Full Length Research Paper

ABSTRACT

The direction of causality between financial sector and economic growth has remained contentious in Ethiopia. This study investigated their linkage for the period of 1980 to 2014. Granger causality test revealed the existence causality that runs from financial sector to economic growth and not the vis-a-versa, while Johnson cointegration analysis confirmed the existence of long-run relationship between financial sector, labor, foreign aid and economic growth. In the short run, however, saving and foreign aid had impact on economic growth. The error correction indicated a full adjustment to the long run equilibrium takes 10 years. The study implies the need for appropriate financial sector development policy, and setting up of appropriate strategy for saving mobilization, increased foreign direct investment and reduction of heavy dependence on foreign aid.

Key words: Vector auto regressive, Johnson cointegration, Granger causality, impulse response, short run dynamics, financial sector development, economic growth, Ethiopia.

INTRODUCTION

The debate of whether the causal relationship runs from financial sector to economic growth or vise-a versa has not settled yet. As different views held by economists, this relationship can be classified into four perspectives that can be categorizing into supply and demand sides. The supply-side states that financial development has a positive effect on economic growth. For instance, Schumpeter (1912) states that well-functioning banks spur technological innovation by funding entrepreneurs successfully implement innovative products and production processes. Similarly, Hicks (1969) argue that financial development played a critical role in igniting industrialization in England by facilitating the mobilization of capital. According to this view, financial intermediation contributes to economic growth. On the other hand the demand side, Robinson (1952) views that where enterprise leads finance follows. According to this view, as the economy expands, its demand for financial services increases, leading to the growth of these services. Empirical support for this demand-side view is provided by Demetrides and Hussein (1996) and Friedman and Schwartz (1963).

The third perspective of the relationship between financial development and economic growth postulates that the two variables are mutually causal. As stated by Greenwood and Smith (1997), the two variables have bidirectional causality.

Finally, the fourth perspective though not as widely held as the other views, states that financial development and economic growth are not causally related at all (Lucas, 1998). This one is in line with the traditional neo-classical literature on growth suggests that financing is not important. They emphasized that if the financial system is to play a role it can be through its effects on factor accumulation or on innovation. The Ethiopian economy has been controlled by the state through a series of industrial development plans since the imperial government of Haile Selassie (1930 to1974) up until present period. The country has passed through three politically distinct regimes: - the imperial government (1930 to 1974), the pre-reform period/ the Derg regime (1974 to 1991) and the post-reform period (1991 to present). The current economic system of the country is transformed; the economy is seen to be market-based system, though the lion-shared part of the economy is owned by government affiliated companies. The government’s expenditure was higher than its revenue generation capability which led to the poor performance of the economy (MEDaC, 1999). Extensions of credit to sectors other than the central government grew slowly because of the restrictions on the economic activities of the private sector. The fragile and inefficient state-dominated banking sector that existed during the Derg regime was a major hindrance to economic growth (Bezabih and Asayehgn, 2014). The Derg policy of expanding the public and socialized sector at the expense of the private sector also proved to be a failure because of inadequate monetary policy which impaired the development of the financial sector. Relative stability in macroeconomic situations was achieved at the cost of overall economic growth because of the restriction on private sector participation and low productivity of the social sector (MEDaC, 1999).

During all these varieties of reforms efforts were made aiming at improving macroeconomic stability, accelerating economic growth, and reducing poverty. The government adopted a market-oriented economic policy which brought about a significant change in the functioning of the financial sector in recent years. Since it took power in 1991, the current government has implemented a number of reforms that have led to marginal improvements in efficiency and competition; there is a great need for additional market oriented reforms to further enhance the sector’s role in mobilizing savings and allocating funds to their optimum usage (Bezabih and Asayehgn, 2014). Even though state control has been reduced in recent years and domestic and foreign (private) investment promoted, the state still plays a dominant role in the economy today. The financial sector is highly regulated by means of credit restriction, equity market control and foreign exchange control. Furthermore, the banking sector remained isolated from the impact of globalization. The policy makers understand the potential importance of financial liberalization, but it is widely believed that liberalization may result in a loss of control over the economy and may not be economically beneficial (Wondaferahu, 2010). In this connection, the financial sector needs deep understanding so as to find the clear impact it has on the economy. Hence, the primary objective of this study is to examine the relationship between financial sector and the economic growth of the country over the recent three decades.

METHODOLOGY

The structural equation

To establish the relationship between financial sector development and economic growth, the neo-classical growth model which was developed by Solow and Swan (1956) was used. According to Aghion and Howitt (1992), the building block of this model is an aggregate production function with a Cobb-Douglas form that exhibit constant returns to scale was used.

Where Yt is the gross domestic product (GDP), Lt is labor force, St is the ration of saving rate to GDP, PRIVY is ratio of private credit to GDP, FA is foreign aid, OPP is degree of openness measured by the ration of volume international trade to GDP and FDI is foreign direct investment

The vector auto regressive model (VARM)

In developing the structural equation, basically economic theory was referred to model the behavioral relationship among the variables of interest. Unfortunately, economic theory is not often rich enough to provide a dynamic specification that identifies all of these relationships. Estimation and inference are complicated by the fact that endogenous variables may appear on both the left and right sides of the equations in the model. However, the VAR (vector auto regressive) approach sidesteps the need for structural modeling by treating every variable as endogenous in the system as a function of the lagged values of all endogenous variables in the system (Rahman, 2004). The general VAR system of equations can be specified as:

Where Yt is an nx1 vector that contains n variables in the system. αo is an nx1 vector of constants and A1 up to An are nxn and εt is vector of white noise process, with mean zero and constant covariance. Since there are only lagged values of the endogenous variables appearing on the right-hand side of the equations, simultaneity is not an issue and ordinary least squares (OLS) yields consistent estimates. The forecasts obtained by the VAR method are better than those obtained from the more complex simultaneous-equation models.

The vector error correction model (VECM)

Since time-series variables have been widely noted to be non-stationary, the results that are obtained from the level VAR are spurious[1] and misleading (Mukhopadhyay and Pradhan, 2010). Moreover, utilizing properly differenced variables in the VAR may lead to model miss-specification if the level variables share the long run relationship or are co-integrated. In this case the VAR should be written in a VECM form as indicated below (Mukhopadhyay and Pradhan, 2010). The VECM captures both the short and long-run relationships, which can be specified as:

[1] When two variables are trending over time, a regression of one on the other could have a high R2even if the two are totally unrelated

The VEC specification restricts the long-run behavior of the endogenous variables to converge to their co-integrating relationships while allowing a wide range of short-run dynamics. The co-integration term is known as the error correction term since the deviation from long-run equilibrium is corrected gradually through a series of partial short-run adjustments.

The augmented Dickey Fuller (DF) test

Estimation of non-stationary data will cause spurious regression problems in that the least square estimators of the intercept and slope coefficients are not consistent (Wooldridge, 2000). In order to have non-spurious estimation outcome, unit root test using the augmented Dickey Fuller test was applied. The functional form for the test is specified as follows:

Where yt is variable of interest, t is time trend and p is lag length. In the above model ![]() captures the long run relationship, while

captures the long run relationship, while ![]() captures the short run dynamics. The ADF test can be biased towards accepting the null hypothesis of unit root in the series if the series exhibits significant structural breaks (Harris, 1995). Therefore, the data should be first tested for the existence of structural breaks. Differencing may lead to a considerable loss of long run properties of the data. So it is appropriate to develop a statistical tool which suits for capturing long-run relations between non-stationary variables in a right manner. Engle and Granger (1987) developed the theory of co-integration relation so as to provide a solution for this problem.

captures the short run dynamics. The ADF test can be biased towards accepting the null hypothesis of unit root in the series if the series exhibits significant structural breaks (Harris, 1995). Therefore, the data should be first tested for the existence of structural breaks. Differencing may lead to a considerable loss of long run properties of the data. So it is appropriate to develop a statistical tool which suits for capturing long-run relations between non-stationary variables in a right manner. Engle and Granger (1987) developed the theory of co-integration relation so as to provide a solution for this problem.

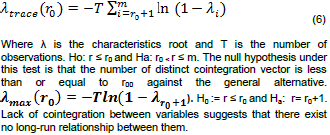

The Johansen co-integration method

The idea of cointegration is to take care of the non-stationarity of the variables and confirm whether there exists a long-run equilibrium relationship. The m x 1 series Yt is co-integrated if Yt is I(1) yet there exists , m x r, of rank r, such that Ζ=β’γ is I(0). The r vectors in are called the cointegration vectors. Even if individual series are non-stationary, their joint distribution can be stationary. For this purpose, the Johansen co-integration method was used, for its known advantage over the Engle-granger approach as expressed below.

The VECM describes how variables are adjusted towards the long-run equilibrium state. The coefficients of the error-correction terms indicate the proportion by which the long-run disequilibrium in the dependent variables is corrected in the short-term period. Johansen represented Ho: π = αβ’ and α and β are (mxr) matrices where the rows of β’ are the r co-integrating vectors while the matrix represents the coefficient of speed of adjustment. This approach enables us to determine the number of co-integrating vectors and estimate the co-integrating vectors. According to Enders (1995), the number of co-integrating vector can be identified based on:

RESULTS AND DISCUSSIONS

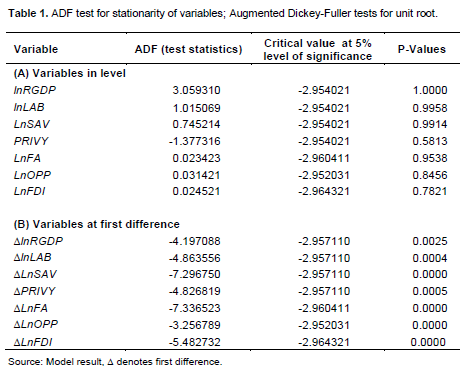

Based on the ADF test (Table 1), the absolute values of the calculated test statistics for all variables are less than its critical value at 5% level of significance, which indicates that all variables are non-stationary at level, that is, the series appears to have unit root. However, after applying the first difference, the data appears to be stationary at first difference. Hence the variables are said to be integrated of order 1.

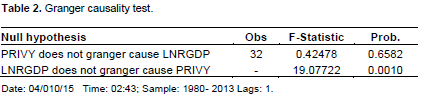

The Pair-wise Granger causality between GDP and financial development indicator PRIVY indicate the acceptance of the null hypothesis that LRGDP does not Granger cause PRIVY, but this study reject the null hypothesis that PRIVY does not Granger cause LRGDP. Therefore, it is shown that granger causality runs one way from PRIVY to GDP and not the other way. Hence, causality is uni-directional from financial sector development to economic growth (Table 2). Therefore, this is a major sign that Ethiopia is still a developing country. This scenario is not different from that of the developed countries: the more the country is developed, the more the financial development is useful to forecast GDP growth (Hurlin and Venet, 2008).

The uni-directional causality from financial development to economic growth may be justified by the fact that: the financial reform of Ethiopia has an immediate effect on economic growth as it facilitate investment and ensure easy flow of finance from one end of the economy to the other; the presence of financial constraints that are imposed on the financial sector, manifest itself in constraining the aspired economic growth rate of the nations. This can be justified by the fact that they interest rates on deposits are centrally controlled, the government interferes with the credit allocation decisions of private banks. Credit is often rationed in favor of larger and more established businesses, where the state-owned enterprises have much better access to credit than private businesses. The state-owned Development Bank of Ethiopia only lends to support the government’s industrial development initiatives, selectively providing capital to firms in sectors were the government wants to promote. Moreover, the National Bank has a directive ordering private commercial banks to buy government bonds worth 27% of the loan disbursements they have made. This measure was set to earn 3% interest while the deposit rates set by the National Bank stand at 5%.

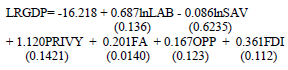

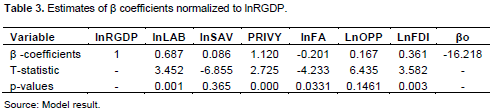

Even though the Johansen trace statistics suggested two co-integrating vectors, based on the objectives of this study only the unrestricted co-integrating vector with ad-hoc normalization on LnRGDP is estimated. Table 3 presents the result. The normalized cointegration equation can be written as:

In this empirical analysis, the covariates are elasticity as the model is specified in log-linear with respect to real GDP. The labor force, financial sector development, foreign aid and FDI have an impact on the real GDP growth in the long run. Holding other factors constant, a 1% increase in labor force increased real GDP per capita by 0.687% which is consistent with endogenous growth theory. Labor force has significant long-run impact on the Ethiopian economy. The possible explanation for this is that the current struggle that Ethiopia is making in transiting from smallholder agriculture based to small and medium enterprise development is highly demanding for labor power. In fact the recent double digit economic growth of Ethiopia is primarily from the labor based productivity and production growth. Saving which is assumed to be the driving force for investment growth remains insignificant detriment of economic growth in the long run. The negative sign contradicts the basic economic theory that saving is the base of economic growth through its impact on investment. Nevertheless, this should be understood from the point of view that domestic saving in Ethiopia has historically remained low and instead development is financed by foreign aid.

With regard to the long run relationship between financial sector development and real GDP growth, there is a strong and positive relationship that is significant at 1% probability level. Holding other things constant, a 1% increase in PRIVY (ratio of credit to private sector to GDP), in the long-run, resulted in 1.12% increase in real GDP. This means, in country like Ethiopia, the most constraint is finance and hence, the development of this sector is crucial for sustainable economic growth. This positive effect of financial sector development on economic growth is theoretically and also empirically supported in the literature by McKinnon (1973). The other critical factor of economic growth in Ethiopia is foreign aid. After several decades, the Ethiopian economy is still dependent on foreign aid. In this regard, the empirical result shows that a 1% increase in foreign would lead to 0.201% in real GDP in the long run, holding other factors constant.

Theoretically and empirically, foreign direct investment is another critical factor for the growth of economy. The growth of the foreign direct investment in Ethiopia has shown significant progress in recent years, especially the past two decades, following the liberalization of certain economic sects. From the empirical result, a 1% increase in the flow of FDI into Ethiopia brings a 0.361% increase in real GDP, while other factors were held constant. This relationship is statistically significant at less than 5% probability level.

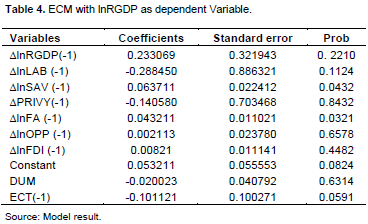

The VEC has cointegration relations built into the specification so that it restricts the long-run behavior of the endogenous variables to converge to their co-integrating relationships while allowing for short-run adjustment dynamics (Harris, 1995). The co-integration term is known as the error correction term since the deviation from long-run equilibrium is corrected gradually through a series of partial short-run adjustments. The error correction terms was lagged by one period (Table 4).

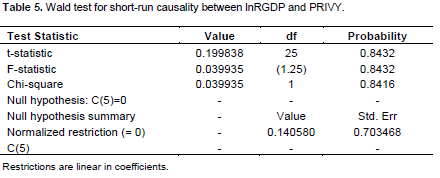

Short-run causality between PRIVY and lnRGDP could be tested from the error correction model using χ2 value of wald statistics. The null hypothesis is that coefficient of DPRIVY is equal to zero against the alternative hypothesis that the coefficient is not equal to zero. The p-value of the chi-square test statistic (Table 5) is more than 5% (0.05). Hence, this study fails to reject the null hypothesis of no short-run causality running from PRIVY to lnRGDP.

In the short-run, all coefficients lagged one period including the dummy variable for regime change are statistically insignificant except for saving and foreign aid. In the short-run domestic saving has statistically significant effect on real GDP. Even though there is still lack of continuous saving behavior in Ethiopia over time, which is still around 19% of the GDP, the empirical result indicate that it is the source of economic growth in the short run. The low level of saving rate in the economy has necessitated increasing reliance on foreign aid to finance investment requirements of the country. Hence, this is evidenced by the fact that foreign aid significant determinant in the empirical result. However, according to Bencivenga and Smith (1991) economic theories though financial development can still promote economic growth, the paramount impact of the shortage of saving cannot be underemphasized, because of the strong linkage it has with investment.

The insignificant coefficient of PRIVY in the short-run might be due to the time lag of the contribution of the private sector to economic growth showing the under-development of the financial sector for short-run impact. Similarly, degrees of openness, foreign direct investment and labor force have a positive but statistically insignificant effect on RGDP in the short-run, unlike their strong impact in the long run. The error correction term is -0.107514 measuring the adjustment of real GDP towards the long-run steady state path, which an implication that each year, about 10.75% of it will be adjusted towards its long-run equilibrium. For full adjustment to take place it needs almost 10 years which shows a slow process.

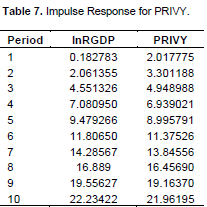

Impulse response function is used to trace the effect of a one standard deviation shock to one of the innovations on current and future values of the endogenous variables. It is possible to identify the positive or negative impact of the variables and determine how long it would take for that effect to work. It is a method of assessing the interaction among the variables in the VAR. This study used the generalized impulse response function because it does not require orthogonalization of innovations and is invariant of the ordering of the variables in VAR.

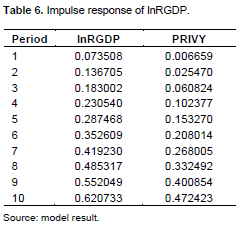

The results of the impulse-response functions (IRF) for the real GDP reveals that in response to one standard deviation shock of lnRGDP and LRGDP itself increases by 0.074 in the first year and continues to grow in the long-run reaching 0.62 in 10th period (Table 6). A one standard deviation disturbance originating from PRIV produces a 0.006 increase in GDP in the first year. Its effect continues to grow as the forecast horizon is extended and reaches 0.47 at the 10th year (Table 6). PRIVY which has a minimum impact on GDP at present and its effect in the current year does not die out, rather it continues to grow over years. In other words, financial development has a long- run impact on economic growth which is consistent with the above findings. The impact of saving and foreign aid which is significant in the current year as compared to PRVIY is also permanent, while their effects vanish in the long-run as compared to PRVIY.

Similarly the impulse response for the PRIV shows that in response to one standard deviation shock of PRIV, PRIV itself increases by 2.02 in the first year and continues to grow in the long-run reaching 21.96 in 10th period (Table 7). A one standard deviation disturbance originating from lnRGDP produces a 0.18 increase in PRIVY in the first year. However, its effect continues to grow and reaches 22.23 at the 10th year.

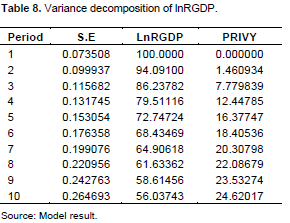

While impulse response functions trace the effect of a shock to one endogenous variable on the other variables in the VAR, variance decomposition separates the variation in an endogenous variable into the component shocks to the VAR. The relative importance of each random innovation in affecting the variables in the VAR can be seen by the variance decomposition results. It highlights the proportion of the movements in the dependent variables as a result of their own shocks, against shocks from the other variables.

The study focuses on the relative importance of endogenous variables in explaining the variation in lnRGDP and PRIVY; hence, the study only decomposes the forecast error variance on lnRGDP and PRIVY. The variance estimates indicate that a greater proportion of the variation in RGDP is due to its own innovations (Table 8). During the first year the variation due to other variables is almost negligible. Over a period of 10 years, the variation due to the other variables grows and reaches a maximum of 43.06. The remaining 56.04% are due to changes in GDP growth itself within the period under consideration. Private credit as percent of GDP has the highest effect on GDP growth followed by foreign aid and labor. In general, 24.62% of future changes in GDP are due to changes in PRIVY, showing the importance of financial development to economic growth.

CONCLUSION

From the empirical result, it can be learned that there existences uni-directional causality from financial development to economic growth. This implies that development of appropriate financial sector drives economic performance over longer period of time. In light of this, the slow progress of the real GDP in the country, which is significantly determined by financial sector development, clearly indicated that the financial sector of the country is still underdeveloped. Hence, it is worth concluding that the substantial gap between saving and investment, which the Ethiopian financial sector is unable to bridge, leads to foreign borrowing to finance investments. Moreover, past performance, saving rate, foreign aid, foreign direct investment and foreign aid in the economy also plays significant role in the present economic conditions. In the long run, the economic improvement initiated by the financial sector creates an economy that will have a resonance of its own; where by present level of the GDP determines the future level of the GDP.

POLICY IMPLICATION

The policy implication from this study could be summarized as follows:

1. The financial sector remained not competitive irrespective of the reform which is said to have taken place over a couple of decades, hence, means has to be in place to improve the competitiveness, efficiency and effectiveness of the industry. This will lay a base that can in turn speed the envisaged double digit economic growth targeted for the 2016 to 2020 growth and transformation plan II. One way of such reform in the financial sector could be subjecting it to some form of competition through the licensing of new banks, of course, taking into account the size of the Ethiopian market. This will help increase the volume of lending and possibly reduce the lending rates and service fees as banks compete for customers. Some of the banks, in a competitive environment, may even start to avail funds to small and medium scale enterprises without collateral security; something which is not significantly happening in Ethiopia in the interim. In addition, the government of Ethiopia may need to relax the regulatory restrictions on private banks in the country and enable the diversification source of its revenue for public investment rather than heavily relying on financial sector as a potential source of ‘’easy’’ resources for the public budget.

2. Given the potential role of saving, the government should enable the national bank to take affirmative action’s like better interest rate on deposit, expansion of branches of financial institutions across the country so as to get closer to the community, diversification of financial services, promotion of education on financial literacy and more. The government should also do more to attract foreign direct investment, diversify the investment ventures and open up the economy for better portfolio investment.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Aghion P, Howitt P (1992). Endogenous Growth Theory. The MIT Press. Cambridge, Massachsets London, England. |

|

|

Bencivenga VR, Smith BD (1991). Financial Intermediation and Endogenous Growth. Rev. Econ. Stud. 58:195-209. |

|

|

Bezabih A, Asayehegn (2014). Banking Sector Reform in Ethiopia. Int. J. Bus. Commerce 3(8):25-38. |

|

|

Demetriades P, Hussein K (1996). Does Financial Development Cause Economic Growth? Time Series Evidence from 16 Countries. J. Dev. Econ. 51:387-411. |

|

|

Enders W (1995). Applied Econometric Time Series. Iowa State University, John Wiley and Sons, Inc. |

|

|

Engle RF, Granger EC (1987). Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica 55(2):251-276. |

|

|

Freidman M, Schwartz Anna J (1963). A Monetary History of the United States: 1867 to 1960 with Princeton University Press, USA. |

|

|

Greenwood J, Smith B (1997). Financial Markets in Development, and the Development of Financial Markets, J. Econ. Dyn. Control 21:145-181. |

|

|

Harris R (1995). Using Co-integration Analysis in Econometric Modeling. London. |

|

|

Hurlin C, Venet B (2008). Financial Development and Growth: A Re-examination on using a Panel Granger Causality Test. |

|

|

Lucas RE (1988). On the Mechanics of Economic Development. J. Monetary Econ. 22:3-42. |

|

|

Ministry of Economic Development and Cooperation (MEDaC), (1999). Survey of the Ethiopian Economy: Review of Post-reform Developments (1992/93-1997/98). Addis Ababa, Ethiopia. |

|

|

Mukhopadhyay B, Pradhan R (2010). An Investigation of the Finance-Growth Nexus: Study of Asian Developing Countries Using Multivariate VAR Model. Inter. Res. J. Finance Econ. Issue 58. |

|

|

Patrick H (1966). Financial Development and Economic Growth in Underdeveloped Countries. Economic Development Cultural Change, 14:174-189. |

|

|

Rahman H (2004). Financial Development-Economic Growth Nexus: A Case Study of Bangladesh. Bangladesh Dev. Stud. 30(3/4):113-128 |

|

|

Robinson J (1952). The Generalization of the General Theory. In: The Rate of Interest and other Essays. London, Macmillan. |

|

|

Schumpeter JA (1912). The theory of economic development. Leipzig: Dunker & Humblot; translated by REDVERS OPIE. Cambridge, MA: Harvard U. Press. |

|

|

Solow M, Swan A (1956) Contribution to the Theory of Economic Growth. Quarter. J. Econ. 70(1):65-94. |

|

|

Wooldridge MJ (2000). Introductory Econometrics: A Modern Approach", 2nd edition. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0