Full Length Research Paper

ABSTRACT

Islamic rural microfinance represents the confluence of three rapidly growing activities: microfinance, Islamic finance and agricultural development. It has the potential to not only respond to unmet demand but also to combine the Islamic social principle of caring for the less fortunate with microfinance’s power to provide financial access to the poor people involved in rural farming. This paper aims to analyze the governmental agricultural microfinance based on the Islamic principle of Murabaha, using the rural area of Hama government, Syria as case study. The qualitative approach and collected data from the microloan provider was used in this research. The main results show the success of this type of agricultural microcredit to develop the livestock production and its high likelihood of sustainability because it does not conflict with religious and social considerations of the targeted group as well as the high repayment, and it uses the participatory approach of the target group. It could play a very important role regarding the empowerment of rural women by establishing their own projects, owning shares in the village fund, obtaining annual profits, and household investment which can help to improve their family's living conditions. The risks to this type of agricultural microfinancing includes agricultural sector exposure to natural, productive, price and institutional risks.

Key words: Agricultural microcredit, microfinance, Murabaha, village funds, Syria.

INTRODUCTION

Achieving "rural development, combating poverty and improving the living standard of rural families" remains meaningless without a change in current modalities of thinking from bureaucratic approaches to a more pragmatic approach that helps implement and practice policy recommendations. A pragmatic approach may better tackle natural, political, economic, administrative and technological constraints as well as financial constraints. Therefore, it is necessary to think of other ways to finance the agricultural sector. Importantly, these methods must be accepted by target groups and rural residents and it should not contradict their beliefs. Agriculture is considered to be the backbone of the Syrian economy, as it accounts for the second largest share of the economy after oil (NAPC, 2013). It is an economic source for more than 46% of the population (Almohamed and Doppler, 2008). Therefore, agricultural development projects, in general, aim to combat poverty, reduce unemployment, and establish the principle of self-help with a participatory approach. Within this context, it aims to activate the participation of rural families to become economically viable and to achieve social and economic development of the community by various rural activities like the micro-foundation projects. The Credits are available to rural families from various institutions or persons, e.g. from the agrarian bank, agricultural cooperatives, relatives or private lenders. The first three sources of loans have an interest rate of between 0 and 8%, while the interest rate of lenders is about 25% (Almohamed and Doppler, 2008). Due to the Syrian crisis and the ensuing inflation, interest rate in the agricultural cooperative bank was raised to 10% in 2012 (NAPC, 2017).

Borrowing from an agricultural bank and cooperative associations remains as an option, despite low interest rates, due to bureaucratic difficulties and unfair conditions required by the agricultural bank. The Rural families find access to such institutions very complicated, since they need a lot of time to fulfill all the formalities. In addition, high formal and informal costs of governmental and money lender credits clearly affect the competitiveness of domestic commodities in global markets due to higher production costs. Furthermore, poor families cannot attain the necessary conditions to meet the required guarantee by the agricultural cooperative bank. The public opinion on the state banks in Syria is even among the individuals who have not interacted with them before, that they have a lot of requirements, too complex and too expensive, and even corrupt (IFC, 2008). Hence the need to find a new, innovative way to provide rural families with the capital necessary to cover the costs of the production process and the formation of fixed productive assets and this new method of finance should appropriate with the economic and social circumstances of the poor rural families. Sometimes the problem of not benefiting from available capital sources is the beliefs of rural farming families themselves. Therefore, many studies recommend that it is necessary to provide loans for the rural production process. At the same time, these studies indicate the need to refuge the rural families to recent forms of loans with interest rate because of their incompatibility with the Islamic religion legislation (Abdo, 2014; Alsawan, 2017). Therefore, there is an urgent need to develop essential programs for an efficient rural credit system. Crises are generally an opportunity for fundamental changes in existing institutions to achieve sustainable rural development, provide financial solutions consistent with religious beliefs, and overcome shortcomings of the previous financing system. Meanwhile, the current credit systems are characterized by administrative and institutional ineffectiveness and the efficiency of public banks has been hampered by institutional deficits, internal governance and lack of qualified staff, low levels of capitalism and statutory legislative impediments (IFC, 2008).

The Aga Khan development network and the World Bank, through the Consultative Group to Assist the Poor (CGAP) has been actively involved in bringing microfinance to the forefront of the Syrian government agenda and Kreditanstalt für Wiederaufbau (KfW) has also been active within the microfinance sector (CGAP, 2008).

Therefore, the main objective of this paper is to highlight the importance of microfinance based on the Murabaha principles as an alternative to current official funding, using the microfinance program in the Livestock development project in Hama as a successful pilot case. Actually, this microcredit system seeks to achieve sustainable development by adopting the principle of Murabaha and it also seeks to help create employment opportunities for target groups, improve the income of the beneficiaries and their participation in funds management, and promote practical ideas managed by the rural people themselves.

Objectives of the paper

The significance of this research is to highlight the importance of the microcredit system principle of Murabaha (sale for Profit) in the agricultural sector as an alternative for the current agricultural financing method and to discuss the system’s strengths and weaknesses for the possibility of expanding it to all rural areas in the country and other developing countries that have the same social, economic and agricultural conditions.

The Murabaha (Cost-Plus Financing or sell for Profit) means sale on profit. Technically, it is a contract of sale in which the seller declares his cost and profit. As a financing technique, it involves a request by the client to the bank to purchase a certain item for him. The bank does that for a definite profit over the cost which is settled in advance. This research aims to study the mechanism of microfinance based on the Murabaha (resale for profit) by using data obtained from the Livestock Development Project (LDP), in the Governorate of Hama, Centre of Syria and finally this study aims to reach conclusions that can be applied and expanded in different rural areas and to ensure acceptance and participation by the target groups and their ability to repay. This research has a bird’s-eye view that collects information, conceptualization, analyze and conclude on the problems of agricultural finance.

LITERATURE REVIEW AND MICROCREDIT EMPIRICAL STUDIES

Investment in microfinance is a multi-purpose investment aim towards social and financial achievements. There are lots of studies on the role of microcredit in fighting hunger and advancing food security. Some relevant literatures will be used to build the conceptual framework of microfinance (CGAP, 2008, IFC, 2008; IFAD, 2009). Microfinance is a powerful tool to combat poverty. If the poor can reach financial services, they can gain more, build their assets, and protect themselves.

In China, Chinese Micro Finance Projects (MFPs) provided a very good case for studying microfinance outreach as they have overwhelmingly targeted the poor areas and households (the core poor) located in remote mountainous areas of northwest and southwest of China. In his study, Cheng (2007) advocates a strategic policy shift for donors and governmental institutions in China to redefine major clients of micro-loan services to those who have no access to formal loan services in the poor areas. However, the rich are effectively excluded, but among eligible households, rich and poor are equally likely to participate.

On the side of demand, farmers require credit for two reasons, the first is the acquisition of working assets to increase agricultural production, including simple inventory of goods to be resold through new marketing channels, and the second is credit as a liquidity reserve as Saris noted (Saris, 2001). These results are not out of line with the findings in Li et al. (2011a) as the microcredit program helped improve households’ welfare such as income and consumption. Despite the optimistic ï¬ndings on how microcredit has changed the rural households’ living conditions, results show that the majority of the program participants are not poor, which represents some doubts on the social potential (such as poverty reduction) of China’s microcredit programs. Li et al. (2011b) continued with microcredit research to examine the factors influencing the accessibility of microcredit by rural households using logistic regression and found that there are 12 household-level factors, including educational level, family size, income, and others such as interest rates and loan processing time.

An interesting paper about the microcredit in rural Morocco suggested that the demand for and use of microcredit is shaped not only by agro-ecological conditions, but by two major partially interrelated factors: debt-related norms articulated with the perception of the sanction in case of repayment default and the social life of microcredit, namely how social actors, credit officers, and local leaders engage with microcredit; the study argued that microcredit markets do not develop from demand-led supply, but instead, are historically, politically and socially constructed (Morvant-roux et. al., 2014). Amin et al., (2003) also evaluated whether microcredit programs reach the relatively poor and vulnerable farmers in two Bangladeshi villages. The study finds that while microcredit is successful at reaching the poor, it is less successful at reaching the group most prone to destitution, the vulnerable poor. It can be noted that there is an urgent need in microfinance programs to identify the main channels to reach real deserving people by involving the local communities in self-assessment process and identifying the groups with most needs for borrowing.

When talking about rural development, one should not lose sight of the role of rural women in development and their involvement in any program. A study about the gender and microcredit in India suggested that when agencies, governmental or non-governmental, in a developing country make credit available to low income women, they can reduce the costs of delivery, greatly increase repayment rates, and substantially improve the well-being of poor families (Elavia, 1994). Other study also suggests that such credit tends to increase women’s participation in decision-making, reduce fertility, substantially improve household nutrition and raise awareness for children’s education (Rosintan and Cloud, 1999). Thus, the microcredit for women is a commonly used strategy for women empowerment. The findings of a research about the empowerment effects of rural women’s access to microcredit in Ghana confirmed that women are empowered as a result of their access to credit of an NGO-run micro-lending program. However, another study shows that some women have little control over the use of loans and are not better off; some are subjected to harassment and are worse off due to their inability to repay loans on time (Ganle et al., 2015). A study in Uganda also presents experimental evidence on gender and receiving micro-loan. Microenterprise owners were randomly offered either capital with repayment (discount loans) or without repayment (grants) and were randomly chosen to receive business skills training in conjunction with the capital. The research found no short-run effects for female-owned enterprise either from capital offered or training received. However, it found large effects on profits and sales for male-owned enterprise that were offered loans and this study suggested that repayment requirements increased the likelihood of profitable investment (Fiala, 2018).

To overcome farmer’s inability to repay loans in low-productivity seasons, Akotey (2016) tried to provide micro insurance to solve this problem in a study conducted in Uganda. He examined the combination of microcredit and micro insurance and their potential to improve the well-being of low-income households. The study indicated that households using microcredit in combination with micro-insurance significantly gain in terms of welfare improvement. Microcredit alone may be good but its benefit to the poor is enhanced and sustained if the poverty trapping risks are covered with micro insurance. To this context, combining microcredit with micro insurance will empower the poor to sustainably combat against poverty (Akotey, 2016).

To confirm the significance of the microfinance, Chliova et al (2015) carried out a meta-analysis of empirical findings from 90 studies conducted to date about the microcredit and the main finding reveals the positive impact of microcredit on key development outcomes at the level of the client entrepreneurs, additionally this study scrutinized that the microcredit generally has a greater impact in more challenging contexts. Over the past 30 years, the Islamic finance has grown markedly to become a global industry alongside other traditional types of financing. The only difference between traditional and Islamic credit is the Islamic financing based on the Murabaha principle.

Murabah is defined by (Skeck, 2015) as a sale on profit and technically a contract of sale in which the seller declares his cost and profit. This has been adopted as a mode of financing a number of Islamic banks. As a financing technique, it involves a request by the client to the bank to purchase a certain item for him. The bank does that for a definite profit over the cost which is settled in advance. The main findings of this study are that Islamic Relief follows a set of criteria that governs the size and type of fund to achieve the growth of the working capital. It also follows clear policies that encourage small investors and fulfill the requirements of several economic sectors using “Murabaha”, as a suitable alternative to the other conventional financial systems. It was also suitable because it agrees with the Islamic laws and regulations and helps to control and organize the relationship with investors.

An interesting study about the impact of Murabaha rate on the financial performance of Jordanian Islamic banks' (2000-2013) concluded that there was a significant impact of Murabaha rate on the Return of Assets (ROA) in the Jordanian Islamic Banks. This result has been a good indication for the increasing demand to finance Murabaha, which increases the volume of investments and assets of the bank and therefore is reflected in the returns achieved in the future. Also, the study showed that there was a significant impact of Murabaha rate on the Return on Equity. This means that the bank has the ability to use its assets properly, whereas the Murabaha rate has no significant effect on the earning per share. Another study by Mohieldin et al. (2011) confirms the same finding. The most important result of this study is that Islam has a rich non-traditional means and mechanisms, if they have been applied in a true way, it can lead to poverty reduction and inequality in Islamic countries with widespread poverty.

The paper of Farsca (2008) explores the use of Islamic finance instruments in MENA, arguing that the experiences of Islamic microfinance (MFIs) operating in the MENA in the last decade demonstrate that Islamic MFIs can be competitive with conventional finance in the region, and can address the basic financial needs of their clients in a cost-effective manner as well as can meet the reported demand of lower income groups for religiously tailored financial services. On both an ideological level and practical level, microfinance and Islamic finance complement one another. Islamic finance’s emphases on entrepreneurship, materiality, and risk sharing are reflected in microfinance basic model of joint-liability lending to the poor entrepreneur.

It must be noted, there are a few studies that cover the agricultural Islamic microfinance, hence the importance of this study as the first one in this Islamic agricultural microfinance research field. The Islamic microfinance for development of livestock production initiative established by the Syrian agricultural ministry is the second initiative at the Syrian-level after the Jabaal Al-Hoss Project in rural Aleppo governorate. This project focused on rural development in general and it does not focus on agriculture. It was established in 1999 by the Syrian government with corporation with UNDP (Farsca, 2011).

METHODOLOGY

Data sources

The data were obtained from the following sources:

(i) Statistical information published in the annual agricultural statistical books, obtained from the Ministry of Agriculture and Agrarian Reform, as well as statistical data provided by the Central Bureau of Statistics, the country study prepared by the research centers on financing and loans such as the National Centre for Agricultural Policies and the reports of international organizations.

(ii) Data provided by the LDP management and interviews conducted in the Department of Livestock Development Project in Hama governorate. A field visiting was also carried out in the targeted villages and discussions with agricultural extension staff and the committees responsible for managing the village fund.

Analytical method

In order to achieve the objective of the study, the qualitative approach was used. A descriptive method is one in which information is collected without changing the environment. It is used to obtain information concerning the status of the phenomena to describe "what exists" with respect to conditions in a situation.

Based on the available data, this research tries to highlight the importance of the agricultural microcredit based principle of Murabaha (sale for Profit (as an alternative for the current agricultural financing method and to discuss the new system’s strengths and weaknesses for the possibility of expanding it to all rural areas in the country that have the same social, economic and agricultural conditions.

Description of the research area and the studied villages

According to the classification of Wattenbach (2006), the research area is in the fourth farming system in the subsystem of “rain-fed middle plains”. 78% of the cultivated land is rain-fed, which explains the low productivity of crops. The research area has increased barley production by two-thirds of the wheat production area. The main cultivated crops in the study area are barley, wheat, olive and cumin. The second main economic activity of the area is animal husbandry with a focus on sheep rearing.

The income sources in the rain-fed agricultural system depend mainly on seasonal agricultural or non-agricultural employment. The reason for seeking non-agricultural work are mainly due to the low yields of agricultural crops in the low rainfall area (average of less than 250 mm per year), which is compounded by the scarcity of other income sources. Rain-fed agriculture has been the result of the state's policies that prevent the drilling of wells in many regions to protect groundwater resources. According to the Wattenbach’s classification, there are three types of families in this sub-system: rich families, who account for 10% of the total population in the region (own more than 60 dunums of land; 1 dunum is equivalent to 1000 m2), medium families, who account for 30% (20-60 dunums), and the poor families, who account for 60% (less than 20 dunums) of the population. Poor and medium farmers are unable to obtain official loans because of their indebtedness to agricultural cooperative banks. Consequently, these farmers tend to borrow from the private sector with high interest rates. Thus, a big part of the governmental support to strategic crop goes to the traders who provide these loans. The poor farmers devote most of their production to household consumption, especially wheat, vegetables, and dairy products; however, they sell the surplus in good rainy years. It must be noted that the proportion of the rural population is 45% of the total population in Syria while the rural population in Hama Governorate is 63% (COS, 2013).

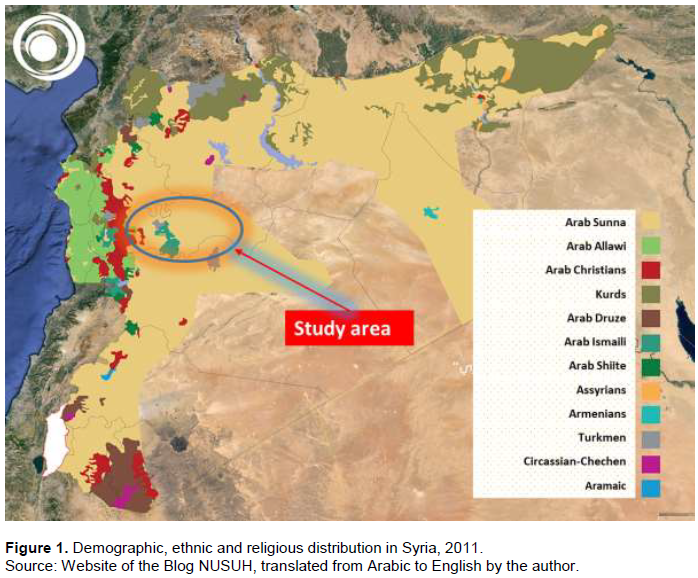

Actually, there is no official statistic on the religious demographic in the study area, but according to the US State Department's report on religious freedoms, the Sunni Muslim community in Syria is 77%, Allawi 10%, Druze 3%, Ismaili and Shi’a 8%, Christians and the Yazidi minority (US Department of the State, 2017). Figure 1 shows the demographic distribution in Syria. It is to note that the majority of the population in the study area regarding this figure is Arabic Sunnah, because of this fact, it is very important to carry out development program of credit based on the Islamic based principles.

RESULTS AND DISCUSSION

Following Prof. Muhammad Yunus’ Nobel Peace Prize, microcredit lending has risen to prominence and the volume of microcredit loans substantially increased. Yunus' initiative is expanding in developing countries, as each country has tried to develop the idea of microfinance in line with its potential and its economic, social and institutional environment.

Describe the traditional official finance in Syria

Although the state seeks to harmonize the financial system with the overall developmental objectives, the official credit system is still characterized by its inflexibility to provide loans for production activities. It experiences liquidity shortages and its complex conditions to access loans make it difficult to reach the poorest people; in some cases, personal relationships play a crucial role in obtaining access to credit. Many families are also unwilling to access bank loans for many reasons: religious factors that prevent borrowing for interest and the lack of experience required by the procedural requirements and guarantees necessary for the official credit; social factors also limit the access of rural families to official bank loans.

There is a great need to find an agricultural financing system that can overcome the above-mentioned problems of recent official credit system based on the principle of Murabaha which will be discussed later. The spread of the microfinance is expected in the agricultural sector and this approach is a socially and religiously acceptable solution to overcome the lack of liquidity by covering investment costs. It can be seen as a comprehensive approach due to its gender-neutral and participatory principle. It is also sustainable and has low risk of default for many reasons. Borrowers are shareholders at the same time and they manage the funds themselves. It is necessary to manage these funds effectively and for the credit to be repaid in monthly instalments. In addition, microcredit is used in animal production projects that are economically viable and have comparative advantage in the research area. The guarantee of each member in the funds reduces the risk of his inability to repay, which is considered as an additional advantage for this type of credit system. Unfortunately, the war in Syria since 2011 stopped production activities in most rural areas and the number of borrowers drastically decreased due to displacement of by the war.

Description of the agriculture and the livestock

Agriculture is considered as a significant sector of Syria’s GDP and more than 35% of rural households have animals (NAPC, 2017). Therefore, the ministry of agriculture has set up a large development project, called Livestock Development Project (LDP), to invest in a livestock sector in areas with low potential for crop production. LDP is seeking to develop a microcredit program as part of its project, so that all investments in the agricultural sector will not depend on sources like personal savings nor from external sources such as private lenders. The LDP has many dimensions of development, economic, and social goals and extension services, so it provides components of an integrated rural development in Hama governorate. It aims to achieve the following goals (Syrian agricultural ministry, 2017):

(i) To increase incomes of poor families in rural areas and small breeders who depend on livestock production in various agricultural stabilization zones and Al Badia (the Step), which is estimated at 311,000 families distributed in 1,260 villages throughout the country and targeting about 100 villages in the project area in Hama branch (research area).

(ii) To apply the principles of herd management through guidance and training in livestock breeding and production and to provide veterinary services such as immunization, treatment and provision of veterinary medicines.

(iii) To supply feed and use feed as resources for rangeland rehabilitation in the steppe, pastoral seeds propagation, and pastoral shrubs cultivation.

(iv) To establish a microfinance fund for targeted poor villages and families that has the capacity to manage the funds in a legal manner.

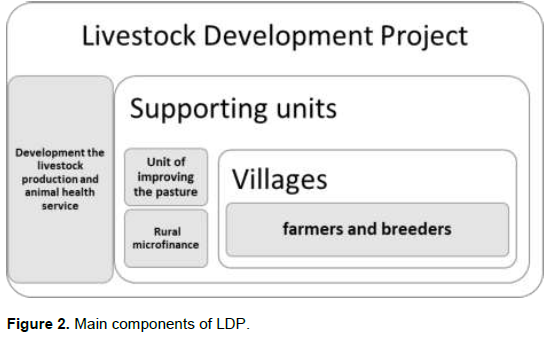

Main components of the LDP

The project is concerning the integrated development of livestock in Syria and is implemented by the ministry of agriculture and the agrarian reform (MOAAR, 2015.) with funding from the Syrian government and a grant from IFAD. One of the LDP primary objectives is to establish sustainable local financial institutions that are owned and managed by the people themselves. The main components of LDP are shown in Figure 2. As shown in the Figure 2, LDP comprises many units regarding livestock production.

(i) Unit for increasing livestock production by supporting animal health and agricultural extension services. This unit supports projects for rural women, human and animal health care, literacy courses and courses on how to make dairy products. These projects were carried out during the last five years.

(ii) Unit for pasture improvement and feed resources development.

(iii) Unit of development for small and medium-sized enterprises and rural finance for livestock production. 42 finance funds were implemented with 1,911 small loans with a total value of 140,956,000 Syrian pounds (SYP) or 281,912 United States dollar (USD) (1USD=500SYP) (LDP website).

Figure 1 shows that the vast majority of the population of the governorate of Hama and its countryside are Muslims. Therefore, this type of small loans will definitely find a great demand in the rural areas. As previously stated that more than half of the rural population in the study area are poor, so the microcredit is a very good capital provider based on the principle of the Islamic principle Murabaha what is suitable for them regarding the believes and small agricultural projects and enterprises.

Working approach of the village microfinance funds

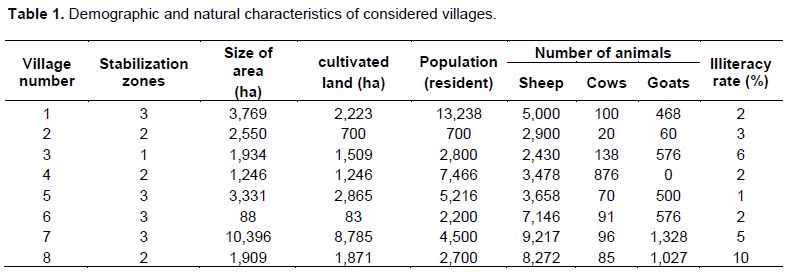

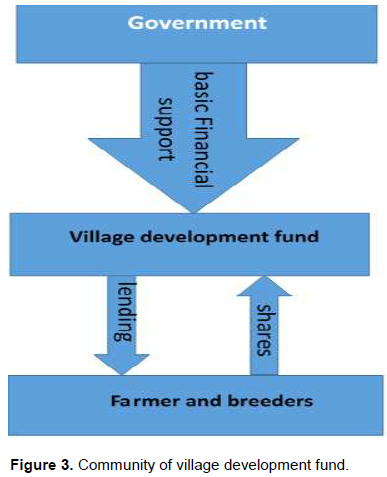

In the governorate of Hama, there were eight established funds by the end of 2014 with a total of 904 shareholders, of which 35% were women, and the loan amount totalled 1,775,000 SYP (MOAAR, 2015). Table 1 describes the demographic and characteristics of the eight villages. As it can be seen, the villages are in the first, second, and third settlement areas. These settlement areas vary in annual rainfall, 600, 350, and 250 mm/year, respectively (NAPC, 2017). Table 1 also shows that sheep breeding dominates the studied villages and there is a high percentage of cultivated land from the total area, which indicates the integration between livestock and crop production. In terms of illiteracy rate, all villages apart from three (6%) and Eight (10%) had relatively low illiteracy rate. Applying for microfinance funds from the LDP begins with the request of village residents to establish a village money box or fund (Figure 3). But the number of the members shall not be less than 100 persons and the contribution fee shall be set at 1,000 SYP per member. A three-member local committee is elected and trained to strengthen the participatory approach in managing the village fund; then, the three to six-month probationary phase begins. The evaluation of the village fund takes place after three years of lending. Figure 3 illustrates how microfinance works for a typical village in the research area.

The most important condition for obtaining the loan is that the applicant is a shareholder between 18-60 years’ old who resides in the village and is supported by two individuals who contribute to the fund. In terms of the microfinance policy, the provided credits are repaid with the Murabaha (Farsca, 2008) till the end of the loan. Murabaha is something different from loan interest. It is established by the banks for religious reasons and beliefs. However, the loan with Murabaha value is paid in monthly instalments. There shall be no other costs paid by the beneficiaries such as fees or penalty interest. Murabaha is the bank's intermediary to buy a commodity at the customer's request and then to sell it at a price equal to the total cost of the purchase plus an agreed amount of profit between the bank and customers (Skeck, 2015). The total cost of the purchase is the purchasing price of the commodity plus all the expenses paid by the bank for purchasing the commodity, less any discount the bank receives from the seller. The Murabaha amount is, therefore, the total purchasing cost plus the bank's profit.

The Murabaha contract consists of three parties: the seller, the buyer, and the investment bank or the trader who is an intermediary between the seller and the buyer.

However, the bank does not offer to buy the commodity until after the buyer has declared his desire to buy and promise to pay. In principle, Muslim scholars believe that Murabaha is allowed if it does not violate its conditions. It is to be noted that the principle of Murabaha is applied more in Islamic commercial and real estate banks.

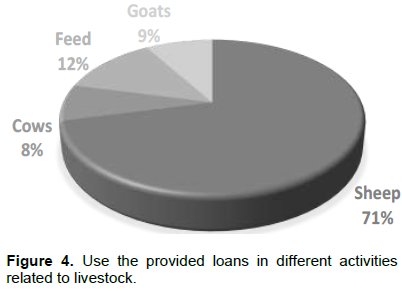

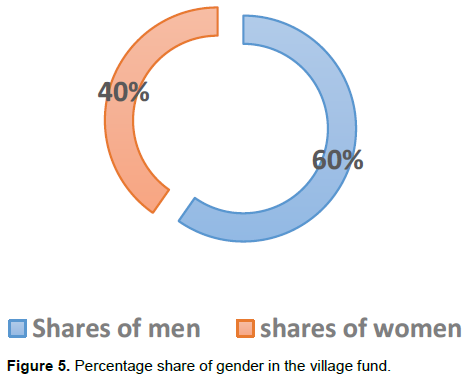

The LDP provides about one million SYP in cash to each village. Once shareholders add funds to the village fund, the money value further increases. Loans are distributed to farmers who periodically contribute to the village fund. The farmers provide the required documents and receive the loan that will be repaid over a period of 12 months. As it can be seen in Figure 4, the majority of the loan is used to purchase sheep for breeding and milk production. Breeding Awassi sheep is widespread in Syria, which is favoured by consumers in importing countries, especially Saudi Arabia. The breeders also prefer Awassi sheep because they are adapted to harsh local conditions and environment. Sheep breeding is a profitable economic activity and it competes against crop production on labor and capital production factors even in regions with high potential of irrigated crop production (Almohamed and Doppler, 2008; Cheikh and Almohamed, 2017). The second biggest part of the loan is used to buy feed; funds are also used to buy goats and cows for breeding. Figure 5 indicates the percentage of men and women in the considered villages. The men’s shares with 60% have a bigger part as the women only with 40%, but the difference is only about 10%. This shows the extent of women involvement in this microfinance program, which are almost completely unnoticed in short, medium and long-term loans provided by public banks such as the agricultural cooperative bank.

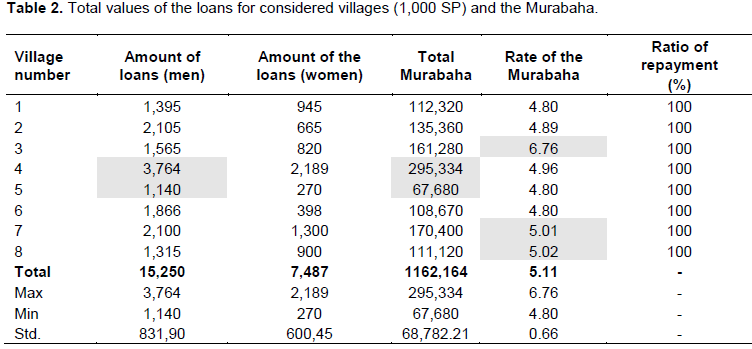

Table 2 shows there are differences in the amount of loans provided to each village without considering the population density of each village. Village Four had the largest share of loans with the biggest number of shareholders, and Village Eight had the lowest share of loans. In terms of the Murabaha, Village Three achieved the highest value of Murabaha while Village Five and Six achieved the lowest value. The project management had provided rewards for the villages with the highest value of Murabaha (Village Three and Eight, 6.76 and 5.02%, respectively). Table 2 also notes that the Murabaha rate is nearly equal to the interest rate of the agricultural cooperative bank (5%), which is less than the interest rate to non-cooperative farmers, which is usually 8%.

The high percentage of loan repayment and good rate of Murabaha in this successful microcredit example in Syria confirmed several advantages of this type of credit system, especially in rural development projects. Microcredit has the advantage of high demand and sustainability because it does not conflict with religious and social considerations of the rural target group and it is suitable to the poor farmer and breeders regarding its small volume. The active participation and contribution of rural women in the village’s funds enhanced the role of rural women in development and decision-making process, which contributed significantly to increase the income and living standards of their families.

The high repayment rate was observed because the credit is paid back monthly and it was used in very profitable small businesses namely livestock production. This Islamic microcredit is also sustainable because it is based on a participatory approach and the funds are self-managed by the local community, which increases the confidence of the borrowers. The process of selecting the supervising committee of the funds is democratically carried out and a free election takes place; the simplicity of getting the loan regardless of the amount and the absence of administrative and bureaucratic complications boost trust and confidence from the borrowers. This type of microfinance system could also have some disadvantages such as the absence of continuous evaluation by government agencies and the risk of the sustainability like other state agricultural project due to lack of continuous evaluation and ongoing maintenance. The lack of governmental evaluation can have negative effects on the effectiveness and efficiency of borrowing over time, which is reflected in other Syrian governorates’ weak performance and in some cases, personal relationships with the local supervising committee and project management play a major role in obtaining loans.

These advantages could encourage the private banks to enter this market of Islamic microcredit. The private sector will be a strong competitor to the public sector because of its administrative efficiency and continuous assessment of the lending process, but that needs more investment in rural infrastructure and increase the number of branches in the rural areas. Despite these disadvantages, it is necessary to find a socially acceptable and viable credit system that can help rural families finance the needed capital for agricultural production, to improve their incomes and living standards, and enhance women’s role in rural development.

CONCLUSIONS

Over the past 30 years, the Islamic finance has grown markedly to become a global industry beside other traditional types of financing. Therefore, Islamic finance and microfinance agree in essence, both of which are primarily concerned with providing social services and helping the neediest people. They also agree not to exploit the need of people and to profit from them but to call for social equality and to encourage the poor to get closer to the layers. The cooperative agricultural bank has played an important role in the Syrian agricultural sector. It provided subsidized loans with fixed interest rates as well as overseeing input provision and commodity purchase. In contrast, despite their needs, many rural residents have been unable to access this type of official funding because of the complex administrative and religious considerations. Thus, religious beliefs and social environment in rural areas have to be considered in any agricultural credit project to facilitate the establishment of a productive credit system as a means of continuously improving living conditions, distributing welfare benefits to all social groups and combating rural poverty. The credit system must also focus on the rural activities in which the target group has been successful in the past like the livestock production. Compared to crop production, livestock production has had lower vulnerability to external risks such as climate fluctuations and irregular rainfall; as a result, loans were focused on investing in livestock (Sheikh et al., 2017). To support income-generating activities for poor livestock breeders, government policies should focus more on the increased added value of milk products and milk processing, especially, Syria enjoys comparative advantage in the animal products in this sub-system that are mainly produced by poor households (NAPC, 2005).

It can be concluded that such an Islamic agricultural microfinance initiative can be considered as a successful one and an important innovation in a rural village of any Islamic developing country that can contribute to rural development, poverty reduction and creating jobs by providing financial services for the establishment of small enterprises. This type of credit can be considered as very suitable for rural areas in developing countries, fistful because it is directed to the small projects as is the agricultural sector based mostly on small family farms and it is centred on the principle of Islamic Murabaha, which corresponds the religious beliefs of the majority of the rural population. The Islamic microfinance has the potential to expand access to finance to unprecedented levels throughout the Muslim world. This type of credit uses the participation approach; the target group contribute to manage the village fund which strengthens farmers' confidence and contributes to the success of this initiative.

Unfortunately, in 2016 as a result of the war, this program stopped but there is hope it can be re-applied in the reconstruction phase in Syria because of its advantages, such as, to strengthen the role of rural women in improving the standard of living of their families and reducing poverty, which can be seen through the provision of about 45% of loans to rural women in the current research. The demand on this type of credit is high and does not conflict with the Islamic beliefs. There is a high potential of obtaining a legal formula for this type of micro financing since it is supported by a government institution which is the Syrian ministry of agriculture.

Agriculture financing is riskier than trade or industry finance. The village funds must therefore build up their institutional capacities to deal with the risks generally related to financial services provided to the poor and low-income families. The capacity-building of microfinance funds will therefore be strengthened by the project within the framework of improving management competencies at the microfinance management level and at the level of competency improvement among agricultural producers and livestock breeders, which are the actual clients of rural microfinance funds. The dependence of village funds on the financial nucleus is another risk to sustainability, so microfinance funds have to work to develop their own financial resources with the time.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

ACKNOWLEDGEMENT

The authors thank the donor Baden-Württemberg Stiftung and the Institute of International Education (IIE) for providing financial support and to thank the University of Hohenheim for hosting this research and our special thanks to Professor Regina Birner for providing scientific advice and logistical support.

REFERENCES

|

Abdo M (2014). The impact of the lending policy on farmers entering Syria in Hama governorate, Ph. D. Dissertation, Press of the Aleppo University, Aleppo, Syria 230 p. |

|

|

Almohamed S, Doppler W (2008). Sozioökonomische Analysen und Evaluierung des Bewässerungsprojektes West Maskana in Nord |

|

|

Alsawan A (2017). Indicative needs of sheep breeders in Hama Governorate, Ph. D. Dissertation, Press of the Aleppo University, Aleppo, Syria 330 p. |

|

|

Amin S, Ashok RS, Topa G (2003). Does microcredit reach the poor and vulnerable? Evidence from northern Bangladesh. Journal of Development Economics 70(2003):59-82. |

|

|

Akotey J, Adjasi C (2016). Does microcredit increase household welfare in the absence of micro insurance. Journal of World Development 77:380-394. |

|

|

Central office of statistic (COS) (2013). The annual statistic book, website of COS: |

|

|

Cheng E (2007). The Demand for Micro-credit as a Determinant for Microfinance Outreach-Evidence from China. Centre for Strategic Economic Studies. Paper presented at the ACESA 2006 Emerging China: Internal Challenges and Global Implications, Victoria University, Melbourne, 13-14 July 2006. |

|

|

Cheikh D, Almohamed S (2017). An analytical study of some economic indicators of sheep breeding in Hama Governorate. Journal of Aleppo University, Agricultural Science series, 123, 2017, Aleppo, Syria. |

|

|

Chliova M, Brinckmann J, Rosenbusch N (2015). Is microcredit a blessing for the poor? A meta-analysis examining development outcomes and contextual considerations. Journal of Business Venturing 30:467-487. |

|

|

Consultative Group to Assist the Poor (CGAP) (2008). Policy and Regulatory Framework for Microfinance in Syria, working paper series 43433, February, 2008. |

|

|

Elavia BH (1994). Women and rural credit - A delivery system, in "Capturing Complexity -An Interdisciplinary look on Women, Household and Development", (Eds.) Romy Borooah, Kathleen Cloud, et. al. Sage Publications, New Delhi/ Thousand Oaks/ London pp. 151-162. |

|

|

Fiala N (2018). Returns to microcredit, cash grants and training for male and female micro entrepreneurs in Uganda. World Development 105:189-200. |

|

|

Farsca A (2008). A Further Niche Market: Islamic Microfinance in the Middle East and North Africa" Center for Middle Eastern Studies & McCombs School of Business, University of Texas at Austin. |

|

|

Ganle J, Afriyie K, Segbefia AY (2015). Microcredit: empowerment and disempowerment of rural women in Ghana. Journal of World Development 66:335-345. |

|

|

International Fund for Agricultural Development (IFAD) (2004). Rural Finance Policy. Rural Finance Working Paper (No. 2). A Background Paper: Challenges, Opportunities and Options for the Development of Rural Financial Institutions. |

|

|

International Fund for Agricultural Development (IFAD) (2009). The annual report about the rural development project in Idleb, Syria. |

|

|

International finance corporation world bank group (IFC) (2008). Syria: microfinance market assessment, final report, publisher Grameen Jameel, Bensilvania, Washigton D.C. |

|

|

Li X, Gan C, Hu B (2011a). The welfare impact of microcredit on rural households in China. Paper Journal of Socio-Economics 40:404-411. |

|

|

Li X, Gan C, Hu B (2011b). Accessibility to microcredit by Chinese rural households, Journal of Asian Economics 22:235-246. |

|

|

Ministry of Agriculture and Agrarian reform (MOAAR) (2015). Projects and institutes, Livestock development project, Damascus, Syria. |

|

|

Morvant-roux S, Gue´rin I, Roesch M, Moisseron J (2014). Adding value to randomization with qualitative analysis: The case of microcredit in rural morocco. Paper in world development. 56:302-3012. |

|

|

Mohieldin M, Iqbal Z, Ahmed R, Xiaochen F (2011). The Role of Islamic Finance in Enhancing Financial Inclusion in Organization of Islamic Cooperation (OIC) Countries, Available at Finance and Financial Sector Development on World Bank Group (December 2011) |

|

|

National Agricultural Policy Centre (NAPC) (2017). Current status of the agricultural sector, Damascus, Syria. |

|

|

National Agricultural Policy Centre (NAPC) (2005). Supply Chain Coordination and Policy Implications the Case of Dairy and Red Meat Products in Syria, working paper N0.7, Damascus, Syria. |

|

|

Nusuh Blog (2016). The demographic change in Syria. |

|

|

Rosintan DMP, Cloud K (1999). Gender, self-employment and microcredit programs, an Indonesian case study. The Quarterly Review of Economics and Finance 39:769-779. |

|

|

Saris A (2001). The strategy of the agricultural development in Syria. Project GCP/SYR/006/ITA, as part of the cooperation program between the Syrian Government, the Italian Government and FAO, Damascus, Syria. |

|

|

Skeck DMA (2015). The impact of Murabaha financing on the growth of the working capital. An empirical study of the small projects funded by Islamic Relief in Palestine. Master dissertation, The Islamic university, the faculty of trade, Gaza, Palestine. |

|

|

Syrian Agricultural Ministry (2017). Project of livestock development, Damascus, Syria. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0