Full Length Research Paper

ABSTRACT

The purpose of this assessment was to identify, analyse and document major policies, laws, regulations, administrative practices, governance and institutional setups that constrained private seed sector investment in Ethiopia and identify evidence based alternative solutions to improve the supply of certified seed to small holder farmers and livelihoods in the country. The study was conducted in 2017 in Oromia, Amhara, SNNPR and Tigray regions. Both primary and secondary data that comprise quantitative and qualitative data sets were used. Primary data collected using on 21 domestic and international private seed companies, 22 Key informant interviews, and 12 focus group discussions were conducted at various levels. The results of the analysis showed that there are problems connected with policy environment, institutional and administrative bottlenecks. Based on the result of the survey, 89.5 and 82.7% of the respondents replied there is inadequate marketing system and inefficient market access, respectively; 84.2% said availability of poor quality of early generation seed (EGS), and 68.4% limited availability of EGS; 71.4% respondents replied there is inadequate government support in terms of finance, and capacity development; 61.9% inadequate access to fertile land and suitable irrigable land. Hence, to improve the private seed sector investment in Ethiopia there is a need to develop a clear policy and directives across the seed value chain. In general, for the private sector to develop in the country there is a need to foster a stepwise reduction of government intervention in private seed production to ensure a level playing field between the public and private sector producers to attract more private companies to the seed sector and expand farmer choice.

Key words: Seed systems, seed policy, early generation seed (EGS) multiplication, seed production, public and private sectors.

INTRODUCTION

Ethiopian agriculture contributes 36% to the GDP, 75% export and 80% employment (World Bank, 2017). Since the 1990s, the Ethiopian government has formulated and implemented the policy framework, known as agricultural development led industrialization (ADLI), with agriculture as a primary stimulus to increase agricultural output, employment, and income of the people. According to ADLI, the agricultural sector should turn Ethiopia into an industrialized economy (MoFED 2013).

The target for improved seed supply is to meet 35 million tons of certified seed that needs to increase from current production levels by about 18 million tons. Therefore, the primary deliverables to resolve seed system bottlenecks in growth and transformation plan (GTP-II) are to attract investment and develop a vibrant and competitive seed sector and strengthen regulatory capacity, structural and legal frameworks to meet international standards. Improved seed is one of the most important inputs for improving crop production and productivity. Its contribution is high when it is available in demanded quality and quantity at the right time and for the right price (Louwaars and De Boef, 2012).

Over 90% of the crops in developing countries are still planted with farmers’ varieties and farm-saved seed (Almekinders et al., 1994; Almekinders and Louwaars, 1999; Maredia et al., 1999; World Bank, 1998). Farmers often cultivate several varieties of the same crop spreading across various plots. Furthermore, farmers may sub-optimally use improved varieties because they may not always use genetically pure seeds of improved varieties (Dawit and Zewdie, 2015). As a result, large international seed companies concentrate on those countries with large commercial seed sectors, often focusing on high-value crops grown by larger farmers in more favorable areas, that is, targeting those who are best able to pay for their seed.

In the past few years, several significant milestones have been achieved towards building a dynamic, efficient and well-regulated seed system in Ethiopia. A new seed sector development strategy has formulated by MoALR where systemic bottlenecks have been identified and key interventions have been formulated. Among these availability and quality of early generation seed (EGS) has been identified as one of the major constraints of the national seed sector (Abebe et al., 2016). The modest growth of the private sector in seed production is contributing towards the sustainability of the seed industry and in reducing the burden on the public. The development of new improved varieties and technologies by federal and regional research institutions continues to equip farmers with tools that improve productivity and livelihoods (Fikre, 2017).

In Ethiopia, the role of different actors in the seed sector has been clearly undefined. There was an attempt to develop a national seed industry policy for Ethiopia in the early 1990s. However, from the time the national seed industry policy was drafted in 1992, it is not known as to what extent the private sector companies are involved in seed production and marketing and how they are faring. Still, the public sector plays the greatest role in the system including regulating access to genetic resources, variety development, variety release and registration seed production, seed distribution and marketing. It is also responsible to monitor and regulate seed certification, variety protection and phytosanitary/seed quarantine control. The private sector’s engagement in the seed sector is limited only to producing certified cleaning and delivering of Hybrid Maize seed to end users. Some are also engaged in producing basic seeds for their seed multiplication. However, the modest growth of the private sector in seed production is contributing towards the sustainability of the seed industry and in reducing the burden of the public sector. Even though, there is a policy directive encouraging the participation of private sector actors, informal price controls are set by the Government in specific areas, like the production and marketing of hybrid maize. To this effect, there is therefore a need to conduct review that focuses on assessing the performance of the private sector and challenges facing in the national seed systems as this will help determine if the seed policy has achieved its intended purposes of facilitating different activities in the seed systems. Therefore, the objectives of this study was to identify, analyze and document major policies, laws, regulations, administrative practices, governance and institutional setups that constrained private seed sector investment in Ethiopia and identify evidence based alternatives solutions to improve the supply of certified seed to small holder farmers.

MATERIALS AND METHODS

In line with the overarching objective of the study both primary and secondary data that comprise quantitative and qualitative data sets were used. A total of four methods were used such as document review, private seed sector survey, key informant interview, focus group discussion at federal, Oromia, Amhara, SNNPR and Tigray Regions. Data source targets were selected a broad range of stakeholders who were involved in the value chain of formal seed system. Hence, the outcome of this assessment would use for Government and its partners to improve the enabling environment to accelerate the development of the private seed sector in Ethiopian situations. The primary survey was conducted on 21 private seed companies (domestic and international) who are member of Ethiopian Seed Association located at Federal, Amhara, Oromia, SNNPR and Tigray Regions. Then, the data obtained through structured questionnaire were edited, coded and entered into SPSS (version 23) for analysis. Descriptive statistics such as percentage, frequency, mean and cross-tabulations were used to analyse the data.

A total of 22 Key Informant Interviews were conducted at various levels. The informants were purposively selected from the offices of Ministry of Agriculture and natural Resources (MoANR), Ethiopian Institute of Agricultural Research (EIAR), Ethiopian Seed Enterprise (ESE), Regional Public Seed Enterprises (RPSEs), Ethiopian Agricultural Investment Agency (EAIA), Ethiopian Agricultural Transformation Agency (ATA), ISSD Ethiopia, ICARDA, CIMMYT, FAO Ethiopia office, and public sectors in federal, Amhara, Oromia and SNNPR regional states. In addition, a total of twelve focus group discussions were done with 8-10 improved seed users’ farmers for each session, and included their voice concerning problems and challenges they faced in the formal seed system at Amhara, Oromia and SNNPR.

RESULTS

Company profiles

In Ethiopia, there are more than 45 public and private seed companies that are formally registered and producing different types of crops. Out of them 26 private and public seed companies are the members of ESA. Out of the total registered companies twenty one (80.8%) were identified for sampling. Out of these 33.3% of them were located in Amhara, 28.6% in Oromia, 14.3% each in Addis Ababa and SNNPR, while 9.5% of them were in Tigray regions. More than 75% of the companies are located in Amhara, Oromia, and SNNPR regions indicating these areas are suitable and potential for agricultural production. From the surveyed seed companies, some local private companies have modern pre- and post-harvest machineries, but some of them are unable to use them because of insufficiently available roads and electric power. The surveyed private seed companies used different machineries and facilities for running seed production, processing, storing and transporting purposes. Most of the respondent (76%) owned tractors to cultivate their land, 70% owned farm implements, 20% had combiners, 70% had threshers, 50% had cleaning machines, 45% had packaging facilities, 25% had labelling machines, 74% had storages to store their products, and 45% owned trucks to transport seed. It is well known fact that the seed industry requires huge capital investments, especially in infrastructure development and machinery purchase. Therefore, those who didn’t have the required machineries and/or facilities would rent from other public/private service providers. Farm machineries for seed production and processing machines are equally expensive. Thus, to full fill those machineries and infrastructure the government has to consider tax free and set up credit mechanism for private seed companies. The total number of permanent and contract employees hired by the twenty one private seed companies were 4,116 and 2,163 per month respectively, and this would contribute for an employment opportunity in the local areas. This indicates that the growth of private sector in the country creates an opportunity to knowledge and technology transfer.

Some local private companies have modern pre- and post-harvest machineries, but they are unable to use them because of insufficiently available roads and electric power. The surveyed private seed companies used different machineries and facilities for running seed production, processing, storing and transporting purposes. Most of the respondent (76%) owned tractors to cultivate their land, 70% owned farm implements, 20% had combiners, 70% had threshers, 50% had cleaning machines, 45% had packaging facilities, 25% had labelling machines, 74% had storages to store their products, and 45% owned trucks to transport seed.

Policy environment in promoting private sector participation

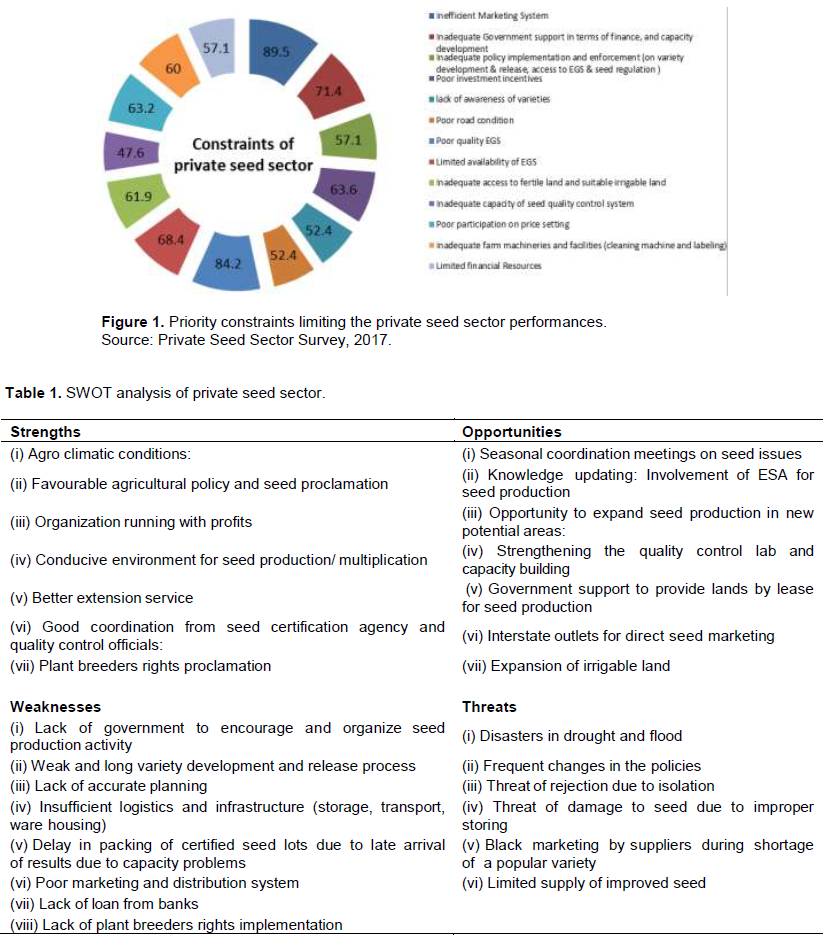

According to the data collected from the 21 private seed companies interviewed, 47.6% of the respondent replied the investment policy was encouraging the private seed growers; whereas 52.4% of the respondents replied the investment policy was not encouraging the private seed growers. The main reasons according to respondents for discoursing private sector were lack of investment incentives (63.6%), no investment guarantees (36.4%), inadequate market access (72.70 %), and no tax exemption (18.2%).

In addition, 71.4% of the respondents replied the support of the government to the private sector is inadequate, 52.4% said inadequate access to public owned varieties of EGS, 57.1% believed there is a problem in policy implementation and enforcement at all level, 47.6% thought there is a challenge in varieties development and release system, 47.6% of the respondents replied that there is limitation in seed production and marketing, 33.3% of the respondents replied that there are inadequate access to germplasm and lack of seed import and export opportunities, 28.6% replied that there is seed regulation but it lacks proper implementation. Therefore, based on the information above, more than half of the respondents were challenged by inadequate support from the government side, followed by poor implementation and enforcement of the policy at all levels and inadequacy access to EGS. This is confirmed by key informants responding that in the country there is no clear policy direction on the role of private sector in seed industry development and investment.

In the study, it was also found that in collaboration with NARS some private seed companies have registered their own varieties. This was evident from the emerging seed companies that were relying on public developed varieties and those that have started their own variety development programs in collaboration with public research institutions. The notable constraints to this were i) the long bureaucratic process involved and the existing legal arrangement among private companies, MoANR and the public research institutions ii) the domestic private sector is under-capacity of the seed companies with regard to human, facility and capital resources. Furthermore, support in terms of variety purity maintenance should be offered to the private seed companies. For instance, in seed multiplication, private companies are accessing EGS from public research institutes that they give it to the seed out-growers for further seed multiplication. In addition, the findings also showed that none of the private companies received support in research and crop improvement and there is no clear guideline on how to establish private breeding institutions in the country.

Institutional and administrative bottlenecks that hinder the development of private sector

The study revealed that there are institutional and administrative bottlenecks that hinder the participation of private sector in the national seed system. These are inadequate supply of disease resistant varieties, lack of infrastructure and modern equipment, limited financial resources, inadequate implementation of policies starting from the grass root (Wereda) administrative up to the apex ministry level, and inadequate partnership and networking among stakeholders. Results showed that 57.1% respondents said that they have limited financial resources, 52.4% of each equally said there is lack of awareness of varieties, lack of modern equipment and poor road infrastructure facilities, 38.1% replied there is lack of disease resistance varieties, 38.1% of the respondent believed there is inadequate partnership and networking with stakeholders, 33.3% said insufficient support from Wereda level. Therefore, as per the collected data more than half of the respondents major institutional and administrative bottle necks are limited financial resources, lack of awareness of varieties, poor road infrastructures and lack of modern equipment, implying for a strong institutional and administrative support.

Constraints related to seed production and quality control

Various constraints in the current seed system prevent private seed companies from increasing seed production and making it available to smallholders. The major constraints for the private sector are the fact that none of them do their own breeding institution. Therefore, they are relying on public institutions for EGS. The private seed companies obtain EGS from the research institutes and they produce certified seeds from it. Production of certified seeds is done in various ways; firstly at the company’s own farm, secondly on private farms, and thirdly, on clustered farmers/farmer’s associations fields. Based on the regulations, all seed fields must be inspected and certified before distribution. However, the current seed certification activity is weak both in coverage and quality of the operation. The number of the seed quality inspectors and their facilities do not match with the vast area of certified seed grown each year. Though, the capacity of inspectors is weak the regional inspectors are trying to monitor and supervise the seed production activities on both the company’s own farms and on those of the contract farms.

Most private owned seed companies in the country lacks fertile and irrigate farm for their seed multiplication. The survey data showed that 29% of companies are multiplied seed on their own farm, 29% on out grower farms, and 43% grow both own and out grower farms. From this result one can understand that private seed companies had limited amount of land for their seed production. Based on the study, the seed companies are accessing early generation seed from different sources. 57.1% respondents replied they get from research centres, 38.1% from public seed enterprises, 23.8% from BoANR, 14.3% from their mother company and 4.8% from Higher Learning Institutions (HLI). From the above data, one can understand that the public seed sectors are the major EGS suppliers in the country.

The identified private sector challenges connected to seed production and quality control systems are indicated as follows; 84.2% of the respondents replied that they are facing with problems of poor quality early generation seed, 68.4% with inadequate availability of EGS, 61.9% with lack of fertile and quality land with irrigation facilities, 61.1% of the respondent had limited skill on seed production, 50% of the respondent replied that they are challenged with quality assurance system on the process of seed production, 47.6% said they are limited on few crops and varieties, and 31.6% of the respondents replied they have scarcity of packaging facility during processing. From the above information collected one can understand that almost more than half of the companies are constrained with limited availability, choice and quality of EGS and fertile land with irrigation facilities for their certified seed production.

In this study, there were different challenges that the companies faced during seed quality control and certification. The major challenges of private sector in quality control and certification were inadequate capacity of seed quality laboratory (47.6%), inspectors did not inspect and report on time (33.3%), inaccessibility of farm to road (14.3%) and poor communication between seed companies and quality control offices (14.3%). During focus group discussion the farmers also complain that poor seed quality and sometimes low germination are the major problems faced after purchase of seeds.

Challenges related to seed marketing and distribution

In Ethiopia, the international private seed companies have developed distribution network for the marketing of their products. Despite the generally very positive experience with the recent direct seed marketing pilots, the local seed enterprises relying on centralised public marketing system. Respondents were asked how the companies set their seed price, and replied that 47.6% set the price by assessing the market/ depend on the market condition, 38.1% depends on the production cost, 23.8% on public enterprise’s prices and 19% based on the last year price. According to the information gathered, price determination is carried out in their own way differently across private sectors. However, the private seed companies who are setting their seed price on public seed enterprises are not considered on the price setting forum. Therefore, in the future considering the participation of private companies would have a positive impact on seed marketing. From the study report, it was revealed that the major challenges of seed marketing and distribution were lack of an efficient marketing system (89.5%), lack of private participation in price setting (63.2%), absence of market competition (38.1%), absence of private agro dealers (28.6%), lack of price setting mechanism (42.9%), and limited resource capacity (47.6%).

Priority constraints for the development of private seed sector

Based on the overall assessment ranges of constraints limiting the private seed sector performance in the country the major problems were identified and prioritized as indicated in Figure 1. Strength, Weakness, Opportunities and Threats of private seed sector are presented in Table 1.

DISCUSSION

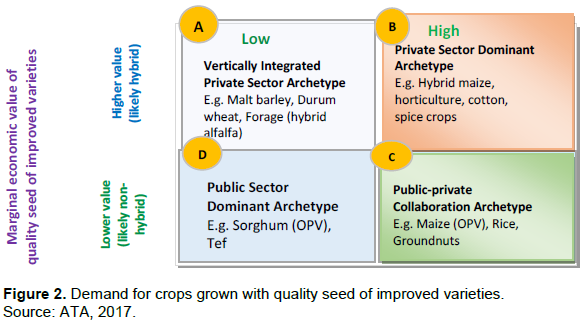

Ethiopia’s seed sector is typical of the ‘emergence stage’ of seed sector development (Zewdie and Abebe, 2016). Seed production and supply is primary public sector, limited scale, with minimal competition from private sector producers. According to the Agricultural Transformation Agenda (ATA) annual report, the current average annual national seed supply of improved varieties for most food crops covers less than 10% of the total agricultural land area compared to 25% in many other African nations. Of the 10% of land, 87% is covered by seed that comes from public producers, 8% from multinational companies and 5% from local private companies. Supply of improved seed from public seed enterprises meets about 60% of government targets while private seed production accounts for less than 15% of supply, compared to 40% in India and 20% in Tanzania (ATA annual report, 2015).

However, both the parastatal seed enterprises and local private sectors are not in a position to adequately meet country’s seed demand. Therefore, multinational companies can play an increasingly important role in helping smallholder farmers acquire improved varieties of seed. The focus of multinationals should be on introducing new varieties to Ethiopia that do not directly compete with existing varieties. Seed sectors typically develop into four main optimally market archetypes, by crop (ATA, 2015). In this regard, ccountries such as Bangladesh, India and Turkey with more developed seed sectors adopt distinct roles for public and private producers by crop group.

(i) Vertically Integrated firms are suited to produce high value, low demand seeds

(ii) Private Sector Dominant archetype is suited for high value, high demand seeds

(iii) Public-private Collaboration is suited for low value, high demand crops

(iv) Public Sector Dominant leads low value, low demand crops (Figure 2)

To improve the private seed sector investment in Ethiopia there is a need to develop a clear policy and directives on variety development and release. In many countries, public research takes the lead in areas such as pre-breeding, germplasm conservation, and crop and resource management. Experiences of other countries showed that they have simplified business registration, automatic and free variety registration.

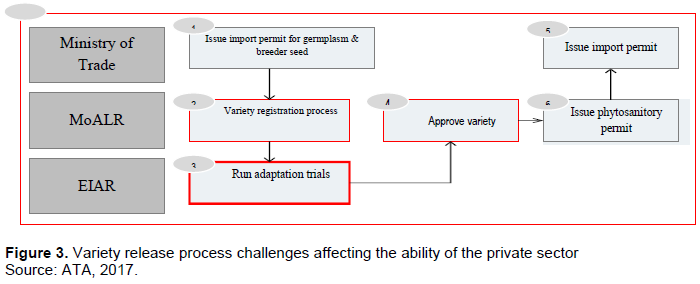

During the study, there are practice constraints the government of Ethiopia should consider addressing to encourage greater private sector participation. The country’s current variety release process has a number of challenges, which discourage private sector companies from entering the country: firstly, the process by which a company applies for and manages the release of a new variety is logistically complex, requiring interaction with a number of different offices, in various geographic locations (Figure 3). This complex process is in contrast to India’s process which is centrally managed by the Indian Council for Agricultural Research where companies simply have to interact with one office in one location to submit a variety for potential release. Therefore, the country should centralizing the variety release and other related administrative process (e.g., import permit application, phytosanitary permit application) into one nodal office; secondly, the pricing of variety testing is relatively high with a single test costing as much as $10,000-15,000 USD, which is much higher with compared to a cost of $200 USD in South Africa (ATA, 2015). This pricing gap should be improved and a clear and transparent pricing will be an important first step to reducing perceptions of bias; and finally, as the public sector is a key player in the seed industry, the objectivity of the variety release process and the variety release committee is in question. In the registration and adaptation trials may also be seed breeders, thus evaluating competitor product. Greater independence of the committee could reduce any perceived bias and needed streamlining the variety release process and increasing technical capacity throughout lower levels of government.

Plant breeders’ rights, are important to private-sector involvement in breeding open-pollinating/self-pollinating crops (Manap et al., 2007; World Bank, 2006; Gerpacio, 2003; Loch and Boyce, 2003; Lyon and Afikorah-Danquah, 1998; Jaffee and Srivastava, 1994; Tripp, 1993; Pray and Ramaswami, 1991). Indeed, multinational companies commonly require that IPRs be in place as a precondition of their investment in research and development activities. Many authors recommend implementing plant breeders’ rights consistent with UPOV 1978 or 1991 (e.g. World Bank, 1998; Louwaars, 2009). However, in Ethiopia even though the PBR law was recently approved by the parliament, it was not yet put for implementation. Therefore, weak guarantee of safe-guards on protected varieties to international companies. This hinders participation of multinational seed companies to enter in the country. An efficient system that produce and distribute enough amount of EGS to public and private seed companies is also essential. Those seed companies wanting to commercialize varieties must be able to readily access sufficient quantities of source seed for growing on. Inadequate production of EGS by public institutions has been shown to be a constraint to diffusion of new varieties in sub-Saharan Africa (Tripp, 2000, 2006). Moreover, it is essential to expand the private seed companies’ access to EGS through issuing and enforcing an open and transparent application process with the clear goal of distributing EGS to all entities that meet a set of standards. Seed companies can improve the production of EGS in the case of limited public capacity.

Seed quality is a major determinant of seed acquisition behaviour (Zewdie and van Gastel, 2008), but is difficult for farmers to determine until the seed has been planted and is growing in their field (Minot, 2008). There are strong arguments for a continuing role for governments in setting and monitoring seed quality standards (Lyon and Afikorah-Danquah, 1998; World Bank, 1998; Kugbei et al., 2001; Minot, 2008), but implementation can increasingly be shared with seed producers themselves (Tripp and Louwaars, 1997). In Ethiopia, most of the private producers are complaining that the quality of EGS offered for sale is inferior in terms of physical and physiological quality. The internal quality control system for EGS production should be strengthened in human and physical capacity and premium prices paid for contract growers to encourage production of high quality seed.

Seed supply in Ethiopia is erratic for a number of reasons, with the key ones being major reliance on rain-fed agriculture, lack of cold storage for keeping carryover certified seed, and erratic supply of high quality foundation seed. Therefore, there is a need to develop support mechanism in provision of fertile and irrigated land to seed producer companies, build cold seed storages in different agro-ecologies to enable seed marketing and carryover certified stocks for sale in subsequent season that could lower production risks and the contractual agreement should be revisited and legally binding.

The government seed regulatory mechanism have different constraints like institutional and human resources capacity limitations, hence they are not able to respond on time to the request of private and public seed producers. Rigid application of seed regulations can hamper the development of seed enterprises, as shown in Ethiopia (McGuire, 2005). Case studies on maize Brazil showed that certification of seed is valuable, ensuring that seed is of a specified variety and meets quality standards (Tripp, 2003), but excessively strict certification schemes can constrain development of the seed sector (Maredia et al., 1999; Kugbei and Zewdie Bishaw, 2002; Loch and Boyce, 2003; David, 2004; Minot, 2008; Smale et al., 2009). To improve the certification process allowing accreditation of private laboratories, private inspectors and university centres will have important role to lessen the burden on the public sector. The World Bank (1998) and Tripp (2006) also recommends voluntary seed certification based on government-set certification standards, with the public sector helping to develop the certification and seed testing capabilities of seed enterprises. The government should promote private sector through access to capital, credits and incentives, and support regional integration and harmonization to create larger markets. Support projects that directly work with private sector and strengthen their capacity. Governments may need to provide incentives to encourage development of seed marketing channels in less favourable areas (Tripp and Rohrbach, 2001). According to the study, availability of basic infrastructures in most of the local private sectors are lacking. This signals a direct need for sustained attention to critical infrastructure development and maintenance, and also an opportunity for public-private partnership in infrastructure investment.

The result of the study indicated that the emerging private sector companies in the country rarely have the experience or skills necessary to be able to ramp up and take over. These critical aspects could help to address: business planning, seed brand development, leadership and management skills, and technical and operational capacity etc. NARS breeders could work with emerging private seed companies to develop the most appropriate varieties for each agro-ecological need.

CONCLUSIONS

It was found that it was actually difficult for a private company to access germplasm, the seed varieties and EGS from public institutions. There is a need for policy support and legal arrangement and direction that all the private seed companies have access to public bred varieties. This will make the seed industry competitive where the private seed companies can be made to bid for the public bred varieties and pay royalties. In such a case the public institutions involved in variety development become self-sustaining. In the other way private companies can also develop own competitive varieties.

The analysis of the seed system reveals that institutions do not govern the seed market in an optimal manner. To incentivize domestic as well as foreign investments, well-designed and stepwise market liberalization is needed. Other countries experiences (India, Vietnam, Bangladesh, Kenya, etc.) also showed that seed market liberalization has enhanced supply and improved import export of seed. The direct seed marketing pilots in Ethiopia shows that the government has recognized the need for change and may slowly deregulate the market.

The policy should provide strategies to encourage the growth of the private seed sector in line with Government’s overall strategy to encourage the private sector to assume command of the commercial components of the seed industry. The key linkage areas of the private seed sector with the public seed sector should be in the areas of the whole seed value chain (from germplasm access to marketing) adequate representation of private companies in relevant seed sector. Here, the ESA can play an important role in catalysing the linkages between all actors.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abebe A, Dawit A, Zewdie B, Tekeste K, Karta K (2016). Early Generation Seed Production and Supply in Ethiopia: Status, Challenges and Opportunities. Ethiopian Journal of Agricultural Science 27(1):99-119. |

|

|

Almekinders CJM Louwaars NP (1999). Farmers' seed production. London: Intermediate Technology Publications Ltd. |

|

|

Almekinders, CJM, Louwaars NP, and de Bruijin GH (1994). Local seed systems and their importance for an improved seed supply in developing countries. Euphytica 78:207-216. |

|

|

Agricultural Transformation Agenda (ATA) (2015). Agricultural Transformation Agenda (ATA) annual report, 2015/16.page 52. |

|

|

Dawit Alemu and Zewdie Bishaw (2015). Commercial behaviours of smallholder farmers in wheat seed use and its implication for demand assessment in Ethiopia. Development in Practice 25(6):798-814. |

|

|

David S (2004). Farmer seed enterprises: a sustainable approach to seed delivery? Agriculture and Human Values 21:387-397. |

|

|

Fikre M (2017). Seed Policy International Best Practices Review for Developing a Comprehensive National Seed policy for Ethiopia. A draft background report submitted to ATA. July 15, 2017 (Unpublished draft). |

|

|

Gerpacio RV (2003). The roles of public sector versus private sector in R & D and technology generation: the case of maize in Asia. Agricultural Economics 29:319-330. |

|

|

Kugbei S, Zewdie B (2002). Policy measures for stimulating indigenous seed enterprises. Journal of New Seeds 4(1):47-63. |

|

|

Loch DS, Boyce KC (2003). Balancing public and private sector roles in an effective seed supply system. Field Crops Research 84(1-2):105-122. |

|

|

Louwaars N (2009). Seed systems and PGRFA. Background Study Paper for the State of the World's Plant Genetic Resources for Food and Agriculture. FAO, Rome, Italy. |

|

|

Louwaars NP, De Boef WS (2012). Integrated seed sector development in Africa: A conceptual framework for creating coherence between practices, programs, and policies. Journal of Crop Improvement 26:39-59. |

|

|

Manap NA, Zainol ZA, Hussein SH, Sidik NM, Shafiee R (2007). The Intellectual Property Rights for new plant varieties: a Malaysian perspective. Paper presented at the 2007 Annual Conference of the British and Irish Law, Education and Technology Association, Hertfordshire, 16-17 April 2007. |

|

|

Maredia M, Howard J, Boughton D, Naseen A, Wanzala M, Kajisa K (1999). Increasing seed system efficiency in Africa: Concepts, strategies and issues. MSU International Development Working Paper. Department of Agricultural Economics, Michigan State University, East Lansing, Michigan, USA. |

|

|

McGuire S (2005). Getting Genes: Rethinking seed system analysis and reform for sorghum in Ethiopia. PhD Thesis Wageningen Agricultural University. |

|

|

Minot N (2008). Promoting a strong seed sector in sub-Saharan Africa. IFPRI Policy Brief 6. International Food Policy Research Institute, Washington, DC, USA. |

|

|

Ministry of Finance and Economic Development (MoFED) (2013). Rural development policy and strategies. Ethiopia: Ministry of Finance and Economic Development (MoFED), Addis Ababa, Ethiopia. |

|

|

Pray CE, Ramaswami B (1991). A Framework for Seed Policy Analysis in Developing Countries. International Food Policy Research Institute, Washington, DC, USA. |

|

|

Smale M, Nagarajan L, Diakité, L, Audi P, Grum M, Jones R, Weltzien E (2009). Tapping the potential of village markets to supply seed in semi-arid Africa: A Case Study Comparison from Mali and Kenya. Paper presented at the conference Towards Priority Action for Market Development for African Farmers 13-15 May 2009, Nairobi, Kenya. |

|

|

Tripp R (1993). Invisible hands, indigenous knowledge and inevitable fads: Challenges to public sector research in Ghana. World Development 21(12):2003-2016. |

|

|

Tripp R (2000). Strategies for seed system development in sub- Saharan Africa. Working Paper Series No. 2. ICRISAT, Bulawayo, Zimbabwe. |

|

|

Tripp R (2003). How to cultivate a commercial seed sector. Paper presented at the symposium on 'Sustainable Agriculture for the Sahel', Bamako, Mali, 1-5 December 2003. |

|

|

Tripp R (2006). Strategies for seed system development in sub-Saharan Africa: A study of Kenya, Malawi, Zambia, and Zimbabwe. SAT eJournal 2(1) [online]. |

|

|

Tripp R, Louwaars N (1997). Seed regulation: choices on the road to reform. Food Policy 22(5):433-446. |

|

|

Tripp R, Rohrbach D (2001). Policies for African seed enterprise development. FoodPolicy 26(2):147-161. |

|

|

World Bank (1998). Initiatives for sustainable seed systems in Africa. In: FAO. Seed Policy and Programmes for Sub-Saharan Africa. Proceedings of the Regional Technical Meeting on Seed Policy and Programmes for Sub-Saharan Africa, Abijan, Côte d'Ivoire 23-27 November 1998. |

|

|

World Bank (2006). Intellectual property rights. Designing regimes to support plant breeding in developing countries. Agriculture and Rural Development Department, The World Bank, Washington DC, USA. |

|

|

World Bank (2017). Ethiopian Agriculture.The World Bank Annual Report 2017. Washington, DC: World Bank. © World Bank. |

|

|

Zewdie B, Abebe A (2016). Enhancing Agricultural Sector Development in Ethiopia: the Role of Research and Seed Sector. ISSN 0257-2605. Special Issue 2016 |

|

|

Zewdie B, van Gastel AJG (2008). ICARDA's seed-delivery approach in lass favorable areas through village-based seed enterprises: conceptual and organizational issues. Journal of New Seeds 9(1):68-88. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0