Full Length Research Paper

ABSTRACT

The sustainable management of tropical forests has been a great concern and challenge for the forest sector in the Brazilian Amazon. This study aimed to better understand sustainable forest management in the Brazilian Amazon focusing on two research questions: (a) Is sustainable tropical timber production financially viable? (b) What are the profit determinants under sustainable forest management? In this research, we assessed information of all approved forest management plans in 2011 in the Sinop region, located in the eastern Brazilian Amazon. Sequentially, we selected and tested using econometric tools these variables: Profit, managed area, volume of timber, number of managed species and timber price. Our results show that the average profit is of US$ 1,003.00 per hectare in sustainably managed forests and we observed that the variables volume of timber per hectare and timber price explain the profit of this forest activity presenting the best fit econometric results.

Key words: Economic analysis, forest management, timber production, tropical forest.

INTRODUCTION

Sustainable Forest Management (SFM) had become an important research topic in the 1990's since the definition of its principles in 1992 at the United Nations Conference on Environment and Development in Rio de Janeiro (Wang, 2007). Sustainable management is a broadly accepted terminology that defines forest management according to the principles of sustainable development and, more specifically, it involves balancing social, economic and environmental values related to forest resources and taking these values into consideration for future generations (Canova, 2012).

The SFM has been an alternative forest use to guarantee continuous long-term tropical timber production and those forest related environmental services. However, the SFM needs to be properly certified to assure to the consumers that forest products meet the environmental criteria. As a result, certification efforts have been fostered as a means of improving sustainability in tropical forest management (Agrawal, 2008).

Selective logging activities in the Amazon rainforest have been carried out in predatory ways. The adoption of practices for SFM is crucial and only a few logging companies are practicing sustainable logging in the Brazilian Amazon. Nevertheless, it is important to promote sustainable logging in the Amazon Basin to assure long-term supplies of environmental goods and services, including climate regulation, regional and global precipitation regulation, conservation of biodiversity and supply of timber and non-timber products (Banerjee et al., 2009).

Although SFM is economically viable, some authors argue its financial viability since there are many barriers to its large-scale application in the Amazon region. Examples of such barriers are: The incipient spread of management techniques among forest users; the higher profitability of agriculture in the short term if compared to forest management; and the lack of efficient control of non-sustainable logging, making it profitable in the short term (Canova, 2012). Overcoming those regional barriers would require implementation of appropriated forest policy that includes a public land occupation plan in the region, an efficient logging control, further economic incentives to forest management and technical assistance forest landowners (Barreto, 1998; Richards, 2000).

Finally, legal regulation itself has not been enough to improve the adoption of SFM. Due to the lack of financial support for SMF, uncertainties of the harvesting costs in sustainably managed forests by forest entrepreneurs, lack of information on management techniques and its economic impacts on forest sustainability. Therefore, a more detailed economic analysis is needed to assess costs and benefits of that type of forest management and to provide information to the development of the sustainably management of tropical forests (Barreto, 1998).

This study aimed to better understand the sustainable timber production in the Brazilian Amazon. More specifically, we assessed financial viability of certified selective logging and its profit determinants

MATERIALS AND METHODS

This research was conducted in the Sinop region, state of Mato Grosso, located in the southern Brazilian Amazon (Figure 1). This region is considered an important timber center in the Brazilian Amazon. The dataset was created by assessed information of all approved forest management plans in 2011 formally approved by the Mato Grosso Environmental State Agency for the highlighted municipalities in Figure 1. The study area included the municipalities of Sinop (a timber center), Claudia, Feliz Natal, Juara, Marcelândia, Nova Bandeirante, Peixoto de Azevedo, Santa Carmem, Tapurah, and União do Sul, located within the Amazon state of Mato Grosso.

The independent studied variables used in this analysis included selectively logged area, the number of harvested tree species, harvested timber volume (m3ha-1), total logging income, and total logging cost.

The data used in this study were acquired by interviewing the 26 owners of forest management plans during the 7th edition of “Promadeira” Meeting at the International Fair of Wood, Furniture, Machine and Equipment of the Forest-Based Sector. That international event lasted for one week during October 2011 in Sinop city, state of Mato Grosso, Brazil.

Economic analysis

The profit per hectare (Π) of timber extraction under sustainable forest management was estimated using Equation 1.

Πt = TRt - TCt (1)

Where: Πt = profit of sustainable timber extraction in dollar per hectare (US$/ha) in the period t; TRt = total revenue of timber production in dollar per hectare (US$/ha) in the period t; TCt = total cost of sustainable timber production in dollar per hectare (US$/ha) in the period t.

Equation 2 as function of forest management profit presented in a log-linear form as the following was used to estimate the profit determinants:

lnΠt = β0 + β1lnMAt + β 2lnNSt + β3lnTVt + β4lnTPt + ε (2)

Where MAt = the forest managed area (hectares) in the period t; NSt = the number of harvested tree species per hectare in the period t; TVt = the harvested timber volume (m3 per hectare) in the period t; TPt the average price of harvested timber in each forest management project in the period t (US$/m3), and ε = the stochastic error.

All variables used in this analysis were transformed (logarithm) as an empirical convenience. Subsequently, the Marshallian elasticities were directly estimated for the used variables in this analysis. Further details is given in previous study (Wooldridge, 2009).

The variable (MA) is the forest-managed area (hectares) in 2010. The variable (NS) is the number of harvested tree species. The variable (TV) is the total harvested timber volume (m3ha-1). The total harvested timber volume was limited to 30 m3ha-1 due to the Brazil´s environmental regulation (Brazil, 2006). The variable (TP) is the timber price estimated based on the gross income of timber production divided by the total harvested timber volume. Therefore, the variable TP is the average price of all harvested tree species (US$/m3).

The variable (MA) was intended to estimate effects of the scale production (forest managed area / total profits of the forest activity). Based on it, our first hypothesis is that the size of the managed forests is directly related to its profit. It is expected that the forest owners will harvest larger areas to increase their profits as the legal regulations limit the timber volume per unit area. The forest-managed area (MA) was used to estimate area of harvested forests in the study period.

The number of tree species (NS) estimates timber diversity. Commonly, loggers choose the most valuable tree species. The dominant tree species in the study area are: Cedrinho (Erisma uncinatum warmi), Cambará (Vochysia sp.), Itaúba (Mezilaurus itauba), Angelim-pedra (Dinizia excelsa Ducke), Peroba (Aspidosperma polyneuron). Other species that appear with a lower frequency are Peroba-cupiúba (Goupia glabra Aublet), Amescla (Trattinnickia burseraefolia), Garapeira (Apuleia leiocarpa) and Tauari (Couratari oblongifolia Ducke).

The harvested volume per hectare (TV) indicates forest productivity and financial profits by logging activities. That productivity, however, is currently limited to 30 m3ha-1 by the environmental regulation applied for the Brazilian Amazon. The forest management plans only are approved if they respect this limitation although even with the government surveillance a small group of timber producers sometimes harvester more than the limit or without authorization and then try to sell it in an illegal market but in this study we gone work only with the official data.

The timber price (TP) is directly related to the financial profit resulted of selective logging. In this case, a close relationship between timber price and profit supports the hypothesis that loggers tend to choose the most valuable tree species for logging.

Equation 1 was arranged by its variable order and rank conditions as suggested by Pindyck and Rubinfeld (1991). Additionally, its coefficients were estimated by the ordinary least squares method.

The econometric efficiency of the models was tested by applying the Snedecor's F statistic. This test intended to assess the dependent variable effects on the independent variables. The Student's t statistic was applied to assess the individual effects of the independent variables on the dependent variables; Durbin-Watson's d statistic was applied to verify the presence or not of autocorrelation in the stochastic terms.

Equation 2 was estimated by the ordinary least squares method (OLS). The OLS assumption is that the coefficients should be expressed as β1, β2, β3 and β4> 0 for one-tailed t test. Multicollinearity was assessed by estimating the indicator of Variance Inflation Factor (VIF). Heteroscedasticity was assessed by using Durbin-Watson's d test, the BPG test (heteroscedasticity), and the RESET test (specification) at a 0.10 significance level. Gujarati (2011) suggested the d test in case of indecision zones and the Geary test may be applied (1970).

RESULTS

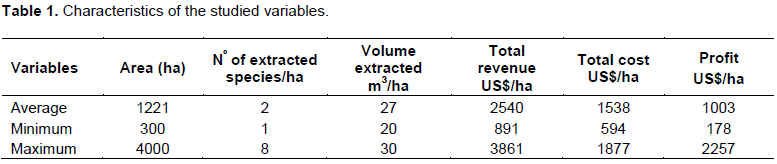

Table 1 shows further details of the studied variables. The harvested timber profit for sustainably managed forests varies from US$ 178.00 to 2,257.00 per hectare and an average of US$ 1,003.00 per hectare (estimated values in October 2010). Based on it, we observed that forest management for timber production is a profitable business and this large profit variation can be explained by the type of the species and the extract volume by hectare in the property because a property with a high valued species and a high volume extraction will be much more profitable than a property with low valued species and low volume extraction that is a natural fact and can occur.

Regarding the remaining studied variables (MA and NS), it is worth highlighting the extensive forest areas management demand which has an average value of 1,221.00 ha, and the low number of species extracted by hectare.

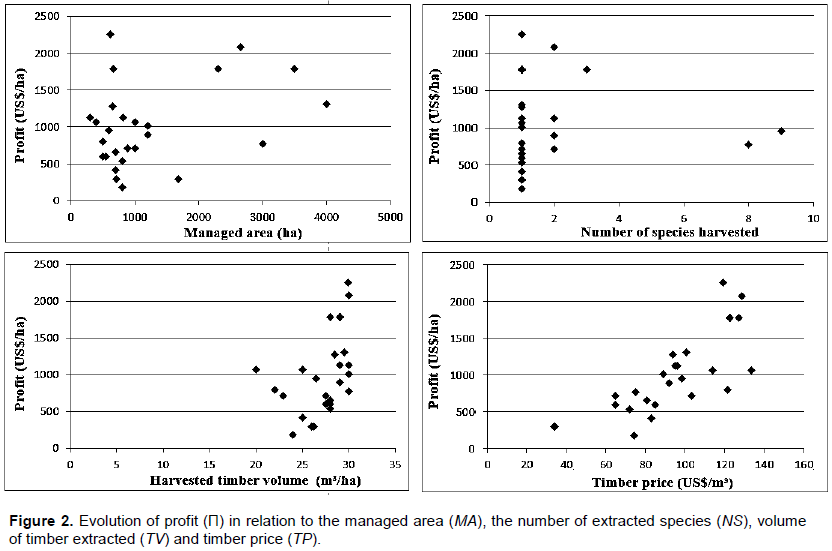

By comparing forest and soybean profits, it was observed that soybean profitability in 2011 varied from US$ 137.94 to 1,009.18 in the municipality of Sorriso, state of Mato Grosso (Lima, 2012). The profit responses of timber production from sustainably managed forests to the area managed, the number of tree species, and timber price are shown in Figure 2. Based on correlation analysis results, the timber profit of managed forests showed moderate relationship with the harvested volume (0.45), and strongly relationship with the timber price (0.78).

The multiple regression model is used to obtain the elasticities of the dependent variables and estimated the profits. The Table 2 shows the statistical results of the estimated linear relationship among the studies independent and dependent variables in this analysis. The result of this analysis showed that the multiple regression model can significantly explain 78% of the dependent variable (timber profit of sustainably managed forests) at α = 0.01 (probability of 99%). In the above specification, all variables present the signs expected according to the theory. More specifically, the harvested volume per hectare (VE) and timber price (P) were significantly different at α = 0.05. The managed forest area (AM) and number of tree species per hectare (NE) were not different at α = 0.05, which means that these two explanatory variables have no significant effects on timber profit. However, they are important explanatory variables for the comprehension of the profit function and for that reason they remained in the model. Finally, the results of Durbin-Watson d statistic test indicates (1.08) residual independence of the dataset at 95% probability level.

DISCUSSION

The timber profit of sustainably managed forests is highly dependent on the timber harvested volume per hectare (VE) and its effects were estimated as following: if the timber harvested volume increases by 10%, the timber profit will increase by 24%. The estimated elasticity was 2.4 for the timber harvested volume, which indicates an elastic response.

The hypothesis that Timber price (P) significantly and positively affects the timber profit of sustainably managed forests cannot be rejected, and its effects were estimated as following: If the timber price increases by 10%, the timber profit will increase by 13.9%. These results indicate that by increasing timber demand and prices, there will increase profits of forest owners or managers. By increasing tropical timber prices, it is expected that forest management will be even more profitable.

Another hypothesis assumed that by increasing number of tree species should directly increase timber profit. Contrarily, we observed a negative effect from number of tree species on timber profits, most likely due to the relatively small number of trees that are commercially valuables for selective logging in the Amazon region. One of the critical aspects of forest management in the Brazilian Amazon, which is the small market of commercial species. Therefore, by harvesting a larger number of tree species, there will increase the overall forest management costs and those additional harvested tree species would not be appropriately accepted and valued by the market and consumers.

Timber harvesting under SFM can be financially viable, even in the absence of payments for other services, in some tropical forests. These will include those where high-value tropical timber species are present in sufficient numbers to support a low-volume, high-value timber harvesting regime; a certification system will be necessary as a tool for maintaining access to high-value markets. They may also include forests with sufficient natural species’ homogeneity (the timber of which is sufficiently distinct to command a ‘loyal’ market niche), or where a high density of currently ‘lesser known’ species prove to be marketable enough, to allow the development of a strong value added sector (Leslie, 2002).

A complementary strategy is to implement SFM in areas where such high-value timbers are not found in sufficient quantities, or where forests are not sufficiently homogenous, supplemented by direct payments for other, global, goods and services. With such payments, SFM that includes timber production could well become financially viable in some regions (Leslie, 2002).

Fortini and Carter (2014) studied the viability of small-scale forest management activity in the estuary of the city of Magazão, located in the state of Amapá. The authors estimated a positive profit and an internal rate varying from 22 to 84% for the production types studied on their analysis.

By conducting an economic analysis of low-impact logging in the Abunã region, located in state of Rondônia, Sartori (2012) observed that a forest area of 560 ha, with an initial investment of approximately US$ 409,294.00, it is possible to reach a profit return between US$ 76,743.00 and 153,485.00 up to the third year of forest activities. By applying Monte Carlo Simulation, Sartori estimated an internal returning rate greater than 13.8% at 90% of probability.

In the Brazilian Amazon, according to the Forest Code, until 2012, 50 to 80% of all landholdings had to be conserved as forest, where only sustainable management of timber and non-timber forest products is allowed. According to official data, at least 40 million hectares of forests are held by smallholders and communities and could potentially be managed through sustainable forest management (SFM). In some states, the existing demand for timber may only be met in the future with an expansion of CFM or small-scale SFM (Piketty, 2015).

The tools available for encouraging SFM begin with policy and regulations that support those who are practicing forest management. They also include inventories, monitoring, forest management certification, stakeholder involvement and forest management plans. Where there is a clear understanding of the ecological circumstances of the forests being managed an appropriate regulatory framework can establish the enabling conditions for SFM (Macdicken, 2015).

Finally, we understand that the harvested volume must be limited by the current Brazilian environmental law. Also, any change in harvesting timber volume per hectare must observed growth rates (volume) of each tree species. That would guarantee that forest production is actually economic, environmental, and social sustainable.

CONCLUSIONS

The estimated equation shows great potential to contribute and support sustainable forest management in the Amazon region, and also provides a rational use of tropical species and bases for the creation of policies to the forest management. Based on this research results, we observed the economic viability of the forest management activities in that region if forest plans are well prepared and properly carried out.

Sustainable forest management requires, however, competitive market prices of tropical timber worldwide. Moreover, the harvested timber volume per hectare substantially contributes to explain profit behavior in sustainable forest management.

We estimated that the elasticity of the harvested timber volume was around of 2.40, which indicates an elastic response. A similar result was observed for the timber price variable (~1.39). We argue that elasticity may decrease as legal restrictions are established and enforced in tropical timber commercialization. It is likely due to the small size of fraction of demand. The timber price components and harvested volume per hectare affected profit behavior in this analysis. As a result, we observed a profit positive feedback to the timber price and harvested volume.

Like in other countries, one of the main challenges in Brazil is to increase the competitiveness and attractiveness of SFM compared with other land uses. Understanding monetary costs and benefits thus plays a central role in developing equitable benefit sharing arrangements and assessing whether the net gains from timber harvesting are sufficient to encourage a community’s long-term commitment to SFM for commercial purposes (Piketty, 2015).

Forest communities and small farmers in the Brazilian Amazon are important actors in the sustainable management of the forest, as they control nearly 60% of public forests in the Brazilian Amazon. Promoting sustainable forest management and incorporating it in agrarian production systems will play a key role in the fight against deforestation in the near future (Sist, 2014).

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Agrawal A, Chhatre A, Hardin R (2008). Changing governance of the world's forests. Science 320:1460-1462. |

|

|

Banerjee O, Macpherson AJ, Alavalapati J (2009). Toward a Policy of Sustainable Forest Management in Brazil A Historical Analysis. J. Environ. Dev. 18:130-153. |

|

|

Barreto P, Amaral P, Vidal E, Uhl C (1998). Costs and benefits of forest management for timber production in eastern Amazonia. For. Ecol. Manag. 108:9-26. |

|

|

Brazil (2006). Normative Instruction Nº5, from December 11th. Provides for technical procedures for the creation, presentation, execution and technical assessment of Sustainable Forest Management Plans - PMFS - in primeval forests and their forms of succession in the Legal Amazon, among other provisions. Federal Official Gazette, Secion 1, Brasília, December 13th, 2006. |

|

|

Canova NP, Hickey GM (2012). Understanding the impacts of the 2007–08 Global Financial Crisis on sustainable forest management in the Brazilian Amazon: A case study. Ecol. Econ. 83:19-31. |

|

|

Fortini LB, Carter DR (2014). The economic viability of smallholder timber production under expanding açaí palm production in the Amazon Estuary. J. For. Econ. 20:223-235. |

|

|

Geary R (1970). Relative efficiency of count of sign changes for assessing residual autoregression in least squares regression. Biometrika 57:123-127. |

|

|

Gujarati DN, Porter DC (2011). Econometria Básica-5. McGraw Hill Brasil. |

|

|

Leslie A (2002). Forest certification and biodiversity: opposites or complements? ITTO. |

|

|

Lima RR (2012). Good for some, excellent for others. In. Agro Analysis - FGV. Available at: View. Accessed in June 2016. |

|

|

MacDicken KG, Sola P, Hall JE, Sabogal C, Tadoum M, de Wasseige C (2015). Global progress toward sustainable forest management. For. Ecol. Manage. 352:47-56. |

|

|

Piketty MG, Drigo I, Sablayrolles P, de Aquino EA, Pena D, Sist, P (2015). Annual Cash Income from Community Forest Management in the Brazilian Amazon: Challenges for the Future. Forest 6(11):4228-4244. |

|

|

Pindyck RS, Rubinfeld DL (1991). Econometric models and economic forecasts. McGraw Hill. |

|

|

Richards M (2000). Can sustainable tropical forestry be made profitable? The potential and limitations of innovative incentive mechanisms. World Dev. 28:1001-1016. |

|

|

Sartori RS (2012). Economic Assessment of low-impact operation in a private property in the Amazon state of Rondônia. 120 p. Dissertation - Master in Forest Resources. Luiz de Queiroz College of Agriculture. |

|

|

Sist PA, Sablayrolles PB, Barthelon SB, Sousa-Ota LC, Kibler JFB, Ruschel AD, Santos-Melo ME, Ezzine-de-Blas DA (2014). The contribution of multiple use forest management to small farmers' annual incomes in the Eastern Amazon Forests 5(7):1508-1531. |

|

|

Wang S, Wilson B (2007). Pluralism in the economics of sustainable forest management. Forest. Policy. Economic 9:743-750. |

|

|

Wooldridge JM (2009). Introductory econometrics: a modern approach. 4th ed. Mason, Ohio: South-Western/Cengage Learning, c2009. xix, 865 p. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0