ABSTRACT

Market opening positively impacts economic growth due to reduction in the cost of capital and international risk diversification, amongst others in Nigeria. Using a robust set of econometric approach involving unit root test, co-integration, vector error correction model and granger causality, there is evidence that current value of economic growth responds to disequilibrium from past values of real gross domestic product, stock market development, foreign direct investment, trade openness, inflation and banking sector development in the long run. The result also shows that past values of real gross domestic product, foreign direct investment and trade openness promotes economic growth in the short run. The study, therefore, concludes that there are bi-directional causalities both in the short term and the long term between the dependent and explanatory variables. Based on the findings, the study recommends that policy makers in Nigeria should pay more attention to factors that can boost stock market development, foreign direct investment, trade openness, inflation and banking sector development in order to impact economic growth more positively in line with theoretical evidence that market opening positively impacts economic growth especially in frontier and emerging markets such as Nigeria.

Key words: Inflation, market opening, trade openness.

The last few decades witnessed an increased interest on the effects of market opening on economic growth especially in the case of emerging markets. The literature is imbued with the positive effects of market opening on economic growth of countries and this became orchestrated following globalization of markets whereby all the economies of the world are integrated with one another through trade and free flow of capital among others.

With respect to financial markets, studies which herald the immense benefits that accrue to nations that open their markets to the outside world include Levine (2001), Bekaert et al. (2003), and Ortiz et al. (2007) while the effectiveness of such openings underscores the need for reform programmes such as financial markets liberalization which gained currency in the 1980s and 1990s in the first place.

The over-view notwithstanding, there are some dissenting voices regarding the avowed benefits that accrue to countries with erstwhile closed markets that eventually liberalize. For example, Kim and Singal, (2000) and Stigliz (2004), canvassed a completely different views about the benefits of globalization especially capital market liberalization. They cited pitfalls in capital market liberalization following the International Monetary Fund’s advocacy of free and unfettered markets, of market fundamentalism, among others and attributing the increased economic instability across the globe especially in markets that were liberalized to aspects of globalization that encouraged short-term capital flows and speculative hot capital. Also, over-estimation of the efficiency of financial markets especially capital markets have often led to misconceptions about the nature of expected benefits from market opening. Maduka and Onwuka (2013) argued that despite the growth record of banks and non-bank financial institutions in Nigeria, and financial liberalization policy, the Nigerian economic growth is sluggish. These views have become important considering the fact that the explosive growth witnessed during the boom period is tapering off apart from the effects of the last global financial meltdown on emerging markets which implies that benefits from market opening in the case of emerging markets are, therefore, not sustainable in the long term.

Quixima and Almeida (2014) argued that the basic arguments point to the fact that financial development may promote economic growth through improved resource allocation efficiency but economic growth also leads to increased demand for credit that should support the development of the financial sector. Njemcevic (2017) informed that most of the empirical findings have discovered a positive relationship between finance and economic growth. Regarding international trade; Manova (2008) showed that liberalization increase exports disproportionately more in sectors intensive in external finance and softer assets, suggesting that pre-liberalization trade was restricted by financial constraint. The new orthodoxy is the integration of world trade, markets and institutions but this has turned the tide against emerging economies based on the challenges facing them.

Therefore, the causality between market openness and economic growth in Nigeria, like other emerging economies no doubt, requires further investigation. In the literature, not much has been done in this regard, hence this study. Our use of several explanatory variables enhances the dis-aggregated nature of this work which has been recommended by Mohtadi and Argawal (2004). For example, majority of the studies on the relationship between financial markets and economic growth use essentially stock market measures but we expand this scope by widening such measures to include stock market development (SMD), financial liberalization (LIB), inflation (INF.), foreign direct investment (FDI), trade openness (TOP) and banking sector development (BSD).

In the case of Nigeria, added to the generic problems of emerging markets following market opening are a new set of other problems such as: shut-down of industries due to unfavourable economic climate, massive delisting of hitherto quoted companies from the stock exchange which has affected market depth, increasing role of the Central Bank of Nigeria in the intermediation process (for example, reduced involvement in the anchor borrowers’ scheme), investors’ apathy, dearth of public offerings which was at its peak in the years immediately following market opening, destabilizing effects of the high ratio of non-performing loans and shrinking size of GDP per capita (in dollar terms). These are not part of the benefits expected for the economy following market opening.

Although actual date of financial liberalization of Nigerian markets had been a source of controversy in the literature, Bekaert et al. (2003) identified August, 1995 and May 1998 as the official liberalization date and first country American Depository Receipts issuance respectively. Also, Miles (2002) identified August, 1998 as official liberalization date of Nigeria. These, not-withstanding, liberalization is a gradual process and the benefits take time to manifest. Attesting to this, Henry (2000) argued that stock market liberalization is a gradual process generally involving several liberalizations subsequent to the first. The question now is: Does Nigeria require further markets opening in order to boost its economic growth? This important question has made it imperative to conduct a research to establish the relationship between market opening and economic growth in the case of Nigeria.

The relationship between financial markets and economic growth has been a subject of discourse that has populated the literature on finance especially in post Second World War era which witnessed greater integration of world trade, markets and institutions. Pagano (1993) observed that considerable evidence exists that financial development correlates with growth and that the resulting growth theories follow new models which have offered important insights into the effect of financial development on growth and vice versa. Ujunwa and Salami (2010) on their part highlighted the fact that one of the oldest debates in economics has remained the relationship between financial development and economic growth while Abida et al. (2015) argued that efficiency of financial market matters to economic growth.

The main theme on the link between financial markets and economic growth revolve around the effects of financial markets especially on factors allowing deeper intermediation processes on economic development and that economic development itself improves the functioning of markets. The importance of the intermediation processes was highlighted by Adeniyi et al. (2012) who pointed out that the standard view, however, appears to provide support for the existence of a close association between investment and economic prosperity. Iheanacho (2016) expanded the perspective on financial intermediation by outlining the three major components of the financial intermediary system that have become important part of the financial literature, viz: the role of financial intermediaries in the mobilization of savings, the role of financial intermediaries in enhancing economic activities in the private sector and the size of the financial intermediary system. Quixima and Almeida (2014) are of the view that the basic arguments point to the fact that financial development may promote economic growth through improved resource allocation efficiency, but economic growth also leads to increased demand for credit that should support the development of the financial sector. Azmeh et al. (2017), characteristically explained that financial systems contribute to the process of economic development while the role of stock markets in economic development has long been recognized in the literature (Pagano, 1993; Obstfeld, 1994; Greenwood and Smith, 1997; Levine and Zervos, 1998; Levine, 2000, 2001; Rousseau and Wachtel, 2000; Bekaert et al., 2001, 2003).

On their part, Madichie et al. (2014) enumerating theoretical considerations in earlier research studies on the pattern of causality between finance and growth, pointed out that causality runs from finance to growth, hence the “supply-leading hypothesis” on the one hand and on the other, that financial development can also be stimulated by economic growth. A new insight, has, however been added to the relationship between finance and growth with Arcand et al. (2012) arguing that although, there is a positive relationship between the size of the financial system and economic growth but that at high levels of financial depth, more finance is associated with less growth.

Rather than dwelling on the general issue of causalities between markets development and economic growth, Levine (2002) harped on which aspects of market (capital markets or banks) promote long-run growth. Likewise, Rioja and Valev (2004) explored the effects of finance on growth in developed and developing countries. Besides, Demirguc-Kunt and Levine (1996) reinforced this segmentation by drawing attention to the increased flow of equity investments to emerging markets. However, the literature is inundated with arguments that economic growth is impacted by several factors: financial markets (Ngongang, 2015; Hassan et al., 2016; Puryan, 2017; Njemcevic, 2017); stock market (Acquah-Sam and Salami, 2014; Njogo and Ogunlowore, 2014; Yadirichukwu and Chigbu, 2014; Niranjala, 2015; Khan and Ahmed, 2015; Khyareh and Oskou, 2015; Jareno and Negrut, 2016; Nordin and Nordin, 2016; Taiwo et al., 2016) and banks (Ngongang, 2015; Puryan, 2017.

The main argument regarding market opening in recent times revolves around allowing greater participation by international investors in domestic markets (Patro, 2005) while Pagano (1993) showed that financial intermediation has both level and growth effects; adding, however, that the resulting models have offered important insights into the effect of financial development on growth and vice versa. Odo et al. (2017) argued that in traditional growth theory, the growth rate is a positive function of exogenous technical progress, but at the same time acknowledge that endogenous growth models on the other hand show that economic growth performance is related to financial development, technology and income distribution. Puryan (2017) giving an insight into how economic growth affects financial development, opined that when an economy grows, the market demand for financial institutions, products and services increases. Njogo and Ogunlowore (2014) opined that a well-developed capital market portrays one of the common features of a modern economy and it is reputed to perform some necessary functions, which promote economic growth in any nation. Pointing at the theoretical basis on the effects of financial development on economic growth, Hassan et al. (2016) informed that economists agreed that financial market development plays a very vital role in economic growth and development. Azmeh et al. (2017) argued and in fact chronicled studies in the literature which recognize that financial systems contribute to the process of economic growth and Ngongang (2015) subscribed that the theory of the relationship between financial development and growth has witnessed a renewal of interest during the 1990s; arguing that the authors involved in the research studies show the important role of the banking system and of the financial markets in the development of economic growth. The role of efficiency in financial markets received attention from Abida et al. (2015) when they stress that efficiency of financial market matters to economic growth. The opinion of Udude (2014) crystalized the nature of efficiency inherent in a well-developed financial system by pointing out that financial development thus involves the establishment and expansion of institutions, instruments and markets that support investment and the growth process.

Empirically, Azmeh et al. (2017) found a negative and significant effect of financial liberalization on economic growth through its effects on the level of financial development. Quixima and Almeida (2014) found that the development of the banking system did not cause economic growth in Angola but that economic growth caused the development of the banking system. On their part, Abida et al. (2015) discovered a strong positive relationship between financial development and economic growth in a panel of 3 countries in North Africa over the period 1982-2012. Ngongang (2015), showed that financial development is without effect on economic growth while Puryan (2017) found that the banking sector impacts economic development. On their part, Njogo and Ogunlowore (2014) established the fact that stock market turnover contributes positively to economic growth in Nigeria. Hassan et al. (2016) showed that there exists positive and highly statistically significant long-run relationship between market capitalization; value of stock traded and money and quasi money growth on the one hand and real gross domestic product in Nigeria on the other. In a similar vein, Aigbovo and Izekor (2015) discovered that market capitalization, turnover ratio, total value of shares traded and all share index positively influence economic growth in the long-run. Furthermore, as it relates to Nigeria, Madichie et al. (2014) established the existence of a long run relationship between the real GDP as dependent variable and Gross Fixed Capital Formation, Financial Development, Liquidity Ratio and interest rates which were the independent variables. They, therefore, concluded that causality runs from economic growth to financial development during the period covered and that there was no bi-directional causality between them. Udude (2014) who used GDP as a dependent variable and broad money supply as a ratio of GDP and domestic credit to the private sector as a ratio of GDP (both as independent variables) finds a negative relationship between broad money supply to GDP and positive relationship between credit to the private sector and GDP. On his part, the results by Iheanacho (2016) indicated that financial development in Nigeria has insignificant negative effect on economic growth in the long-run and significant negative effect in the short-run.

RESEARCH METHODS AND DATA

This research study focused on the impact of market opening on the economic growth in Nigeria for the period: 1986 – 2016. Secondary data were sourced from Central Bank of Nigeria (CBN) Statistical Bulletin (various issues), National Bureau of Statistics (NBS), 2017, Nigerian Stock Exchange (NSE) Factbook (various years) and World (Bank) Development Indicator Database, 2017.

The study adopted a time series method of regression analysis and used Stationarity tests involving Augmented Dickey-Fuller, (1979) (ADF) tests, Johansen co-integration test and VECM to analyze the impact of market opening on economic growth in Nigeria. It also used the Granger causality test to establish the direction of the causality of the variables used, viz: Gross Domestic Product (GDP), Stock Market Development, Financial Liberalization, Inflation, Foreign Direct Investment, Trade Openness and Banking Sector Development. The Co-integration test was used to test the Null Hypothesis that market opening does not have significant effect on economic growth in Nigeria. Furthermore, the Granger, (1969) causality test was used to test the Null Hypothesis that market opening does not Granger cause economic performance of Nigeria.

Model specification

The following specifies the relationship between the Dependent variable (GDP) and the Explanatory variables – Stock Market Development, Financial Liberalization, Inflation, Foreign Direct Investment, Trade Openness and Banking Sector Development.

GDP = ƒ(SMD, LIB, INF, FDI, TOP and BSD) (1)

Transformed into an econometric model, thus:

Where, GDP = Gross domestic product growth rate; SMD = stock market development; LIB = financial liberalization; INF= inflation; FDI = foreign direct investment; TOP = trade openness; BSD = banking sector development; εt = error term.

Definition and measurement of variables

GDP is measured as yearly percentage change in the growth of real GDP. It is the dependent variable and in effect establishes a causal relationship between the dependent and explanatory variables. Ali and Amir (2014) explained that this explanatory variable in the partial regression represents economic growth and taken to be GDP per capita. GDP per capita is gross domestic product divided by mid-year population (Ali and Aamir, 2014). Rationalizing labour effect on growth, Njemcevic (2017) pointed out that labour is a significant factor and is expected to have important effect on growth. GDP in our context in this study is taken to be GDP per capita.

Stock market development which shows the size of the stock market was measured by the ratio of market capitalization to GDP and we believe that this measure provides a clearer picture of how the stock market impacts economic growth. This measure was similarly used by Khyareh and Oskou (2015). Also, Levine and Zervos (1998) explained that the market capitalization ratio equals the value of listed shares divided by GDP and was used by them as a measure of market size.

Financial liberalization index was used following the study by Auzairy et al. (2011). They defined stock market liberalization as the event when there is a percentage change in foreign ownership of local companies hence, we adopted their approach.

On our part, inflation was used to measure the annual percentage change in consumer price index as a measure of price-cum-economic stability. Inflation has equally been used in the literature (Abida et al., 2015; Azmeh et al., 2017; Njemcevic, 2017). Abida et al. (2015) in addition, pointed out that a negative coefficient is expected as high inflation has been found to negatively affect growth while Njemcevic expressly informed that inflation is the variable that could have a positive impact if it has a low rate and negative if the rate is high, causing economic instability.

With regards to trade openness, the method used by Khyareh and Oskou (2015) was adopted who used Total Trade Ratio to GDP which is the value of imports plus exports as a fraction of GDP per capita to measure the degree of openness to international trade.

In the case of foreign direct investment (FDI), Naceur et al. (2008) argue that it is regarded in the literature as an effective channel to transfer technology and foster growth in developing countries, hence, we emulated their adoption of FDI as a measure of economic growth.

With regards to Banking Sector Development as an explanatory variable of GDP, it was measure as the ratio of credit to the private sector to GDP. This measure was used by Ngongang (2015) and Naceur et al. (2008) in similar fashion. Abida et al. (2015) argued that this indicator is the ratio of domestic credit to GDP but point out that a high ratio of domestic credit to GDP indicates not only a high level of domestic investment, but also higher development of the financial system.

Descriptive analysis

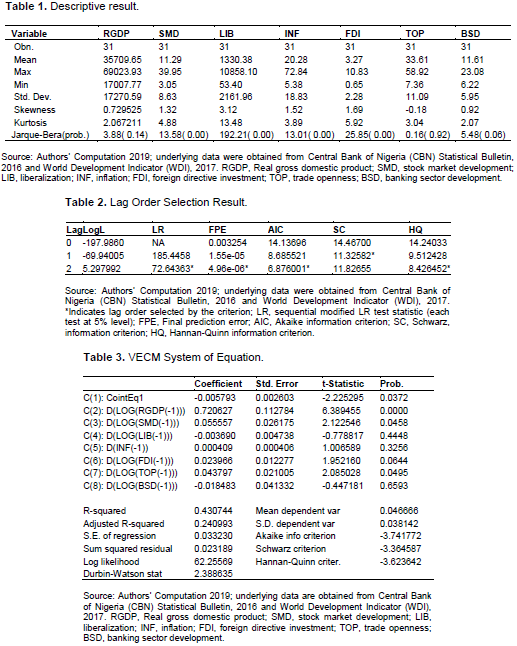

Table 1 presents the descriptive statistics of variables considered in the study. Generally, the standard deviation shows diverse variability in the series. From the Table 1, real gross domestic product (RGDP) has an average value of N35,709.65b Nigerian Naira. Stock market development (SMD), proxied by ratio of market capitalization to GDP, averaged 11.29%. Financial Liberalization (LIB), proxied by percentage change in the foreign ownership of local companies quoted on the Nigerian stock exchange, has an average value of 1330.38%.

Furthermore, Inflation (INF) has a mean of 20.28%. Foreign directive investment (FDI) has an average value of 3.27%. Trade openness (TOP) has an average value of 33.61%. Banking sector development (BSD), proxied by ratio of credit to the private sector to GDP, has a mean value of 11.61%. Skewness is a measure of asymmetry of the distribution of the series around its mean. A variable that is normally distributed will have its skewness to be zero (0). The kurtosis of the normal distribution is 3. However, Jarque-Bera being a superior test statistic for testing whether the series is normally distributed or not, have small probability values (less than 0.05), hence, we rejected the null hypothesis of a normal distribution. Thus the study concludes that virtually all the series are not normally distributed.

Stationarity tests

These comprise unit root tests (Augmented Dickey-Fuller and Phillips-Peron, (1988) unit root test). From the results, the p-value of the series suggests the acceptance of the null hypothesis of no stationarity in each series at all levels with the exception of LOG(LIB), LOG(FDI) and LOG(TOP) under PP criteria. However, based on the ADF result, the study considers the first difference transformation of each series. The results of first difference fail to accept the null hypothesis of no stationarity within the 1% and 10% conventional levels of significance, hence, we accepted the alternative hypothesis and conclude that each of the series are stationary at first difference. This is to say that all the series are integrated of order one (I (1)) and having regard to the order of integration, the study proceeds to integration test.

Lag selection structure

Table 2 presents lag order selection result on the variables considered in this study. The lag length selection criteria begin with the specification of maximum lag of 2. An asterisk indicates the selected lag from each column of the criterion statistic. Based on the Schwarz information criterion (SC), the study considers the lag length of 1 as the optimal lag length.

Co-integration test

Table 3 presents co-integration test result on the selected series. The test statistic indicates that the hypothesis of no co-integration (Ho) among the variables can be rejected. It shows that there is at most, three co-integrating relation in our model. Knowing fully well that one co-integrating relation is enough to prove that long-run relationship exists among the variable in the model. This suggests that the study can proceed to estimating VECM.

Vector error correction estimates

Table 3 presents the vector error correction model (VECM) result of target model using system of equation. There are several important observations that can be made from the result, however, the most prominent of all are the error correction terms (CointEq1), the first difference and lag operators which indicate that the results were obtained from the first step VAR in first deference, R-squared and F-statistic, at the lower part of the Table 3. From the result, the R2 value of 0.431 shows that the explanatory variables explain about 43.1% of the variation in economic growth.

The F-Statistics value of 2.27 indicates that the model is significant. The value (D.W Statistics = 2.39) shows that the model is free from autocorrelation problem. The negative and significance of the coefficient of error correction term (-0.0058) provides the evidence that the current value of RGDP respond to disequilibrium from the values of RGDP, SMD, LIB, INF, FDI, TOP and BSD one year ago. Interpreting the short run effect, according to Hoxha (2010), the estimates of parameters associated with the lagged differences of the explanatory variables can be interpreted in the usual way. In general, the result shows that, past values of real gross domestic product (RGDP t-1), stock market development (SMDt-1), foreign directive investment (FDI t-1) and trade openness (TOP t-1) are positively related to current value of GDP within the 1 and 10% conventional alpha levels. These imply that the past values of RGDP, SMD, FDI and TOP improve economic growth during the period of this study. In contrast, the result of the coefficients of inflation (INF t-1), financial liberalization (LIB t-1) and banking sector development (BSD t-1) are insignificant indicating that the indicators are not major determinants of economic growth.

Diagnostics check

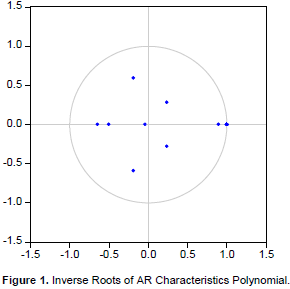

Inverse roots of the AR

The test on stability condition for the model indicates that no root lies outside the unit circle. The graphical output of the stability condition is displayed in Figure 1. It clearly shows that all the inverse roots of the AR characteristic polynomials lie within and on the unit circle thus conclude that the VECM models satisfy the stability condition.

Granger causality test

To further investigate the short run causal relationship among the explanatory variable and employment in the VECM, the study used pairwise granger causality since all the variables are integrated of order 1; I(1). As can be seen from the results, there is no bi-directional relationship. However, the result clearly shows that there are short run causalities that run from SMD to RGDP, INF, FDI and BSD, from RGDP to LIB, FDI and BSD. Also, it shows that there are causalities that flow to LIB from TOP, FDI from INF, TOP from INF, FDI from BSD and TOP from BSD. All these relationships are established within the 1 and 10% levels of significance.

From the analysis, it can be seen that during the period of study (1986 – 2016), there was a change in real GDP growth rate by 306% (minimum value N17,007.77 Nigerian Naira and maximum N69,023.93 Nigerian Naira). Similarly, the size of the market as measured by the ratio of market capitalization to GDP increased by more than 12 times (minimum value 3.05 and maximum value 39.95) its value prior to liberalization. This inferred that market opening has led to increase in the depth of the Nigerian stock market. The same growth trajectory can be observed in the case of change in the percentage ownership of equities listed on the local bourse (Nigerian Stock Exchange) by foreign investors as measured by LIB. LIB changed by as much as 202334% (minimum ratio 53.40 and maximum ratio 10858.10) during the period of study which simply means that foreign portfolio investments increased significantly which can point to the fact that market opening has provided ample opportunity for international risk diversification. However, the rate of inflation changed by as much as 1253%; which can be attributed largely to the effects of foreign inflow of funds sequel to the market opening. In the case of FDI, which measured its effectiveness in the transfer of technology and measure of economic growth, ceteris paribus, the growth rate increased further by 1566% during the period of study which suggest that market opening spurred economic growth in Nigeria during the period of study. As regards trade which was openness which measured the value of imports and exports as a fraction of GDP, the results showed an increase of well over 700% (minimum value 7.36 and maximum value 58.92) during the period of study which suggested that the Nigerian market became more integrated with the global markets. This integration of the local market with the global market justified the need for liberalization which was needed to speed up the process of economic development as it has been stated in the literature (Abida et al., 2015 argued that countries embark on reforms in order to speed up their growth rates). Banking sector developed measured by the ratio of credit to the private sector to GDP changed by as much as 271% which indicated not only a high level of increase in domestic investment but equally established a higher level of development of the financial system. With respect to the result from the descriptive analysis, it has to be pointed out that increases witnessed in the performance indicators did not point to the fact that the minimum levels indicated were as at the date of announcement of liberalization and the maximum levels indicated were as at the terminal date of the study but the statistics established the positive growth trajectories which occurred during the period of study since liberalization events and its effects occur sequentially.

In terms of stationarity of the data set, the series are integrated of order one (I(1) and the co-integrating test result showed that there was a long-run relationship among the variables used. Furthermore, the VECM established that past values of SMDt-1, FDIt-1 and TOPt-1 positively improved economic growth as measured by RGDPt-1 (real economic growth) in Nigeria. However, results from the VECM showed that INFt-1, LIBt-1 and BSDt-1 were not major determinants of economic growth in Nigeria.

CONCLUSION AND RECOMMENDATION

From the result of the study conducted within the period 1986 to 2016, using a robust set of econometric approach involving unit root tests, co-integration test, vector error correction model and granger causality; the unit root test results show that all the series are integrated of order 1, the Johansen co-integration test for the VEC model indicates that the series are co-integrated and that long-run equilibrium exists among the selected series.

The negative and significant value of the error correction term in the VECM estimates confirms the stability of the system and provides evidence that the current value of economic growth responds to disequilibrium from the past values of real gross domestic product, stock market development, foreign directive investment, trade openness, inflation and banking sector development. The result also shows that past values of real gross domestic product (RGDP t-1), stock market development (SMDt-1), foreign directive investment (FDI t-1) and trade openness (TOP t-1) promotes economic growth in Nigeria in the short run.

Furthermore, the granger causality result confirms the existence of short run causal relationships that run from stock market development (SMD) to economic growth. Also, evidence from the ganger causality result shows that economic growth stimulate financial liberalization (LIB), foreign direct investment (FDI) and banking sector development (BSD) in Nigeria, hence, financial liberalization (LIB), foreign direct investment (FDI) and banking sector development (BSD) were found not invariant to economic growth.

Therefore, it can be

concluded that there are bi-directional causalities both in the short-term and long-term between the dependent and explanatory variables. Based on the findings, it is recommended, among other things, that policy makers in Nigeria should pay more attention to factors that can boost stock market development (SMD), foreign direct investment (FDI), trade openness (TOP), inflation (INF) and banking sector development (BSD) in order for these to impact economic growth more positively. This will in turn spur more positive development of the financial markets.

The authors have not declared any conflict of interests.

REFERENCES

|

Abida Z, Sghaier IM, Zghidi N (2015). Financial Development and Economic Growth: Evidence from North African Countries. Economic Alternatives 2:17-33.

|

|

|

|

Acquah-Sam E, Salami K (2014). Effect of Capital Market Development on Economic Growth in Ghana. European Scientific Journal 10(7):511-534.

|

|

|

|

|

Adeniyi O, Omisakin O, Egwaikhide FO, Oyinlola A (2012). Foreign Direct Investment, Economic Growth and Financial Sector Development in Small Open Developing Economies, Economic Analysis and Policy 42:1.

Crossref

|

|

|

|

|

Aigbovo O, Izekor AO (2015). Stock Market Development and Economic Growth in Nigeria: An Empirical Assessment. International Journal of Business and Social Science 6(9):1.

|

|

|

|

|

Ali MA, Amir N (2014). Stock Market Development and Economic Growth: Evidence from India, Pakistan, China, Malaysia and Singapore. International Journal of Economics Finance and Management Sciences 2:220-226.

Crossref

|

|

|

|

|

Arcand J, Berkes E, Panizza U (2012). Too Much Finance. International Monetary Fund Working Paper WP/12/161.

Crossref

|

|

|

|

|

Auzairy NA, Ahmad R, HO CSF (2011). The Impact of Stock Market Liberalization and Macroeconomic Variables on Stock Market Performances. International Conference on Financial Management and Economics 11:358-362.

Crossref

|

|

|

|

|

Azmeh C, Al Samman, Mouselli S (2017). The Impact of Financial Liberalization on Economic Growth: The Indirect Link. International Business Management 11(6):1289-1297.

|

|

|

|

|

Bakaert G, Harvey CR, Lundblad C (2001). Emerging Equity Markets and Economic Development. Journal of Development Economics September pp. 1-31.

Crossref

|

|

|

|

|

Bekaert G, Harvey CR, Lundblad CT (2003). Equity Market Liberalization in Emerging Markets. Journal of Financial Research 26(3):275-299.

Crossref

|

|

|

|

|

Demirguc-Kunt, A. and Levine, R. (1996), "Stock Markets, Corporate Finance and Economic Growth: An Overview", World Bank Economic Review 10(2):223-239.

Crossref

|

|

|

|

|

Dickey DA, Fuller WA (1979). Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association 74(366):427-431.

Crossref

|

|

|

|

|

Granger CWJ (1969). Investigating Causal Relations by Econometric Models and Cross Spectral Methods. Econometrica 37:24-35.

Crossref

|

|

|

|

|

Greenwood J, Smith BD (1997). Financial Markets in Development and the Development of Financial Markets. Journal of Economic Dynamics and Control 21:145-181.

Crossref

|

|

|

|

|

Hassan A, Babafemi OD, Jakada AH (2016). Financial Market Development and Economic Growth in Nigeria: Evidence from VECM Approach. International Journal of Applied Economic Studies 4(3):1-13.

|

|

|

|

|

Henry PB (2000). Do Stock Market Liberalizations Cause Investment Booms? Journal of Financial Economics 58(1-2):301-334.

Crossref

|

|

|

|

|

Hoxha A (2010). Causality between Prices and Wages: VECM Analysis for EU-12. Theoretical and Applied Economics 5(546):27-48.

|

|

|

|

|

Iheanacho E (2016).The Impact of Financial Development on Economic Growth in Nigeria: An ARDL Analysis. Economies 4(4):26.

Crossref

|

|

|

|

|

Jareno F, Negrut L (2016). US Stock Market and Macroeconomic Factors. The Journal of Applied Business Research 32(1):325-340.

Crossref

|

|

|

|

|

Johansen S (1995). Likelihood-based Inference in Cointegrated Vector Autoregressive Models Oxford. Oxford University Press on Demand.

Crossref

|

|

|

|

|

Khan K, Ahmed I (2015). Impact of Stock Prices on Macroeconomic Variables: Evidence from Pakistan. KASBIT Business Journal (KBJ) 8(1):42-59.

|

|

|

|

|

Khyareh MM, Oskou V (2015). The Effect of Stock Market on Economic Growth: The Case of Iran. International Journal of Academic Research in Economics and Management Sciences 4(4):52-62.

Crossref

|

|

|

|

|

Kim EH, Singal V (2000). The Fear of Globalizing Capital Markets. Emerging Markets Review 1:183-198.

Crossref

|

|

|

|

|

Levine R, Zervos S (1998). Capital Control Liberalization and Stock Market Development. World development 26(7):1169-1183.

Crossref

|

|

|

|

|

Levine R (2000). International Financial Liberalization. Review of International Economics pp. 1-28.

|

|

|

|

|

Levine R (2001). International Financial Liberalization and Economic Growth. Review of International Economics 9 (4):688-702.

Crossref

|

|

|

|

|

Levine R (2002). Bank-Based or Market-Based Financial Systems: Which one is Better? Journal of Financial Intermediation 11:398-428.

Crossref

|

|

|

|

|

Madichie C, Maduka A, Oguanobi C, Ekesiobi C (2014). Financial Development and Economic Growth in Nigeria: A Reconsideration of Empirical Evidence. Journal of Economics and Sustainable Development 5:28.

|

|

|

|

|

Maduka AC, Onwuka KO (2013). Financial Market Structure and Economic Growth: Evidence from Nigeria Data. Asian Economic & Financial Review 3(1):75-98.

|

|

|

|

|

Manova K (2008). Credit Constraints, Equity Market Liberalizations and International Trade. Journal of International Economics 76:33-47.

Crossref

|

|

|

|

|

Miles W (2002). Financial Deregulation and Volatility in Emerging Equity Markets. Journal of Economic Development 27(2):113-126.

|

|

|

|

|

Mohtadi H, Agarwal S (2004). Stock Market Development and Economic Growth: Evidence from Developing Countries.

|

|

|

|

|

Naceur S, Ghazouani S, Omran M (2008). Does Stock Market Liberalization Spur Financial and Economic Development in the MENA region? Journal of Comparative Economics 36(4):673-693.

Crossref

|

|

|

|

|

National Bureau of Statistics (2017). FISCAL STATISTICS JANUARY - JULY 2017.

|

|

|

|

|

Ngongang E (2015). Financial Development and Economic Growth in Sub-Saharan Africa: A Dynamic Panel Data Analysis. European Journal of Sustainable Development 4(2):369-378.

Crossref

|

|

|

|

|

Niranjala SAU (2015). Stock Market Development and Economic Growth in Sri Lanka. Global Journal of Management and Business Research: Economics and Commerce 15(8):1-7.

|

|

|

|

|

Njemcevic F (2017). Capital Market and Economic Growth in Transition Countries: Evidence from South East Europe. Journal of International Business Research and Marketing 2(6):15-22.

Crossref

|

|

|

|

|

Njogo BO, Ogunlowore AJ (2014). Impact of Nigerian Financial Markets on the Economic Growth. International Journal of Financial Markets 1(3):77-82.

|

|

|

|

|

Nordin S, Nordin N (2016). The Impact of Capital Market on Economic Growth: A Malaysian Outlook. International Journal of Economics and Financial Issues 6(S7):259-265.

|

|

|

|

|

Obstfeld M (1994). Risk-Taking, Global Diversification and Growth. The American Economic Review 84(5):1310-1329.

|

|

|

|

|

Odo SI, Anoke CI, Onyeisi OS, Chukwu BC (2017). Capital Market Indicators and Economic Growth in Nigeria; An Autoregressive Distributed Lag (ARDL) Model. Asian Journal of Economics, Business and Accounting 2(3):1-16.

Crossref

|

|

|

|

|

Ortiz E, Cabello A, Jesus RD (2007). The role of Mexico's Stock Exchange in Economic Growth. Journal of Economic Asymmetries 4(2):1-135.

Crossref

|

|

|

|

|

Pagano M (1993). Financial Market and Growth: An Overview. European economic review 37(2-3):613-622.

Crossref

|

|

|

|

|

Patro D (2005). Stock Market Liberalization and Emerging Market Country Fund Premiums. The Journal of Business 78(1):135-168.

Crossref

|

|

|

|

|

Phillips PCB, Perron P (1988). Testing for a Unit Root in Time Series Regression. Biometrika 75(2):335-346.

Crossref

|

|

|

|

|

Puryan V (2017). The Causal Relationship Between Economic Growth, Banking Sector Development and Stock Market Development in Selected Middle-East and North African Countries. International Journal of Economics and Financial Issues 7(3):575-580.

|

|

|

|

|

Quixima Y, Almeida A (2014) Financial Development and Economic Growth in a Natural Resource Based Economy: Evidence from Angola. FEP Working Paper pp. 1-16.

|

|

|

|

|

Rioja F, Valev N (2004). Finance and the Sources of Growth at Various Stages of Economic Development. Economic Inquiry 4(1):127-140.

Crossref

|

|

|

|

|

Rousseau PL, Wachtel P (2000). Equity Markets and Growth: Cross-Country Evidence on Timing and Outcomes, 1980-1995. Journal of Banking and Finance 24:1933-1957.

Crossref

|

|

|

|

|

Stigliz JE (2004). Capital Market Liberalization, Globalization and the IMF. Oxford Review of Economic Policy 20(1):57-71.

Crossref

|

|

|

|

|

Taiwo JN, Adedayo A, Evawere A (2016). Capital Market and Economic Growth in Nigeria. Accounts and Financial Management Journal 1(8):497-525.

|

|

|

|

|

Udude C (2014). Financial Development and Economic Growth in Nigeria: An Empirical Investigation (1980-2012). International Journal of Social Sciences and Humanitarian Reviews 4(4):198-204.

|

|

|

|

|

Ujunwa A, Salami OP (2010). Stock Market Development and Economic Growth: Evidence from Nigeria. European Journal of Economics, Finance and Administrative Sciences 25:44-53.

|

|

|

|

|

Yadirichukwu E. Chigbu EE (2014). The impact of capital market on economic growth: the Nigerian perspective. International journal of development and sustainability 3(4):838-864.

Crossref

|

|