Full Length Research Paper

ABSTRACT

The SMEs form a vibrant pillar of the Mauritian economy through their important contribution to Gross Domestic Product (GDP) growth and socio-economic development. SMEs are recognized for their significance and their resilience in responding to fast changing conditions, even in times of the economic downturn. This paper aims to address financial illiteracy among Mauritian SMEs by proposing an integrated financial assistance strategy for small firms in view of enhancing the financial sustainability, growth and development of their business entities. The study adopts a dual methodology to address the study objectives. Two focus groups were held as part of the qualitative approach to quantify the level of financial literacy and to ultimately assess the extent of the problem. The paper also highlights the specific gaps and needs in terms of financial education and contributes to designing the most adapted solutions in terms of training and IT to respond to these needs. The research findings confirm the lack of financial knowledge among the Mauritian SMEs and the extent of their IT readiness. The survey has also revealed that although there is some degree of awareness about the most common sources of finance, the cost implications are not always fully understood. This lack of awareness on the mode of finance and the conditions apply thereto point to the existing financial education gap in the Mauritian SME sector. This further reinforces the need to implement an integrated financial platform.

Key words: SMEs, financial literacy, financial assistance strategy, Mauritius.

INTRODUCTION

The importance of Small Medium Enterprises (SMEs) to the economy is long established. Despite continuous efforts by governments and concerned institutions to provide an adequate structure for SMEs, information asymmetries with regards to access to finance, skills and global value chain, remain a challenge. Indeed, this issue has been recognised and there is ongoing research regarding the set-up of an e-platform to disseminate pertinent information to SMEs. The reference point in this context would be The European Small Business Portal

(European Commission, 2009) which provides financial assistance and information about market access and support programmes, albeit. However, proactive measures to assist SMEs are lacking in many developing countries including Mauritius.

SMEs in Mauritius covers diverse economic sectors. They make up an approximate 40% of the GDP share and absorb nearly 54.6% of employees in the job market (Ministry of Business Enterprise and Cooperatives (MoBEC), 2016). Given its potential, the Mauritian government is working towards making the latter a vibrant pillar of the economy. The actual target is to increase the SMEs’ GDP contribution to 52% and to aim an increased export market penetration by 2026. However, this goal can only be materialised once the major barriers have been removed. The current situation is sluggish with 175 of registered SMEs being out of business for the period 2014/2015; this could be an underestimate given that 62% of SMEs are not registered (Statistics Mauritius, 2016). As highlighted by the 10-Year Master plan, the main reasons for closing down are: (1) financial difficulties; (2) lack of capacity; (3) inadequate management; (4) bureaucracy and (5) lack of financial knowledge.

It is thus important to design appropriate financial assistance for SMEs. Existing measures in Mauritius taken by banks include financial schemes, training and ICT programmes such as ‘Business Boost’ -provides high bandwidth access to SMEs. Despite these aforementioned supports, SMEs continue to struggle. This paper identifies the lack of financial knowledge as the missing link between the existing support providers and SME’s growth potential. Against this backdrop, the forward-looking strategy as proposed by the 10-year Master Plan (2016) is to encourage innovation and build an IT Enabler E-platform for Mauritian SMEs. This paper follows the same strategy and builds on The European Small Business Portal and other African countries’ experiences. The focus is primarily on the financial knowledge gap among SMEs in Mauritius. The aim is to tailor an interactive E-platform which will make the latter more financially literate. This will eventually ensure increased efficiency, productivity and growth.

A dual methodology is used to answer the main research objective. The starting point of this research is to assess the existing IT infrastructure available to SMEs. A micro-level study through the administration of survey and focus groups was used to discern the current financial awareness and knowledge of SMEs. The focus groups and surveys served as an identification measure of the financial education gap. A similar approach was also used to quantify the IT readiness of the entrepreneurs. These preliminary researches provide the foundation of the proposed e-platform.

The remaining parts of this paper are organised as follows. First is a discussion of literature on the financial literacy of SMEs with a focus on the country experiences on the usage of existing e-platform. This is followed by the employed detailed methodology which is then linked to the analysis. The analysis part sheds light on the current situation of SMEs pertaining to financial knowledge and IT readiness to embrace digital tools. Given the nature of the study, the technical feasibility in this research provides information on the technical aspects of the proposed solution, namely; requirement analysis, system analysis and design and prototype developments. Finally, the study is wrapped up with the main findings and discussion, along with implications of the study.

LITERATURE REVIEW

Policymakers have come to see SMEs as a medium for inclusive growth and employment opportunities. The literature regarding its socio-economic benefits is well-documented. However, given the context of this paper, the relevant strand of the literature is narrowed to the issues SMEs face. The consensus across studies is that SMEs continue to struggle despite several support schemes. Lack of access to external finance (Pissarides et al., 2003); technology, innovation and expertise (Lal and Peedoly, 2006) regulatory and tax constraints feature as the most pertinent issues.

Financial literacy

Indeed, financing remains an important factor when it comes to business continuity (Nunoo and Andoh, 2012). However, the influence of financial literacy is often overlooked. Hall’s (1992) findings show that the inability to understand accounting concepts and system significantly increases the chance of going out of business. Intuitively, the lack of financial literacy is tied with other complications with regards to seeking credit, detecting wasteful cash flows-to list a few. This aspect is well embedded in the definition of financial literacy as proposed by Noctor et al. (1992). They defined financial literacy as “the ability to make informed judgements and to take effective decisions regarding the use and management of money”. It can thus be understood that financial literacy dictates attitude and the financial habit of an individual (Beal and Delpachitra, 2003; Mandell and Klein, 2009).

This theoretical argument is in line with the findings of Nalukenge and Tauringana (2013) where they argue that SMEs who are financially literate make more informed decisions, have knowledge of financial products that have high yield and are willing to leverage credit for future growth. It is thus fair to argue that a commendable level of financial literacy is a driver of growth for any enterprise and in this context, SMEs. Beal and Delpachitra (2003) agrees to the said argument and extended the benefit of financial literacy to wealth creation. Karadag (2017) further built on this concept factored for the educational level of small business entrepreneurs, and found that knowledge of financial management remains vital for firm performance. Having well-founded courses on business operations and management systems are hence necessary. Chang et al. (2014) tested for the efficiency of similar programmes and confirmed that the latter enhanced the problem-solving skills of entrepreneurs and managers. This is also corroborated by the findings of Staniewski (2016).

SME and the economy

The literature accrues significant attention on how SMEs form a pivotal aspect in the economy. Schumpeter’s (1912) work forms the basis of SMEs as economic drivers through his concept of creative destruction. The idea of small entrepreneurs being innovative and pushing incumbent firms to invest in new technologies and to be forward looking is indeed observed across industries. In the process of ensuring efficiency and non-complacency in big firms, SMEs implicitly drives investment; hence the positive link between SME development and growth (Beck et al., 2005). Kuratko (2006) further argued that SMEs played as revival tools following economic downturns in both developed and developing economies. When employment opportunity in the SME sector is factored in, Birch (1979) found that the latter is a significant contributor to employment level. Biggs et al. (1998) observed a similar finding in Sub-Saharan African countries. However, an a priori claim cannot be made regarding SMEs having a positive and significant impact on job creation. Few studies (Snodgrass and Biggs, 1996; Dunne et al., 1989) contested the view that small firms increase employment opportunities. It is noteworthy that in the Mauritian context, the economic benefits of the SME sector are well observed. A report by Statistics Mauritius (2013) supports significant employment growth generated by the SME sector by 34% between 2007 and 2013. It was further mentioned that value added by the sector is approximately 62% of gross output. The main takeout from this aspect of the literature is that the positive association between SMEs, growth and employment is country-specific. Although few studies reported insignificant relationship between SME development and growth; they do not dismiss efforts to invest and assist to the needs on SMEs in a country.

Needs and challenges

The literature also recognises that SMEs need certain preconditions to sustain its survival. The main constraints highlighted across studies relate to access to finance (Pissarides et al., 2003) and training facilities, existing infrastructure, technology and institutional support framework (Lal and Peedoly, 2006). When this issue is narrowed to the Mauritian context, high production costs unmatched by productivity gains, logistics constraints, lack of capabilities in ancillary services, design development, a narrow base for technology diffusion and absorption, altogether constitute major hurdles. The SME sector continues to be constrained by shortage of finance and financial instruments, high rate of interest and high rentals, the short reimbursement period, and a lack of commercial and industrial space (Lal and Peedoly, 2006). Kadiri’s (2012) paper highlighted a similar scenario in the Nigerian SME sector and portrayed lack of finance as a barrier to growth.

An important gap identified in the literature on SME development particularly in the African context, is that the linkages between institutions and SME entrepreneurship are yet to be adequately explored and understood. Institutions are often argued to play a critical role in the promotion of inclusive growth (Bartlett et al., 2005). However, there are still important institutional and policy related hurdles to overcome in order to harness the full potential of SMEs in terms of poverty reduction, social protection and empowerment. This argument agrees with the findings of Bartlett et al. (2005). These issues become even more pertinent in the context of the recent global economic crisis and its adverse impacts upon SMEs, with women and youth girls being the worst hit given their reliance on employment in the SME sector (ILO, 2010). Moreover, Migiro and Wallis (2006) found that information on sources of finance needs to be more readily available to SMEs and their advisors through an SME portal. Such reform is underway in the Philippines (Guzman et al., 2015). Also, the barriers to the utilisation and adoption of IT in SMEs can broadly be classified as internal which exist within the organisation, and include organisational culture, lack of resources and the level of training of employees. Yet, studies state that these barriers can be overcome only if there is a concerted effort among SMEs (Kapurubandara and Lawson, 2006). As proposed by Kadiri (2012), there is a need to integrate SMEs activities with financial institutions. This would arguably serve to bring coherence and build a good synergy between SMEs and the concerned institutions.

There is thus a need to invest in intellectual capital. As such, an integrated financial information system to educate the SMEs is deemed as an appropriate strategy. Ives and Mason (1990) proclaimed that ICT offers exciting opportunities to revitalise customer service by moving the company and respective product closer to customers, so that Information Systems (IS) would enhance flexibility of SMEs. Moreover, Migiro and Wallis (2006) found that information on sources of finance needs to be more readily available to SMEs and their advisors through an SME portal. Such reform is underway in the Philippines (Guzman et al., 2015). The same is observed in Nigeria with the M-Pesa mobile money disruption enabling many SMEs to be more efficient (Ndemo, 2017). It is an undeniable fact that digital technology is an opportunity for SMEs to benefit from increased market reach and knowledge networking at an arguably cheaper cost (OECD, 2017). While the debate of technological innovation in business promises new possibilities for SMEs, the OECD report (2018) reports that the latter are still lagging in embracing the shift to digitalisation. The general observation is that the technological gap widens when e-commerce systems are controlled for.

African experiences

Surveying the literature revealed significant efforts to establish SME portal for data sharing; however the spin-offs of such initiatives are not well-established in the African context. The ITC report (2015) further adds that African countries are lagging behind when it comes to IT readiness. In view of addressing the existent digital divide, the Rwanda government is working with the private sector on their “#GoConnect” initiative to make digital services more accessible and cheaper (ITC, 2015). Similar initiatives were adopted in Kenya to cater for the microfinancing issues and fund transfer through the M-pesa mobile application (International Finance Corporation, 2009). The country also created a hotline, “Kilimo Hotline” to mitigate information asymmetry with regards to trade information, current support programmes, market prices, among others.

In the African context, it appears that countries are at different stages. This is mainly attributed to financial resource gap and lack of skills across the continent. This current situation formed the basis of the Microsoft’s Biz4Africa initiative (ITC, 2015). Biz4Africa is an online platform that provides cloud-based business solutions by aggregating relevant trade information and enhances networking opportunities for small firms (Hain and Juriwetzki, 2017). It can be understood as a platform that assists firms throughout its business life cycle. Moreover, ICT impacts much on the lives of entrepreneurs by supporting them to cultivate their small enterprises and have a competitive edge in the market (Ozigbo and Ezeaku, 2009).

The country experiences have shown in different degree the extent of ICT infiltration to enhance the business activities of SMEs. The African experiences is something for the Mauritian government to replicate while the Asian experience, in particular, the Malaysian extent of ICT use is of great interest to make the Mauritian SMEs more competitive. Further, the European degree of digital use to ensure a buoyant SME sector is a good example that most other jurisdictions can embark on to tap into the potential of SMEs to create economic growth.

METHODOLOGY

The purpose of this research is to come up with an online strategy to assist SMEs in their financial literacy. This research is descriptive given that the profile of entrepreneurs and their related business are known whereby the who, what, where and how questions are well defined. With reference to Zikmund (2000), this research attempts to use exploratory research in order to have a clearer and better interpretation of the nature of a problem through exploring the problems that entrepreneurs are facing in their daily operational activities, and research is conducted to provide understanding and observation on the subject which is financial literacy of SMEs, rather than the provision of conclusive evidence. Micro and small enterprises are targeted in this study. This investigation aspires from Yin (1994) who defines five principal research strategies to use when collecting and analysing empirical evidences namely experiment, survey, archival analysis, history and case study. The study adopts a dual methodology to address the study objectives, that is, both qualitative and quantitative. Two focus groups were held as part of the qualitative approach to gauge into the SMEs level of financial literacy and to assess the extent of the problem. The quantitative approach was possible through the development of a survey instrument. A stratified random sampling has been used for the study so as to ensure that the sample is representative of the population of SMEs in Mauritius. The determinants of size of SME firms were based on the level of turnover.

The objective of the first focus group with SMEs was to gauge into the financial awareness and knowledge of SMEs to identify gaps in financial education among entrepreneurs. The targeted SME audience consisted of 16 SMEs from various sectors of the economy. Some major constructs were identified which ultimately contributed in the design of the questionnaire. Additionally, the findings of the focus group were important for the first design of the prototype e-platform. The second focus group was held with some key stakeholders of SMEs. The participants contributed much to findings towards the existing strategies that they are providing to facilitate financial literacy of SMEs in Mauritius. These findings will be linked back to the survey results to validate the extent of the awareness about these existing schemes.

The quantitative approach was used to collect primary data from the owner manager of SMEs operating in different industry groups in Mauritius and Rodrigues. The questionnaire was designed based on an extensive review of the literature and the first and second focus groups which were instrumental in identifying some of the constructs relevant for the study. The instrument includes a number of questions with a view to assessing the respondents’ financial attitude and behaviour. The questions are of nominal and ordinal scale. Some of the questions make use of multiple choice questions and dichotomous type. Some of the questions relates to about how money is handled in the business, profit/loss/pricing calculation and awareness about financing options.

In order to measure the SMEs financial knowledge, seven questions on basic financial literacy measured on an ordinal-index were used to calculate a financial knowledge score. The survey also attempts to capture the ICT adoption and usage by the owner manager as a means to run and manage their businesses. The questions set range from basic use of ICT tools/ devices to more advanced applications software that have been developed to facilitate business operations. There are also a set of questions to assess the extent of internet banking, mobile banking, Point of Sales (PoS) and other e-banking channels. Only the micro and small firms are of interest for our study. The objectives of the study are to gauge into their awareness and knowledge of financial products, procedures and obligations and evaluate their financial education needs.

FINDINGS AND ANALYSIS

Here the survey response are analysed with a view to gauge into the financial literacy of the owner manager. The survey instrument also attempts to assess the level of digital literacy as the study’s main objective is to propose an integrated financial assistance strategy using an IT platform. The owner manager and firms’ characteristics are first given to better profile the respondents. This is followed by an assessment of the SMEs’ perception on financial literacy; their financial attitude and behaviour, the extent of ICT adoption and usage. Most importantly, the instrument uses seven basic financial literacy questions to calculate the SMEs financial knowledge score. Lastly, the survey attempts to measure the need for financial education and assistance of the owner manager of Mauritian SMEs.

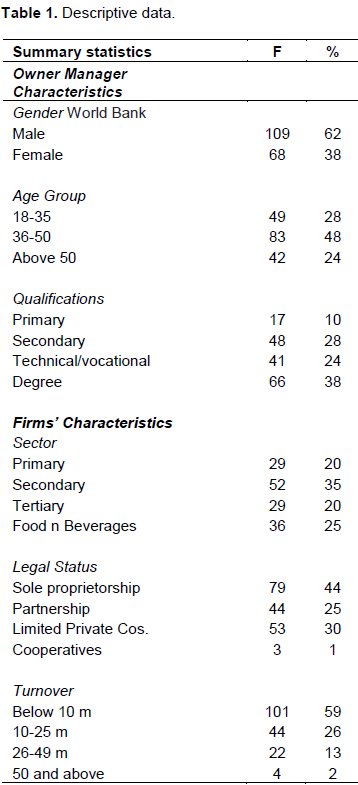

Table 1 reveals that the majority of the respondents are male, representing 62% of the sample. The age group 36 to 50 is more represented and this points to the competency of the owner managers in managing their businesses. This would be important when assessing their level of financial literacy and also the extent of FinTech usage. As expected, the qualifications of the owner manager are basically technical/vocational; and secondary level with only some 38% had studied up to university level. Next, the firm’s profile is analysed in terms of its legal status, sector of operation and the yearly turnover, a common proxy to measure size of firms. The majority of the firms are organised as sole proprietorship and private companies, representing 44 and 30% respectively. 25% of the sample firms operate as a partnership, where the requirements for compliance to preparation of accounts are less stringent. The initial survey form has captured the sampled firms sector using a number of categories ranging from agriculture to heath care. In order to facilitate later analysis, the sector was regrouped into primary, secondary and tertiary sector, with the food and beverages as a separate industry group. The primary and services sectors are represented by 20% of the sample and 35% are from the secondary sector while the food and beverages is 25%. Based on the turnover figured, nearly half of the sampled firms are classified as small, which is a focus of the study.

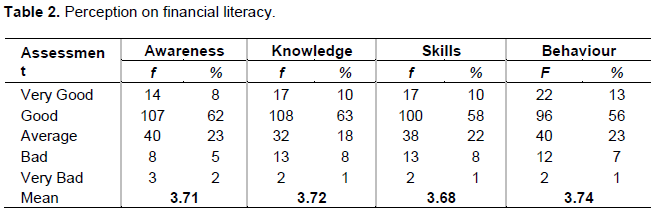

In line with the study objectives, the respondents’ perception on financial literacy is measured using a 5-point Likert scale. Financial literacy is defined as a combination of awareness, knowledge, skills, attitudes and behaviour needed to make sound financial decisions, in order to achieve individual financial wellbeing. Table 2 summarises the results and report the mean score for the different dimension of financial literacy. It appears that the owner managers perceive their level of financial literacy to be high where their financial knowledge, skills, attitude and behaviour are rated as good.

Accounting records

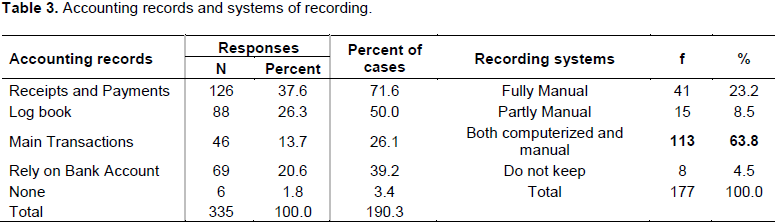

The literature on the financial management practices has revealed the lack of attention to basic accounting records of SMEs (Padachi, 2012). This is often viewed as a major weakness when the owner manager of firms accesses formal credit. The survey results confirm this situation. Table 3 shows that the most popular records kept by the firms is the receipts and payments (72% of the sample firms) while there are still 50% of the sample firms that keep the transactions in a log book and some 39% use the company’s bank account to keep track of the business transactions.

The system of recording of transactions is predominantly a combination of manual and computerised – 64% of the sample firms claim to have both systems. This has implication on the readiness of our SMEs to adopt computer applications to facilitate the business operations, where 64% of the SMEs claimed that they use a combination of manual and computerised recording systems. This finding points to the widely known fact that the SMEs are credited as “resource poverty” (Cressy, 1991).

ICT Adoption and Usage

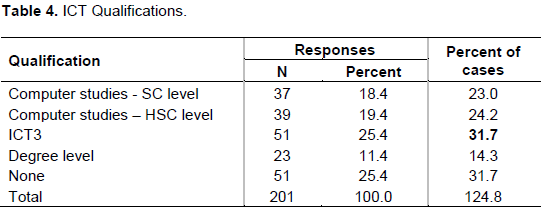

The basic ICT qualification of the 174 SME owner managers is displayed in Table 4, which shows that 32% of the owner manager does not possess a qualification in ICT related studies. This in itself would be a handicap for the owner managers to use ICT in the running of their business. However, it is interesting to observe that 32% of the owner managers have undergone training in computer studies as part of the government project to make the population more IT literate. 32% of the respondents have followed the ICT 3 courses.

The survey data attempts to assess the SMEs’ readiness to embrace ICT in carrying the operation of the business. Table 5 summarises the nine (9) questions set to gain an insight into the firms’ ICT strategy, internet access, human capital and the usage of technology. There is some evidence as to the SMEs preparedness to use ICT as the majority of the respondents claim that they have access to internet, have their own home page, have skilled staff, or they avail the services of expert in IT. However, they do not make enough use of e-banking or e-commerce as only 49% of the sampled firms use the MRA e-filing services for payment of tax.

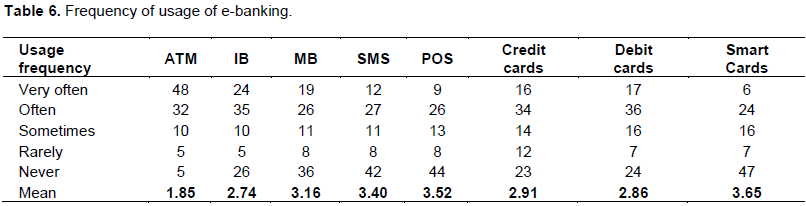

Table 6 displays the result on the usage of e-banking channels. The most common one is the ATM (mean score = 1.85) and the least often used is the smart cards (with a mean score of 3.65). The use of debit and credit cards are quite popular among the Mauritian SMEs. However, it is important to point out that nearly a quarter of the sample firms do not make use of debit and credit cards. Moreover, the point of sale technology is not often used as more than 50% of the firms hardly used this device for trading. It is interesting to note that internet banking is used by most of the respondents with a mean score of 2.74. The two latest Fintech devices, namely SMS banking and mobile banking have not captured the attention of the owner manager.

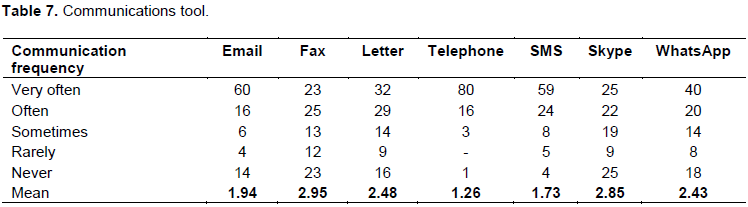

In order to gain an insight into the extent of the use of technology devices, the respondents were asked to choose the most often used communication tools. Table 7 shows that most traditional forms of communication remain; telephone, letter and fax having a mean value of 1.26, 2.48 and 2.95, respectively. Alternatively, the most commonly used communication tool in the advent of technology is SMS followed by email and WhatsApp. 60% of the respondents claimed that they use WhatsApp while 73% used text message. It is interesting to note this trend as this will facilitate the implementation of an e-platform as a solution to the financial assistance strategy.

Financial knowledge score

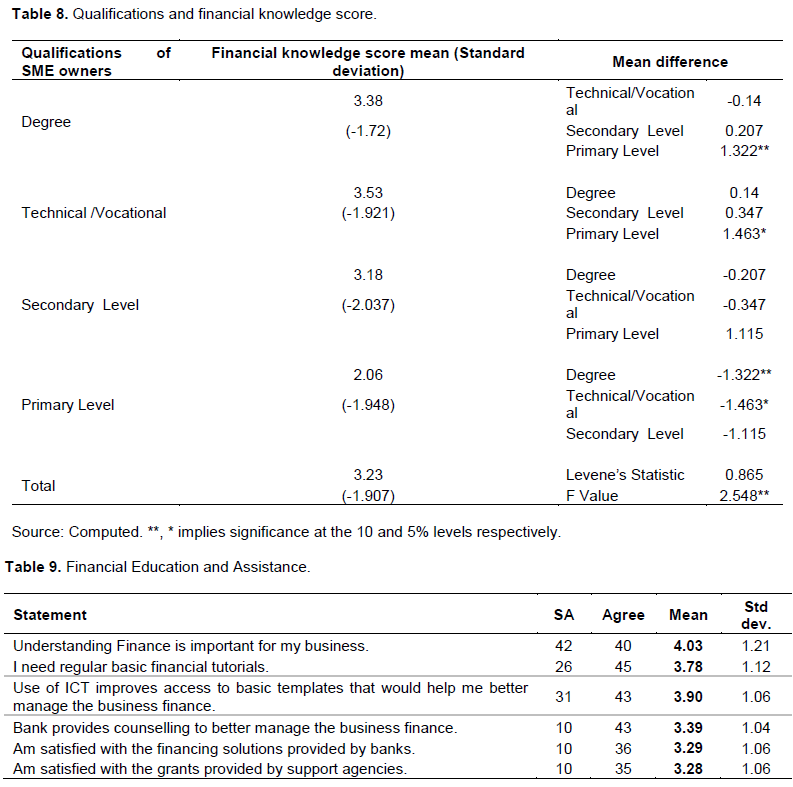

The study attempts to gauge into the financial knowledge of the SME owners by asking some basic questions on the calculation of interest, understanding concept of risk, cost of capital and financial statement. Tables 8 and 9 give the summary statistics grouped into the owner manager characteristics and firms’ characteristics. The Financial Knowledge score is based on the questions in the survey and encompasses the core areas which follow that of Atkinson and Messy (2012) whereby each correct answer was given an equal score of 1 with each question bearing equal weightage. The maximum Financial knowledge score is therefore 7. The average knowledge score of SME owners was found to be 3.21 (45.9%) implying a below average performance in terms of financial knowledge.

The study prompts further, to investigate the extent to which demographic factors including gender, age, qualifications of SME owners as well as the firm characteristics such as legal status, the business sector in which they operate and the annual turnover affect financial knowledge. The analysis revealed that the only significant demographic determinant of financial knowledge for our sample group is the level of qualifications of the SME owners. Summary statistics related to qualifications of the respondents are reported in Table 10 and the Levene’s test for testing the homogeneity of variances is also given. There was no evidence to reject the null hypothesis of homogeneity of variances at 10%. To identify where the differences in qualifications lie, the Tukey HSD Post-hoc test is performed which shows that degree holders and those having a technical or vocational training have higher financial knowledge than those having basic education.

Financial education and assistance

Here the survey instrument captures the need for financial education and assistance for the Mauritian SMEs to better run their businesses. There is a comfortable number (48%) of the respondents who confirm that they would need training on business education. Next the questionnaire contains a six-item statement to evaluate the need for financial education and what assistance the SMEs are benefiting from.

There is a good consensus (X = 4.03) among the owner manager that finance is important for the running of the business. This is followed by the need to have regular basic financial tutorials (X=3.78; SD=1.12). Given the time constraint which SMEs face, they are of the view that the use of ICT will facilitate access to business templates that would prove beneficial to manage the business finance. On the other hand, the survey results point to the lack of support from the banks and the support agencies. The owner managers are of the opinion that the banks should make more effort to counsel them in business finance. This is further evidenced by the low satisfaction level (46%) with regards to the financing solutions provided by their banks. A similar observation is made about the grants which are provided by the support agencies. These findings add credence to the focus of this study; that is the need to develop an e-platform as a means to better assist in the financial education and assistance of the Mauritian SMEs.

The analysis of the survey has uncovered the relative low financial knowledge especially for SME owners having basic education as well as the lack of awareness about basic financial planning tools useful for the business. This is observed despite the fact that SME support agencies do have training on financial tools to support SMEs. For instance, the SMEDA in collaboration with ACCA “conduct workshops on basic finance for the SME owners; Other organisations like the MEF and NWEC conduct basic “Adult literacy and life skills programme to empower human capital”. Furthermore a representative of the NCC avers that “there are many non-financial people who submit their financials to the registrar”. The organisation is therefore planning to introduce a non-award programme on financial management, book keeping and accountancy for SMEs. On the other hand, the focus groups with SME owners suggest lack of responsiveness to the training programme “not because they are not interested” but because they are “so busy with their business routines” that they often “do not find time to attend the training”. Some even pointed that they miss out on the training because the information does not reach out to them as they do not always have the attitudinal reflex “to check websites” of support agencies

Additionally, the desk work has highlighted the numerous financial schemes of banking institutions and support agencies; however, it has been observed that although entrepreneurs are generally aware of these, it becomes “tedious to take appointments with all of them” to decide on their most suitable options. The respondents also highlighted that a forum where the community could exchange their experiences and share practical information would also be “helpful” and “instructive”. Moreover, the survey has revealed that although there is some degree of awareness about the most common sources of finance, the cost implications are not always fully understood.

In the light of the above and given that there is evidence of ICT readiness among the Mauritian entrepreneurs, the proposed solution is an e-platform which encompasses (1) Short clips on basic accounting terminology and on initiatives and operational activities of entrepreneurs; (2) Tutorials on bookkeeping and basic financial management by a professional SME advisor acting as an online tutor to explain the concepts of basic accounting and finance; (3) Accounting templates in Excel format that can be used by entrepreneur in handling their basic financial matters; (4) An interactive discussion forum where the registered users can log in to interact with other entrepreneurs and SME advisor to discuss financial management and other related issues; (5) Centralised information centre from relevant financing institutions and support agencies where SMEs can search for relevant information provided by them and other service providers; and (6) News and events alerts to provide relevant information related to SMEs in Mauritius. This proposed solution draws mainly from previous studies conducted by Mazur (1998).

TECHNICAL FEASIBILITY

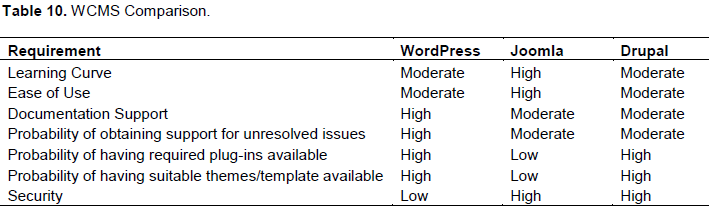

This part of the research elaborates on the technical aspects of the proposed solution and the major technical issues concerning the development of the web-based SME finance Literacy project. The phase consists of the design, development and deployment of a web application to provide useful information to intended users. Indeed, the Web Content Management System (WCMS) as a powerful tool has allowed the development of this proposed web-based application from a central interface. One of the primary aims of using WCMSs is to bypass the need for hand coding and development from scratch (Patel et al., 2011), where Plug-ins are readily available to perform complex tasks as well as maintenance tool to bring modifications to web content (Ghorecha and Bhatt, 2013). The three common WCMSs have been analysed and compared with respect to the key requirements of this project. Table 10 illustrates the result of this evaluation.

As can be observed from Table 10, WordPress, Joomla and Drupal have various notable strengths and weaknesses. All the 3 WCMSs meet more or less the same goals; however, they do not all contain the same features. WordPress has been considered best suited for this project because of its large array of built-in features as well as a large selection of additional plug-ins (43,427) which enhances the value of websites as well as enrich visitors' experience. Moreover, a substantial amount of documentation and support for WordPress is available in the form of live chat with WordPress representatives, published books, online forums and video tutorials as well as pre-packaged graphical themes and templates readily available.

Requirement analysis

SMEs require a web application designed to enable them access resources related to facilities provided to setup/enhance business. The initial requirements have been captured from the focus group conducted at SMEDA with 16 SME owners representing a cross-section of the Mauritian SMEs. Their feedbacks were gathered to know their needs for the requirements of the proposed solution and in the design of the survey instrument.

Problems with actual system

There is no such system that provides information to intended users. As such, SMEs need to search information by themselves that they find suitable and sometimes they land at the wrong place. Entrepreneurs need to contact appropriate authorities to have valuable information which takes a day or two. Hence, it is a loss of time in monetary terms.

Functional specifications

The following functional specifications are proposed by the SME target audience:

i) Easy to use by any person (children, students, matured entrepreneurs, novice entrepreneurs);

ii) Simple in terms of design for easy usage such as Google;

iii) Inter-operable on various devices namely PC, laptop, mobile systems such as smart phones, IPhones;

iv) Informative with easy information contents;

v) Facilitate SMEs operational activities/tasks;

vi) Forum for knowledge sharing for various communities of practices and sectors of the economy;

vii) Animated and interactive for better understanding;

viii) Responsive and accessible quickly with easy navigation menus with more informative as possible in terms of literature, video tutorials and maintenance easiness and content update;

Technical specifications

The website has been designed to be available on a 24/7 basis where it can be (a) accessible to a large number of users without affecting performance of the website itself; (b) highly resilient; (c) scalable and easily maintainable in the future and (d) enhanced with security features to protect user credentials and data. The website is hosted on a 24/7 Linux server with domain name http://www.domain-name.com. To access the website, users should have one of the following browsers installed, namely; Internet Explorer (IE) min version 10, Chrome and Firefox. The website OS is also accessible via mobile devices. The website is being designed using HTML 5 for the presentation layer. Mysql database is being used as back-end where all the information pertaining to the website is stored. The intermediary language between the front-end and the back-end used is the PHP language.

Project management methodology

The development methodology of the proposed prototype is based on Rapid Application Development (RAD) and the prototyping approach used to develop the website. It is tuned and enhanced after peer review and basis requirement. The proposed solution is derived after working on various prototyping, an evolutionary prototyping approach, that is, an initial prototype is worked on and tested, leading towards a second prototype, until the final has been approved to be the most suitable one. Two types of user group were defined namely (i) Normal User and (ii) Admin user. The development tools were (i) HTML, JavaScript as frontend, (ii) PHP programming to push and pull data from Database and (iii) MySQL Database as backend. The solution intends to bring an all-in-one platform that can provide useful information at the tip of fingers to intended SME users who will have a major advantage in saving time and money. Information on the e-platform can be accessed anywhere and anytime provided they are connected to the internet, comprising of videos, tutorials, post and even chat to be incorporated.

Prototypes development

One of the main focuses of the study is to propose an innovative e-platform of financial assistance for Small Medium Enterprises. This has necessitated a number of prototypes with the involvement of key stakeholders which were deemed important to come up with an appropriate Logo Design as displayed in Figure 1

Final prototype

After evaluation and testing with some targeted SME users, the last prototype finally comprised of a welcome page (Figure 2), a web page stating the vision and mission statements of the e-platform (Figure 3), a web page containing all the useful links for SME web users, events to display events organised by stakeholders in favour of the SMEs, a chat room for SMEs to share knowledge related to the SME sector, a site map to guide the SME users, contact us page to enable communication with the e-platform administrators, login function to facilitate networking with SME peers and the main service is the entrepreneur learning corner (ELC). The ELC provides several facilities, namely; the financial templates, online dictionary on basic accounting terms to facilitate quick reference, online video tutorials from tutor, and a televised short film/video on sources of finance. This e-platform acts as a knowledge sharing platform for the SMEs and among the SME peers. The pilot e-platform can be accessed at: http://smefinance.mu/.

CONCLUSION AND IMPLICATIONS OF STUDY

The main contribution of this project is the design of an e-platform to improve the financial knowledge of entrepreneurs through videos and podcasts on basic accounting and finance terminology, as well as sources of finance. The e-platform will give access to financial tools to assist entrepreneurs in their business decision making process, and includes the possibility of a sharing platform among SMEs peers to share their difficulties in order to learn and develop their financial capabilities. So far, each financial institution (FI), namely banks and SME authorities and stakeholders have their own platform in terms of their website to display financial information for SMEs. As such, important information is diluted and does not reach the SMEs as targeted. Moreover, given their limited time and business obligations, SMEs require an integrated e-platform for a self-help and one-stop shop information for their financial needs. The significance of this project is to bring forth one integrated platform to educate SMEs of their financial needs whereby all FIs, SME stakeholders, related government bodies can also provide information to outreach the SMEs. This e-platform is planned to act as a Win-Win situation for both parties, namely, SMEs as well as stakeholders. Online videos, chat, forums among peers, member registration are among the proposed functionalities to support in the mentioned project objectives.

The main takeout of this research is that SMEs are fundamentally resource constraint and that the sustainability of their growth demands a holistic strategy. This research has answered important questions regarding the degree of financial and digital literacy in the Mauritian context. It is expected that this prototype research will result in a spin-off and materialise into a fully operational and integrated financial education platform.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Atkinson A, Messy FA (2012). Measuring financial literacy: Results of the OECD. OECD Publishing. |

|

|

Bartlett W, Cuckovic N, Xheneti M (2005). Institutions, entrepreneurship development and SME policies in South East Europe. In 6th International Conference on Entrerprise in Transition", University of Split, Split. |

|

|

Beal DJ, Delpachitra SB (2003). Financial literacy among Australian university students. Economic Papers: A Journal of Applied Economics and Policy 22(1):65-78. |

|

|

Beck T, Demirgüçâ€Kunt ASLI, Maksimovic V (2005). Financial and legal constraints to growth: Does firm size matter? The Journal of Finance 60(1):137-177. |

|

|

Biggs T, Ramachandran V, Shah MK (1998). The Determinants of Enterprise Growth in Sub-Saharan Africa: Evidence from the Regional Program on Enterprise Development. World Bank. RPED Discussion Paper, 103:283-300. |

|

|

Chang WL, Liu JY, Huang WG (2014). A study of the relationship between entrepreneurship courses and opportunity identification: An empirical survey. Asia Pacific Management Review 19(1):1-24. |

|

|

Cressy R (1996). Are business startups debt-rationed?. The Economic Journal pp.1253-1270. |

|

|

Dunne T, Roberts MJ, Samuelson L (1989). Plant turnover and gross employment flows in the US manufacturing sector. Journal of Labour Economics 7(1): 48-71. |

|

|

European Commission (2009). European Union Support Programmes SMES: An overview of the main funding opportunities available to European SMEs. |

|

|

Ghorecha V, Bhatt C (2013). A guide for selecting content management system for web application development. International Journal of Advance Research in Computer Science and Management Studies, 13-17 |

|

|

Guzman GM, Torres GCL, Serna MCM, Garcia SM (2015). Information Technology and Competitiveness: The Mexico's SMEs Context. In Proceedings of the International Symposium on Emerging Trends in Social Science Research. |

|

|

Hall G (1992). Reasons for insolvency amongst small firms-A review and fresh evidence. Small Business Economics 4(3):237-250. |

|

|

International Trade Centre (ITC) (2015). International e-commerce in Africa: the way forward. |

|

|

International Labour Office (ILO) (2010). Gender Dimensions of agricultural and rural employment: differentiated pathways out of poverty. |

|

|

Ives B, Mason RO (1990). Can information technology revitalize your customer service?. The Executive 4(4):52-69. |

|

|

Kapurubandara M, Lawson R (2006). Barriers to Adopting ICT and e-commerce with SMEs in developing countries: An Exploratory study in Sri Lanka. University of Western Sydney, Australia, pp.2005-2016. |

|

|

Kadiri IB (2012). Small and medium scale enterprises and employment generation in Nigeria: the role of finance. Kuwait Chapter of the Arabian Journal of Business and Management Review 1(9):79. |

|

|

Karadag H (2017). The impact of industry, firm age and education level on financial management performance in small and medium-sized enterprises (SMEs) Evidence from Turkey. Journal of Entrepreneurship in Emerging Economies 9(3):300-314. |

|

|

Kuratko DF (2006). A tribute to 50 years of excellence in entrepreneurship and small business. Journal of Small Business Management 44(3):483-492. |

|

|

Lal K, Peedoly AS (2006). Small Islands, New Technologies and Globalization: A Case of ICT adoption by SMEs in Mauritius, UNU-MERIT pp.1-39. |

|

|

Ozigbo N, Ezeaku P (2009). Adoption of information and communication technologies to the development of small and medium scale enterprises (SMEs) in Africa. Journal of Business and Administrative Studies 1(1):1-20. |

|

|

Mandell L, Klein L (2009). The impact of financial literacy education on subsequent financial behaviour. |

|

|

Mazur GH (1998). Strategy deployment for small and medium enterprises. In Proceedings of the International Symposium on Quality Function Deployment. Sydney, August. |

|

|

Ministry of Business Enterprise and Cooperatives (MoBEC) (2016). 10 - year Master Plan for the SME Sector in Mauritius – Accelerating SME Innovation and Growth, Ministry of Business Enterprise and Cooperatives. |

|

|

Migiro S, Wallis M (2006). Relating Kenyan manufacturing SMEs' finance needs to information on alternative sources of finance. South Africa's Journal of Information Management 8(1):1-12. |

|

|

Ndemo B (2017). The paradigm shift: Disruption, creativity, and innovation in Kenya. In Digital Kenya. Palgrave Macmillan, London pp.1-23. |

|

|

Noctor M, Stoney S, Stradling R (1992). Financial literacy: a discussion of concepts and competences of financial literacy and opportunities for its introduction into young people's learning. National Foundation for Educational Research. |

|

|

Nunoo J, Andoh FK (2012), August. Sustaining small and medium enterprises through financial service utilization: Does financial literacy matter. In Unpublished Paper) presented at the Agricultural & Applied Economics Association's (2012) AAEA Annual Meeting, Seattle, Washington. |

|

|

Organisation for Economic Co-operation and Development (OECD) (2017). Financing SMEs and Entrepreneurs. An OECD Scoreboard 2017, OECD Publishing, Paris. |

|

|

Organisation for Economic Co-operation and Development (OECD) (2018). Financing SMEs and Entrepreneurs. An OECD Scoreboard 20189, OECD Publishing, Paris. |

|

|

Padachi K (2012). Factors affecting the adoption of formal Accounting systems by SMEs'. Business and Economics Journal Vol. BEJ 67. |

|

|

Patel SK, Rathod VR, Prajapati JB (2011). Performance Analysis of Content Management Systems - Joomla, Drupal and WordPress, International Journal of Computer Applications 21(4):39-43. |

|

|

Pissarides F, Singer M, Svejnar J (2003). Objectives and constraints of entrepreneurs: evidence from small and medium size enterprises in Russia and Bulgaria. Journal of Comparative Economics 31(3):503-531. |

|

|

SME Performance Review - European Commission. [online] |

|

|

Snodgrass DR, Biggs T (1996). Industrialization and the small firm: Patterns and policies. International Center for Economic Growth: Harvard Institute for International Development. |

|

|

Staniewski MW (2016). The contribution of business experience and knowledge to successful entrepreneurship. Journal of Business Research 69(11):5147-5152. |

|

|

Statistics Mauritius (2013). Census of Economic Activities – Phase 1 Small Establishments. Port Louis: Government of Mauritius, 2013. |

|

|

Subrahmanya MH, Mathirajan M, Krishnaswamy KN (2010). Importance of technological innovation for SME growth: Evidence from India (No. 2010, 03). Working paper//World Institute for Development Economics Research. |

|

|

Yin R (1994). Case study research: Design and methods. Beverly Hills. |

|

|

Zikmund WG (2000) Business Research Methods. 6th Edition, The Dryden Press, Fort Worth. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0