Full Length Research Paper

ABSTRACT

The information content of dividend hypothesis has been a controversial debate for a number of decades. This research therefore examines the validity of information content of dividend hypothesis and the reaction of share prices to dividend change announcements that contradict the market phase. That is, observing the reaction of the market to the announcements of dividend decrease (increase) when the market is in a bull (bear) market phase. This is because a bull market is generally characterized by persistent increase in share prices, higher financial wellbeing and strong investor interest. While the bear market on the other hand, is seen as the opposite of the bull market cycle. Using the OLS method of regression and the market model, it was observed that investors have a higher expectation with respect to their investments (in terms of dividends) when the market is in a bull phase and vice-versa in the case of the bear market. The results of this research give a strong backing for the information content of dividend hypothesis as it was discovered that dividend change announcements are positively related to share prices. That is, investors earn abnormal returns around dividend change announcement day especially those that contradict the market phase. The findings of this study also show that investors have similar investment behaviour across different financial markets even in a contradicting bull and bear market phase.

Key words: Dividend announcement, share prices, bull and bear market.

INTRODUCTION

Dividend is seen as an important means of communication between the management of a firm and its investors. It is believed that stockholders do not have sufficient information about the true situation of the firm and therefore see dividend paid out as providing inside information about the company (Bhattacharya, 1979). According to Richardson (2000), when information asymmetry between shareholders and management is high, shareholders have insufficient resources and information for monitoring the action of managers. Investors thereby tend to engage in the practice of earnings and dividend management. In this vein, Pettit (1972) points out that firms in most cases have the tendency to announce dividend increase only in situations when profit is estimated to be high enough and expected future cash flow would be sufficient to sustain the increase in dividend payments. The announcement of a decrease on the other hand, is made when estimations of the management about the future cash flow is seen to be insufficient to continue the present dividend paid out which Below and Johnson (1996) referred to as management’s last resort. Shareholders can therefore take the increase or decrease in dividend as an information and signal from the management about the state of the company. It is therefore expected that when a firm announces an increase, it is seen as a positive signal that the firm has good prospects thereby leading to the purchase of its stocks and vice versa in the case of a dividend decrease announcement.

Gonzalez et al. (2005) described a bull market as a market cycle characterized by persistent increase in share prices, higher financial wellbeing and strong investor interest. While the bear market on the other hand, is seen as the opposite of the bull market. With respect to this definition, Below and Johnson (1996) investigated the S&P 500 index to determine if dividend announcements which contradict the market phase convey any signal to the market. It was observed that the positive reaction of the market to dividend increase announcements when the market was in a bear phase was statistically significant than the market’s reaction to dividend increase announcements when the market was in a bull phase. It was also discovered that the market reacts more negatively to dividend decrease announcements especially when the market was in a bull phase.

Many empirical studies have been carried out using both developed and emerging markets to determine the validity of signalling theory and the findings have yielded mixed results. More so, little research has been carried out to determine the validity of signalling theory when dividend announcements that contradict the market phases are made. The identified research that looked at this area was by Below and Johnson (1996) which looked at the S&P 500 index which is an index in the US stock market. This study therefore looks at the FTSE 100 index, an index in the London Stock Exchange to determine if the behaviour of investors in the US (S&P 500) also applies to investors in the UK (FTSE 100) with respect to the validity of the signalling theory as well as the impact of dividend announcements that contradict the market phase.

Aims and objectives

This research aims to determine if investors see increase or decrease in dividend announcements as conveying any information (signalling theory) about the future of a security thereby acting on it by either responding positively or negatively to such announcements. Further-more, it aims to examine if dividend announcements contradicting the market phase convey any extra information to the market thereby having impact on share prices. It also purposes to investigate whether investors react more to the announcement of dividend decrease when the market is in a bull phase than a decrease in a bear phase and vice-versa. It also aims to investigate if investors have similar investment behaviour irrespective of their location.

Research questions

1. Does dividend announcement send any signal to the market?

2. Do investors react more to dividend announcements that contradict the market phase (bull and bear)?

Expectations

It is expected that for signalling theory to be valid, dividend announcements that contradict the market phase (i.e. the announcement of a decrease in dividend when the market is in a bull phase and an increase in dividend when the market is in a bear phase) should convey more information about a security than when dividend announcements move in the same direction with the market phase. It is also expected that a security should have higher negative abnormal return when dividend decrease is announced in a bull phase than in a bear phase. Similarly, a security with dividend increase in a bear phase is expected to have higher positive abnormal return than increase in a bull phase.

Structure of study

Having introduced the research in Section 1, Section 2 provides in-depth review of past empirical studies on dividend theories as well as the effect of dividend announcements on investors and returns. Section 3 focuses on the research methodology, statistical issues, data sampling and sources. Section 4 comprises data analysis and interpretation of results while Chapter 5 concludes with the summary and necessary recommendations.

LITERATURE REVIEW

Quite a number of event studies have been carried out in Economics and Finance researches to discover the impact dividend announcement has on share prices. Some empirical evidences have shown that in most of the cases, investors react positively to the announcement of an increase in dividend while the announcement of a decrease on the other hand brings about negative reactions. Other researches, on the other hand, show that there are no relationships between dividends announced and market reaction.

MacKinlay (1997) pointed out that the focus of an event study is to establish the impact an event has on security’s value especially the common equity class of security. A study by Dolley (1933) was perhaps the first to make public a research on event studies. The study examined the effect stock-splits have on share prices using a sample of 95 splits between 1921 and 1931. Out of these 95 samples, 57 cases were found to experience increase in prices while 26 cases experienced fall in prices.

Frankfurter et al. (2003) define dividend as present or past earnings distributed to shareholders of a firm in a proportion that is equal to their ownership in the firm. They went further to divide this definition into three different components, the first is that dividend can only be distributed from a firm’s after tax earnings. Secondly, dividends must be distributed in the form of real assets that is, either cash or extra shares. Lastly, stakeholders have their share of dividend according to the portion of their holding in the firm. Dividends are therefore seen by shareholders as income and are therefore, looked forward to. Frankfurter et al. (2003) went further to point out that what does not seem to fit into context is the fact that shareholders see an announcement of an increase in dividend as good news while the announcement of a decrease is considered as bad news suggesting that there is an impending financial doom. They described this incongruity as what Black (1976) referred to as “dividend puzzle”. According to Bhattacharya (2007), despite the fact that dividend policy has been studied for some decades, it has not been completely understood those factors that influence dividend policy as well as the manner of interaction between these factors.

Asymmetry information/signalling theory and dividend policy

The major debate that surrounds the effect of dividend announcement on share prices centres on the type of information that is conveyed to the market by the announcement of a change in dividend. A number of empirical evidences have used the “signalling theory” which was developed by Spence (1973) to determine the role of dividends in conveying information to market participants. The phrase “information content of dividend” according to Watts (1973) refers to a statement of hypothesis which says that dividends convey information about a firm’s expected earnings and this information allows the market participants to predict expected earnings in a more accurate way.

Arguments in favour of signalling theory

Some of the earlier empirical evidences favouring the existences of signalling theory are Bhattacharya (1979), Asquith and Mullins (1983), Aharony and Swary (1980), John and Williams (1985) etc. Bhattacharya (1979) shows that shareholders are not perfectly informed like the managers about the state of the firm and that the size of a dividend policy does convey signal of the expected cash flow. It was also pointed out that there is a high transaction cost involved in the payment of dividends as well as the fact that dividends are highly taxed when compared to capital gains. These lead shareholders to believing that the firm is profitable and as such investing more in the firm which push share prices further up and ultimately leading to increase in expected earnings. Richardson (2000) also confirms that when information asymmetry is high, shareholders have insufficient resources or information for monitoring the action of managers thereby result to engaging in the practice of earnings and dividend management. In this view also is Brickley (1983) who supports the notion that managers use the announcement of dividend increase especially “labelled” increase such as year-end, special or extra dividend to convey positive information to the shareholders about the potential prospects of the firm in the future.

A research by Healy and Palepu (1988) posits that dividend initiating firms have positive changes in earnings before and after the announcement of increase in dividend while non-dividend paying firms on the other hand, experience negative abnormal returns. It also suggests that earnings analysts depend on dividend announcements because subsequent changes in earnings have a positive relationship with dividend announced and the reaction of stock prices after the announcement of earnings are found to be less than usual. The result therefore concludes that investors see dividend omission and initiation announcements as reflecting the expectation of the management with respect to changes in future earnings.

Like Ahrony and Swary (1980), Leftwich and Zmijewski (1994) investigated the information content of quarterly earnings and dividend announcements. The study acknowledges that both announcements have information content than any other type of announcements such as stock splits repurchase etc. It however contradicts Ahrony and Swary (1980) by affirming the claims of Gonedes (1978) that earnings announcement provide more information content than dividend announcement and the latter only conveys little (if any at all) information that has not been conveyed already by its counterpart i.e. the earnings announcement.

A recent research by Bozos et al. (2011) examined a developed market, the London Stock Exchange (LSE) during the period of economic adversity in 2007 and 2008. It was affirmed that there is a significant positive relationship between dividend announcements and stock prices. The testing of the dividend signalling hypothesis also proves that dividends pass less information during the boom period but have more information content during economic adversity.

A unique financial environment of the Muscat Securities Market in Oman was examined by Al-Yahyaee et al. (2011) between 1997 and 2005. The Oman financial market is an emerging market and seen as unique because of four major factors.

The first is the fact that dividends are not taxed; secondly, citizens invest highly in the stock market. Thirdly, the management of firms are not very transparent and lastly, dividends are changed frequently by firms. It was observed that the market begins to react to changes in dividend from a day to the announcement which also suggests that information is being leaked into the market. The major impact of the dividend announcement was on day 0 when the announcement was made with a positive average abnormal return of 5.78% in the case of an increase and negative average abnormal returns of 2.49% in the case of a decrease. The results of this study therefore support the claims that dividend announcements do have information content which is passed to the market. The market also reacts positively to dividend increase announcement and negatively to dividend decrease announcement especially in Oman. Similarly, Adelegan (2003) studied the Nigeria Stock Exchange (NSE) which is also a developing market and concluded with the same results except that in the case of the NSE, the market begins to react to information 30days prior to the announcement day which also suggests the existence of insider trading as observed by Ariff and Finn (1989).

A pretty recent study by Dasilas and Leventis (2011) using the market model, investigates the reactions of the Greek stock market to dividend announcements for the period 2000-2004 taking their sample to include all firms listed in the Athens stock Exchange during this period. This period can be seen as a recession period which developed after the dot.com and technology boom of the Y2K syndrome. They defined the event period to include day -1 which is the day before the announcement, day 0 which is the day of the announcement and day +1 which is the day after the announcement. More so, in order not to contaminate their result, they excluded days that have other announcements such as earnings, right issues, stock splits and stock dividends as the usual practice in Greece is a joint announcement of dividends with other earnings.

The results of the study indicate a positive reaction of stock price to dividend announcement on day 0 at 0.374% also, a CAR on the day before the announcement (day-1) and the day of the announcement (day0) of 0.694%. Both the reaction of stock prices to dividend changes and CAR are statistically significant at 10% level of significance. It therefore concludes that the null hypothesis that dividend announcement is not significant to share prices should be rejected and supporting the existence of the “informational content of dividends hypothesis”.

Arguments against signalling theory

However, some empirical evidences have stated the opposite that dividend does not convey informational content to investors and even if it does, it is not pronounced. Among of the first of these researchers is Watts (1973) who argues that dividends do not convey as much information as claimed by the dividend theory. The results of the test conducted by Gonedes (1978) agree with Watts (1973) that dividend signals do not disclose any exceptional management information beyond any information conveyed by earnings. Kalay (1980) agrees that the informational content of dividend cut cannot be refuted but not all dividend cuts can be seen as a signal of a firm’s expectation of low future earnings. It was stated that dividend cuts could also be as a result of constraints such as tax and transaction cost which are out of the manager’s discretion. This was described as ‘forced reduction’ hence, does not convey a firm’s expected earnings.

Black (1998) purports that dividend changes or elimination could be as a result of a firm wanting to save taxes for the benefit of its shareholders. A fall in share prices would be temporary and would eventually return to its initial level before the cut or even higher. It was although confirmed that dividend policy of a firm may express the mind of the managers in that, managers in most cases prefer not to reduce dividend and will therefore only increase dividend when they are certain that the expected cash flows of the firm will be sufficient to pay the increased dividend for a period of time which will in turn increase share prices. Dividend decrease on the other hand, is made when the managers see a poor prospect for a quick recovery which also leads to a drop in share prices.

A more recent research by Uddin and Chowdhury (2003) took a sample of 137 dividend paying companies that are listed on the Dhaka Stock Exchange and concluded that dividend announcement has no effect on shareholders’ value. It was discovered that about 20% of shareholders’ value was lost over a period of thirty days before the announcement through to thirty days post announcement. An increase in the Cumulative Abnormal Return (CAR) was observed before the announcement of an increase in dividend which later became negative after the announcement. He went further to explain that the negative CAR could be as a result of tax on dividend which would be added to investor’s overall tax payable. It was therefore concluded based on the evidences from the DSE that investors do not gain from the announcement of dividends and reemphasizes the irrelevancy of dividend hypothesis proposed by Miller and Modigliani (1961).

To investigate the relationship between dividend changes and future profitability, Nissim and Ziv (2001) examined a large sample of 100,666 dividend changes starting from the second quarter of 1963 through to the first quarter of 1998. In estimating expected profitability, Nissim and Ziv (2001) used the regression model and like earlier studies calculated abnormal earnings as the actual change in earnings less the expected change. The initial result was similar to prior studies i.e. changes in dividend has no positive relationship with changes in future earnings. The regression model was then modified to address omitted correlated variables and measurement errors. A different result was realized which supports the signalling theory hypothesis stating that dividend changes has a positive relationship with changes in future earnings for two consecutive years after dividend change. The paper went further to contend that prior studies have failed to discover the actual relationship between dividend changes and changes in earnings because the wrong model has been used. From the analysis of past empirical evidences, it can be noted that there are mixed opinions about the effect of dividend changes on share prices and it is therefore, inconclusive. It can also be observed that more focus has been placed on whether or not dividends do have informational content. The gap this research aims to fill in addition to testing the signalling theory hypothesis is to determine if changes in dividend that contradicts the market phases (bull and bear) convey any significant information to the market which in this case, is the FTSE100 index. It also aims to determine if the behaviour of investors in the FTSE100 is similar to the investment behaviour of the S&P 500 examined by Below and Johnson (1996), which could then be inferred that investors have similar investment behaviour across markets.

METHODOLOGY

Research data

The population to be investigated in this study comprises the 100 companies listed in the FTSE 100 and the time series secondary data is extracted from the Reuters Database for both the bull and the bear market phases. The sample cuts across all sectors e.g. financial, telecommunication, oil and gas, utilities etc. The FTSE is used because it is made up of the largest capitalized companies in the UK and the index exists in a developed market where transparency rules apply. More so, it is a widely used index for the purpose of analysis and data is easily obtainable. The study makes use of daily closing trading prices for each of the selected securities and the index which are required in calculating the daily share price and market returns. The share prices were also obtained from Reuters Database.

To test the effects of dividend announcements on share prices, the final dividend dates were obtained from the Reuters Database. Similar to Dasilas and Leventis (2011), this research defines the announcement dates used as the days which the company declares its intention to pay the next dividend. The ex-div dates or the dates the dividend will be paid are not considered as it happens after the event and the reaction of investors mostly surrounds when the announcements were made (McWilliams and Siegel, 1997).

In the vein of Below and Johnson (1996) and Dasilas and Leventis (2011), for a firm to qualify to be included in the sample, it is required to meet certain conditions. They include:

1. Stock dividend and interim dividend are not announced during the event period

2. Firms must be listed in the FTSE 100 during both assessment periods. Firms that were in the bear period but not in the bull period as a result of changes in index’s constituents will be eliminated. Similarly, firms present in the bull period but not in the bear period for same reason will also be eliminated.

3. Price data for securities must be available from 220 days before dividend was announced and 20 days after the announcement day

4. Firm must have being paying dividend two years before and two years after the assessment period.

5. Dividend announcements such as stock splits, earnings, stock dividends, right issues and share repurchases will be taken into account and eliminated in order to avoid overlapping and contamination of results. The criteria above reduced the final sample to 86 firms having a total of 172 announcements out of which 114 are dividend increase, 37 dividend decrease and 21 no change for both the bull and the bear phases. This study went further to select firms into the highest increase and the highest decrease as well as the no change. For a firm to qualify in this sample, the change in dividend should be ± 50% leaving a total of 47 dividend increase announcements, 20 dividend decrease announcements and 19 no change on dividend.

Grouping the announcements into three major portfolios as suggested by MacKinlay (1997), these are the dividend increase (good news), the dividend decrease (bad news) and the no dividend change (no news) group to determine the validity of signalling theory. The study went further to add two portfolios which are the dividend increase announcements in the bull and the bear phase and the dividend decrease announcements in the bull and the bear phase in order to establish the impact of dividend announcements which contradict the market phases.

Event window and estimation period

In defining the event window in the bull and bear phase identified above, the study will take after MacKinlay (1997) who pointed out that it is best to construct an event window which is larger than the exact period of interest in order to create room for the assessment of periods around the event. The event window was defined to include some days before the announcement, the day of the announcement and some days after the announcement.

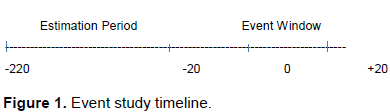

Following the approach of Dasilas and Leventis (2011), this research will be making use of a 41 day trading period for the event window which includes 20 days pre-announcement day, the announcement day which is day 0 and 20 days post announcement day (i.e. -20, 0, +20) (Figure 1). The examination of pre-event day is necessary in order to take into account any information that might have leaked into the market before the announcement as proven by Ariff and Finn (1989) and Adelegan (2003). The post-event days are also examined in order to take into cognisance any aftermath effect of the announcements.

The study will similarly take after Dasilas and Leventis (2011) in estimating the observation period and this will be the 200 trading days prior to the event window which is from -220 to -20 for each company in the sample. The length of the observation interval is likewise set at one day.

ESTIMATION OF EXPECTED RETURNS AND ABNORMAL RETURNS

This study will therefore be taking after Below and Johnson (1996) and Dasilas and Leventis (2011) by using the market model as recommended by Klein and Rosenfield (1987) and MacKinaly (1997).

MacKinaly (1997) defines market model as one that relates a security’s return to the index’s return. The market model is written thus;

E(Rit) = αi + βiRmt + eit (2)

Where ERit is the expected return on individual security, Rmt is the return on market index, ei,t is the random error and αi & βi are market model parameters.

Abnormal return is the deviation of the expected returns from the actual returns and will also be estimated using the market model as used by Dasilas and Leventis (2011). The calculation of the abnormal return is then followed by the computation of the Cumulative Abnormal Returns (CAR) for the event window.

ARi,t = Rit−E(Ri,t) (3)

Hence: ARit = Actual Return – Expected Return

Where;

ARit is the abnormal return on security i on day t

Rit is the actual return on the security on day t

E(Ri,t) is the expected return on security i on day t

According to Dasilas and Leventis (2011), the next step is to obtain the Average Abnormal Returns (AAR) of each of the portfolios of dividend change which in this study includes the dividend increase, dividend decrease, the no dividend change, increase in the bull and the bear market phases and decrease in the bull and the bear market phases.

AARp,t = ΣARp,t (4)

N

Where AARp,t is the average of the abnormal returns for each portfolio, ΣARp,t is the sum of the abnormal returns and N is the number of observations.

Estimation of parameters

This research will be making use of the Ordinary Least Square (OLS) regression model in estimating the market model parameters as used in Dasilas and Leventis (2011). The return on security i (dependent variable) will therefore be regressed against the return on the market index (independent variable) during the estimation period (-220, -21) to obtain both parameters (ai & bi). MacKinlay (1997) explains that excluding the event window from the estimation period in estimating the parameters would help to avoid the returns arising from the event from having an abnormal influence on the normal returns measure. The regression model is specified below:

Rit = a + bRmt + eit (5)

Where Ri,t is the daily actual return on the security i on day t, Rm,t is the return on the market index on day t and ai & bi are the market model parameters and ei,t is the random error term.

To calculate the daily security returns (Rit) and daily market returns (Rmt), Barndorff-Nielsen and Shephard (2002) endorse the use of log normal prices of securities as it permits the volatility terms to vary overtime. It is therefore calculated as;

Rit = LN(Pt / Pt-1) (6)

Rmt = LN(Xt / Xt-1) (7)

Where Ri,t is the return on security i on day t, Rm,t is return on the market on day t, Pi,t is the closing stock price of security at time t, Pt-1 is the closing stock price at time t-1, Xt = closing price of market index at time t and Xt-1 = closing price of market index at time t-1.

In order to test for the significance of the AARp,t of each portfolio, the t(mean) of the averages will be calculated using the following formula.

Where

is the mean of the increased dividend announcement portfolio

is the mean of the decreased dividend announcement portfolio

is the standard deviation of the increased dividend announcement portfolio

is the standard deviation of the decreased dividend announcement portfolio

is the number of observations

Hypothesis testing

The hypothesis will be testing the validity of the signalling theory and its effect on share prices when dividend announcement that contradicts the market phase is made.

H0: Dividend announcement has no significant effect on share during a bull and a bear market phase.

H1: Dividend announcement has significant effect on share price during a bull and a bear market phase.

H0: Stocks with dividend increase in a bear phase earn no abnormal positive returns than those with dividend increase in a bull phase.

H1: Stocks with dividend increase in a bear phase earn abnormal positive returns than those with dividend increase in a bull phase.

H0: Stocks with dividend decrease in a bull phase earn no abnormal negative return than stocks with dividend decrease in a bear phase.

H1: Stocks with dividend decrease in a bull phase earn abnormal negative return than stocks with dividend decrease in a bear phase.

H0: Investors have no similar investment behaviour across diverse financial markets

H1: Investors have similar investment behaviour across diverse financial markets

Data analysis

The regression model and the market model used in the methodology make use of the Gretl and Excel Data Analysis packages in estimating both the market model parameters as well as the expected returns for each of the securities. The results from the analysis will be tested using the student t-test distribution. Also, tables are presented to show the summary of the analysis

EMPIRICAL RESULTS AND DISCUSSION

The expected returns and abnormal returns were estimated using the market model that is, equations (2) and (3) respectively for each portfolio as used in Dasilas and Leventis (2011).

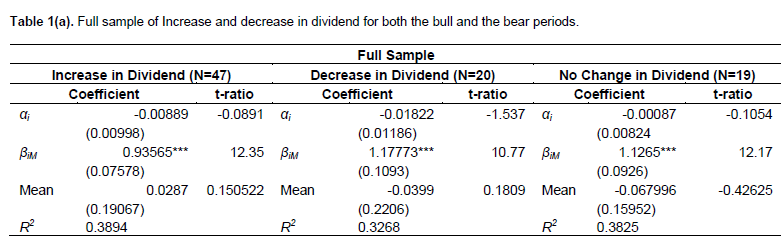

Tables 1(a) and 1(b) show a total of 86 announcements made by 43 firms during the bull and the bear periods combined. It also shows the mean of the returns for the event window. Total dividend decrease announcements made were 20 which have average negative returns of 0.0399%. The positive abnormal returns earned by the dividend increase announcement portfolio and negative abnormal returns earned by the dividend decrease port-folio confirm the claims of Bhattacharya (1979), Asquith and Mullins (1983), Daislas and Leventis (2011) and a host of other researches that dividend announcement is positively related to returns.

Also shown above is the relationship between Rjt which is the average return on securities in the FTSE 100 index and Rmt which is the market returns estimated using the regression model for both the bull and the bear market phases. The results show that α which is the intercept is negatively related to the dependent variable in all the portfolios except for the increase in dividend announcements in the bull phase. While βi on the other hand, is positively related to the dependent variable and statistically significant at 1% for all portfolios. This implies that market returns have a positive relationship with the securities’ returns and statistically significant at 1% level.

Data analysis

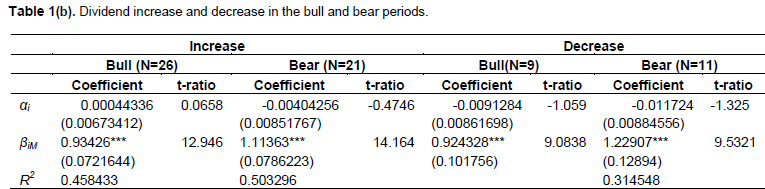

Following the method of Below and Johnson (1996) and Dasilas and Leventis (2011), the expected returns and abnormal returns of the securities were estimated using the market model, and the Average Abnormal Returns (AARs) were estimated using equation (4) as used in Dasilas and Leventis (2011) for each of the portfolio. The first portfolio consists of all firms that increased their dividend in both the bull and the bear periods while the second consists of firms that announced dividend cuts in both periods. The third comprises of firms that increased dividend in the bull and the bear market phases, while the last portfolio consists of firms that announced dividend decrease in both the bull and the bear market phases. The following sub-sections show the analysis as well as the interpretation of results obtained for each of the portfolios.

Combined announcements of increase and decrease in dividend

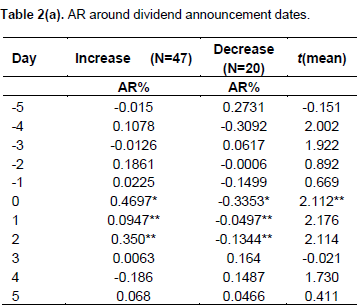

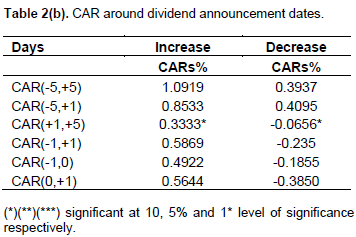

Still looking at the effect of dividend announcements but focusing on days around day0 which is the announcement day, Table 2(a) and 2(b) show the average daily abnormal returns and cumulative abnormal returns for the event window showing five days before and five days after the announcement days as used in Dasilas and Leventis (2011) for both dividend increase and decrease announcements in the bull and the bear market phases combined.

Table 2(a), first column presents the average abnormal returns of 47 dividend increase announcements made both in the bull and the bear market phases and Table 2(b) shows the corresponding CAR for the same period. It can be observed that the market reacted positively to the announcement of increase in dividend as the abnormal returns on day 0 is positive at 0.4697% and statistically significant at 10% level (t=1.679). Also, the CAR following the dividend announcement day (+1,+5) is positive at 0.333% which is also statistically significant at 10%.

Table 2(b) second column on the other hand, shows the average abnormal returns of 20 dividend decrease announcements made in the bull and the bear periods. The result proves that the market reacts negatively to dividend cut announcements with negative average abnormal returns of 0.3353% on day 0 which is statistically significant at 10% level (t=1.7247) and remained negative through to day 11. The t(mean) shows that the average abnormal returns earned on day t=0 are significantly different from zero at 5% level of significance. It also shows the abnormal returns of day +1 and +2 statistically different from zero at 5% level of significance. Also testing the CAR around the announcement day at 10% level of significance, shows that the result is statistically significant. The results support Below and Johnson (1996), Dasilas and Leventis (2011) and a host of other researchers by confirming the information content of dividend hypothesis and the validity of signalling theory. It also shows that investors in different markets behave alike as the behaviour of investors in the FTSE100 (UK), investigated in this study is similar to the behaviour of investors in S&P500(US) that was investigated by Below and Johnson (1996). It therefore means that the Null Hypothesis that dividend announcement does not convey any information to the market should be rejected. Also, the null hypothesis that investors have no similar investment behaviour across diverse financial markets should be rejected.

Dividend increase announcements in the bull and bear market phases

Table 3(a) focuses on firms that announced increase in dividend in a bear phase and firms that announced increase in dividend in the bull phase. The results confirm that dividend announcements have information content that is conveyed to the market with the results of the analysis showing positive returns on the announcement days for both the increase in the bull and the bear market phases. The increase in the bear has average positive abnormal returns of 0.4942% on day 0 while the increase in the bull has average positive abnormal returns of 0.3928% on day 0 and are both statistically significant at 5% level of significance (t=1.7056). This shows that the reaction to dividend increase announcements in the bear phase is higher than that of the bull phase with about 22% increase and statistically significant at 5% level. This is in agreement with the findings of Below and Johnson (1996) which concluded that the reaction to the increase in dividend in bear market phase is higher than the reaction in the bull market phase.

Table 3(b) shows the cumulative abnormal returns for 11days in the event window including the dividend announcement date i.e. day0 for dividend increase in the bull and the bear periods. Both CARs show positive abnormal returns around the days while CAR (+1,+5) and (-5,+5) are statistically significant at 10%. This therefore supports Dasilas and Leventis (2011) in rejecting the hypothesis that share prices do not react to dividend announcements by earning positive abnormal returns around dividend increase announcement.

This also points to the fact that the market reacts more to dividend increase in the bear phase than in the bull phase. Furthermore, it can be noted that the market began to react to the increase announcement even before it was made. That is, CAR (-5,+5) in both the bull and the bear markets are positive and statistically significant. These findings confirm the observation of Ariff and Finn (1989) and Adelegan (2003) that there is information leakage i.e. the presence of insider trading which causes the market to react before the announcements were made.

The results of this analysis therefore reject the second null hypothesis which states that dividend announcements have no impact on share prices in both the bull and the bear market phases especially the bear market phase which is categorized as a period where investors are not encouraged economically to invest in the stock market. Based on these findings also, the third null hypothesis which states that stocks with dividend increase in a bear phase earn no abnormal positive returns than those with dividend increase in a bull phase will also be rejected.

.png)

.png)

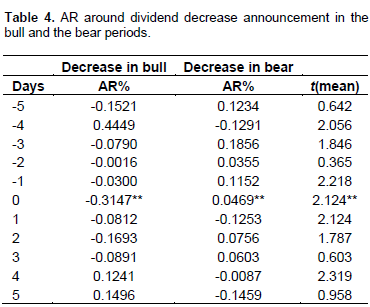

Dividend decrease announcements in the bull and the bear periods

Table 4 presents dividend decrease announcements in both the bull and the bear periods. It can be observed from the results that the market earned negative abnormal returns of 0.3147% on the average when announcements of dividend cuts were made in the bull phase and statistically significant at 5%. In addition, it can be noted that despite the announcements of decrease in dividend when the market was in a bear phase, the market earned positive abnormal returns of 0.0469% also statistically significant at 5%. The t(mean) shows that the average abnormal returns of the decrease in the bull is statistically different from the average abnormal returns of the decrease in the bear at 5% level of significance. This confirms the results of Below and Johnson (1996) that investors react more to dividend decrease that contradicts the market phase as well as supports what Benesh et al. (1984) and Eades et al. (1985) described as inappropriateness of investors to dividend cuts.

SUMMARY AND IMPLICATIONS OF FINDINGS

The findings of this research have a strong support for the validity of signalling theory and the information con-tent of dividend hypothesis as posited by Bhattacharya (1979), Asquith and Mullins (1983), Aharony and Swary 1980, Dasilas and Leventis (2011) etc. This can be observed from the results (Table 2a and 2b) which show dividend increase announcements earning positive average abnormal returns (0.4697%) and statistically significant at 10% level of significance. While the announcements of dividend decrease on the other hand, earn a negative average abnormal return (0.3353%) which is also significant at 10% level of significance. In addition, the study also supports the findings of Below and Johnson (1996) that dividend announcements that contradict the market phases do have significant impact on share prices. That is, dividend decrease (increase) when the market is in a bull (bear) phase convey more information to the market and investors on the other hand, react more to dividend cuts especially in a bull phase.

It also shows that what obtains in S&P500 (USA) as investigated by Below and Johnson (1996) also happens in the FTSE100 (UK) with respect to investors’ behaviour. It can therefore be deduced that investors have similar investment behaviour across the financial markets. This can be noted from the average abnormal returns earned when announcements that contradict the market phases were made. From Table 3(a) when the announcements of dividend increase were made in the bull and bear phase, it can be observed that the market earned an average abnormal return of 0.4924% in the bear market and 0.3928% in the bull market. Though both abnormal returns are positive but that of the increase in the bear market is higher than the increase in the bull market. The t(mean) shows the difference in these averages as statistically significant at 5% level of significance. It can also be seen from table 4 when decrease in dividends were announced in the bear and the bull periods that the market earned average positive abnormal returns (0.0469%) despite the fact that it were dividend cuts. The announcements of dividend cuts when the market was in a bull phase on the other hand, earned negative average abnormal returns (0.3147%) and the t-test shows both results statistically significant at 5%.

The findings of this study on the other hand, refute the claims if Watts (1973), Gonedes (1978), Benartzi et al. (1997), DeAngelo and DeAngelo (1990) etc who are of the opinion that there are no relationships between dividend announced and share prices. This research especially disagrees with the findings of Grullon et al. (2005) which conclude that regardless of the model used in the estimation of parameters, there are no relationship between dividend announcements and returns. This is because, the research makes use of market model as used by Below and Johnson (1996), Dasilas and Leventis (2011) and still confirms that dividend announcements have a positive relationship with stock returns in days around the day the announcement was made.

Some behavioural biases have been identified to be responsible for investor behaviour in the bull and the bear market phases. The first of these biases is the optimism and pessimism bias. According to Nofsinger (2005), investors are subject to pessimism bias which is more pronounced when the announcement of a change in dividend that contradicts the market phase is made. Generally, in a bull market phase, securities are expected to earn higher returns as well as increased dividends. As a result, when a firm announces a dividend cut instead of an expected increase, the market takes it as a signal that the company is in a distress. This is because, dividend cuts according to Below and Johnson, (1996) is seen as a management’s last resort. The results of this study also point this out in Table 4 as the announcements of decrease in dividend in the bull phase earn negative abnormal returns of 0.3147% and statistically significant at 5% and the announcement of dividend decrease in a bull phase earns positive average abnormal returns of 0.0469% also significant at 5% level. Pessimism bias can therefore be said to explain the pessimistic nature of investors leading to a higher negative reactions in the bull phase than in the bear phase.

The announcement of dividend increase on the other hand, brings about optimism bias especially when it is in a bear phase. Table 3(a) shows the average abnormal returns of dividend increase announcements in a bear phase to be 0.4924% while increase announcements in the bull phase earned lower average returns of 0.3928% which are both statistically significant at 5% level. According to Pettit (1972), management announces dividend increase only when it is certain that future cash flow would be able to sustain the increase. Investors receiving the good news of dividend increase when the market is in a bear phase see it as an information that the firm is doing well irrespective of the nature of the current market phase. This can be seen to explain why investors’ reaction to dividend increase in a bear phase is higher than dividend increase in a bull phase.

Another factor responsible for investor behaviour was identified by Barberis and Thaler (2003) as positive feedback trading where investors buy shares because prices are rising and sell shares because prices are falling. This can also be observed from the results of this study which show average abnormal returns of dividend increase announcements in the bear period to be 0.4924% while similar announcements in the bull period earned 0.3928% with both averages statistically significant at 5%level of significance.

From the findings of this research, it can be concluded that the information content of dividend hypothesis fits equally well into the bull and the bear market phases. This is because; the bull phase as mentioned earlier is characterized by investors’ willingness to invest and a stable financial wellbeing while the bear market is seen as the opposite of the bull market. It therefore follows that when an announcement of dividend increase (decrease) is made in a bull (bear) market, it confirms the opinion of investors who react by purchasing (selling) stocks thereby pushing prices further up (down). On the other hand, when an announcement of a decrease (increase) is made in a bull (bear) market phase, it contradicts the expectation of investors who also react negatively in the case of the bull market because it is seen as a signal that the company might be in distress despite the favourable economic condition. Positive reaction on the other hand, follows the announcement of dividend increase in the bear phase because the firm is seen to be performing well despite the contradicting market phase. Generally, investors tend to buy more shares in the case of dividend increase announcements which are seen as good news in order to make more profit. While dividend decrease announcements are seen as bad news thereby selling their stocks in order to avoid further loses.

SUMMARY AND CONCLUSION

This research sets out to examine the validity of signalling theory that is, the information content of dividend hypothesis as well as testing the validity of the theory in a situation when dividend announcements that contradict the market phases are made. This study generally aims to determine if investors earn abnormal returns around dividend announcement days especially those announcements that contradict the market phase e.g. a significant positive abnormal return when dividend increase announcements are made in a bear market phase and a significant negative abnormal return when dividend decrease announcements are made in a bull market phase. It also seeks to establish if investors in different markets have similar investment behaviour.

Based on the above analysis and tests, the findings of this research have a strong support for the validity of signalling theory and the information content of dividend hypothesis as purported by Bhattacharya (1979), Asquith and Mullins (1983), Aharony and Swary (1990), Dasilas and Leventis (2011) etc. It was observed that generally, investors earn positive abnormal returns around dividend increase announcements while dividend decrease announcements on the other hand, earn negative abnormal returns around the announcement day which shows that dividend announcement is positively related to share prices. In addition, it was discovered that investors react more to dividend cut than they react to dividend increase which is consistent with Benesh et al. (1984) and Eades et al. (1985).

Although the study by Uddin and Chowdhury (2003) concludes that dividend announcements have no positive relation with returns, it shares the same opinion with the findings of this research that there exists the presence of insider trading. That is, the market begins to react to dividend announcements days before they are made which is also consistent with Ariff and Finn (1989) and Adelegan (2003).

Also consistent with Below and Johnson (1996) is the fact that investors react more to dividend announcements that contradict the market phases especially the announcement of dividend cuts when the market is in a bull phase. It was also noted that announcements of dividend increase in the bear phase earned higher positive abnormal returns than dividend increase announcements in the bull phase. This study was also able to determine in addition to the existence of signalling theory, that investors in different financial markets have similar investment behaviour.

RECOMMENDATIONS AND CONCLUDING REMARKS

The study of the effects of dividend announcements in the bull and the bear markets has been carried out in developed markets that is, this study which made use of the FTSE100 index and the study by Below and Johnson (1996) which made use of S&P 500 index and both suggest that investors react more to dividend announcements that contradict the market phases. It is therefore recommended that future researches be carried out in emerging markets in order to determine whether the results will be consistent with those of the developed markets. Future researches could also look into the impact of dividend change announcements on small capitalized and large capitalized firms during the bull and the bear periods. That is, to investigate if dividend changes announcements made by large capitalized firms convey more information than small capitalized firms in the bull and bear markets and vice versa.

CONFLICT OF INTERESTS

The author has not declared any conflict of interests

REFERENCES

|

Adelegan OJ (2003). 'Capital Market Efficiency and the Effects of Dividend Announcements on Share Prices in Nigeria'. African Development Review 15(2â€3) : 218-236 |

|

|

|

|

|

Aharony J, Swary I (1980). 'Quarterly Dividend and Earnings Announcements and Stockholders' Returns: An Empirical Analysis'. J Financ. 35(1) : 1-12 |

|

|

|

|

|

Al-Yahyaee KH, Pham TM, Walter TS (2011). 'The Information Content of Cash Dividend Announcements in a Unique Environment'. J Bank. Financ. 35 (3): 606-612 |

|

|

|

|

|

Ariff M, Finn FJ (1989). 'Announcement Effects and Market Efficiency in a Thin Market: An Empirical Application to the Singapore Equity Market'. Asia Pacific J Manag. 6 (2): 243-265 |

|

|

|

|

|

Asquith P, Mullins Jr, DW (1983).'The Impact of Initiating Dividend Payments on Shareholders' Wealth'. J Bus., 77-96 |

|

|

|

|

|

Barberis N, Thaler R (2003). 'A Survey of Behavioral Finance'. Handbook of the Economics of Finance 1, 1053-1128 |

|

|

|

|

|

Barndorff-Nielsen O, Shephard (2002). Econometric Analysis of Realized Volatility and its use in Estimating Stochastic Volatility Models.: Wiley-Blackwell |

|

|

|

|

|

Below SD, Johnson KH (1996). 'An Analysis of Shareholder Reaction to Dividend Announcements in Bull and Bear Markets'. J o Financ. Strategic Decisions 9 (3):15-26 |

|

|

|

|

|

Benartzi S, Michaely R, Thaler R (1997). 'Do Changes in Dividends Signal the Future Or the Past?'. J Financ. 52 (3): 1007-1034. |

|

|

|

|

|

Benesh GA, Keown AJ, Pinkerton JM (1984). 'An Examination of Market Reaction to Substantial Shifts in Dividend Policy'. Financial Review 17 (2), 14-14 |

|

|

|

|

|

Bhattacharya S (1979). 'Imperfect Information, Dividend Policy, and" the Bird in the Hand" Fallacy'. The Bell J Econ., 259-270 |

|

|

|

|

|

Bhattacharyya N (2007). 'Dividend Policy: A Review'. Managerial Finance 33 (1): 4-13 |

|

|

|

|

|

Black F (1998).'The Dividend Puzzle'. Streetwise: The Best of" the J Portfolio Manag.", 10 |

|

|

|

|

|

Black F (1976). 'The Dividend Puzzle'. J Portfolio Manag. 2, 5-8 |

|

|

|

|

|

Bozos K, Nikolopoulos K, Ramgandhi G (2011). 'Dividend Signaling Under Economic Adversity: Evidence from the London Stock Exchange'. International Review of Financial Analysis 20 (5), 364-374 |

|

|

|

|

|

Brickley JA (1983). 'Shareholder Wealth, Information Signaling and the Specially Designated Dividend: An Empirical Study'. J Financ. Econ. 12 (2), 187-209 |

|

|

|

|

|

Dasilas A, Leventis S (2011). 'Stock Market Reaction to Dividend Announcements: Evidence from the Greek Stock Market'. International Review of Economics & Finance 20 (2), 302-311 |

|

|

|

|

|

DeAngelo H, DeAngelo L (1990). 'Dividend Policy and Financial Distress: An Empirical Investigation of Troubled NYSE Firms'. The J Financ. 45(5): 1415-1431 |

|

|

|

|

|

Dolley JC (1933). 'Characteristics and Procedure of Common Stock Split-Ups'. Harvard Business Review 11(3): 316-326 |

|

|

|

|

|

Eades KM (1985). 'Empirical Evidence on Dividends as a Signal of Firm Value'. J Financ. Quant. Anal. 17(4): 471-500 |

|

|

|

|

|

Frankfurter G, Wood GB, Wansley J (2003) Dividend Policy Theory and Practice. USA: Academic Press, Elsevier Science |

|

|

|

|

|

Gonedes NJ (1978). 'Corporate Signaling, External Accounting, and Capital Market Equilibrium: Evidence on Dividends, Income, and Extraordinary Items'. J Accounting Res. 16(1): 26-79. |

|

|

|

|

|

Gonzalez L, Powell JG, Shi J, Wilson A (2005). 'Two Centuries of Bull and Bear Market Cycles'. International Review of Economics & Finance 14(4): 469-486. |

|

|

|

|

|

Grullon G, Michaely R, Benartzi S, Thaler R (2005). 'Dividend Changes do Not Signal Changes in Future Profitability'. Available at SSRN 431762 |

|

|

|

|

|

Healy PM, Palepu KG (1988) 'Earnings Information Conveyed by Dividend Initiations and Omissions'. J Financ. Econ. 21(2):149-175. |

|

|

|

|

|

John K, Williams J (1985). 'Dividends, Dilution, and Taxes: A Signalling Equilibrium'. J Financ. 40(4):1053-1070 |

|

|

|

|

|

Kalay A (1980). 'Signaling, Information Content, and the Reluctance to Cut Dividends'. Journal of Leftwich R, Zmijewski ME (1994). 'Contemporaneous Announcements of Dividends and Earnings'. J Accounting, Auditing & Finance 9(4):725-762 |

|

|

|

|

|

Klein A, Rosenfeld J (1987). 'The Influence of Market Conditions on Event-Study Residuals'. J Financ. Quant. Anal. 22(3):345-351. |

|

|

|

|

|

MacKinlay AC (1997). 'Event Studies in Economics and Finance'. J Econ. Lit. 35(1):13-39. |

|

|

|

|

|

McWilliams A, Siegel D (1997). 'Event Studies in Management Research: Theoretical and Empirical Issues'. Academy of Manag. J, 626-657 |

|

|

|

|

|

Miller MH, Modigliani F (1961). 'Dividend Policy, Growth, and the Valuation of Shares'. J Bus. 34(4):411-433. |

|

|

|

|

|

Nissim D, Ziv A (2001). 'Dividend Changes and Future Profitability'. J Financ. 56(6):2111-2133 |

|

|

|

|

|

Nofsinger JR (2005). 'Social Mood and Financial Economics'. J Behavioral Financ. 6(3):144-160. |

|

|

|

|

|

Pettit RR (1972). 'Dividend Announcements, Security Performance, and Capital Market Efficiency'. J Financ. 27(5):993-1007. |

|

|

|

|

|

Richardson VJ (2000). 'Information Asymmetry and Earnings Management: Some Evidence'. Review of Quantitative Finance and Accounting 15(4):325-347 |

|

|

|

|

|

Spence M (1973). 'Job Market Signaling'. The Quarterly J Econ. 87(3): 355-374. |

|

|

|

|

|

Uddin MH, Chowdhury GM (2003). 'Effect of Dividend Announcement on Shareholders' Value: Evidence from Dhaka Stock Exchange'. Finance and Banking, 1-16 |

|

|

|

|

|

Watts R (1973). 'The Information Content of Dividends'. J Bus.46(2):191-211 |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0