ABSTRACT

The paper examines the contributions of co-operative and saving societies in poverty reduction in Lango and Kigezi sub-region. The study adopted a comparative and cross-sectional survey design where bivariate and multivariate data analyses were used to analyze the data. Specifically, correlation and regression analysis were done to determine the relationship between financial contribution by savings and credit co-operative (SACCOS), saving culture and poverty reduction. The findings established that low-income households had inadequate access to cheap and affordable credit. In the two regions, the available credits offered by SACCOS were not cheap per say and the SACCOS offered credit at 10% per month, which translated into 120% per annum. The study reveals that microcredits create long-term indebtedness among the rural poor, and yet households are not competent in managing their finances. The saving culture in Kigezi sub-region is associated with political motivations and support from politicians. In contrast, in Lango sub-region, saving culture is associated with response to government programs that were aimed at reconstructing northern Uganda after the two decades of insurgency. The provision of more financial services would contribute to poverty reduction and training of households on the utilization of financial credit.

Key words: Cooperative and saving societies, savings and credit co-operative (SACCOS), financial services, poverty reduction.

Cooperative and saving societies have been acknowledged as a crucial means for poverty reduction, and that is why most developing nations have widely adopted it and promoted the growth of the co-operative movement since the colonial period. Develtere et al. (2008) observed that the co-operative movement has been on the growth. Thus in every seven persons, one member belongs to a co-operative and saving group, and the total number of co-operatives have continued to grow. The first era of co-operative movement was taken up with strong stringent government control system through the creation of policies and legislation that supported co-operatives cooperatives as a drive to economic growth and development. The second eras have has been seen by relieving co-operatives from the state of enjoying autonomy and operate a business venture, which response to market demands. Accessing financial products and services are an essential tool in poverty reduction and alleviation at the community and individual level. Different models and approaches have been tried to improve the income levels of individuals, community and ultimately, the government. The introduction of Cooperative and saving societies in the country has recently regained immense consideration as one of the most critical strategies for poverty reduction and alleviation. Arguably, it is assumed that this approach achieves developmental programs with citizens or community participation, and it is seen as a key requirement, which is likely to create a better development outcome through addressing poverty. The Ministry of Trade and Industry in Uganda by 30 August 2012 had registered 13,179cooperatives, which comprised in the areas of savings and credit co-operative (SACCOS), Agriculture and Marketing, Diary, Transport, Housing, Fishing, Multipurpose, and Others. SACCOS was 40%, and Diary was 2% respectively, and for this study, it will concentrate on SACCOS. In a developing country like Uganda, access to credit to the poor in the rural areas is through microfinance schemes (Peace, 2011). The increase in the demand for financial services has brought a need for changes to co-operative societies as a factor in financial inclusion and deepening. Reports have tended to suggest that poverty has been reportedly falling in Africa, but not as rapidly as in South and East Asia. Africa Progress Panel (2014) indicated that Africa's share of global poverty increased from 22.0% in 1990 to 33.0 % in 2010. Over the years, concerned people have neglected the income inequality issue out rightly. Time series data has been documented citing the changes in poverty level, economic growth and macroeconomic drivers of poverty. The performance of the rural economy primarily determines the poverty-alleviating situation. Poverty has continued to receive global attention by international organizations, donor agencies, and civil societies among others in developing countries where the rate is already alarming despite efforts directed towards curbing the problem. Uganda has registered some important success in poverty reduction strategy with the proportion of those living in poverty whether measured using the international or national poverty line shows that more than half still live below the poverty line. According to the national poverty line, the proportion of the population living in poverty line declined from 56.4% in 1993 to 19.7% in 2013, despite the low level of the national poverty line. Uganda has experienced a remarkable decline in poverty and Lango Sub-region experienced the highest decline in poverty levels in Northern Uganda, showing a reduction from 43.7% in 2012/2013 to 32.5% in 2016/2017 (UBOS, 2018). While poverty incidence remained higher in rural areas at 31%, compared to urban areas at 15%, poverty estimate in Uganda has been further disaggregated by region. In their study, Daniels and Minot (2015) observes that in the last ten years Uganda has shown a great reduction in poverty amongst the citizens living under $1.25 and this has shown it as faster than any other country in Sub-Saharan Africa (World Bank, 2015). The poverty trends in Kigezi and Lango regions are not any different from that of other rural areas in the country.

The principle-agency theory has also been used to explain the dynamics in co-operatives. This theory postulates that Principal-agent problems arise because the objectives of the agent are usually not the same as those of the principal, and thus the agent may not always best represent the interests of the principal (Alchian and Demsetz, 1972; Sykuta and Chaddad, 1999). The terms of an agency relationship are typically defined in a contract between the agent and the principal. Because contracts are generally incomplete, "there are opportunities for shirking due to moral hazard and imperfect observability" (Royer, 1999: 50). Richards et al. (1998: 32) pointed to various studies which argued that co-operatives experienced more significant principal-agent problems than proprietary firms due to "the lack of capital market discipline, a clear profit motive, and the transitive nature of ownership.” Cook (1995) developed a five-stage co-operative life cycle that sought to explain the formation, growth and eventual decline of a co-operative. As the co-operative matures and the members become increasingly aware of the inherent problems, as well as the cooperating benefits that may be lost if operations ceased, members and their leadership will have to consider their long-term strategic options (tradeoffs between the benefits and costs) and decide whether to exit, continue, or convert into another business form.

PROBLEM STATEMENT AND RESEARCH QUESTIONS

The global poverty incidence is still high and the developing countries have registered a rising trend, which is worrying (The World Bank Global Findex, 2019). It is noted that every five persons living in developing economies live on less than $ 1.25per day (World Bank, 2018a). Sub-Saharan Africa is highly affected where the proportion of people living below $ 1.25 is 28% followed by Southern Asia at 30% except India at 22%.SACCOS have played a major role in providing financial products and services to the low-income earners in rural and urban areas who are financially excluded by formal financial institutions in many countries (Dibissa, 2015). Savings and Credit cooperatives have played a unique and significant role in providing various financial services in rural areas. The performance of rural SACCOS in mobilizing saving and the provision of credit to their clients have not been satisfactory and these have created a gap in financial mobilizations (Kifle, 2012). Uganda uses SACCOS as a strategy to poverty reduction and or alleviation in the community; however, it has not performed credibly well and therefore it has not played to the expected vital and vibrant role in poverty reduction. While performance reports from different government agencies allude to improvements in poverty levels and hail the number of SACCOS that have increased, not much has been reported about cooperative savings and their capacity to improve poverty. Moreover, no such studies have attempted to compare two distant regions of the country. UBOS (2018) observes that poverty level in Lango stood at 17.6% while the Kigezi sub-region stood at 19.5%.Despite the increasing number of Cooperative and saving societies (SACCOS) in Uganda, Lango and Kigezi sub-regions, the majority of the populations in the two regions are still below the poverty line (UBOS, 2018); thus, necessitating an empirical study to be conducted.

The following research questions guided the study

(i) How do financial services provided by cooperative and saving societies contribute to poverty reduction in Lango and Kigezi sub-region?

(ii) Does the saving culture adopted by members of the SACCOS contribute to poverty reduction in Lango and Kigezi sub-region?

(iii) Is there a relationship between Cooperative and saving societies and poverty reduction in Lango and Kigezi sub-region?

The concept of savings and credit co-operatives societies

The SACCOS also referred to as a credit union is a co-operative financial institution whose ownership and members own control and they operate purposely with the primary objective of providing credits with lower interest rates and providing services to its members (Ikua, 2015). SACCOS operating within the society play a significant role in bringing about broad-based development agenda in poverty alleviation (Tesfay and Tesfay, 2013). The financial products and services provided by conventional banks and micro lenders are facing constraints such as ever-increasing transaction cost, institutional weaknesses, harsh collateral requirements, limited infrastructure and low returns (Mashigo and Schoeman, 2011). Most co-operatives are located both in rural and urban areas with the vast majority only having one branch with membership drawn from the local community (Brown et al., 2015). SACCOS ensure that microfinance service provision expands to include a large number of clients and should introduce entrepreneurial training to all members for effective poverty reduction (Kihwele and Gwahula, 2015). SACCOS offer several financial products and services such as welfare fund, loans, risk management fund, credit facilities to the population (Momanyi and Njiru, 2016). The study conducted by World Bank (2013) notes that citizens are aware of the availability of the several financial products and services provided by multiple financial institutions which meet the needs of the population. Pearlman (2012) notes that additional income sources generated from the micro-credit programs can be used for education, expenditure and saving purpose to address the economic vulnerability.

World Bank (2014) observes that poor households benefited from savings, basic payments and insurance services and notes that microcredit experiences a mixed opinion about the significance of microfinance products and services, which targets a specific group of the population. Bateman (2017) notes that those who get multiple loans from both formal and informal sources to pay off the previous or the running loans end into over-indebtedness or become heavily indebted. Begajo (2018) asserts that SACCOS face several challenges such as shortage of physical capital, irregular savings by members, weak recovery of loans, no collaborations amongst financial institutions and limited support from government. Aniodoh (2018) points out that the government should encourage co-operative professionals to make it a point to educate the public more on their activities and its importance to the national development of the economy. Elem (2019) observes that governments should establish co-operative institutions where rural cooperators could have access to co-operative education programs and training in co-operative management. Mashigo and Kabir (2016) argue that village banks create financial accessibility to the poor households by offering those financial products and services, which are sustainable through mutual agreement, accountability and personal relationships.

The World Bank Global Findex (2019) which assessed financial inclusion worldwide, routinely finds that unaffordability and inaccessibility are the most cited reasons for people not operating a formal savings account (Demirguc-Kunt and Klapper, 2012). Mobilizing funds outside the banking system opens a large stream of additional resources for investment (Porter, 2015). Churk (2015) notes that SACCOS should develop strategies which address the root cause of poverty such as limited capital, insufficient finance, inadequate human resources and other support services that meet the

demands of the rural population other than concentrating in only business.

Olga et al. (2017) posit that most critical challenges facing co-operatives among others include lack of concessionary credit facilities by financial institutions and lack of standardized accounting standards. Aregawi (2014) notes that co-operatives could not generate an adequate substantial amount of profit in their operations. Tumwine et al. (2015) argue that all stakeholders should be involved in the review of the loan terms, and such terms should be adequately communicated to all stakeholders. Members should be allowed to withdraw from their savings when need arises and leave minimum balance as required. Chowa et al. (2010) argue that wealth, proximity to financial institutions, financial education and financial incentives may have an impact on higher savings performance. Further challenges are inadequate infrastructure, enormous documentation requirements and high account fees are associated with lower levels of savings culture (Beck et al., 2008). Evidence indicates very poor savings and investment culture in developing economies relative to most developed economies. However, Chowa et al. (2012) note that despite the barriers, poor people in sub-Saharan Africa, including those in rural areas still save. Banerjee et al. (2010) establish that family planning policies have contributed to an increase in household saving and wealth accumulation for retirement. Alesina and Giuliano (2010) demonstrate that differences in family ties can help explain how a family can have and adopt a saving culture, which would supplement household income in future. Thus stronger family ties could lead to more saving, and the reverse is true.

Fraczek (2011) notes that interest rates motivate and lure one into saving culture. Interest rates on savings are based upon the stated period; fixed deposit has higher interest rates, which can also be negotiated, while ordinary savings pays lower interest rates (Thomas, 2007). A proportionate loan amount that matches with the client needs, reasonable interest rate and adequate savings, regular and consistent repayment of loans and achievement of the scale can lead to sustainability (Nabulya, 2007). Credits enable the population to expand the generation of income activities and support payments of the necessities, which included health, food and education. Urassa and Kwai (2015) argue that the provision of investment advisory services and small loan are some of the financial services offered by formal financial institutions. Access to financial products and services plays a significant role in the fight against poverty. Formal financial institutions take customers’ saving history seriously while advancing any loan to a client (CGAP, 2010). Cheruiyot et al. (2012) observe that the primary objective of SACCOS is the promotion of the economic interest of the welfare of the members of the community by providing borrowings that supports the production and thus reflects the various products offered by SACCOS. Ksoll et al. (2016) found out that access to microcredit facilities through village savings and loan associations improved on the welfare of its members through improved food security and strengthened household income indicators.

Poverty reduction

Reducing poverty requires one to understand poverty and its various dimensions. Nussbaum and Sen (1993) argued that any definition of poverty should be based on people’s capabilities, while Townsend (1979) gave a broader definition of poverty not limited only to subsistence needs. He described poverty as the inability of a person to participate in society due to lack of resources. This resource-based definition of poverty focusing on basic needs has resulted in the “one dollar a day” definition of poverty. It has been criticized for not including non-material elements and also seen as being confined to areas of life where participation or consumption in society are determined by command over financial resources (Lister, 2004). World Bank (2014) describes poverty as “hunger, lack of shelter, being sick and unable to see a doctor, inability to read and write and lack of access to school, high infant mortality, maternal mortality, lack of job and fear of the future. Poverty has become a multidimensional problem in developing and underdeveloped countries. World Bank (2018b) observes that 2.4 billion people live in deplorable conditions spending less than US$ 1.90 each day. These poor low-income households are unable to invest in any meaningful venture due to inadequate access to cheap and affordable credit and financial support.

FAO (2017) notes that the extremely poor people are often located in remote or isolated rural areas, which are poorly connected with the surrounding rural areas. However, investments in infrastructure and basic services often do not reach the more isolated areas, which tend to be more disaster-prone, thus lowering the poverty reduction effect on income growth for more marginalized areas (Barbier and Hochard, 2014). While most countries world over would want to achieve the Sustainable Development Goals to end poverty around the globe, the problem seems to be persistent in developing countries (Elem, 2018). Multidimensional poverty measures are excellent complements of income and consumption because poverty measures provide more in-depth insight into the degrees of deprivation and vulnerability of the extreme poor. OPHI (2018) observes that traditional income-based poverty is measured by capturing the severe deprivations faced by individuals in terms of health, education and living standards.

Khan et al. (2017) point out that micro-credit and training programs cannot reach the poorest and three- quarters of the low-income households do not benefit from any forms of assistance from development partners.

Wichterich (2017) argues that micro-credit creates indebtedness that can cause long-term poverty. Panigrahi (2017) observes that inadequate training programs negatively affect the way households utilize their credits due to incompetence in managing their finance. Lack of capacity and week capital base often force most grassroots SACCOS to offer minimal product range, thereby leaving them unattractive to a broad segment of the rural population (CRDB Microfinance, 2015). SACCOS seem unevenly distributed and have difficulties attracting savings deposits from their members; consequently; lack of saving remains a significant blockage to growth for SACCOS (Distler and Schmidt, 2011). Similarly, (Banturaki, 2012) argues that frauds such as corruption, embezzlement, mis-appropriation of funds and theft of assets result in high administrative cost, which is detrimental to SACCOS’ growth. Anania et al. (2015) note the need to promote good governance practices among SACCOS, provide education and training, increase capacity; ensure proper financial management, better accounting practices, keep records properly and networking.

Eton et al. (2019b) reveal the need for a comprehensive analysis on the current poverty reduction models and their impact on the very poor, in terms of production capacity, owning productive assets and living a meaningful life. Fadun (2014) observes that continuous efforts on the part of stakeholders in a financial sector are necessary to decrease the number of people that are excluded from financial services, thereby alleviating poverty and facilitate income redistribution in developing countries. Rutten and Mwangi (2012) argue that the redistribution of wealth affects the overall level of poverty within countries, although it is difficult to trace the society's segments affected. While it is not the only factor behind growth and poverty reduction, Mmolainyane and Ahmed (2015) consider it as one of the sources, in addition to factors like regulatory issues, governance, law, zero tolerance to corruption and competition are behind raising poverty. Most governments and development partners have changed their focus mainly in the areas of improving welfare, general living standards of the citizens, and economic development to targeting wealth creation, employment generation and poverty reduction (CBN, 2018).

Financial services

Financial service refers to the process involved in acquiring a financial good such as buying a house, a car or a piece of land. In this case, a mortgage loan to acquire a house and an insurance policy to cover a car constitute financial services (Asmundson, 2011; Turkekole, 2015). A report by World Economic Forum (2015) identifies six financial services: payments, market provision, investment management, insurance, deposit and lending, and capital raising. While the services are critical to poverty reduction, deposit and lending, and capital raising have inclinations to rural consumers. Access to affordable financial services, which is a characteristic of developed financial systems, is critical to poverty reduction. The use of basic financial services improves household incomes, increases resilience and lives (Pazarbasioglu et al., 2020). Access to financial services is critical to reducing persistent income inequality. However, the mechanism remains a challenge to many governments, especially in Africa, where one out of five households lack formal access to financial services (Beck et al., 2009). Financial services like banking, saving and investment, debt and equity financing protect the public from uncertainty (Turkekole, 2015). Innovations in financial services focus on adopting mobile banking and internet to improve consumer satisfaction (Mohammad, 2016). However, the adoptions are contextually productive in developed than developing economies. A study by Daze and Dekens (2016) focused on financial services and climate risk management in Uganda. They found that access to savings and credit supports credit risk management especially by diversifying livelihood and sources of income. While banks cater to wealthier clients, poverty reduction requires lending to individuals and entrepreneurs who lack a credit history or official income records (World Bank, 2009). The majority of the populations live outside urban centers and lack access to infrastructure like banking, transport, electricity and roads. This leaves them to one financial service competitor: the mobile money, yet majority of the rural customers lack proper training and interaction with the service (Scharwatt et al., 2014). Alongside infrastructural limitations, customers suffer risks associated to use of financial services. Customers, especially from rural communities encounter difficulty in judging the appropriateness and quality of financial products (Ennew and Sekhon, 2007). There are gaps in the way financial services institutions inspire trust in rural consumers. This seems to justify the role of informal institutions in providing financial services to Uganda’s rural population. Informal financial institutions serve approximately 12% of the rural population in Uganda (Kironde, 2015).

Cooperative and saving societies and poverty reduction

Ramath and Preethi (2014) observe that SACCOS provide small loans and savings facilities to financially excluded individuals from commercial services, and this help develops a key strategy in poverty reduction throughout the world. Bwana and Mwakujonga (2013) note that SACCOS contribute to Gross Domestic Products, leaving most citizens deriving their livelihood through co-operative movements. The establishment of co-operative societies centered on economic growth and development programs that aim at poverty reduction through access to financial services to the micro-entrepreneurs, low-income earners and poor citizens that cannot access similar services from formal banking institutions would be a better strategy (Edeme and Nkalu, 2019). SACCOS play their share of bringing about broad-based development and poverty alleviation (Tesfay and Tesfay, 2013). Urassa and Kwai (2015) find a significant impact of SACCOS on poverty reduction. Microfinance initiatives can effectively address material poverty, the physical deprivation of goods, services, and the income to attain them (Micro Finance Africa, 2018). A Microfinance is known as microcredit with a low-interest rate with a potential tool to encourage the existing and new business opportunities that can subsequently create employment, extra income, and individual monthly income for all as well as the poor (Kaboski and Townsend, 2012). The poor needs access to a variety of financial services such as deposit accounts, credit, and microfinance and payment/transfer accounts. These products can provide households with consumption smoothing and prevent income fluctuation (Akpandjar et al., 2013). Most notably microfinance borrowers often take business loans and use it for other purpose but not limited to medical cost, school fees, Land purchase, burial expenses and others, which makes them venerable (Chan and Lin, 2013).

Providing financial access to the poor is believed to reduce the level of poverty and inequality amongst the community (Miled and Rejeb, 2018). Macroeconomic stability and a sustainable balance of payments should be able to reduce poverty through a trickle-down effect, primarily through job creation. Garon (2013) in his study found out that many countries that have introduced public saving banks are also ranked amongst the highest savings countries today. Awojobi (2019) establishes that while microcredit was a strategy for poverty reduction, some challenges hinder the accessibility to microcredit. Eton et al. (2019a) note that poverty-related problems can be solved as long as citizens are in a position to access cheap capital. This would call for government interventions to review its microcredit policy. Hussaini and Chibuzo (2018) observes that for financial inclusion to be more robust in the rural areas and to make microfinance a more effective means in poverty reduction other services such as education loan, technological support loan, skills training and housing appliance loan should be included in microfinance services. Financial inclusion is a tool that promotes growth and stability while reducing poverty (Soederberg, 2013). Modern economic growth is not possible without a well-functioning monetary and financial system (Suri et al., 2012). Access to finance is an integral part of the mainstream thinking on economic development based on a countries strategy. Omoro and Omwange (2013) observe that the utilization of microfinance loans results in improved household consumption, the standard of living and leading to earning of extra income as well as reduction of unemployment. Also, Alio et al. (2017) note that the government should invest more in SACCOS since they serve to improve the welfare of especially rural households and improve their income.

The study adopted a cross-sectional survey design. In a cross-sectional study, the researcher collects participants’ opinions, attitude and trend on a given phenomenon at one point in time. In the present study, the researchers adopted a cross-sectional design to allow for gathering unbiased and independent data from participants on SACCOs and poverty reduction. The study took a quantitative approach that formed a background for reasoning and debating participants’ opinions. Both primary and secondary information were consulted in developing and designing self-administered questionnaires. The study was conducted in the districts of Lira, Apac and Dokolo in Lango sub-region Northern Uganda and Kabale, Kisoro and Rukungiriin Kigezi sub-region southwestern Uganda. The choice of the districts under study was because the revival of co-operatives had taken shape in those districts. Thirty registered co-operatives were selected from the chosen districts (Ministry of trade, industry and Cooperatives 2017). A target population of 1900 with 320 participants constituting the study sample. The sample size was determined using the Morgan 1970 table. Registered members in registered SACCOs in the selected districts constituted the unit of analysis. From the chosen districts, registered saving groups were chosen to determine the number of respondents needed. We adopted a probability proportional to determine the sample size for each of the Cooperative and saving societies. The categories of participants included executive members, ordinary members, employees and co-operative officers, who were selected purposively. Ordinary members, employees and cooperative officers were randomly selected while executive members were purposively selected (Amin, 2005). Descriptive, Bivariate and Multivariate data analysis was used. Chi-square test was conducted where the correlation of the emerging factor components under co-operative societies was determined, and those of poverty reduction was examined in order to establish the strength of the relationship between co-operatives and saving societies and poverty reduction in Lango and Kigezi sub-region. Regression analysis was used to provide a linear prediction of the study.

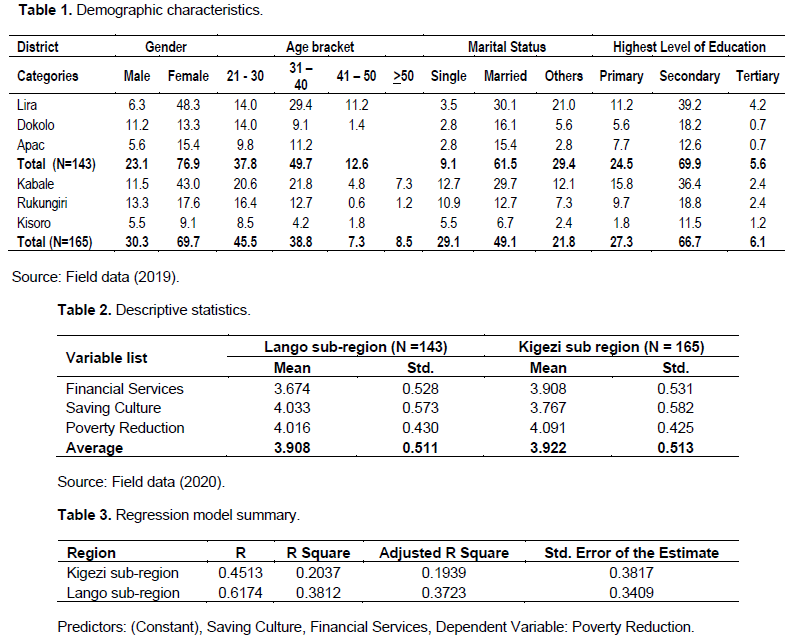

The researchers summarized participants' demographic characteristics on the frequency table. Frequency tables helped to bring out nature and unique attributes embedded in these characteristics. Table 1 summarizes the demographic characteristics of participants. Participation by gender indicates that females dominated the study than men from both regions. In Lango sub-region, 76.9% were female, while 23.1% were male. In Kigezi, 69.7% were female, while 30.03% were male. The dominance of females is associated with the fact that women have less economic assets to present to formal financial institutions as collateral security compared to men. Men in both communities majorly own such assets like land, land titles and cows, which women lack. This implies that women are likely to join co-operative associations than their male counterparts. Secondly, most of the co-operative associations aim at empowering the poor, of which women are amongst the poorest of Uganda's poverty-stricken population (UBOS, 2018). Therefore, recognizable participation of women in the study comes as no surprise.

In Lango sub-region, most of the women (48.3%) came from Lira district while in Kigezi sub-region; most of the women (43.0%) came from Kabale district. The dominance of these districts owes from the fact that Lira and Kabale are Municipalities, with more economic and financial attractions than the rest of the districts under investigation. Secondly, the level of financial inclusion in Lira and Kabale is relatively higher than the other districts in which the study was conducted. The implication of financial inclusion justifies the rate of participation among these districts. In Lango sub-region, Dokolo district had the highest percentage of men (11.2%) who took part in the study’ while Kigezi sub-region, Rukungiri district had the highest percentage of male participants (13.3%).

In respect to age brackets of participants, majority participants from Lango sub-region fell within 31 -40 years (49.7%), while in Kigezi sub-region, majority of the participants fell within 21-30 years (45.5%). The statistics in Lango might relate to higher dependency burden and the need to survive independent of men, while in Kigezi, the statistics are partly due to financial knowledge and partly due to lack of land for cultivation, which pushes women into accessing credit to set-up income-generating projects. The statistics indicate that no participants older than 50 years came from Lango sub-region. In contrast, at least 8.5% of the same age bracket came from Kigezi sub-region, and particularly from Rukungiri and Kabale districts. Perhaps the older persons in Kigezi are empowered economically more than those from Lango sub-region, who survive on the UGX 25,000 per month from the Social Assistant Grant for Elders (SAGE) project.

In respect to marital status, Lango sub-region had more of the married participants (61.5%) than the Kigezi sub-region (49.1%). These statistics might relate to differences in the level of early marriages in both regions. Among the single participants, however, 29.1% came from Kigezi sub-region; while only 9.1% came from Lango sub-region. Perhaps the level of financial literacy is higher among the youths from Kigezi sub-region than from Lango sub-region. The study does not reveal significant differences in the percentage of participants who indicated the 'others' option. However, most of the participants from the two regions who indicated the 'others' option pointed to 'separated' followed by divorce and widowhood.

In respect to education, most of the participants from Lango sub-region (69.9%) and Kigezi sub-region (66.7%) indicated 'secondary' as their highest level of education compared to 'tertiary', which was the least. In practice, most of the educated individuals among which tertiary graduates belong tend to bank with formal financial institutions than with co-operative associations. They consider saving with banks to be more secure and safe than with savings and co-operative associations. The study employed descriptive statistics to portray the status of co-operatives and poverty reduction in Lango and Kigezi sub-region. The researchers adopted the following range of scores to interpret mean scores for financial services, saving culture or poverty reduction:

If 0.0 < mean < 2.0, financial services, saving culture or poverty reduction is ‘irrelevant.’

If 2.0< mean < 3.0, financial services, saving culture, or poverty reduction is 'moderate.'

If 3.0 < mean < 4.0, financial services, saving culture or

poverty reduction is ‘relevant.’

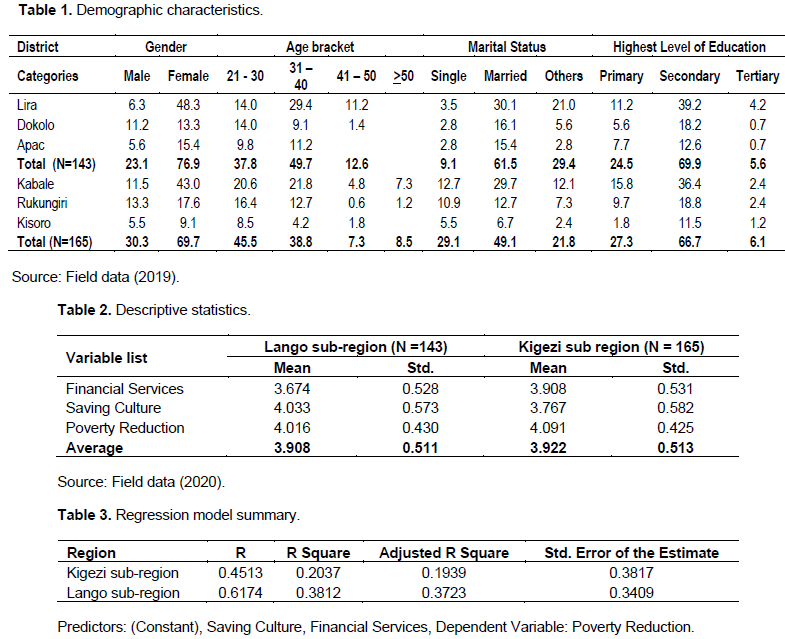

If 4.0 < mean < 5.0, financial services, saving culture, or poverty reduction is 'very high.' (Table 2).

The study considered the financial services provided by co-operatives in Lango sub-region (mean = 3.674; Std. = 0.528) and Kigezi sub-region (mean = 3.098; Std. =0.531) to be relevant to peoples' lives and the economy of Uganda. The standard deviations further indicate that participants' opinions were consistent and therefore, genuine. Similarly, the study indicates saving culture in Lango sub-region with (mean = 4.033; Std. =0.573), and Kigezi sub-region with (mean = 3796; Std. =.582) to be relevant to peoples' efforts to reduce poverty and to improve their standards of living. Consequently, governments' efforts to reduce poverty appear relevant in both Lango (mean = 4.016) and Kigezi (mean = 4.091). In both regions, the study does not indicate any significant differences in participants' opinions on co-operative activities and poverty reduction. The absence of differences in opinion rests on the fact that SACCOS germinate on similar goals and visions ‘fighting poverty through mobilizing savings’. While descriptive statistics appear relevant in detailing the status of financial services and saving culture of poverty reduction in both regions, they are unable to present in quantitative terms the contribution of financial services and saving culture on poverty reduction. To understand the contribution of access to financial services and saving culture on poverty reduction, the researchers used regression coefficients and Adjusted R Square. The adjusted R Square revealed the aggregated amount of variation in poverty reduction predicted by co-operative associations. In contrast, regression coefficients revealed the amount of variation in poverty reduction explained by a unit-change in access to financial services and or saving culture. Table 3 shows the regression model summary.

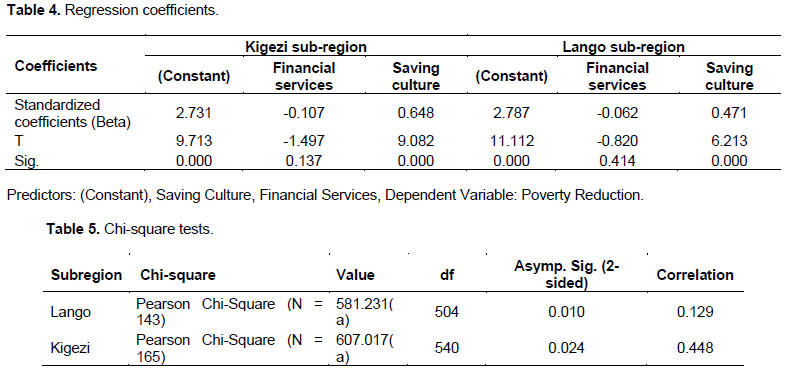

In Kigezi sub-region, the financial services provided by co-operative associations and peoples' saving culture account for 19.4% of the level of poverty reduction, as depicted from (Adjusted R Square = .1934). In Lango sub-region, the financial services provided by co-operative associations and saving culture account for 37.2% of the level of poverty reduction, as depicted from (Adjusted R Square = .3723). These statistics suggest that the financial services provided by co-operative associations in Lango sub-region and the saving culture have contributed to poverty reduction than the case in Kigezi sub-region. In Kigezi sub-region, financial services and members saving culture are associated with a moderate variation in poverty reduction (r = 0.4531). In contrast, in Lango sub-region, the same factors are associated with a substantial variation in poverty reduction (r =0.6174). The reason for the variations in the degrees of association is multifaceted. Formation of co-operative and savings groups in Lango sub-region was perceived as a government's effort towards the socio-economic reconstruction of northern Uganda and was highly embraced. On the contrary, the formation of savings and co-operative groups in Kigezi sub-region was politically driven. People with different political orientations found no need to join these saving groups. Table 4 shows the regression coefficients.

In both sub-regions, the type and nature of financial services provided negligibly reduce poverty. The statistics suggest that saving culture appears to contribute more to poverty reduction than the nature of financial services provided by the savings and co-operative associations.

The significant values (sig. >0.05), suggest that the type and nature of the financial services provided by saving groups are not significant in reducing poverty. In Kigezi sub-region, the type and nature of financial services (β = -0.107) negligibly reduce poverty compared to peoples’ saving culture (β = 0.648) which appears to reduce poverty by 64.8% for every unit-change in saving culture practices. Similarly, in Lango sub-region, saving culture (β = 0.471) appears to reduce poverty by 47.1% for every unit-change in saving culture practices. The reasons for the negligible effect of financial services provided by saving groups on poverty reduction is that formal financial institutions tend to provide similar services at lower rates moreover. For example, most of the saving groups offer their loans at 10% per month, which translates into an interest rate of 120% per annum. This is far high compared to what formal financial institutions provide, that is about 30% per annum. However, the high impact of saving culture on poverty reduction is associated with an informal way of saving and access to savings. Saving groups, due to their informal nature encourage the very poor to save and to borrow.

Hypothesis testing

Hypothesis testing is the statistical technique of verifying a claim or assertion about a population basing on sample results. The researchers denoted H0 as the Null Hypothesis and HA as the Alternative Hypothesis. The Null hypothesis is the claim the researcher's tests while the alternative hypothesis is the claim the researchers accept if the null hypothesis is rejected.

H0: Access to financial services does not play any significant role in poverty reduction.

HA: Access to financial services plays a significant role in poverty reduction.

Since the (sig. < 0.05) in both cases, it means that the observed distribution does not conform to the hypothesized distribution. Therefore, the null hypothesis was rejected and the alternative hypothesis was accepted that access to financial services contributes to poverty reduction (Table 5). Pearson Chi-square (asymp. Sig = 0.010 < 0.05) suggests that there is some association between financial services and poverty reduction in Lango sub-region. However, the correlation (r = 0.129) suggests that the association between financial services provided by co-operative associations and poverty reduction is a weak one. Münkner (1976: 11) argued that efforts to improve the social and economic position of the poor could not be realized if the poor fail to contribute themselves and do not participate actively in self-help actions. The researchers rejected the null hypothesis and accepted the alternative hypothesis that access to financial services plays a significant role in poverty reduction in Lango sub-region. Pearson Chi-Square (asymp. Sig = 0.024 < 0.05) suggests that there is some association between financial services and poverty reduction in Kigezi sub-region. The correlation (r = 0.448) suggests that the association between poverty reduction and the financial services provided by co-operative associations in Kigezi sub-region is moderate. The researcher rejected the null hypothesis and accepted the alternative hypothesis that financial services play a significant role in poverty reduction in Kigezi sub-region.

Rejecting the null hypothesis and accepting the alternative hypothesis confirms the significant role played by financial services in poverty reduction in both Lango and Kigezi sub-region. However, the level of significance varies from one region to the other. In the Kigezi sub-region, financial services play a moderate role in poverty reduction. In Lango, however, financial services play a weak role in poverty reduction. The variation insignificance in both regions is multifaceted. It is moderate in Kigezi because those with secure attachments to the political shorts have access to financial services. Politicians tend to donate much money to Village SACCOS. It is, however, weak in Lango sub-region because the requirement to obtain credit is 'ability to pay'. Therefore, those who fail to demonstrate the ability to pay do not access such financial services and continue in poverty.

The study sought to examine how financial services provided by co-operative associations contribute to poverty reduction in the two regions. The study established a non-significant contribution of financial services on poverty reduction in both regions. The finding is in agreement with World Bank (2007), where it was established that low-income households have inadequate access to cheap and affordable credit and financial support. Consequently, they are unable to invest in meaningful ventures that help them come out of poverty. In line with Kigezi and Lango sub-regions, the available credit offered by SACCOS is not cheap per say. For instance, most of the savings and co-operative groups offer credit at 10% per month, which translates into 120% per annum. This rate is far above the 30% per annum, which is offered by commercial banks. While the rate at which SACCOS offer credit appears 'cheap' theoretically, it is practically expensive and therefore inadequate to help households overcome poverty. This observation supports Wichterich (2017) who concludes that micro-credit creates long-term indebtedness among rural households. Contrary to the rate at which SACCOS provide interest, the very nature of households in terms of managing their finance renders financial services inadequate in poverty reduction. Without exception of whether in Kigezi or Lango sub-regions, rural households, who are the targets of SACCOS, are incompetent in managing finances. This observation is supported by Panigrahi (2017) who observes that most grassroots SACCOS lack adequate programs that train households on how to utilize financial credit. Real cases of incompetence in financial management at household level reveal how many rural households borrow money for a business start-up but channel it to acquiring household assets and consumption.

The study determined if saving culture contributes to poverty reduction in Lango and Kigezi sub-region. The findings established a significant contribution of saving culture on poverty reduction, with a slightly higher contribution of savings culture on poverty reduction in Kigezi than in Lango. The findings is supported Pearlman (2012) who established that the incomes generated from micro-credit could be used in education, expenditure and addressing economic vulnerability. In reality, if members can put to the right use of their savings, they are likely to reduce their financial vulnerability and shocks. Saving culture in Kigezi sub-region is associated to political motivations and backing while in Lango sub-region, saving culture is associated with responding to government programs that were aimed at reconstructing northern Uganda after the two decades of insurgency. The difference in the two places, however, is associated with political drivers. In Kigezi sub-region, SACCOS have the support of the ruling government, which motivates savers. In Lango sub-region, most of the politicians are opposition supporters, which affect financial support from the ruling government. Consequently, the low inflow of financial resources from the ruling government translates into low savings and low poverty reduction.

The findings, however, disagree with (Begajo, 2018) who observed that savings might not contribute to poverty reduction due to irregular savings by members and lack of collaboration between savers and financial institutions. More than often, savers tend to divert savings from economic to non-economic goals. The findings disagrees with that of Bateman (2017), who observed that those who get involved in multiple loans become heavily indebted, and such actions do not reduce poverty. The researcher finds that though actions on the part of savers may not contribute to poverty reduction, some actions on the part of saving associations do not contribute to poverty reduction. For instance, some co-operatives lack concessionary credit facilities and standardized accounting standards (Olga et al., 2017), have limited capital, insufficient finance, inadequate human resources and support services (Churk, 2015). These practices handicap SACCOS from contributing to poverty reduction in Uganda.

The study sought to establish the relationship between co-operatives and savings and poverty reduction in the two regions of Kigezi and Lango. The relationship between co-operative associations and poverty reduction in Kigezi and Lango was moderate and vigorous, respectively. The findings agrees with (Ramath and Preethi, 2014), who established that SACCOS provide small loans and saving facilities to those who are financially excluded from commercial services. The poor can use these loans and savings to establish income-generating projects for their households. The findings agree with (Bwana and Mwakujonga, 2013; Edeme and Nkalu, 2019) who assert that SACCOS contribute to GDP since citizens derive their livelihood and provide access to financial services to micro-entrepreneurs, low-income earners and poor citizens. The researcher’s findings maintain that the way individuals use finance from SACCOS determines how such finances contribute to poverty reduction. Access to financial services from SACCOS has coupled with improper use does not contribute to poverty reduction. The study also tested the hypothesis that access to financial services does not play any significant role in poverty reduction. The researchers rejected the null hypothesis and accepted the alternative hypothesis that access to financial services plays a significant role in poverty reduction in both Lango and Kigezi sub-region. The findings is supported Urassa and Kwai (2015) as well as Miled and Rejeb (2018) who found a significant impact of SACCOS in poverty reduction.

CONCLUSION AND IMPLICATIONS

The study examined the contribution of co-operative and saving societies on poverty reduction, drawing reference to Lango and Kigezi sub-region. The study established a moderate association between co-operative activities and poverty reduction in Kigezi sub-region, and a strong association in Lango sub-region. The introduction of SACCOS in Lango sub-region followed a government program to reconstruct northern Uganda after the Lord's Resistance Army (LRA) war that lasted close to two decades. Consequently, several rural poor from the north embraced SACCOS as a fight against poverty. In Kigezi, however, SACCOS were politically introduced and popularized under the multiparty system. Consequently, their economic effect on the poor Bakiga took a political propensity. These conclusions appear to contradict our hypothetical conclusion, in which we accepted the claim that access to financial services plays a moderate and significant role in poverty reduction in Kigezi sub-region, and a weak role in Lango sub-region. The researchers maintain that individuals with secure attachments to politically backed SACCOS in Kigezi sub-region have access to financial services and are likely to take strides in poverty reduction than those who do not have. In Lango sub-region, however, individuals with 'the ability to pay' have access to financial services and are likely to take strides in poverty reduction than their counterparts who do not have. In effect, a good number of older persons in Kigezi sub-region appear to be economically empowered. At the same time, their counterparts from Lango sub-region survive on UGX 25,000 under the SAGE program. The contribution of saving culture to poverty reduction is likely to be higher than access to financial services because SACCOS promote informal savings, which are characteristic of the rural poor in both Kigezi and Lango sub-region. The fact that financial services play a significant role in poverty reduction confirms the relevancy of the principal-agency theory in explaining the dynamics in co-operatives and offers an extension to its adoption in explaining government interventions in uplifting the welfare of its citizenry. These findings offer foundations to policy reviews and designs in poverty reduction in especially in Uganda, where the overall vision and mission of promoting SACCOS stands in a mess. The government, through the ministry of co-operatives, should revise the tenets upon which co-operative movements were built. This will shape the functioning of SACCOS to the benefit of those who are incapacitated due to poverty. The researchers found that more women than men are members of SACCOS, which relates to the ownership of commercial assets (land and cows). Accordingly, women cannot access financial services from formal institutions, which require collateral security and guarantors. Government, through the Ministry of Gender, should continue prioritizing women economic empowerment to empower women socially and economically. The researchers found that most of the participants from the two regions had 'secondary' as the highest level of education. Government and district leaders should sensitize girls to join tertiary education, which can help them to be economically empowered. The study established that financial services contribute to poverty reduction but to smaller degrees than saving culture. Future researchers should consider examining the limiting factors to access to financial services and their effect on poverty reduction in Uganda.

The authors declared no conflict of interest in the work.

REFERENCES

|

Africa Progress Panel (2014). Grain Fish Money: Financing Africa's Green and Blue Revolutions: Africa Progress Report 2014. Africa Progress Panel.

|

|

|

|

Akpandjar GM, Quartey P, Abor J (2013). Demand for financial services by households in Ghana. International Journal of Social Economics 40(5):439-457.

Crossref

|

|

|

|

|

Alchian AA, Demsetz H (1972). Production, information costs, and economic organization. American Economic Review 62(5):777-795.

|

|

|

|

|

Alesina A, Giuliano P (2010). The Power of the Family. Journal of Economic Growth 15(2):93-125.

Crossref

|

|

|

|

|

Alio D, Okiror JJ, Agea JG, Matsiko FB, Ekere W (2017). Determinants of credit utilization among SACCO members in Soroti District, Uganda. African Journal of Rural Development 2(3):381-388.

|

|

|

|

|

Amin ME (2005). Social Science Research Methods: Conception, Methodology and Analysis, Makerere University, Kampala.

|

|

|

|

|

Anania P, Gikuri A, Hall JN (2015). SACCOS and members' expectations: Factors affecting SACCOS capacity to meet members' expectations. In A Paper Presented to the Co-operative Research Workshop held on 24th March, 2015 at JK Nyerere Hall, Moshi Co-operative University (MoCU).

|

|

|

|

|

Aniodoh AN (2018). The effect of Cooperative Professionals in National Development: A Study of selected Co-operatives in Enugu State. International Journal of Academic Research in Economics and Management Sciences 7(3):441-456.

Crossref

|

|

|

|

|

Aregawi GT (2014). Financial performance of rural saving and credit cooperatives in Tigray, Ethiopia. Research Journal of Finance and Accounting 5(17):63-74.

|

|

|

|

|

Asmundson I (2011). Back to Basics-What are financial services? How consumers and businesses acquire financial goods such as loans and insurance. Finance and Development-English Edition 48(1):46-47.

|

|

|

|

|

Awojobi ON (2019). Microcredit as a strategy for poverty reduction in Nigeria: a systematic review of literature. Global Journal of Social Sciences 18(1):53-64.

Crossref

|

|

|

|

|

Banerjee A, Meng X, Qian N (2010). The Life Cycle Model and Household Savings: Evidence from Urban China. mimeo, Yale University (New Haven: Yale University).

|

|

|

|

|

Banturaki JA (2012). Tanzania co-operatives: their role in socio-economic development. Perspectives for Co-operatives in East Africa. Kampala.

|

|

|

|

|

Barbier EB, Hochard JP (2014). Poverty and the spatial distribution of rural population. The World Bank.

Crossref

|

|

|

|

|

Bateman M (2017). Post-War reconstruction and development in Cambodia and the destruction role of microcredit. Paper presented at the 8th International Scientific Conference" Future World by 2050", Pula Croatia, June 1-3rd, 2017.

|

|

|

|

|

Beck T, Demirguc-Kunt A, Honohan P (2009). Access to financial services: Measurement, impact and policies. World Bank Observer.

Crossref

|

|

|

|

|

Beck T, Demirguc-Kunt A, Peria MS (2008). Banking Services for everyone?Barriers to bank access and use around the world. World Bank Economic Review 22:397-430.

Crossref

|

|

|

|

|

Begajo MK (2018). The Role of Saving and Credit Cooperatives in Improving Rural Micro Financing: The Case of Bench Maji, Kaffa, Shaka Zones.

Crossref

|

|

|

|

|

Brown A, Mackie P, Smith A (2015). Microfinance and economic growth: Rwanda. Inclusive Growth: Rwanda Country Report, Cardiff School of Geography and Planning.

|

|

|

|

|

Bwana K, Mwakujonga J (2013). Issues in SACCOS Development in Kenya and Tanzania. The Historical and Development Perspectives. Developing Countries Studies 1(3):5.

|

|

|

|

|

Central Bank of Nigeria (CBN) (2018). A Quarterly Publication of the Financial Secretariat 2nd Quarter. Central Bank of Nigeria Financial Inclusion Newsletter. 2018

|

|

|

|

|

CGAP (2010). Advancing Saving Services: Resource Guide for Funders.

|

|

|

|

|

Chan SH, Lin JJ (2013). Financing of Micro and Small enterprises in China: An exploratory study. Strategic Change 22:431-446.

Crossref

|

|

|

|

|

Cheruiyot TK, Kimeli CM, Ogendo SM (2012). Effect of saving and Credit Co-operative Societies Strategies on Members' Saving Mobilization in Nairobi, Kenya. International Journal of Business and Commerce 1(11):40-63.

|

|

|

|

|

Chowa GA, Massa RD, Sherraden M (2012). Wealth effects of an asset-building intervention among rural households in sub-Saharan Africa. Journal of the Society for Social Work and Research 3:329-345.

Crossref

|

|

|

|

|

Chowa GAN, Ansong D, Masa R (2010). Assets and Child well-being in developing countries: A research review. Children and Youth Services Review 32:1508-1519.

Crossref

|

|

|

|

|

Churk JP (2015). Contributions of savings and credit co-operative society on Improving Rural Livelihood in Makungu Ward Iringa, Tanzania. Proceedings of the second European Academic Research Conference on Global Business, Economics, Finance and Banking (EAR15Swiss Conference). Zurich-Switzerland, 3-5 July 2015 Paper ID: Z550

|

|

|

|

|

Cook ML (1995). The future of U.S. agricultural co-operatives: A neo-institutional approach. American Journal of Agricultural Economics 77(5):1153-1159.

Crossref

|

|

|

|

|

CRDB Microfinance (2015). Common Problems Faced by Grassroots Financial Intermediaries.

|

|

|

|

|

Daniels L, Minot N (2015). Is Poverty Reduction Over Stated in Uganda? Evidence from Alternative Poverty Measures. Social Indicators Research 121:115-133.

Crossref

|

|

|

|

|

Daze A, Dekens J (2016). Financial services for climate-resilient value chains: The case of the Centenary Bank in Uganda. International Institute for Sustainable Development (IISD).

|

|

|

|

|

Demirguc-Kunt A, Klapper L (2012). Measuring Financial Inclusion: The Global FindexDatabase. Policy Research Working Papers, Washington, DC: The World Bank.

Crossref

|

|

|

|

|

Develtere P, Pollet I, Wanyama F (2008). Cooperating out of poverty: The renaissance of the African co-operative movement. Dar es Salaam, ILO, World Bank Institute.

|

|

|

|

|

Dibissa N (2015). Determinants of Savings and Credit Cooperatives Societies (SACCOs) outreach in Addis Ababa. Addis Ababa University, Ethiopia.

|

|

|

|

|

Edeme RK, Nkalu CN (2019). Reducing inequality in developing countries through microfinance: Any correlation so far? In handbook research on micro-financial impacts on women empowerment, Poverty and Inequality IGI Global, 2019, 281-301

Crossref

|

|

|

|

|

Elem EO (2018) Sustainable Security in Nigeria through poverty reduction: Issues and Challenges. South East Journal of Political Science 4(2):265-277.

|

|

|

|

|

Elem EO (2019). Co-operatives and Eradication of Poverty and Hunger in Rural Communities in South-East Nigeria through Inclusive Sustainable Agricultural Development: Issues and Challenges. United Nations Inter-Agency Task Force on Social and Solidarity Economy.

|

|

|

|

|

Ennew C, Sekhon H (2007). Measuring trust in financial services: the Trust Index. Consumer Policy Review 17(2):62-68.

Crossref

|

|

|

|

|

Eton M, Ayiga N, Agaba M, Mwosi F, Ogwel BP (2019a). Small Medium Enterprises (SMEs), Environmental Management and Poverty Reduction in Western Uganda.

|

|

|

|

|

Eton M, Odubuker PE, Ejang M, Ogwel BP, Mwosi F (2019b). Financial Accessibility and Poverty Reduction in Northern Uganda, Lango Sub-Region.

|

|

|

|

|

Food and Agriculture Organization (FAO) (2017). The state of food and agriculture. Leverage food systems for inclusive rural transformation. Rome, FAO. 160p.

|

|

|

|

|

Fadun SO (2014). Financial inclusion, tool for poverty alleviation and income redistribution in developing countries: Evidences from Nigeria. Academic Research Journal International 5(3):137-146.

|

|

|

|

|

Fraczek B (2011). The factors affecting the level of household savings and their influence on economy development. 8th International Scientific Conference Financial Management of Firms and Financial Institutions. Ostrava: VSB_TU Ostrava.

|

|

|

|

|

Garon SM (2013). Promoting Savings and Financial Literacy: Historical and Global Perspectives on the Institutional Framework. Proceedings of the OECD/Infe/Gflec Global Policy Research Symposium To Advance Financial Literacy. A

|

|

|

|

|

Hussaini U, Chibuzo IC (2018). The effects of financial inclusion on Poverty reduction: The moderating effects of microfinance. International Journal of Multidisciplinary Research and Development 5(12):188-198.

|

|

|

|

|

Ikua KS (2012). Effect of Credit Management practices on financial Performance of Savings and credit co-operative societies in Hospitality Industry in Nairobi. Masters Thesis, University of Nairobi.

|

|

|

|

|

Kaboski JP, Townsend RM (2012). The impact of credit on Village Economies. American Economic Journal: Applied Economics 4(2):98-133.

Crossref

|

|

|

|

|

Khan IH, Bibi S, Javaid A (2017). Solving Poverty through Management: Experience in Pakistan. European Online Journal of Natural and Social Sciences 6:637-645.

|

|

|

|

|

Kifle TS (2012). The Impact of Savings and Credit Cooperatives in Ofla Wereda Tigray Region of Ethiopia. European Journal of Business and Management 4(3):78-89.

|

|

|

|

|

Kihwele EA, Gwahula R (2015). Impact of Saving and Credit Cooperative Societies in Poverty Reduction. Empirical Evidence from Tanzania. European Journal of Business Management 7(23):104-110.

|

|

|

|

|

Kironde SI (2015). Overview of the financial sector in Uganda. Kampala: Bank of Uganda.

|

|

|

|

|

Ksoll C, Lilleør HB, Lønborg JH, Rasmussen OD (2013). Impact of Village Savings and Loan Associations: Evidence from a cluster randomized trial. Journal of Development Economics 120:70-85.

Crossref

|

|

|

|

|

Lister R (2004). Poverty. Loughborough University.

|

|

|

|

|

Mashigo MP, Schoeman CH (2011). Micro credit and the transforming of uncertainty since 1976: international lessons for South Africa. New Contree 62:149-176.

|

|

|

|

|

Mashigo P, Kabir H (2016). Village banks: A Financial Strategy for Developing the South African Poor Households. Banks and bank System 11(2):8-13.

Crossref

|

|

|

|

|

Miled KBH, Rejeb JEB (2018). Can Microfinance Help to reduce poverty? A Review of Evidence from developing countries. Journal of Knowledge Economy 9(2):613-635.

Crossref

|

|

|

|

|

Ministry of Trade, Industry and Cooperatives- Uganda (2017). Sustainable cooperatives, competitive trade and world class industrial products and services.

|

|

|

|

|

Mmolainyane KK, Ahmed AD (2015). The impact of financial integration in Botswana. Journal of Policy Modeling 37(5):852-874.

Crossref

|

|

|

|

|

Mohammad GN (2016). Research on financial services innovations: A quantitative review and future research directions. International Journal of Bank Marketing 34(7):1042-1068.

Crossref

|

|

|

|

|

Momanyi OJ, Njiru A (2016). Financial Risk Management and Performance of Savings and Credit Co-operative Societies in Nakuru East Sub-County, Kenya. International Journal of Research in Business Management 4(4):56-66.

|

|

|

|

|

Münkner H (1976). Co-operatives for the Rich or for the Poor? With Special Reference to Co-operative Development and Co-operative Law in Asia. Asian Economies 17:32-54.

|

|

|

|

|

Nabulya J (2007). Loan Terms and Clients Retention. Research report submitted to school of Postgraduate studies Ndeje University Kampala Uganda.

|

|

|

|

|

Nussbaum M, Sen A (1993). The quality of life. Clarendon Press.

Crossref

|

|

|

|

|

Olga A, Gladys A, Anyango W (2017). Factors affecting the financial performance of savings and credit co-operative society in Kenya: A Case of Mwalimu Saving and Credit co-operative society. Imperial Journal of Interdisciplinary Research 3(4):1476-1487.

|

|

|

|

|

Omoro NO, Omwange AM (2013). The utilization of microfinance loans and household welfare in the emerging markets. European International Journal of Science 2013:59-78.

|

|

|

|

|

Oxford Poverty and Human Development Initiative (OPHI) (2018). Global Multidimensional poverty index 2018. Oxford, UK.

|

|

|

|

|

Panigrahi RK (2017). Role of self-help group on Poverty Alleviation: A Study in Western Odisha. International Journal of Research in Business Studies 2:127-136.

|

|

|

|

|

Pazarbasioglu C, Mora AG, Uttamchandani M, Natarajan H, Feyen E, Saal M (2020). Digital Financial Services, World Bank Group.

|

|

|

|

|

Peace K (2011). Small Savings and Credit Schemes and Financial Accessibility in Rural areas: A Case study of Mitaaana SACCO in Rukungiri District. Master Thesis, Makerere University, Kampala.

|

|

|

|

|

Pearlman S (2012). Too Vulnerable for Microfinance? Risk and vulnerability as determinants of microfinance selection in Lima. The Journal of Development Studies 48:1342-1359.

Crossref

|

|

|

|

|

Porter B (2015). A means to an end: The post-2015 future of financial inclusion. New York: UNCDF.

|

|

|

|

|

Ramath P, Preethi (2014). Microfinance in India- for Poverty Reduction. International Journal of Research and Development-A Management Review 2(4):20-23.

|

|

|

|

|

Richards TJ, Klein KK, Walburger A (1998). Principal-agent relationships in agricultural cooperatives: An empirical analysis from rural Alberta. Journal of Cooperatives 13:21-33.

|

|

|

|

|

Royer JS (1999). Co-operative organizational strategies: A neo-institutional digest. Journal of Cooperatives 14:44-67.

|

|

|

|

|

Rutten M, Mwangi M (2012). Mobile Cash for Nomadic Livestock Keepers: The Impact of the Mobile phone money innovation (M-pesa) on Maasai pastoralist in Kenya. Transforming Innovations in Africa: explorative studies on appropriations in African Societies, Leiden: Brill. pp. 79-102.

Crossref

|

|

|

|

|

Scharwatt C, Katakam A, Frydrych J, Murphy A, Naghavi N (2014). State of the Industry: Mobile Financial Services for the Unbanked. Retrieved November, 7, 2015.

|

|

|

|

|

Soederberg S (2013). Universalizing Financial Inclusion and the Securitization of Development. Third World Quarterly 34(4):593-612

Crossref

|

|

|

|

|

Suri T, Jack W, Stoker TM (2012). Documenting the birth of a Financial Economy. Proceedings of the National Academy of Science 109(26):10257-10262.

Crossref

|

|

|

|

|

Sykuta ME, Chaddad FR (1999). Putting theories of the firm in their place: A supplemental digest of the new institutional economics. Journal of Cooperatives 14:68-76.

|

|

|

|

|

Tesfay H, Tesfay A (2013). Relative efficiency of rural saving and credit cooperatives: An application of data envelopment analysis. International Journal of Cooperative Studies 2(1):16-25.

Crossref

|

|

|

|

|

The World Bank Global Findex (2019). Global Financial Development Report 2019 / 2020: Bank Regulation and Supervision a Decade after the Global Financial Crisis. Washington, DC. World Bank.

Crossref

|

|

|

|

|

The World Bank (2013). The New Microfinance Handbook: A Financial Market System Perspective. 2013. International Bank for Reconstruction and Development/ the World Bank 1818 H Street NW, Washington DC.

|

|

|

|

|

Thomas JS (2007). SACCO saving product development training guide: USAID funded project. Chemonics International Inc.

|

|

|

|

|

Townsend P (1979). Poverty in United Kingdom. A survey of household resources and standards of living. Los Angeles: University of California Press.

|

|

|

|

|

Tumwine F, Mbabazi M, Jaya S (2015). Savings and Credit Co-operatives (SACCOs) Services Terms and Members Economic Development in Rwanda: A Case study of Zigama SACCO Ltd International Journal of International Journal of Community and Cooperative Studies 3(2):1-56.

|

|

|

|

|

Türkeköle T (2015). Strategic Approach to Financial Services Industry. Available at:

View

|

|

|

|

|

UBOS (2018). Uganda National Household Survey 2016/2017. Kampala, Uganda: UBOS. Available at:

View

|

|

|

|

|

Urassa KJ, Kwai DM (2015). The contribution of SACCOs to income Poverty Reduction. A Case Study of Mbozi District, Tanzania.

|

|

|

|

|

Wanyama FO, Develtere P, Pollet I (2008). Encountering the evidence: cooperatives and poverty reduction in Africa. Working Papers on Social and Co-operative Entrepreneurship WP-SCE, 08-02.

Crossref

|

|

|

|

|

Wichterich C (2017). Microcredits, Returns and Gender: Of Reliable Poor Women and Financial Inclusion in South Asia. In Work, Institutions and Sustainable Livelihood. Palgrave Macmillan, Singapore. pp. 275-301.

Crossref

|

|

|

|

|

World Bank. (2007). World Development Report. Agriculture fore Development. Washington, DC: World Bank.

|

|

|

|

|

World Bank (2009). Financial Access 2009: Measuring access to financial services around the world. Washington, DC: Consultative Group to Assist the Poor/world Bank.

|

|

|

|

|

World Bank (2013). World Bank Annual Report 2013. Washington, DC. World Bank.

Crossref

|

|

|

|

|

World Bank (2014). Global Financial Development Report 2014: Financial Inclusion. Washington, DC. @ World Bank. IGO

Crossref

|

|

|

|

|

World Bank (2015) Uganda Systematic Country Diagnostic: Boosting Growth and Accelerating Poverty Reduction. 4 December 2015

|

|

|

|

|

World Bank (2018a). Poverty and Equity Database. In: The World Bank Online Washington, DC.

|

|

|

|

|

World Bank (2018b). Understanding Poverty. Available at:

View

|

|

|

|

|

World Economic Forum (2015). The future of financial services: How disruptive innovations are shaping the way financial services are structured, provisioned and consumed, s.l.: World Economic Forums

|

|