship between the number of tax evaders and the rate of tax. Other studies have also confirmed a positive relationship between tax rates and tax payer non-compliance (Pommerehne and Weck-Hannemann, 1996; Weck-Hannemann and Pommerehne, 1989). However, Porcano (1988) and Baldry (1987) find no significant relationship between tax rates and tax compliance and Dubin and Wilde (1988) find an inverse relationship between tax rates and tax compliance. Since the applicable tax rate is determined by a person’s level of income, then the relationship between income levels and tax compliance is also inconclusive (Cox, 1984).

Alm et al. (1992); Yaniv (1999), Elffers and Hessing (1997) and Bernasconi and Zanardi (2004) propose that tax payer compliance can be explained with prospect theory.

Deterrence theory is based on a presumption of expected total utility where a tax payer is indifferent to a ‘reference point’ (Kahneman and Tversky, 1979) and makes tax compliance decisions based on an evaluation of absolute wealth rather than relative wealth specific to a situation. Unlike deterrence theory, prospect theory contends that tax payers will evaluate losses and gains from any compliance behavior differently and will often consider and/or react to the effects of gains separately from the effect of loses, even if they relate to the same transaction. Based on the prospect theory, tax-payers disutility for loss is generally higher than the perceived utility from gains and therefore typically, a tax payer will make more effort to avoid a loss than to increase gains. In the context of framing, taxpayers will be more averse to the risk of non-compliance in a situation where tax compliance leads to a refund than a tax payment. This is because tax payers, based on their ‘reference points’ are likely to consider refunds as gains and tax payments as a loss. In line with prospect theory Cox and Plumley (1988); Chang et al. (1987); Robben et al. (1990) and Carroll (1992) find evidence to suggest that voluntary compliance increases consistently with the amount of refund that taxpayers expect to receive after filing a tax return and decreases consistently with the amount of tax to be paid. Following prospects theory, Yaniv (1999) demonstrates empirically that advance tax payment can substitute for the costly detection efforts in enhancing tax compliance even though a deliberately high advance tax payment is unlikely to eliminate the incentives of noncompliance. Elffers and Hessing (1997) argue that when advance taxes are higher than the true tax liability, and considering that most tax payers evaluate gains and losses (even if the relate to the same transaction) differently, tax payers are likely to be tax compliant (risk averse) as they expect a gain (refund) from filing their return. In such a circumstance tax payers may opt to be risk averse and be as compliant as possible to benefit from a refund. In circumstances where advance tax payments are less than the true tax liability, tax, taxpayers perceive a loss arising from tax compliance and considering the fact that taxpayers are more sensitive to losses than to gains, taxpayers may become risk seeking and opt to be non- compliant with their tax obligation even if the amount of estimated ‘loss’ is very minimal.

Tversky and Kahneman (1982) argue that the prospect theory, even though relevant, is not completely universal and on occasions has provided inconsistent results (Robben et al., 1990; Hite et al., 1988; Schadewald, 1989) and only describes how some individuals will behave some of the time.

Reckers et al. (1994) argue that the inconsistent results from deterrence theory and the prospect theory, as well as the inconclusive findings on the relationship between tax rate and non-compliance could be because other considerations such as social norms, ethical consi-derations and personal characteristics are critical in understanding compliance behavior of tax-payers.

Like Recker et al. (1994), this study hypothesizes that an individual’s ethical beliefs plays a critical role in a Ghanaian tax payers decisions regarding compliance. Essentially, an individual’s ethical beliefs define the boundary of available choices to a tax payer and may have a moderating effect on prospect framing, deterrence mechanisms or expected utility. Therefore (a) different tax payers will react to similar scenarios differently based on their ethical orientation; and (b) the relationship between individual ethical orientation and tax compliance is more consistent than the relationship between tax rate and/or ‘withholding positions with compliance. Withholding position is conceptualized as the estimated gain (refund) or loss (tax due) by a tax payer based on a ‘reference point’.

METHODOLOGY

Most studies on ethics and tax behavior have been based on survey studies (Wenzel, 2005). Wenzel (2005) acknowledges the limitations of surveys in behavioral studies and proposes that experiments provide a more effective mechanism to obtain credible results. This study combines a survey methodology with an experimental task, in the form of a scenario to obtain relevant information of tax payer behavior. Scenarios are widely used in ethics study (Randall and Gibson, 1990) and provide an opportunity to measure multiple variables in decision making by respondents. All respondents were given a questionnaire comprising four sections. Section A requested for demographics of the respondents excluding any unique identification information such as names. Section B included a test instrument based on a scenario that involved a hypothetical case where a tax payer was presented with an opportunity to evade tax (adopted with modification from Reckers et al., 1994). In line with Madeo et al. (1987), a transaction with a relatively low level of detection (a cash transaction from a side job with an individual) was used to frame the opportunity for evasion. Respondents were asked to evaluate the action of the tax-payer on a seven point Likert scale ranging from strongly disagree (coded as 7) to strongly agree (coded as 1). Reckers et al. (1994) asked respondents tax payers if they will report appropriately if faced with a similar situation based on a hypothetical case. Specifically, Reckers et al. (1994) stated ‘If faced with an identical situation, I would report the $12,000 in income’ and required respondents to provide a response on a six point Likert Scale. There is a risk of socially desirable responses based on scenarios that personalizes an action especially if actual behavior is not being observed and respondents are relied on to be honest with their responses (Bampton and Cowton, 2002). To mitigate this risk, this study, as part of the hypothetical scenario enumerates a chosen course of action by the actor(s) within the scenario and rather requests respondents to state the extent to which they agree with the actions of the actor(s) within the scenario. The chosen course of action of the actor(s) within the scenario was to opt to evade tax and as such a response of strongly disagree (coded as 7) will suggest a respondent was unwilling to evade tax whereas a response on strongly agree (coded as 1) will suggest a respondent was willing to evade tax if faced with a similar scenario.

To confirm this analogy, a second question was framed in the manner of Reckers et al. (1994). Specifically respondents were asked to state their agreement or otherwise on a seven point Likert scale to the statement that ‘‘If faced with an identical situation, I would report the GHS2,000 in income’. Responses to this statement were only used to confirm the credibility of responses to the earlier question that required respondents to state their agreement or otherwise with the choice of action by the actors in the scenario.

Section C attempted to measure respondents ethical orientation about that evasion and specifically asked respondents if tax evasion was wrong at all times and in any amount. Respondents provided their responses on a seven point Likert scale similar to section B with strongly disagree coded as 1 and strongly agree coded as 7.

Section D was a post experimental questionnaire that measured among other things, respondents’ opinion on whether the tests provided anonymity and whether they were free to choose any response they preferred. Each section was preceded by instructions to guide respondents on what was required of them.

Each respondent received an identical survey instrument and experimental task. However, the experimental task was similar in all material aspects except for the tax rate and the withholding positions. The marginal tax rather used in a scenario was either 22.5 or 15%. The withholding position for each scenario either involved a situation of a refund or tax due after filing of annual tax returns. Overall therefore four different set of scenarios were used; tax rate of 22.5% with a situation of a refund; tax rate of 22.5% with a situation of tax due; tax rate of 15% with a situation of a refund; tax due of 15% with a situation of tax due. Each respondent received only one scenario, which was randomly assigned so as to mitigate the bias from subjects knowledge about the intend objective of the manipulations.

The scenario used in Reckers et al. (1994) and this study did not provide the income level of the hypothetical tax payer so as to avoid the likelihood of confounding any rate effect that the study may reveal. It is unlikely that most respondents will be able to compute accurately the appropriate level of income from the rates provided within their case because often individuals do not know their own marginal rate of tax (Lewis, 1978) as most tax payers pay very little attention to tax matters (Reckers et al., 1994). Therefore to allow for a meaningful comparison of the effects of tax rates, this study, unlike Reckers et al. (1994), provides a hypothetical reference point for comparison of tax rates by stating that the average marginal rate of tax for most Ghanaians is at 17.5%

The sample was made up of self-employed persons mainly within the capital city of Ghana, who are required to file their own tax returns at specified periods and pay the relevant tax due or claim the appropriate refund. This sample group was preferred because, unlike employees who are subjected to obligatory deduction at source and often have no requirement to file returns at year end, self-employed persons represented an appropriate segment of society with an opportunity and perhaps a desire to be non-compliant. Self-employed person was defined to include ‘independent contractors’, sole proprietorships and partnerships.

Regression equation

An OLS regression is performed using SPSS on the following equation

TEvade= a + B1TRate+ B2WHTPosition + B3 Ethics + B4 (TRate X Ethics) + B6 (WHTPosition X Ethics) + (WHTPosition X TRate)+ ei

Where TEvade = Likelihood to evade tax; Ethics =Individual Ethical Orientation (influenced to some extent by social norms); TRate = Marginal Tax rate (coded as 0 for 15% and 1 for 22.5%); WHTPosition (Withholding position coded as 0 for refund and 1 for tax payment).

However please note that the essence of this study is not to provide a prediction model for tax compliance. Rather it is to emphasis the critical and perhaps moderating effect of individual ethical orientation on compliance decisions.

ANALYSIS AND DISCUSSION

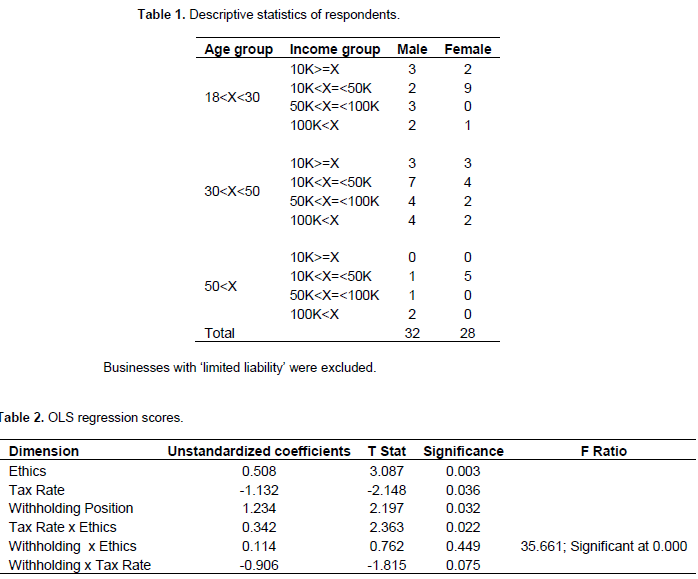

80 questionnaires (with test instruments) were distributed and 60 useable responses were received implying a response rate of 75%. A descriptive statistics of the respondents is provided in Table 1. Using Chi Square tests, no significant effect on responses was based on age, marital status, income level, and gender. A t-test of relatedness also suggests’ no significant differences between early and late responses.

All three independent variables are significant (at 5%) in the prediction of tax compliance. Hence variations in the tax rate (t=-2.1, p=0.036), as well as the likelihood of refunds (t=2.2, p=0.032) had a significant influence on tax payers compliance behavior. Compared to the other two independent variables however, individual ethical orientation was the most significant factor in determining the likelihood of tax compliance among Ghanaian taxpayers (t=3.09, p=0.003) (Table 2).

The interactions between the independent variables also reveals that an individual’s ethical orientation interacts with the tax rate to influence compliance behavior (t=2.4, p=0.022). However, unlike Reckers et al. (1994), this study suggests that individuals with a high sense of morality, who believed that tax evasion was morally wrong, were more greatly influenced by considerations of the tax rate than ‘unethical persons’. For instance, on average a highly ethical person (with a score of 7 on the Likert Scale) varied his response by 1.262 [computed as -1.132 + (0.342 *7)] compared to -0.79 [computed as -1.132 + (0.342 *1)] for unethical persons (with a score on 1 on the Likert Scale). Reckers et al. (1994) find the opposite in their study. Despite this however, ethical persons, even after being influenced by considerations of the tax rate and withholding positions, still remained largely more tax compliant than unethical persons. The explanation for this behavior of ethical persons doing ‘unethical things’ may lay in the preposition by Bersoff (1999) of ‘motivated reasoning’. It will seem that unethical persons’ are less influenced by other variables except their own extreme self- interest devoid of considerations of relativism. However considering the fact that considerations of ethics are sometimes influenced by social norms, perceptions of what is socially desirable can influence ethical behavior. The fact that ethical persons are relatively more easily subjected to influences is therefore grounded in existing theory.

Following on from existing theory, a scenario of low tax rate, with refund is expected to result in the most tax compliant behavior among tax payers, if the effects of ethics are not considered. The results of this study showed that in such a scenario, highly ethical person’s average a compliance score of 6.599 (which per the Likert scale suggest a high rate of tax compliance) compared to 2.867 for unethical persons[1]. In a scenario of high tax, no refund (rather a tax payment), highly ethical persons averaged a compliance score of 5.829 compared to 0.729 for unethical persons.

Even though the interaction between ethics and withholding position is not significant, highly ethical persons are more heavily swayed by considerations of outcome framing than unethical persons even though ethical persons still remain largely more tax compliant than unethical persons after considerations of outcome framing. Therefore prospects with the same monetary outcome may results in different compliance behaviors due to the ethical orientation of the tax payers.

[1]Computed from the OLS regression TEvade= a -1.13TRate+ 1.23WHTPosition + 0.51 Ethics + 0.34 (TRate X Ethics) + 0.11 (WHTPosition X Ethics) -0.91 (WHTPosition X TRate)+ ei with TRate = code 0; Ethics = 7 on the Likert Scale; WHTPosition = code 1)

CONCLUSION AND LIMITATIONS

The findings of this research suggest that tax rate, withholding position and individual ethical orientation can influence a tax-payers compliance behavior. Overall ethical persons are more tax compliant than unethical persons. Ethical orientation has a relatively stronger predictive power than tax rate and withholding position on tax compliance. However tax rate and withholding positions interact with ethics in that; very ethical persons can be marginally influenced to change their compliance behavior (compared to unethical persons) due to the withholding position or the tax rate. Even in such a situation however, ethical persons still remain significantly more compliant than unethical persons. This is a departure from Reckers et al. (1994) who find that ethical persons are relatively less influenced by considerations of tax rates and withholding positions. In this study, even though morality may have been mediated by considerations of tax rates and withholding positions, the extent of influence does not aggravate the tax compliance behavior of ethical persons to levels comparable to unethical persons. This is still a cause for concern because in Ghana, considerations of ethical orientation are influenced more significantly by social norms and cultural values, perhaps in greater proportion compared to western economies and as such wide spread non-compliance especially among unethical persons, if not checked could influenced the behavior of ethical persons.

The findings of this study support the preposition of Reckers et al. (1994) that decision making models on tax compliance will be more effective if they incorporate non-monetary variables such as individual ethical orientation. This study however differs from the pioneering study by Reckers et al. (1994) in a number of ways. Firstly, whereas Reckers et al. (1994) find a significant interaction of ethics on withholding positions among USA tax payers, this study rather finds a significant interaction of ethics on tax rates among Ghanaian tax payers. Secondly, this study suggests that ethical persons are more influenced by tax rates and withholding positions even though they still remain largely more ethical than ‘unethical’ persons. Reckers et al. (1994) find the opposite among USA Tax payers.

In generalizing the findings of this research, due regard must be paid to the limitations of the methodology used. Essentially, the findings of this study, are based on a principal assumption, as with other experimental tests, that respondents, will respond in the same manner during the test as they will when confronted with an actual scenario (Reckers et al., 1994). Whilst the researcher has no reason to believe that respondents hid their real behavior (especially based on the number of ‘negative responses’ provided, as well as the visible efforts by the researcher to ensure anonymity), the results provided may be specific to the context provided (Henderson & Kaplan 2005). Therefore it is possible that a revision of the construct of the scenario, such as the source of income under consideration (Madeo et al., 1987), the penalties for default etc, could have an effect on the response and reaction of taxpayers.

Secondly, converting a purely qualitative measure (TEvasion) into a continuous variable in order to perform a regression analysis has limitations. However, studies have used a similar approach especially when the qualitative variable is of a ranking nature, as is the case of this research, on a Likert scale (Nunnally, 1978). Also, the sample size of 60 participants may not be representative of the entire population. Judge et al (1985) argue findings from a small sample size are still relevant, if the data set does not include outliers, as is the case with this research). Lastly, McGee (2012) argues that tax evasion may not always be unethical and hence non-compliance behavior cannot necessarily be seen as unethical. This study does not presume compliance behavior as ethical or non-ethical but rather seeks to suggest that ethical persons are more compliant than unethical persons. Therefore the conclusions of this study are not in any way contradictory to McGee (2012). Moreover, the scenarios applied in the experimental test do not provide enough background to support occasions where non-compliance can be judged as ethical.

CONFLICT OF INTERESTS

The author has not declared any conflict of interest.

REFERENCES

|

Allingham MG, Sandmo A (1972). Income tax evasion: A theoretical analysis. J. Public Econ. 1(3):323-338. Crossref |

||||

|

Alm J, McClelland GH, Schulze WD (1992). Why do people pay taxes?. J. Public Econ. 48(1):21-38. Crossref |

||||

|

Alm J, Sanchez I, De Juan A (1995). Economic and noneconomic factors in tax compliance. Kyklos 48(1):3-18. Crossref |

||||

| Andreoni J, Erard B, Feinstein J (1998). Tax compliance. J. Econ. Literature pp.818-860. | ||||

|

Arrington CE, Reckers PM (1985). A social-psychological investigation into perceptions of tax evasion. Account. Bus. Res. 15(59):163-176. Crossref |

||||

| Baldry JC (1987). Income tax evasion and the tax schedule: Some experimental results. Public Financ. 42(3):357-83. | ||||

|

Bampton R, Cowton CJ (2002). The teaching of ethics in management accounting: Progress and prospects. Business Ethics: Euro. Rev. 11(1):52-61. Crossref |

||||

|

Bernasconi M, Zanardi A (2004). Tax evasion, tax rates, and reference dependence. FinanzArchiv: Public Financ. Anal. 60(3):422-445. Crossref |

||||

|

Bersoff DM. (1999). Why good people sometimes do bad things: Motivated reasoning and unethical behavior. Pers. Soc. Psychol. Bull. 25(1):28-39. Crossref |

||||

|

Blasi A (1980). Bridging moral cognition and moral action: A critical review of the literature. Psychol. Bull. 88(1):1-45. Crossref |

||||

|

Bobek DD, Hatfield RC (2003). An investigation of the theory of planned behavior and the role of moral obligation in tax compliance. Behav. Res. Account. 15(1):13-38. Crossref |

||||

|

Carroll JS (1987). Compliance with the law: A decision-making approach to taxpaying. Law Human Behav. 11(4):319-335 Crossref |

||||

| Carroll J (1992). "How Taxpayers Think About Their Taxes: Frames and Values." In: Slemrod, J. (1992). Why people pay taxes: Tax compliance and enforcement. Ann Arbor, MI: University of Michigan Press, pp.43-63. | ||||

| Chang OH, Schultz JJ, (1990). "The Income Tax Withholding Phenomenon: Evidence from TCMP Data." J. Am. Tax. Assoc. 9:88-93. | ||||

|

Chang OH, Nichols DR, Schultz JJ (1987). "Taxpayer Attitudes toward Tax Audit Risk." J. Econ. Psychol. 8:299-309. Crossref |

||||

|

Clotfelter CT (1983). Tax evasion and tax rates: An analysis of individual returns. Rev. Econ. Stat. pp.363-373. Crossref |

||||

| Collins JH, Plumlee RD (1991). The taxpayer's labor and reporting decision: The effect of audit schemes. Account. Rev. pp.559-576. | ||||

|

Cowell FA (1992). Tax evasion and inequity. J. Econ. Psychol. 13(4):521-543. Crossref |

||||

|

Cowell FA, Gordon JPF (1988). Unwillingness to pay: Tax evasion and public good provision. J. Public Econ. 36(3):305-321. Crossref |

||||

| Cox D (1984). Raising revenue in the underground economy. National Tax J. pp.283-288. | ||||

| Cox D, Plumley A (1988). Analyses of voluntary compliance rates for different income source classes. Unpublished Report, Research Division, IRS, Washington, DC. | ||||

| Dubin JA, Wilde LL (1988). An empirical analysis of federal income tax auditing and compliance. National Tax J. pp.61-74. | ||||

|

Elffers H, Hessing DJ (1997). Influencing the prospects of tax evasion. J. Econ. Psychol. 18(2):289-304. Crossref |

||||

| Etzioni A (2010). Moral Dimension: Toward a New Economics. Simon and Schuster. New York Free Press | ||||

| Fischer CM, Wartick M, Mark MM (1992). Detection probability and taxpayer compliance: A review of the literature. J. Account. Literature 11(1):1-46. | ||||

|

Friedland N, Maital S, Rutenberg A.(1978). A simulation study of income tax evasion. J. Public Econ. 10(1):107-116. Crossref |

||||

|

Goerke L (2014). Tax Evasion by Individuals (No. 201409). Institute of Labour Law and Industrial Relations in the European Union (IAAEU). Crossref |

||||

|

Grasmick HG, Bursik Jr. RJ (1990). Conscience, significant others, and rational choice: Extending the deterrence model. Law Soc. Rev. pp.837-861. Crossref |

||||

|

Haan N (1975). Hypothetical and actual moral reasoning in a situation of civil disobedience. J. Pers. Soc. Psychol. 32(2), 255. Crossref |

||||

|

Henderson B C, Kaplan SE (2005). An examination of the role of ethics in tax compliance decisions. J. Am. Taxation Assoc. 27(1):39-72. Crossref |

||||

| Hessing DJ, Henk E, Robben HS J, Webley,P (1992). "Does Deterrence Deter? Measuring the Effect of Deterrence on Tax Compliance in Field Studies and Experimental Studies." In: Slemrod, J. (Eds), Why people pay taxes: Tax compliance and enforcement, Ann Arbor: The University of Michigan Press pp.291-310. | ||||

| Hite PS, Jackson BR, Spicer MW (1988). The Effect of Framing Biases on Taxpayer Compliance. University of Colorado. Working Paper. | ||||

| Hodgson GM (1998). The approach of institutional economics. J. Econ. Literature pp.166-192. | ||||

| Ickes W, Tooke W (1988). The observational method: Studying the interaction of minds and bodies. In: S. Duck D, Hay S, Hobfoll W Ickes, B.Montgomery (Eds), The handbook of personal relationships: Theory, research and interventions, Chichester, England, Wiley pp.79-9). | ||||

| Jackson BR, Milliron VC (2002). Tax Compliance Research. Taxation: Critical Perspectives on the World Economy, 3:56-65 | ||||

| James S, Hasseldine J, Hite P, Toumi M (2001). Developing a tax compliance strategy for revenue services. Bull. Int. Fiscal Documentation 55(4):158-164. | ||||

| Judge GG, Carter-Hill R, Griffrths EW, Lutkepohl H Tsoung- Chao Lee. (1985). The Theory and Practice of Econometrics, 2nd Edition. New York: John Wiley & Sons, Inc. | ||||

|

Kahneman D, Tversky A (1982). On the study of statistical intuitions. Cognition 11(2):123-141. Crossref |

||||

| Kohlberg L (1976). Moral stages and moralization: The cognitive-developmental approach. Moral development and behavior: Theory, Res. Soc. Issues pp.31-53. | ||||

| Long JE, Gwartney JD (1987). Income tax avoidance: Evidence from individual tax returns. Natl. Tax J. 517-532. | ||||

| Madeo SA, Schepanski A, Uecker WC (1987). Modeling judgments of taxpayer compliance. Account. Rev. pp.323-342. | ||||

|

Mason R, Calvin LD (1978). Study of Admitted Income Tax Evasion, Law Soc. Rev. 13:73-89 Crossref |

||||

|

McGee RW (2012). 'The Ethics of Tax Evasion: Perspectives in Theory and Practice, New York: Springer. Crossref |

||||

| Nunnally JC (1978). Psychometric Theory, 2nd Edition. New York: McGraw-Hill. | ||||

| Osei RD, Quartey P (2005). Tax reforms in Ghana (No. 2005/66). Research Paper, UNU-WIDER, United Nations University (UNU). | ||||

|

Park CG, Hyun, JK (2003). Examining the determinants of tax compliance by experimental data: A case of Korea. Journal of Policy Modeling, 25(8):673-684. Crossref |

||||

| Pommerehne WW, Weck-Hannemann H (1989). Tax rates, tax administration and income tax evasion in Switzerland, Discussion Paper No. B8904, Department of Economics, University of Saarland, Saarbrucken. | ||||

|

Pommerehne WW, Weck-Hannemann H (1996). Tax rates, tax administration and income tax evasion in Switzerland. Public Choice 88(1-2):161-170. Crossref |

||||

|

Porcano TM (1988). Correlates of tax evasion. J. Econ. Psychol. 9(1):47-67. Crossref |

||||

|

Randall DM, Gibson AM (1990). Methodology in business ethics research: A review and critical assessment. J. Bus. Ethics 9(6):457-471. Crossref |

||||

| Reckers PM, Sanders DL, Roark SJ (1994). The influence of ethical attitudes on taxpayer compliance. Natl. Tax J. pp.825-836. | ||||

|

Robben HS, Webley P, Elffers H, Hessing DJ (1990). Decision frames, opportunity and tax evasion: An experimental approach. J. Econ. Behav. Organ. 14(3):353-361. Crossref |

||||

| Schadewald MS (1989). Reference point effects in taxpayer decision making. J. Am. Taxation Assoc. 10(2):68-84. | ||||

| Scholz JT (1985). Coping with complexity: A bounded rationality perspective on taxpayer compliance. Proc. Seventy-Eight Annu. Conference Taxation pp.13-16. | ||||

| Sheffrin SM, RK Triest (1992). Can Brute Deterrence Backfire? Perceptions and Attitudes in Taxpayer Compliance, In: J. Slemrod (ed.), Why People Pay Taxes. Tax Compliance and Enforcement, Ann Arbor: University of Michigan Press pp.193-218. | ||||

|

Slemrod J, Blumenthal M, Christian C (2001). Taxpayer response to an increased probability of audit: evidence from a controlled experiment in Minnesota. J. Public Econ. 79(3):455-483. Crossref |

||||

| Smith KW (1990). Reciprocity and fairness: Positive incentives for tax compliance (No. 9025). American Bar Foundation. | ||||

|

Smith KW, Kinsey KA (1987). Understanding taxpaying behavior: A conceptual framework with implications for research. Law Soc. Rev. pp.639-663. Crossref |

||||

|

Song YD, Yarbrough TE. (1978). Tax ethics and taxpayer attitudes: A survey. Public Adm. Rev. pp.442-452. Crossref |

||||

| Spicer MW, Lundstedt SB (1976). Understanding tax evasion. Public Finance 31(2):295-305. | ||||

|

Spicer MW, Thomas JE (1982). Audit probabilities and the tax evasion decision: An experimental approach. J. Econ. Psychol. 2(3):241-245. Crossref |

||||

| Terkper SE (1995). Ghana Tax Administration Reforms (1985-1993). Harvard Institute for International Development, Development Discussion Papers. | ||||

|

Trivedi VU, Shehata M, Lynn B (2003). Impact of personal and situational factors on taxpayer compliance: An experimental analysis. J. Bus. Ethics 47(3):175-197. Crossref |

||||

| Tyler TR (1990). Why people obey the law: Procedural justice, legitimacy, and compliance. New Haven, Yale. | ||||

|

Wärneryd KE, Walerud B (1982). Taxes and economic behavior: some interview data on tax evasion in Sweden. J. Econ. Psychol. 2(3):187-211. Crossref |

||||

|

Wenzel M (2005). Motivation or rationalisation? Causal relations between ethics, norms and tax compliance. J. Econ. Psychol. 26(4):491-508. Crossref |

||||

| Yaniv G (1999). Tax compliance and advance tax payments: A prospect theory analysis. Natl. Tax J. pp.753-764. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0