Full Length Research Paper

ABSTRACT

In this study, we deal with the effect of internal auditor and family control on operational accrual items measurements across the Tehran Stock Exchange registered firms. The operational accrual items of the Giuli and Hin Model have been used to measure the conservatism level. In comparison with other models, including Basu’s model, the above-mentioned model is more reliable. "Herfindal-Hirschman Model” has been used to measure the family control. A total of 125 corporations were selected randomly in 2009 - 2011 for this study. Both regression and Pearson methods were used as the statistical methods of the study. Our findings approved the very intensive relationship between the internal auditor and the operational accrual measurement item. The impact of the family control over corporations on their conservatism level has been verified, as well; there was a positive and direct relation between the two mentioned variables. Also, the effects of firm size and financial leverage on the operational accrual items have been approved; the relation between these variables was more intense.

Key words: Conservatism, family control, internal auditor.

INTRODUCTION

According to the International Accounting Standard manifesto (SFAC No. 95), conservatism is a warily response to any type of ambiguity caused by the environ-mental hazards across the firm. Therefore, if there is an equal probability for estimating a sum which would be paid or received in the future, the conservatism allows estimation with lower optimism. Moreover, in the case of an unequal probability, using the pessimistic sum will not be allowed by the conservatism theory. Basu (1997) has examined the conservatism concept in the on-time reflection of accounting earnings in stocks and effect of both good and bad news and also has formulated amodel for measuring. Watts (2003) has offered three overall criteria for measuring the conservatism as net assets, earnings and accrual items and earnings to stock return. He also posed four interpretations for conservatism and scrutinized them through contractual, legislative, fiscal and legal aspects.

According to the Iranian accounting standards (2009), the financial statement providers are bound to urge caution when disclosing nature and amount of un-certainties. From Iranian accounting standards point of view, conservatism is a degree of surveillance in which adjudication is necessary to make estimation when uncertainty is dominant, as revenues and assets should not be exaggerated and expenses or liabilities should not be understated. It will be explained that using the conservatism should not be led to recognition of the unnecessary reserves, because it violates the neutrality of the financial reporting.

Given the definition broadcasted by the organization for Economic Co-operation and Development (OECD) in 2001and Ghirmai (2011), the corporate governance is the structure of relations and responsibilities among a major group including stockholders, board members and managing director to promote the necessary competitive performance to achieve the initial participation objectives (judge, 2010). Some other definitions stress the legal aspect of the corporate governance, e.g. IFAC which has considered the corporate governance fundamentally a proper measure to compare various countries and it believes that rules of each country play a key role in the corporate governance system; others emphasize keeping broader groups’ interests and deem corporate as responsible for any damages over the society, upcoming generation, natural resources and the environment (Young et al., 2011; Judge, 2010 ; Piot and Janin , 2007) Hasaasyegane (2009), Hesiang and Li-Jen (2010) and Nicolae et al. (2010) define corporate governance as a set of rules, regulations, structures and processes and cultures which make us able to achieve transparency and accountability necessary for observing stockholders’ rights. Some authors (Wang et al., 2009; Mohamad et al., 2010; Mehrani et al., 2009) have used conditional and unconditional conservatism terms. The conditional conservatism includes imperative accounting standards such as application of the minimum prime cost or market price apart from their good or bad consequences; usually, it is called income statements conservatism. However, the unconditional conservatism covers the financial behaviors which are not considered imperative according to the accounting standards and the book values of net assets are shown lower than the actual amount. This kind of book value is called balance sheet book value.

Accordingly, we will deal with the conducted studies in Iran and other countries with different accounting, legislative and legal conditions aiming to elicit our study hypotheses (Hasasyegane, 2009; Annelies et al., 2010; Midary, 2006; Renders et al., 2010).

Prior research and hypothesis development

Lara and Osama (2009) embarked on analyzing the relation between conservatism and the corporate governance. They examined corporate governance through either internal or external aspects and used market and book values for conservatism. They found that there is a direct relationship between firms with stronger corporate governance and conservatism level. They also came to a conclusion that firms with stronger corporate governance use discretionary accrual items to inform investors about bad news.

Rahmani and Gholamzadeh (2009) have analyzed the relation between the public ownership in the capital market and conservatism in the financial reporting. They consider conservatism as an index to improve the quality of the financial reporting. They have examined different conservatisms across financial reporting of 40 firms before and after their enrollment in TSE. Their results showed that the conservatism of financial reporting grew pale after enrolment in TSE.

Mashayekh et al. (2009) have begun to analyze the impact of the accounting conservatism on income stability and have concluded that income dividends decrease through increasing conservatism across the Iranian firms.

Karami et al. (2010) have analyzed the relationship between corporate governance mechanisms and conservatism across the TSE registered firms. They believe firms’ boards can act as the supervisor of the CEOs’ performance and prevent them from divulging income information and postponing losses. Basu model has been used for conservatism. Their results approve the meaningful and positive relationship between ownership percentage of the executive board members ad holding investors with conservatism and the negative relationship between non-executive board members and conservatism of firms.

Mohamad et al. (2010) found that bad news consequences act quicker than good news; moreover, the correlation coefficients of audit committee, size of directors and independence of directors are stronger and conservatism has grown in such firms. They also found the trivial effect of the political condition on price alterations caused by good and bad news. There was a negative relation between them while the government ownership has a positive effect.

Kung et al. (2010) have fathomed impact of the capital structure on conservatism of accounting digits in China. They used either Basu model or its refined version, “Ball and Shivakumar”, to measure conservatism. They found that firms whose stocks turnover is low have lower conservatism rate as well. In confirmation of their previous studies, they discovered that there is a direct relationship between ownership concentration and asymmetry of information and hence agency expenses in firms; thus demands for conservative profits will be dropped in such firms.

Chi et al. (2009) have analyzed the effective factors of the conservative behavior occurrence across firms. To do so, they studied corporate governance factor. They believed that firms which face agency expenses problem often prefer to be conservative. Therefore, any weak corporate governance system in such firms may end to more accounting conservative behavior. They also came to the conclusion that firms whose corporate governance is weaker are more inclined to conduct accounting conservative behavior.

Relying on Giuli and Hin Model, Banimahd and Baghbani (2009) measured conservatism rate across TSE registered firms. They analyzed the effect of corporate ownership type, firm size and financial leverage/unprofitability ratio across firms. They found a strong relationship between unprofitability and conservatism rate of firms, so, conservatism enhances value of unprofitable firms in the long term.

Given the results gained from both Iranian and foreign studies, the following hypotheses are set down:

H1: There is a meaningful and positive relationship between accounting conservatism and an internal auditor in a firm.

H2: There is a meaningful and positive relation between accounting conservatism and family control in a firm.

METHODOLOGY

All variables and the procedure used to measure them are explained as the first step to fulfill the study and then the model used for the study is described considering the theoretical concepts and the results of other studies.

Internal auditor

According to the Iranian Corporate Governance Law, the commercial firms must be equipped with an internal audit department which is monitored and controlled by their managing director or board of directors. The internal auditor can act and make report from all operational and financial fields of accounting. There is no audit committee in Iran; instead the internal audit plays this role in a more limited framework. Aiming to analyze hypotheses of our study, we marked firms with internal audit and without internal audit as 1 and 0, respectively.

Family ownership

Major shareholders of Iranian firms typically select the directors and minor stockholders are not allowed to select either directors or managing director. It is expected that the major stockholders maintain their own interests in this issue and disregard minor and dispersed stockholders. The Iranian Corporate Governance Law has not posed any certain controlling mechanism for this problem (Abdoli, 2011). In order to measure this variable across all questioned firms the corporate governance concentration rank is measured. The higher the index obtained, the more concentrated stockholders will be (Yu, 2010).

Ownership concentration is the manner in which stocks are distributed across stockholders of different firms. The less the number of stockholders is, the more concentrated ownership will be. In this study, Herfindal-Hirschman Index (HHI) has been used to qualify ownership concentration ratio. The index is the sum square of stocks percent belonging to stockholders. As the index increases, ownership concentration rate will be increased too and whenever the whole shares belong to an individual, then it will obtain the highest value, i.e. 10,000 units. If the ownership structure is dispersed and all stockholders have equal ratios, then the "HHI "will have the lowest value, i.e. N/10000.

HHI = ∑ (pi /p *100 )2

Conservatism

With regard to shortages of Basu model and other relevant models as well as the weak efficient capital market of Iran and relying on a model independent from market prices, we have decided to employ Giuli and Hin model (2000), to measure conservative index; the conservative index is measured here as:

Conservative index = Total Accruals x (-1)/ Total Asset and

Total accruals = (Net Income – Net Operating Cash Flow) + Depreciation of Assets

The total assets are equal to book value of assets for 2011. Giuli and Hin (2000) believed, “Increased accrual items can be an index of any change in the accounting conservatism degree in the long term”. In other words, if accrual items increase, then the conservatism drops and vice versa. Therefore, in order to specify direction of the conservatism alterations, the accrual items have been multiplied by -1 which homogenizes information across firms with different sizes; so, total accrual items have been divided by total assets.

Control variable – firm size and leverage ratio

Sizes of firms have been calculated using total assets logarithm, as large as book value recorded for the end of 2011. The leverage ratio has been obtained through dividing total liability by total assets of each firm.

Given the theoretical concepts of the study, relations among variables are evaluated and modeled as follows:

TOTAL ACCRUAL *-1 /TOTAL ASSET = α0 + + α1 * INT AUD +α2 *OWN CONC +α3 * SIZE + α4* LEVE+ ?

Where, Total accrual x -1/ total asset is considered as the dependent variable while INT AUD and OWN CONC which show internal auditor and ownership concentration rank in firms respectively are independent variables of the study and SIZE and LEVE show leverage ratio of firms.

Now, we analyze the results of the descriptive statistics of the firms; the results of presumptions of the regression test are presented which are accompanied with the results of our hypotheses.

Statistical population and sample

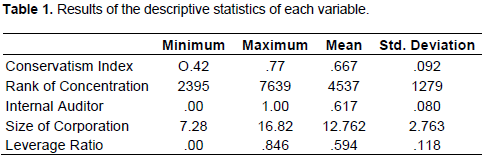

In order to analyze the model and to test the hypotheses, the TSE registered firms have been examined. End of fiscal year of the selected firms, excluding investment and brokerage firms, should be March 20 and their financial data for 2009 - 2011 period should be available. As mentioned previously, a total of 125 firms active in different industries were selected randomly. The information is summarized in Table 1.

As seen in the table, most firms have applied the conservative behavior in their financial report and have reported high optional accrual items. 62% of firms have internal audit, their sizes are relatively equal and most of them suffer from high rates of liability and financial leverage and their average leverage ratio is 60%, which is very high.

The statistic of this test is 1.532 (Table 2). Standing 1.5 and 2.5 makes it appropriate. Therefore, it can be concluded that errors are independent of each other, so a regression model can be used to test the hypotheses. Now all results obtained for our hypotheses are analyzed statistically.

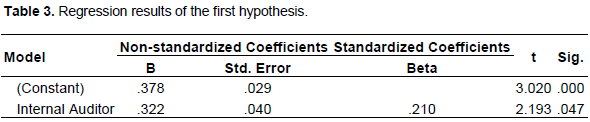

1. There is a meaningful and positive relationship between accounting conservatism and internal audit in the firm. This hypothesis develops the expectation that despite an internal auditor in the firm, the possibility of financial behaviors leading to development of an accounting conservative report is very rare. Results are shown in Table 3.

As the table represents, sign value is lower than alpha 5%; hence, the hypothesis is approved. In other words, there is a meaningful relationship between internal auditor and conservatism level in the firm. Beta coefficient value confirms the relation too; however, the relation type between them is determined as positive.

2. There is a meaningful and positive relationship between accounting and ownership concentration rank of a firm. According to the theoretical concepts, it is expected that firms whose ownership concentration rank is higher (~10000) have higher conservatism which is because of the higher monitoring possibility by the major stockholder as well as higher family control. The related results are shown in Table 4.

This table shows that Sign value is lower than Alpha 5% level; therefore, our hypothesis is confirmed and there is a relationship between percent of the major shareholders and family control across firms and conservatism level of financial behavior of directors.

The Forward model has been employed to analyze control variables. The seven variables used as the corporate governance specifications to predict conservatism have been selected out of many corporate governance specifications. As normal issues some specifications (variables) may not be good predictors. Therefore, when the irrelevant variables are used in this model, the criterion error is raised without improvement of prediction. Separate application of each of two control variables including firm size and financial leverage ratio for each of the above-mentioned hypotheses changed (increased) their correlation value and this level is meaningful given the “alpha” value. R2 rate for firm size and financial leverage were 35% and 39%, respectively.

DISCUSSION AND CONCLUSION

According to the theoretical concepts, the results of otherstudies on the conservatism, the hypothesis about the effect of political behaviors and agency theory it is expected that directors of larger firms suffering from external pressures embark on taking more conservative behaviors and recognize their profits later and understate interest rates through identifying expenses and various reserves. It is the case for firms whose leverage ratio is higher.

Our findings indicated that both family control and major stockholders who assume themselves as the main owners of firms, select executive directors and do not consider interests of minor stockholders, emphasize and support conservative behavior in firms. Directors can meet expectations and requirements of major stockholders on paying profits and withdrawing cash from the firms through submitting delayed reports on incomes and quicker identification of expenses; they also can postpone taxpaying. Tax issue is one of the most important effective factors of the financial behavior of the Iranian firms who consider this goal and issue in their financial reports.

Internal audit in firms has not prevented them from fulfilling conservative behavior and they have emphasized the delayed recognition of interests and have tried to recognize liabilities sooner. It can be explained by their dependency to executive director and particularly managing director of the Iranian firms. The dependency of the internal auditors is due to lack of precise definition of their position in firms and also lack of corporate governance law of Iran.

Like other studies, in this study the effect of firm size and their financial leverage ratio on conservatism of firms was positive. In other words, these components increase conservatism level imposed by the executive directors of firms. Such increase is justified by keeping interest and escaping from surveillance of others such as financers, the government and policy makers (according to politic and agency theory).

CONFLICT OF INTERESTS

The author has not declared any conflict of interests.

REFERENCES

|

Abdoli MR (2011).Relation of non-executive directors and ownership concentration with discretionary Accrual accounting. Aust. J. Bus. Manage. Res. 1(4):93-101. |

|

|

|

|

|

Annelies R, Ann G, Piet S (2010).Corporate governance ratings and company performance: Across – European study. Corporate Gov.: Int. Rev. 18(2):87-106. |

|

|

|

|

|

Basu S (1997). The conservatism principle and the asymmetric timeliness of earnings. J. Account. Econ. 24(1):3-37. |

|

|

|

|

|

Banimahd B, Bagebani T (2009). Conservatism, governmentownership, size of corporation,leverage. Iran.J. Account. Rev. 16(58): 53- 70. |

|

|

|

|

|

Chi W, Liu C,Wang T (2009). What affects accounting conservatism: A corporate Governance Perspective. J. Contemp. Account. Econ. 5(2):47-59. |

|

|

|

|

|

Ghirmai K (2011). Good governance enhance the efficiency and effectiveness public spending –sub Sahara countries. Afr. J. Bus. Manage. 5(11):3995 – 3999. |

|

|

|

|

|

Hasasyegane Y (2009). Effect of board of directors on corporate governance. J. Hesabdar. 174(21):12-32. |

|

|

|

|

|

Hesiang T, Li-Jen H (2010).Board supervision capability and information transparency. Corporate Governance: Int. Rev. 18(1):18-31. |

|

|

|

|

|

Judge W (2010). Corporate governance mechanisms throughout the world. J .Corporate Governance: An International Review .18(3):159-160. |

|

|

|

|

|

KaramiG, Hosieni SA, Hasani A (2010). Corporate governance and conservatism. Iran J. Account. Res. (4):36-43. |

|

|

|

|

|

Kung F, Cheng C, James K (2010). The effects of corporate ownership structure on earning conservatism : evidence from China. Asia J. Financ.Account. 2(1):48-65 . |

|

|

|

|

|

Lara J , Osma B (2009) . Accounting conservatism and corporate governance. J. Rev Account Stud. 14:161-201. |

|

|

|

|

|

Mashayekh B, Mohamadabadi M, HesarzadehR (2009). Conservatism and stability of earnings. J. Stud.Account. 3(14):25-41. |

|

|

|

|

|

Mehrani K, Halaj M, Hasani A (2009). Conservatism and accrual accounting. Iran. J. Account. Res. 3:88- 99. |

|

|

|

|

|

Midary A (2006) .Relation type of corporate governance and economics Iran. Doctoral Thesis. Tehran University. Tehran. |

|

|

|

|

|

Mohamad N, Ahmed K, Ji X (2010). Accounting conservatism, corporate governance and political influence: evidence from Malaysia. SSRN.COM / ABSTRACT = 1416485 . |

|

|

|

|

|

Nicolae F,Liliana F, Voica D (2010). Comparative legal perspectives on international models of corporate governance . Afr. J. Bus. Manage. 4(18):4135 – 4145 . |

|

|

|

|

|

Piot C, JaninR (2007). External auditors, audit committees,and earnings management in France. J. Eur. Account. Rev. 16(2):429. |

|

|

|

|

|

Rahmani A, Golamzadeh M (2009). General ownership and conservatism. Iran J. Account. Res. 3:12-28. |

|

|

|

|

|

Renders A, Gaeremynck A, Sercu P (2010). Corporate governance ratings andcompany performance: A cross - European study. J. Corporate governance: Int. Rev. 18(2):45-76 . |

|

|

|

|

|

Wang E, Ohogartaigh C, Zijl T (2009). Measures of accounting conservatism: A construct validity perspective. J. Account. Literature 28:165-203. |

|

|

|

|

|

Watts RL (2003).Conservatism in accounting part I: explanations and implications. J. Account. Horizons 17(3):207-221. |

|

|

|

|

|

Young BH, Seok HL, Lee L W (2011) .Value information of corporate decisions and corporate governance practices. Asia –Pacific. J. Financ.Stud. 40:69-108. |

|

|

|

|

|

Yu C (2010).Ownership concentration, ownership control and enterprise performance: Based on the perspective of enterprise life cycle. Afr. J. Bus. Manage. 4(11):2309–2322. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0