ABSTRACT

This paper investigates the relationship between money laundering and economic growth in Trinidad and Tobago. It utilizes annual secondary time series data for the period 1990 to 2017. The proxy of fraud offences and narcotics is used to estimate the volume of money laundering. Cointegration analysis and Error Correction Modelling is employed to test the long-run and short-run relationship between money laundering and economic growth. Long-run analysis revealed that there is a positive significant relationship between fraud offences and economic growth while narcotics offences maintained a negative significant relationship with economic growth. In the short-run, estimations revealed that only fraud offences had a significant negative impact on economic growth.

Key words: Money laundering, economic growth, Trinidad Tobago, Caribbean.

This paper examines the issue of money laundering and its impact on the Trinidad and Tobago economy. Trinidad and Tobago have been branded as a major money laundering country by the 2018 International Narcotics Control Strategy Report. This was harmonized by the Basel Anti-Money Laundering (AML) Index 2017 Report. The country received a Basel AML Index of 6.8 placing it in the high- risk category of countries vulnerable to money laundering. Accordingly, it was ranked the 35th highest risk country prone to money laundering out of 146 countries worldwide. The country received a ranking of the 5th highest risk country susceptible to money laundering in the Latin American and the Caribbean region after Paraguay, Haiti, Bolivia and Panama which received Basel AML Indices of 7.53, 7.50, 7.17 and 7.01 respectively. The Basel AML Index 2017 Report distinctly identified five factors which constituted a high- risk ranking in the Basel AML Index. These factors included a high-level of perceived corruption, shortfalls in the AML/ Combating Terrorist Financing (CFT) framework, poor financial standards, lack of public transparency and weak political rights and rule of law.

There is a lack of empirical research which assesses the impact of money laundering on the economic stability and welfare within the Caribbean and more specifically, Trinidad and Tobago. The increasing risk of money laundering should necessitate consistent updating of pragmatic research efforts to follow and examine any ongoing trends which may be linked to money laundering. Although it is intrinsically challenging to measure and assess the impact of money laundering on an economy, this study endeavours to combine both existing economic theory and prior empirical studies to formulate an appropriate model to explain Trinidad and Tobago’s experience of money laundering.

This paper uses cointegration and error correction analysis to test both the short-run and long-run relationship between money laundering and the economic growth using time series data for the period 1990-2017. Two variables are used as money laundering proxies; narcotics offences and fraud offences, in the econometric model as they were assumed to generate adequate volumes of illegal proceeds which require laundering.

The paper is structured into five sections. This first section provides context to why it was vital to explore the issue of money laundering in Trinidad and Tobago. Then there is a brief survey of literature. The third section looks specifically at the economic environment which may possibly be conducive to money laundering. Section 4 discusses the data, the methodology and the model used to examine the short- run and long- run impact on economic growth. Section 5 concludes and proposes some policy recommendations.

Money laundering and the macro-economy

There have been several international studies which examined the relationship between money laundering and economic growth. For example, A

rgentiero et al. (2008), in their case study of Italy, the analysis suggested two main results. First, money laundering accounts for approximately 12 percent of aggregate GDP. Secondly, money laundering is negatively correlated to GDP and it is more volatile than aggregate GDP itself. Stancu and Rece (2009) examined data collected from USA, Russia, Romania and eleven other European countries, using a linear regression model. Their results supported the hypothesis that money laundering can lead to short- run economic benefits. These findings contradicted the prevalent hypothesis that money laundering and economic growth are inversely related. Using an annual dataset spanning from 1985- 2013, Villa et al. (2016) estimated the volume of laundered assets in the Colombian economy. Their results confirmed that the volume of laundered assets increased from about 8 percent of gross domestic product in the mid-1980s to a peak of 14 percent by 2002 and declined to 8 percent in 2013. Bett and Muturi (2016) utilized dynamic ordinary least squares to estimate the relationship between economic crimes and economic growth. Annualized data from the period 2000-2014 were used. Findings confirmed a strong negative and significant relationship between illicit financial flows and economic growth in Kenya both in the short and long run. Barone et al. (2017) analysed the influence of the business cycle on illicit capital, money laundering and legal investment at the macro level. It was concluded that as legal capital is accumulated by organized crime, a decelerating growth trend is observed. The stagnation assumption can be said to hold for the illegal economy. Results showed that illegitimate capital is affected by the business cycle mainly through the capital multiplier, which in turn depends on the interest rate path.

More recently, Hetemi et al. (2018) evaluated the impact of money laundering on economic growth concentrating on Republic of Kosovo and its trade partners. Using data from 2008-2015, a GMM technique was employed. They tested three hypotheses: one, whether money laundering has an effect on the level of economic growth; two, whether the effect of money laundering on economic growth was negative, and three, whether the increases in crime, corruption and informal economy decreases economic growth. Results supported the hypothesis that money laundering has a significant and negative effect on economic growth. These results are consistent with past literature. They also found that the informal economy and corruption have a negative and significant effect on economic growth. Whilst, the consequence of the number of crimes was not as anticipated, it was found to be statistically insignificant.

To date, there are only two non-published studies which have attempted to use econometric analysis to access the impact of money laundering in the English-speaking Caribbean. These studies include those of Gray-Farquharson (2007) which provided an empirical assessment for the period 1972- 2005 of the impact of money laundering on the financial system and economy of Jamaica. Sectioned into two parts, first, the relationship between money laundering and economic growth was tested. Using cointegration and Vector Error Correction model (VECM) methods, the results revealed a positive and significant relationship between the economic growth and money laundering in Jamaica in the long run. Thereafter, she estimated how money laundering activities affected the Jamaican financial system. Using the money demand variable as the proxy representative of the financial system, the results indicated a positive relationship between money demand and money laundering. Results suggested that the persistence of money laundering has the ability to threaten the financial stability of Jamaica which can consequently affect economic growth.

Subsequently, Jones (2015) attempted a similar analysis for the case of Trinidad and Tobago. She investigated the effects of money laundering on economic and financial stability using an annual time-series data for the period 1990-2014. Cointegration and error correction models were also used to estimate the long run and short run relationships between money laundering and the financial system and the economy. Additionally, the Granger causality test was performed to determine the direction of causal flow among the variables. Two variables were used to represent the money laundering phenomenon; drug trafficking and fraud, as they were assumed to generate sufficient volumes of proceeds which necessitated laundering.

The results confirmed a positive and statistically significant relationship between the money laundering proxy, drug trafficking and economic growth, while a negative one existed between the proxy, fraud, and economic growth. Interestingly, in the Trinidad and Tobago setting, it was confirmed that a negative and significant relationship exists between the money laundering variables and the money demand. Using the Granger Causality test, it was suggested that both drug trafficking and fraud were found to Granger cause economic growth, whilst only fraud was found to Granger cause money demand.

THE ENVIRONMENT FOR MONEY LAUNDERING IN TRINIDAD AND TOBAGO

Referenced as an ideal “cocaine and marijuana trans-shipment” point by the US Department of State, Trinidad and Tobago are susceptible to several transnational criminal activities involving both domestic and international organised criminal individuals and organizations. The country is located just about 7 miles off the Venezuelan coast, and given the recent troubles, it is not surprising that there are spill over effects. Much of this activity revolves around the informal economy. Studies have shown that the informal economy represents a significant segment of the country’s economic activity. The informal sector accounts for between 26- 33% of total economic activity (Peters, 2017). This estimate by Amos coincides with previous approximations, 35% of GDP (Schneider et. al 2010), 25% of GDP in 2000 (Vuletin 2008) and the earliest estimation of the informal economy found was 20% of GDP in 1999 (Maurin et al., 2006).

Corruption has been strongly linked to money laundering. The 2017 Corruption Perception Index (CPI) ranked Trinidad and Tobago as the 77th least corrupt country out of 180 countries, with a CPI score of 41/100 in 2017. This had slightly increased from 35 points in 2016. However, a CPI of 41 points still indicates that the country is perceived relatively corrupt. Trinidad and Tobago’s CPI score falls short of the internationally acceptable average score of 43 (TTTI, 2018). A high predisposition to corruption has serious implications, exposing the country to the risk of money laundering. Corrupt persons and institutions make the process of money laundering easier to conceal illicit proceeds.

The lack of effective investigation and prosecution of financial crimes in Trinidad and Tobago makes it an attractive location to launder illicit funds without severe consequences. There has been no adjudication or criminal convictions for the offence of money laundering in Trinidad and Tobago. Consequently, the country has received low ratings for compliance by CFATF. The cases presently before the courts are predicate crimes of: fraud, illegal gambling, drug trafficking, larceny servant, corruption, robbery, conspiracy to defraud and falsification of accounts. The FIUTT (2017) highlighted that the effectiveness of money laundering investigation and prosecution was low. The CFATF Mutual Evaluation emphasized that “the lack of ML arrests coupled with the risks associated with the jurisdiction along with the lack of priority given to investigation suggests that the offence of ML is not properly investigated” (CFATF, 2016, 6). Swift convictions of individuals for financial crimes can act as a preventive measure in decreasing the probability of money laundering occurring within Trinidad and Tobago. Although, there has been multiple charges laid against persons, no individual has faced the full brunt of the law for the criminal act of money laundering. As such, the CFATF declared that the crime of money laundering is not given priority within the Court system of Trinidad and Tobago.

Like in many other countries, there is a pronounced disparity between the punishment associated with white-collar crimes and blue-collar crimes. Money laundering falls within the realm of white- collar crime. More leniency is granted to white-collar criminals by the judicial system in Trinidad and Tobago. The variance in treatment of white-collar criminals in Trinidad and Tobago occurs in the form of a “failure to press criminal charges, delayed investigation and state protection of the elite” (Kerrigan and Sookoo, 2013, 165). Violent crimes received more severe punishment in terms of prison sentences and fines imposed when compared to white-collar crimes even though white-collar crime has a greater financial cost and much more victims impacted as opposed to “violent street crimes”. Unfortunately, these implications are not reflected in the punishment of white-collar crime.

The following section highlights the high- risk sectors prone to the occurrence of money laundering. Observing that some sectors were more vulnerable than others to the risk of money laundering, the FIUTT adopted a risk-based methodology to supervision and identified five high- risk sectors amongst Listed Businesses (LBs): Attorneys-at-law, Accountants, Private Members Clubs, Real Estate and Motor Vehicle Sales which were deemed as exposed to a higher occurrence of money laundering. Other sectors apart from those listed as high risk which are of equal importance to understanding the threat of money laundering were discussed.

Sectors susceptible to money laundering in Trinidad and Tobago

One of the most susceptible areas of money laundering globally is the financial sector. Trinidad and Tobago have one of the most sound, well-developed financial sectors in the Caribbean region. It is highly liquid banking, stock market, insurance sectors, has been the most dominant in terms of expansion into other CARICOM markets. Therefore, it is a net capital exporter to neighbouring states.

The banking sector is seen as the “gatekeeper” of the financial sector (CFATF 2016, 72). However, as Seuraj and Watson (2012) emphasized, banks in their daily operations are predisposed to several risks which, if not managed or controlled, may result in unfavourable implications for the entire economy. In Trinidad and Tobago, banks are cognizant of the money laundering risks which exist and the associated AML/CFT requirements, especially as the country is frequently struggling to get itself off various “black lists”. The sector has been extra vigilant in ensuring that the risk of money laundering is minimized. The CFATF explained that four of the commercial banks operating within Trinidad and Tobago are each part of an international group headquartered in North America where domestic banking operations in Trinidad and Tobago are subjected to a more stringent AML/CFT requirement than the home country.

The banking sector is heavily regulated by the CBTT (Central Bank), supported by the Securities Exchange Commission (TTSEC), with suspicious transactions being monitored by the FIUTT (Financial Intelligence Unit); all in an effort at minimizing the risk of money laundering through this channel. It must be acknowledged that, unlike many of its neighbours, Trinidad and Tobago do not have a large and thriving offshore financial sector. However, many of these Caribbean countries with vibrant offshore banking operations have been scrutinized and criticized for fuelling unacceptable and criminal behaviours such as tax evasion, tax avoidance and money laundering.

Attorneys-at-law, accountants and real estate agents are the architects behind several activities including but not limited to facilitating the exchange of ownership of assets, management of client’s money, securities and other assets, facilitating financial transactions, provision of financial and legal advice inter alia. Attorneys, accountants and real estate agents are privy to sensitive legal and financial information related to their clientele which may be able to help in the fight against money laundering. Strict AML coverage must include these professions to improve the country’s image in the eyes of international agencies. Attorneys, accountants and real estate agents are obligated to act both ethically and within the confines of the law. These professionals are expected not to aid and abet clients with committing the crime of money laundering or any of its predicates. It is imperative that attorneys, accountants and real estate agents are able to detect and report any suspicious activities in which they may encounter in their professions. Listed businesses’ supervision falls under the purview of the FIUTT in the initiative to combat money laundering. There is much room for improvement in the regulation of this sector in Trinidad and Tobago.

The FIUTT (2018) has categorized the real estate sector in Trinidad and Tobago as the one most vulnerable to the risk of money laundering. The real estate sector is used to convert “dirty money” into a secure and long-term investment. The ownership of real estate creates a façade of respectability, legitimacy and normality for scheming criminals engaged in obscuring the proceeds from their criminal activity. This method is commonly used in the integration stage of the money laundering process.

On an annual basis via the FIUTT Annual Reports, suspicious activities have been reported to be recurring within the real estate sector. Notably, the real estate sector involves large volumes of funds and multiple parties engaged in every single real-estate transaction. This creates additional layers in the concealment of illegal proceeds making it tremendously challenging to detect property dealings and transactions connected to money laundering. Consequently, the globalisation of the real estate market makes it even more difficult to identify real estate transactions associated with money laundering especially when potential owners can be elusive international criminal elements.

Money laundering creates distortions in the real estate market such as unexplained increases in the demand for real estate. This inexplicable demand creates an upward pressure on real estate prices which leads to spiralling real estate prices (CBTT, 2007). This impacts a large cross-section of prospective buyers as the market prices are inflated, and in some cases deflated, due to the manipulation of the real estate market to ensure that there is little suspicion of the high volume of illegitimate proceeds being channelled into the sector.

A major drawback in the fight against money laundering in Trinidad and Tobago is that LBs, particularly those in the real estate, do not possess a comprehensive understanding of money laundering risk or the scope and depth of actions necessary to alleviate varying money laundering risks in this sector. Furthermore, it was noted that real estate agents have not properly analysed their money laundering risk, nor have they adequately applied mitigating measures commensurate with their risks (CFATF, 2016). Much improvement in risk assessment, monitoring and enforcement of anti-money laundering policies by all stakeholders is required to minimize the occurrence of money laundering within this sector.

Money launderers can easily convert illegal proceeds through the used-car industry or the motor-vehicle sales industry by procuring motor vehicles especially through cash transactions to legitimize unlawful earnings. The purchase of luxury vehicles is done to conceal “dirty” money within the real economy. According to the United States Department, law enforcement (2017; 2018) sources indicated that incomes from the black-market sale of firearms and suspicious sales of smuggled used luxury vehicles rival income from local drug sales.

Trinidad and Tobago remain one, if not the only country, with a thriving gaming sector that is completely unregulated. The allure of the high cash-intensive nature of casinos makes it a perfect “playground” for money launderers worldwide. In Trinidad and Tobago, public casinos and online gaming are all illegal. However, casinos have been operating under the guise of Private G Club (PMC). Though the supervision of PMCs falls under the purview of the FIUTT, the non-existent regulations and poor controls which govern the operations of these types of organizations makes it a prime target for money laundering. Money launderers are able to exploit the “casino-like environment” of PMCs which handle large sums of money under archaic regulatory supervision presently followed in Trinidad and Tobago.

There is a significant presence of PMCs within Trinidad and Tobago which provide gambling activities through gaming tables and machines that are similar to casinos. The high-cash intensity of these institutions, the unscrupulous nature of the clientele which PMCs attract and the non-rigorous application of the AML/CTF requirements all signals a poorly regulated sector which make it highly susceptible to money laundering. There have been instances where some banking institutions have declined to conduct business with some of these PMC institutions because of the perceived high risks posed by this industry.

Noticeably, there is an inadequate AML/CFT regime within Trinidad and Tobago especially for the supervision of PMCs. There are no provisions in place which prevents criminals or their associates from holding key influential positions in a PMC or having a significant or controlling interest or holding a management function or being an operator of a PMC (CFATF, 2016).

Since November 2017, when Trinidad and Tobago made a high-level political commitment to work with the FATF and CFATF to strengthen the effectiveness of its AML/CFT regime and address any related technical deficiencies. Trinidad and Tobago have taken steps towards improving its AML/CFT regime, by proclaiming laws on NPO supervision and civil asset recovery. Trinidad and Tobago should continue to work on implementing its action plan to address its strategic deficiencies, by implementing: (1) the remaining measures to further enhance international cooperation; (2) the issues related to transparency and beneficial ownership; and (3) the measures to monitor NPOs on the basis of risk (FATF, 2019) (http://www.fatf-gafi.org/publications/high-risk-and-other-monitored-jurisdictions/documents/fatf-compliance-june-2019.html).

Money laundering is a challenging economic problem to model as its monetary value cannot be easily quantified. Nevertheless, Cointegration analysis and an Error Correction Model (ECM) were used here to examine both the short run and long run relationship between money laundering and economic growth. Secondary time series data, for the period 1990 to 2017 , were obtained from various databases, including: the Central Bank of Trinidad and Tobago (CBTT), Handbook of Key Economic and Financial Statistics, the Central Statistical Office (CSO) of Trinidad and Tobago, the Crime and Problem Analysis Unit (CAPA) of the Trinidad and Tobago Police Service (TTPS), the World Bank’s World Development Indicators and the United Nations (UN).

The following is the general form of the model used in the analysis:

RGDP = f (FRD, NAR, INF, GFCF)

Where, Real GDP = The dependent variable; FRD = fraud offences, expected to be positively related to with money laundering, negatively related to GDP; NAR = narcotics offences, narcotics offences can have a negative impact on the economic stability and growth of a country; GFCF = Gross Fixed Capital Formation measures investment. Based on the premise that economic growth is not possible without an increase in capital formation, this implies that investments will have a positive impact on economic growth; INF = Inflation, money laundering can cause fluctuations in the demand for cash, making interest and exchange rates more volatile, and thereby triggering high- levels of inflation.

In order to prevent the occurrence of spurious results, the Augmented Dickey Fuller (ADF) was used to test for stationarity of all variables included in the model. Using the Schwarz criterion for the optimal lag selection process, it was determined that one lag should be included in the model. The results of the ADF tests are summarized in Table 1. The Gross Fixed Capital Formation, Narcotics offences and Inflation variables were determined as I(1) or integrated of the first order at the 5% level of significance. However, both the real GDP and Fraud offences variable were found to be integrated of the second order or I(2), as seen in Table 1.

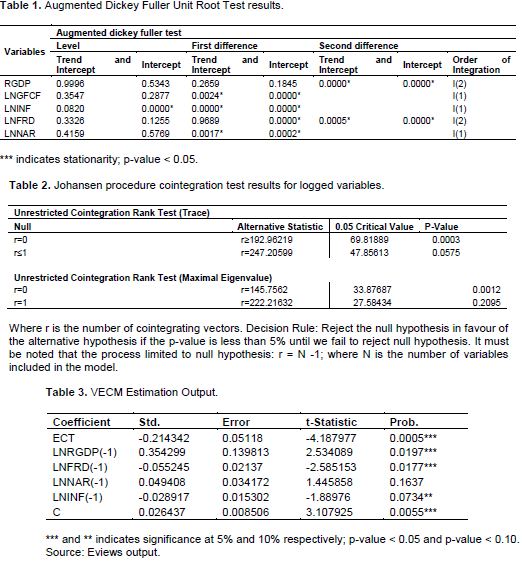

Due to the small sample size, the t-statistics are not valid as the large sample properties do not hold. The p- value criteria at a 5% significance level were used to determine the stationarity or order of integration of the variables. Owing to the sporadic nature of the time series, the intercept and trend assumption would be adopted as the most appropriate test for stationarity. LNGFCF, LNNAR and LNINF were I(1) or integrated of order one whilst LNRGDP and LNFRD were I(2) variables or integrated of the second order. In this study, both LNRGDP and LNFRD were I(2) variables which meant that jointly they form an I(1) process and can be combined with LNGFCF, LNNAR and LNINF, I(1) variables, to test for cointegration, satisfying the condition that all variables be integrated of the same order.

The results from the trace test indicated that there is only one cointegrating equation at the 5% level of significance which was validated by the max-eigenvalue statistic test. This implies that there is in fact a long-run relationship between real GDP, gross fixed capital formation, fraud offences, narcotic offences and inflation (Table 2).

From the above, the cointegrating equation is given as:

lnrgdp = 0.431523lngfcf + 0.067631lnfrd - 0.329627lnnar + 0.116430lninf

The signs are reversed because of the normalization process. All independent variables included in the model were statistically significant, as the estimated p-values related to the coefficients were all less the 5% significance level; (0.02616), (0.04868), (0.04124) and (0.04327).

Results show that the long-run estimated relationship between GFCF and real GDP is positive which aligns with the a priori expectations. The inverse relationship between narcotics offences and RGDP verifies the negative a priori expectation. On the other hand, the positive estimated long-run relationship between fraud offences and RGDP and inflation and RGDP contradicts the a priori expectations. This inconsistency suggests that an increase in fraud offences has the ability of increasing the real GDP of Trinidad and Tobago in the long run. Similarly, the positive relationship between inflation and real GDP implies that increases in the rate of inflation increases the real GDP.

Error correction modelling

Given the variables are cointegrated; it suggests that there exists an adjustment process which prevents the errors in the long run relationship from increasing (Engle and Granger, 1987). As such, VECM can be used since we have a cointegrating equation. The VECM is an appropriate estimation procedure which adjusts to both short run changes in variables and deviations from significant at a 5% level of significance which validated that there is a long run relationship among the variables included in the model. The coefficient of the ECT represents the speed of convergence of the short-run model to the equilibrium. The adjustment coefficient of the ECT informs that the previous year’s deviation from long run equilibrium is corrected in the current period at an adjustment speed of approximately 22%.

The VECM estimations revealed the short run dynamics; the individual lagged coefficients for LNRGDP and LNFRD were statistically significant at a 5% significance level while LNINF(-1) was statistically significant at the 10% significance level. LNNAR(-1) was found to be statistically insignificant within the short-run model. To ensure robust and reliable results the Breusch-Godfrey Serial Correlation LM Test was conducted to test for serial correlation, Breusch-Pagan Test and the Jarque-Bera test were employed to check for heteroscedasticity and normality. Using the p-value approach at a 5% level of significance, we failed to reject their null hypotheses, suggesting that the residuals were normally distributed, homoscedastic and not serially correlated.

The significant negative impact of narcotics offences on economic growth in the long-run is consistent with the both a priori expectations and past empirical literature. On the contrary, the money laundering variable, fraud offences, was ascertained at a 5% significance level to have statistically significant positive relationship on long-run economic growth. This finding contradicts the leading hypothesis that money laundering and economic growth are inversely related.

However, in the short-run, the money laundering proxies exhibited the opposite relationship when compared with long-run estimations. Fraud offence was determined as statistically significant and negative within the short-run model validating that there exists a negative relationship between fraud offences and short-run economic growth. On the other hand, the narcotics offences variable was revealed as statistically insignificant within the short-run model. Though, the estimated coefficient observed indicated a positive relationship in the short-run.

Although, a positive relationship was established between economic growth and the money laundering proxies; fraud offences in the long-run model and narcotics (not statistically significant) in the short-run, it must not minimize the destabilizing effects that money laundering causes the overall economy and the importance of reducing its occurrence. Most theories posit that by neglecting to aggressively fight against m

oney laundering more funds are to be made available for scheming individuals to be reinvested in unlawful activities which can lead to a breakdown of the socio-economic environment.

SUMMARY AND POLICY RECOMMENDATION

The main objective of this study is to evaluate the economic growth- money laundering relationship in Trinidad and Tobago using secondary time series data for the period 1990-2017 using cointegration and ECM techniques. The evidence generated indicates that there is a statistically significant negative impact of narcotics offences on economic growth in the long-run which is consistent with the a priori expectations and past empirical literature. Conversely, fraud offences at a 5% significance threshold, was confirmed as having a statistically significant positive relationship on long-run economic growth. This finding contradicts the leading hypothesis that money laundering and economic growth are inversely related.

In the short-run, the money laundering proxies exhibited the opposite relationship when compared with long-run estimations. Fraud offences were statistically significant and negative, validating an inverse relationship exists between fraud offences and short-run economic growth; while the narcotics offences variable was positive and statistically insignificant within the short-run model.

Although, a positive relationship was established between economic growth and the money laundering proxies; fraud offences in the long-run model and narcotics (not statistically significant) in the short-run, it must not minimize the destabilizing effects that money laundering causes the overall economy and the importance of reducing its occurrence.

In conclusion, the following results were observed: it was determined that money laundering influences economic growth in Trinidad and Tobago in both the short-run and long-run. The effect of money laundering on economic growth is both positive and negative depending on the proxy and time- span; that is, short-run or long-run.

It is critical that Trinidad and Tobago implements specific policies designed to improve mechanisms used to combat money laundering, thus, minimizing the negative impact on economic growth. Policy decisions and appropriate actions must be consistent with the risks faced by Trinidad and Tobago. Given the empirical results, several areas of improvement were identified.

Trinidad and Tobago should strive towards attaining the status of a fully compliant member of the CFATF by improving its partial compliance and non-compliance ratings in the 40 FATF recommendations. Improvement in the effectiveness level ratings is also necessary as currently all 11 categories received a low or moderate compliance rating.

Archaic money laundering regulations and laws urgently need to be updated within Trinidad and Tobago, especially for the gaming sector and LBs which are high risk. The Gambling (Gaming and Betting) Control Bill 2016 is yet to be enacted in Trinidad and Tobago. Focus also needs to be directed on tackling the predicate offences of money laundering as choosing to combat only money laundering instead of fighting the underlying criminal activity can be ineffective.

It is also necessary that the borders of Trinidad and Tobago are effectively monitored and protected to fight against the illegal drug trade. An enhancement of the enforcement capabilities by ensuring that there is adequate, skilled and well-equipped manpower geared towards reducing the incidence of money laundering either through fighting crime, gathering intelligence and conducting investigations can lead to the fair and timely prosecution of guilty parties.

Continuous money laundering risk assessment of various sectors should be conducted to ensure that the necessary resources are allocated proportionate to the risk posed in each sector. Additionally, this can be used to track whether the level of risk within various sectors of the country are increasing or decreasing. This will give an indicator of the effectiveness of the existing regulatory and legal framework aimed at fighting money laundering.

Continuous empirical research should be completed to examine the evolution of the relationship between money laundering and economic growth. It is important that pragmatic research extends throughout the Caribbean. This, however, is restricted due to the unavailability of data. In most instances, only a short time period of available data can be tested as seen in this study.

Additional areas of research can be completed by including other money laundering proxies to the model or creating a new model. Additional money laundering proxies which can be incorporated in econometric testing are the annual STR/SAR (sector specific or aggregate) and the CPI. Alternative econometric models can also be used such as panel estimation or GMM to analyse the impact of money laundering on the economy.

The author has not declared any conflict of interests.

REFERENCES

|

Argentiero A, Bagella M, Busato F (2008). Money Laundering in A Two Sector Model: Using Theory for Measurement. European Journal of Law and Economics 26(3):341-359.

Crossref

|

|

|

|

Barone R, Delle SD, Masciandaro D (2017). Drug trafficking, money laundering and the business cycle: Does secular stagnation include crime?. Metroeconomica 69(2):409-426.

Crossref

|

|

|

|

|

Bett A, Muturi W (2016). Does Economic Crimes Affect Kenya's Economic Growth? A Cointegration Approach. International Journal of Economics, Commerce and Management 4(11):231-250.

|

|

|

|

|

Central Bank of Trinidad and Tobago (CBTT) (2007). Caribbean Financial Action Task Force AML/CFT Compliance Conference.

|

|

|

|

|

Caribbean Financial Action Task Force (CFATF) (2016). Anti-money laundering and counter-terrorist financing measures; Trinidad and Tobago Mutual Evaluation Report.

|

|

|

|

|

Engle RF, Granger CW (1987). Co-integration and error correction: representation, estimation, and testing. Econometrica: Journal of the Econometric Society pp. 251-276.

Crossref

|

|

|

|

|

Financial Action Task Force (FATF) (2019). Improving Global AML/CFT Compliance: On-going Process.

|

|

|

|

|

Financial Intelligence Unit of Trinidad and Tobago (FIUTT) (2017). Financial Intelligence Unit of Trinidad and Tobago Annual Report 2017.

|

|

|

|

|

Financial Intelligence Unit of Trinidad and Tobago (FIUTT) (2018). Financial Intelligence Unit Overview. Accessed December 4, 2018. View

|

|

|

|

|

Gray-Farquharson N (2007). The Observed Effects of Money Laundering for Jamaica. Paper presented at the Caribbean Centre for Money and Finance 39th Annual Monetary Conference, Belize City, Belize, November 6 - 9, 2007. CCMS 2007, St. Augustine.

|

|

|

|

|

Hetemi A, Merovci S, Gulhan O (2018). Consequences of Money Laundering on Economic Growth - The Case of Kosovo and its Trade Partners. Acta Universitatis Danubius. OEconomica 14(3)113-125.

|

|

|

|

|

Jones P (2015). Evaluating the Effects of Money Laundering on the Economic and Financial Stability of Trinidad and Tobago. Department of Economics, UWI St Augustine.

|

|

|

|

|

Kerrigan D, Sookoo N (2013). White-Collar Crime in Trinidad. Gangs in the Caribbean. Edited by Randy Seepersad, Ann Marie Bissessar, Cambridge Scholars Publishing pp. 150-157

|

|

|

|

|

Maurin A, Sookram S, Watson P (2006). Measuring the Size of the Hidden Economy in Trinidad and Tobago, 1973-1999. International Economic Journal 20 (3):321-341.

Crossref

|

|

|

|

|

Peters A (2017). Estimating the Size of the Informal Economy in Caribbean States.

Crossref

|

|

|

|

|

Seuraj S, Watson P (2012). Banking Regulation: does compliance pay? Evidence from Trinidad and Tobago. Social and Economic Studies 61(4):131-144.

|

|

|

|

|

Schneider F, Buehn A, Montenegro C (2010). New Estimates for the Shadow Economies all over the World. Policy Research working paper no. WPS 5356. Washington,DC: World Bank.

Crossref

|

|

|

|

|

Stancu I, Rece D (2009). The Relationship between Economic Growth and Money Laundering - a Linear Regression Model. Theoretical and Applied Economics, Asociatia Generala a Economistilor din Romania - AGER 9(09(538)):3-8.

|

|

|

|

|

Trinidad and Tobago Transparency Institute (TTTI) (2018). Corruption Perceptions Index 2017 shows a high corruption burden in more than two-thirds of countries.

|

|

|

|

|

The Gambling (Gaming and Betting) Control Bill (2016). An ACT to provide for the regulation and control of gaming and betting and matters related thereto, Printed by The Government Printer, Caroni Republic Of Trinidad And Tobago, Legal Supplement Part C to the "Trinidad and Tobago Gazette'', Volume 55, No. 97.

View

|

|

|

|

|

United States Department of State; Bureau of International Narcotics and Law Enforcement Affairs (2017). International Narcotics Control Strategy Report. Volume II- Money Laundering. Accessed July 27, 2018.

View

|

|

|

|

|

United States Department of State; Bureau of International Narcotics and Law Enforcement Affairs (2018). International Narcotics Control Strategy Report. Volume II- Money Laundering. Accessed August 8, 2018.

View

|

|

|

|

|

Villa E, Misas M, Loayza N (2016). Illicit activity and money laundering from an economic growth perspective: a model and an application to Colombia (English). Policy Research working paper no. WPS 7578. Washington, D.C.: World Bank Group. Accessed March 2, 2019.

Crossref

|

|

|

|

|

Vuletin GJ (2008). Measuring the Informal Economy in Latin America and theCaribbean. IMF Working Paper WP/08/102. Washington, DC: International Monetary Fund.

Crossref

|

|