Full Length Research Paper

ABSTRACT

The inauguration of Microfinance Banks (MFBs) in Nigeria in 2007 by the federal government was to provide finance to the low-income poor rural entrepreneurs, which is inclusive of the smallholder farmers located in rural areas that are often excluded from conventional banks’ financing. This paper systematically reviewed literature between January 2007 and April 2019 from the Web of Science and Scopus databases on the impact of MFBs on the development of smallholder agriculture in Nigeria. Using the Boolean search terms of (microfinance bank*), followed by (microfinance bank* AND farm*), then (microfinance bank* AND farm* AND Nigeria*), ten articles were identified. After eliminating duplicates, five articles were left. The articles were analysed using the VOS viewer, which generated three clusters with 14 terms, 60 links and total link strength of 90. The clusters are (i.) farmer; (ii.) credit; and (iii.) microfinance bank. This review found out that MFBs positively impacted the development of smallholder agriculture in Nigeria. However, constraints such as farmers’ location, level of awareness, interest rate, credit rationing and corruption among the MFB official constitutes setbacks in the availability and accessibility of credit. It is recommended that the governing body – the Central Bank of Nigeria and concerned microfinance banks, put more regulations in place to address these constraints. Also, more scientific study on the impact of MFB in smallholder agricultural development needs to be carried out.

Key words: Agricultural development, agricultural finance, microfinance banks, Nigeria, rural development, smallholders farmers, thematic analysis, VOS viewer.

INTRODUCTION

In Nigeria, the Microfinance banks (MFBs) have emerged as an important source of entrepreneurial finance at the grassroots level (Gul et al., 2017). The failure of the pre-existing smallholder finance schemes such as the Nigerian Agricultural and Co-operative Bank Limited (1972), Agricultural Credit Guarantee Scheme (1978), the Nigerian Agricultural Insurance Corporation (1987), the Peoples Bank of Nigeria (1992), and the Community Banks (1990) necessitated the establishment of the MFB. Perhaps, these failed schemes were anchored incomplete or wrong information and guided by improperly defined structures (Gul et al., 2017).

The MFB was inaugurated in 2007 in Nigeria and is borne with a focus to provide increased access of the poor and low-income earners to factors of production, especially credit (Central Bank of Nigeria, 2019). The pre-existing Community Banks were required to increase their paid-up capital from N5m to N20m. Today, around 882 MFBs licensed, governed and monitored by the Central Bank of Nigeria (CBN) and are in operation in various locations in the country. Generally, the MFBs main goal is to provide financial services to the poor who are traditionally not served by conventional financial institutions (Central Bank of Nigeria, 2019). Other services provided by the MFBs include savings, loans, domestic funds transfer, and other financial services that are needed by the economically active poor, micro, small and medium enterprises to conduct or expand their businesses as defined in the guideline for MFB in Nigeria. The MFBs are tasked with the responsibilities of providing financial services to the grassroots entrepreneurs among which are smallholder farmers. MFBs have provided financial support to several smallholder farmers, over the years; however, assessing the impact of the credit from the MFBs to the smallholder farmers is important. Prior research has focused largely on understanding and unraveling the extent to which MFBs finance smallholder farmers. Some of these studies suggest that MFBs faces challenges in this aspect. Some these challenges are regular changes in government policies, lack of requisite human capital, infrastructural inadequacies and socio-cultural misconceptions (Efobi et al., 2014; Uchenna et al., 2017). While other studies identified religious barrier, and lack of banking culture in the rural area are among the challenges faced MFBs (Ogujiuba et al., 2013). However, none of these studies has systematically reviewed all the published literature on MFBs credit provision to smallholder farmers in Nigeria.

Therefore, this study aims to carry out a systematic review of all relevant scientific literature from January 2007 until April 2019. This is done to gain insights into the activities of MFBs in providing credit to the smallholder farmers and the consequential impact on agricultural development on agriculture in Nigeria. The results of the articles were analysed using the VOS viewer.

METHODOLOGY

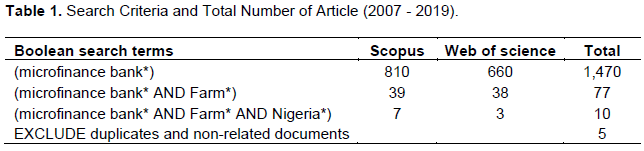

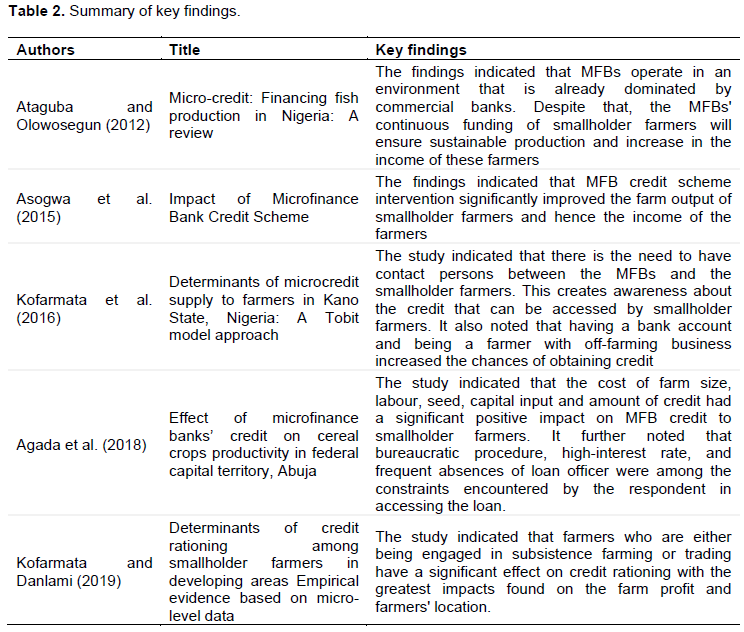

An online literature search was conducted using the databases – Scopus and Web of Science. These databases are collections of high quality, peer-reviewed articles and conference papers. Also, these two databases allow researchers to quickly see main journals, disciplines and authors and also provide tools for eliminating and selecting articles based on the purpose of the research (Wang and Waltman, 2016). The following Boolean search terms were defined based on the presented research questions and the outlined research boundaries. The terms (microfinance bank*) was used in the title, abstract or keywords with the publication year set as 2007 to 26 April 2019. This resulted in an initial sample of 1,470. The wildcard asterisk (*) was applied after a word stem to retrieve all articles that include words starting with this word stem (Creswell and Creswell, 2017). The publication year of 2007 to April 2019 was chosen as Microfinance Banking scheme as inaugurated in Nigeria in 2007 (Central Bank of Nigeria, 2019). With the publication year held constant, additional ‘inclusion’ term was introduced sequentially from (microfinance bank* and farm*) to (microfinance bank* and farm* and Nigeria*). This resulted in a total of ten samples – seven from Scopus and three from Web of Science databases. The review was set to include articles, conference proceeding papers, book chapters and reviews as the source of the most up-to-date knowledge in the field (López-Fernández et al., 2016). After the study selection had been done, the reference lists of the articles were reviewed to ensure that no relevant article not covered by the search criteria was missed. This resulted in no additional articles. After reading the abstracts and eliminating duplicated articles those articles that did not refer agricultural technology adoption by smallholder farmers in Africa, the final number of articles generated by the search criteria was 5 (Table 1). A list of these sample documents with some additional information was then recorded in an excel workbook (Table 2).

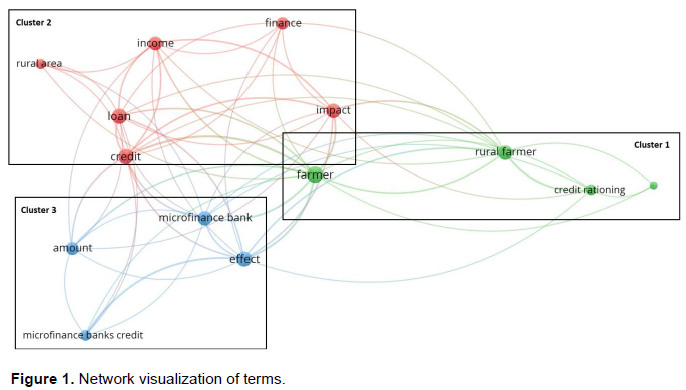

After identifying the articles, the bibliometric technique of co-words was used (Dias et al., 2019). The unit of analysis is the article, while the variables correspond to the terms included in the titles and abstracts of the resultant 60 articles. This technique is based on the analysis of the co-occurrences of terms. This allows the description of the state-of-the-art research, being produced at the end a mapping with the relations between the various terms and their association in thematic clusters (López-Fernández et al., 2016). The extraction of the terms was done using the software VOS Viewer. In using the VOS viewer, the term is understood as a sequence of names in text documents and the distance between two terms is calculated using the association strength (Perianes-Rodriguez et al., 2016).

In other words, as noted by Van Eck and Waltman (2014), The colours indicate clustering of terms in thematic clusters, and term with similar colours belong to the same cluster are more closely related than to other terms of different colours. Thus, terms with similar colours tend to co-occur with each other more than with terms of different colours. The binary counting method was chosen. The binary count is recommended as takes into consideration the presence or absence of a term (Van Eck et al., 2010). Therefore, the number of terms, as well as the number of occurrences of each term in all the documents, was considered.

RESULTS

The result identified 14 terms in 3 clusters with 60 links and a total link strength of 90 (Figure 1).

To analyse the main themes in the literature on microfinance banks and smallholder farmers in Nigeria, the co-words bibliometric technique was used on the title and abstracts of the 7 documents obtained. The extraction of the relevant terms was done using the VOS viewer application (Chavalarias and Cointet, 2013). This produced a map of the relationship between the different terms and their association in thematic clusters (Figure 1). Three clusters were identified from the review:farmer (Cluster 1); credit (Cluster 2); and microfinance bank (Cluster 3).

Cluster 1: Farmer

Studies have suggested that farmers, especially the smallholder farmers; in Nigeria are disadvantaged, vulnerable and make low incomes (Adelekan and Omotayo, 2017; Coker and Audu, 2015). However, these smallholder farmers are responsible for producing 98% of the food consumed (FAO, 2018). They also make up 80% of the farmers in Nigeria, while the remaining 20% are large scale farmers. The smallholder farmers are identified to cultivate around ≤5ha of farmland and also play important roles in employment creation (FAO, 2012). They are known to often practice mono-cropping, inter-cropping or a mixture of cropping and animal husbandry. They also extensively rely on family labour with minor hiring of external labour (World Bank, 2018). It is noted that smallholder farmers have the potential to increase their level of production if they have access to adequate resources. However, these farmers are constrained by access to input/output markets, land, capital, new technologies, among other several other resources.

Over the years, successive government has made deliberate efforts to improve the agricultural production contribution of the smallholder farmers. This led to the implementation of several policies and programmes over the years. MFBs was inaugurated in 2007 as an outcome of the development of several financial policies geared towards providing funds for the less privileged, and rural entrepreneurs.

Credit rationing as a term can be explained as the condition in which the demand for credit far exceeds its supply (Cenni et al., 2015). Even if the borrower is willing to pay higher interest rates, the credit is not available. This indicates the market imperfection of ‘credit’ and should not be confused cases where ‘credit’ is too expensive. It is worth noting that improvements in underwriting processes may have dramatically altered the practical impact of credit rationing in recent years. Some Nigerian smallholder farmers who are financially constrained and are willing to borrow more for economic reasons are unable to do so as the available credit needs to be rationed to cater for credit request presented by all the smallholder farmers and other entrepreneurs as well, hence, credit rationing (Kofarmata and Danlami, 2019). Using the discrete choice model, Kofarmata and Danlami (2019) study in Nigeria showed that smallholder farmers who are involved in subsistence farming or other trading activities have a significant effect on credit rationing. In other words, smallholder farmers who make regular profit from their farming activities can comfortably operate with credit rationed to them rather than credit-constrained smallholder farmers who required more than what is rationed to them. Furthermore, smallholder farmers who are committed to credit repayment are observed to have an impact on credit rationing (Cenni et al., 2015).

Credit has been identified as the backbone for any business, more so for agriculture which has traditionally been a primary occupation of the rural population in Nigeria (Boserup, 2017). Credit provision is one of the principal components of rural development which helps to attain rapid and sustainable growth of smallholder agriculture (Akinnagbe and Adonu, 2014). Credit is needed for farming operation purposes and consumption expenses. Credit plays an important role in the elimination of the financial constraints of smallholder farmers and increases their productivity.

Credit, loan and finance have different meaning however they are been used interchangeably in the literature of MFB in Nigeria as indicated in Cluster 2. In the various literature reviewed, it was observed that the term ‘credit’ was used interchangeably with loan and finance.

Agricultural credit has been a key missing link given that farm inputs and operation farm resources are costly and often out of the reach of the low-income smallholder farmers (CBN, 2018). For instance, Awotide et al. (2015) in their study on the impact of access to credit on agricultural productivity among smallholder cassava farmers in Nigeria revealed that access to credit is positively significant in the productivity of cassava. The study further recommended that credit institutions should consider boosting their credit services to smallholder farming households to guarantee that more households benefit from it.

Access to credit is a major problem of smallholder farmers; even then, many banks perceive agricultural credit as risky. The need for credit by smallholder farmers who are involved in agricultural production is often constrained by the MFBs’ lending terms and conditions, lack of information about the credit, time-lag between credit application and disbursement, insincerity and corruption of MFB credit officers, interest rate and collateral (Mattthew and Uchechukwu, 2014).

Microfinance is defined as the provision of a broad range of financial services including loans, savings, insurance, remittances and transfers to low-income households and their microenterprises (World Bank, 2018). In Nigeria, the institution of MFB has evolved from the People’s Bank of Nigeria (PBN) which was established in 1989 (CBN, 2018). PBN derives its philosophical ideology from the Grameen Bank of Bangladesh; a specialised financial institution inaugurated by the government to provide credit to the poor. PBN achieved considerable success, however in most cases they did not reach out to the people in the rural areas so that small-scale businesses they were supposed to support did not feel their presence (Agbaeze and Onwuka, 2014). The PBN operation was further restricted by a stipulated credit ceiling for each client, thus the need for the creation of another rural banking structure. Thus, in 1992, the Central Bank of Nigeria by Decree 46 established Community Banks (CBs). The CBs were created to promote rural development through the provision of banking and financial services, enhance rural productive activities and improve economics status of small-scale producers in total and urban areas (Ayadi et al., 2008). The determination of the CBN to provide a healthy banking environment necessitated a review of the capital bases of banks operation in Nigeria. Existing CBs in 2007 were mandated to increase their capital base and these reforms into MFBs (Central Bank of Nigeria, 2019). The action was justified with the lack of institutional capacity and weak capital base of existing CBs, the existence of huge un-served market and the need for increased savings opportunity (Central Bank of Nigeria, 2019).

In their study, Ataguba and Olowosegun (2012) observed that MFBs operates in an environment that is already dominated by commercial banks. However, the ability of the MFBs to provide the credit needed by the smallholder farmers, though in small amounts, makes them attractive to these set of farmers. The amount of credit accessible by the individual smallholder farmer is determined by several factors which include the repayment capacity of the smallholder farmer, amount, collateral among other several determinants factors (Central Bank of Nigeria, 2019).

DISCUSSION

In the present study, a systematic literature review of MFBs’ credit to smallholder farmers in Nigeria was carried out in the period between 2007 and 26 April 2019, covering only 5 articles from the Scopus and Web of Science databases. Based on the co-word bibliometric technique and cluster analysis, it was possible to group the literature into three major themes: farmer, credit and microfinance.

The research on MFBs’ contribution to the development of smallholder agriculture in Nigeria maintains an important focus on the credit provided to smallholder farmers. A review of the literature selected indicates that MFBs have a significant positive impact on smallholder agricultural development. However, the limited number of studies indicates that little attention is been paid to the relationship between MFBs and smallholder farmers. The establishment of the MFBs has been able to achieve its set goals but requires that more attention should be paid to the development of smallholder agriculture. The review further indicates that though the MFBs have credit provisions for agriculture, the smallholder farmers lack information about the availability of such credit (Kofarmata and Danlami, 2019). Also, due to the distance of the smallholder farmers to the MFBs, access of smallholder farmers to information is limited. To this end, Kofarmata et al. (2016) suggest that MFBs employ relationship staff that will sell the available credit to the smallholder farmers.

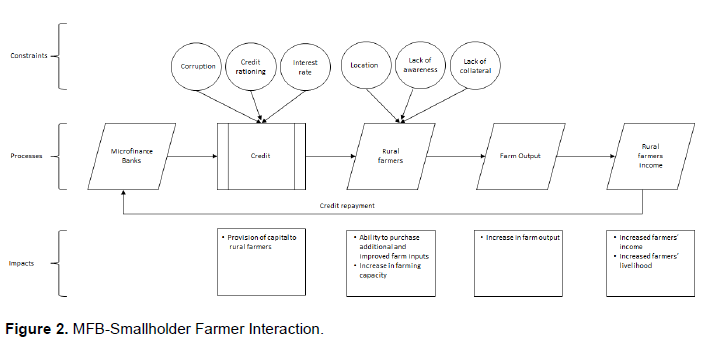

One of the main objectives of the MFBs is to be able to provide credit to rural entrepreneurs among which are smallholder farmers. Assessing the impact of this credit on smallholder agriculture is important in knowing if the MFBs roles in assisting the smallholder farmers are achieved, and to what extent this role is been played (Kofarmata et al., 2016, Agbaeze and Onwuka, 2014). The amount of credit rationed among the smallholder farmer is determined by several factors major of which is the availability of the credit and repayment attitude of the smallholder farmer (Ataguba and Olowosegun, 2012). From the reviewed literature, the diagrammatic interaction between the MFB and smallholder farmers can be presented as in Figure 2. Although the articles reviewed focused on the effects of MFBs on agricultural development in the rural area, another effect of the MFB is the increase in the farm income of the smallholder farmers. This ultimately impacts on the livelihood of the smallholder farmers.

CONCLUSION

Smallholder farmers in Nigeria constrained by the non-availability of a credit institution in the rural areas and lack of access to credit. MFBs have been able to address the issue of credit provision to smallholder farmers. However, there exist constraints in the availability and accessibility of credit in the MFB, and research suggests that the CBN should put in place measures to address them.

Though the objective of the credit to smallholder farmers is to increase their production level, this will

cause an increase in their income and ultimately their livelihood. Given an increase in the income of the smallholder farmer, it will be expected that their credit request will reduce and whither over time, and this will give room for more new farmers to benefit from the MFB credits. More efforts should also be directed at improving the credit rationed to the smallholder agricultural sector. This will increase the availability of credit that can be accessed by smallholder farmers.

Further studies are also required in each of the clusters considering that some terms relevant to microfinance banking in other countries such as ‘gender’ (Nanayakkara, 2012) were missing from the selected literature. New studies must assess issues besides these three main thematic areas identified in the literature and comprehensively understand the causal linkages between the terms in each cluster.

This study has some limitations as it relies only on articles from the Scopus and Web of Science databases and the bibliometric analysis was for a defined range of publication period. The option for another database or range of publication period may also change some of the observations and conclusions obtained.

CONFLICTS OF INTERESTS

The authors have not declared any conflicts of interests.

REFERENCES

|

Adelekan YA, Omotayo AO (2017). Linkage between rural non-farm income and agricultural productivity in Nigeria: A Tobit-two-stage least square regression approach. The Journal of Developing Areas 51(3):317-333. |

|

|

Agada GO, Adebayo C, Agada SI (2018). Effect of microfinance bank's credit on cereal crops productivity in federal capital territory, Abuja. International Journal of Scientific and Technology Research. |

|

|

Agbaeze EK, Onwuka I (2014). Microfinance Banks and Rural Development: The Nigeria Experience. International Journal of Rural Management. |

|

|

Akinnagbe OM, Adonu AU (2014). Rural farmers sources and use of credit in Nsukka local government area of Enugu state, Nigeria. Asian Journal of Agricultural Research 8(4):195-203. |

|

|

Asogwa BC, Ater PI, Yakubu SM (2015). Impact of microfinance bank credit scheme. Banking, Finance, and Accounting: Concepts, Methodologies, Tools, and Applications. |

|

|

Ataguba GA, Olowosegun OM (2012). Micro-credit: Financing fish production in Nigeria: A review. Journal of Fisheries and Aquatic Science. |

|

|

Ayadi OF, Hyman LM, Williams J (2008). The Role Of Community Banks In Economic Development: A Nigerian Case Study. Savings and Development 32(2):159-173. |

|

|

Boserup E (2017). The conditions of agricultural growth: The economics of agrarian change under population pressure. Routledge. |

|

|

Cenni S, Monferrà S, Salotti V, Sangiorgi M, Torluccio G (2015). Credit rationing and relationship lending. Does firm size matter? Journal of Banking and Finance 53:249-265. |

|

|

Central Bank of Nigeria (2019). Microfinance. Central Bank of Nigeria. Retrieved 25 April |

|

|

Chavalarias D, Cointet JP (2013). Phylomemetic patterns in science evolution-the rise and fall of scientific fields. PloS ONE 8(2):e54847. |

|

|

Coker A, Audu M (2015). Agricultural micro-credit repayment performance: Evidence from Minna Microfinance Bank, Nigeria. African Journal of Agricultural Research 10(9):877-885. |

|

|

Creswell JW, Creswell JD (2017). Research design: Qualitative, quantitative, and mixed methods approaches. Sage publications. |

|

|

Dias CSL, Rodrigues RG, Ferreira JJ (2019, 2019/01/01/). What's new in the research on agricultural entrepreneurship? Journal of Rural Studies 65:99-115. |

|

|

Efobi U, Beecroft I, Osabuohien E (2014). Access to and use of bank services in Nigeria: Micro-econometric evidence. Review of Development Finance 4(2):104-114. |

|

|

FAO (2012). Sustainable Pathways: Smallholder and Family Farmers. |

|

|

FAO (2018). Small Family Farms Country Factsheet. Food and Agriculture Organization of the United Nations. Retrieved 27 April |

|

|

Gul FA, Podder J, Shahriar AZM (2017). Performance of Microfinance Institutions: Does Government Ideology Matter? World Development 100:1-15. |

|

|

Nanayakkara G (2012). Gender, operational efficiency, population density and the performance of mirofinancing institutions. Pacific Accounting Review 24(3):314-333. |

|

|

Kofarmata YI, Danlami AH (2019). Determinants of credit rationing among rural farmers in developing areas Empirical evidence based on micro level data. Agricultural Finance Review 79(2):158-173. |

|

|

Kofarmata YI, Hassan S, Applanaidu SD (2016). Determinants of microcredit supply to farmers in Kano State, Nigeria: A Tobit model approach. Actual Problems of Economics. |

|

|

López-Fernández MC, Serrano-Bedia AM, Pérez-Pérez M (2016). Entrepreneurship and Family Firm Research: A Bibliometric Analysis of An Emerging Field. Journal of Small Business Management 54(2):622-639. |

|

|

Ogujiuba K, Jumare F, Stiegler N (2013). Challenges of microfinance access in Nigeria: Implications for entrepreneurship development. Mediterranean Journal of Social Sciences 4(6):611-611. |

|

|

Perianes-Rodriguez A, Waltman L, Van Eck NJ (2016). Constructing bibliometric networks: A comparison between full and fractional counting. Journal of Informetrics 10(4):1178-1195. |

|

|

Uchenna OL, Adedayo EO, Ahmed A, Isibor A (2017). Corporate Governance and Financial Sustainability of Microfinance Institutions in Nigeria. Sustainable Economic Growth, Education Excellence, and Innovation Management through Vision 2020. |

|

|

Van Eck NJ, Waltman L (2014). Visualizing bibliometric networks. In Measuring scholarly impact (pp. 285-320). Springer. |

|

|

Van Eck NJ, Waltman L, Dekker R, van den Berg J (2010). A comparison of two techniques for bibliometric mapping: Multidimensional scaling and VOS. Journal of the American Society for Information Science and Technology 61(12):2405-2416. |

|

|

Wang Q, Waltman L (2016). Large-scale analysis of the accuracy of the journal classification systems of Web of Science and Scopus. Journal of Informetrics 10(2):347-364. |

|

|

World Bank (2018). Nigeria: Distribution of Gross Domestic Product GDP Across Economics Sectors from 2006 to 2016. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0