Full Length Research Paper

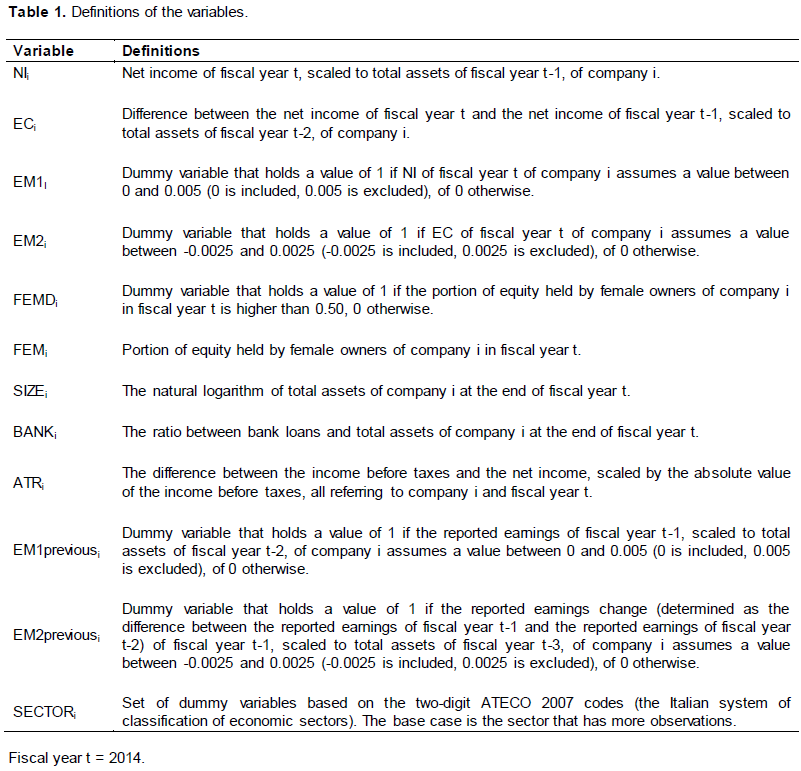

ABSTRACT

The study investigates whether and how gender diversity in ownership structure (here intended as female ownership) is related to private (unlisted) Italian companies’ propensity to engage in earnings management practices, specifically in “earnings minimization” (EM) and “earnings change minimization” (ECM). Companies practice EM when they manage earnings to bring them close to zero. They practice ECM, instead, when they manage earnings to avoid large earnings changes or, in other words, to “smooth” company earnings. Companies that engage in such practices are detected by adopting the earnings distribution approach. The results of chi-square tests for equality of distributions show that the earnings frequency distributions and the earnings change frequency distributions, conditional on the portion of equity held by female owners, are significantly equal from a statistical point of view, demonstrating that gender diversity in ownership structure and private Italian companies’ propensity to engage in EM and ECM are not related. Logit analysis models confirm these findings. The main contribution this study brings to the literature consists in the fact that it is the first study that investigates the relationship between gender diversity in ownership structure and earnings management practices.

Key words: Earnings management, earnings minimization, earnings change minimization, gender diversity, private companies, Italy.

INTRODUCTION

A large body of research has addressed the issue of the relationship between the type and characteristics of shareholders on one side and earnings management practices on the other, analyzing whether and how the former influences the latter. Previous studies have focused on specific types of owners, such as institutional investors (Almazan et al., 2005; Bange and De Bondt, 1998; Bushee, 1998; Chung et al., 2002; Claessens and Fan, 2002; Cornett et al., 2008; Duggal and Millar, 1999; Ebrahim, 2007; Koh, 2003; Porter, 1992; Pound, 1988; Sundaramurthy et al., 2005), public authorities (Aharony et al., 2000; Capalbo et al., 2014; Chen and Yuan, 2004;

Ding et al., 2007; Liu and Lu, 2007; Roodposhti and Chashmi, 2011; Wang and Yung, 2011), or foreign investors (Beuselinck et al., 2013). Although the findings of previous studies are not conclusive, in most cases the existence of a relationship between the type and characteristics of shareholders and earnings management practices has been discovered.

Despite the fact that the relationship between the type and characteristics of shareholders and earnings management practices constitutes a vast area of research, to the best of our knowledge, the issue of whether and how gender diversity in ownership structure (here intended as female ownership) influences earnings management practices has not yet been studied. This could be due to the fact that the influence of gender diversity in ownership structure should be investigated in smaller companies in which equity is held only by individuals. Instead, most of the studies that have investigated whether and how the type and characteristics of shareholders influence earnings management practices, in fact, have focused on public (or listed) companies (e.g. all the studies cited earlier).

To contribute to filling the knowledge gap thus identified, this study investigates whether and how gender diversity in ownership structure is related to private (unlisted) Italian companies’ propensity to engage in earnings management practices, and specifically, in “earnings minimization” (EM) and “earnings change minimization” (ECM). Companies practice EM when they manage earnings to bring them close to zero (Coppens and Peek, 2005; Marques et al., 2011; Poli, 2013a, b, 2015a). They practice ECM, instead, when they manage earnings to avoid large earnings changes or, in other words, to smooth earnings (Coppens and Peek, 2005; Poli, 2013a, 2015a).

LITERATURE REVIEW AND RESEARCH HYPOTHESES

Whether and how the behavior of individuals is influenced by gender in different contexts has been widely investigated in the literature. Byrnes and Miller (1999), for example, have found that women show a greater aversion to risk and are less likely than men to be overconfident. Dwyer et al. (2002), Graham et al. (2002), Jianakoplos and Bernasek (1998), Olsen and Cox (2001), Sunden and Surette (1998), Watson and McNaughton (2007) and Watson and Robinson (2003) have reported similar findings in the field of accounting and finance. Barber and Odean (2001), Bliss and Potter (2002), Johnson and Powell (1994) and Schubert (2006) have found that women seem to be less overconfident on financial matters than men. Ford and Richardson (1994), in their review of the literature, have shown that some studies have found that women behave more ethically than men, while other studies have found that there are no differences between women and men with respect to ethical behavior. Eynon et al. (1997), Khazanchi (1995) and Ruegger and King (1992) have found that women are more ethical in a business context. Bernardi and Arnold (1997) and Betz et al. (1989) have found that women are less likely to engage in unethical behavior in the work place to gain financial rewards.

The fact that the differences highlighted earlier between women and men, especially those related to ethical judgments and behavior, suggests that gender diversity in ownership structure may be related to companies’ propensity to practice earnings management. Because women are more risk averse and they behave more ethically than men, female owners may be less willing to practice earnings management than male owners. It is therefore plausible to assume that female owners should be inclined to contrast earnings management practices both directly, when they are involved in the management of the company (which frequently occurs in smaller companies when female owners hold the requisite portion of equity), and indirectly, when they appoint or influence the appointment of managers that are less inclined to practice earnings management or when they monitor managers’ behavior. Therefore, the research hypotheses that will be tested are the following:

H1: Gender diversity in ownership structure is related to companies’ propensity to engage in EM.

H2: Gender diversity in ownership structure is related to companies’ propensity to engage in ECM.

RESEARCH DESIGN AND SAMPLE SELECTION

The methodology used to detect the presence of EM and ECM is the earnings distribution approach suggested by Burgstahler and Dichev (1997). Although, it has been criticized by some scholars (Beaver et al., 2007; Dechow et al., 2003; Durtschi and Easton, 2005, 2009; Holland, 2004; Lahr, 2014; McNichols, 2003), it has been widely used in the literature (Baber and Kang, 2002; Beatty et al., 2002; Brown and Caylor, 2004; Collins et al., 1999; Coppens and Peek, 2005; Daske et al., 2006; Degeorge et al., 1999; Easton, 1999; Gore et al., 2007; Hamdi and Zarai, 2012; Hayn, 1995; Holland and Ramsay, 2003; Huang and Hsiao, 2011; Jacob and Jorgensen, 2007; Kerstein and Rai, 2007; Marques et al., 2011; Moreira, 2006; Phillips et al., 2004; Poli, 2013a, b, 2015a; Revsine et al., 2009).

In adopting this approach, EM is signaled by the presence of discontinuities between the first negative earnings interval and the first positive earnings interval and between the first positive earnings interval and the second positive earnings interval of the earnings frequency distribution (Coppens and Peek, 2005; Marques et al., 2011; Poli, 2013a, b, 2015a). ECM, on the other hand, is signaled by the presence of discontinuities between the second negative earnings change interval and the first negative earnings change interval and between the first positive earnings change interval and the second positive earnings change interval of the earnings change frequency distribution (Coppens and Peek, 2005; Poli, 2013a, 2015a). A discontinuity emerges if the number of the observations falling in a given interval of the frequency distribution is significantly higher than expected and if the number of the observations falling in one or both of the immediately adjacent intervals of the frequency distribution is significantly lower than expected. To verify the existence of discontinuities, the type of graphical and statistical analysis suggested by Burgstahler and Dichev (1997) is used.

The graphical analysis consists in the construction and exploration of the earnings frequency distribution and the earnings change frequency distribution. To this end, histograms are used, in which the x-axis and the y-axis show earnings or earnings change intervals and frequencies (percentages of the observations falling in each interval), respectively.

The statistical analysis consists in the use of a statistical test in order to verify the statistical significance of the discontinuities that emerge in the graphical analysis.

where Zi is the statistical test referring to interval i with approximately normal distribution; nai is the actual number of observations falling in interval i; nei is the expected number of observations falling in interval i, equal to the average of the number of observations falling in the two adjacent intervals (nai-1 and nai+1); σi is the standard deviation of the differences between the actual and the expected number of observations falling in interval i; ni, ni-1 and ni+1 are the actual number of observations falling in intervals i, i-1 and i+1, respectively; N is the total number of observations; pi, pi-1 and pi+1 are the portions of actual observations falling in intervals i, i-1 and i+1, respectively.

To test the research hypotheses, the earnings frequency distribution and the earnings change frequency distribution, conditional on the portion of equity held by female owners (FEM), are constructed and analyzed in the way described earlier. If FEM is not related to the companies’ propensity to engage in EM and ECM, the conditional frequency distributions will be statistically equal. To verify this, the chi-square test is used.

The study is conducted on the basis of the assumptions that follow: earnings are computed as the net income of the current fiscal year, scaled to the total assets at the end of the previous fiscal year; earnings changes are computed as the difference between the net income of the current fiscal year and the net income of the previous fiscal year, scaled to the total assets at the end of the second previous fiscal year; the earnings interval amplitude is 0.005; the earnings change interval amplitude is 0.0025. They are the assumptions that are normally made in the literature.

To construct the frequency distributions conditional on FEM, FEM is divided into two intervals: up to 0.50 (0.50 is included) and more than 0.50. To test the research hypotheses, logit analysis models are also adopted. They are the following:

EM1i (EM2i) = β0 + β1FEMDi (β1FEMi) + β2SIZEi + β3BANKi + β4ATRi + β5EM1previousi + (β5EM2previousi) + β6SECTORi (2)

All the variables are analytically described in Table 1.

To test the research hypothesis H1, the dependent variable is EM1. To test the research hypothesis H2, it is EM2. The independent variable is, alternatively, FEMD and FEM. Our attention is focused on the statistical significance of its coefficient. The research hypotheses will be confirmed if this coefficient is statistically significant.

A set of control variables is included in order to control for the influence of those factors that previous studies have found to affect companies’ propensity to engage in EM and ECM (Baralexis, 2004; Burgstahler and Dichev, 1997; Marques et al., 2011; Moreira, 2006; Poli, 2013b, 2015a): company size (SIZE), financial incentives (BANK), fiscal incentives (ATR), previously displayed behavior (EM1previous and EM2previous), and industry sector (SECTOR). Consistent with the findings of previous studies, it is expected that the coefficients of all the control variables are positive and statistically significant.

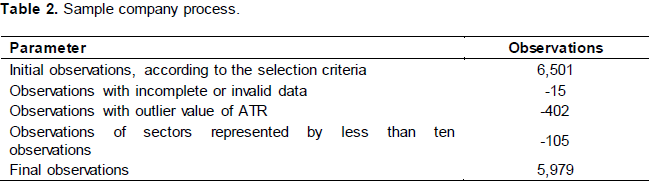

The sample of companies was extracted from the “Analisi Informatizzata Delle Aziende” (AIDA) database supplied by Bureau van Dijk (the date of extraction is 3rd May 2016). The AIDA database provides financial statement data for a vast set of private Italian companies operating in sectors other than the financial one.

It was selected on the basis of the criteria that follow: limited liability companies; active companies; unlisted companies; (non-consolidated) financial statements prepared in ordinary form according to Italian legislation and generally accepted accounting standards in each year of the period 2011 to 2014; number of employees comprised between 10 and 249 in each year of the period 2011 to 2014; balance sheet total of more than € 2 million and up to € 43 million in each year of the period 2011 to 2014; turnover of more than € 2 million and up to € 50 million in each year of the period 2011 to 2014; positive total shareholders’ equity in each year of the period 2011 to 2014; companies that are owned only by individuals.

The number of companies that meet the aforementioned selection criteria amounts to 6,501. To these sample companies, we subtracted (1) the observations with incomplete or invalid data (15), (2) the observations with outlier value of ATR (402), and (3) the observations of sectors represented by less than ten observations (105). Subtraction (2) was considered necessary in order to have a more homogeneous sample of companies on which to conduct the analysis. To identify outlier values of ATR, the Tukey method of leveraging the interquartile range is used. The outlier values are the values below the first quartile decreased by 1.5 times the interquartile range and the values above the third quartile increased by 1.5 times the interquartile range. Subtraction (3) was considered necessary to ensure that each sector was represented by the minimum number of observations considered adequate for the analysis. The final sample companies total 5,979. Table 2 reports the sample company process.

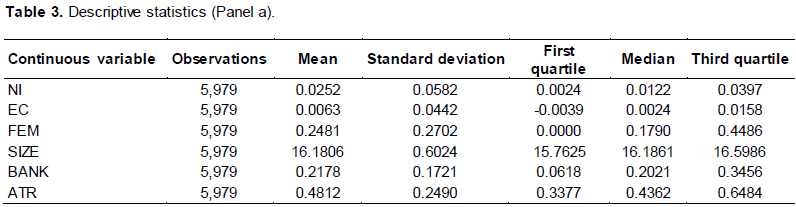

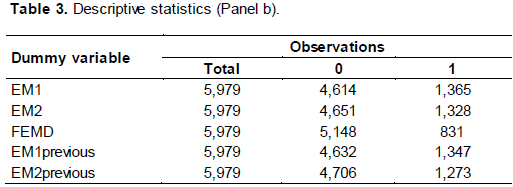

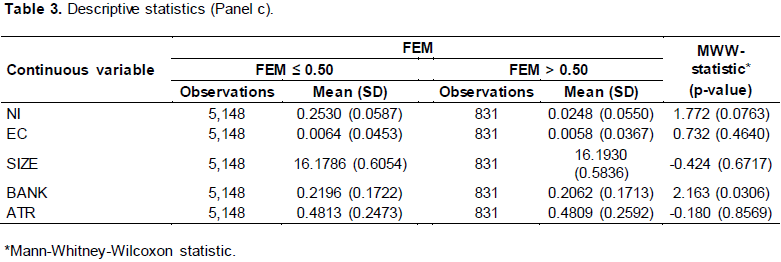

Table 3 shows the main descriptive statistics referring to the sample companies. The companies in which women hold a portion of their equity amount to 33% of the sample.

Those in which they hold the majority of their equity amount to 14% of the sample.

The companies in which men hold the majority of their equity, instead, amount to 79% of the sample. Within the sample, then, female entrepreneurship appears restricted. At the level of statistical significance of 0.05, the differences between the means of NI, EC, SIZE, and ATR, conditioned on FEM, are not statistically significant. At the level of statistical significance of 0.01, also the difference between the means of BANK, conditioned on FEM, is not statistically significant.

With reference to the variables considered, therefore, there are no statistically significant differences between the companies that are controlled by women and the companies that are not controlled by women.

FINDINGS AND DISCUSSION

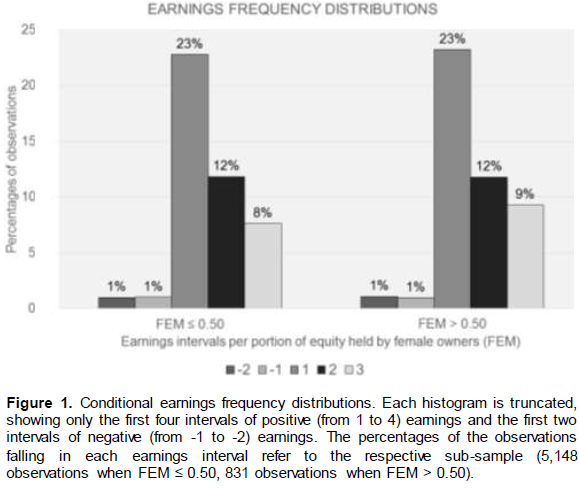

The earnings frequency distributions conditional on FEM are shown in Figure 1. Each histogram in Figure 1 presents a peak of observations in the first positive interval 1, corresponding to the range [0-0.005) and a marked discontinuity both to the left and to the right of it, that are the typical characteristics of earnings management practices aiming to minimize earnings (Coppens and Peek, 2005; Marques et al., 2011; Poli, 2013a, b, 2015a).

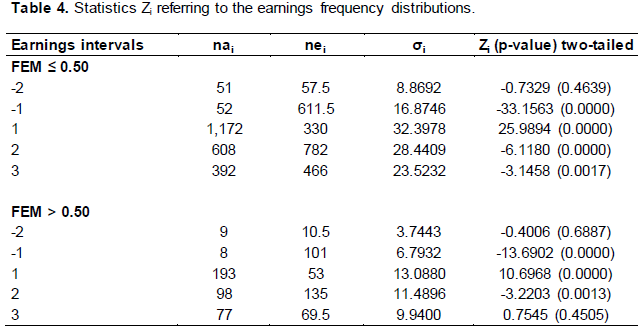

Table 4 shows the test statistics suggested by Burgstahler and Dichev (1997). It shows that, with reference to both histograms in Figure 1, the difference between the actual and the expected number of observations is positive and statistically significant (at a level of 1%) with reference to interval 1, it is negative and statistically significant (at a level of 1%) with reference to interval -1 and with reference to interval 2. Thus, the test statistics confirm the presence of a discontinuity both to the left and to the right of interval 1.

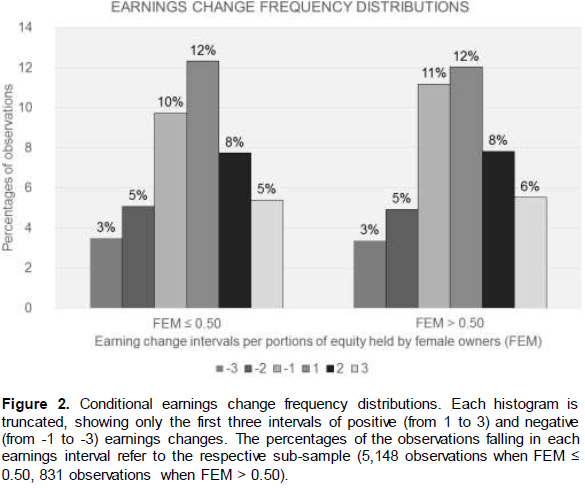

The earnings change frequency distributions conditional on FEM are shown in Figure 2. Each histogram in Figure 2 presents peaks of observations in correspondence to the first negative interval -1, corresponding to the range (-0.00250-0), and to the first positive interval 1, corresponding to the range (0-0.0025) and a marked discontinuity both to the left of the first negative interval and to the right of the first positive interval, that are the typical characteristics of earnings management practices aiming to minimize earnings changes (Coppens and Peek, 2005; Poli, 2013b, 2015a).

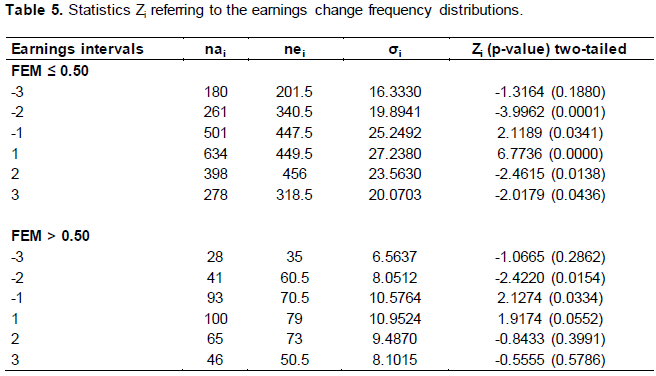

Table 5 shows the test statistics suggested by Burgstahler and Dichev (1997). It shows that, with reference to the histogram to the left of Figure 2 (FEM≤0.50), the difference between the actual and the expected number of observations is positive and statistically significant (at a level of 5%) with reference to interval -1, it is positive and statistically significant (at a level of 1%) with reference to interval 1, it is negative and statistically significant (at a level of 1%) with reference to interval -2, it is negative and statistically significant (at a level of 5%) with reference to interval 2. Thus, the test statistics confirm the presence of a discontinuity to the left of interval -1 and to the right of interval 1. Table 5 also shows that, with reference to the histogram to the right of Figure 2 (FEM>0.50), the difference between the actual and the expected number of observations is positive and statistically significant (at a level of 5%) with reference to interval -1, it is positive and statistically significant (at a level of 10%) with reference to interval 1, it is negative and statistically significant (at a level of 5%) with reference to interval -2, it is negative and statistically not significant with reference to interval 2. Thus, the test statistics confirm the presence of a discontinuity to the left of interval -1, but they do not confirm the presence of a discontinuity to the right of interval 1.

To verify whether the two histograms of each figure are or are not equal from a statistical point of view, the chi-square test is applied. The test statistic assumes value χ2(4)=1.8323 (p-value=0.7666) with reference to the two histograms in Figure 1, value χ2(5)=1.4327 (p-value=0.9207) with reference to the two histograms in Figure 2. Thus, the two histograms in each figure are statistically significantly equal. In other words, the frequency distributions of earnings and the frequency distributions of earnings changes are independent from FEM. Thus, both research hypotheses are rejected.

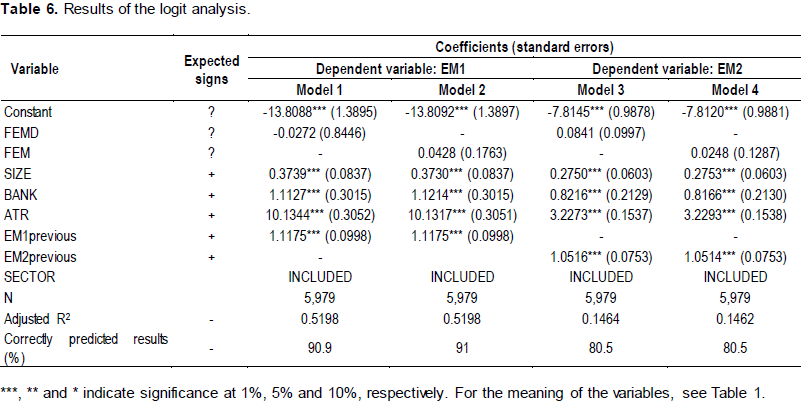

Table 6 shows the results of the logit analysis used to test the research hypotheses. It shows that statistically significant relationships between each configuration of the independent variable (FEMD and FEM) and the companies’ propensity to practice EM and ECM do not exist. Thus, the rejection of both research hypotheses is confirmed. Table 6 also shows that the coefficients of all the control variables are positive and statistically significant, as expected.

The analysis conducted to verify whether the models suffer collinearity issues, that are not reported, has shown that these problems do not exist.

Although several previous studies (most of which were cited in the second section of our study) have shown that women, in different contexts, display more risk-averse and ethical behaviors than men, our findings show that women and men have the same propensity to practice EM and ECM, which, like other earnings management practices, are considered risky and unethical behaviors (Healy and Wahlen, 1999; Roychowdhury, 2006). It is likely that there are some very strong incentives for both women and men to engage in these practices that affect their behavior in the same way. Previous studies (Coppens and Peek, 2005; Marques et al., 2011), and our findings as well, suggest that these incentives may be of a fiscal nature.

In countries such as Italy (Gavana et al., 2013; Poli, 2015b), where there is a close alignment between accounting and tax rules, if there are no other factors that lead people to manifest different behaviors, companies are likely to engage in EM and ECM practices (Coppens and Peek, 2005; Marques et al., 2011). This is due to the impact of two fiscal incentives that work in opposite directions. On the one hand, companies with negative earnings have incentives to manage them upward to overcome the threshold of zero, thus decreasing the probability of investigations or audits by tax authorities. On the other hand, companies with positive earnings have incentives to manage them downward to bring them close to zero, thus minimizing tax payments. As a result, they tend to report slightly positive earnings.

If adopting behaviors that reduce the risk of tax inspections could be consistent with the fact that women are risk averse, engaging in behaviors that reduce the burden of taxes to be paid is not necessarily consistent with the fact that they are ethical. Fiscal incentives, therefore, may strongly influence the behavior of both women and men.

It has been written that fiscal incentives work with the greatest intensity when there are no other factors that lead to different behaviors. Moreira (2006) suggests that one of these other factors could be financial incentives. He has explored the impact of the degree of bank indebtedness on private Portuguese companies’ earnings management practices. He has found that companies with a higher degree of bank indebtedness have a higher propensity to manage earnings upward to avoid losses and a lower propensity to manage earnings downward to minimize tax payments than companies with lower degree of bank indebtedness. He has suggested that “the probability of obtaining the necessary funds at a reasonable cost is positively related to the quality of their accounting numbers, given that bank’s credit decisions are based on firms’ financial information. Thus, this […] incentive tends to motivate firms into adopting accounting choices that provoke an impact on reported earnings in the opposite sense to that related taxes”. It is as if the bank system acts as a controller of earnings management practices of private Portuguese companies. However, our findings have shown that this does not occur in the Italian context. In fact, in the logit analysis models the coefficients of BANK are always positive and statistically significant, demonstrating that the higher the degree of bank indebtedness the higher the propensity to practice EM and ECM. Thus, in the Italian context, the bank system does not act as a controller of earnings management practices of private Italian companies. Probably, this can be due to the fact that Italian banks do not traditionally rely very much on financial reporting when they are considering whether or not to lend money. This is why, especially with reference to the type of organization under analysis in this study, Italian banks almost always approve financing only on the condition of personal guarantees from shareholders.

CONCLUSION

The study has investigated whether and how gender diversity in ownership structure affects private Italian companies’ propensity to engage in EM and ECM, showing that it is not associated with both types of earnings management practices. As previously noted, to the best of our knowledge, this is the first study that has investigated such a relationship in the literature, thus filling this knowledge gap.

In addition, our study extends the current knowledge on the relationship between aspects of corporate governance and earnings management practices in private companies, especially SMEs, and on the earnings quality of Italian companies. These have been under-explored issues in the literature.

The main limitation of our study refers to the method used to detect companies that practice EM and ECM (Dechow et al., 2010). In fact, it is difficult to distinguish companies that report slightly positive earnings and slight earnings changes because of chance circumstances (or as a result of credible alternative explanations including non-accounting issues) from those that report them as a result of earnings management practices. Thus, caution should be used in interpreting the findings. This study notwithstanding, whether and how gender diversity in ownership structure affects earnings management practices remains an insufficiently investigated topic. Therefore, further studies are required to gain a full understanding of this relationship.

CONFLICT OF INTERESTS

The author has not declared any conflict of interests.

REFERENCES

|

Aharony J, Lee CWJ, Wong TJ (2000). Financial packaging of IPO firms in China. J. Account. Res. 38(1):103-126. |

|

|

Almazan A, Hartzell JC, Starks LT (2005). Active institutional shareholders and costs of monitoring: Evidence from executive compensation. Financ. Manage. 34(4):5-35. |

|

|

Baber V, Kang S (2002). The impact of split adjusting and rounding on analysts' forecast error calculations. Account. Horiz. 16(4):277-289. |

|

|

Bange M, De Bondt W (1998). R&D budgets and corporate earnings targets. J. Corp. Financ. 4(2):153-84. |

|

|

Baralexis S (2004). Creative accounting in small advancing countries: The Greek case. Manage. Audit. J. 19(3):440-461. |

|

|

Barber BM, Odean T (2001). Boys will be boys: Gender, overconfidence, and common stock investment. Q. J. Econ. 116(1):261-292. |

|

|

Beatty AL, Ke B, Petroni KR (2002). Earnings management to avoid earnings declines across publicly and privately held banks. Account. Rev. 77(3):547-570. |

|

|

Beaver WH, McNichols MF, Nelson KK (2007). An alternative interpretation of the discontinuity in earnings distributions. Rev. Account. Stud. 12(4):525-556. |

|

|

Bernardi RA, Arnold DF (1997). An examination of moral development within public accounting by gender, staff level, and firm. Contemp. Account. Res. 14(4):653-668. |

|

|

Betz M, O'Connell L, Shepard JM (1989). Gender differences in proclivity for unethical behavior. J. Bus. Ethics 8(5):321-324. |

|

|

Beuselinck C, Blanco B, Garcia Lara JM (2013). The Role of Foreign Shareholders in Disciplining Financial Reporting. |

|

|

Bliss RT, Potter ME (2002). Mutual fund managers: Does gender matter? J. Bus. Econ. Stud. 8(1):1-15. |

|

|

Brown LD, Caylor ML (2005). A temporal analysis of earnings management thresholds: propensities and valuation consequences. |

|

|

Account. Rev. 80(2):423-440. |

|

|

Burgstahler DC, Dichev I (1997). Earnings management to avoid earnings decreases and losses. J. Account. Econ. 24(1):99-126. |

|

|

Bushee B (1998). Institutional investors, long-term investment, and earnings management. |

|

|

Byrnes JP, Miller DC (1999). Gender differences in risk taking: A meta-analysis. Psychol. Bull. 125(3):367. |

|

|

Capalbo F, Frino A, Mollica V, Palumbo R (2014). Accrual-based earnings management in state owned companies: Implications for transnational accounting regulation. Account. Audit. Accountab. J. 27(6):1026-1040. |

|

|

Chen KC, Yuan H (2004). Earnings management and capital resource allocation: Evidence from China's accounting-based regulation of rights issues. Account. Rev. 79(3):645-665. |

|

|

Chung R, Firth M, Kim JB (2002). Institutional monitoring and opportunistic earnings management. J. Corp. Financ. 8(1):29-48. |

|

|

Claessens S, Fan JPH (2002). Corporate governance in Asia: A survey. Int. Rev. Financ. 3(2):71-103. |

|

|

Collins DW, Pincus M, Xie H (1999). Equity valuation and negative earnings: the role of book value of equity. Account. Rev. 74(1):29-61. |

|

|

Coppens L, Peek E (2005). An analysis of earnings management by European private firms. J. Int. Account. Audit. Taxat. 14(1):1-17. |

|

|

Cornett MM, Marcus AJ, Tehranian H (2008). Corporate governance and pay-for-performance: the impact of earnings management. J. Financ. Econ. 87(2):357-373. |

|

|

Daske H, Gebhardt G, McLeay S (2006). The distribution of earning relative to targets in the European Union. Account. Bus. Res. 36(3):137-168. |

|

|

Dechow PM, Ge W, Schrand C (2010). Understanding earnings quality: a review of the proxies, their determinants and their consequences. J. Account. Econ. 50(2-3):344-401. |

|

|

Dechow PM, Richardson SA, Tuna I (2003). Why are earnings kinky? An examination of the earnings management explanation. Rev. Account. Stud. 8(2/3):355-384. |

|

|

Degeorge F, Patel J, Zeckhauser R (1999). Earnings management to exceed thresholds. J. Bus. 72(1):1-33. |

|

|

Ding Y, Zhang H, Zhang J (2007). Private vs state ownership and earnings management: evidence from Chinese listed companies. Corp. Gov. 15(2):223-238. |

|

|

Duggal R, Millar JA (1999). Institutional ownership and firm performance: The case of bidder returns. J. Corp. Financ. 5(2):103-117. |

|

|

Durtschi C, Easton P (2005). Earnings management? The shapes of the frequency distributions of earnings metrics are not evidence ipso facto. J. Account. Res. 43(4):557-592. |

|

|

Durtschi C, Easton P (2009). Earnings management? Erroneous inferences based on earnings frequency distributions. J. Account. Res. 47(5):1249-1281. |

|

|

Dwyer PD, Gilkeson JH, List JA (2002). Gender differences in revealed risk taking: Evidence from mutual fund investors. Econ. Lett. 76(2):151-158. |

|

|

Easton P (1999). Security returns and the value relevance of accounting data. Account. Horiz. 13(4):399-412. |

|

|

Ebrahim A (2007). Earnings management and board activity: An additional evidence. Rev. Account. Financ. 6(1):42-58. |

|

|

Eynon G, Hill NT, Stevens KT (1997). Factors that influence the moral reasoning abilities of accountants: Implications for universities and the profession. J. Bus. Ethics 16(12-13):1297-1309. |

|

|

Ford RC, Richardson WD (1994). Ethical decision making: A review of the empirical literature. J. Bus. Ethics 13(3):205-221. |

|

|

Gavana G, Guggiola G, Marenzi A (2013). Evolving connections between tax and financial reporting in Italy. Account. Euro. 10(1):43-70. |

|

|

Gore P, Pope P, Singh A (2007). Earnings management and the distribution of earnings relative to targets: UK evidence. Account. Bus. Res. 37(2):123-150. |

|

|

Graham JF, Stendardi EJ, Myers JK, Graham MJ (2002). Gender differences in investment strategies: An information processing perspective. Int. J. Bank Mark. 20(1):17-26. |

|

|

Hamdi FM, Zarai MA (2012). Earnings management to avoid earnings decreases and losses: empirical evidence from Islamic banking industry. Res. J. Financ. Account. 3(3):88-107. |

|

|

Hayn C (1995). The information content of losses. J. Account. Econ. 20(2):125-153. |

|

|

Healy PM, Wahlen JM (1999). A review of the earnings management literature and its implications for standard setting. Account. Horiz. 13(4):365-383. |

|

|

Holland D, Ramsey A (2003). Do Australian companies manage earnings to meet simple earnings benchmarks? Account. Financ. 43(1):41-62. |

|

|

Holland D (2004). Earnings management: a methodological review of the distribution of reported earnings approach. |

|

|

Huang SLCLH, Hsiao HC (2011). Study of earnings management and audit quality. Afr. J. Bus. Manage. 5(7):2686-2699. |

|

|

Jacob J, Jorgensen BN (2007). Earnings management and accounting income aggregation. J. Account. Econ. 43(2-3):369-390. |

|

|

Jianakoplos NA, Bernasek A (1998). Are women more risk averse? Econ. Inq. 36(4):620-630. |

|

|

Johnson JEV, Powell PL (1994). Decision making, risk and gender: Are managers different? Br. J. Manage. 5(2):123-138. |

|

|

Kerstein J, Rai A (2007). Intra-year shifts in the earnings distribution and their implications for earnings management. J. Account. Econ. 44(3):399-419. |

|

|

Khazanchi D (1995). Unethical behavior in information systems: The gender factor. J. Bus. Ethics 14(9):741-749. |

|

|

Koh PS (2003). On the association between institutional ownership and aggressive corporate earnings management in Australia. Br. Account. Rev. 35(2):105-128. |

|

|

Lahr H (2014). An improved test for earnings management using kernel density estimation. Euro. Account. Rev. 23(4):559-591. |

|

|

Liu Q, Lu ZJ (2007). Corporate governance and earnings management in the Chinese listed companies: A tunneling perspective. J. Corp. Financ. 13(5):881-906. |

|

|

Marques M, Rodrigues LL, Craig R (2011). Earnings management induced by tax planning: the case of Portuguese private firms. J. Int. Account. Audit. Taxat. 20(2):83-96. |

|

|

McNichols MF (2003). Discussion of "Why are Earnings Kinky? An examination of the earnings management explanation". Rev. Account. Stud. 8(2-3):385-391. |

|

|

Moreira JAC (2006). Are financing needs a constraint to earnings management? Evidence from private Portuguese firms. |

|

|

Olsen R, Cox C (2001). The influence of gender on the perception and response to investment risk: The case of professional investors. J. Behav. Financ. 2(1):29-36. |

|

|

Phillips JD, Pincus M, Rego SO, Wan H (2004). Decomposing changes in deferred tax assets and liabilities to isolate earnings management activities. J. Am. Taxat. Assoc. 26(supplement):43-66. |

|

|

Poli S (2013a). Small-sized companies' earnings management: evidence from Italy. Int. J. Account. Financ. Report. 3(2):93-109. |

|

|

Poli S (2013b). The Italian unlisted companies' earnings management practices: the impacts of fiscal and financial incentives, Res. J. Financ. Account. 4(11):48-60. |

|

|

Poli S (2015a). Do Ownership Structure Characteristics Affect Italian Private Companies' Propensity to Engage in the Practices of "Earnings Minimization" and "Earnings Change Minimization"? Int. J. Econ. Financ. 7(6):193-207. |

|

|

Poli S (2015b). The links between accounting and tax reporting: the case of the bad debt expense in the Italian context. Int. Bus. Res. 8(5):93-100. |

|

|

Porter M (1992). Capital choices: Changing the way America invests in industry. J. Appl. Corp. Financ. 5(2):4-16. |

|

|

Pound J (1988). Proxy contest and the efficiency of shareholder oversight. J. Financ. Econ. 20:237-265. |

|

|

Revsine L, Collins D, Johnson W, Mittelstaedt F (2009). Financial reporting and analysis (4th ed.). New Jersey, NJ: Prentice Hall. |

|

|

Roodposhti FR, Chashmi SN (2011). The impact of corporate governance mechanisms on earnings management. Afr. J. Bus. Manage. 5(11):4143-4151. |

|

|

Roxas M, Stoneback J (2004). The importance of gender across cultures in ethical decision making. J. Bus. Ethics 50:149-165. |

|

|

Roychowdhury S (2006). Earnings management through real activities manipulation. J. Account. Econ. 42(3):335-370. |

|

|

Ruegger D, King EW (1992). A study of the effect of age and gender upon student business ethics. J. Bus. Ethics 11(3):179-186. |

|

|

Schubert R (2006). Analyzing and managing risks - on the importance of gender differences in risk attitudes. Manage. Financ. 32(9):706-715. |

|

|

Sundaramurthy C, Rhoades DL, Rechner PL (2005). A Meta-analysis of the effects of executive and institutional ownership on firm performance. J. Manage. Issues 17(4):494-510. |

|

|

Sunden AE, Surette BJ (1998). Gender differences in the allocation of assets in retirement savings plans. Am. Econ. Rev. 88(2):207-211. |

|

|

Wang L, Yung K (2011). Do state enterprises manage earnings more than privately owned firms? The case of China. J. Bus. Finan. Account. 38(7â€8):794-812. |

|

|

Watson J, McNaughton M (2007). Gender differences in risk aversion and expected retirement benefits. Financ. Anal. J. 63(4):52-62. |

|

|

Watson J, Robinson S (2003). Adjusting for risk in comparing the performances of male- and female-controlled SMEs. J. Bus. Venturing 18(6):773-788. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0