Full Length Research Paper

ABSTRACT

This study was to identify challenges and contribution of informal financial services on rural households’ livelihood in selected Woredas of Gamo Gofa Zone. A multistage sampling technique was employed. Primary data on households’ motives, challenges and contribution of informal financial services were collected from household heads and focus group discussants. The collected data were analysed using descriptive statistics and inferential statistics. Users reported the transaction cost to access the service in informal financial services is low while others reported that the service is responsive for immediate problems. Users also reported that the service doesn’t need any criteria to be member while and some households are using informal financial service because of no more options available in the area. Others reported that the participation in the service has social benefit as it increases social networks, connectedness and the service doesn’t need collateral. Lack of legal support, lack of trainings, administration of members, small money size, undocumented money transfer are among challenges of informal financial services. Informal finance contributed as source of money for non-farm activities partially and fully. Legal support, training and linking informal and formal financial service institutions need future intervention.

Key words: Informal finance, challenges, contribution.

INTRODUCTION

Availability of key-assets (such as savings, land, labor, education and/or access to market or employment opportunities, access to common property natural resources and other public goods) is a an evident requisite in making rural households and individuals more or less capable of diversifying their livelihood (Ellis, 2000; Barrett et al., 2001). Sustainable livelihood framework adapted by Chambers and Conway (1991) identified five important assets for livelihood (physical, natural, social, human and financial assets).

Low income households in developing countries are seen as particularly vulnerable. Their personal problems of low education and skill levels, low incomes, lack of marketable assets, and uncertain job markets have been compounded by external factors that have failed to provide adequate infrastructure and social services that would have enabled them to participate in mainstream economic activities. As a result, this has affected every facet of their life: employment (predominantly in the informal sector), education (non-existent or up to primary levels only), health (low quality or traditional), housing (impermanent materials and illegal settlements) etc (Hari, 2016).

According to Ashenafi (2015), informal financial market is important for households who are far away from formal one. However, informal financial markets are rudimentary, poorly organized and limited to small close friendship or neighborhood.

Informal financial service involves diverse forms which is aimed at meeting different needs like; consumption smoothing, enterprise financing and promoting savings (Michael, 2015).

The economic situation of rural households in Ethiopia is highly constrained with financial capital shortage due to the nature of economic structure which is predominantly depending on rain fed and subsistence agriculture. For many rural households in most developing countries, it is difficult to access financial sources due to complicated challenges. For this, rural households use informal financial services as important source for financial access.

Mwangi and Kimani (2015) identified poor governance of the groups, low attendance of group meetings, defaulting by members, poor record keeping, poor group leadership, lack of clear structure to guide group operations, conflict among members, low income, burden of gender roles, capacity building of informal finance and mechanisms to enforce group registrations as challenges facing informal financial groups in Kenya.

Basic education of business operators, maladministration of the business, inadequate finance, lack of registration by the government, and the problem of high interest rate are among the problems/challenges identified by Adetiloye (2006).

Dejene (1993), in his study, pointed that equb (informal financial institution) has encountered some problems of default. A member may not be able to pay his dues as a result of business failure or for other reasons. In that case guarantors are obliged to cover the default.

In Ethiopia, informal financial services are used for diverse financial needs of rural households. Due its nature, the sector lacks important technical and institutional support from development organizations and the government.

The sector also faces various challenges which are affecting its possible contribution towards rural households’ livelihood. However, these challenges are not well studied and documented for possible interventions. Therefore, it is quite important to study contribution of informal financial services for rural household livelihood and challenges that the sector is facing.

RESEARCH METHODOLOGY

Description of the study area

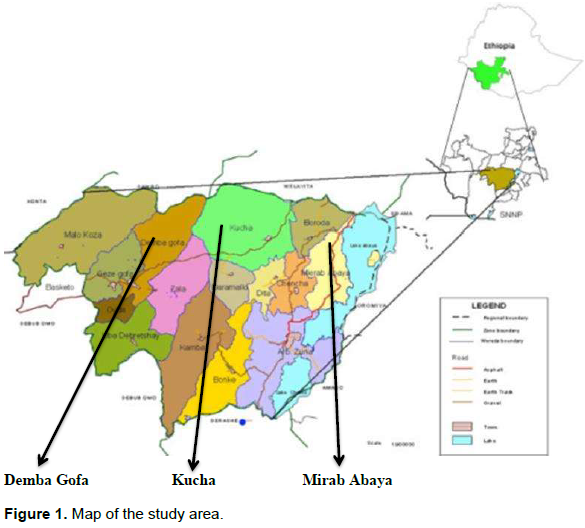

Gamo Gofa Zone is one of 14 Zones of the Southern Nations, Nationalities and People Regional State (SNNPRS) and consists of 15 rural districts and two town administrations namely, Arba Minch Zuria, Mirab-Abaya,Boreda, Chencha, Dita, Kucha, Daramlo, Bonke, Kemba, Zala, Ubadebretsehay, Oyida, Demba Gofa, Geze Gofa and Melakoza; and two reform towns called Arba Minch and Sawla. Gamo Gofa Zone lay center of the region around 5°57 –6°71 N latitude and 36°37–37°98 E longitude. Gamo Gofa general elevation ranges from 680 to 4207 m.a.s.l. and it receives 600 -1600 mm rainfall per annum and annual temperature ranges from 10 to 34°C (CSA, 2007). The Zone has a total population of 1,593,104, of whom 793,322 are men and 799,782 women; with an area of 18,010.99 square kilometers, Gamo Gofa has a population density of 144.68; while 157,446 or 9.88% are urban inhabitants, a further 480 or 0.03% are pastoralists. A total of 337,199 households were counted in this Zone, which results in an average of 4.72 persons to a household, and 324,919 housing units (Gamo Gofa Zone Agriculture and Natural Resource Department, 2016). (Figure 1)

Research design

Descriptive survey research design was followed as descriptive research is used to obtain information concerning the current status of the phenomena and to describe "what exists" with respect to variables or conditions in a situation.

Sampling techniques

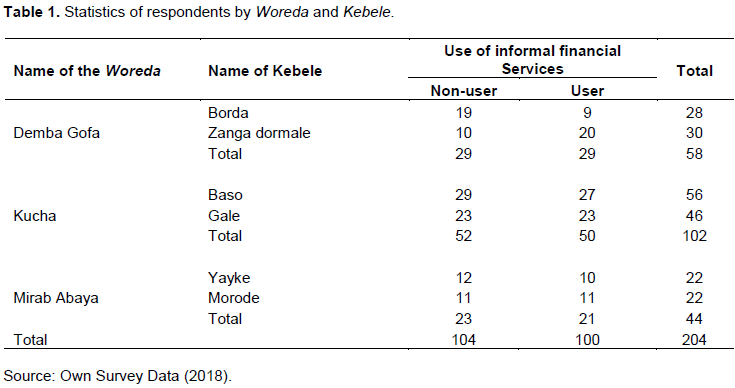

In this research, multistage sampling technique was followed. Gamogofa Zone was purposively selected for its convenience and resource limitations. Three Woredas were randomly selected through simple random sampling technique and two (2) Kebeles (lower administrative structure in Ethiopia) from each Woreda were randomly selected assuming that informal finance is practiced in all Woredas and Kebeles. Users of informal financial services were selected following snow ball sampling as there is no documented list of users of informal financial services in the study area. 100 users of informal financial services were sampled from three Woredas.

Data types and sources

Households background characteristics (age, sex, family size, number of economically active family members, educational level of household heads), land holding size (farm and irrigation land), contact with agricultural extension agents, membership in cooperatives, number of livestock ownership (number of oxen), family labour supply, distance to the urban center, presence of transfers, remittance, and pensions, history (failure) of previous loan, perception towards formal financial institutions, households reason for using informal financial sources, challenges of informal financial services, households utilization of money they get from informal financial sources and others will all be collected from respondent households.

Formal saving and credit services, cooperatives, presence of awareness creation, training by formal financial services, credit amount, criteria for formal lending, challenges of financial services, wealth grouping and status of the households collected from Kebele offices.

Methods of data collection

Data from respondent households were collected through interview schedule, key informant interview and Focus Group Discussion (FGD) while secondary data were collected through reviewing available files, reports, and website documents.

Methods of data analysis

Descriptive data were analysed using descriptive statistics such as; percentage, mean and frequency while comparison and association of different groups on different household characteristics was done by using t-test and chi-square with SPSS version 16.

RESULTS AND DISCUSSION

Household characteristics and use of informal financial services

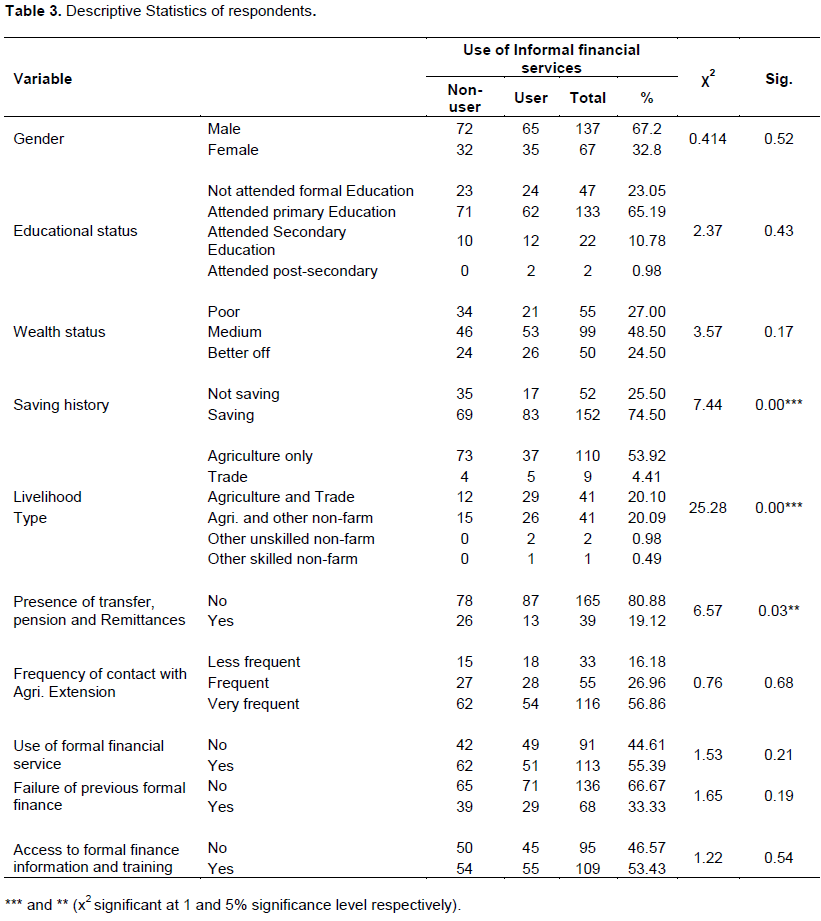

As depicted in Table 1 to 3, out of ten categorical variables of the study, 3 variables (saving history of the household, presence of other income sources and livelihood strategy of the household) have significant association with use of informal financial services at significance level of 1 and 5%.

Gender of household heads and use of informal financial services

Out of 204 sample respondents, 137 were male headed households whereas 65 were users of informal financial services implying that 65% of users of informal financial services were male headed households while 67 sample respondents were female headed households, and 35 respondents (35%) of respondents out of 100 users of informal financial services were female headed households. This indicates that in sampled areas, male headed households are participating more in informal financial services than female headed households which is against prior expectation of this research where male headed households were less expected to use informal financial services as formal financial services with more favoring men than women due to resource endowment for collateral and other social status which make them more trusted for loaning by financial institutions and finding group members for group lending. However, there is no significant association between gender and use of informal financial services.

Educational level of household heads and use of informal financial services

Though educational level of respondents is not significantly associated with use of informal financial services, 71 and 62 respondents from non-users and users of informal financial services respectively attended primary education while 10 and 12 respondents from non-users and users respectively attended secondary education. The results shows that 12% of users and 10% of non-users attended secondary education while 2% of users and 0% of non-users attended secondary education which is against prior expectation as education level expected to affect use of informal financial services negatively. This result is similar with Eshetu (2015) whose study on “determinants of credit constraints in Ethiopia” found that educated respondents use informal finance while their uneducated counterparts pick formal financial sources.

Wealth status of household and use of informal financial services

Wealth status of households is an important variable expected to affect households’ use of informal financial services. The highest number of respondents of both non-users and users 46 and 53 were medium while the least number of non-users were better-off households while the least number of user households were poor indicating even better-off households are using informal financial services in sampled areas, highlighting importance of the sector for livelihood of rural households in the area. Shocking result here is that out of 55 poor households, only 21 (38.2%) households use informal financial services while 34 (61.8%) did not use informal financial services. As it is difficult for poor households to access formal financial services, this obviously confirms that their financial need is still not addressed well by any financial service providers which would worsen their livelihood and poverty situation. This also opposes initial expectation as better-off households have better access to formal finance therefore were less expected to use informal financial services.

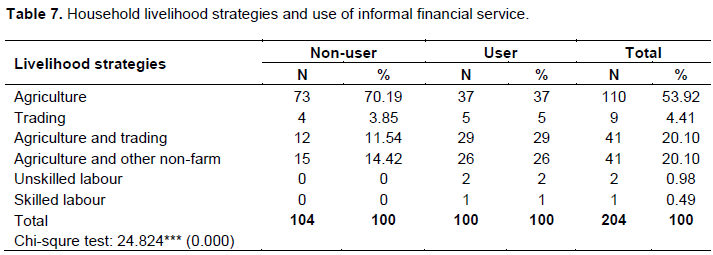

Livelihood strategies and use of informal financial services

Out of 100 respondents of informal financial service users, 63 (63%) of respondents depend on non-farm income activities (5% in trading, 29% in agriculture and trading, 26% in agriculture and other non-farm income, 2% in unskilled non-farm income activity and 1% in skilled non-farm income activity). 73 (70.2%) of non-users of informal financial services depend only on agriculture while only 37 (37%) of users of informal financial services depend on agriculture. This shows households using informal financial services have diversified income activities which is desirable with current vulnerable agricultural economy. Therefore, it can be concluded that informal finance encourages rural non-farm income diversification. χ2 test also shows that there is significant association between use of informal financial services and presence of transfer, pension and remittances at 1% significance level.

Presence of transfers, pensions and remittances and use of informal financial services

Prior expectation of the study was that presence of any possibly financial source may solve financial need of households and those households might not opt for informal financial services whereas those without any additional financial source opt for informal financial services. Out of 204 respondents, 165 respondents (80.9%) reported that they have no transfer, pension and remittance while 39 respondents (19.1%) reported they have additional financial sources from transfer, pension and remittance. In agreement with previous expectation, the study result shows that out of 39 respondent households with transfer, pension and remittances, 26 (66.7%) respondents’ were not using informal financial services whereas only 13 (33.3%) of respondents were using informal financial services. χ2 test also shows that there is significant association between use of informal financial services and presence of transfer, pension and remittances at 5% significance level.

Contact with agricultural extension agents and use of informal financial services

In rural areas of Ethiopia, agriculture extension plays a great role in multidimensional areas of livelihood. In this study also contact with agricultural extension agents expected to affect use of informal financial services negatively as those households with very frequent contact may have better access to many formal financial services while those with less frequent expected to depend on informal financial services to meet their financial need. The result shows that out of 204 respondents 33 (16.18%), 55 (26.9%) and 116 (56.86%) had less frequent, frequent and very frequent contact with agricultural extension agents respectively. Out of 33 respondents with less frequent contact majority 18 (54.5%) are users of informal financial services while only 15 (45.5%) are non-users of informal financial services showing households with less frequent contact opting informal financial services. Similarly, out of 116 respondents with very frequent contact, 62 (53.5%) were non-users of informal financial services while only 54 (46.5%) were users of informal financial services.

Use of formal financial services and use of informal financial services

Out of 204 respondents, 91 (44.6%) were non users of formal financial services while 113 (56.4%) of respondents were users of formal financial services. Out of 100 user respondents of the study, 49 (49%) and 51 (51%) were user and non-user of formal financial services. It can be concluded that some households use both formal and informal financial services. Though there is insignificant difference between the two groups, households not using formal financial services are more than those who use informal financial services and vice versa.

Failure of previous formal financial loan and use of informal financial services

It was assumed that households who loaned from formal financial institutions and failed to be successful in investing and repayment were likely to opt for informal financial services. Out of 204 respondents, 136 (66.6%) reported no failure of previous formal finance loan while 68 (33.4%) respondents reported failure of previous formal finance. The result indicates that out of 104 non-users of informal financial services, 65 (62.5%) and 39 (37.5%) did not report previous failure of formal financial services and reported failure of previous financial services, respectively. This shows majority of non-users of informal financial services did not report failure; therefore, it is possible to conclude that they depend on formal financial services, whereas 71 and 29% of users of informal financial services reported no failure and failure of previous formal financial service respectively.

Access to formal financial information and training and use of informal financial services

Access to formal financial service information and training was expected to affect use of informal financial services negatively. The survey result shows that 95 (46.57%) respondents reported they had lack of access to formal financial service information and training while 109 (53.43%) respondents had access to formal financial service information and training. Out of 100 users of informal financial services, 45 and 55% reported lack of access and presence of access to formal financial service information respectively. This indicates that use of informal financial service is not depending on access to formal financial information and training as 55% of informal financial services users had access to the information and training of formal financial services, but still using informal financial services which highlights the continued function and importance of the sector even for the future.

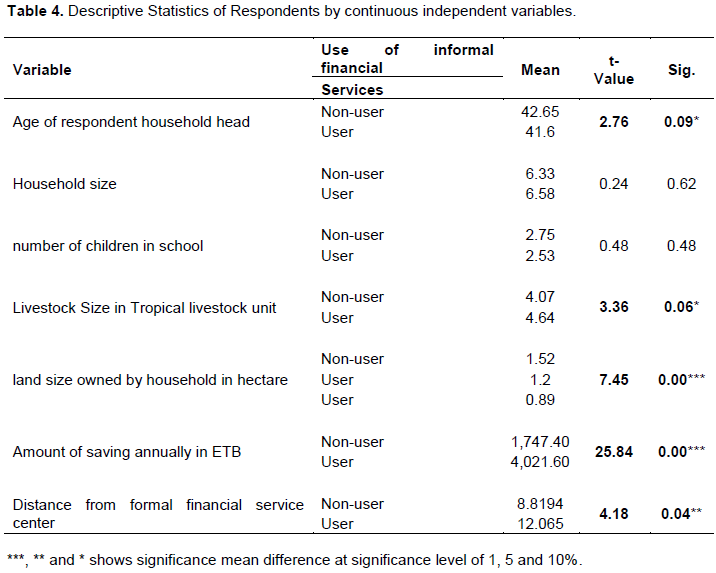

Descriptive statistics of respondents by continuous independent variables

As evident in Table 4, out of 8 continuous variables of the study, 5 variables have significance mean difference between users and non-users of informal financial services at significance levels of 1, 5 and 10%.

Age of respondents and use of informal financial services

The study results shows that mean age of non-users and users of informal financial services is 42.65 and 41.60 years, respectively. The t-test also shows that there is significant mean age difference between users and non-users of informal financial services at significance level of 10%. The result contradicts initial expectation as young respondents were expected to use more of formal financial services while old aged respondents expected to rely on informal one. This might be because informal financial service is more of being associated with non-farm income activities, particularly trading which is more of that practiced by young households as they have better motivation to use emerging opportunities in rural areas, and in most cases, have shortage of farming land which forces them to opt for other non-farm income activities.

Household size and use of informal financial services

Mean household size of non-users and users of informal

financial services is 6.33 and 6.58 respectively. Though it is statistically not significant, the result agrees with initial expectation of the study as large sized households are expected to use informal financial service to their financial needs.

Number of children in school and use of informal financial services

Though there is no significant mean difference of number children in school between the two groups, mean number of children is 2.75 and 2.53 for non-users and users of informal financial services respectively.

Livestock size of respondent households and use of informal financial services

T-test shows that at 5% significance level, there is significant mean difference of livestock size in tropical livestock unit (TLU) between non-users and users of informal financial services. Mean livestock size of non-user and user of informal financial services is 4.07 and 4.64 TLU, respectively, meaning livestock size of households positively affects use of informal financial services which opposes initial expectation, as livestock which is proxy to wealth status was expected to affect use of informal financial services negatively and wealthy households are expected to depend more on formal financial services.

Land ownership of respondent households and use of informal financial services

Land is an important and basic asset for rural livelihood and its proxy to wealth status of household was expected to affect use of informal financial services negatively. T-test result shows that there is significant mean land size difference between non-users and users. Mean land size of non-users and users of informal financial services is 1.52 and 1.20 ha, respectively. This result is similar with prior expectation.

Distance from formal financial institutions and use of informal financial services

Distance from formal financial service institutions was expected to affect use of informal financial services in that households living in distant areas are less likely to go to formal and opt for informal financial services to meet household financial need. The study result shows that at 5% significance level, there is significant mean difference of distance in kilometer between two groups. For non-users of informal financial services, mean distance is 8.81 km while it is 12.06 km for users of informal financial services. This result agrees with expectation of the study.

Contribution of informal financial services towards rural non-farm income activities

Financial capital is crucial for rural households’ livelihood improvement. In most rural areas, agriculture is becoming unable to support livelihood of many households due to various constraints like climate variability, land shortage, crop and livestock diseases, market fluctuation and failure are some among many. For these reasons, it is becoming very important to encourage rural livelihood diversification towards non-farm income activities. Non-farm activities require financial capital that is highly scarce in rural areas for this household’s quest for all possible options available around.

In this research also, informal financial services contribution towards rural non-farm activities is analyzed by using three components (type of rural non-farm business sector invested, share of informal financial services contribution for starting rural non-farm income activities and specific non-farm activity that rural informal financial services used.

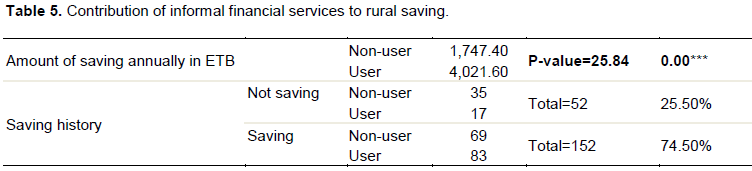

Rural saving and non-farm income activities

Saving rural income diversification is becoming very important than ever due to current challenges that agriculture is facing like climate change, land productivity problem, land shortage and landlessness, shortage of pasture land for livestock, diseases and pests of crops and livestock among others. Therefore, promoting rural non-farm sector income diversification is crucial for improving rural food security and livelihood. This can be possible only if household have access to financial sources to undertake non-farm income activities.

The result in the Table 5 shows that 52 (25.5%) of respondents were without saving history in any formal and informal financial sectors while 152 (74.5%) of respondents are with saving history in formal and informal financial services. Out of this 52 households without saving history, 35 (67.3%) are non-users of informal financial services while 83 households out of 152 households with saving history 83 (54.6%) are users of informal financial services highlighting that rural saving is highly associated with informal financial services and the sector plays important role in providing saving services. This can be generalized as informal financial services that contribute towards rural income diversification and non-farm sector development as saving encourages investment. χ2 test also shows that there is significant association between use of informal financial services and saving history of households at 1% significance level.

Independent T-test shows that there is significant saving amount difference between users and non-users of informal financial users. The result shows that mean annual saving amount of users of informal financial services is 4,021.60 ETB which is far more than mean annual saving amount of non-users of informal financial services that is 1,747.40 ETB. This indicates contribution of informal financial services towards rural saving which is a base for rural income diversification and investment. It can be assumed that informal financial services contribute towards financial capital of livelihoods of rural households.

Therefore, it is important to support and encourage informal financial services through various institutional and technical areas.

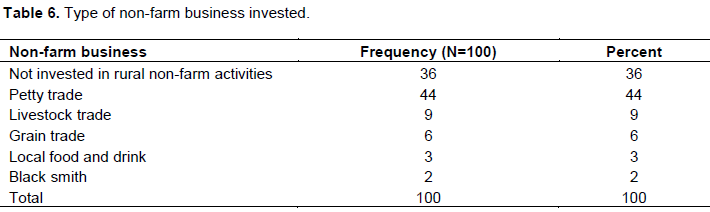

Investment of money from informal finance

Rural households use money from informal financial services for various purposes. This study intended to analyse contribution of this informal financial services towards non-farm income activities.

As shown in Table 6, about 64% of informal finance user households invested in non-farm activities while only 36% of respondents reported that they did not invest in non-farm income activities. This highlights importance of informal financial services for rural non-farm income activities.

Household livelihood strategy and use of informal financial services

Rural households participate in diverse livelihood strategies based on the livelihood capita that they have, such as entitlement and access. Rural household livelihood strategy choice is highly dependent on financial capital. The chi-square test also shows that there is significant association between use of formal financial services and use of informal financial services. In Table 7, it is revealed that household using informal financial services have more diversified livelihood strategies. 70.19% of non-users households of informal financial services depend on agriculture while only 37% of user households of informal financial services depend on agriculture. Rural trading is an important livelihood strategy that most rural households use in diversifying their livelihood. Only 15.39% of non-users households participate in trading while 34% of user household of informal financial services participate in trading. This highlights that contribution of informal financial services on rural household livelihood diversification and meeting financial need for diversification is significant.

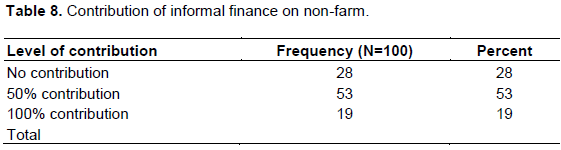

Contribution of informal finance for rural non-farm activity

Level of using money from informal finance still varies across the households because of variability in household assets. Financial capital is believed to be an important determinant for rural livelihood diversification. Access to this capital in rural areas is highly constrained due to geographical disadvantages and information asymmetry that formal financial institutions face. In this study, we tried to assess whether households use the money from informal financial services for rural livelihood diversification.

Table 8 shows that out of 100 users of informal finance, for 53 (53%) of respondents, level of contribution of informal finance in non-farm activities is 50% while informal finance helped 19% of the respondents to run non-farm activities by all money (100%) from informal finance. The same table also shows that 28 respondents reported that informal finance did not contribute towards non-formal activities in the study areas. In general, the sector contributed towards 72 users (72%) non-farm activities in the area. This indicates importance of informal finance for rural households in supporting their livelihood and meeting financial needs.

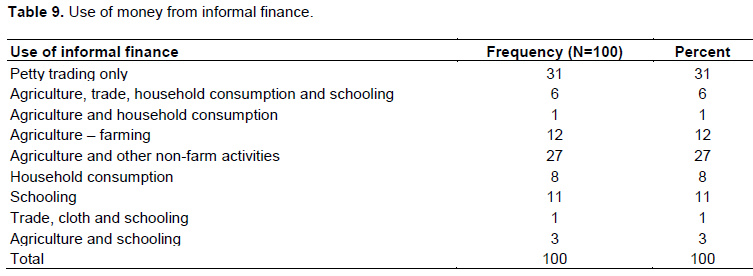

Use of money from informal financial services

Rural households use money that they get from informal financial services for various purposes. Main purposes that households use it for are mentioned in Table 9.

Data collected indicates that rural households use money from informal financial services for various purposes as financial capital is very scarce in most rural areas. Table 9 shows various areas that rural households allocate the money from informal financial services.

Focus group discussants raised money from informal financial services has been used for petty trade, for buying house in towns, house construction, motor bike for renting, generator for video rooms, barber, fertilizer and improved seed, small ruminant, and household consumption. This indicates contribution of the sector to non-farm income activities.

Table 9 shows the variety of purposes for which households utilize money that they get from informal financial sources. As can be seen from the table, out of 100 users of informal finance, 31(31%) used theirs for petty trade, 27 (27%) used theirs for agriculture and other non-farm sector, 12 (12%) used for agricultural activity (farm inputs), 11 (11%) users used for sending their children to school (cloths, stationery and other school fee) while other purposes that informal finance money used for shares (19%). In general, 92% of households use money from informal finance for productive activities which highlights contribution of informal finance for non-farm involvement and over all livelihood improvement of rural households in the area. 21% of respondents reported that they use money from informal finance for education purpose like for school fees, stationary, cloths and other school payments. This indicates the sector’s contribution towards proper utilization of money.

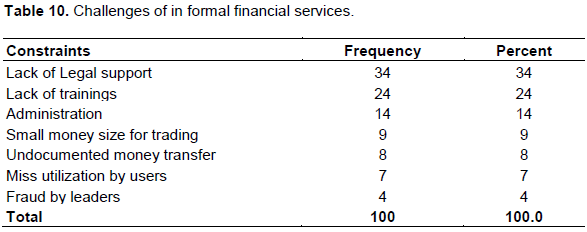

Challenges of informal financial services in the study areas

Informal financial services face many constraints which hinder effectiveness of the sector in contributing to rural households’ livelihood development.

Table 10 shows that lack of legal support by government offices, lack of trainings (management, small business development), administration of members, lack of documented money transfer, small loan/credit size for business/trading are among constraints of informal financial services in the area. This result is also similar with Adetiloye (2006), Dejene (1993) and Mwangi and Kimani (2015) as they identified poor governance of the groups, low attendance of group meetings, defaulting by members, poor record keeping, poor group leadership, lack of clear structure to guide group operations, members conflict, low income, burden of gender roles, capacity building of informal finance and mechanisms to enforce group registrations. Lack of registration by the government, the problem of high interest rate and inadequate finance are also among constraints.

CONCLUSION

Though informal financial service is considered as traditional and long history, the sector is still an important financial service provider for many rural households. Also, it is understood that during FGDs, the trend of using informal financial service in the study area is not declining even though there is expansion of formal financial service providers. At lower administrative level, the government offices have no organized information about the informal financial service providers. Informal finance is almost important for both female headed and male headed households.

Informal financial services are contributing for rural money saving, non-farm sector participation and livelihood diversification. Informal financial services had significant contribution towards non-farm activities, especially petty trading, livestock and grains trades. Use of informal financial services in the study areas is not limited to some wealth groups. All wealth groups are using the service in varying level. Remoteness of the rural areas is an important factor that determines the use of informal financial service as there is significant mean distance difference between users and non-users; therefore, it can be concluded that informal financial services are more important for remote rural areas than nearest areas to market and formal financial service centers.

Informal financial services in the area are used by all households in spite of various educational levels. The sector also contributes to education development in rural areas as it covers various financial needs for sending children to schools. Informal financial services had got less attention by government and other concerned bodies in terms of training, legal support, technical support, etc. Despite its strengths, the sector is facing challenges that all concerned should advance more. The study result shows that informal financial services are contributing towards non-farm income activities, household asset development, household consumption and other relevant aspects. It would be better if the service providers’ informal financial groups are registered and recognized at local government bodies for legal and technical supports that they seek.

Government bodies and others concerned should organize information on informal financial service providers for any support and follow up. Governmental and other organizations working around rural areas on livelihood improvement programs should consider trainings on record keeping, leadership, business development and resource management.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

ACKNOWLEDGEMENTS

The authors appreciate Arba Minch University for funding this study, and also all respondent households for their valuable contribution.

REFERENCES

|

Adetiloye K (2006). Problems and Prospects of the Informal Financial Market. Journal of Economics and financial Studies pp. 81-95. |

|

|

Agricultural Finance (2012). Enabling Environment: Access to Financial Services and Transportation chapter of the World Bank report on Agribusiness Indicators: Ethiopia. |

|

|

Ashenafi B (2015). Informal finance as alternative route to sme access to finance: evidence from Ethiopia. Journal of Governance and Regulation 4(1):94-102. |

|

|

Barrett CB, Reardon T, Webb P (2001). Nonfarm Income Diversification and Household Livelihood Strategies in Rural Africa: Department of Applied Economics and Management, Cornell University, Ithaca, NY 14853-7801, USA.31 p. |

|

|

Chambers R, Conway GR (1991). Sustainable Rural Livelihoods: Practical concepts for 21st Century. Institute of Development Studies Discussion Paper No. 296. 33 p. |

|

|

Dejene A (1993). The informal and semi-formal financial sectors in Ethiopia: a study of the equb, iddir and savings and credit co-operatives. |

|

|

Ellis F (2000). Rural Livelihood and Diversity in Developing Countries. Oxford University. |

|

|

Hari S (2016). Reasons why the Informal Credit Market is used by the Poor: Policy Implications for Microcredit Programmes in Developing Countries. Case study Series. |

|

|

Michael A (2015). The importance of Informal Finance in Promoting Decent Work Among Informal Operators: A Comparative Study of Uganda and India, Human Sciences Research Council, South Africa* International Labour Organization. Working Paper No. 66. |

|

|

Mwangi J, Kimani E (2015). Challenges Experienced by Men and Women in Informal Finance Groups in Gachagi Informal Settlement in Thika Sub-County, Kenya. International Journal of Innovative Research. |

|

|

Signe M, Mark M, David M (2005). Use of the Formal and Informal Financial Sectors: Does Gender Matter? Empirical Evidence from Rural Bangladesh. World Bank Policy Research Working Paper 3491. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0