Full Length Research Paper

ABSTRACT

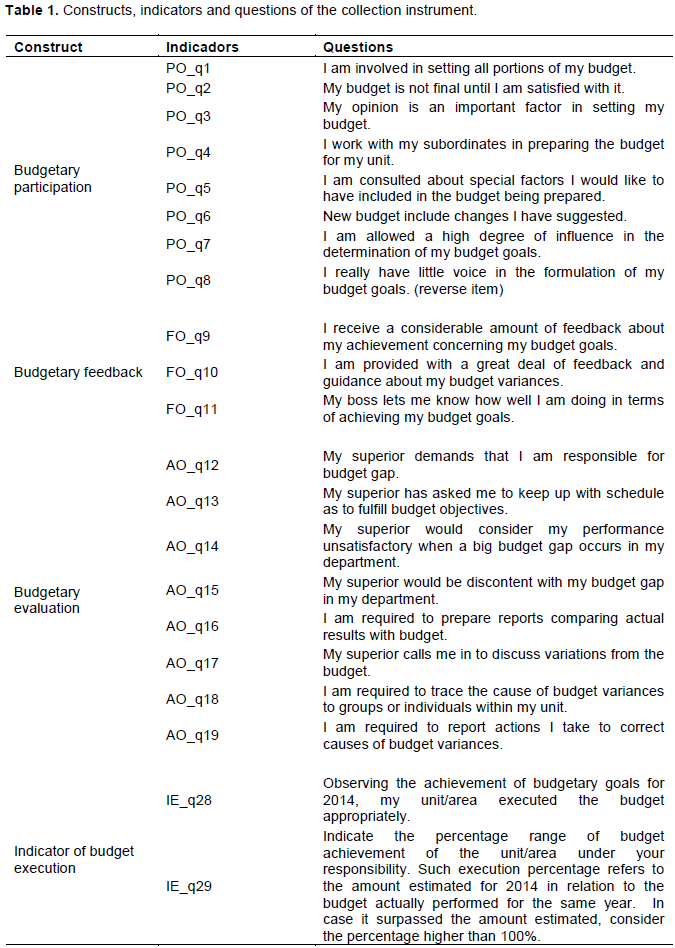

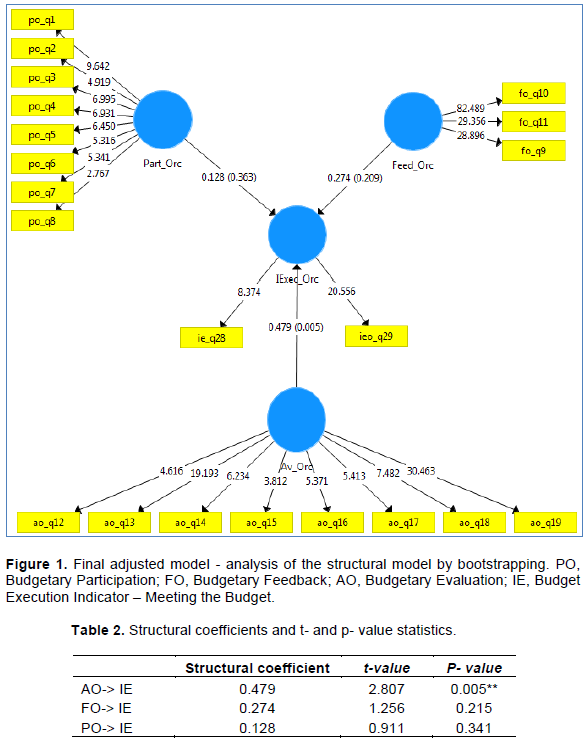

Budgetary control is pointed as a managerial mechanism suitable for cost reduction and control as well as performance evaluation of institutions. In health organizations, budget is used for funds allocation, coordination, control and communication of the institutions’ strategies. In this context, the research will observe the phenomenon of budgetary process from the perspective of Health Service managers of public and private hospitals, called “clinical managers”. It aims to check whether there is a relation between the budgetary process characteristics and the budgetary execution performance. Three hypotheses were tested for the analysis of the following budget characteristic, budgetary participation, budgetary feedback and budgetary evaluation. This theoretical research model is going to be analyzed using the structural equation method. The study evaluates if there is a relationship between the budget process characteristic and the budget execution indicator, called meeting the budget. The snowball sample technique was used to sample the research respondents. Thirty three clinical managers were used as sample for the study. The hypotheses were tested using the Smart Pls software. Only Hypothesis 3 was supported statistically, asserting that there is a positive and significant relationship between the budgetary evaluation characteristic and the budget execution performance. These evidences indicate that health service managers recognize the budgetary evaluation as a predominant feature which interferes with the budgetary execution of their field due to the liability on the result of such execution and the possibility of using this metrics in performance evaluation.

Key words: Budgetary control, budget, budgetary evaluation, performance.

INTRODUCTION

LITERATURE REVIEW

METHODOLOGY

RESULTS AND DISCUSSION

FINAL CONSIDERATIONS

CONTRIBUTIONS

LIMITATIONS AND FUTURE RESEARCH

CONFLICT OF INTERESTS

REFERENCES

|

Abernethy M, Chua WF, Grafton J, Mahama H (2007). Accounting and Control in Health Care: Behavioural, Organisational, Sociological and Critical Perspectives, w: eds. CS Chapman, AG Hopwood, MD Shields, Handbook of Management Accounting Research. |

|

|

Abernethy M, Guthrie CH (1994). An empirical assessment of the "fit" between strategy and management information system design. Accounting and Finance 34(2):49-66. |

|

|

Abernethy M, Stoelwinder JU (1991). Budget use, task uncertainty, system goal orientation and subunit performance: a test of the 'fit' hypothesis in not-for-profit hospitals. Accounting, Organizations and Society 16(2):105-120. |

|

|

Aidemark LG (2001). Managed health care perspectives: a study of management accounting reforms on managing financial difficulties in a healthcare organization. European Accounting Review 3(10):545-560. |

|

|

Almeida AG, Borba JA, Flores LCS (2009). A utilização das informações de custos na gestão da saúde pública: um estudo preliminar em secretarias municipais de saúde do estado de Santa Catarina. Revista de Administração Pública 43(3):579-607. |

|

|

Anthony RN, Govindarajan V (2008). Sistemas de Controle Gerencial. São Paulo: McGraw-Hill. |

|

|

Atkinson AA, Kaplan RS, Matsumura EM, Young SM (2011). Contabilidade Gerencial. São Paulo: Atlas. |

|

|

Beaton DE, Bombardier C, Guillemin F, Ferraz MB (2000). Guidelines for the process of cross-cultural adaptation of self-report measures. Spine 25(24):3186-3191. |

|

|

Bonacim CAG, Araújo AMP (2010). Gestão de custos aplicada a hospitais universitários públicos: a experiência do Hospital das Clínicas da Faculdade de Medicina de Ribeirão Preto da USP. Revista de Administração Pública 44(4):903-931. |

|

|

Buzzi DM, dos Santos V, Beuren IM, Faveri DB (2014). Relação da folga orçamentária com participação e ênfase no orçamento e assimetria da informação. Revista Universo Contábil 10(1):06-27. |

|

|

Cardoso LC, Mário PC, Aquino ACB (2007). Contabilidade Gerencial: mensuração, monitoramento e incentivos. Editora Atlas, São Paulo-SP. |

|

|

Church B, Kuang Xi, Liu Y (2018). The effects of measurement basis and slack benefits on honesty in budget reporting. Accounting, Organizations and Society 72(C):74-84. |

|

|

Covaleski M, Evans JH Luft J, Shields MD (2007). Budgeting research: three theoretical perspectives and criteria for selective integration. Handbooks of Management Accounting Research 2:587-624. |

|

|

Dallora MEL, Forster AC (2008). A importância da gestão de custos em hospitais de ensino-considerações teóricas. Medicina (Ribeirao Preto. Online) 41(2):135-142. |

|

|

de Oliveira WT, Haddad MDCL, Vannuchi MTO, Rodrigues AVD, Pissinati PDSC (2014). Capacitação de enfermeiros de um Hospital Universitário público na gestão de custo. Revista de Enfermagem da UFSM 4(3):566-574. |

|

|

Elhamma A (2015). The relationship between budgetary evaluation, firm size and performance. Journal of Management Development 34(8):973-986. |

|

|

Francisco IMF, Castilho V (2002). A enfermagem e o gerenciamento de custos. Revista da Escola de Enfermagem da USP 36(3):240-244. |

|

|

Gibbons R, Roberts J (2013). Economic theories of incentives in organizations. Handbook of Organizational Economics pp. 56-99. |

|

|

Hair J, Babin B, Money A, Samouel P (2005). Fundamentos de métodos de pesquisa em administração. Bookman Companhia Ed. |

|

|

Hair J, Babin B, Money A, Samouel P (2009). Fundamentos de métodos de pesquisa em administração. Bookman Companhia Ed.. Análise Multivariada de dados. Porto Alegre: Bookman. |

|

|

Hair JF, Sarstedt M, Ringle CM, Mena JA (2012). An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science 40(3):414-433. |

|

|

Hammad SA, Jusoh R, Oon EY (2010). Management accounting system for hospitals: a research framework. Industrial Management and Data Systems 110(5):762-784. |

|

|

Imoniana JO, Silva WL (2019). Understanding internal control environment in view of curbing fraud in public healthcare unit. African Journal of Business Management 13(18):602-612. |

|

|

Jacobs K (1998). Costing health care: a study of the introduction of cost and budget reports into a GP association. Management Accounting Research 9(1):55-70. |

|

|

Jensen MC, Meckling WH (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3(4):305-360. |

|

|

Kenis I (1979). Effects of Budgetary Goal Characteristics on Managerial Attitudes and Performance. The Accounting Review 54(4):707-721. |

|

|

King R, Clarkson PM, Wallace S (2010). Budgeting practices and performance in small healthcare businesses. Management Accounting Research 21(1):40-55. |

|

|

LA Forgia GM, Couttolenc BF (2009). Desempenho hospitalar no Brasil: em busca da excelência, São Paulo: Singular. |

|

|

Li W, Nan X, Mo Z (2010). Effects of budgetary goal characteristics on managerial atitudes and performance. International Conference on Management and Service Science. pp. 1-5. |

|

|

Lu CT (2011). Relationships among budgeting control system, budgetary perceptions, and performance: A study of public hospitals. African Journal of Business Management 5(15):6261-6270. |

|

|

Lunkes J R (2009). Manual de orçamento, São Paulo: Atlas. |

|

|

Macho-Stadler I, Perez-Castrillo D (2020). Agency Theory meets matching theory. In Series, pp.1-33. |

|

|

Macinati MS (2010). NPM Reforms And The Perception Of Budget By Hospital Clinicians: Lessons From Two Caseâ€Studies. Financial Accountability and Management 26(4):422-442. |

|

|

Macinati MS, Bozzi S, Rizzo MG (2016). Budgetary participation and performance: The mediating effects of medical managers' job engagement and self-efficacy. Health Policy 120:1017-1028. |

|

|

Macinati MS, Rizzo MG (2014). Budget goal commitment, clinical mangers1 use of budget information and performance. Health Policy 117:228-238. |

|

|

Merchant KA, Manzoni JF (1989). The achievability of budget targets in profit centers: A field study. In Readings in Accounting for Management Control pp. 496-520. |

|

|

Mucci DM, Frezatti F, Dieng M (2016). As múltiplas funções do orçamento empresarial. RAC-Revista de Administração Contemporânea 20(3):283-304. |

|

|

Pettersen IJ (1995). Budgetary control of hospitals-Ritual rhetorics and rationalized myths? Financial Accountability and Management 11:207-207. |

|

|

Pizzini MJ (2006). The relation between cost-system design, managers' evaluations of the relevance and usefulness of cost data, and financial performance: an empirical study of US hospitals. Accounting, Organizations and Society 31(2):179-210. |

|

|

Silva MT, Lancman S, do Carmo Alonso CM (2009). Conseqüências da intangibilidade na gestão dos novos serviços de saúde mental. Revista de Saúde Pública 43(suppl. 1):36-42. |

|

|

Swieringa RJ, Moncur RH (1975). Some effects of participative budgeting on managerial behavior. National Association of Accountants. |

|

|

Yuen DCY (2004).Goal Characteristics, communication and reward systems, and managerial propensity to create budgetary slack. Managerial Auditing Journal 19(4):517-532. |

|

|

Zucchi P, Del Nero C, Malik AM (2000). Gastos em saúde: os fatores que agem na demanda e na oferta dos serviços de saúde. Saúde e Sociedade 9(1-2):127-150. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0