Full Length Research Paper

ABSTRACT

The evolution of technology, mandated the innovation numerous and different functions within the economic unit. Cost systems are also included to these system upgrades, since detailed planning regarding expenses greatly impacts the economic stability and sustainability of an organization. Therefore, the combined utility derived from use of cost data and information systems; after taking into consideration each unique goals an organization sets’, results in development, optimization of processes, sufficient control mechanisms. The latter greatly improve and guide managers to proper strategic and everyday planning. However, these systems are affected easily by a number of factors that could differ depending on the region or sector the company is based. This paper evaluates the variables that can have a positive effect on the use of cost and information systems in Retail businesses operating in a vital agricultural area. A questionnaire was administered via e-mail to retail’s employees from the urban and suburban areas of Thessaly. Statistical analysis included descriptive statistics, scale reliability control and multiple regressions. The results demonstrated a positive impact of cost and information systems on performance, assuming the cost system does not increase complexity, while a company is capable of integrating information systems. Concerning the latter result, the ability and knowhow of employees operating these systems was of particular interest, since companies do not always consider employees’ training as part of the overall system’s investment.

Key words: Integrated information technology, cost systems, information systems, business performance, and human factor.

INTRODUCTION

Over the years, significant changes and developments took place in all aspects of the economy. Consequently, society, people and the business world need to adapt. A very important role for better operation is the ability of companies to keep up with technological changes. The use of information systems has been established worldwide in operations. Competitiveness is achieved by understanding factors that affect operating systems and how companies utilize the aforementioned systems (Sorros et al., 2021).

One system greatly affected is costing (Sorros et al., 2021). In fact, technology and cost systems interfere with each other. Given this assumption, the entire business world has to address the impact factors of this relationship in the most productive way and achieve combined operating benefits. In the context of this requirement, it was necessary to delve into specific factors influencing these systems. That is, in the ways of performance levels are predicted in an environment of cost and information systems, taking into account complexity of the cost systems and the human factor. The results indicate that through the implementation of cost information systems an entity could increase its operational benefits.

Through a set of data, this paper efforts to identify factors that balance the difficulty of implementing and sustaining costing and information systems in improving performance. Traditionally, the importance of costing and the basic product of information systems is evident (Butterworth, 1972)). The difficulty of balancing the cost of an implementation and afterwards maintenance of information systems is a demanding process. The retail sector is constrained by restrictions on investments (Stout and Bedenis, 2007) in the two aforementioned systems. An attempt is made to identify and manage these limitations. It is an issue that does not seem to have been analyzed in depth. Recently, research has begun to look at the redesign of costing systems for performance in a medium-sized company (Stout and Bedenis, 2007; Karagiorgos et al., 2020) but not the combination of the two systems.

This paper is divided as follows: Following the introduction, section two depicts the literature review examining the most important research approaches related to the variables discussed, specifically the conceptual framework of costing, costing systems and information technology systems. Within section two, the research hypotheses are presented. Section three discusses the methodology together with the main parts and items of the questionnaire, as well as the variables to be tested. Section four shows the results of descriptive statistics and correlation analysis and the paper concludes with the most substantial conclusions of the empirical research, limitations and suggestions for future research.

LITERATURE REVIEW

Costing and Information Systems (IS)

Yasin and Quigley (1995) conducted a survey on 25 executives and IS heads on information systems’ usefulness for organizations. Through this research, a gap was identified between the views of the two groups regarding system satisfaction. According to their conclusions, the aforementioned gap is reduced through training and education, in order to reach IS effectiveness.

Leek (1997) investigated the reasons behind IS management providers’ failure to deliver systems that meet the needs of its users. Important factors found include the lack of a strategic perspective of IS and information support technology, but also the different views among organizations on what the management of IS requires.

In addition, according to a research performed by Dechow et al. (2007), it seems that with the introduction of advanced information technologies, such as Enterprise Resource Planning (ERP) systems, administrative control is performed from different departments, since technology is integrated. As a result, the functions performed with information accounting systems were changed.

Tsai et al. (2010) conducted a survey to suggest ways of integrating Activity-Based Costing (ABC) costing systems and environmental costing systems. Results showed that through integration, management could be given financial information for activities as part for the product’s total cost, and support decision-making.

In 2014, in a study conducted by Tan et al. (2014) they compared the costing systems of 12 European countries in hospitals. Results showed that costing systems in European hospitals differ significantly depending on the existence of mandatory costing instructions, costing methods or data controls regarding cost data.

Costing systems and business performance

Fry et al. (1995) dealt with the importance of well-developed strategy in construction organizations. One of the most important features of this strategy is to achieve consistency in the way products and services compete in a selected market, in order to achieve best performance. The catalytic factor in this consequence is the costing system. This research has shown that many companies use accounting systems not suitable to implement this strategy. Instead, companies choose systems that do not fit the market and are not in line with the appropriate strategy.

Subsequently, in 2013 a study conducted by Cugini et al. (2013) assessed the importance of accounting innovation in costing systems of rail transportation systems. Results showed that a new accounting practice facilitates the functional link between the company's resources and their consumption in the provision of transportation services.

In addition, Krumwiede and Charles (2014) investigated the impact of ABC systems on business performance. In particular, they researched ABC’s influence on strategic customer service and low cost priorities or those that do not prioritize such strategies. They argued that ABC systems have a higher impact on profitability for companies that emphasize the aforementioned strategies.

Consequently, the following research hypothesis was formulated in line with the research problem, H1: “Costing Systems and Business Performance” influence “Costing and Information Systems”.

Information systems and business performance

Meldrum and Berranger (1999) analyzed the problems of trying to adapt knowledge development on small and medium-sized enterprise IS through higher education institutions. The importance of knowledge of information systems is also shown by the fact that states provide funding to small and medium-sized enterprises in order to apply to higher education institutions. This research compared the different views that exist on the subject, and concluded that there is a great willingness on the part of small and medium enterprises.

In addition, Chan (2000) examined the increasing impact of information technology (IT) on business processes through specific forms of technology - mainly computer, telecommunications and display technology. Results showed that a complete and thorough understanding of the roles of IT would lead to the systematic identification and evaluation of risk and cost relationships associated with the application of IT in the business processes of an organization.

Later in 2007, Roy and Sivakumar (2007) studied the role of IT in the globalization of business market behavior. The results showed that the adoption of information technology presupposes adoption by both the buyer and the seller, but also compatibility of these two information systems. The globalization of purchasing behavior is influenced by factors at the enterprise level (e.g., perceived risk, digitization) and globally (e.g., availability of alternative suppliers in the buyer’s country, political stability in the supplier’s country).

Moreover, Lindh and Nordman (2017) examined the effects of information technology on business development and performance in business relationships of industrial companies. According to its findings, it seems that there is no direct effect of IT on the performance of the relationship but it acts as a mediator for business development, which is characterized by business creativity and product development.

Finally, in a study conducted in 2020 by Martínez-Caro et al. (2020) explored how IT assimilation can encourage capability and facilitation of organic flexibility and performance. The results showed that there is a positive relationship between the above characteristics.

Consequently, the following research hypothesis was formulated in line with the research problem, H2: “Information Systems and Business Performance” influences “Costing and Information Systems”.

Complexity of costing systems

Schoute (2009) sought to examine the relationship between complexity, purpose, and cost-effectiveness of a system, using research data from medium-sized construction companies. Results showed that when a cost system is used more for product design purposes, its complexity negatively affects the intensity of system use, while when it is used more for cost management purposes; its complexity positively affects the intensity of use of the system. According to this view, the cost system can be more efficient when its design and purposes of use are aligned.

Consequently, the following research hypothesis was formulated in line with the research problem, H3: “Complexity of Costing Systems” influence “Costing and Information Systems”.

Integrated information technology

Lee (2004) evaluated integrated information technology, which incorporates business strategy, business process design, and IT investment support. The results suggest that it is vital to measure the impact on the time cycle for a repurchase decision by customers in order to assess the potential value of a process-based IT investment.

Also, Maiga et al. (2014) attempted to investigate the effect of the interaction of cost control systems and IT integration on cost-effectiveness of a production plant. Results have shown that the financial performance is positively affected when investments are made in ABC control systems, combined with the integration of information technology.

Moreover, Vanpoucke et al. (2017) showed that exchange of information, which has increased in companies, help to develop their supply chain. The latter is an important element in a partnership, but does not improve performance, if not combined with other integrated IT. According to the results, the exploitation of the benefits of information exchange presupposes this integration through information technology.

Finally, Razak et al. (2018) intended in their research to understand the conditions and to explain the systemic contradictions that facilitate the successful integrated information and communication technology in schools. According to the results, three conditions emerged for the successful integration of information and communication technology:

1) Types of tools of this integration in the school,

2) Rules and regulations in the school that shape the culture of integration and

3) Division of labor within the school community.

Cooperation is required from the interested bodies, in order to resolve tensions created by systemic contradictions in different systems of activities, which shape the culture of successful integration of information and communications technology (ICT) in schools.

Consequently, the following research hypothesis was formulated in line with the research problem, H4: “Integrated Information Technology” influence “Costing and Information Systems”.

Cost, information systems and the human factor

Boudreau and Robey (2005) conducted a research study of an ERP system after its implementation in a government agency, in order to assess the importance of the human factor in an organizational change. According to the research, users initially chose to avoid using it as much as possible (inactivity) and later to resolve system constraints in involuntary ways (reinvention). The conclusion was that an integrated technology, such as the ERP system, could be developed and rediscovered in use by the human factor. In addition, Agourram and Ingham (2007) conducted research to understand the interpretation given to IS and their success by people from different national cultures. Participants from France, Canada and Germany showed that people from different national cultures define information systems differently.

Nagirikandalage and Binsardi (2017) conducted a study to examine the impact of Sri Lankan cultural and local characteristics on the adoption of cost systems, that is, the factors that facilitate or hinder their implementation. Their research showed a complete institutional isomorphism and partial institutional heterogeneity in Sri Lanka. In addition, insufficient access to information and the orientation of the local culture affected the implementation of cost systems, as there was a lack of awareness of the importance of the cost system.

Consequently, the following research hypothesis was formulated in line with the research problem, H5: “Cost, Information Systems and the Human Factor” influence “Costing and Information Systems”.

METHODOLOGY

This research is quantitative based on a survey questionnaire administered to a sample consisting of 78 retail companies with moderate to good experience in applied cost techniques activity in the retail trade. The paper utilizes a regression model to describe the relationships by fitting a line to the observed data and estimate how a dependent variable is affected by the changes of independent variables. A multiple linear regression is used to estimate the strength of the relationship between variables.

The empirical research questionnaire consisted of seven (7) basic parts with a total of 45 five-level Likert scale questions. The questions derived from the literature review and tools from precious researched. The first part concerns the demographic data (operating years, the position and education). The second part was about "Cost Systems and Information Systems" (9 items) and evaluates the degree of application, use and operation of costing, as well as information systems.Τhe next part, concerns the Costing Systems and the performance of companies (7 items). This section examined the impact of costing system on performance, strategy, growth and profits of a business. The fourth part concerns Information Systems and Business Performance (8 items) and the degree of impact of its use on flexibility, business relationships, online stores and advertising. The next section examined the complexity of costing systems on business control, decision-making, cost management and inventory management. The next part, Integrated Information Technology, consisted of two (2) items and examined its impact on the operations and performance of the business. The questionnaire is completed with a set of items measuring cost and information systems’ relation with the human factor. More specifically, it measured the degree that the company's culture, investments in training employees to learn the systems, and the latter’s willingness to use them relate.

Statistical analysis methods and variables

Hejase et al. (2012) contend that informed objective decisions are based on facts and numbers, real, realistic and timely information. Furthermore, according to Hejase and Hejase (2013), “descriptive statistics deals with describing a collection of data by condensing the amounts of data into simple representative numerical quantities or plots that can provide a better understanding of the collected data”. Therefore, in order to capture the purpose of the empirical research, descriptive statistics were used. Then from the parts of the questionnaire related to the thematic units, variables were defined and created. These variables were evaluated for reliability using Cronbach alpha index. More specifically, the research variables are:

1) The use of "Cost and Information Systems." Is considered as dependent variable Y, resulting from questions 1 to 9 (Part B of the questionnaire).

2) The first independent variable is the effect of "Business Performance in Cost Systems", resulting from questions 10 to 16 (Part C of the questionnaire).

3) The second independent variable is the effect of "Business Performance in Information Systems", resulting from questions 17 to 24 (Part D of the questionnaire).

4) The third independent variable is the effect of "Complexity of costing systems", questions 25 to 28 (Part E of the questionnaire).

5) The fourth independent variable is the effect of "Integrated Information Technology", resulting from questions 29 and 30 (F part of the questionnaire).

6) The fifth and final independent variable is the link between "cost and information systems and the human factor", resulting from questions 31 to 42 (Part G of the questionnaire).

These variables were initially analyzed for their correlations using the Pearson’s Correlation coefficient. Finally, the empirical analysis is completed by listing the results of the multiple regression analysis.

Since the relationship between the variables X and Y is linear, the following multiple linear regression models were used to examine the strength of association between the different independent variables and the dependent variable:

y = b0 + b1X1 + b2X2 + b3X3 + b4X4 + b5X5 + ei

Where, Y: is the dependent variable "Cost Systems and Information Systems" "(V1), X1, X2, X3, X4, X5: are the independent variables; b1, b2, b3, b4, b5: are the independent variables parameters or coefficients which quantify the relationship with the dependent variable; ei: is the error.

RESULTS

Descriptive statistics results

The first part which consists of questions 1-3 refers to the demographics of the participants from the companies in the empirical research. More specifically, the years in which each entity that participated in the research operates and is active are examined. Most companies operate for 2 to 10 years. Question 2 investigates the position of responsibility of the respondent. From the respondents, 55.8% were corporate staff. Subsequently, 18.2% were administrative staff, 13% were business owners, 9.15% were accountants and only 3.9% were IT personnel. 37.7% of the respondents 37.7% have completed secondary education, 36.4% higher education, while a 22.1% holds a master's degree and 3.9% have completed a PhD.

Research variables

Costing and information systems

The first part of the study "Cost and Information Systems" examines whether the integration of costing systems gives important information for the company. 64.9% of the respondents said that the integration of costing systems gives information about the company to a great extent, while 28.6% believe that it gives a very large degree of information. Also, 61% of companies invest heavily in costing systems, while 22.1% invested lightly. 67.5% of respondents believe that the business's costing system contributes more or less to addressing its weaknesses, while 85.8% believe that the costing system used by a company contributes more or less to addressing its threats.

83.1% of the respondents believe that the company's information systems are more or less affected by its operation. 63.6% of the respondents believe that ease of use more or less influenced the choice of information system, according. In addition, 22.1% of the respondents believe that ease of use significantly influenced the choice of information system. On the other hand, 57.2% believe that ease of learning greatly influenced the choice of information system, according to 57.2%. While, 28.6% believe that ease of use significantly influenced the choice of information system. The cost of implementation more or less influenced the choice of the information system as declared by 77.9% of the respondents. Also, 79.2% of them believe that customer needs influenced the choice of information system.

Costing systems and business performance

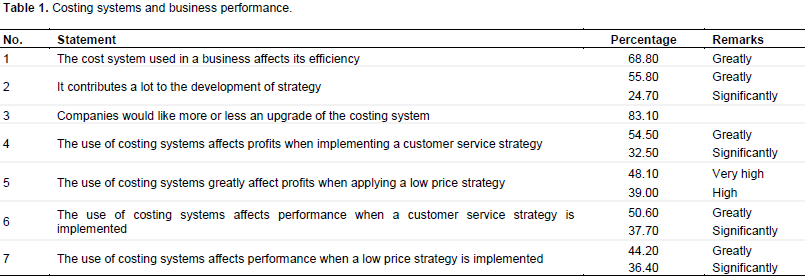

Table 1 show that respondents were mostly interested to upgrade the costing system and at the same time were satisfied with the efficiency of the cost system. On the other hand, respondents agreed on the average that their cost system serves the company profits and performance.

Information systems and business performance

Eight questions constitute of the third Thematic Section, examining Information Systems and Business Performance. The use of information systems by employees is based on the training received from academic institutions according to 45.5%. In addition, a 33.8% believe that their IS is well-founded. The next question examines whether the use of information systems by employees is based on training from seminars or workshops (Public or Private). Information technology affects the performance of business, while it also affects business relationships. Information technology contributes to organic flexibility and advertising according to 85.7% of responses. Information technology affects online stores, according to 89.6% of responses. The impact of digitization on business processes has increased more or less, according to 90.9% of responses.

Complexity of costing systems

The first question examines the degree of contribution of the quantification of a company's operations to decision-making, whereby 56.60% believe it has large contribution. The second question shows that 63.60% of respondents believe that quantifying the operations of a company contributes a lot to control. Moreover, 58.40% of the respondents believe that the costing system contributes a lot to cost management [third question]. Finally, 58.40% of the respondents believe that a cost management system contributes lot to inventory management.

Integrated information technology

Integrated information technology examines the degree to which operation of business is facilitated by investing in new technology tools. 64.90% of respondents believe that investing in new technology greatly facilitates the operation of businesses. While 63.60% of the respondents believe the contribution of investing in new technology tools affects a lot the increase of profitability of the business.

Cost-Information systems and the human factor

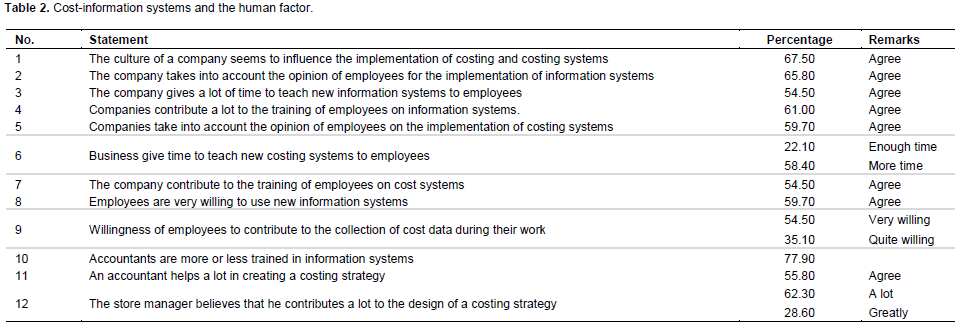

The last thematic unit analyzes the correlation of cost systems and information systems with the human factor. Table 2 shows that respondents are comfortable on the average with the human factor involvement, impact and influence on the cost information system.

Correlation analysis

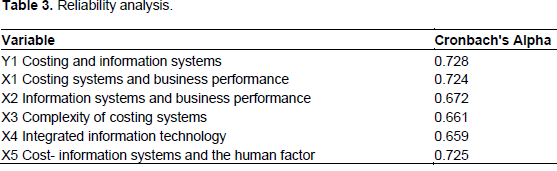

The Internal Reliability of the 6-item scale is assessed using the Cronbach’s Alpha technique. Table 3 shows that the 6-item scale produced a Cronbach’s Alpha if items deleted all fall in the range 0.659 to 0.728 matching the range 0.6 - 0.8 labeled “Good” (Hejase and Hejase, 2013:570; Burns and Burns, 2008:481).

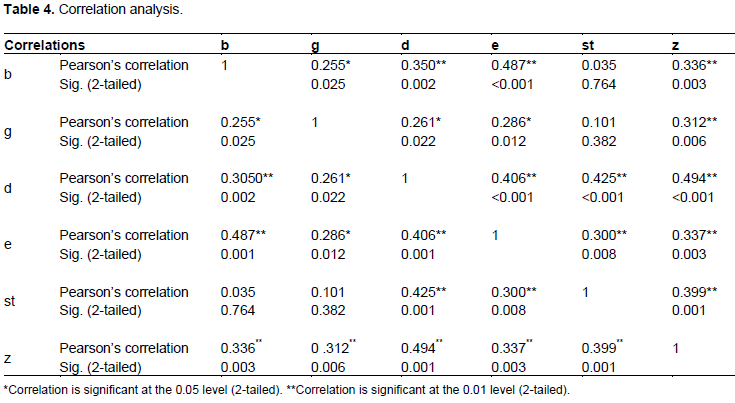

According to Chehimi et al. (2019), “this indicates a very good strength of association and proves that the selection of the questions is suitable for the questionnaire purpose” (1915). Then, Pearson’s correlations of variables were checked. Table 4 presents the statistically significant linear correlation between the dependent variable "Cost Systems and Information Systems" and the independent variable "Integrated Information Technology" (V5). Also, there is a statistically significant linear correlation between the dependent variable "Cost Systems" and the independent variable "Cost Systems and Business Performance" (V2), the independent variable "Information Systems and Business Performance" (V3) and independent variable "Cost Complexity Systems" (V4). Therefore, no negative linear correlation of the dependent variable with the independent ones is observed.

More specifically, the regression model to be evaluated is:

“Costing Systems and Information Systems = bo + b1 * Costing Systems and Business Performance + b2 * Information Systems and Business Performance + b3 * Complexity of Costing Systems + b4 * Integrated Information Technology + b5 * Cost Systems, Information Systems and the Human Factor”

The Coefficients are depicted in Table 5. Consequently, the resultant regression equation of the model is derived as follows:

“Costing Systems and Information Systems = 2.02+

0.044* Costing Systems and Business Performance + 0.168* Information Systems and Business Performance + 0.333* Complexity of Costing Systems + 0.24* Integrated Information Technology + 0.171* Cost Systems, Information Systems and the Human Factor”.

.png)

The Coefficients show that the first independent variable "Cost Systems and Information Systems" (V2), sig = p-value = 0.048 <0.05, the null hypothesis is rejected and therefore has a statistically significant effect on the dependent variable "Cost Systems and Information Systems".

For the second independent variable "Information Systems and Business Performance" (V3), sig = p-value = 0.041 <0.05, the null hypothesis is rejected and therefore the independent variable has a statistically significant effect on the dependent variable "Costing Systems and Information Systems "(V1).

For the third independent variable "Cost Complexity Systems" (V4), sig = p-value = 0.000 <0.05, the null hypothesis is rejected and therefore the independent variable has a statistically significant effect on the dependent variable "Costing Systems and Information Systems" V1).

For the fourth independent variable "Integrated Information Technology" (V5), sig = p-value = 0.031 (<0.05), the null hypothesis is rejected and therefore the independent variable has a statistically significant effect on the dependent variable.

For the fifth and last independent variable "Cost Systems, Information Systems and the Human Factor" (V6), sig = p-value 0.013 <0.05, the null hypothesis is rejected and therefore the independent variable has a statistically significant effect on the dependent variable " Cost Systems and Information Systems "(V1).

DISCUSSION

Most companies participated in this survey have been operating for ten years. Given the general Greek problematic economy, the financial crisis of 2009, the recent health crisis of Covid19; many companies faced problems or been led to solve them. Retail and its commercial activity are characterized by lower capital costs and therefore companies are entered and leave the market faster compared to their larger counterparts. A great number of respondents were managers. This implies the small number of staff or the direct correlation of managers and overlapping responsibilities.

Most respondents (93.5%) were positive about ??implementing costing practices and information systems. Generally, companies invest heavily or lightly in costing systems, admitting that a business's costing system contributes in addressing weaknesses and threats. It was expected that information systems in addition to great investment costs, would also be affected by operational needs, user and training friendliness. Results demonstrate that the retail sector, in terms of information systems implementation, is affected by the needs of the company's customers.

Successful costing seems to affect performance and business strategy. Businesses are willing to upgrade their costing system. The goal of using and upgrading these systems is to develop customer service strategies. There are companies that have chosen or want to use cost methods for low priced products. Retail companies are heavily involved in products of different price ranges. Those that aim to utilize the costing of low products are those realized cost’s usefulness in marginal profit. As retailers deal with different profit margins, accurate costing allows maximized profit due to separation of goods by type. With this in mind, it is understood that the percentage that has a full understanding of costing both as a method and a strategy is lower than what initially appeared (near 40%). Nevertheless the percentage of utility of costing in performance remains important.

Nearly half of the respondents argue that an employ’s ability to use information systems is based mostly on training received prior to their recruitment in the work environment. This translates that half employees do not expect significant training after being hired, while simultaneously half of the companies had not made budget or investment preparations for training costs. On the other hand, while only 33.8% believe the IS used by the company is well-founded, 85.7% answered that Information technology contributes to organic flexibility and advertising. Furthermore, respondents are aware that Information technology affects business performance, business relationships. The questionnaires show a 90.9% agreement on the impact of digitization on business processes. Results demonstrate an understanding of a changing environment in which technology’s role is increasing. Most businesses turn towards recruitment techniques to acquire personnel capable of implementing new technologies in the work place. Few businesses are willing or capable of continually training employees. This could be interpreted by constant changes in technology or high employee turnover rates.

It is worth mentioning that regarding integrated information technology 64.9% argues greatly for new investments in technology towards facilitating business operations. While 63.60% of the respondents believe the contribution of investing in new technology tools significantly increases profitability. This approach characterized by willingness to invest in technology, but lacking the necessary plan of training employees to use it could explain a serious gap in the understanding of the incorporation of informational systems as part of business. However, it is possible to emanate a lack of knowledge originating inside the company’s intellectual capital. This absence of know how could stem from the company’s higher management. Thusly a company finds difficulty in training new employees.

This research verifies the contribution of quantifying operations and goals to decision-making and control. Generally, cost managements are found as a vital contribution to the operation of a company, while in the same time increases its cost system complexity.

“Costing Systems and Business Performance” was found to significantly affect "Cost Systems and Information Systems". Thusly management invests in costing and information systems mostly for improving performance and in particular through expenses reduction and management. A similar case was observed regarding "Information Systems and Business Performance" effect on "Costing Systems and Information Systems”.

A cost system’s complexity and integrated information technology were both found to affect the utilization and implementation not only of the costing System but also the choice of an information system. Significance drops when integrating the human factor in the cost and information system equation. This correlation strengthens this research interpretation of results regarding employees training, since the latter do not expect to be trained and corporations do not include it in system investment costs.

CONCLUSION

Companies are willing to invest and ??implement cost practices and information system strategies. Respondents declare that a business's costing system contributes in addressing weaknesses and threats. Costing seems to affect performance and business strategy. Regarding information systems, companies work towards constant upgrading to develop customer service strategies. However, retail fails to perceive employees’ training as a significant part of the investment and budget. Results demonstrate the constant changing of the industry and technology’s role in it. The paper verifies the contribution of quantifying operations and goals to decision-making and control. Finally, a cost system’s complexity and existing integrated information technology each separately found to affect the utilization and implementation both of the costing system and the information system.

Implications

Results support retail businesses that operate away from a country's largest urban centers, develop strategies and general to decentralize the economy. At the same time, the importance of staff training is evident. The approach a retail company adopts seems to affect its ability to assimilate costing and information systems. The continuous investment in systems aimed at efficiency and the inclusion of lifelong learning must be impressed in modern business policies.

Research limitations

The sample consisted from retail companies operating away from the largest urban centers. The survey was performed during the Covid 19 pandemic and restrictive measures. Many employees were unable to answer the questionnaire.

Future research

The exact reasons that affect the importance of employee training in costing and information systems can be explored further. This could clarify whether the lack of training plans is a result of expenses or a retail managers and owners’ approach. Furthermore, a more in depth survey could try replicating results for different industries, or integrating additional geographical factors.

CONFLICT OF INTERESTS

The authors have not declared any conflicts of interests.

REFERENCES

|

Burns R, Burns R (2008). Cluster Analysis In: Business Research Methods and Statistics Using SPSS. Sage Publications, Thousand Oaks. |

|

|

Butterworth JE (1972). The accounting system as an information function. Journal of Accounting Research 10(1):1-27. |

|

|

Chan SL (2000). Information technology in business processes. Business Process Management Journal 6(3):224-237. |

|

|

Chehimi GM, Hejase AJ, Hejase NH (2019), An Assessment of Lebanese Companies' Motivators to Adopt CSR Strategies. Open Journal of Business and Management 7(19):1891-1925. |

|

|

Dechow N, Granlund M, Mouritsen J (2007). Interactions between modern information technology and management control. Issues in Management Accounting 3:45-64. |

|

|

Agourram H, Ingham J (2007). The impact of national culture on the meaning of information system success at the user level. Journal of Enterprise Information Management 20(6):641-656. |

|

|

Boudreau MC, Robey D (2005). Enacting integrated information technology: A human agency perspective. Organization Science 16(1):3-18. |

|

|

Cugini A, Michelon G, Pilonato S (2013). Innovating Cost Accounting Practices in Rail Transport Companies. Journal of Applied Accounting Research 14(2):147-164. |

|

|

Fry TD, Steele DC, Saladin BA (1995). The role of management accounting in the development of a manufacturing strategy. International Journal of Operations and Production Management 15(12):21-31. |

|

|

Hejase HJ, Hejase AJ, Hejase HANJ (2012). Quantitative Methods for Decision Makers: Management Approach. Beirut, Dar Sader Publishers. |

|

|

Hejase AJ, Hejase HJ (2013). Research Methods: A Practical Approach for Business Students (2nd edition). Philadelphia, PA, USA: Masadir Incorporated. |

|

|

Karagiorgos A, Alexandra G, Ignatiou O, Terzidou A (2020). Role and contribution of administrative accounting to small and very small businesses. Journal of Accounting and Taxation 12(2):75-84. |

|

|

Krumwiede KR, Charles SL (2014). The use of activity-based costing with competitive strategies: impact on firm performance. Advances in Management Accounting 23:113-148. |

|

|

Lee I (2004). Evaluating Business Process?integrated Information Technology Investment. Business Process Management Journal 10(2):214-233. |

|

|

Leek C (1997). Information Systems Frameworks and Strategy. Industrial Management and Data Systems 97(3):86-89. |

|

|

Lindh C, Nordman ER (2017). Information technology and performance in industrial business relationships: the mediating effect of business development. Journal of Business and Industrial Marketing 32(7):998-1008. |

|

|

Maiga AS, Nilsson A, Jacobs FA (2014). Assessing the Interaction Effect of Cost Control Systems and Information Technology Integration on Manufacturing Plant Financial Performance. The British Accounting Review 46(1):77-90. |

|

|

Martínez-Caro E, Cepeda-Carrión G, Cegarra-Navarro JG, Garcia-Perez A (2020). The Effect of Information Technology Assimilation on Firm Performance in B2B Scenarios. Industrial Management and Data Systems 120(12):2269-2296. |

|

|

Meldrum M, De Berranger P (1999). Can Higher Education Match the Information Systems Learning Needs of SMEs? Journal of European Industrial Training 23(8):323-344. |

|

|

Nagirikandalage P, Binsardi B (2017). Inquiry into the cultural impact on cost accounting systems (CAS) in Sri Lanka. Managerial Auditing Journal 32(4/5):463-499. |

|

|

Razak NA, Jalil HA, Krauss SE, Ahmad NA (2018). Successful implementation of information and communication technology integration in Malaysian public schools: An activity systems analysis approach. Studies in Educational Evaluation 58:17-29. |

|

|

Schoute M (2009). The Relationship between Cost System Complexity, Purposes of Use, and Cost System Effectiveness. The British Accounting Review 41(4):208-226. |

|

|

Sorros J, Lois P, Charitou M, Karagiorgos AT, Belesis N (2021). Improving competitiveness in education institutes-ABC's neglected potential. Available at: |

|

|

Roy S, Sivakumar K (2007). The role of information technology adoption in the globalization of business buying behavior: a conceptual model and research propositions. Journal of Business and Industrial Marketing 22(4):220-227. |

|

|

Stout DE, Bedenis GP (2007). Cost-system redesign at a medium-sized company: Getting the right numbers to drive improvements in business performance. Management Accounting Quarterly 8(4):9-19. |

|

|

Tan SS, Geissler A, Serdén L, Heurgren M, Van Ineveld BM, Redekop WK, Hakkaart-van RL (2014). DRG systems in Europe: variations in cost accounting systems among 12 countries. The European Journal of Public Health 24(6):1023-1028. |

|

|

Tsai WH, Lin TW, Chou WC (2010). Integrating activity-based costing and environmental cost accounting systems: a case study. International Journal of Business and Systems Research 4(2):186-208. |

|

|

Vanpoucke E, Vereecke A, Muylle S, (2017). Leveraging the Impact of Supply Chain Integration through Information Technology. International Journal of Operations and Production Management 37(4):510-530. |

|

|

Yasin MM, Quigley JV (1995). The Utility of Information Systems Views of CEOs and Information System Executives. Information Management and Computer Security 3(2):34-38. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0