ABSTRACT

Credit is an important instrument used to improve the welfare of the poor. It could enable the rural households in overcoming liquidity problems, enhancing productive capacity and adopting new technologies. In Ethiopia, the government is promoting microcredit services, but the participation of rural households for credit service is limited. Inappropriate use of loan money also exacerbated the challenges in achieving the desired goal, and consequently, it influenced the loan repayment performance of the household. Therefore, this study was conducted with the aim of identifying socioeconomic factors prompting farm households` participation in Omo Microfinance services and factors determining the utilization of loan money for proposed activities. To conduct this study, 120 rural households were selected randomly from 6 kebeles of Damot Gale District. The participation decision of the households in the credit market and factors determining the level of credit utilization for proposed activity are analyzed using double hurdle model. The study result shows that distance to formal lending institutions, education status, total livestock unit and frequency of contact with extension agents have significantly influenced access to credit. The second hurdle of the model reveals that amount of loan received, peer-monitoring system, expenditure in social festive and frequency of contact with extension agents affected the performance of loan utilization. Therefore, minimizing the barriers of access to credit and considering factors affecting loan money utilization for proposed activity is vital to achieve the desired goal.

Key words: Credit, credit market participation, loan utilization, Omo microfinance, Damot Gale.

Credit is an important instrument to improve the welfare of the poor by enhancing their productive capacity (Okurut et al., 2004) and overcoming liquidity problems (Fuentes, 1996). If it is adequately accessed and used, it would have more impact on technology adoption and poverty reduction (Ebisa et al., 2013). In Ethiopia, wide scale financing started in 1990 with the aim of financing the Market Towns Development Project (MTDP) (Bezabih, 2010). Currently, the government of Ethiopia is promoting micro-credit service via its regulatory frame work and this increased the number and capacity of credit cooperatives and microfinance institutions in the country. Though the government of Ethiopia has put various efforts to solve rural financial problems by extending rural financial institutions, rural households’ participation in credit service is limited (ILRI, 2011). Besides that, inappropriate use of loan money also influenced its effectiveness and loan repayment performance of the household. As a result, lending institutions also faced problems of self and operational sustainability (Mengistu et al., 2013). Therefore, this study identifies socioeconomic factors influencing farm households` participation in formal credit services and factors determining utilization of loan for proposed activities.

Omo Micro Finance institution is among 31 Micro finance institutions operating in Ethiopia (NBE, 2011). It is a widely used microfinance institution in Southern Nation Nationality and People Regional State in general and Damot Gale District in particular.

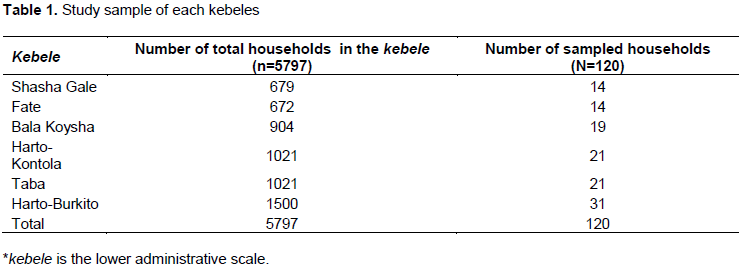

This study was conducted in 120 rural households of Damot Gale District in Southern Ethiopia. The district has 31 administrative kebeles with a total area of 24285.861 ha. Agriculture is the mainstay of people in the district with the major crop production of wheat, teff, maize, and root and tuber crops. Production of cattle, sheep, goat, horse, donkey, mule and poultry is also a very common practice (WARDO, 2014). The study site is selected on the basis of access to credit providing agencies. Data for this study were obtained from randomly selected 120 households from 6 kebeles of the district in proportion to the total number in each kebele, where the sample size was determined using Yamane (1967) formula with 90% confidence interval (Table 1).

The data obtained from rural households were analyzed by using double hurdle model which is firstly proposed by Cragg (1971) with the assumption of that household makes two decision for purchasing an item. For this study, household participation decision in formal credit market and its determinants were identified in the first hurdle; and factors determining the amount of loan money spent for the proposed activity were determined in the second hurdle. For the first hurdle, the dependent variable takes either 0 or 1 value. According to Heckman (1979), and Flood and Grasjo (2001), the function is:

(i) Participation decision:

Under the assumption of independence between the two error terms, the log-likelihood function of the double-hurdle model is equivalent to the sum of the log likelihoods of a truncated regression model and a univariate Probit model (McDowell, 2003; Martinez-Espineira, 2006; Aristei et al., 2007). Consequently, the log-likelihood function of the double-hurdle model can be maximized by maximizing the two components independently: the Probit model (over all observations) followed by a truncated regression on the non-zero observations (Jones, 1989; McDowell, 2003; Shrestha et al., 2006).

The estimated coefficients in the Probit model (first decision) cannot be interpreted in the same way as in a linear regression model but marginal effects have to be analyzed for which the marginal effects show the percent change of the dependent variable. The marginal effects of dummy variables are analyzed by comparing the probabilities of that result when the dummy variables take their two different values 1 and 0. While for continuous variables, the marginal effect is calculated by multiplying the coefficient estimate by the standard probability density function by holding the other independent variables at their mean values (Wooldridge, 2002).

From a total of 120 sampled rural households, 50.83% were formal credit users, while the rest were not. Out of the total credit market participants, 96.7% were borrowed from Omo Micro Finance institution of the district.

Determinants of credit market participation

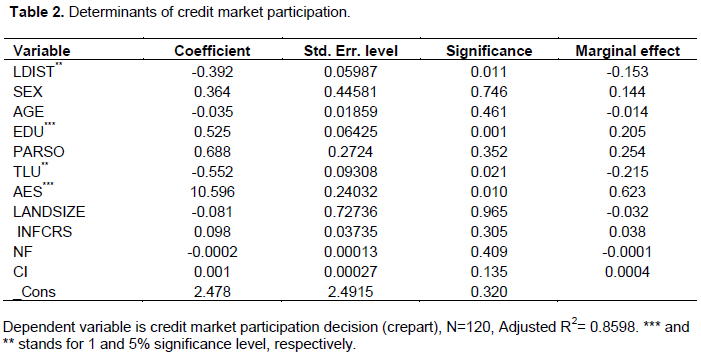

The first stage of double hurdle model of this study employed the maximum likelihood estimation of the probit model in order to estimate the parameters of the variables that are expected to influence the credit market participation decision of the household. In the model, 11 socioeconomic explanatory variables were hypothesized to determine households’ credit market participation and out of them distance to formal lending institutions and total livestock unit were found to influence negatively, and education status of household head and frequency of contact with extension agents were found to have a significant positive impact (Table 2).

Distance of farmers' residence to the nearest lending institutions (LDIST)

In line with a research by Hussien (2007) in Ethiopia, the result of this finding showed that distance of farmers' residences from the nearest MFI is negatively associated with the participation decision of farmers at 5% significance level. The negative association implies that for a unitary increase in a distance between the farmers' residence and the credit market centers, there will be a lesser chance for participating in formal credit market. Farm households with nearby MFIs have a location advantage and use less transportation cost than those far from the institutions. The marginal effect of this variable indicates that, keeping other variables constant, as a distance farmer travels to formal lending institutions increases by one kilometer, the probability of credit market participation decreases by 15.3%.

Education status of household head (EDU)

This continuous variable was determined in number of school years. The highest educational status of the sample respondents were college diploma. This variable had a positive relationship with household decision and found to be statistically significant at 1% significant level. At this significance level, the marginal effect of education on credit market participation decision is 0.205. The positive marginal effect of 0.205 implies that, the probability of change in credit market participation decision increases by 20.5% for a unitary increase in a class year while keeping other variables constant. This result is actually consistent with studies done on adoption of different technologies and credit use by Musebe et al. (1993) and Hussien (2007).

Total livestock unit (TLU)

This variable was found to influence the credit market participation decision of the household negatively and significantly which is supported by the finding of Zelalem et al. (2013). Since livestock are an important source of cash in rural areas, it enables the household to have a better financial position and economic strength to purchase sufficient amount of input without needing credit services. The marginal effect of this variable indicates that, keeping other variables constant, the probability of credit market participation decision decreases by 21.5% as a total livestock unit increases by one unit at 5% significance level.

Frequency of contact with extension agents (AES)

Studies of Holloway et al. (1999) in Ethiopia; Muhongayire et al. (2013) in Rwanda and Sisay (2008) in Ethiopia show that extension contact and its frequency had a significant impact on farmers’ participation decision in credit services. This variable was found to be positively associated with the participation decision of the household in credit market at 1% level of significance. The marginal effect of this variable, which is the probability of change in credit market participation decision for change in frequency of contact with extension agents, is 62.3%.

Determinants of amount of credit utilization for proposed action

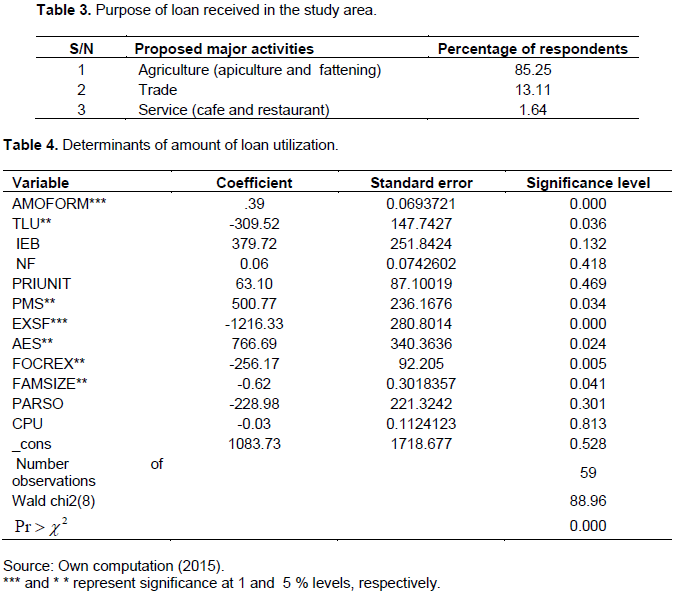

Omo Micro Finance Institution, the largest supplier of loan money in the study area, provides loan for individuals who are interested to involve in either of agricultural activities, service sector, trade, construction or manufacturing sector. Among this, all of the credit users in the sampled households in the study area used a loan for agricultural activities, service sector and trade (Table 3). Out of the credit users, only 16.39% were fully utilized for the proposed activity while the remains used in different levels with maximum of ETB 6000 and mean of ETB 1550.

In order to determine variables that influence the amount of credit utilization for proposed action, 12 explanatory variables were examined and out them 7 were found to be significant. Out of these, amount of loan received, peer-monitoring system and frequency of contact with extension agents were observed to positively influence the amount of loan money utilization on proposed activity while total livestock unit, expenditure in social festive, former credit use experience and family size influenced negatively (Table 4).

Amount of loan received (AMOFORM)

This variable has strongly influenced smallholder rural household loan utilization performance. It was directly related with the dependent variable at 1% significance level. The result shows that a unit ETB increment in the amount of loan money increases the level of utilizing loan money by 0.39 units for the proposed action.

Total livestock unit (TLU)

The second stage results of the model showed that the total livestock unit is associated with the level of utilization of loan money negatively and significantly. The level of utilizing loan money for the proposed activity decreases in ETB 309.52, for one more increment of total livestock unit. This is because the household could meet its input demand from income obtained from livestock products.

Peer-monitoring system (PMS)

This dummy variable positively and significantly affects the level of utilization of loan money in proposed action at 10%. This is because if the borrowed household member has a strong monitoring system on a way of expenditure, its probability of proper utilizing of loan money increases. The study result revealed that the level of utilization increases in 500.77 units if the members have a monitoring system.

Expenditure in social festive (EXSF)

This continuous variable had a negative relationship with household utilization level of loan money for the proposed activity and it was found to be statistically significant at a 1% significance level. The coefficient -1216.33 shows that, a unit ETB changes in the expenditure of social festive affects the level of loan money utilization for proposed action by the amount 1216.33 while other variables are kept constant. The negative relationship indicates that households with more expenditure on social festivals were unable to use loan money properly than those who had less or no expenses at all.

Frequency of extension agents contact (AES)

The result of the study showed that frequency of extension contact is positively and significantly associated with the level of credit utilization of rural household. The level of use from loan money for proposed action increases in 766.69 for an increase in the frequency of extension contact with extension agents. This implies that frequency of extension service had a systematic association with the level of utilization at 1% significance level.

Formal credit use experience (FOCREX)

The second stage of double hurdle model supported that former credit use experience had a negative and significant impact in level of loan money use at citrus paribus. The analysis shows that the level of utilizing from cash credit to proposed activity decreases by 256.17 units when the households had one more year of experience in credit market participation. This is because, since 85.25% of the respondents use credit for agricultural activities, the household purchase the necessary inputs from former loan money.

Family size (FAMSIZE)

This variable was statistically significant at 1% significant level and had a negative effect on the level of credit utilization for proposed activity. The negative relationship indicates that households with more number of family members consume loan money for other personal needs rather than utilizing in the proposed activity. The model output shows that for every increase in the number of household member, the level of utilization from loan money to proposed action decreases by 0.62.

CONCLUSION AND RECOMMENDATIONS

The aim of the study is to assess the socio-economic factors influencing credit participation decision and level of utilization of loan money for proposed activity. Double-hurdle model was used to analyze the data and it is found that frequency of extension service contact, amount of loan received, peer-monitoring system and expenditure in social festive affected the amount of loan utilization to be spent in proposed activity. It is found that only 16.39% fully utilized the loan money for the proposed activity. Therefore, concerning bodies should have to work in improving the performance of loan utilization. Based on the finding of the study, the following recommendations are drawn:

(i) A frequency of contact with extension agents positively affected both accesses to credit and amount of loan utilization for the proposed activity. Therefore, high emphasis should have to be given in providing information about credit-providing institutions and in follow up of loan utilization. Moreover that, it might also help in minimizing rural households expenditure in social festivals.

(ii) Pear-monitoring system, where borrowing members monitor each other, also found as a motivating factor to influence the amount of credit used for the proposed activity. So it is better to develop a strong monitoring system where one follow-up the other. Since distance to the lending institution negatively and significantly affects households’ participation decision, credit providing institutions should have to minimize the barriers by networking them with the main urban and nearby supply of the service.

The author has not declared any conflict of interests.

REFERENCES

|

Aristei D, Perali F, Pieroni L (2007). Cohort, Age and Time Effects in Alcohol Consumption by Italian Households: A Double-hurdle Approach. Empirical Economics 35(1):29-61.

Crossref

|

|

|

|

Bezabih E (2010). Market assessment and value chain analysis in Benishangul Gumuz Regional State, Ethiopia. SID-Consult-Support Integrated Development, Addis Ababa, Ethiopia.

|

|

|

|

|

Cragg J (1971). Some Statistical Models for Limited Dependent Variables with Application to the Demand for Durable Goods. Econometrica 39(5):829-844.

Crossref

|

|

|

|

|

Ebisa D, Getachew N, Fikadu M (2013). Filling the breach: Microfinance. Journal of Business and Economic Management 1(1):010-017.

|

|

|

|

|

Flood L, Grasjo U (2001). A Monte Carlo Simulation Study of Tobit Models. Applied Economics Letters 8:581-584.

Crossref

|

|

|

|

|

Fuentes A (1996). The use of village agents in rural credit delivery. The Journal of Development Studies 33(2):5-22.

Crossref

|

|

|

|

|

Heckman J (1979). Sample Selection Bias as a Specification Error. Econometrica 47(1):153-161.

Crossref

|

|

|

|

|

Holloway G, Nicholson C, Delgado C (1999). Agro industrialization through Institutional Innovation: Transactions Costs, Cooperatives and Milk-Market Development in the Ethiopian Highlands. Mss. Discussion Paper No. 35.

|

|

|

|

|

Hussien H (2007). Farm Household Economic Behavior in Imperfect Financial Markets, Doctoral Thesis, Swedish University of Agricultural Sciences, Uppsala.

|

|

|

|

|

International Livestock Research Institute (ILRI) (2011). Apiculture value chain development, Ethiopia.

|

|

|

|

|

Jones A (1989). A Double-Hurdle Model of Cigarette Consumption. Journal of Applied Econometrics 4:23-39.

Crossref

|

|

|

|

|

Martinez-Espineira R (2006). A Box-Cox Double-Hurdle Model of Wildlife Valuation: The Citizen's Perspective. Ecological Economics 58(1):192-208.

Crossref

|

|

|

|

|

Mengistu K, Mengistu U, Nigussie D, Endrias G, Mohammadamin H. Temesgen K,Yemisrach G(eds.) (2013). Proceedings of the National Conference on 'Loan and Saving: the Role in Ethiopian Socioeconomic Development', Haramaya, Ethiopia.

|

|

|

|

|

McDowell A (2003). From the help desk: hurdle models. The Stata Journal 3(2):178-184.

Crossref

|

|

|

|

|

Moffatt P (2005). Hurdle Models of Loan Default. Journal of the Operational Research Society 56:1063-1071.

Crossref

|

|

|

|

|

Muhongayire W, Hitayezu P, Lee Mbatia O, Mukoya-Wangia SM (2013) Determinants of Farmers' Participation in Formal Credit Markets in Rural Rwanda Determinants of Farmers' Participation in Formal Credit Markets in Rural Rwanda. Journal of Agricultural Science 4(2):87-94.

Crossref

|

|

|

|

|

Musebe R, Oluoch W, Kosura Wangia C (1993). An Analysis of Agricultural Credit Market In Vihiga Division of Kakamega District, Kenya. East Africa Agriculture and Forestry Journal 58(3):4.

Crossref

|

|

|

|

|

National Bank of Ethiopia (NBE) (2008/09-2010/2011). Annual Reports. Addis Ababa, Ethiopia.

|

|

|

|

|

Okurut N, Schoombee A, Van der Berg S (2004). Credit demand and credit rationing in the informal financial sector in Uganda. Paper to the DPRU/Tips/Cornell conference on African Development and Poverty reduction: the Macro-Micro linkage.

|

|

|

|

|

Shrestha R, Alavalapati J, Seidl A, Weber K, Suselo T (2006). Estimating the Local Cost of Protecting Koshi Tappu Wildlife Reserve, Nepal: A Contingent Valuation Approach. Environment, Development and Sustainability 9(4):413-426.

Crossref

|

|

|

|

|

Sisay Y (2008). Determinants of Smallholder Farmers Access to Formal Credit: The Case of Metema Woreda, North Gondar, Ethiopia. MSc Thesis, Unpublished. Haramaya University.

|

|

|

|

|

Woreda Agricultural and Rural Development office (WARDO) (2013). Annual report of Woreda agricultural office.

|

|

|

|

|

Wooldridge M (2002). Econometric Analysis of Cross Section and Panel Data. MIT Press. London, England pp. 551-573.

|

|

|

|

|

Yamane T (1967). Statistics, An Introductory Analysis, 2nd Ed., New York.

|

|

|

|

|

Zelalem G, Hassen B, Jemma H (2013). Determinants of Loan Repayment Performance of Smallholder Farmers: The Case of Kalu District, South Wollo Zone, Amhara National Regional State, Ethiopia. International Journal of Economics, Business and Finance 1(11):431-446.

|

|