ABSTRACT

In Uganda like many developing countries, financial management units are facing numerous performance challenges as a result of untold pressure, overwhelming deadlines, limited resources, political patronage and limited professional skills among the practioners. To unravel these impediments, drastic mechanisms need to be put in place to ensure a common balance among all stakeholders; financial resources must be used in a frugal but in a strategic manner to ensure effective and efficient allocation to all sectors of governance both in the urban and rural administrative units. Urban governance in Uganda like many developing countries has its own peculiarities ranging from provision of key social service delivery to mandatory urban infrastructural development, hence the reason for taking calculated steps to deliver effectively. The study advances the argument that capacity enhancement of staff and the strict observance of internal control mechanisms is the epitome of a vibrant financial management system in the administration of urban authorities.

Key words: Fiscal devolution, internal control systems, decentralisation, urban governance.

Internal control systems is a strategic mirror of hierarchical strategies, sanctions and internal procedures created by institutions to provide management with essential targets of guaranteeing that the organisation delivers her mandate effectively (Puttick, 2001). Puttick further argues that, an institution whether public or corporate can only develop if it keeps up with the strict and robust protocols of audit and accounting principles without manipulation of any accounting and audit information.

In Baringo County Administration in Kenya, for instance the Auditor General’s Report (2018), revealed that a number of anomalies were observed in the accounting and audit systems as noted below; (i) no financial statements/records were available, (ii) No internal financial and non-financial control systems in place, (iii) Un clear financial management procedures, (iv) the utilisation of the new integrated financial management and IT systems were very lean on the ground throughout the county administration to remedy the collapsing systems (Bird 2015). Notably, these were occurrences in most of the County administrative systems despite the introduction of the Integrated Financial Management and technology Systems and Audit management procedures in all government institutions in Kenya.

Internal control systems presupposes institutions coming up with clear and robust procedures of managing the financial and audit aspects of the Company so as to guarantee successful deliverance of the service agenda in the spirit of accountability, effective service delivery and transparency (Abubakari and Adam, 2018). Yang et al., (2012) compares internal control systems in an institution as a human sensory system, which controls the operation or functionality of the company/body where demands to and fro management are tendered in and responded to by management for the rationale of maintaining the set out standard operating procedures set out as protocols meant to ensure the smooth running and working of the company business.

Urban governance refers to a government technique (local, regional and national) where stakeholders decide on how to plan, finance and manage the development of urban areas. It is a continuous process of negotiation and agreement over the allocation of social and material resources and political power. The rationale for urban administration is broad ranging from provision of basic amenities like street lights, garbage collection, water supply, maintenance of street cleanliness, tax collection and drainage management only to cite but a few.

In sum, according to Pearce (2015), urban management has six (6), cardinal functions namely; urban planning, regulation of land use, planning for economic and social development, water supply for domestic, industrial and commercial purposes, Public health, sanitation conservancy and solid waste management and fire services. Urban planning is very fundamental in the overall urban management practices, because it takes lead in the following critical areas; use of land, environmental protection, infrastructural development, supply network, all these cause urban areas to be functional and operational.

The study explores key internal control systems (ICS) which are applied globally but specific to urban governance in a developing terrain. It attempts to qualify the various internal control systems and the relevance of these ICSs in urban governance in Uganda.

Overall objective of the paper

The overall objective of this paper is to establish how internal control systems can influence the financial management function to deliver effective service delivery in urban governance in Uganda.

Research questions

The paper is guided by the following research questions;

1) What are the core internal control systems that support the financial management function in urban governance in Uganda?

2) What are the benefits of maintaining an effective internal control system for the financial management function in urban governance in Uganda?

Theoretical review

Various theories have attempted to explain the relationship between internal control systems and the financial management function in urban administration both in the developed and developing world. This paper is anchored on the Principal - Agency theory as discussed below.

Principal-agency theory

The Principal Agency Theory (PAT), originates from the relationship between the shareholders (Principals) and managers (Agents) of the company, notably the two parties have differing interests especially, the risk sharing problem where most times the principal and the agent have differing standpoints towards the aspect of risk taking. The principal has different interests from the agent, however the principal delegates the running of the business to the agent who ideally is technical, competent and skilled to deliver, and he has the technical know-how and the information advantage of the company, more elaborately than the principal. Due to the fact that the agent has the information advantage and also personal interests outside the principal’s knowledge, two administrative impediments occur which grossly affect the performance of the Company which include; moral hazard, meaning the agent does not commit to the agreed targets of his/her work, secondly, the problem of adverse selection, implying that the principal has no capacity to probe the technical competence of the agent as he/she performs his/her duties (Eisenhardt, 1989).

The Principal-Agency theory provides an explanation of the operations of public agencies where government is the principal and employees, in these agencies for this case of urban management workers are the agents who technically work on behalf of the government who is the principal. The provisions of internal control systems as mechanisms to introduce best practices in the financial management function is relayed by government bodies as the principal and expected to be implemented to the later by the employees in the urban authority as agents. The explanation of the relationship between the government and the employees clarifies the different roles for each of them towards the achievement of the overall goals of the organisation.

Internal control systems are the cornerstone of a company’s checks and balance protocols for the performance measurement on standards and procedures (Kakuru, 2001). Ibid, further contends that an institution without a control system especially in the financial management framework normally affects its performance and consequently retards its ability to propel productivity in a given period of time. A robust internal control system facilitates the organization’s managers to comprehend the direction of its portfolio investment thus promoting proper accountability and transparency.

Carr and Chen (2004), argues that if an institution is to fix her accountabilities for all the financial resources it receives and spends, a perfect internal control system is a must have tool. Chen, further argues, that innovations in the financial management sector have climaxed the need for enhanced demand for an enhanced risk management system as well as an elaborate corporate governance procedures in an institution, therefore, the areas that are captured in the implementation of good corporate control frameworks are highlighting areas such as authorization, review of employee performance, reconciliation of accounts, security of company assets and development of schedules of duty for each responsibility portfolio. Therefore, many organizations today use control measures, monitoring of both financial and non-financial control systems and information communication technology as prescribed protocols for ensuring vibrant financial management hygiene (Brink 2009).

If companies are to survive, there is need to create and maintain resources for the smooth running of those institutions and this greatly depends on accountability which is premised on the principles and procedures of governance structures of organisations (Green, 2003). Green further contends that there is a nexus between accountability and performance measurement and that, this should not be utilised to enforce sanctions but instead it should be used for corrective approaches and replication for purposes of stimulating budgetary administration. Green (2003) alludes to the fact that control systems facilitate an organisation’s ability to deploy solutions to mitigate its actions. It is contended that institutions that have put up control systems realise enormous benefits to its actors to perform as expected and hence these approaches enhance management relationships with her stakeholders and other donor partners. Through all these efforts the organisation’s accountability requirements increases the efficient and effective management of institutions and therefore legitimacy and credibility of its systems is highly enhanced.

Financial accountability, control systems and financial management practices in both the public and semi-autonomous institutions in Uganda presented that, strict control systems have a direct bearing on the outcomes than accountability framework on the organizational systems (Ntongo, 2012). The implication of these studies is that until when public institutions grapple and fix their internal control systems the financial management systems cannot achieve the organisation’s desired financial management hygiene which is a prerequisite for financial mobilisation and utilisation.

Walker et al. (2003), postulates that information, communication and technology systems or processes provide the identification, the recording and utilisation of relevant information that supports employees to perform their duties, it is further argued that information, communication and technology systems provide feedback relating to operational financial and compliance related requirements that champions the management and support of a company/organization (Ndanyi, 2019). Adeyemi and Odunayo (2019), on the other hand states that, if established financial management systems are to perform up to the expected standards, it is imperative to secure the relevant data from both the internal and external stakeholders which information should systematically and logically be discerned, recorded, processed and disseminated to all relevant partners in a timely and appropriate timeframe.

Internal control systems on financial management systems in the public realm in Uganda have not impacted on public institutions, this has instead led to the closure or suspension of some of the public institutions due to undesirable financial management practices as reported in the financial audit reports (Kakuru, 2001). Kakuru espouses that the frequent under performance of the financial management function occurs due to weak internal control systems which are either or deliberately avoided to the advantage of these institutions hence causing improper and un planned financial management irregularities in most of the public agencies/departments. Ibid, further observes that, some public institutions especially in the local governments lack up to-date financial records because of the limited capacity competence gaps among the employees of the finance and audit units of public agencies.

Prawit (2008:1-29) observes that, due to the enormous increase in the auditing and accounting flaws in Uganda like many developing countries in the recent years, the internal and external audit function has heightened its performance and this has caused a marked change in the corporate governance and financial reporting systems in the government departments in Uganda. The local Government Financial and Accounting Regulations (2007), is mandated to ensure full protection of the local council property, adequate and proper maintenance of the local council resources, proper use and utilisation of council financial resources and hence reduction of any form of financial misappropriation.

The internal Audit function of the government departments takes the cardinal coordination of these activities code named internal control systems for a government body. The organisation‘s Internal Audit department presides over all the regulations and procedures relating to financial management framework in government institutions.

The case study design was used because it provided an opportunity for intensive and extensive analysis of both financial and non-financial internal control systems in relation to financial management practices in public agencies. Besides the case study, design was also useful since aspects such as behavior, opinion, beliefs and knowledge of the respondents in relation to financial management function in urban governance was ably discerned and utilized in the study. Both qualitative and quantitative approaches were used, but largely the qualitative approach was deployed.

To ensure effective data quality assurance and control, it was important to choose carefully the data collection instruments that would preserve the integrity of the data (Most et al., 2003). Data collection instruments included: self-administered questionnaires and the use of an interview guide.

Seven (7) employees were purposively selected from each ward and used in the study. Seven (7) wards were purposively used in the study, specifically heads of departments were identified and used in this study, the departments used included; finance, education and sports, agriculture and production, health services, gender and social development, trade, industry and investment, works and engineering.

The data that informed the findings were collected using the self-administered questionnaires and the interview guide from respondents identified from the administrative wards of Kampala Capital City Authority in Uganda.

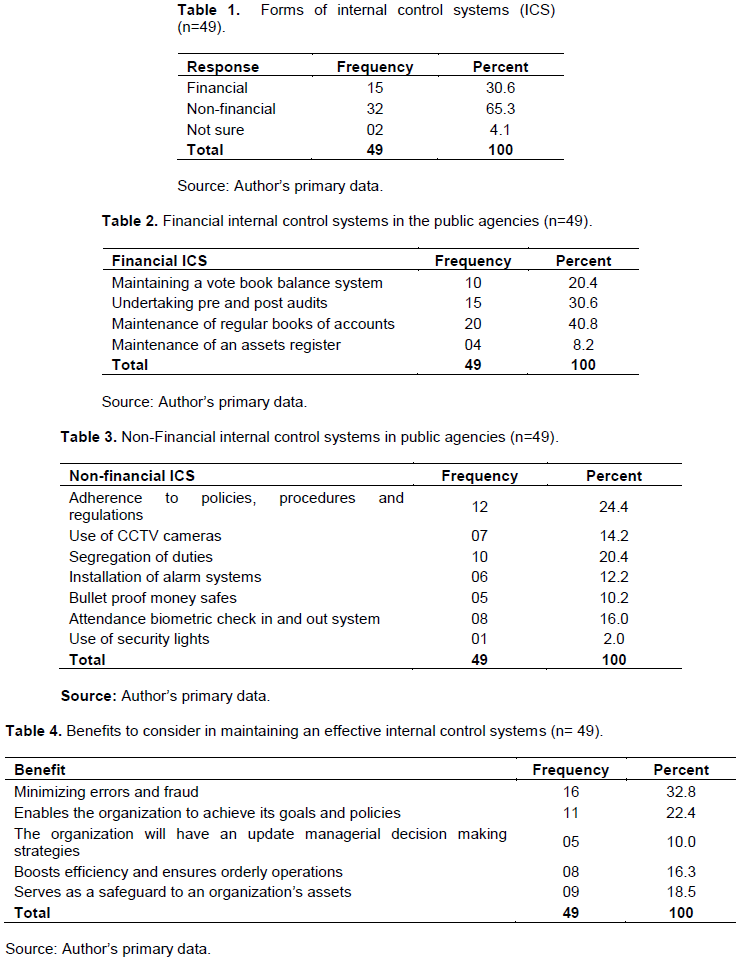

Table 1 shows that there was evidence that the majority (65.3%) of the respondents stated that there were non-financial internal control systems in their organisation. The argument is that the respondents were involved in the non-financial internal control systems and (30.6%) further stated that there were also financial internal control systems in their organisation. On the other hand (4.1%) of the respondents were not aware of any ICSs in place. The argument here is that in order to create sound financial management practices in the Ugandan public institutions both financial and non-financial internal control systems must be in place. One of the Key Informants (KIs) interviewed stated that:

“The idea of financial prudence must be double edged if it has to respond to the purpose it is meant to achieve, when you fail to fix sound financial management practices, you will not achieve the intended outputs and you will also fail to satisfy the requirements of proper mandatory periodic financial statements and accountability to attract financial support from both government and other development partners. It is therefore essential to utilise both financial and non-financial internal control systems to remedy the situation. The interview quotation above indicates that all government agencies need to utilise both financial and non-financial internal control systems in order to have the

best financial management practices.

Table 2, states that there are four key financial internal control systems as follows, maintenance of regular books of accounts (40.8%), undertaking pre and post audits (30.6%), maintaining a vote book balance system (20.4%), and maintenance of an asset register (8.2%). The findings above reveal that if public institutions are to have sound financial management bench marks, maintenance of periodic books of accounts must be enforced in order to have a sound financial system to attract any form of financial support.

Table 3, indicates that the non-financial internal control systems include; adherence to internal policies (24.4%), segregation of duties/work for instance use of initiator and approver arrangement (20.4%), attendance to duty biometric checking in and out system (16.0%), utilisation of CCTV cameras (14.2%), use of alarm systems (12.2%), use of bullet proof money safes (10.2%), utilisation of security lights (2.0%). The results in Table 3 indicate that it is imperative to deploy non-financial internal control systems to ensure compliance with the existing procedures for the effective management of financial resources in government agencies like the local governments. One KI interviewed made the following observation:

“As administrators the author cannot afford to wait for big plans yet there are minor initiatives that we can utilise to control the abuse of public funds and if these are well utilised it could attract their division/ward to get more funding from both public and private partners, minor initiatives such as enforcing the existing regulations, ensuring prompt accountability, adherence to update payment procedures are small initiatives that managers can enforce with little difficult.

In short, the KI is arguing that instead of waiting for the robust procedures of enforcing the financial internal control systems, which are cumbersome, it is much easier for administrators to enforce what is easy but within the confines of the existing regulations and procedures.

On the issue of ICS, one of the KIs argued that:

“In this country, there are many oversight institutions which are established to oversee the utilization, absorption and accountability of institutional funds, in the recent past government has created an office in state house to handle cases of abuses of public offices and corruption generally and therefore control systems are to check on the abuses in the public institutions before they get out of hand.

The argument here is that financial management practices require taking strong decisions whether they hurt employees, but as long as they lead to the wider agenda of service delivery to the citizens such as health, education, works, and water points etc. It is only when tough and strict measures are put in place that employees will be able to comply with the procedures and laws in place.

Table 4, indicates that there are a number of benefits that accrue out of maintaining an effective internal control system namely; reduction of errors and fraud (32,8%), the organization working towards achieving its goals and policies (22.4%), up to date managerial decision making

strategies (10.0%), efficiency and orderly operations (16.3%), protection of organization’s assets (18.5%).

From the findings it can be adduced that both financial and non-financial ICS, realize enormous benefits to government agencies through elimination of abuses andalso abuse of financial resources as per the existing procedures in government. One of the KIs interviewed argued that;

“Internal control systems should be observed in every organization, no organisation can thrive without observing established systems in place, by adhering to the existing regulations in place, it will be easy to achieve enormously in the area of financial management function.

What the KI is alluding to is that organizations must operate within the boundaries of the law and established financial regulations if they are to meet the mandates and goals of their organisation within a specified period of time. This is supported by Bossert et al. (2002) when they argue that ’’for any public agency to deliver there must be strict observance of established rules and regulations in place’’. One of the KIs reacting on challenges facing implementation of ICSs argued that;

“Internal control systems greatly support the established systems of any organisation since public officials constitutionally work in public trust. This implies that these officials act on behalf of the public as tax payers and hence they (public officials) must pay attention to what they do because the owners of the business are the public. Due to the fact that the public service has a weak performance evaluation system, it is at times difficult to enforce the ICSs after all those officers who may not achieve their targets are most times not sanctioned due to the weak performance evaluation systems in the public organisations.

One of the KI argued that;

‘’It is true internal control systems are essential for not only the public agencies but also for corporate organisations because of the fact that ICSs greatly align the established legislations in place, therefore all employees need to comply with these controls, since financial management function acts as the spring board to other resources in the organisation’’.

One of the KIs interviewed on the implementation of internal control systems argued that, ICSs must be embraced to fix the organisation’s systems;

“Internal control systems are very pertinent tools of improving the culture of individual responsibility and accountability among employees, it should be observed that the managers should take lead in the initiation, development and implementation of the internal control systems in the organization.

The KI observed that the following are the likely causes of failures to the implementation of the ICS, 1) lack of adequate training among staff both supervisors and supervisees, 2) Inadequate work enablers to facilitate work proficiency, 3) Limited staff retention programmes.

The observations being raised by the KIs points to the fact that, an employee’s performance is very important and should be underscored at every level of the organisation if ICS are to make any meaningful impact at all in any private or public organisation.

Following the interviews and questionnaire results of the following accrued as important findings to the study. Two forms of internal control systems were identified, namely financial and non-financial; the two forms complement each other as pillars of ICSs. The respondents rank and scored the forms of ICSs in terms of importance as follows; maintenance of regular books of accounts (40.8%) as the most crucial that accounts for the financial internal control systems (ICS). The reasons advanced included; aligning investment and planning opportunities, avoiding cash flow challenges and enhancing income or decreasing overspending. Other factors included managing pre and post audits in the accounting system (30.6%), managing vote book balance system (20.4%) and utilisation of an asset register (8.2%).

The findings further revealed that in the public sector there were critical factors that supported non-financial ICS as follows; strict use of policies, procedures and regulations (26.6%). They argued further, that it is the observance of existing regulations that causes the effective implementation of ICS and hence the enhancement of the financial management functions in the public sector. The findings also revealed the following factors in support of non-financial ICS; biometric system of checking in and out (16.0%), segregation of duties by schedules (20.4%), utilisation of CCTV cameras in strategic sites (14.2%), use of alarm systems (12.2%), utilisation of bullet proof money safes in offices (10.2%), and installation of security lights in strategic places (2.0%).

Respondents in Table 4, revealed that the use of a robust internal control system in managing the financial function in the public sector provides a number of advantages as follows; checking on financial errors and fraud (32.8%), enhancing goal attainment and achievement by the organisation (22.4%), safeguarding assets of the organisation (18.5%), enhancing efficiency and ensuring orderly organisation operations (10.0%) ensuring up to date management decision making policies (10.0%). There are however, some flaws that affect the implementation of internal control systems in many organisations as follows; inadequate training among employees, limited continuous professional development programs and uncoordinated performance management system.

The article argues that, the use of an elaborate and robust internal control systems in managing the financial function in the public sector brings on board a number of advantages as highlighted below; minimising errors and fraud in the organisation (32.8%), enhancing the company to achieve her goals in a timely manner (22.4%), safeguarding the organisation’s assets (18.5%), ensuring efficient and orderly operations in the organisation (16.3%) and ensuring that the organisation ‘s decision making policy is vibrant (10.0%). There are however, challenges and failures in the implementation of Internal Control Systems such as: inadequate professional training, inadequate professional development and inappropriate performance management strategies.

The article argues that; the design, development and implementation of ICS in any public body is crucial, timely and value adding, specifically the element of minimising of errors and fraud, is a fundamental pillar to the financial management function in all agencies. If ICS are in place the organisation is able to plan and budget well, provide the basic social services to the population, attract financial resources and above all motivate its staff to perform better.

In view of the findings and discussions unveiled in this paper, the following policy recommendations are made:

1) Both financial and non-financial ICSs need to be instituted at all spheres of management in public organisations local governments inclusive.

2) There is need to develop and implement a robust monitoring and evaluation framework to check on the implementation of ICSs in the public organisations. Currently minimal monitoring and evaluation mechanism is in place especially in the local governments and yet if internal control systems are widely embraced government would save lots of money lost in corruption tendencies. The monitoring and evaluation policy should have an elaborate home (Ministry) where all government entities are monitored and policed from to ensure compliance and adherence.

3) Institutions in charge of accountability such as Auditor General’s office, Inspectorate of Government, Public Accounts Committees (Parliament and Local governments) should work closely and hold regular (quarterly accountability review meetings) to chart progress.

The author has not declared any conflict of interests.

REFERENCES

|

Abubakari AR, Adam B (2018). Evaluating the Effects of Employee Motivation on Organizational Performance of XXX Limited. International Review of Management and Business Research 7(2):358-367.

Crossref

|

|

|

|

Adeyemi FK, Odunayo MO (2019). Internal Control System and Financial Accountability: An Investigation of Nigerian South-Western Public Sector. Acta Universitatis Danubius. Œconomica 15(1).

|

|

|

|

|

Bird RM (2015). "Improving tax administration in developing countries", in the Journal of Tax Management 1(1)23-45.

|

|

|

|

|

Brink N (2009). Theoretical Approach in Internal Control Systems: A conceptual framework and usuability of Internal Audit, in the International Journal of Economics Sciences and Applied Research 4(1):19-34.

|

|

|

|

|

Carr M, Chen M (2004). Globalisation, Social Exclusion and work: With special reference to informal employment: Institute of social development, University of Birmingham, UK.

Crossref

|

|

|

|

|

Eisenhardt KM (1989). Building theories from case study research. Academy of management review 14(4):532-550.

Crossref

|

|

|

|

|

Green FL (2003). Accountability: Putting Ethical Principles to work in your organization. Alert 17(3):1-15.

|

|

|

|

|

Kakuru J (2001). Basic Financial Management, MUBS, Kampala.

|

|

|

|

|

Local Government Finance and Accounting Regulations (2007). Ministry of Finance Planning and Economic development, Kampala Uganda.

|

|

|

|

|

Ndanyi MD (2019). Performance management and health service delivery in the local governments of Uganda, in the Journal of African Studies and Development 11(6):84-93.

Crossref

|

|

|

|

|

Ntongo V (2012). Internal Controls, Financial Accountability and service delivery in private health providers of Kampala Capital City. Unpublished MBA dissertation.

|

|

|

|

|

Pearce DG (2015). Urban management, destination management, and urban destination management: A comparative review with issues and examples from New Zealand. International Journal of Tourism Cities.

Crossref

|

|

|

|

|

Prawit (2008). Internal control systems in Teacher Training through school based program in participatory learning promotion.

|

|

|

|

|

Puttick VE (2001). The Principles and practice of Audit: Business and Economics. Revised Edition McGraw Hill High Education.

|

|

|

|

|

Walker PL, Shenkir WG, Barton TL (2003). ERM in practice. Internal Auditor 60(4):51-55.

|

|

|

|

|

Yang Y, Zhao T, Wang Y, Shi Z (2012). Research on impacts of population related factors on carbon emissions in Bejing from 1984 to 2012. Environmental Impact Assessment Review 55:45-53.

Crossref

|

|