Full Length Research Paper

ABSTRACT

Agriculture plays a great role in the economy of many countries including Tanzania where the majority depends on agriculture-based activities for their livelihoods. Access to agricultural credit is vital for growth and development of agricultural sector in Tanzania, hence financing agriculture is a key issue in rural development. Despite effort of the Government to make agricultural credit services available and affordable to its majority, access to credit among smallholder farmers is still very low. The aim of this study was to assess the determinants of credit demand by smallholder farmers. A multistage sampling technique was employed in this study. Ten (10) wards were selected with 30 respondents from each ward making a sample of 300 smallholder farmers. A binary logistic regression model was used to analyze the influence of smallholder farmer’s socio-economic characteristics on credit demand. The maximum likelihood estimates of the logistic regression revealed that access to agricultural credit among smallholder farmers was determined by age of the respondents, gender, number of years of schooling, household size, distance, awareness, collateral, type of crops, farm size, contact with extension services, membership to economic farm groups, location of the farm and interest rate. However, gender of the respondent, distance, collateral and interest rate though statistically significant, had negative influences on smallholder farmer’s decision to demand and access agricultural credit. The study recommends that Microfinance Institutions (MFIs) should be strengthened and smallholder farmers be ensured to access agricultural credit with minimum and bearable formalities for agricultural development in Tanzania.

Key words: Credit, demand, smallholder farmers, agriculture, microfinance institutions.

INTRODUCTION

Smallholder farmers in Tanzania dominate the agricultural sector, cultivating 5.1million ha annually, of which 85% is used for food crops. They contribute to over 75% of total agricultural outputs in Tanzania, producing mainly for home consumption, and using traditional technologies. Smallholder families in Tanzania primarily grow food and staple crops. Maize is the most commonly grown staple crop, followed by beans, cassava, sweet potatoes, and rice. Since credit is regarded to be a key element or component in raising agricultural productivity, then improving access of credit to smallholder farmers is perceived as an effective strategy to increase smallholder productivity and alleviate poverty (Binswanger and Khandker 1995; Adugna and Heidhues, 2000). Therefore, provision of credit to smallholder farmers in Tanzania has to be regarded as an important instrument for improving the welfare of smallholder farmers directly and for enhancing productive capacity through financing investment by the farmers in their human capital and physical capital.

Adequate access to credit has the potential to impact technology adoption, thereby improving agricultural productivity and sustainable agricultural intensification (Simtowe et al., 2009). In Tanzania agricultural credit has positive impacts on smallholder farmer’s productivity as it enables them in farming operations that is, to have access to inputs such as improved seeds, fertilizers, chemicals etc. and hiring labour when needed (Zeller et al., 1998; Feijo, 2001; Mahmood et al., 2013; Girabi and Mwakaje, 2013; Masuku et al., 2015). Furthermore, farmer’s access to adequate credit has consequences on food security, household welfare, and poverty (Bashir et al., 2010; Reyes and Lensink, 2011; Awunyo-Vitor and Al-Hassan, 2014a). Credit rationing affects farmers’ ability to purchase farm inputs and make farm-related investments (Ghosh et al., 1999; Okurut et al. 2005; Reyes and Lensink, 2011). It also affects the risk behavior of producers (Eswaran and Kotwal, 1990). A farmer that is credit rationed will undertake investments in less risky and less productive technologies, rather than in more risky and productive ones (Dercon, 1996). In addition to agricultural productivity, credit rationing could affect rural development by preventing households from taking up off-farm activities, which are critical for structural transformation and the ability to move out of poverty (Ghosh et al., 1999; Ellis, 2000; Okurut, 2005).

The Tanzania banking sector embarked on a plan for financial liberalization in 1992 in order to sustain its economic growth (BOT, 2011). This has been accomplished through the mobilization of financial resources as well as by increasing competition in the financial markets and by enhancing the quality and efficiency of credit allocation. As a result of the liberalization, new merchant banks, commercial banks, bureaus de change, credit bureaus and other financial institutions have entered the market. Currently, according to the latest banking report of the Bank of Tanzania (BOT), the number of branches has increased to 821 in 2017 from 810 reported in 2016 which corresponds to an increase of 11 branches or 1.36% (BOT, 2011).

Several studies worldwide have been conducted with regard to credit demand by smallholder farmers. In Tanzania, despite the presence of credit providing institutions, financing of smallholder farmers has been an issue of debate, hence agriculture has not yet impacted in raising the living standards of its people. On the other hand, little has been done to ascertain the factors constraining smallholder farmers in accessing credit from microfinance institutions. If this problem will not be solved, the agricultural productivity will be low and cannot match with the process of economic transformation from agrarian to industrialization since agriculture-based industries need enough raw materials from agricultural sector. Hence this study is geared at investigating the determinants of credit demand by smallholder farmers in Tanzania.

Theoretical and analytical framework

This study has a theoretical background from the rational choice theory, an approach used by social scientists to understand human behavior (Becker, 1976). The rational choice theory was developed by the first economist Adam Smith on the ideas of rational choice theory through his studies of self-interest and the invisible hand theory. Rational choice theory in this case assumes that smallholder farmers have preferences among the available choice alternatives that allow them to state which option they prefer. These preferences are assumed to be complete and transitive (that is, if a farmer prefers A to B and B to C, then he/she necessarily prefers A to C. If he/she is indifferent between A and B, and indifferent between B and C, then he/she is necessarily indifferent between A and C). The rational agent is assumed to take account of available information, probabilities of events, and potential costs and benefits in determining preferences, and to act consistently in choosing the self-determined best choice of action. The theory dictates that every individual, even when carrying out the most mundane of tasks, perform their own personal cost and benefit analysis in order to determine whether the action is worth perusing for the best possible outcome. Therefore, this approach takes preferences as primitive and views them as determining choices.

Conceptual framework of the study

The conceptual framework of the study as depicted in Figure 1 shows that, there are several factors that determine smallholder farmers’ demand for credit from micro financial institutions. These factors include farmer’s characteristics such as age of the household head, gender, education level and household size. Also, other factors emanate from lending institutions, such as distance to bank, awareness of lending institutions, collateral requirements and interest rates. Finally, are farm related independent variables such as, type of crop grown, farm size, contact with extension services, membership to farm economic group and location of his/her farm.

MATERIALS AND METHODS

Description of the study area

The study was conducted in Morogoro Municipality. Morogoro Region occupies a total of 72,939 km2 which is approximately 8.2% of the total area of Tanzania mainland. It is the third largest region in the country after Tabora and Rukwa Regions. Morogoro region covers an extensive area well-endowed with fertile land, numerous water sources (Ngerengere River, Ruaha River, Wami River, Morogoro River, Mindu Dam, Kilakala River, Melela River, Kilombero River etc.), irrigable areas and a low population density. All these factors put together make the region very much attractive for agricultural investment. Total arable land is estimated to be about 5,885,800 ha, of which 1,177,500 ha are under agricultural production (URT, 1997) (Figure 2).

Demographically, the total estimated population of Morogoro Municipal Council according to URT (2012) was 315,866 people of which 151,700 were male and 164,166 were female. Population density was 31 persons per square kilometer (URT, 2012: 6). Morogoro municipality is located in the eastern part of Tanzania, 196 kilometers (122 miles) west of Dar es Salaam, the largest and commercial city in the country and 260 km (160 mi) east of Dodoma, the country’s capital city. Its geographical coordinates are 6° 49’ 0” South, 37° 40’ 0” East. The social-economic activities in Morogoro municipality are agriculture, tourism, wildlife and forestry, and industry. However, agriculture is the major economic activity in the Morogoro Region (URT, 1997). Morogoro lies at the base of the Uluguru Mountains and it is a centre of agriculture in the region. Also, Morogoro municipality has a total number of 7766 smallholder farmers in different 20 wards (Waluse, 2020).

Sample size and sampling technique

A multistage sampling technique was employed to selected representative households for the study (Barnett, 1991). The first stage involved a reconnaissance survey conducted to identify smallholder farmers that have applied for agricultural credit in Morogoro municipality. Ten wards out of 20 wards namely, Bigwa, Mindu, Kingolwira, Tungi, Mzinga, Kichangani, Mafisa, Mazimbu, Chamwino and Mkundi were purposively selected because they have a large number of smallholder farmers and location advantage to lending institutions that is, Co-operative and Rural Development Bank (CRDB), National Bank of Commerce (NBC), Kenya Commercial Bank (KCB), National Microfinance Bank (NMB), Bank of Africa (BOA) etc. The second stage involved random sampling of 30 respondent households from each ward in order to get a total of 300 representative sample of the whole community.

Data type and collection

Primary data were collected from 300 smallholder farmers of the study area who were interviewed using structured questionnaires from a cross section of the household heads who had applied for agricultural credit. Data were collected on households’ demographic and socio-economic characteristics as well as on income.

Data analysis

The binomial logit regression model was used to determine the factors influencing smallholder farmer’s decision to demand and access agricultural credit in the study area. The logit model was chosen since it is a standard method of analysis when the outcome variable is dichotomous (Hosmer and Lemeshow 2000). Therefore, the cumulative logistic probability model is econometrically specified as follows:

Where;

= the probability that a household head is credit user or non-credit user given Xi;

? = the base of natural logarithms, which is approximately equal to 2.71828;

α = Constant term;

Are parameters to be estimated (the regression coefficients or slope of the individual predictor (or explanatory) variables.

Xi (1-13) = the explanatory or predictor variables.

The logistic regression model could be written in terms of the odds ratio (OR) and log of odds because it enables one to understand the meaning and the interpretation of the coefficients (Hosmer and Lemeshow, 2000). The odds ratio implies the ratio of the probability (Pi) that an individual would choose an alternative to the probability (1-Pi) that he/she would not choose it.

Therefore; the odd ratio becomes,

Or to get linearity, we take the natural logarithms of odds ratio in equation (3), which results in the logit;

As P goes from 0 to 1 (that is, as Z varies from −∞ to +∞), the logit L goes from −∞ to +∞. That is, although the probabilities lie between 0 and 1, the logits are not so bounded (Gujarati, 2003). If the disturbance term µ is taken into consideration and for estimation purposes, the logit model becomes,

Whereby

L = the logit, and hence the name logit model

Ln = log

=The odds ratio

=The odds ratio

α = Constant term

βi = Are parameters to be estimated (the regression coefficients or slope of the individual predictor (or explanatory) variables that will be modeled.

Xi (1-13) = The explanatory or predictor variables

µ = Stochastic error term

The explanatory (independent) variables specified as factors influencing farmer’s decision to access credit and utilize for production are defined hereunder;

X1 = Age of the household head (Years)

X2 = Gender (Dummy: 1= Male, 0= Female)

X3 = Education level (Categorical, Cat1= No education, Cat2=Primary education, Cat3=Secondary education, Cat4= Post-secondary education)

X4 = Household size (Number of people)

X5 = Distance to Credit Source (km)

X6 = Awareness of lending institution (Dummy: 1=yes, 0=no)

X7 = Collateral Need (Dummy: 1=yes, 0=no)

X8 = Interest rate (%)

X9 = Type of Crop Grown (Dummy: 1 = Cash crops, 0 = food crops)

X10 = Farm size (Ha)

X11 = Contact with Extension services (Dummy: 1 = yes, 0 = no)

X12 = Membership to farm economic group (Dummy: 1 = yes, 0 = no)

X13 = Location of farm (km) (Dummy: 1= favourable location for Agriculture that is, nature of the soil, 0= unfavourable location

In a more detailed specification, equation is written as;

Whereby L=Logit as defined above

α = Constant term or intercept of the equation

RESULTS AND DISCUSSION

Determinants of credit demand by smallholder farmers

In this study, the estimated determinants of credit demand by smallholder farmers from MFIs using logit model encompassed the age of the farmer, gender of household head, education level (years of schooling), household size, distance from farmer’s residence to the MFIs, awareness of lending institution, collaterals, type of crops grown (that is, cash or food crops), farm size, contact with extension officers, membership to farm economic groups (group membership), geographical location of the farm and perception of interest rate charged by MFIs.

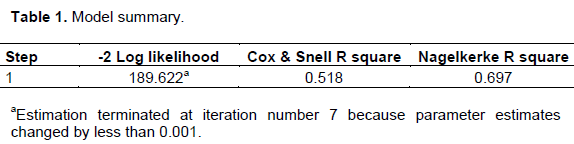

The maximum likelihood method using SPSS 20 was used to estimate the coefficients of the specified binary logistic regression model. The model fit was tested using the Hosmer and Lemeshow statistics. Table 1 presents the estimated logistic regression model that gave an adjusted Pseudo R-squared about 0.697 implying that all explanatory variables included in the model were able to explain about 69.7% of the probability of smallholder farmer’s decision to demand and access credit from MFIs. Though the Pseudo R-squared value was 69.7%, on the other hand, the log likelihood ratio (LR) is significant at 1% meaning that the independent (explanatory) variables in the binary logistic regression model together (jointly) explain perfectly well the probability of smallholder farmer’s decisions to demand agricultural credit from MFIs in Morogoro municipality.

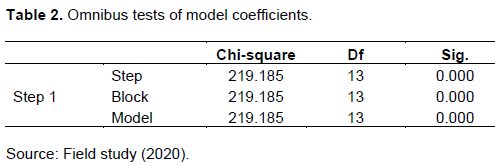

In other words, the study findings show that there is a strong relationship between dependent variable and explanatory variables included in the model. Furthermore, on the basis of the two goodness of fit measures namely, the Pseudo R-squared and the log likelihood ratio (LR), it is concluded that the logistic regression model used is accurate, relevant and appropriate in the prediction of the level of probability of farmers to apply and acquiring credit. Also, the study findings show the overall percentage of correct prediction was 88% while p-value was 0.000 shows that there is a highly significant difference between the observed and predicted values of independent or explanatory variables implying that the model’s estimates well the data and fit the data at acceptable level. Also, in this analysis the distribution reveals that the probability of the likelihood ratio Chi-square (219.185) was 0.000 than 0.001 (1%) level of significance that is, p<0.001 indicates that the logit model in this study was appropriate and is highly statistically significant at 1% implying that all the variables included in the model were jointly different from zero (0). Table 2 presents the results.

The findings of the study also reveal that the smallholder farmer’s socio-economic characteristics have significant influence on the household decisions to demand and access agricultural credit from MFIs in Morogoro municipality. The study findings show that the application of the logistic regression model in estimating the determinants of credit demand by smallholder farmers in Morogoro municipality was valid and consistent with similar empirical studies on credit demand surveyed in the previous chapter two (Malik and Nazli, 1999; Benerjee, 2001; Ayamga et al., 2006; Akram et al., 2008; Akudugu et al., 2009b). In Table 3 variables like age, gender, education level, household size, distance, awareness or information about lending institution, collaterals, type of crops (that is, cash or food crops), farm size, contact with extension office, group membership, location of the farm and perception on the interest rate charged by MFIs were identified and hypothesized to explain the smallholder farmer’s decision to demand and access agriculture credit from MFIs. The binary logit regression analysis indicates that nine variables were significant and positively related to dependent variable while four variables were significant but negatively signed as assumed in our model specification. Table 4 presents the results.

As displayed by standard errors (SE), the Wald χ2 statistic and p-value (sig) which yields the largest value of the probability of making a Type 1 error, the study findings indicated that age of respondent, household size, collaterals, education level, and interest rate were highly statistically significant at one percent level of significance; gender, distance, farm size, contact with extension officers and location of the farm were statistically significant at five percent level of significance while awareness of the lending institution, types of crops and group membership were statistically significant at ten percent level of significance. Also the study found out that among these determinant factors, there are those with positive marginal effect on probability of the smallholder farmer’s decision on demand to and access to agricultural credit which includes age, education level, household size, awareness, types of crops grown, farm size, contact with extension officers, group membership, location of the farm and those with the negative marginal effect on credit demand namely gender, distance, collaterals and interest rate charged by MFIs. All these outcomes are according to the expectation.

Age of the respondent

The study findings revealed that the age was highly statistically significant at one percent level of significance. Also, age of the respondents met the a priori expectation that there is a direct relationship between age and the probability of smallholder farmer’s decision to demand and access agricultural credit from MFIs. The farmers were categorized into two groups, the old and young farmers. So, age was a dichotomous variable like the rest of the variables in the model. Old farmers were assigned the value of 1 and young one the value of 0. The slope coefficient of age implies that the log odds ratio of old smallholder farmer decision to demand credit changes to young farmers is 2.656 units. But since it is not straight to comprehend changes in log of odds, it is usually more revealing to analyze the estimated logit equation in terms of changes in the odds ratio which is the ratio of the probability that the smallholder farmer demands credit to the probability that he/she will not demand credit. The respective odds ratios of different regressors are listed in the Exp (B) column in Table 4.

The odds ratio of the age variable is equal to 14.237, this means that the odds ratio of age in favour that the smallholder farmer will demand credit will increase 14.237 times if his/her age increases by one unit that is switching from 0 to one in other words switching from young small holder farmers to old ones. The evidence shows that as the age of respondents increases, the probability that demand for agricultural credit by smallholder farmers increases implying that older farmers are assumed to accumulate knowledge, experience in farm production activities and well informed about lending institutions, hence, the demand for and access to agricultural credit will increase (Mignouna et al., 2011; Kariyasa and Dewi, 2013). This study result is in line and/or consistent with the findings of various related studies in which age was found to be significant and positively related to smallholder farmer’s decision to demand and access agricultural credit (Crook, 2001; Diagne and Zeller, 2001; Akram et al., 2008; Akudugu et al., 2009a; Akudugu, 2012; Akpan et al., 2013; Mohammed et al., 2013; Hananu et al., 2015; Filli et al., 2015). Therefore, the study concludes that age plays a pivotal role in influencing smallholder farmer’s decision to demand and access agricultural credit from MFIs.

Gender of the respondents

In this study gender was found to be negatively related to smallholder famer’s decision to demand and access agricultural credit. Gender was found to be statistically significant at 5% level of significance indicating that male farmers are less likely to access agricultural credit from MFIs than their female counterparts. This is shown by the odds which are equal to 0.355. This means that male smallholder farmers are more than 0.355 times likely to get credit than their female counterparts. Put in a reverse way, female smallholder farmers are more than 2.8 times likely to get credit than male farmers. The study result is consistent with the various related studies which reported a negatively significant relationship between gender and access to agricultural credit by smallholder farmers (Akudugu, 2012; Ololade and Olagunju, 2013; Tetteh et al., 2015; Hananu et al., 2015; Lemessa and Gemechu; 2016). This is consistent with what is happening in practice in Tanzania where there are many credit venues exclusively for women. This is deliberate to raise the welfare status of women. It is generally agreed that female faces many challenges in accessing credit from MFIs which is linked to the inferior status of women in many societies, their underestimation as an economic agent as well as gender bias (Blanchflower et al., 2003; Adesua and Adebimpe, 2011). The study results imply that the chains that tied down females to have access to credit services compared to males have been broken. The reasons that restrict females’ access to credit services from MFIs were lacks of a control of economic resources and the nature of their economic activity (Matheswaram and Amita, 2001). Therefore, the fact that female is the most disadvantaged, vulnerable and above all, not credit worthy is no longer valid in the context of smallholder farmers in Tanzania.

Education of the respondents

The literacy met the apriori expectation of positive influence on the smallholder farmer’s decision to demand and access agricultural credit from MFIs. It was found that education level of the respondents had a highly statistically significant positive effect on smallholder farmer’s demand and access to agricultural credit at 1% level of significant implying that educated farmers were associated with the ability to access and comprehend information on credit services and MFIs criteria also the ability to fill loan application forms properly. The odd ratio for education is 12.462 indicating that smallholder farmers who have acquired education of some kind are more than 12.5 times likely to access credit than smallholder farmers who have no education. This finding regarding education level of the respondents is consistent with the findings of various related studies which found that education significantly influences the smallholder farmer’s decision to demand agricultural credit, access to and participate in formal credit programmes (Feder et al., 1985; Crook, 2001; Ayamga et al., 2006; Hussein, 2007; Lukytawati, 2009; Bakhshoodeh and Karami, 2008; Nwaru et al., 2011; Dzadze et al., 2012; Akudugu, 2012; Etonihu et al., 2013; Ibrahim and Bauer, 2013; Baiyegunhia and Fraser, 2014; Abraham, 2014). Therefore; level of education influences smallholder farmer’s decision to adopt new agricultural technologies that led to the improvement of agricultural productivity.

Household size

Household size variable is a dummy variable which assigned the value of 1 if the household has 4 and more members and it is assigned the value 0, if the number of members is less than 4. The study findings revealed that the coefficient on household size was positively and highly statistically significant at 1% level significance and translated literally it implies that an increase in household size by one (1) unit increases the log of odds by 1.443 units. But since it is a dummy, it means that households with 4 members plus are more than 4 times more likely to access credit than households with 3 members and less. This study meets the apriori expectation of positive relationship with the probability of the smallholder farmers demanding agricultural credit from MFIs. This implies that increase in household size that is, number of family members makes labour force available for production purpose. This influences the smallholder farmer’s decision to demand agricultural credit for purchasing inputs that is, improved seeds, fertilizer, pesticides and equipment’s as an effort to maximize outputs to meet family needs. This indicates that the households with a large number of family members are likely to demand more loans to meet their production targets. The study result is consistent with the various related studies which reported a positively significant relationship between household size and access to agricultural credit by smallholder farmers (Chitungo and Munongo, 2013; Tetteh et al., 2015; Hananu et al., 2015).

Distance

The study findings revealed that distance from the smallholder farmer’s residence to the lending institutions that is, MFIs was found to meet a priori expectation of negative relationship with the credits accessibility. Though was negative but found to be statistically significant at 5% ) level of significance. The study result implies that the smallholder farmers who live far away from the credit service provider are less likely to consider decision to demand and access agricultural credit compared to those who live closer to credit services. Small holder farmers who live in the proximity of lending institutions are 3.3 (1/0.233) times more likely to apply for and access than smallholder farmers who live far away. The study result is consistent with the findings of various related studies which agreed that the closer the source, the higher the probability of the smallholder farmer’s decision to demand and access credit from MFIs and vice versa (Ayamga et al., 2006; Fakayode and Rahji, 2009; Hashi and Toçi, 2010; Oboh and Ineye, 2011; Henri-Ukoha, 2011; Akudugu, 2012; Abraham, 2014). Therefore; the findings of this study revealed that farming households who lives near to the lending institutions that is, MFIs have location advantage and positively effects smallholder farmer’s decision to demand and access agricultural credit and vice versa.

Awareness of MFIs

The smallholder farmer’s awareness of lending institutions in this study was found to be statistically significant at 10% level of significance. The study result met a priori expectation of positive relationship implying that smallholder farmer’s awareness increases the probability of accessing loan. The farmers were categorized into two groups, the smallholder farmers who are aware with credit facilities from MFIs were assigned the value 1 and zero otherwise. The odd ratio for awareness of MFIs is 3.723 indicating that smallholder farmers who are well informed and aware on the availability of credit services, credit type, procedures and conditions of MFIs are more likely to demand and access agricultural credit 3.7 times than smallholder farmers with no information about credit facilities. The study result is consistent with the findings of various related studies which found that adequate flow of information influences smallholder farmer’s decision to demand credit due to the awareness of MFIs and procedures in accessing loan (Ennew and Bink 1997; Jappelli and Pagano 2002; Abraham 2014; Tetteh et al., 2015).

Collaterals

The study findings revealed that though was negative but was found to be highly statistically significant at 1% level of significance. The smallholder farmers with collateral were assigned the value one and zero otherwise. The study result indicates that having collateral hinder the demand for agricultural credit as it was found to have a negative relationship with credit accessibility as shown by the odd ratio which is 0.104. This implies that smallholder farmers with collaterals are more likely to have more assets that can help them to finance their production activities without credit and vice versa. The study result is consistent with various related studies which found that collateral have negative effect to smallholder farmer’s decision to demand and access agricultural credit (Assogba et al., 2017; Ololade and Olagunju 2013).

Type of crops grown

The study findings revealed that the cultivation of cash crops was positively related to the credit accessibility. In this study type of crops grown was found to be statistically significant at ten percent level of significance. The study result met our priori expectation of positive relationship that influences smallholder farmer’s decision to demand credit from MFIs. The smallholder farmers were categorized into two groups, those who cultivate cash crops and those who cultivate food crops. The odd ratio of the type of crops is 3.074 implying that the smallholder farmers who cultivated cash crops that is, rice (paddy), banana were more likely to demand agricultural credit from MFIs for financing their production activities 3.1 times than those who cultivated food crops. This study result is consistent with the findings of various related studies which found that cash crops influences positively demand for agricultural credit (Dzadze et al., 2012; Akudugu, 2012; Chauke et al., 2013; Hananu et al., 2015). Therefore, the smallholders’ farmers who cultivate cash crops are profit maker hence demands agricultural credit for expanding their production activities and hence take advantage of economies of scale than those who cultivate food crops for their own consumption.

Farm size

The study findings revealed that the farm size was positively related to the smallholder famer’s decision in demanding and access to agricultural credit from MFIs. Farm size was found to significant at five percent level of significance. It was agreed that access to credit services is influenced by the size of farm that a household invests and adoption of new agriculture technologies which needs additional capital (Nyangena, 2007; Langyintuo and Mulugetta, 2008; Jogo et al., 2013; Mwangi and Kariuki, 2015). Farm size in this study met the apriori expectation of positive relationships; it was a significant determinant of the credit demand by smallholder farmers from MFIs. The odd ratio is 2.735 indicating that famers with large farm size have the odd in favour of demand for agricultural credit 2.735 times than those with small farm size. This study result is consistent with the findings of various related studies (Uaiene et al., 2009; Simtowe et al., 2009; Oboh and Ekpebu, 2011; Mignouna et al., 2011; Akudugu, 2012; Abraham, 2014; Hananu et al., 2015). Despite the fact that land plays a pivotal/vital role as a collateral security for granting credit, it also gives the smallholder farmers freedom to consider risk option in adopting new agricultural technologies which demands additional capital which might be obtained through credit. Therefore, the study concludes that increase in farm size increases demand for the factors of production that is, labour, capital, improved seeds, fertilizers, and equipment which needs additional capital that might be obtained through agricultural credit.

Contact with extension

The study findings revealed that extension contact had a positive relationship with access to agricultural credit from MFIs. The smallholder farmers were categorized into two groups, those who had contacted agricultural officers were assigned the value 1 and zero otherwise. It was found to be statistically significant at 5% level of significance with positive marginal effect on smallholder farmer’s decision to demand and access agricultural credit. This implies that the extension service enhances agricultural credit accessibility by smallholder farmers 3.655 times than those without contact with extension agents’ who links farmers to the credit sources. The study result met our apriori expectation and is consistent with the findings of other related studies which have shown that a number of contacts with agricultural extension officers enhance smallholder farmers to acquire better agriculture technique/practice which require additional capital that might be obtained through credit (Beck, 2007; Sanusi and Adedeji, 2010; Muhongayirea et al., 2013; Chauke et al., 2013; Abraham, 2014; Tetteh et al., 2015; Lemessa and Gemechu, 2016). From the finding the study concludes that the frequent contact between smallholder farmers and agricultural extension officer’s influences farm household’s decision to demand agricultural credit from MFIs.

Membership of social group

The study findings revealed that membership to social groups was positively related to the probability smallholder farmer’s access to agricultural credit that is, it was found to have a positive marginal effect on credit accessibility. It was found to be statistically significant at 10% level of significance. The smallholder farmers were categorized into two groups, those who belongs to socio-economic groups were assigned the value 1 and those who do not have social group was assigned the value zero (0). The odd ratio for membership of social group was 11.623 indicating that the farmer with a group membership their demand and access to agricultural credit is 11.623 times those who don’t have social groups. The study result met apriori expectations and is consistent with the findings of related studies which found that formation of economic and social associations helps smallholder farmers improve access to agricultural credit since there is a joint guarantee by association members (Zeller et al., 1998; Armendariz and Morduch, 2005; Kah et al., 2005; Lawal et al., 2009; Akudugu et al., 2009a; b; Akudugu, 2012; Mahmood et al., 2013; Gerald and Deogratius, 2013; Abraham, 2014; Lemessa and Gemechu, 2016). Therefore, the membership group increases smallholder farmers ability to demand and access agricultural credit from MFIs.

Location of the farm

The regional disparities were found to be positive and statistically significant at five percent level of significance with a positive marginal effect on credit accessibility. The study result implies that regional differences affects smallholder farmer’s decision to demand and access agricultural credit that is, farmers who live to the area that favours agricultural activities are more likely to have access to the microcredit and vice versa. The odd ratio for location of the farm is 3.252, indicating that smallholder farmers with favourable geographical location that is, good soil, availability of water, inputs such as improved seeds, pesticides etc. have the access to demand agricultural credit 3.3 times those with unfavourable geographical location of their farms. Basing on probability formula (Equation 3) in chapter three, farmers with favourable geographical farm location its probability for demanding agricultural credit is 0.7648 (76.48%). The study result is consistent with the findings of the various studies which found that the location of the farm greatly influences probability of access agricultural credit (Kochar, 1997; Tetteh et al., 2015). Hence, the study concludes that the location of the farm is the influencing factor/determinant in accessing agricultural credit as it has a positive marginal effect on credit accessibility.

Interest rate

The study findings revealed that smallholder farmer’s perception on interest rate charged by MFIs met apriori expectation of negative relationship to credit demand. Though was negative but was highly statistically significant at one percent level of significance. The negative effect of interest rate indicates that credit scheme with higher interest rate lowers the probability of smallholder farmers to access agricultural credit and vice versa. The interest rate was included in this estimation as dummy variable, smallholder farmers who perceived the interest rate to be high were assigned the value 1 and those who indicated low interest rate were assigned the value zero (0). The odd ratio for interest rate was 0.146 indicating that the farmers who perceive the interest rate to be high had an odd ratio which is 0.146 times those who considered the interest rate to be low. In other words, the smallholder who perceives interest rate to be low had an odd ratio is 6.85 times those who perceive interest rate to be high. This result is consistent with various related studies which found that smallholder farmers are reluctant to credit scheme with higher interest rate (Ibrahim and Aliero, 2012; Ololade and Olagunju, 2013; Assogba et al., 2017). Also, from the law of demand; the higher the price of loan charged (that is, high interest rate) the low the credit demand by smallholder farmers from credit scheme. Therefore, the study concludes that smallholder farmers who perceived the interest rate charged by MFIs to be high are less likely to demand agricultural credit from them.

CONCLUSION AND RECOMMENDATIONS

The study examined the determinants of credit demand by smallholder farmers in Tanzania. The study focused on demand side and used Delegated Monitoring Theory together with Rational Choice Theory; these theories provided a general framework for demand for financial services that is, demand dimension of access. Basing on the findings the study found that age of the respondents, gender, education level, household size, farmers distance from lending institutions, awareness of lending institution, collaterals, interest rate, type of crops, farm size, number of contact with extension officers in a year, membership of economic group and location of farm were playing a great role in determining credit demand by smallholder farmers. The study recommends that MFIs should be strengthened and to ensure that smallholder farmers get access to agricultural credit with minimum and bearable formalities for agricultural development in Tanzania.

The Government’s Agriculture Sector Programme II (ASDP II), the program aims at transforming the agricultural sector (crops, livestock and fisheries) towards higher productivity, commercialization level and smallholder farmer income for improved livelihood, food and nutrition security and contribution to the GDP. The program strategy is to transform gradually subsistence smallholders into sustainable commercial farmers by enhancing and activating sector drivers and supporting smallholder farmers to increase productivity of target commodities within sustainable production systems and forge sustainable market linkages for competitive surplus commercialization and value chain development.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abraham E (2014). Factors Influencing SEDA Agricultural Credit Rationing to Smallholder Farmers in Dodoma Municipality and Bahi District, Dodoma: Tanzania 1-110. Available at http://www.suaire.sua.ac.tz/xmlui/handle Accessed on 23rd September, 2019. |

|

|

Adesua L, Adebimpe P (2011). Assessing Nigerian Female Entrepreneur's Access to Finance for Business start-up and Growth, Nigeria: African Journal of Business Management 5(13):5348-5355. |

|

|

Adugna T, Heidhues F (2000). Determinants of Farm Households Access to Informal Credit in Lume District, Central Ethiopia: Savings and Development 24(4):27-46. |

|

|

Akpan SB, Patrick IV, Udoka SJ, Offiong EA, Okon UE (2013). Determinants of Credit Access and Demand among Poultry Farmers in AkwaIbom State, Nigeria: American Journal of Experimental Agriculture 3(2):293-307. |

|

|

Akram Z, Ajmal S, Munir M (2008). Estimation of Correlation Coefficient among some yield Parameters of Wheat under Rainfed Conditions. Pakistan Journal of Botany 40(4):1777-1781. |

|

|

Akudugu MA (2012). Estimation of the Determinants of Credit Demand by Farmers and Supply by Rural Banks in Ghana's Upper East Region, Ghana: Asian Journal of Agriculture and Rural Development 2(2):189-200. |

|

|

Akudugu MA, Egyir IS, Mensah-Bonsu A (2009a). Women Farmer's Access to Credit from Rural Banks in Ghana. Agricultural Finance Review 69(3):284-299. |

|

|

Akudugu MA, Egyir IS, Mensah-Bonsu A (2009b). Access to Rural Bank in Ghana: The Case of Women Farmers in the Upper East Region, Ghana. Ghana Journal of Development Studies 6(2):142-167. |

|

|

Armendariz BA, Morduch J (2005). The Economics of Microfinance. Massachusetts Institute of Technology Press pp. 25-30. |

|

|

Assogba PN, HarollKokoye SE, Yegbemey RN, Djenontin JA, Tassou Z, Pardoe J, Yabi JA (2017). Determinants of Credit Access by Smallholder Farmers in North-East Benin. Journal of Development and Agricultural Economics 9(8):210-216. |

|

|

Awunyo-Vitor D, Al-Hassan RM (2014a). Credit constraints and smallholder maize production in Ghana. International Journal Agricultural Resources, Governance and Ecology 10(3):239-256. |

|

|

Ayamga M, Sarpong DB, Asuming-Brempong S (2006). Factors Influencing the Decision to Participate in Microcredit Programmes: An Illustration for Northern Ghana. Ghana Journal of Development Studies 3(2):57-65. |

|

|

Baiyegunhia LJS, Fraser GCG (2014). Smallholder Farmer's Access to Credit in the Amathole District Municipality, Eastern Cape Province, South Africa. Journal of Agriculture and Rural Development in the Tropics and Subtropics 115(2):79-89. |

|

|

Bakhshoodeh M, Karami A (2008). Determinants of Poor Accessibility to Microcredits in Rural Iran. International Conference on Applied Economics (ICOAE), 5. |

|

|

Barnett V (1991). Sample Survey: Principles and Methods, London: Edward Arnold. |

|

|

Bashir MK, Yasir M, Sarfraz H (2010). Impact of Agricultural Credit on the Productivity of Wheat Crops. Pakistan Journal of Agricultural Science 47(4):405-409. |

|

|

Beck T (2007). Financing constraints of SMEs in developing countries: Evidence, determinants and solutions. Journal of International Money and Finance 31(2):401-441. |

|

|

Becker GS (1976). The Economic Approach to Human Behaviour: The Economic Approach to Human Behaviour. The University of Chicago Press pp. 3-14. |

|

|

Benerjee A (2001). Contracting Constraints, Credit Markets and Economic Development. Massachusetts Institute of Technology, Department of Economics pp. 2-17. |

|

|

Binswanger HP, Khandker SR (1995). The Impact of formal finance on the rural economy, India. Journal of Development Studies 32(2):234-262. |

|

|

Blanchflower DG, Levine PB, Zimmerman DJ (2003). Discrimination in the Small Business Credit Market. Review of Economics and Statistics 85:930-943. |

|

|

BOT (2011). Tanzania Mainland's 50 Years of Independence: The Role and Functions of the Bank of Tanzania, Dar es Salaam. |

|

|

Chauke PK, Motlhatlhana ML, Pfumayaramba TK, Anim FDK (2013). Factors influencing access to credit: A case study of smallholder farmers in the Capricorn district, South Africa. African Journal of Agricultural Research 8(7):582-585. |

|

|

Chitungo SK,Munongo S (2013). Determinants of Farmer's Decision to Access Credit, Zimbabwe. Russian Journal of Agricultural and Socio-Economic Sciences 5(17):7-12. |

|

|

Crook J (2001). The Demand for Household Debt in the USA: Evidence from 1995 Survey of Consumer Finance. Applied Financial Economics 11:83-91. |

|

|

Dercon S (1996). Wealth, Risk and Activity Choices: Cattle in Western Tanzania, CSAE Working Paper Series 1996-08 Centre for the Study of African Economies: University of Oxford. |

|

|

Diagne A, Zeller M (2001). Access to Credit and Its Impact on Welfare. Malawi: Research Report No. 116, International Food Policy Research Institute P 153. |

|

|

Dzadze P, Aidoo R, Mensah JO (2012). Factors determining access to formal credit in Ghana: A case study of smallholder farmers in the Abura-AsebuKwamankese district of central region. Journal of Development Agricultural Economics 4(14):416-423 |

|

|

Ellis F (2000). The Determinants of Rural Livelihood Diversification in Developing Countries. Journal of Agricultural Economics 51:289-302. |

|

|

Ennew C, Bink M (1997). Relationships between UK Banks and their Small Business Customers. Journal of Small Business Economics 9:167-178. |

|

|

Eswaran M, Kotwal A (1990). Implications of Credit Constraints for Risk Behaviour in Less Developed Economies: Oxford Economic Papers. |

|

|

Etonihu KI, Rahman SA, Usman S (2013). Determinants of Access to Agricultural Credit among Crop Farmers in a Farming Community of Nasarawa State, Nigeria. Journal of Development and Agricultural Economics 5(5):192-196. |

|

|

Fakayode SB, Rahji MAY (2009). A Multinomial Logit Analysis of Agricultural Credit Rationing by Commercial Banks in Nigeria. International Research Journal of Finance and Economics 4:90-100. |

|

|

Feder G, Just RE, Zilberman D (1985). Adoption of Agricultural Innovations in Developing Countries. A survey. Economic Development and Cultural Change 33(2):255-298. |

|

|

Feijo RLC (2001). The Impact of a Family Farming Credit Program on the Rural Economy of Brazil. University of Sao Paulo, Ribeirao Preto, BR, pp. 1-21. |

|

|

Filli FB, Onu JI, Adebayo EF,Tizhe I (2015). Factors Influencing Credits Access among Small Scale Fish Farmers in Adamawa State, Nigeria. Journal of Agricultural Economics, Environment and Social Sciences 1(1):46-55. |

|

|

Gerald A, Deogratius A (2013). Credit rationing and loan repayment performance: the case study of Victoria savings and credit cooperative society. Journal of Management and Business Studies 2(6):328-341. |

|

|

Ghosh P, Mookherjee D, Ray D (1999). Credit Rationing in Developing Countries:An Overview of the Theory, A Reader in Development Economics, London: Blackwell. |

|

|

Girabi F, Mwakaje AELG (2013). Impact of Microfinance on Smallholder Farm Productivity in Tanzania. Asian Economic and Financial Review 3(2):227-242. |

|

|

Gujarati DN (2003). Basic Econometrics. Fourth Edition, New York. U.S.A: McGraw-Hill Inc. |

|

|

Hananu B, Abdul-Hanan A, Zakaria H (2015). Factors influencing agricultural credit demand in Northern Ghana. African Journal of Agricultural Research 10(7):645-652. |

|

|

Hashi I, Toçi VZ (2010). Financing Constraints, Credit Rationing and Financing Obstacles: Evidence from firm-level data in South-Eastern Europe. Economic and Business Review 12(1):29-60. |

|

|

Henri-Ukoha A (2011). Determinants of Loan Acquisition from the Financial Institutions by Small-Scale Farmers in Ohafia Agricultural zone of Abia State, South East Nigeria. Journal of Development and Agricultural Economics 3(2):69-74. |

|

|

Hosmer DW, Lemeshow S (2000). Applied Logistic Regression: Second Edition, New York: A Wiley-Inter-science Publication. |

|

|

Hussein H (2007). Farm Household Economic Behaviour in Imperfect Financial Markets. Journal of Development Economies 56:265-280. |

|

|

Ibrahim AH, Bauer S (2013). Access to Microcredit and its Impact on Farm Profit among Rural Farmers in Dry land of Sudan. Global Advances Research Journal of Agricultural Science 2(3):88-102. |

|

|

Ibrahim SS, Aliero HM (2012). An Analysis of Farmers Access to Formal Credit in the Rural Areas of Nigeria. African Journal of Agricultural Research 7(47):6249-6253. |

|

|

Jappelli T, Pagano M (2002). Information Sharing, Lending and Defaults: Cross-Country Evidence. Journal of Banking and Finance 26(10):17-45. |

|

|

Jogo W, Karamura E, Tinzaara W, Kubiriba J, Rietveld A (2013). Determinants of Farm-Level Adoption of Cultural Practices for Banana Xanthomonas Wilt Control, Uganda. Journal of Agricultural Science 5(7):70-81. |

|

|

Kah JML, Dana L, Kah MMO (2005). Microcredit, Social Capital and Politics. Journal of Microfinance 7(1):121-151. |

|

|

Kariyasa K, Dewi YA (2013). Analysis of factors affecting adoption of integrated crop management farmer field school (ICM-FFS) in swampy areas, Indonesia. International Journal of Food and Agricultural Economics 1(2):29-38. |

|

|

Kochar A (1997). An Empirical Investigation of Rationing Constraints in Rural Credit Markets in India. Journal of Development Economics 53:339-371. |

|

|

Langyintuo A, Mulugetta M (2008). Assessing the Influence of Neighborhood Effects on the Adoption of Improved Agricultural Technologies in Developing Agriculture, Mozambique. African Journal of Agricultural and Resource Economics 2(2):151-169. |

|

|

Lawal JO, Omonona BT, Ajani OIY, Oni AO (2009). Effects of Social Capital on Credit Access among Cocoa Farming Households in Osun State, Nigeria. Nigeria Agricultural Journal 4(4):184-191. |

|

|

Lemessa A, Gemechu A (2016). Analysis of Factors Affecting Smallholder Farmer's Access to Formal Credit in Jibat District, West Shoa Zone Ethiopia. International Journal of African and Asian Studies pp. 43-53. |

|

|

Lukytawati A (2009). Factors Influencing Participation and Credit Constraints of Financial Self-help Group in Remote Rural Areas, West Java. Journal of Applied Sciences 9(11):2067-2077. |

|

|

Mahmood AN, Khalid M, Kouser S (2013). The Role of Agricultural Credit in the Growth of Livestock Sector, Faisalabad. Pakistan Veterinary Journal 29(2):81-84. |

|

|

Malik SJ, Nazli H (1999). Poverty and Rural Credit: Evidence from Pakistan. The Pakistan Development Review 38(4):699-716. |

|

|

Masuku MB, Raufu M, Malinga NG (2015). The Impact of Credit on Technical Efficiency among Vegetable Farmers, Swaziland. Sustainable Agriculture Research 4(1):114. |

|

|

Matheswaram S, Amita D (2001). Empowering rural women through self-help groups: Lesson from Maharashtra rural credit project, India. Journal of Agricultural Economics 54:20-44. |

|

|

Mignouna B, Manyong M, Rusike J, Mutabazi S, Senkondo M (2011). Determinants of Adopting Imazapyr-Resistant Maize Technology and its Impact on Household Income in Western Kenya. AgBioForum Journal 14(3):158-163. |

|

|

Mohammed S, Egyir IS,Amegashie DPK (2013). Social Capital and Access to Credit by Farmer Based Organizations in the Karaga District of Northern Ghana. Journal of Economics and Sustainable Development 4(16):146-155. |

|

|

Muhongayirea W, Hitayezu P, Mbatia OL, Mukoya-Wangia SM (2013). Determinants of Farmers Participation in Formal Credit Markets in Rural Rwanda. Journal of Agriculture Science 4(2):87-94. |

|

|

Mwangi M, Kariuki S (2015). Factors Determining Adoption of New Agricultural Technology by Smallholder Farmers in Developing Countries. Journal of Economics and Sustainable Development 6(5):208-216. |

|

|

Nwaru JC, Essien UA, Onuoha RE (2011). Determinants of Informal Credit Demand and Supply among Food Crop Farmers in AkwaIbom State, Nigeria. Journal of Rural and Community Development 6(1):129-139. |

|

|

Nyangena W (2007). Social determinants of soil and water conservation in rural Kenya. Environment, Development and Sustainability 10(6):745-767. |

|

|

Oboh VU, Ekpebu ID (2011). Determinants of Formal Agricultural Credit Allocation to the Farm Sector by arable Farmers in Benue State, Nigeria. African Journal of Agricultural Research 6(1):181-185. |

|

|

Okurut FN, Schoombee A, Van der Berg S (2005). Credit Demand and Credit Rationing in the Informal Financial Sector. South Africa Journal of Economics 73(3):482-497. |

|

|

Ololade RA, Olagunju FI (2013). Determinants of Access to Credit among Rural Farmers in Oyo State, Nigeria. Global Journal of Science Frontier Research 13(2):17-22. |

|

|

Reyes A, Lensink R (2011). The Credit Constraints of Market-Oriented Farmers, Chile. Journal of Development Studies 1851-1868. |

|

|

Sanusi W, and Adedeji I (2010). A Probit Analysis of Accessibility of Small-Scale Farmers to Formal Source of Credit in Ogbomoso Zone, Oyo State, Nigeria. Agric. Subtrop 43(1):49-53. |

|

|

Simtowe F, Zeller M, Diagne A (2009). The Impact of Credit Constraints on the Adoption of Hybrid Maize, Malawi. Review of Agricultural and Environmental Studies 5-22. |

|

|

Tetteh AB, Sipiläinen TAI, Bäckman ST, Kola JTS (2015). Factors Influencing Smallholder Farmer's Access to Agricultural Microcredit in Northern Ghana. African Journal of Agricultural Research 10(24):2460-2469. |

|

|

Uaiene RN, Arndt C, Masters WA (2009). Determinants of Agricultural Technology Adoption, Mozambique. Agricultural and Food Economics pp. 67-68. |

|

|

URT (1997). Morogoro Region Socio-economic Profile, the Planning Commission Dar es Salaam and Regional Commissioner's Office Morogoro. |

|

|

URT (2012). Population and Housing Census: Population Distribution by Administrative Areas. |

|

|

Waluse M (2020). Smallholder Farmers Database, Office Report: face-to-face interviewed by the author, Morogoro 4 February, 2020. |

|

|

Zeller M, Diagne A, Mataya C (1998). Market Access by Smallholder Farmers in Malawi. Agricultural Economics 19(1-2):219-229. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0