Full Length Research Paper

ABSTRACT

The purpose of this study is to provide empirical evidence on the effect of institutional quality on stock market performance. In order to evaluate the effect of institutional quality on stock market performance, Calderon Rossell models have been estimated using generalized method of moment’s technique. A panel data of 41 emerging countries for the period 1996 to 2011 is used to estimate the results. The results suggest that institutional quality has a positive and significant influence on stock market performance. Policy makers in emerging countries must follow a parallel policy agenda of improving the quality of their institutions as well as education. These are paramount to the performance of stock markets performance in emerging countries.

Key words: institutional quality, stock market, emerging economies, macroeconomic variables.

INTRODUCTION

Gani and Ngassam (2008) examine the links between institutional factors and stock market performance in a sample of eight Asian countries with developing as well as mature stock markets. These are enough to conclude that economic growth, technology, rule of law and political stability affect capital market performance while poor institutional quality negatively affect it. The results support the proposition that institutional quality is an integral part of enhancing the performance of stock markets in a country hence institutional quality matters for stock market performance.

Hearn and Piesse (2010) and Adjasi and Biekpe (2006) finding support the fact the stock market performance relate positively with economic performance. For instance, Kemboi and Taru (2012) and Yartey (2008) established that confidence in investments is enhanced with improvement in property right. It is believed that a country with strong institutional structures leads to institutional efficiency and productivity. An improvement in institutional quality leads to higher gross domestic product (GDP) which implies more money for investment. Countries with strong institutional quality have more liquid stock markets. These articles reviewed very little literature of emerging economies on the effect of institutional quality on stock market performance of emerging economies, using a panel data.

This study outlines the main determinants of capital market performance for an emerging economy. This study contributes to literature by confirming the evidence on the relationship between dimensions of institutional quality such as the efficiency of the government, the political climate, the level of corruption and the regulatory authority and performance of stock markets.

Emerging economies

As we can observe from Appendix 1, stock market performance indicators exhibit a considerable variability across countries, according to the stock market capitalization ratio. The top ten countries in terms of mean stock market capitalization for the period under review are South Africa, Malaysia, Jamaica, Jordan, Chile, Zimbabwe, Saudi Arabia, Thailand, Philippines and India in that order. The countries with lowest stock market capitalization are Ecuador, Slovak Republic, Bangladesh, Paraguay and least Uruguay. As we can see stock market performance in terms of total value trade as percentage of GDP, South Africa move from the first to third position with Saudi Arabia occupying the first position from our sample. Market capitalization does not relate with size of a country. Over the period under study China with the largest economy has smaller average market capitalization than Hong Kong whiles South Africa market capitalization is almost the same as China despite their smaller GDP and population. Again even though Nigeria has a larger economy than Ghana, Ghana is ahead of Nigeria in terms stock market capitalization as a measure of performance of the capital market.

Performance of stock markets in emerging economies does not imply that even the most advanced stock markets are mature. With developing economies, considerable part of their total market capitalization is accounted by trading in few stocks. Most stocks on these markets often have informational and disclosure deficiencies hence weakness in the transparency of transactions of these markets. For this reason Tirole (1991) and El-Erian and Kumar (1995) established that share prices in emerging economies are considerably more volatile than advance markets. In spite of this high volatility, most corporations have benefited from stock market in less developed economies for instance Indian stock market.

Market liquidity is one the measures of stock market performance. Market Liquidity is ability for investors to buy and sell shares. We measure the activity of the stock market using total value traded as a share of GDP, which gives the value of stock transactions relative to the size of the economy. According to the work of Levine and Zervos (1998), this measure is used to gauge market liquidity. This is because it measures trading relative to economic activity. Of the 41 countries Pakistan, Saudi Arabia, Bangladesh, Turkey and India turnout to be countries with liquidity as shown in Figure 1. The liquidity in these countries were recorded around the late 90’s and the early part of 2000 were most of these countries have undertaken successful financial liberalization (Figure 1).

Institutional quality

Institutional quality can broadly be explained as guidelines to govern and direct the formation of expectations of human beings by one another. Conventional growth models tend to focus largely on the role of physical and human capital in explaining the growth performance within and across time and countries. These have a lot to do with the cost and the ease of doing business. In particular, it has been found that there is a major role that is played by institutions in influencing the effects of either human or physical capital or both in influencing the growth path of economies. It is a common knowledge that disparity in financial market performance and economic performance across countries is due to institutional factors the various countries. This view is also captured in Adam Smith work, The Wealth of Nations.

Many researchers like Williamson (1995), Acemoglu et al. (2001), Aron (2000), Collier (2006) and North (1990) established that institutional factors play vital role in economic performance of countries. Researchers like Collier (2006), World Bank (2007), IMF (2003) and Ndulu (2006) have confirmed the assertion by attributing the poor performance of countries in Africa to poor institutional factors. Subramanian and Roy (2001) and Sobhee (2009) on the other hand also confirmed it by saying that good institutional factors explain the impressive track record Mauritius. To operationalize the definition of institutional factors we say it pertains to elements that have to be in place to encourage an enabling business environment. Knack and Keeffer (1995), Hall and Jones (1999), Acemoglu et al. (2002) and La Porta, et al. (1998) all concluded that key determinants of economic development are institutional factors.

The encounter between neoclassical economics and developing societies served to reveal the institutional underpinnings of market economies. Clearly defined system of regulatory apparatus prevents worst fraud. In other words incentives would not work in the absence of adequate institutions, hence market need to be supported by non-market institutions in order to perform well. Example of this point is the Russia experience in price reforms and privatization in the absence of a supportive legal, regulatory and political apparatus. Other examples are Asian financial crisis which has shown that allowing financial liberalization to run ahead of financial regulation is an invitation to disaster, and also that of Latin America. The question therefore is that do institutions matter and how does one acquire them?

LITERATURE REVIEW

It is argued that weak institutional control mechanisms may expose investor’s wealth (Khanna, 2009; La Porta et al., 1998; World Bank, 2005). For this reason Hearn and Piesse (2010) concluded that this situation is more prevalent in developing economies where weak regulatory institutions and poor systems of corporate governance are common feature.

Governments throughout the world have become aware of the importance of corporate governance for the efficient performance of the stock market. In the last few years’ corporate governance has become an important issue throughout the world. A market that has sound institutional qualities proves to be very efficient. An efficient market in turn attracts more investment and increased transaction thus increasing market capitalization and liquidity.

Although economies are becoming increasingly global, firms with international operations are still subject to the principles and practice of national corporate governance. It has been rightfully seen that a firm’s valuation does not only depend on the profitability or the growth prospects embedded in its business model, but also on the effectiveness of control mechanisms, which ensure that investors’ funds are not wasted in value decreasing projects. Investors’ however are encouraged to invest in sound, orderly and transparent markets. Numerous recent studies on transition economies have emphasized the relevance of law, judicial efficiency and the regulatory framework (Lombardo and Pagano, 1999; Pistor, 1999, 2000; Coffee, 1999; Hooper, 2009; La. Porta et al., 1997, 1999).

Empirical evidence suggests that better legal protection of outside shareholders is associated with easier access to external funds in the form of either equity or debt (La. Porta et al., 1997), higher valuation of listed firms (La. Porta et al., (2002), and lower private benefits of control (Zingales, 1994; Nenova, 1999). Moreover, it has been shown that the enforcement of law and regulations has much higher explanatory power for the level of equity and credit market development than the quality of the law on the books (Pistor et al., 2000; Coffee, 1999).

Edison (2003) found that institutions have a statistically significant influence on economic performance, substantially increasing the level of per capita GDP. These findings hold whether institutional quality is measured by broad-based indicators (such as an aggregate of various perceptions of public sector governance) or by more specific measures (for example, the extent of property rights protection or application of the rule of law). The findings are also consistent for all measures of institutions.

These results suggest that economic outcomes could be substantially improved hence stock market performance if developing countries strengthened the quality of their institutions. In other words, the results indicate that institutions have a strong and significant impact on per capita GDP growth.

METHODOLOGY

To understand the economic importance of the stock market in our sample of 41 countries, we examine the stock market capitalization ratio. The choice of countries and times series data for this article rests on the availability of data. Data for this article are from World Development Indicator (WDI) and Global Finance and Development (GEF). The stock market capitalization ratio is defined as the value of domestic equities traded on the stock market relative to GDP. Institutional quality is modeled by assuming that country believes there is probability of institutional quality not leading to stock market performance. The probability a country places on the likelihood that the institutional quality of a country will not yield returns is a function of institutional quality in the country. Using multiple indicators to measure institutional quality raises the problem multicolinearity. To develop the model, we take from existence causal factors and then concentrate on how to choose and optimally combine the factors to inference on the unobserved underlying process. By this we get indicators that we believe is closest to the unobserved factors. Kaufmann et al. (1990) used a variant of this approach to combine factors. We assume that each observed score for a particular indicator is a linear function of unobserved institutional quality and a disturbance term, which is assumed to be uncorrelated across indicators. The variance of each factor shows how information that factor is with respect to unobserved institutional quality.

Empirical models

Using Cadeleron-Rossell (1990) behavioral structural model economic growth and stock market liquidity are considered the main determinants of stock market performance. We use market capitalization to measure stock market performance. In this study, we modified Cadeleron-Rossell model by introducing institutional quality. Cadeleron-Rossell (1991) revealed that macroeconomic are important determinants of stock market performance. The general econometric model used in the study is as follows:

Where Y is stock market capitalization relative to GDP, α, is the unobserved country specific fixed effect, and  is the white noise. M is a matrix of macroeconomic variables made up of GDP per capita, credit to the private sector as a percentage of GDP and its square, gross domestic investment as a percentage of GDP, stock market value traded as a percentage of GDP, private capital flow as a percentage of GDP, foreign direct investment as a percentage of GDP, macroeconomic stability (measured by current inflation and the real interest rate), and gross domestic savings. Cadeleron-Rossell (1991) also included one lag of the dependent variable as one of the right hand side variables because they believed that stock market performance is a dynamic concept. P and E are institutional quality variable and secondary school enrolment respectively.

is the white noise. M is a matrix of macroeconomic variables made up of GDP per capita, credit to the private sector as a percentage of GDP and its square, gross domestic investment as a percentage of GDP, stock market value traded as a percentage of GDP, private capital flow as a percentage of GDP, foreign direct investment as a percentage of GDP, macroeconomic stability (measured by current inflation and the real interest rate), and gross domestic savings. Cadeleron-Rossell (1991) also included one lag of the dependent variable as one of the right hand side variables because they believed that stock market performance is a dynamic concept. P and E are institutional quality variable and secondary school enrolment respectively.

To avoid multicollinearity problems (1) becomes (2) below. Panel regressions are estimated to test the importance of institutional quality on stock market performance.

Where P represents institutional quality of country i, and  is the standard error of institutional quality for country i.

is the standard error of institutional quality for country i.

Estimation technique

Arellano and Bond (1991) used a dynamic panel data estimator based on Generalized Method of Moments (GMM) which is instrumental variable estimator that optimally exploits restrictions implied by the dynamic panel growth model. GMM can be estimated using the levels or the first differences of the variables. Arellano and Bond (1991) proposed two estimators—one step and two step estimators—with the two step being the optimal estimator. The practice is to estimate using two step estimator but base hypothesis tests on the one step estimator’s statistics.

However, before proceeding with the GMM the following identifying assumption is necessary. We assume that there is no second order serial correlation in the first differences of the error term. The consistency of the GMM estimator requires that this condition be satisfied. Given the construction of the instruments as lagged variables the presence of second order serial correlation will render such instruments invalid. The specification tests for the GMM estimator are the Sargan test of over identifying restrictions and the test of lack of residual serial correlation. The Sargan test is based on the sample analog of the moment conditions used in the estimation process and evaluates the validity of the set of instruments and, therefore, determines the validity of the assumptions of predeterminacy, endogeneity, and exogeneity. Since in this case the residuals examined are those of the regressions in differences, first order serial correlation is expected by construction and thus only second and higher order serial correlation is a sign of misspecification.

In the case of time-invariant country characteristics (fixed effects) correlating with the explanatory variables, we use the first difference GMM to transform (3) into

Bringing in the specific variables in the matrix M and P, the (3) now becomes general empirical form as shown below;

Expected signs are:

Where P a vector institutional quality; CC, VA, RL, RQ, PS and GEFF

Descriptive analysis

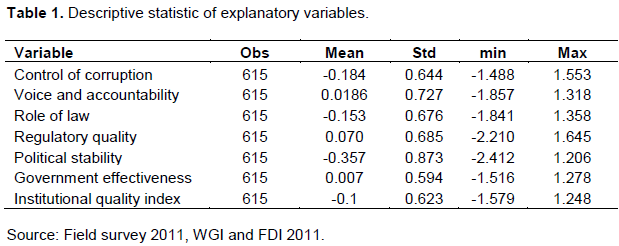

Due to lack of data for institutional quality for periods before 1996, we limit this paper to cover 1996 to 2011 (Table 1). The extremity of the institutional quality indicator range is approximately -2.5 and 2.5 with lower values representative of poorer institutional quality scores. Differences across countries in the margins of error associated with governance estimates are due to cross-country differences in the number of sources in which a country appears and or the differences in the precision of the sources in which each country appears. Of 41 emerging economies studied, countries like Uruguay, Slovenia, South Africa, Slovenia, Romania, Slovakia Rep, Poland, Panama, Malaysia, Jordan, Hungary, Czech Republic, Costa Rica, Chile, Bulgaria, Brazil and Botswana on the average are classified as countries with good institutional quality. On the other hand twenty five (25) of countries were cited as countries with poor institutional quality because on the average were negative for these countries. Differences across countries in the margins of error associated with voice and accountability are due to cross-country differences and differences in the precision of the sources in which each country appears. Of all the elements of institutional quality voice and accountability, regulatory quality and then government effectiveness had positive mean values for the period under consideration. In other words for the countries sampled for this article, institutional quality in relation to these areas were strong on the average. The element of institutional quality with the highest standard deviation is political stability. There exists high correlation for each of the governance indicators for the entire period as a whole, and similarly for each individual period. The CC indicator and the RL indicator have the highest correlation amongst indicators for all periods.

Voice and accountability

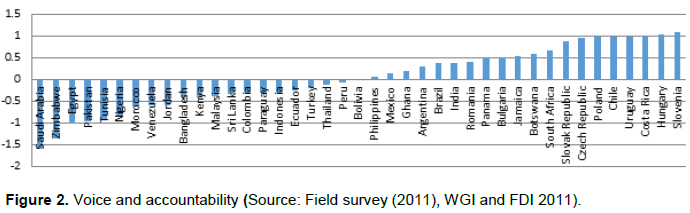

Voice and accountability covers degree of involvement of citizens in government and in the policy making process. There are different types such as moral, administrative, political, managerial, market, legal, constituency, and professional accountability (Jabbra and Dwivedi, 1989). To enhance the quality of this indicator, civil liberties, political rights should be not only properly and systematically secured, but also significantly improved. Media should be able to publish or broadcast stories of their choice without fear of censorship. Countries with higher scores of WGI in voice and accountability have scores of positive 2.5 while those in lower scores have under negative 2.5 Figure 2 shows the mean value for the various countries sampled for this article. From Figure 2 slightly about 50% of emerging economies sampled have good voice and accountability. Slovenia came out as the country with good voice and accountability with Saudi Arabia recorded as the country with worse voice and accountability. For African countries in the sampled South Africa, Botswana and Ghana came out with good voice and accountability index.

Political stability and absence of violence (PV)

This indicator addresses those factors which undermine political stability such as conflicts of ethnic, religious, and regional nature, violent actions by underground political organizations, violent social conflicts, and external public security. Also included are assessments of fractionalization of the political spectrum and the power of these factions, fractionalization by language, ethnic or religious groups and the power of these factions and restrictive measures required to retain power. Societal conflict involving demonstrations, strikes, and street violence are also considered in this indicator, as well as the military coup risk. Major insurgency and rebellion, political terrorism, political assassination, major urban riots, armed conflict, and state of emergency or martial law are also major determinants of this indicator.

Internal conflict like political violence and its influence on governance is assessed in this measure and external conflict measure is also employed to assess both the risk to the incumbent government and to inward investment. Government stability is measured for the government’s ability to carry out its declared programs, and its ability to stay in office. Ethnic tensions component measures the degree of tension within a country attributable to racial, national, or language divisions.

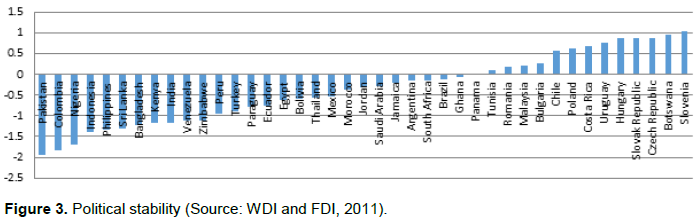

Figure 3 shows that 34% of emerging economies sampled have good political stability index with 66% having bad political stability record. Slovenia and Botswana are the two emerging economies with the highest recorded of good political stability and Pakistan, Colombia and Nigeria had the worst record for political stability respectively. Ghana and South Africa also had bad political stability record.

Government effectiveness (GE)

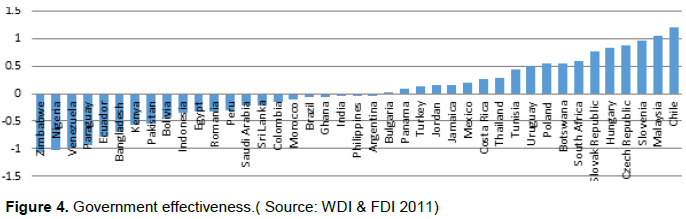

Government effectiveness measures the quality of public services and policy formulation and implementation, and thus indicates the credibility of the government's commitment to such policies. This covers government citizen relations, quality of the supply of public goods and services, and capacity of the political authorities. This variable being negative means there is low quality of bureaucracy with excessive bureaucracy or red tape, government ineffectiveness with low personnel quality, institutional failure which deteriorates government capacity to cope with national problems as a result of institutional rigidity that reduces the economic growth. The better the bureaucracy the quicker decisions are made and the more easily foreign investors can go about their business. Figure 4 also show that 46% of emerging economies sampled for this article have positive government effectiveness. Chile and Malaysia have the highest positive value with Zimbabwe and Nigeria having the highest absolute negative value.

Regulatory quality (RQ)

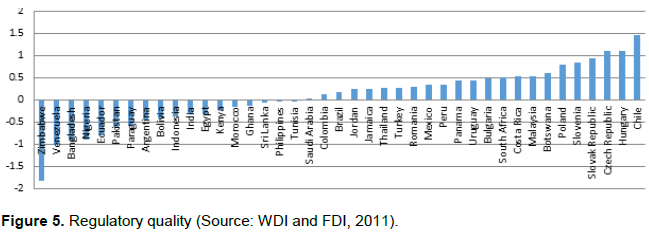

The regulatory quality indicator of WGI defines the capacity for government to formulate and implement sound policies and regulations that permit and promote private sector development. It covers the concept of business start-up formalities set by government, the difference between government-regulated administrative prices and self-controlled market prices, the ease of market entry for new firms, and the competition regulation arrangements between or among businesses. In developing countries particularly, the rural region regulations on local financial services, local businesses, and agricultural produce market may determine the quality of this indicator as well. Other factors affecting regulatory quality indicators also include financial institutions' transparency, public sector contracts open to foreign bidders, anti-protectionism measures to other countries, and reduction of subsidies to specific industries. As portrayed in Figure 5, 56% of the emerging economies countries sampled had good regulatory quality and 44% bad. Chile, Hurgary, Czech Republic, Slovenia, Poland and Botswana were identified as countries with good regulatory quality respectively. On the other hand Zimbabwe, Venezuela, Bangladesh and Nigeria were tagged with bad regulatory quality.

Rule of law (RL)

There different interpretation given to rule of law due to the ethical nature of the word. This paper we are using the meaning given by legal profession as impartial judiciary, the right to fair and public trial without undue delay, equality of all before the law. These are fundamental of rule of law (IBA, 2009).

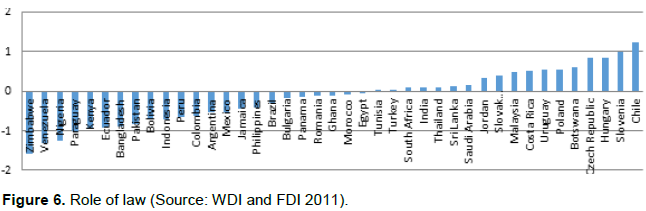

However, in Asian traditional and cultural contexts, they view good governance as rule by leaders who are benevolent and virtuous. Chu et al. (2008) indicated that throughout East Asia, only South Korea, Japan, and Hong Kong have societies that are robustly committed to a law bound state. On the other hand, Thi (2008) concluded that rule of law in Thailand, Cambodia, and most of Asia is weak or nonexistent. The term ‘rule of law’ is the enforceability of government, direct financial fraud, money laundering and organized crime, losses and costs of crime, quality of police, the independence of the judiciary from political influences of members of government, etc. Of the total sample 44% of the emerging economies sampled were tagged with practicing rule of law whiles the rest had bad records in relation to rule of law as depicted in Figure 6. Once again Chile and Slovenia were on top whiles Zimbabwe and Venezuela were at the tale of end of countries with bad record on rule of law.

Control of corruption (CC)

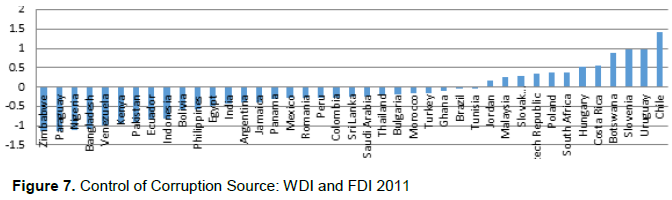

Corruption can be explained in many different ways. Transparency International (2007) and Chinhamo and Shumba (2007) explained corruption as the abuse of public power, office, or resources by government officials or employees for personal gain. The control of corruption indicator is measured by the frequency of corruption, cronyism, and government efforts to tackle corruption. 26% of emerging economies sampled were tagged as having good record on control of corruption. Brazil and Tunisia were neutral in relations to whether good or bad. As Chile, Uruguay, Slovenia and Botswana are ranked high in terms of good policies to control corruption, Zimbabwe, Paraguay and Nigeria were rank high for poor control of corruption as shown in Figure 7.

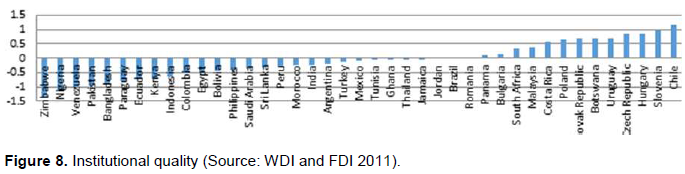

Institutional quality

This is a composite index computed by row average of component of institutional quality computed by the researcher. The data used to compute the composite index is from World Development Indicator (WDI). Figure 8 below shows how good an emerging economy is term of institutional quality. A value of 2.5 means very good and negative 2.5 means bad institutional quality. Of the emerging economies sampled for this article 39% of them on the average are classified as having good institutional quality with the remaining 71% having bad institutional quality. Out of 39% countries like Chile, Slovenia, Hurgary, Czech Republic, Urguay and Botswana came on the top respectively in relation to good institutional quality. Zimbabwe, Nigeria, Venezuela, Pakistan and Bangladesh were also identified as emerging economies with bad institutional quality as depicted in Figure 8.

Statistical analysis

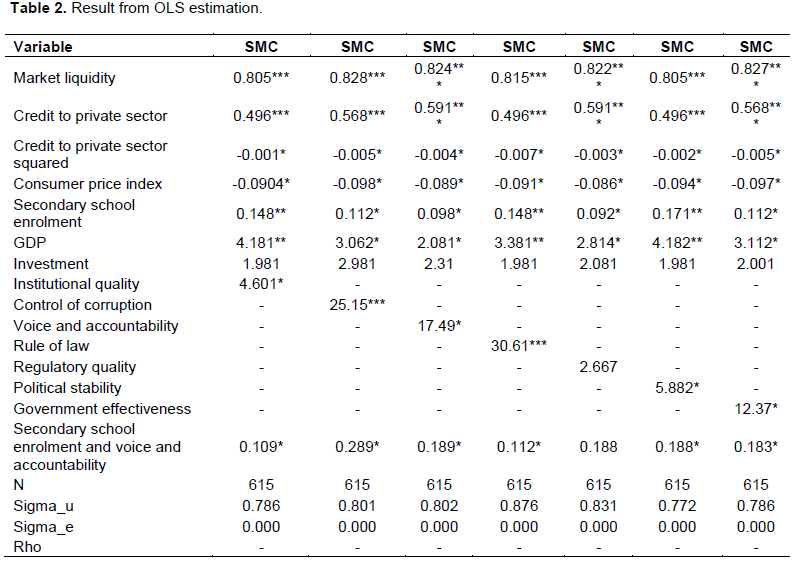

We examine the impact of institutional variables on stock market performance using different estimation techniques. Table 2 presents the results of pooled ordinary least square (OLS) estimate. We include as regressors institutional quality. The high correlation among the governance indicators motivates the use of separate regressions for each governance variable to avoid multicollinearity problems. When the explanatory variables are highly correlated, it becomes difficult to disentangle the separate effects of each of the explanatory variables on the dependent variable and would lead to substantial increases in the standard errors of the coefficient estimates of the governance indicators. Statistical inference based on these standard errors would be problematic. The use of each governance indicator separately for each regression overcomes these problems.

Column 1 in Table 2 is the baseline regression model where we used a composite index that takes into consideration all elements of institutional quality. The results show market liquidity, credit to private sector (banking sector development), GDP (economic growth), secondary school enrolment and institutional quality are all significant and the signs positive, indicating a percentage point increase in these variables will bring about an improvement in stock market performance. Investment in this case tends out insignificant. On the other hand consumer price index and square of credit to private sector are negative and significant indicating an inverse relationship with stock market performance. The variable of interest secondary school enrolment and institutional quality are all positive and significant as expected at 10 percent significance level indicating that a percentage point increase in secondary school enrolment and institutional quality increases stock market performance by 0.148 and 4.601 respectively. This outcome indicates that institutional environment is a good predictor of stock market performance in emerging economies. If we simply look at the coefficient on secondary school enrolment (E), we will incorrectly conclude that a percentage point increase secondary school enrolment will lead to 0.481 improvements in stock market performance. But this coefficient supposedly measures the effect when institutional quality is zero, which is not interesting because the minimum institutional quality from this sample is not even zero. Also since the p-value for the F test of this joint hypothesis is 0.003, so we certainly reject the null hypothesis of ,  Using the mean value of institutional quality we compute

Using the mean value of institutional quality we compute  . Because secondary school enrolment is measured as percentage, it means that a 1% percentage point increase in secondary school enrolment increase stock market capitalization of emerging economies by 0.506 standard deviations from the mean stock market capitalization. This finding is consistent with the results Winful et al. (2013).

. Because secondary school enrolment is measured as percentage, it means that a 1% percentage point increase in secondary school enrolment increase stock market capitalization of emerging economies by 0.506 standard deviations from the mean stock market capitalization. This finding is consistent with the results Winful et al. (2013).

The problem with institutional quality is that it tells us very little about which aspect of institutional quality attention should be directed towards. Also because of multicollinearity problem, we introduce the elements of institutional quality one at time to determine its effect on stock market performance. To remedy this deficiency, the article studies the effect of the components of the index of institution quality on stock market performance. The results are show in table 2 below from the second column onwards. In column two of Table 2 we replace the composite index of institutional quality with control of corruption to determine its effect on stock market performance. The results shows that control of corruption have significant effect on stock market performance. With effect of secondary school enrolment on corruption we determine the partial effect of control of corruption on stock market performance. The indication here is that as emerging economies put in place measures to reduce control of corruption they affect positively on stock markets of emerging economies. The sign is as expected. We fail to reject the hypothesis that there is positive effect between control of corruption and stock market performance of emerging economies. The ability of the judiciary to enforce contractual rights of shareholders impinges on the likelihood of managerial expropriation and ultimately the profitability of firms. All other dimensions of institutional quality with exception of regulatory quality are having positive coefficients and have an estimated coefficient that obtains statistical significance at the 10% level as shown in Table 2 below. Legal systems supportive of investor protections tend to increase the amount of funds risk-averse investors are willing to channel towards firms. Aggarwal et al. (2002) find that fund managers invest less in countries with poor legal environments and low corporate governance standards. This is supported by the higher shareholder returns in countries with better governance systems. If the quality of legal institutions is considered a sub-set of the quality of governance, then the results are consistent with Lonbardo and Pagano (2000) but contrary to Demirguc-Kunt and Maksimovic (1998).

However, the latter authors failed to control for global risk factors in their analysis, which could explain the variation in the results. If institutional quality influences transaction costs associated with firm operations, then it would be expected that the excess return on equity would be higher in countries which rate highly on institutional structure. Reduction in transaction costs would enlarge the profitable project opportunity set available to firms and thus the demand for equity. This, in connection with reduced agency costs due to better institutional enforcement increases return to shareholders.

We introduce an interactive term to allow as determine the partial effect of secondary school enrolment with respect to the dimensions of institutional quality. This is because of influence of institutional quality on secondary school enrolment. The result shows explicitly that there is statistically significant in all interaction between secondary school enrolment with respect to various dimensions institutional quality shown in Table 2.

AIC analysis confirms that the interaction term should be included in the model. The adjusted–R2 for the OLS estimates shown in column one to seven respectively indicate the percent of systematic variations explained by the variables in the models. The F-values for the various models estimates are significant at the less than 1 percent level, indicating a significant linear relationship between the dependent variable (SMC) and the independent variables taken together.

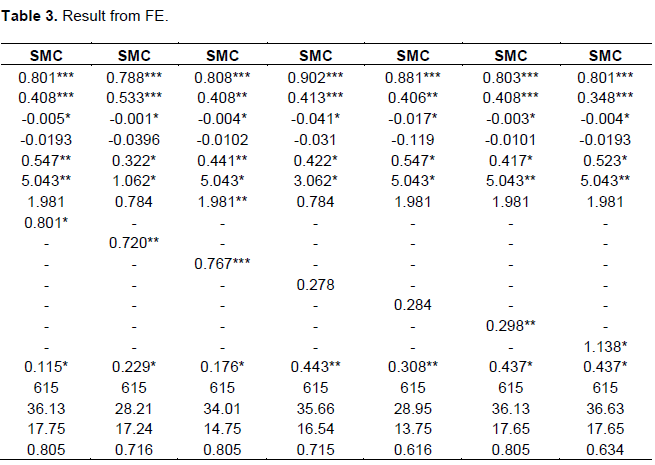

Table 3 below presents different assumptions about the correlation structure of the errors which is used to

analysis panel data the fixed effects and random effects. With the FE we explore the relationship between predictor and outcome variables with countries. Each emerging economies has its own individual characteristics that may or may not influence the predictor variables. Using FE the assume is that something within the individual emerging economies may bias the predictor or outcome variables and we need to control for this. The other assumption is that time-invariant characteristics are unique to individual emerging economies and should not be correlated with other emerging economies characteristics. An effect of the features of fixed-effects technique is that they cannot be used to investigate time-invariant causes of the dependent variables.

Using RE we assume that the error terms are correlated. The rationale behind random effects model is that, unlike the FE model, the variation across emerging economies is assumed to be random and uncorrelated with the independent variables included in the model. A comparison of the consistent FE with the efficient RE estimates using the Hausman specification test, rejects the RE estimates at p<0.05 in favor of the fixed-effects model. The results from random effect are not reported in this article.

The results of the FE are as shown in Table 3. The result confirms the pooled OLS results on economic growth, market liquidity, and credit to private sector, consumer price index, financial market performance and secondary school enrolment in Table 2. The composite index for institutional quality is again significant. As we considered the various dimensions of institutional quality using FE technique, rule of law and regulatory quality tend out to be insignificant in explaining stock market performance.

Surprisingly, when voice and accountability is introduced investment tends out to significant in explaining stock market performance as shown in column three. F test of less than 1% for the columns of Table 3 implies that models are okay and all the explanatory variables are different than zero. A test for heteroskedasticity of a p-value of 0.000 for the seven estimates using fixed effect rejected the null hypothesis of homoskedasticity. To correct the problem of heteroskedasticity we used robust fixed effects. The robust fixed effect results are not different from Table 3. The robust fixed effect results are not shown in this article. Lagram-Multiplier test of serial correlation fail to reject null hypothesis and we conclude that the data does not have first-order autocorrelation. Clustering the data by countries did not give different results from fixed effect.

Ramsey RESET test using powers of the fitted values of the dependent variable Stock Market Capitalization reject the null hypothesis that the model has no omitted variables at all the traditional significance levels. The article failed to rejects the null hypothesis for the simple

reason that the lag of the dependent variable which is expected to explain variation in dependent variable is missing in the model. According to Nickel (1981) introducing lag of the dependent variable into the model give rise to dynamic panel bias. The difficulty in applying OLS to this empirical problem is that lag of SMC is correlated with the fixed effects in the error term. Correlation between a regressors and the error violates an assumption necessary for the consistency of OLS.

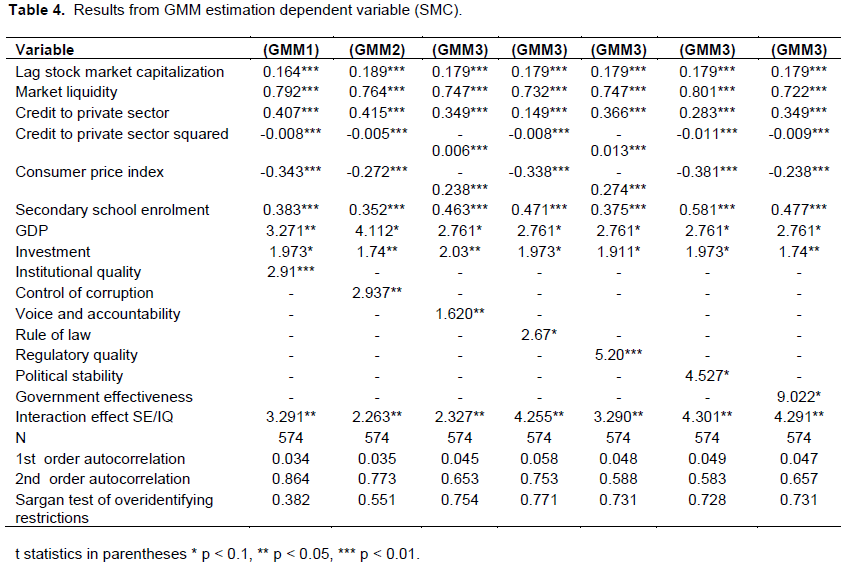

To improve efficiency of our results from the previous techniques discussed above we introduce the GMM technique and the outputs are as shown in Table 4. Using GMM estimation technique we address the endogenous problem by instrumenting the lag of the dependent variable and any other similarly endogenous variables with variables thought uncorrelated with the fixed effects. The first column of Table 4 is the baseline regression control for variables such as; market liquidity, credit to private sector, financial sector performance, consumer price index, GDP, investment, secondary school enrolment and institutional quality.

The results as shown in Table 4 column one below, shows that explanatory variables are positive and significant with the exception of credit to private sector squared and consumer price index which tend out to be negative and significance and signs as expected. Investment is insignificant but with the expected sign.

The implication of the results is that percentage point increases in market liquidity increases stock market capitalization by 0.792. The sign is as expected because although profitable investments require long run commitment to capital, savers prefer not to relinquish control of their savings for long periods. Liquid equity markets ease this tension by providing assets to savers that are easily liquidated at any time, while simultaneously allowing firms permanent access to capital that are raised through equity issues there by increasing the market value of firms. Market liquidity boosts investors’ confidence. A negative coefficient of -0.008 for credit to private sector squared is expected since money market and capital market tend to substitute each other as financing vehicle for investors. That is very high levels of banking sector development have negative impact on growth of stock market because stock markets and banks tend to substitute as financing vehicles. It was also established that consumer price index influence stock market performance of emerging economies negatively as expected at significance level of 1%. This is because high inflation rate does not encourage long term financing for which the capital market seeks to address. These results do not contradiction the findings of Ali (2011) and Yartey (2008) as reviewed in this article.

Secondary school enrolment and economic growth has significant positive influence on stock market performance. An increase in the secondary school enrolment brings about 0.383 and 3.271 changes in stock market capitalization at 1% and 5% significant levels respectively. We fail to reject the null hypothesis that economic growth and secondary school enrolment have no significant effect on stock market performance. It is also established that composite institutional quality has 2.91 influences on stock market performance also at 1% significance level. The result suggests that policies that seek to improve institutional quality are important for stock market performance in emerging economies. Interestingly, investment which is not significant using the OLS and fixed effect tends significant from column one to seven in the Table 4. The null hypothesis that the population moment condition are correct is not rejected because Sargan p=0.382 is greater than 0.05 as shown in column one of Table 4. For the test of autocorrelation in the errors, we except to reject at order 1 but not at higher order for us to concluded that the errors are serially uncorrelated. AR(1) of (0.034) which is less than 0.05 and AR(2) of 0.864 implies that the error are not serially correlated. The F-value (which is a measure of the overall goodness of fit of the regression) of 0.000 is highly significant at 1% level thus the hypothesis of a significant linear relationship between dependent and independent variables is validated as a group.

The problem with the concept of institutional quality is that it tells us very little about the influence of specific components of institutional quality on stock market performance and hence which aspect of institutional quality should policy maker pay attention to if stock markets are to perform well. Yartey (2007) for instance, find that these components are important for stock market performance in African countries. To resolve this deficiency the article investigates the effects of the components of the index of institutional quality on stock market performance. This exercise is done in column 2 to 7 of Table 4 as shown. We examine the effect of all the six components of institutional quality on stock market performance one at time. Results show that all the six components have positive significant influence on stock market performance in emerging economies. The signs are as expected. The article suggests that development of good policies to improve on components of institutional quality is an important determinants of stock market performance in emerging economies. The finding also affirms that secondary school enrolment has positive significant influence of 0.352, 0.352, 0.463, 0.471, 0.375, 0.581 and 0.477 respectively from column one to seven respectively on stock market performance at different significant level. Increased investment in human capital is expected to affect income per capita positively. That is emerging economies with better educated work force or populace can easily adopt new technologies and innovate new technology domestically which leads to wealth maximization of firms thereby increasing their market value.

We also find that market liquidity, credit to private sector, credit to private sector squared, economic growth, consumer price index and lagged of the dependent variable to be significant and also with the expected signs for all the seven columns. It is interest to note that by accounting for dynamic nature of the data and solving the endogeneity problem all components of institutional quality which were insignificant in Table 3 tend out significant with the right signs.

The implication is that ability of institutional quality to enforce contractual rights of shareholders impinges on the likelihood of managerial expropriation and ultimately the profitability of firms. Legal systems supportive of investor protections tend to increase the amount of funds risk-averse investors are willing to channel towards firms. Managers invest less in countries with poor legal environments and low corporate governance standards. The payoffs from institutional quality improvements include not only larger stock markets, but also greater integration with world capital markets via the influx of capital. Better governance environments increases returns to shareholders by reducing both transaction costs and agency costs.

Himmelberg et al. (2004) stated that lack of investor protection forces company insiders to hold higher fractions of the equity of the firms they manage. These high holdings subject insiders to greater levels of idiosyncratic risk, which in turn increases the risk premium and, therefore, the marginal cost of capital. The results of Lombardo and Pagano (2002) confirm the view of Shleifer (1999), who emphasizes that, in order to reap the benefits from market-oriented reforms, policy makers in emerging economies must make sure that a fair level playing field is established, so that investors can focus their attention on exploiting growth opportunities without fearing for their property rights.

Autocorrelation 1 (AR 1) of 0.035 which is less than 0.05 and AR (2) of 0.773 imply that the errors are not serially correlated for column two. The F-value (which is a measure of the overall goodness of fit of the regression) of 0.000 is highly significant at 1% level thus the hypothesis of a significant linear relationship between dependent and independent variables is validated as a group. Sargan test of over identifying restrictions of 0.551 supports the results. The same applies to the other columns of Table 4.

The inclusion of an interaction between secondary school enrolment and components of institutional quality is due to the fact that strong institutional quality creates the environment for more of the populace to have education. We are interested in the effects of secondary school enrolment on stock market performance in emerging economies so we need to determine the partial effect of secondary enrolment on stock market performance. If we simply look at the coefficient on secondary school enrolment (E), we will incorrectly conclude that a percentage point increase in secondary school enrolment will lead to 0.471 improvements in stock market performance for instance column four. But this coefficient supposedly measures the effect when institutional quality is zero, which is not interesting because the minimum value of institutional quality from this sample is not even zero. Also since the p-value for the F test of this joint hypothesis is 0.003, so we certainly reject the null hypothesis of , Using the mean value of the various components of institutional, we compute the partial effect. For column two for instance we used the mean of control of corruption to compute the partial effect of secondary school enrolment on stock market performance.

Because secondary school enrolment is measured as percentage, it means that a 1% percentage point increase in secondary school enrolment increase stock market capitalization of emerging economies by 0.387 standard deviations from the mean stock market capitalization.

To determine the partial effect of secondary school enrolment on SMC for column two for instance we replace the interaction variable with  We then run the regression which gives as the new coefficient on secondary school enrolment (E), the estimated effect at CC=0.186, along with its standard error. Running this new regression gives the standard error of 2.66 as 0.07, which yields t= 7.93. Therefore at the average CC, we conclude that secondary school enrolment (E) has a statistically significant positive effect on Stock Market Capitalization of emerging economies. The sign is as expected. The sign for education is positive because school enrolment has been on the increase since early part 1990 in most emerging economies under study. The trend has been so because government contribution to education for emerging economies has been on the ascendency over the last 10 decade. Most countries have introduced free and compulsory basic education and this have increased enrolment in many countries.

We then run the regression which gives as the new coefficient on secondary school enrolment (E), the estimated effect at CC=0.186, along with its standard error. Running this new regression gives the standard error of 2.66 as 0.07, which yields t= 7.93. Therefore at the average CC, we conclude that secondary school enrolment (E) has a statistically significant positive effect on Stock Market Capitalization of emerging economies. The sign is as expected. The sign for education is positive because school enrolment has been on the increase since early part 1990 in most emerging economies under study. The trend has been so because government contribution to education for emerging economies has been on the ascendency over the last 10 decade. Most countries have introduced free and compulsory basic education and this have increased enrolment in many countries.

The results also established that market liquidity, economic growth, lagged dependent variable and credit to private sector have positive and significance influence on stock market capitalization. Credit to private sector squared and macroeconomic stability variable (consumer price index) on the other hand have negative and significance effect on stock market capitalization. The reasons that can be attributed to this inverse relation between consumer price index and stock market performance is that multinational corporations are set up after studying the macroeconomics of the host country. Any change in the macroeconomics of a country will affect a multinational corporation. For a multinational corporation to grow and thrive, the macroeconomics of the host country should be stable. The host country is like an anchor which gives a corporation the stability at its roots. When the corporation spreads its wings over developing nations, it is a known factor that the macroeconomics in a developing nation will be volatile. Hence stability of Macroeconomics in the host country is extremely important for a multinational corporation.

Stable low inflation (consumer price index) encourages higher investment which is a determinant of improved productivity and non-price competitiveness. Control of inflation helps to main price competitiveness for exporters and domestic businesses facing competition from imports. Stability breeds higher levels of consumer and business confidence. The maintenance of steady growth and price stability helps to keep short term and long term interest rates low, important in reducing the debt-servicing costs of people with mortgages and businesses with loans to repay. A stable real economy helps to anchor stable expectations and this can act as an incentive for an economy to attract inflows of foreign direct investment.

Market liquidity concerns such as why liquidity changes over time, why large trades move prices up or down, and why these price changes are subsequently reversed, and why some traders willingly disclose their intended trades while others hide them. These issues have been established to have positive and significant effect on stock market performance of emerging economies.

All six component of institutional quality had the right signs. According to the International Monetary Fund (IMF, 2007), Institutional quality is important for stock market performance because efficient and accountable institutions tend to broaden appeal and confidence in equity investment. Equity investment thus becomes gradually more attractive as political risk is resolved over time. Therefore, the development of good quality institutions can affect the attractiveness of equity investment and lead to stock market performance. This is because institutional quality supportive of investor protections tend to increase the amount of funds risk-averse investors are willing to channel towards firms. Managers invest less in countries with poor legal environments and low corporate governance standards. The payoffs from institutional quality improvements include not only larger stock markets, but also greater integration with world capital markets via the influx of capital. Better governance environments increases returns to shareholders by reducing both transaction costs and agency costs. All these go to improve on the performance of stock market. Policy makers in emerging economies must make sure that a fair level playing field is established, so that investors can focus their attention on exploiting growth opportunities without fearing for their property rights.

The p-value of Sargan test of overidentifying restrictions 0.731 and first and second order of autocorrelation of 0.048 and 0.631 support the results as consistent and efficient. The Sargan test for the null hypothesis of valid specification is used to test whether these instruments are valid. The test failed to reject the null hypothesis in all the regressions implying that the instruments are valid. This indicates that the model has high explanatory and predictive power. The Wald test for joint significance of the dependent variables strongly rejected the null hypothesis that the coefficients on all the variables are jointly equal to zero for all the models shown in Table 4.

CONCLUSION

It has been established that components of institutional quality also have positive influence on stock market performance of emerging economies. By this findings policies tailored to reduce corruption, government effectiveness, political stability, voice and accountability, regulatory quality and rule of law should be taken seriously and encouraged. The payoffs from strong institutional quality include not only larger stock markets, but also greater integration with world capital markets via the influx of capital. Better governance environments increases returns to shareholders by reducing both transaction costs and agency costs. All these go to improve on the performance of stock market. This study findings have important policy implications for emerging economies that development of good quality institutions can affect the attractiveness of equity investment and lead to stock market performance. Also emerging economies should improve their institutional framework because strong institutional quality reduces political risk which is an important factor in investment decision. Policy makers must sure that a fair level playing field is established, so that investors can focus their attention on exploiting growth opportunities without fearing for their property rights.

Policy implications

The findings of this article have important policy implications for emerging economies. The new phase of developmental economics has achieved much in helping us understand this unexplored channel of causation since Bagehot (1873).

The result suggests that policy makers in emerging economies must not concentrate all their efforts on technological innovation, investment in physical capital but rather emerging economies must follow a parallel policy agenda of improving the quality of their institutions and Labor force. In addition, these policies should focus on the institutional qualities that affect stock market performance most such as rule of law, government effectiveness, political instability, and voice and accountability. This implies that adopting market-friendly policies, providing an effective judiciary system, making contracts enforceable by law, building political stability, providing effective government service, and strengthening civil liberty and political rights should be the major policy agendas of these countries.

In situations where these factors were not significant in explaining stock market performance it suggests that emerging economies can set aside those variables at least in the short run but in the long run they have to work on them. Technical inefficiency is not the only channel through which bad governance may translate into poor performance of the stock market. Head of states should spearhead promulgation of fiscal responsibility act along the lines of Financial Administration Act of United States of America that would require the government to commit itself to fiscal discipline and provide for transparency and impose sanctions. To hence political accountability, we need to establish political institutions which could hold the government accountable, as pertains in developed countries. Civil society should assume the lead role in amplifying the voice of the people and demanding greater domestic accountability, but said governments and donors should support this by ensuring that more relevant information is provided, and is in a format and language people can understand.

It is obviously costly to build institutions from scratch when imported blueprints can serve just as well. Much of the legislation establishing a SEC like watchdog agency for securities markets, for example, can be borrowed wholesale from those countries that have already learned how to regulate these markets by their own trial and error. The same goes perhaps for an anti-trust agency, a financial supervisory agency, a central bank, and many other governmental functions. One can always learn from the institutional arrangements prevailing elsewhere even if they are inappropriate or cannot be transplanted. Some societies can go further by adopting institutions that cut deeper.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Acemoglu D (1998). Why Do New Technologies Complement Skills? Directed Technical Change and Wage Inequality. Q. J. Econ. 113(4):1055-1090. |

|

|

Acemoglu D, Johnson S, Robinson JA (2001). An African Success Story: Botswana, MIT Department of Economics Working Paper No. 01-37. |

|

|

Acemoglu D, Angrist J (2001). How Large are the Social Returns to Education: Evidence from Compulsory Schooling Laws" in B. Bernanke and K. Rogoff (eds.) NBER Macroeconomic Annual, (2000) (Cambridge, MA: The MIT Press) 9-59. |

|

|

Acemoglu D (2002). Directed Technical Change. Rev. Econ. Stud. 69(4):781-810. |

|

|

Acemoglu D, Aghion P, Zilibotti F (2006). Distance to Frontier, Selection and Economic Growth. J. the European Econ. Assoc. 4(1):37-74. |

|

|

Calderon-Rossell RJ (1991). The Determinants of Stock Market Growth," in S. Ghon, Rhee and Rosita P. Chang (eds.), Pacific Basin Capital Markets Research Proceeding of the Second Annual Pacific |

|

|

Coffee J (1999). Privatization and corporate governance: the lessons from securities market failure. Columbia Law School Center for Law and Economics Studies Working Paper 158, New York, NY. |

|

|

Demirguc-Kunt A, Maksimovic V (1998). Law, finance and firm growth. J. Financ. 53:2107-2137. |

|

|

Edison H (2003). Testing the Links; How strong are the links between institutional quality and economic performance, J. Financ. Dev. 40(2):35-37. |

|

|

Gani A, Ngassam C (2008). Effect of institutional factors on stock market development in Asia, Am. J. Finance Account. 1:2 |

|

|

Hearn B, Piesse J (2010). Barriers to the Development of Small Stock Markets: A Case Study of Swaziland and Mozambique. J. Int. Dev. 22:1018-1037. |

|

|

Himmelberg C, Hubbard G, Love I (2004). Investor protection, ownership, and the cost of capital. World Bank Policy Research Working Paper 2834, Washington, DC. Hooper V, Sim |

|

|

AB, Uppal A (2009). Governance and stock market performance, J. Econ. Syst. 33:93-116. |

|

|

International Finance Cooperation (1991) IFC Fact book, New York : IFC International Finance Cooperation (1996) IFC Fact book, New York : IFC. |

|

|

Johnson S, Shleifer A (1999). Coase vs. the Coasians. NBER Working Paper 7447, Cambridge, MA. |

|

|

Kemboi JK, Taru DK (2012). Macroeconomic Determinants of Stock Market Development in Emerging Markets: Evidence from Kenya, Research J. Financ. Account. 3(5):57-68. |

|

|

Knack S, Keefer P (1995). Institutions and economic performance: La Porta R, Lopez -de Silanes F, Andrei S, Robert V (1998). Law and Finance, J. Polit. Econ. 106:1113-1155. |

|

|

La Porta R, Lopez-de Silanes F, Andrei S, Robert V (1997). Legal Determinants of External Finance, J. Financ. 52:1131-1150. |

|

|

Levine R (1996). Stock Markets: A Spur to Economic Growth, Finance & Development, International Monetary Institute, Washington, D.C. |

|

|

Levine R, Zervos S (1998). Stock Markets, Banks, and Economic Growth, Am. Econ. Rev. 88:536-558. |

|

|

Levine R, Zervos S (1996). Stock Market Development and Long-run Growth, Policy Research Working Paper 1582. |

|

|

Lombardo D (2000). Is there a cost to poor institutions? SIEPR Discussion Paper 00-019, Stanford, CA. |

|

|

Lombardo D, Pagano M (2000). Legal determinants of the return on equity. CSEF Discussion Paper 24, Naples. |

|

|

Lombardo D, Pagano M (2002). Law and equity markets: a simple model. CSEF Discussion Paper 25, Naples. MA. |

|

|

North DC (1995). The Adam Smith Address: Economic Theory in a Dynamic Economic World." Business Economics: 7. |

|

|

North D (1994). Economic performance through time. Am. Econ. Rev. 84:359-368. |

|

|

Sala-i-Martin X (1997). I Just Ran Four Million Regressions." National Bureau of Economic Research (Cambridge, MA) Working Paper No. 6252, November 1997. |

|

|

Sobhee SK (2009). Do Better Institutions Help to Shrink Income Inequality in Developing Economies? Evidence from Latin America and Sub-Saharan Africa.", Paper presented at the PEGnet (Poverty and Economic Growth network) Conference, The Hague, Netherlands, 3-4 Sept. |

|

|

Subramanian A, Roy D (2001). Who can explain the Mauritian Miracle: Meade, Romer, Sachs or Rodrik, IMF working paper. 7:3. |

|

|

World Development Indicator (2011), World Bank Group, World Bank, |

|

|

William E, Ross L (1997). Africa's Growth Tragedy: Policies And Ethnic Divisions, Quarterly Journal of Economics. |

|

|

Winful EC, Kumi-Koranteng P, Owusu-Mensah M (2013). Investment Education" on Stock Market Performance: Case of GSE, J. Contemp. Manage. ID: 1929-0128-2013-04-29-17 |

|

|

Yartey CA (2008). Determinants of Stock Market Development in Emerging Economies: Is South Africa Different? IMF working Paper-WP/08/32 Washington, International Monetary Fund. |

|

|

Yartey CA, Adjasi CK (2007). Stock Market Development in Sub Saharan Africa: Critical Issues and Challenges, IMF Working Paper, WP/07/209. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0