Full Length Research Paper

ABSTRACT

The purpose of this study is to determine the effects of the major macroeconomic indicators on U.S. current account deficit. Using the quarterly data from January 1973 to April 2013, this study attempts to examine whether those factors are truly the cause of massive current account deficit in the United States. We have considered a range of variables such as inflation rate, interest rate, exchange rate, and the gross domestic product (GDP) growth rate. We find in the presence of autocorrelation, the ordinary least square (OLS) coefficients having the right signs, and are statistically significant. However, we conducted the ARMA model to remedy the problem associated with ordinary least square and performed the CUSUM test, QLR test, and the test for serial correlation. The study estimation results suggest that an increase in GDP growth rate, inflation rate, and a decrease in the interest rate causes the country's imports to exceed exports. The trade-weighted U.S. dollar index as a measure of exchange rate did not generate any significant impact on the current account deficit in the study estimation results.

Key words: Current account deficit, inflation rate, GDP growth rate, interest rate.

INTRODUCTION

The current account balance as a percent of gross domestic product (GDP) implies the relative strength of a country in the field of international competition predicated on domestic growth. Usually, countries facing a substantial current account surplus represent a comprehensive dependence on exports revenues, with a high level of national savings. On the other hand, countries experiencing a current account deficit might have a strong dependence on imports, therefore indicating a low level of savings rate and a high personal consumption rate as a percentage of disposable incomes.

Therefore, current account deficit represents a measure of a country's foreign trade imbalance in which the total value of imported goods and services exceeds the value of the exported goods and services. Researchers have investigated the causes of the global imbalances. For example, Chinn (2004) examined various factors indicating that they are intricately intertwined. Therefore, creating "up-hill" flows of excess savings from developing countries with high rates of return to rich countries with low levels of growth, but with more developed financial markets (the "Lucas Paradox").

During the years of 1998 to 2008, economists focused their attention on the various causes and consequences of the expanding current account deficit and surplus. The dynamics of current account balance was revealing from an economic standpoint, as it did not appear to conform to what would be predicted by standard economic theories.

They were troubling from a policy perspective in that they were unprecedentedly large by postwar standards. Holman (2001) analysis reveals that the U.S. current account deficit has grown steadily since 1991, hitting 3.6% of GDP in 1999 and 4.4% in 2000. Much of the rise in the current account deficit over the past decade is related to two factors:

Accelerating the U.S. productivity and a surge in household wealth that is driven by the stock market In an earlier forecasting survey over the past decade conducted by the Wall Street Journal where a group of economists agreed that the current account deficit might be a major threat facing the U.S. economy as elaborated by Ford (2000).

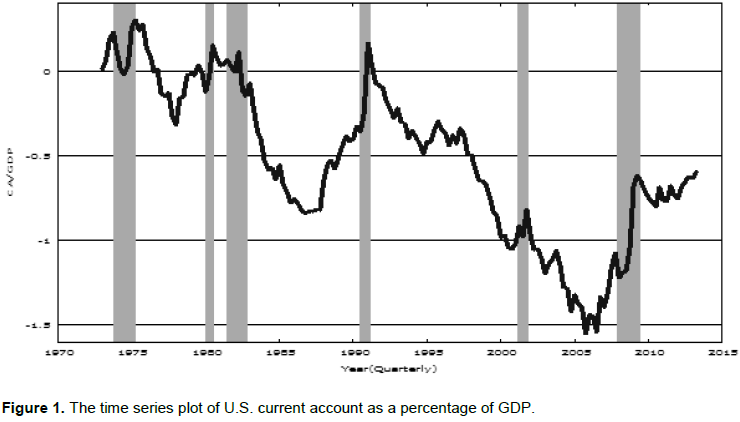

Some policymakers have also suggested that the significant and substantial part of the U.S. current account deficit may be unsustainable and is likely to create problems for the economy. The sharp decrease in current account deficit from the year 2002 to 2007 onward was at 1.5% of GDP. After that, it shows some improvement in that area. However, in the present decade, the growing deficit shows an upward trend over the years. In the recent past years (2012 to 2014), the growing deficits have increasingly raised concerns. Many economists unequivocally agree that the current account deficit is unsustainable and articulated as a major threat facing the U.S. economy. Figure 1 provides a non- stationary graph that exhibits an overall picture of the U.S. current account movement for the period 1970-2013. In this analysis, an unsustainable deficit may trigger a sharp increase in interest rates, as well as a rapid depreciation of the dollar, or some other domestic or global economic disruption.

This study examines the impact of factors−such as inflation rate, the rate of interest, exchange rate, and growth rate of GDP on the large current account deficits facing the United States and also tries to explain the significance of possible consequences.

LITERATURE REVIEW

This study is undertaken to identify and provide remedies on the causes and the consequences of the massive current account deficit facing the United States. Holman (2001) elaborated that the rise in the current account deficit may require a range of other variables. These variables constitute part of the U.S. economy's external sector. They are trade account, foreign financial flows, as well as the currency exchange rate. Changes in the current account deficit are due primarily to the movement in the trade deficit (Figure 1).

The current account deficits are mostly financed by net capital inflows from abroad when the foreign government takes any expansionary fiscal policy. This will depreciates the exchange rate that is related to the current account because international transactions (including trade in goods, services, and financial assets) require exchanging dollars for foreign currencies. Brook et al. (2004) argue that the U.S. current-account deficit was around 5.2 percent of GDP and peaked at its highest level ever recorded in 2005 at 6.4% of GDP. Although it has fallen slightly, it remains significant by historical standards (Figure 1). For a large economy like the United States, a deficit of this amount absorbs a large proportion of total world savings and implies an increasing share of the U.S. assets in foreign investors' portfolios. While the United States remains an attractive investment destination, it remains uncertain for how long foreigners will continue to accumulate debt and equity claims against U.S. residents at the current pace. When the deficit does narrow, however, it will have implications both within and outside of the United States, with specific effects depending on the channels of adjustment.

Edwards (2006) reveals that in 1991, and after eight years of running a deï¬cit, the U.S. posted a current account surplus of 0.7% of GDP. He also mentioned that the current account balance was positive for the last time over the whole decade. Some analysts have become increasingly alarmed by these enormous external imbalances. Some authors have argued that by relying on foreign central banks' purchases of government securities, the U.S. has become vulnerable to changes in expectations and economic sentiments (Feldstein, 2006). Many analysts argued that the U.S. current account deï¬cit of more than 6 percent is clearly unsustainable. And they expected that it would have to be cut approximately in half percentage points over the next few years. And that in the next few years it will have to be cut approximately in half. However, from a global perspective, a reduction in the U.S. deï¬cit implies a decline in the rest of the world's current account surpluses.

Clower and Ito (2011) argued that after the global financial crisis in 2008 and the European debt crisis that followed, sustainability of the U.S. massive debt has been an important consideration for policymakers, especially those in the developed economies. Concerns about the sustainability of deficits and the likelihood of downgrades or speculative attacks on government bonds have made many economies such as the United States and some European countries vulnerable. Causing severe constraints on fiscal policy despite the urgent need for significant stimulus expenditures. Unable to meet those limitations, some economies have already sought out international bail-outs to ensure solvency or short-term liquidity. These countries continue to struggle to meet their debt obligations; others are amassing savings to send abroad. The underlying causes of the global debt crisis of advanced economies are related to the "global imbalances" financed by excess savings of emerging market economies, most notably China, and oil exporting countries. The imbalance capital flows have ensured that some economies run massive current account deficits, and others keep running excess current account surpluses.

Gruber and Kamin (2007) provided reasonable explanations for the global current account imbalances that have been seen in recent years. The large U.S. current account imbalance is associated with the massive surpluses of the Asian developing economies. By using the panel regression approach, they found that the Asian economies surplus might have explained this deficit which was something similar to the one that was adopted by Chinn and Prasad (2003). Their model incorporates per capita income, output growth, fiscal balances, net foreign assets, economic openness, and demographic variables. But their estimated parameters have failed to explain the massive U.S. current account deficit of recent years and the large developing Asian surpluses. However, their model, even augmented by measures of institutional quality, also failed to explain the large U.S. current account deficit. Another study conducted by Ferguson (2005) used the Federal Reserve staff's open economy macroeconomic simulation model to measure the effect of different shocks to the U.S. trade deficit. The rise in U.S. productivity growth, a fall in the risk premium on dollar assets, and the weakening of foreign domestic demand may be contributing factors. Nevertheless, the simulation model is unlikely to capture the relationships determining the external balance, and identifying the shocks affecting the trade deficit are both challenging and subjective.

According to Coughlin et al. (2006), it was worth noting that the current account imbalance has accumulated over relatively long time. The net foreign investment of the United States that is the difference between U.S.-owned assets abroad and foreign-owned assets in the United States has also grown ever larger. Firms build operations in other countries based on plans extending many years into the future. Demographic developments unfold over decades. What may appear to be an imbalance in the short-run is likely to make sense on a long-term basis. The adjustment of the current account is likely to change the foreign exchange value of the U.S. dollar. It is possible that these changes will take place in orderly markets over time. There is no apparent reason that these changes would lead to a financial crisis; as the United States with a stable, very diversified, and growing economy, is not likely to suffer from a lack of confidence by investors so long as it maintains sound economic policies. Obstfeld and Rogoff (2007) took into account terms of trade as well as shifts in the relative price of traded and non-traded goods in a general equilibrium framework analyzed trade imbalance and exchange rate, pointing to a substantially steeper dollar decline. They maintain that the current account deficit running at 4.4 percent of GDP is unsustainable trajectory over the medium term. The inevitable reversal would precipitate a change in the real exchange rate of 12 to 14 percent if the rebalancing were gradual. Therefore, the idea that global imbalances might spark a sharp decline in the dollar value has created considerable skepticism at the time.

The dynamics of U.S. net international indebtedness has been somewhat different from that of the accumulated measure of current accounts, due primarily to the rate-of-return effect highlighted by Gourinchas and Rey (2005). The current account deficits historically predict high future dollar returns on U.S. foreign assets compared to U.S. foreign liabilities.

According to Adalet and Eichengreen (2007) current account strengthens when output was high and weakens when it was low. Its fluctuation was indicative of a country's ability to smooth its consumption. An ongoing current account deficit in a rapidly growing country may also be an indication that investment and growth are not overly constrained by domestic savings capacity, facilitating the country's convergence to a steady-state level of output and capital intensity. In practice, however, these advantages may be neutralized by large or persistent current account deficits that increase the likelihood of disruptive adjustments that produce large output losses. They found a negative correlation between government budget deficit and the incidence of reversal (devaluation of the dollar) in the larger actual sample.

Jarrett (2005) mentioned that the massive deficit in the current account financed with debt may not be sustainable in the long run. Luckily, the U.S. enjoys the benefit of being able to borrow in its currency–the US dollar as the world's primary reserve currency. However, how long this peculiarity would allow the U.S. to continue dodging a disruptive adjustment was difficult to figure out. Although the U.S. is the world's largest debtor, it is still far from being the most significant as a percentage of GDP. In short, trade-related factors are not the only cause of the current account deficit. At present the U.S. economy and the rest of the world are growing at the same rate, the U.S. trade deficit tends to widen. The result of this long-standing trend is that as imports exceed exports by 60%, the dollar value of the imbalance will continue to rise. Backus et al. (2009) revealed that current account deficits did not follow any notable deprecations in U.S. dollar. There has been no connection between the ratio of net exports to GDP and subsequent movements in the real effective exchange over periods of 4 to 16 quarters. In other words, the trade imbalance has not been useful for forecasting future changes in the actual exchange rate.

There is a short-run relationship between the real exchange rate and the trade balance. Fluctuations in real exchange rates (the ratio of international prices to domestic prices) are typically negatively correlated with future trade balances and positively associated with past trade balances.

Warnock and Warnock (2009) used a simple empirical model demonstrating that international flows have a statistically and economically significant impact on the U.S. long-term rates. Using their benchmark-consistent flows, for a monthly sample spanning January 1984 to May 2005 they found that international inflows into U.S. bonds reduce the 10-year Treasury yield by an economically and statistically significant amount. Their model highlighted that the contributing factor to the decline in nominal long-term interest rates from nine percent in 1987 to roughly 5 percent by the end of the 1990s was reductions in inflation expectations and the volatility of long-term rates. International capital flows have a significant impact on the long-term rates. The foreign inflows have a tendency to reduce long-term U.S. rates, as well as to spur the U.S. economic activity. In a global economy substantial amount of capital inflows into U.S. bonds, making the Fed policy that is less restrictive than otherwise. At a sectoral level, one would expect the most interest rate sensitive sector, such as the housing market, to bear the bulk of this effect. Indeed, they show that the U.S. mortgage rates are also depressed by the foreign inflows. A related but less obvious implication is that their results are consistent with the notion that international flows are behind some of the flattening of the yield curve.

Bernanke (2005) has pointed out that the massive U.S. current account deficit would be attributed to an increase in the availability of saving from overseas. He argues that most of the increased flow of international savings has come from developing countries. A development that may be attributed to a significant part to the financial crises we have witnessed in the 80s through 90s. Emerging market financial crises are likely to generate current account surpluses (or lower deficits) through several channels. These channels are: The economy is likely to lose access to foreign credit, obstruction of financial intermediation within the economy, and causing a credit crunch. Balance sheet problems of firms and consumers may restrain domestic spending. The reasons for the widening of the U.S. current account deficit and corresponding tightening of trading partners' imbalances are fairly obvious. These factors are: The rise in the dollar between 1995 and early 2002 (which has given up only part of its gains since then). The pickup in the U.S. real GDP growth rate relative to that of its trading partners. And the higher elasticity of U.S. imports with respect to income than that of the U.S. exports with foreign income (the Houthakkere-Magee effect). Along with the slide in public saving rates, the decline in U.S. private saving since the mid- 1990s could help explain the widening of the United States' current account deficit. However, it is not clear whether the decline in saving has been autonomous, perhaps reflecting Wall Street innovations that have made it easier for Americans to borrow or the endogenous response to other developments.

METHODOLOGY

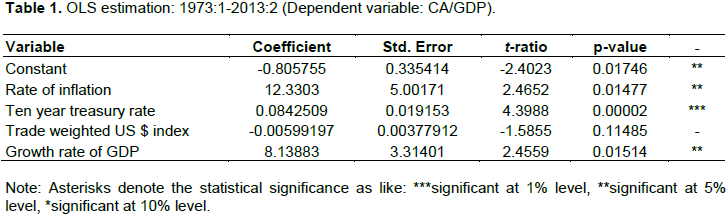

This empirical work uses quarterly data set from the Federal Reserve Bank of St. Louis that covers the period of the first quarter of 1973 to the second quarter of 2013.However, it is useful at the outset to review details of the variables and the sample construction. We use the following parameters to investigate the causes of U.S. trade imbalance as elaborated by prior studies. These are inflation rate, interest rate, exchange rate, and the GDP growth rate. The inflation rate tends to make exports less competitive and imports more attractive.

We took Consumer's Price Index (CPI) for all urban consumers as a measure of the inflation rate. The ten-year Treasury constant maturity rate is chosen as a measure of interest rate. The exchange rate also plays a vital role in the unbalancing current account as the overvaluation of the currency makes import relatively cheaper. On the other hand, the export will become more uncompetitive and is likely to fall.

The trade-weighted index of the U.S. dollar is used as a measure of the exchange rate. We took the balance of the current account in billions of dollars and divided them by nominal GDP to calculate the actual imbalance as a percentage of GDP. In our research, we postulate to survey some of these factors that have been put forward to explain the deficit. As we do so, we will be referring to several macroeconomic simulation models, using Ordinary Least Squares (OLS) model and later the Autoregressive moving average (ARMA) model that are designed to measure the effects of these factors on the U.S. external imbalance.

The time series data and the non-stationary trend of these data set will create biases in the standard errors of the estimates for positive autocorrelation. The estimated standard errors will be smaller than the true standard errors. The result is that one can no longer trust the t−statistics from OLS. The usual OLS equation will therefore be:

Where  is inflation rate in period t,

is inflation rate in period t, is the Ten-year Treasury rate in period t,

is the Ten-year Treasury rate in period t, is the trade-weighted U.S. dollar index, and

is the trade-weighted U.S. dollar index, and  represents the growth rate of GDP, and

represents the growth rate of GDP, and  is expected to capture all the effects of the unobserved factors that can affect current account deficit. The proposed causes of the deficit are by no means mutually exclusive, of course. Table 1 presents the results for the OLS estimates.

is expected to capture all the effects of the unobserved factors that can affect current account deficit. The proposed causes of the deficit are by no means mutually exclusive, of course. Table 1 presents the results for the OLS estimates.

Econometric strategies

The following tests reveal that there is a serious flaw in the conventional OLS model and a structural break on the parameters creating a bias in the standard errors of the estimates.

Serial correlation test

The null hypothesis for the absence of autocorrelation test isrejected. However, the residuals might follow an AR (ρ) autoregressive scheme of up to order 4

CUSUM test

The CUSUM test is a sequential analysis technique used to find structural break on the data. Our findings reveal that there is a structural break on the data as encountered by prior studies as well.

ARMA analysis

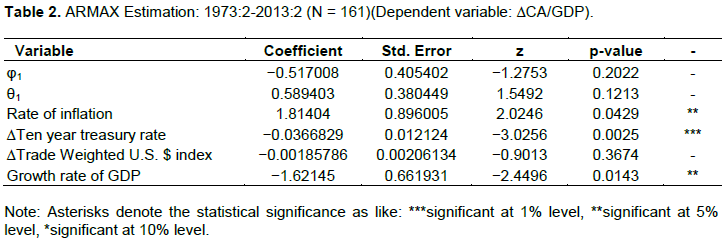

To resolve these problems related to the study estimated OLS model we then run the following Auto Regressive Moving Average ARMA (1, 1) model. We conduct the test for non-stationary nature of our variables as follows. The functional form and the forecasting expansion of the model is follows:

Where ∼ N (0,1 ) is a white noise error term and θ (L) is a polynomial in the lag operator L of order q. The estimation result for the ARMA model is illustrated in Table 2.

RESULTS AND DISCUSSION

A large part of the reason that investors disagree what will be needed to bring current account alignment is that they disagree about what has led the deficit to become so large in the first place. Assuming the increase in the current account deficit has been caused by deficit spending. It is possible to identify reversal of those policies to bring about current account adjustment. Furthermore, if the current account imbalance primarily reflects developments in the private sector, it is more likely that the marketplace will be the source of subsequent correction. Surprisingly, researchers have made relatively few attempts to assess and compare the full range of explanations that have been proposed for the emergence of the large U.S. external deficit. It has been argued that the United States has become a "net debtor" country, increasing the likelihood of currency depreciation and subsequent financial crisis.

Table 1 reveals that the inflation rate has a positive impact on the massive current account deficit. The rate of interest and the GDP growth rate also have positive coefficients. The above findings reveal that the current account deficit will worsen more if there is an increase in the T-bond or T-bills interest rate as well as higher the growth rate. That is an increase in national income, people will tend to have more disposable income to consume goods. In case domestic producers cannot meet the demand, consumers will have to import goods from abroad. In the U.S. we have a high marginal propensity to imports because we do not have a comparative advantage in the production of manufactured goods. Therefore, if there is a faster economic growth imports are expected to increase significantly.

The coefficient of the exchange rate is negative implying dollar devaluation tends to make imports relatively cheap, and tightening current account deficit is likely to improve export. However, this coefficient is not significant at any conventional level of significance.

Table 2 provides some different scenarios in this case. The coefficient of the inflation rate is positive in the ARMA model as well. However, the signs of ten-year Treasury or T-bills rate and the GDP growth rate are negative as compared to the OLS estimates. After making the series stationary (first difference) in nature, the coefficient produced opposite sign. Both of these variables are significant in this case. The Trade-weighted dollar index is negative but insignificant.

CONCLUSION

The U.S. current account imbalance is in danger of falling into a "vicious cycle," as the borrowing required to finance this deficit is likely to crowd out private sector borrowing, and the interest payments required to service our foreign debt will negatively impact the growth rate of GDP. On the other hand, the combination of liberalized financial markets, high real interest rates at home, and economic volatility abroad has attracted massive inflows of foreign capital into the U.S. which in turn have caused a revaluation of the U.S. dollar and making our products less price competitive than our trading partners. Theoretically, deficit financing is likely to raise interest rates making debt more attractive for investors than equity. However, the real sector of the economy is likely to suffer as a result of high-interest rate and subsequent lower economic growth. Indeed, with a current account deficit hovering around 6 percent of GDP and a negative net international investment, some have drawn comparisons with Argentina, Brazil, Mexico and other countries that at times have experienced severe balance-of-payments crises.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Adalet M, Eichengreen B (2007). Current account reversals: Always a problem? NBER Volume title: G7 Current Account Imbalances: Sustainability and Adjustment, University of Chicago. |

|

|

Backus D, Henriksen E, Lambert F, Telmer C (2009). Current account fact and fiction (No. 15525). National Bureau of Economic Research. |

|

|

Bernanke B (2005). The global saving glut and the U.S. current account deficit. Homer Jones Lecture, St. Louis, Missouri. |

|

|

Brook A.-M, Sédillot F, Ollivaud P (2004). The Challenges of narrowing the U.S. current-account deficit and implications for other economies. OECD Econ. Stud. 38(1):157-186. |

|

|

Chinn MD (2004). Incomes, exchange rates, and the U.S. trade deficit, once again. Int. Financ. 7(3):451-469. |

|

|

Chinn MD, Prasad ES (2003). Medium-term determinants of current accounts in industrial and developing countries: an empirical exploration. J. Int. Econ. 59:47-76. |

|

|

Clower E, Ito H (2011). The Persistence and determinants of current account balances: the implications for global rebalancing. Santa Cruz Institute for Int. Econ. 11(9):1-57. |

|

|

Coughlin CC, Pakko MR, Poole W (2006). How dangerous is the U.S. current account deficit? The Regional Economist. pp. 4-9. |

|

|

Edwards S (2006). The U.S. current account deficit: Gradual correction or abrupt adjustment? J. Policy Model. 28:629-643. |

|

|

Feldstein M (2006). The 2006 economic report of the President: Comment on chapter one (The year in review) and chapter six (The capital account surplus) (No. 12168). National Bureau of Economic Research. |

|

|

Ferguson RW (2005). US current account deficit: causes and consequences: a speech at the Economics Club of the University of North Carolina at Chapel Hill, Chapel Hill, North Carolina, April 20, 2005 (No. 93). |

|

|

Ford CM (2000). Economists Split on Fed's Strategy to Curb Inflation. Wall Street Journal, June 3. |

|

|

Gourinchas P-O, Rey H (2005). International financial adjustment (No. w11155). National Bureau of Economic Research. |

|

|

Gruber JW, Kamin SB (2007). Explaining the global pattern of current account imbalances. J. Int. Money Fin. 26(4):500-522. |

|

|

Holman JA (2001). Is the large U.S. current Account Deficit Sustainable? Econ. Rev-Fed. Reserve Bank Kansas City 86(1):5-23. |

|

|

Jarrett P (2005). Coping with the inevitable adjustment in the US current account. OECD Economics Department Working Papers, No. 467, OECD Publishing. |

|

|

Obstfeld M, Rogoff K (2007). The unsustainable US current account position revisited. In G7 current account imbalances: Sustainability and Adjustment (pp. 339-376). University of Chicago Press. |

|

|

Warnock FE, Warnock VC (2009). International capital flows and U.S. interest rates. J. Int. Money Financ. 28:903-919. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0