Full Length Research Paper

ABSTRACT

This study examined the effect of welfare status on insurance uptake. The reason for the study is that formal insurance is still underutilized amongst farmers in Nigeria despite the incessant risk and uncertainties faced in agriculture. For this study, 200 households were randomly drawn from four local government areas of Ondo state through a 2-stage sampling technique. The analytical tools used were descriptive statistics and the Heckman selection model. The result obtained from the study showed that the risk coping strategies adopted by cocoa farmers in the study area included the use of pesticides, herbicides and manual weeding of their farms. Insurance awareness was low among cocoa farmers in the study area. Also, factors that influenced farmers’ decision to take insurance were years of formal education, distance of household from insurance company, access to extension agent and total land cultivated. Household size which was used as instrumental variable for welfare status was also significant in the model influenced farmers’ decision to take crop insurance.

Key words: Heckman selection model, cocoa, risk, welfare, crop insurance.

INTRODUCTION

Cocoa is a major cash crop in Nigeria and has a rich history in the economic development of the country, especially when agriculture was the main stay of her economy. It is the main source of agricultural export in Nigeria, even though its production accounts for only 0.3% of the country’s agricultural Gross Domestic Product (GDP) (IFPRI, 2010). The cocoa plant generally requires high humidity, fairly high rainfall and a dry forest area, ecological requirements which are most readily available in the western states of Nigeria (Ondo, Oyo, Osun, Ogun and Ekiti). As a result, most of the cocoa beans produced in Nigeria come from the southwest according to the National Bureau of Statistics (2012). According to FAOSTAT (2013), cocoa production increased in Nigeria from 150,000 tonnes in 1987 to 391,000 tonnes in 2011 making export to steadily increase from 106,000 tonnes to 262,000 tonnes within the same period. Nigeria therefore became the third leading exporter of cocoa in the world, after Cote d’Ivoire and Ghana (Rifin, 2013). According to the United Nation International Trade statistics (Uncomtrade, 2018) Nigeria is the seventh largest cocoa exporter in world and the third in Africa after Cote d’Ivoire and Ghana

Cocoa Production in the Agricultural sector is not being given the required attention to strategically place it for growth, unlike the way it used to be, as a result of the oil boom (Nchuchuwe and Adejuwon, 2012). The discovery of oil is therefore one out of the many factors that affected the growth potential of the cocoa industry and its position as a major exporter. As stated by Verter and Becvarova (2014), Nigeria’s cocoa export as a percentage of world cocoa export has fluctuated and decreased from 12.6% in 1981 to 8.5% in 2011 due to concentration of the Nigerian government more on crude oil than on cocoa. To further substantiate this claim, Olaiya (2016) stated that the petro-dollar dominated economy of the late seventies and early eighties created many opportunities in urban centres and cities and facilitated rural urban migration which led to continuous decline of aggregate cocoa output and export. This, coupled with others risk factors and uncertainties has in one way or the other led to the decline in its production, when compared to times past.

Olayemi (2004) defines risk as a situation in which, although the actual outcome of a decision is not known, all the possible outcomes are known as well as the probability associated with each possible outcome. Therefore, agricultural risks and uncertainties cannot be overemphasized. This grouped the major risks within the cocoa supply chain as production, commercial (or market), and environmental risks. These categories of risk identified are the paramount risks encountered by cocoa farmers and envelop specific uncertainties and risk components which include but are not limited to theft, fire, pests and diseases price instability, bad weather (erratic rainfall patterns, insufficient rainfall, drought and high temperature), market developments and other events that cannot be controlled by the farmer and have a direct effect on the returns to the farming household (Baquet et al., 1997). It can also, bring about colossal loss of monetary value, psychological displacement and total business failure (Hamid and Chiman, 2010).

The International Cocoa Organisation (ICCO, 2019) found that there were decreases in the global cocoa production from 4.3 million metric tonnes in 2010/2011 to 4.0 million metric tonnes in 2011/2012 and 3.9 million metric tonnes in 2012/2013. It rose in the following season to 4.37 million metric tonnes and dropped in 2015/2016 to 3.97 million metric tonnes and has risen above the 4 million metric tonnes mark in the proceeding seasons. The decline in production has been attributed majorly to pest and disease attack, price instability of cocoa in the global market, weather conditions, amongst many other risks and uncertainties. According to Wessel and Quist-Wessel (2015) four major cocoa producing countries; Cote d’Ivoire, Ghana, Nigeria and Cameroun have common causes of low yield in which they identified low input, inadequate maintenance, old age of cocoa farms and pest and disease outbreaks.

In order to ensure an increase in cocoa production, farmers have depended so much on their traditional crop maintenance practice to cope with, control and mitigate risks. According to Aidoo et al. (2014), these methods include but not limited to: weeding, use of insecticides, herbicides, contract sales, etc., with the most recent one being the need to take up insurance, as it is seen to be effective in ensuring that farming households are not left with nothing in an event of total crop damage. Insurance is a risk management strategy and the primary motive of having an insurance policy is to serve as a security for losses resulting from natural disaster (Akinrinola, 2014). Also, several studies (Salimonu and Falusi, 2009; Nnadi et al., 2013) have identified crop insurance as an effective means of mitigating risk. Nnadi et. al., (2013) identified three mechanisms by which insurance can be an important adaption to risk. The first is by direct transfer of the risk away from the farmers and to an insurance firm and enjoying a payout in case of shock to sustain their livelihood. The second is by allowing farmers take productive risk by taking a loan to invest, in their own productive capacity and the third mechanism is by placing a price tag on activities based on the level of perceived risks such that if certain activities become riskier the insurance price will rise to reflect the risk.

The Nigerian government has been taking conscious steps to help farmers mitigate agricultural risk by making available several formal insurance programs. Examples of such insurance programs include: The National Insurance Corporation of Nigeria (NICON), the National Cooperative Insurance Society of Nigeria (NCISN), The Nigerian Agricultural Insurance Company (NAIC), and The Nigeria Incentive Based Risk Sharing system for Agricultural Lending (NIRSAL), etc. Although, several insurance programs exist, the decision to take formal crop insurance is left to the farmers especially since a premium is attached. Willingness to take insurance will depend on certain factors that will border around the household income and general welfare. According to Jensen (2007) farmers’ welfare in developing countries depends directly on the price at which they sell their produce. In addition, many household heads may need to diversify to earn more money which will most likely improve their welfare (Adepoju and Obayelu, 2013). The implication of this is that, if the harvest in the previous seasons was good and devoid of risks and uncertainties, cocoa farmers will be able to make optimum sales which will translate to increased profit and enhance their welfare status. With more income at their disposal, they may be willing to pay premium to protect them in case of shock.

But Nigerian farmers are to a large extent are not keying into formal crop insurance due to lack of awareness Chikaire et al. (2016). Other reasons may include little or no formal education, lack of understanding of the concept, low income and most importantly poor welfare of the farming household. Although some work has been done so far on insurance and welfare, there is still a need to go back and research on the findings of previous literature and also bearing in mind areas that need to be researched upon with the primary purpose of filling knowledge gaps, hence the reason why this research was conducted to establish the relationship between welfare and insurance uptake. The main objective of the research is to examine the effect of cocoa farmers’ welfare on their participation in insurance. This was achieved by profiling the risk coping strategies adopted by cocoa farmers other than formal crop insurance; profiling the level of farmer’s awareness and participation in insurance; examining the interplay between welfare status and insurance uptake and the relationship between farmers’ welfare on participation in formal crop insurance. It seems awareness of crop insurance is still very low and farmers continue to face a lot of risks and uncertainties in their agricultural activities.

Consumer decision model

This research is based on the theory of consumer decision model (Blackwell et al., 2001). The model is structured around a seven-point decision process: need recognition followed by a search of information both internally and externally, the evaluation of alternatives, purchase, post purchase reflection and finally, divestment. These decisions are influenced by two main factors. Firstly, stimuli are received and processed by the consumer in conjunction with memories of previous experiences, and secondly, external variables in the form of either environmental influences or individual differences. The environmental influences identified include: Culture; social class; personal influence; family and situation. While the individual influences include: Consumer resource; motivation and involvement; knowledge; attitudes; personality; values and lifestyle.

Jorgenson and Slesnick (1987, 2014) and Lewbel (1989) have shown how to deal with the issue of scaling consumption expenditures to achieve comparability among households. In the theory of household behavior, economic well-being of a household k (k=1, 2, …K) is presented by a utility function Wk that, in its simplest form, depends on the flow of consumption of consumer goods and services available to the household. According to Jorgenson and Schreyer (2017), the traditional theory of consumer behavior is based on individuals. After further research, a conclusion was reached that the household paints a better picture as a decision making unit. The necessary framework was provided by the theory of household behaviour of Samuelson (1956). This coincides with the fact that empirical sources of information on consumption or income are typically collected for households, not individuals. At the same time, households may have quite different characteristics, for example in terms of the number of individuals living in a household so one household’s economic well-being cannot be directly compared to another household’s well-being unless they share the same characteristics. The concept of welfare is rather vague. It is easier to restrict attention to material well- being, that is, the well-being obtained from consumption. It is obvious that this is an extremely narrow view of human welfare. Nevertheless, it has a couple of advantages. First, it is relatively easy to operationalize, which makes it useful for empirical purposes. Furthermore, material well-being is interesting for a number of policy-making issues, such as determining transfers and taxation. The two concepts welfare and well-being can be used interchangeably.

METHODOLOGY

Study Area

Ondo state is located in the South-West Region of Nigeria and lies between latitude 5°45’ and 7°52 and longitudes 4°20’ and 6°5. It is typically an agrarian economy with most of her inhabitants engaged in cocoa production which has earned it the status of the largest cocoa producing state in Nigeria(National Bureau of Statistics, 2012). Other crops produced in the state include kolanut, oil palm, plantain, oranges, yam and cassava. Of the eighteen local governments in Ondo state, about thirteen produce cocoa in varying quantities depending on the fertility level of the land. Idanre, Ile-Oluji, Owo, Ondo West, Akure South and Odigbo local government areas produce the largest quantities of cocoa in the State (Falola et.al.,2013)

Data Collection

The data on which this paper is based are primary data obtained from individuals from cocoa farming households. Information of other members of the household were also collected. The questionnaire was structured to collect socio-economic and demographic information of respondents as well as information on their production activities, risk and risk mitigating strategies, assets, income and expenditure. A two-stage sampling technique was employed in the selection of farming households.Four Local Government Areas (LGAs) (Idanre, Ile-Oluji, Owo and Ondo) were purposively selected because they are the largest producers. From each LGA, five villages were randomly selected (to make a total of 20 villages) and from each village ten households were randomly selected which brought the total number of selected households to 200. The table of random numbers was used to select households.

Analytical Tools

Descriptive Statistics

Descriptive statistics were used to profile the socioeconomic and demographic characteristics of the cocoa farmers and also to analyze the risk coping strategies adopted by farmers in the study area.

Foster-Greer-ThorbeckeModel

The Foster Greer Thorbecke model is a combined measure of poverty and income inequality. The FGT poverty measures are additively decomposable and it is a class of poverty measures that allows one to vary the weight assigned to the income (or expenditure) level of the poorest members of a society.

The Forster-Greer-Thorbecke index is defined as:

Where:![]() is the poverty line defined as 2/3 of mean annual per capita expenditure, q is the number of households below the poverty line, N is the total sample population, yi is the mean adult equivalent expenditure of the ith household, and

is the poverty line defined as 2/3 of mean annual per capita expenditure, q is the number of households below the poverty line, N is the total sample population, yi is the mean adult equivalent expenditure of the ith household, and![]() is the Foster et al., (1984) parameter, which takes the value 0 (which measures head-count ratio), 1 (which measures poverty depth) and 2 (which measures poverty severity), depending on the degree of concern about poverty.This analytical tool has been used by several studies (Akangbe et.al 2012, Adetayo 2014). The welfare status of the cocoa farmers was computed using The Foster Greer Thorbecke model and poverty was used as proxy for welfare status. Two-third of the mean per capital household expenditure was used as poverty line such that those who were above the line had high welfare and those below had moderate welfare status. All households that fell below one-third of mean per capita income had low welfare status.

is the Foster et al., (1984) parameter, which takes the value 0 (which measures head-count ratio), 1 (which measures poverty depth) and 2 (which measures poverty severity), depending on the degree of concern about poverty.This analytical tool has been used by several studies (Akangbe et.al 2012, Adetayo 2014). The welfare status of the cocoa farmers was computed using The Foster Greer Thorbecke model and poverty was used as proxy for welfare status. Two-third of the mean per capital household expenditure was used as poverty line such that those who were above the line had high welfare and those below had moderate welfare status. All households that fell below one-third of mean per capita income had low welfare status.

Total Expenditure (TE) = Food Expenditure + Non-food Expenditure

Per Capital Income (PCE) = Total Expenditure/household Size

Mean Per Capital Income (MPCE) = Per Capital Expenditure/Number of household

Heckman Selection Model: Heckman model was selected because it helps eliminate problems of endogeneity. The Heckman selection model is a two-equation model. First Van de Ven and Van Prag (1981) provide an introduction and an explanation of the model. The first model i.e. probit model is written as:

The selection equation is written as:

Where:

Where Yi denotes the dependent variables, Xi denotes the observable feature of the independent variables, β denotes the parameters to be estimated, Zi denotes observable features including the overlapping variables with Xi and Y denotes the vectors of parameters to be estimated μ_2 is a distributed error with mean zero and standard deviation of one. P represent the correlation between the two error terms to be estimated. In the main equation of the study, it is assumed that a regression model can be used to explain the relationship between welfare and insurance uptake.

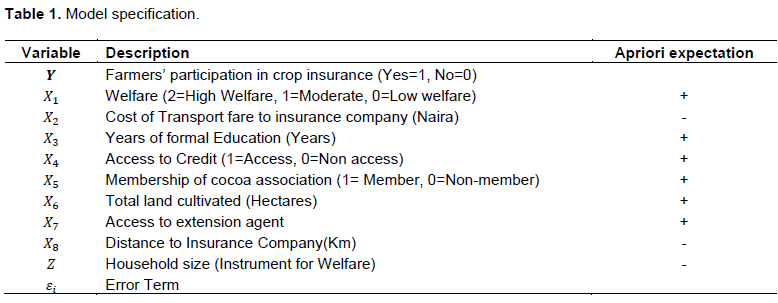

Family size was used as an instrumental variable for welfare because it has a direct effect on the family’s welfare status, the smaller the household size the higher the per capita income and the welfare status of the family (Table 1).

RESULTS AND DISCUSSION

Risk Coping Strategy

The risk coping strategies adopted by cocoa farmers in the study areas as shown in table 1 include: the use of pesticides; it was made use of by 93.5% to fight off pests, especially insects that affect the pods. Approximately73% of them used herbicides on their farms while about 76.6% got rid of weed from their farms manually. None of the cocoa farmers fenced their farm lands against invaders and they did not engage in contract farming; thereby allowing them to make the best from their sales by being able to dictate prices and sell any quantity demanded.Every single one of the farmers processed their cocoa pods by removing the beans from the pod, fermenting it for about 3-5 days and sun drying it before sales. None of them processed the beans to derive other products such as cocoa powder and cocoa butter.

Crop Insurance and welfare computation

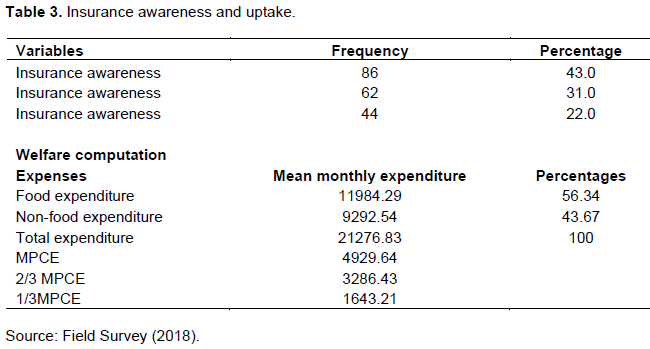

Table 2 shows that 57% of the respondents were not aware of insurance or what it is meant for while only 43% of them were aware. This is contrary to the finding of Falola et al. (2013) who stated that 77.5% of the farmers sampled were aware of insurance. The difference in the result was that awareness of insurance was separated into categories of strongly aware, partially aware, fairly aware and not aware. This study did not provide a middle point for respondents to stay. The table further showed that 69% of the respondents do not have any form of insurance policy while only 31% have one form of insurance or the other such as car,and motorcycle insurance and crop insurance. About78% of the respondents do not have formal crop implying that they are exposed to risks.

Welfare status of Cocoa Farmers and Insurance Uptake

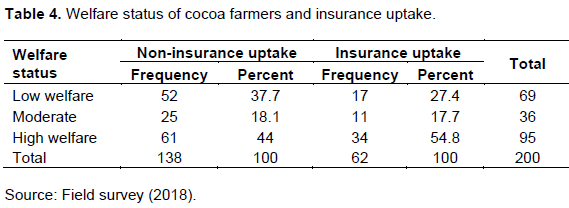

Table 3 showed the relationship between the welfare status of the farmers and their use of crop insurance. Approximately, 38% of the cocoa farmers have low welfare status and do not use formal crop insurance while 27.4% of them have low welfare and make use of crop insurance. Among those with moderate welfare, 18.1% do not use formal crop insurance while 17.7% of them make use of it. 54.8% of the cocoa farmers who have high welfare status make use of crop insurance as opposed to 44% of them who although have high welfare status do not make use of crop insurance. The difference in the percentage of cocoa farmers that use formal crop insurance and have high welfare status and those ones who have moderate and low welfare status and do not use formal crop insurance could be an indication that welfare status greatly influences farmers’ decision on insurance uptake. That is however subject to further analysis.

Effect of Cocoa Farmer’s Welfare on Formal Crop Insurance

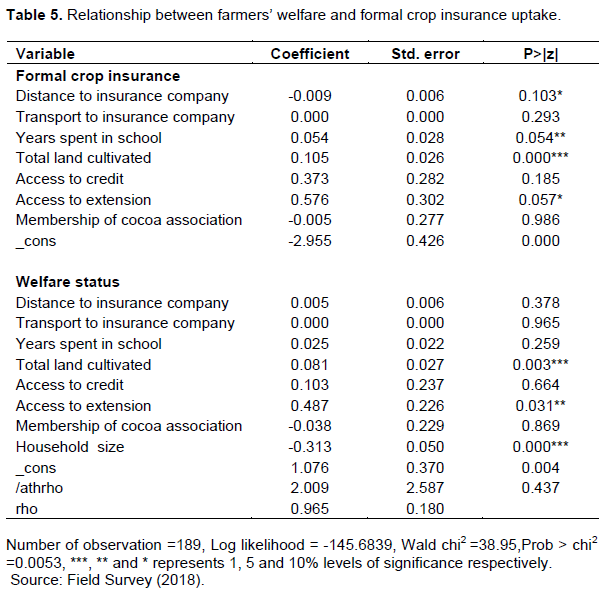

Table 4 shows the effect of cocoa farmers’ welfare on their decision to take formal crop insurance. The model is significant at 1% significance level. Among the independent variables only four factors were significant and hence influence the farmers’ decision to take formal crop insurance. They are, years spent in school, distance to insurance company, total land cultivated and access to extension agent.

Years of formal education has a positive relationship with farmers’ decision to take formal crop insurance and the table shows that an additional year of formal education will increase the chances that the cocoa farmer will take formal crop insurance by 5.4%. An increase in total land cultivated by has a positive relationship with insurance uptake and an increase by 1 hectare will increase the chances of insurance uptake by 10.5%. Access to extension agents has positive relationship with insurance uptake and a unit increase in extension visits to cocoa farmers can increase the chances of cocoa farmers taking formal crop insurance by 57.6%. Distance from insurance company has negative effect on insurance uptake and a 1 kilometer decrease in distance of farming household from the insurance company will increase the chances of cocoa farmers taking formal crop insurance by 0.9%. The second part of the table shows that Household size used as instrumental variable for welfare status is negatively related to welfare status. Those with fewer household members will enjoy better welfare. Access to extension agents and total land cultivated also has a positive relationship with welfare and are also factors that influence insurance uptake.

CONCLUSION AND RECOMMENDATIONS

In conclusion, only 43% of the respondents are aware of the insurance. Although 31% of the respondents have one form insurance or the other, only 22% of the respondents in the study area have formal crop insurance. The risk coping strategies adopted by farmers include: use of pesticides, herbicides, manual weeding and processing to the point of getting the dried cocoa beans. The welfare status presented in Table 3 shows that 37.5% have high welfare status compared to 34.5% whose welfare status is low and 28% that have moderate welfare status. It means that most of the farmers in the study area have high welfare status.

Some of the factors that influences formal crop insurance uptake include; years of formal education, total land cultivated, access to extension agents, distance to the insurance company. Factors that influence insurance uptake also affects welfare. Household size which was used as instrumental variable for welfare status and total land cultivated were significant at 1% level of significance. The converging point between insurance uptake and welfare in this study is, for all that eventually use formal crop insurance, their welfare status is a determining factor. This study recommends that extension agents should educate cocoa farmers on crop insurance and its relevance, also the government needs to create a much more enabling environment for farmers by bringing insurance facilities and services closer to the rural communities and making the insurance packages more attractive.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

ACKNOWLEDGEMENT

This research was supported by Agricultural Policy Research in Africa (APRA) and we will not fail to show our appreciation. We are thankful for the expertise that greatly assisted the research.

REFERENCES

|

Adepoju AO, Obayelu OA (2013) Livelihood diversification and welfare of rural households in Ondo State, Nigeria. Journal of Development and Agricultural Economics 5(12):482-489 |

|

|

Adetayo A (2014). Analysis of farm households poverty status in Ogun states, Nigeria. Asian Economic and Financial Review 4(3):325-340 |

|

|

Aidoo R, JamesOM, Prosper W, Awunyo-Vitor D (2014). Prospects of crop insurance as a risk management tool among arable crop farmers in Ghana. |

|

|

Akangbe HO, Adeola OO, Ajayi AO (2012) The effectiveness of microfinance banks in reducing the poverty of men and women at Akinyele Local Government, Oyo State Nigeria. Journal of Development and Agricultural Economics 4(5):132-140 |

|

|

Akinrinola OO (2014) Evaluation of effects of agricultural insurance scheme on agricultural production in Ondo State. Russian journal of Agricultural and Socio-Economic Sciences 28(4):3-84 |

|

|

Baquet AE, Hambleton R, Jose D (1997).Introduction to Risk Management understanding agricultural risks: production, marketing, financial, legal, human Resources. US Department of Agriculture, Risk Management Agency. |

|

|

Blackwell RD, Miniard PW, Engel JF (2001). Consumer behaviour. Thomson. South Western. |

|

|

Chikaire JU, Tijjani AR, Abdullahi KA (2016) The perception of rural farmers of agricultural insurance as a way of mitigation against climate change variability in Imo State, Nigeria. International Journal of Agricultural Policy Research 4(2):17-21. |

|

|

Falola A, Ayinde OE and Agboola BO (2013) Willingness to take agricultural insurance by cocoa farmers in Nigeria. International Journal of Food and Agricultural Economics. 1(1):97-107 |

|

|

Food and Agriculture Organization (2013). FAOSTAT database [Data file]. |

|

|

Hamid, MY, Chiaman ES (2010). Risk and Uncertainty Assessment Of Nomadic Cattle Pastoralist in Mubi-North Local Government Area of Adamawa State Proceedings of 11th Annual National Conference of National association of Agricultural Economists (NAAE). Pp. 109-113. |

|

|

International Cocoa Organization. (2019). Quarterly Bulletin of Cocoa Statistics, Vol. XLV - No. 2 - Cocoa year 2019. |

|

|

International Food Policy Research Institute (2010). A 2006 Social Accounting Matrix of Nigeria: Methodology and results. www.ifpri.org |

|

|

Jensen R (2007) The digital provide: Information (technology), market performance, and welfare in the South Indian fisheries sector. The Quarterly Journal of Economics, 122(3):879 -24 |

|

|

Jorgenson DW, Schreyer P (2017). Measuring Individual Economic Well?Being and Social Welfare within the Framework of the System of National Accounts. Review of Income and Wealth 63:S460-S477. |

|

|

Jorgenson DW, SlesnickDT (1987). "Aggregate Consumer Behavior and Household Equivalence Scales," Journal of Business and Economic Statistics, 5(2): 219-232. |

|

|

Jorgenson DW, SlesnickDT (2014). "Measuring social welfare in the U.S. national accounts", inJorgenson DW,Landefeld S andSchreyer P (eds.), Measuring Economic Sustainability and Progress: NBER Book Series Studies in Income and Wealth, pp. 43-88. |

|

|

Lewbel A (1989), "Household Equivalence Scales and Welfare Comparisons", Journal of Public Economics 39(3):377-39 |

|

|

National Bureau of Statistics (2012) Review of the Nigerian Economy in 2011 & Eco-nomic Outlook for 2012-2015. Abuja: National Bureau of Statistics. |

|

|

Nchuchuwe FF, Adejuwon KD (2012). "The challenges of Agricultural and Rural Development in Africa: The case of Nigeria", International Journal of Academic Research in Progressive Education and Development 1(3):45-61. |

|

|

Nnadi FN, Chikaire J, Echetama JA, Ihenacho RA, Umunnakwe PC, Utazi CO (2013). Agricultural insurance: A strategic tool for climate change adaptation in the agricultural sector. Net Journal of Agricultural Science 1(1):1-9. |

|

|

Olaiya TA (2016). Examining the political economy of cocoa exports in Nigeria. International Journal of Applied Economics and Finance 10(1-3):1-13 |

|

|

Olayemi JK (2004). Principles of microeconomics. Ibadan: Sico Publisher. Oluwatusin F M (2008). Cost and Returns in Modern Beekeeping for Honey Production in Nigeria. Department of Agricultural Economics and Extension, University of Ado-Ekiti, Nigeria. |

|

|

Rifin A (2013 Competitiveness of Indonesia's cocoa beans export in the world market. International Journal of Trade, Economics and Finance 4(5):279 |

|

|

Salimonu KK, Falusi AO (2009). Sources of risk and management strategies among food crop farmers in Osun State, Nigeria. African Journal of Food, Agriculture, Nutrition and Development 9(7). |

|

|

United nation international trade statistics (un comtrade 2018) vol.1 comtrade.un.org |

|

|

Verter N,Be?vá?ová V (2014). Analysis of some drivers of cocoa export in Nigeria in the era of trade liberalization. Agris on-line Papers in Economics and Informatics, 6(665-2016-45040), 208. |

|

|

Wessel M, Quist-Wessel PF (2015) Cocoa production in West Africa, a review and analysis of recent developments. NJAS-Wageningen Journal of Life Sciences, 74:1-7 |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0