Full Length Research Paper

ABSTRACT

The purpose of this paper is to investigate empirical evidence on capital structure determinants in Nigeria. This research has been performed using a sample of 50 companies listed on the Nigeria Stock Exchange from 2001 to 2010. The relationship between the short-term and long-term debt and four explanatory variables were observed. The results of the cross-sectional OLS regression revealed that the static trade-off theory and agency cost theory are relevant to Nigerian companies whereas there was a little evidence in support of pecking order theory. The findings of this study confirm that profitability, growth, firm size and tangibility are explanatory variables of capital structure.

Key words: Capital structure, static trade-off theory, pecking order theory, agency cost theory.

INTRODUCTION

In the past several decades, the role of capital structure has been an important consideration in corporate finance (Chen and Chen, 2011). A number of theories have explained the variations in capital structure across firms and these theories suggest that the selection of capital structure depends on attributes that determine the various costs and benefits associated with debt and equity financing. Modigliani and Miller (1958 and 1963) posit that, in a frictionless world, capital structure is independent of the value of a firm but in a world of tax, value of a firm is influenced by capital structure. Due to Modigliani and Miller hypothesis (1958), three theories have been developed. These theories include static trade- off theory, pecking order theory and agency cost theory. The static trade – off theory (also known as tax-based theory) posits that optimum capital structure is achieved at a point where the net tax advantage of debt financing balances various costs associated with leverages such as bankruptcy cost. Pecking order theory states that companies finance new investment internally with retained earnings, debts and equities. The agency cost theory of capital structure states that an optimal capital structure will be determined by minimizing the costs arising from conflict of interests between the parties involved.

Jensen and Meckling (1976) argued that agency costs play an important role in financing decisions due to the conflict that may arise between shareholders and debt holders. Most empirical studies on capital structure are based on data from developed countries (Rajan and Zingales, 1995; Bevan and Danbolt, 2000 and 2002; Antoniou et al, 2002).

Few empirical researches were conducted on determinants of capital structure in developing countries (Pandey, 2001; Omet and Nobanee, 2001; Al- sakran, 2001; salawu, 2007).

The aim of this research is to provide further evidence on the determinants of capital structures relating to developing countries. The paper concentrates on the structure theory that is relevant in the Nigerian context.

LITERATURE REVIEW

Financial managers should choose an appropriate mix of capital structure so as to maximize shareholders’ wealth. A number of factors have been suggested to have an influence on a firm’s capital structure. There is a wide range of empirical studies on the determinants of firm’s capital structure but the findings of these studies are not consistent in terms of direction and strength of the relationship between capital structure and its determinants. Cross – countries empirical studies (Rajan and Zingales, 1995; Booth et al., 2001) argued that the influence of institutional characteristics is as important as the influence of firm’s characteristics on capital structure. Both theoretical and empirical studies have generated mixed results (Buferna et al., 2008). Some broad categories of capital structure determinants have emerged as a result of various studies.

Bancel and Mitto (2002) conducted a survey on managers of firms in seventeen European countries on capital structure and its determinants. They found that financial flexibility, credit rating and tax advantage of debt are the most important factors influencing debt policy while the earnings per share dilution is the most important factor influencing equity.

Banner (2004) investigated the determinants of capital structure in Czech Republic, Hungary, Poland and Slovak Republic from 2000 to 2001. The research evidence shows that capital structure is influenced by size, profitability, tangibility, growth opportunities, non-debt tax shields and volatility.

Rajan and Zingales (1995) investigated how different country backgrounds affect capital structure among G-7 countries. This research evidence shows that capital structure is affected by bankruptcy laws, the development of bond market and patterns of ownership.

Gleason et al. (2000) examined the determinants of capital structure in the fourteen European countries. They found that legal environment, tax environment, economic system and technological capabilities influence capital structure.

Bervan and Danbolt (2001) examined capital structure of 822 UK companies and found that determinants of capital structure appear to vary significantly depending on the component of capital structure being analyzed. Most of the empirical studies on the determinants of capital structure are based on data from developed countries. It was not until the last ten years that some researchers focused their attention on developing countries, for example, Booth et al. (2001) analyzed data from ten developing countries (Brazil, Mexico, India, South Korea, Jordan, Malaysia, Pakistan, Thailand, Turkey, and Zimbabwe). Pandey (2001) analyses data from Malaysia, Chen (2004) analyses data from China, Omet and Nobanee (2001) analyse data from Jordan, Al-Sakran (2001) utilizes data from Saudi Arabia and Deesomsak et al. (2004) utilize data from the Asia pacific region.

Like other developing countries, research on capital structure determinants is still unexplored in Nigeria only Salawu (2007) has carried out a study in this area. He examined the determinants of capital structure in Nigeria banking industry.

His study revealed that capital structure is influenced by ownership structure and management control, growth opportunity, profitability, issuing cost and tax advantage associated with debt.

In this study, four key variables will be considered as identified in studies by Rajan and Zingales (1995), Bevan and Danbolt (2002) and Booth et al. (2001). The selected explanatory variables are profitability, tangibility, size and growth opportunities. The following three conflicting theories of capital structure will be examined. These include static trade-off theory, pecking order theory and agency cost theory.

Static trade – off theory

The static trade-off theory (also known as tax-based theory) suggests that optimal capital structure could be achieved at a point where the net tax advantage of debt financing balances leverage related costs such as bankruptcy cost. The static trade-off theory states that more debt will be employed by profitable firms since they may likely have high tax burden and low bankruptcy risk (Ooi, 1999).

Um (2001) posits that a high level of profit gives rise to a higher debt capacity and accompanying tax shield. He argued further that firms with high level of tangible assets will be able to provide collateral for debts. If the company defaults on its obligations on debts, the assets will be seized but the company may be in a situation to avoid bankruptcy.

Companies with high level of tangible assets are less likely to default and will be able to secure more debts which may result in a positive relationship between tangibility and capital structure. Most of the empirical studies conducted in developed countries found a positive relationship between tangibility and capital structure, for instance, Titman and Wessels (1988), Rajan and Zingales (1995) among others while empirical studies in developing countries found mixed relationship between tangibility and capital structure; for instance, Wiwattanakantang (1999) in Thailand reported a positive relationship between tangibility and capital structure while other studies showed that tangibility is negatively related to capital structure, for instance, Booth et al. (2001) in ten developing countries, and Huang and Song (2002) in China.

Antoniou et al. (2002) argued that size is a good explanatory variable for a firm’s capital structure. Bevan and Danbolt (2002) assert that large firms tend to hold more debt because they are regarded as “too big to fail” and therefore gain better access to capital market.

Hamaifer et al. (1994) also argued that large firms are able to hold more debt than small firms because large firms possess higher debt capacity. Wiwattanakantang (1999), Booth et al. (2002), Pandey (2001), and Huang and Song (2002) reported a significant positive relationship between capital structure and size in developing countries. Rajan and Zingales (1995) also found a positive relationship between size and capital structure in G -7 counties. On the other hand, Bevan and Danbolt (2002) found that size is negatively related to short – term debt and positively related to long – term debt.

Pecking order theory (information asymmetry theory)

The pecking order theory of capital structure holds that managers or insiders possess private information about the characteristics of the firm’s return or investment opportunities which is not known to common or equity investors.Consistent with the pecking order theory, Titman and Wessels (1988), Ragan and Zingales (1995), Antoniou et al. (2002) and Bevan and Danbolt (2002) in developed countries, Booth et al. (2001), Pandey (2001), Wiwattanakantang (1999), Chen (2004) and Al-Sakran (2001) in developing countries reported a negative relationship between profitability and capital structure. Booth et al. (2001) found a positive relationship between growth and capital structure except for South Korea and Pakistan. Pandey (2001) reports a positive relationship between growth and capital structure in Malaysia.

Titman and Wessels (1988) and Rajan and Zingales (1995) found a positive relationship between tangibility and capital structure for developed countries whilst Wiwattanakantang (1999) reported that a positive relationship exists between tangibility and capital structure in Thailand and South Korea, respectively.

Agency cost theory

Debt agency cost arises as a result of conflict of interests between debt providers and shareholders on one hand and, shareholders and managers on the other hand (Jensen and Meckling, 1976). The use of short-term sources of debt may reduce the agency problems.

Titman and Wessels (1988) argued that agency related costs between shareholders and debt holders are likely to be higher for firms in growing industries, hence, a negative relationship is expected between growth and capital structure. Consistent with these predictions,Titman and Wessels (1988), and Rajan and Zingales (1995) reported a negative relationship between growth and capital structure in developed countries.

Jensen and Meckling (1976) asserted that the use of secured debt might mitigate agency cost of debt. Um (2001) asserts that if a firm’s level of tangible asset is low, the management may choose a high level of debt to mitigate equity agency costs. Therefore, a negative relationship between tangibility and capital structure is consistent with an equity cost explanation.

This study aims to present empirical evidence on the determinants of capital structure in Nigerian context. This study also provides as avenue to access the private sector in Nigeria, identify its constraints and proffer solutions. Another issue in prior research is the robustness of results under different estimation techniques and different measures for both the dependent and the explanatory variables. Limiting the data analysis to certain estimation techniques for dependent and explanatory variables may produce subjective results.

Therefore, it is important to conduct a comprehensive analysis that considers these issues in order to avoid such bias.

This study will provide empirical evidence on the model of capital structure that is applicable to Nigerian firms. Extending the debate beyond debt – equity mix is important in Nigerian context because there is no perfect capital market from which firms can raise capital. The research will help policy makers on how they can use policy to reduce financial constraints for firms so that they can have a wider and affordable choice of finance resources. It is perceived that the result of the study will serve as a guide to researchers in conducting future studies on the determinants of capital structure in Nigeria.

RESEARCH DESIGN AND METHODOLOGY

The broad objective of this research is to investigate the determinants of capital structure in Nigerian context. The data to be used for the purpose of this study will be obtained from balance sheets and income statements of 50 companies quoted on the Nigerian Stock Exchange (NSE). A period of 10 years will be considered (2001 – 2010). The data will be averaged over the 10-year period to smooth the capital structure and explanatory variables. To test the hypothesis, the relationship between the level of debt and four explanatory variables representing profitability, growth, tangibility and size will be examined using ordinary least square regression.

The study will decompose debt into long-term and short –term debt. The debt ratios to be considered are total debts to total assets, short-term debts to total assets and long –term debt to total assets. Tangibility will be measured by the ratio of fixed assets to total assets, growth will be measured by the percentage change in the value of total assets, size will be measured by the natural logarithm of assets and profitability will be measured by the ratio of profit before tax to the book value of total assets.

Bevan and Danbolt (2002) argued that studies on the determinants of capital structure based on total debt may disguise the significant differences between long-term debt and short – term debt.

Consistent with Bevan and Danbolt (2002) and Michaels (1998), this study decomposes debt into long-term and short-term debt. Total debts to total assets, short-term debts to total assets, and long-term debts to total assets are the debt ratios to be considered. The cross – sectional regression to be used in this study is based on models used in Rajan and Zingales (1995), Bevan and Danbolt (2002), with some adjustments on both the leverage and explanatory variables.

In line with studies by Rajan and Zingales (1995), tangibility is measured by the ratio of fixed assets to total assets and growth is measured by market to book ratio of assets.

The first regression model to be used for the study is as follows:

Z= α + β1Xn +β2D +β3XnD +µ

Where:

Z represents capital structure or leverage

α represents the intercept

Xn represents the explanatory variables (n=1, 2, 3 and 4)

1- Profitability is measured by the ratio of profit before tax to the book value of total assets

2- Growth is proxied by the percentage change in the value of assets

3- Tangibility is proxied by the ratio of fixed assets to total assets

4- Size is proxied by the natural logarithm of total assets

D represents a dummy value

µ is the stochastic error term

The second regression analysis with four dummy variables is done to examine industry classification effect with the manufacturing industry as the intercept. DR (firm i) is the dependent variable in all regression models representing the two long-term debt ratios for each firm and D1 to D4 represent the four industry dummies utility, real estate, conglomerate, and oil and gas respectively.The variables are defined as follows:

DR (firm i) = α + β1D1 + β2D2 +β3D3 +β4D4 + µ

The third regression analysis is done to estimate whether firm characteristic variables influence capital structure.

The model is stated as follows:

DR (firm i) = α + β1T + β2S +β3G + β4P

Where α= intercept

T = Tangibility

S = Size

G = Growth

P = Profitability

DR (firm i) = α +β1D1 +β2D2 +β3D3 +β4D4 +β5T + β6S + β7 G + β8P

Most studies of this nature focus on quoted companies as the units of measurement. The reason is that such firms have a wide range of sources for raising capital. This study also uses quoted companies as the units of measurement.

The fourth regression model includes both industry dummies and firm characteristic variables. This model is developed to provide an explanation on whether firm characteristics are significant in explaining the choice of capital structure after controlling for variation across industries,

ANALYSIS AND RESULTS

The variables used for the purpose of the study were deflated by the book value of total assets according to Bevan and Danbolt (2000 and 2002) to control for potential heteroscedasticity. This study also employs White (1980)’S heteroscedasticity-consistent standard errors and covariance so as to mitigate heteroscedasticity in calculating the T-statistics. As could been seen in Table 3 , explanatory variables provide high explanatory power as provided by R2 values of 0.90 for total debt, 0.86 for short-term debt and 0.72 for long-term debt respectively.

Significant positive slope coefficients are expected for explanatory variables such as profitability, tangibility and size if the static trade-off theory holds. There is a strong evidence for the static trade off theory for total debt and long-term debt as revealed by the coefficients of profitability and size. Given that most Nigerian companies rely on long-term debt, there is a strong support for the static trade-off theory. This shows that larger companies with higher profits will have higher debt capacities and thus, will be able to borrow more and take advantage of any tax shield.

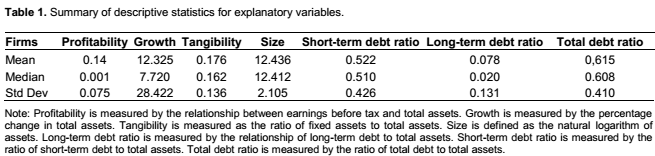

The results of various explanatory variables and leverage measures for selected firms are summarized in Table 1. It could be seen that Nigerian companies have a low rate of profitability (14%). The growth rate on average is 12.33%. Correlation matrix of the leverage and explanatory variables are presented in Table 2. The results revealed that growth and size are positively related to profitability whereas tangibility has a negative relationship with profitability. This justifies that large firms and growing firms tend to have higher profitability whereas less tangible assets are possessed by profitable firms (Table 4).

Although the correlation matrix ignores joint effects of more than one variable on leverage, the tangibility and growth variables have positive correlation with long term debt and a negative correlation with short-term debt ratios. This implies that growing firms and firms with high levels of tangible assets tend to use long-term debt rather than short-term debt. Large and profitable firms are more likely to use long-term debt and less likely to use short-term debt.

CONCLUSION

The findings of this paper provide further evidence on capital structure determinants in Nigeria during the period of 2001 to 2010. The relationships between short-term and long-term debt and four explanatory variables such as profitability, growth, tangibility and size were examined to explain the capital structure theory that is relevant in Nigerian context.

The results show that profitability and size are negatively correlated with short-term debt ratio and positively correlated with long-term debt ratio and total debt ratio.

The results also show that growth and size are positively correlated with profitability whereas negative relationship was found between tangibility and profitability. Given that most Nigerian firms rely heavily on long-term debt, there is a strong evidence for static-trade off theory. A significant negative correlation was found between tangibility and leverage which provides further evidence in support of agency cost theory.

The results suggest that both static trade-off theory and agency cost theory are relevant theories in Nigeria whereas there was a little evidence in support of pecking order theory.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Al-Sakran S (2001). Leverage Determinants in the Absence of Corporate Tax System: The Case of Non-financial Publicly Traded Corporation in Saudi Arabia. Manage. Financ. 27(10):58-86. |

|

|

Antoniou A, Guney Y, Paudyal K (2002). Determinants of Corporate Capital Structure: Evidence from European Countries. Working paper, University of Durham. |

|

|

Bancel F, Mitto U (2002). European Managerial Perceptions of the Net Benefits of Foreign Stock Listings. J. Financ. Manage. 7(2):213-236. |

|

|

Banner P (2004). Capital Structure of Listed Companies in Visegrad Countries. Research Seminar Paper Presented at Seminar for Comparative Economics, LMU, Munich. |

|

|

Bevan A, Danbolt J (2000). Dynamics in the Determinants of Capital Structure in the UK. Working Paper, University of Glasgow. |

|

|

Bevan AA, Danbolt J (2001). Testing for Inconsistencies in the Estimation of UK Capital Structure Determinants. Working paper 2001/4, Department of Accounting and Finance, University of Glasgow. |

|

|

Bevan A, Danbolt J (2002). Capital Structure and its Determinants in the UK: A Decompositional Analysis. J. Appl. Financ. Econ. 12(3):159-170. |

|

|

Booth L, Aivazian V, Demirguc- Kunt A, Maksimovic V (2001). Capital Structures in Developing Countries. J. Financ. 56(1):87-130. |

|

|

Buferna F, Bangassa K, Hodakinson L (2008). Determinants of Capital Structure: Evidence from Libya. Research Paper Series, University of Liverpool. |

|

|

Chen J (2004). Determinants of Capital Structure of Chinese Listed Companies. J. Bus. Res. 57(12):1341-1351. |

|

|

Chen S, Chen L (2011). Capital Structure Determinants: An Empirical Study in Taiwan. Afr. J. Bus. Manage. 5(27):10974-10983. |

|

|

Deesomsak R, Paudyal K, Pescetto G (2004). The Determinants of Capital Structure: Evidence from the Asia Pacific Region. J. Multinatl. Financ. Manage. 14(4-5):387-405. |

|

|

Gleason K, Mathur L, Mathur I (2000). The Interrelationship between Culture, Capital Structure and Performance: Evidence from European Retailers. J. Bus. Res. 50(2):185-191. |

|

|

Huang S, Song F (2002). The Determinants of Capital Structure: Evidence from China. Working Paper, University of Hong Kong. |

|

|

Jensen M, Meckling W (1976). Theory of the Firm: Managerial Behaviour, Agency Costs and Ownership Structure. J. Financ. Econ. 3(4):305 -360. |

|

|

Michaels N (1998). Financial Policy and Capital Structure Choice in UK Privately held Companies. Unpublished Ph.D Thesis. Manchester Business School, University of Manchester. |

|

|

Modigliani F, Miller M (1958). The Cost of capital, Corporation Finance and Theory of Investment. Am. Econ. Rev. 48:261-297. |

|

|

Modigliani F, Miller M (1963). Corporate Income Taxes and the cost of Capital: A correction. Am. Econ. Rev. 53:433- 443. |

|

|

Omet G, Nobanee H (2001). The Capital Structure of Listed Industrial Companies in Jordan. Arabic J. Adm. Sci. 8:273-289. |

|

|

Ooi J (1999). The Determinants of Capital Structure. Evidence on UK Property Companies. J. Property Invest. Financ. 17(5):464-480 |

|

|

Pandey M (2001). Capital Structure and the Firm Characteristics: Evidence from an Emerging Market. Working Paper, Indian Institute of Management. |

|

|

Rajan R, Zingales L (1995). What Do you know about Capital Structure? Some Evidences from International Data. J. Financ. 50(5):1421-1460. |

|

|

Salawu RO (2007). An Empirical Analysis of the Capital Structure of Selected Quoted Companies in Nigeria. Int. J. Appl. Econ. Financ. 1:16 -28. |

|

|

Titman S, Wessels R (1988). The Determinants of Capital Structure Choice. J. Financ. 43(1):1-19. |

|

|

Um T (2001). Determinants of Capital Structure and Prediction of Bankruptcy in Korea. Cornell University: Unpublished Ph.D Thesis. |

|

|

White H (1980). A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity. Econometrical, 48(4):817-838. |

|

|

Wiwattanakantang Y (1999). An Empirical Study on the Determinants of Capital Structure of Thai Firms. Pacific- Basin Financ. J. 7(3-4):371-403. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0