Full Length Research Paper

ABSTRACT

INTRODUCTION

METHODOLOGY

RESULTS AND DISCUSSION

Sex distribution of sample

The study showed 14.2% of the creditworthy borrowers were male, which was lower than the corresponding figure (85.8%) for female. Moreover, only 85% of the female were defaulters while the corresponding figure for the male (15%) were non-defaulters. The study implies that being male/females were not related to loan repayment performance as expected, although the difference was not statistically significant. This result is in agreement with the findings of Retta (2000) and Fikirte (2011).

Distance of borrowers from the institutions

The survey result clearly showed about 69.16% of the sample respondents’ residence and businesses’ were near Harari MFI whereas 30.8% were not near to Harari MFI. As result, indicated distance of borrowers from the offices does not affect the repayment rate of borrowers. This implies that being far and/ near to the microfinance institutions was not related to loan repayment performance as expected, although the difference was not statistically significant. This result is in agreement with the findings of Abafita (2003) and Fikirte (2011); but was inconsistent with the findings of Assefa (2008).

Educational level of the borrowers

Result of the study clearly showed 92.4% of the sample respondents were literate with different educational level whereas 7.5% of the sampled borrowers were illiterate. The result from the data indicates that non-defaulters have better educational background than defaulters. The mean average school years of the total respondents were 5.00 while average class years of non-defaulters and defaulters were 3.98 and 1.97 respectively. However, there was no significant difference between non-defaulters and defaulters with respect to educational levels on loan repayment performance of the Harari microfinance institutions. This result is in agreement with the findings of Retta (2000) and Fikirte (2011).

Age of the borrower

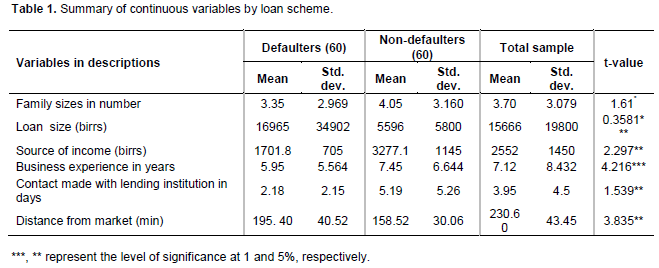

The mean age of defaulters and non-defaulters were 35.72 and 39.45 respectively. The result of t-test indicated that there is statistically significant difference (t-test= 94.867) between the mean age of defaulter and non-defaulters at 10% significance level. This result is in agreement with that of Abafita (2003).

Family size

The basic sampling unit for this analysis is the family household, which had an average family size of 3.4, less the national average of 4.7 persons (CSA, 2008). The mean average family size of defaulter and non-defaulter was found to be 3.35 and 2.969 respectively. Statistically there is a significant mean difference (t=2.772) at 10% probability level on their family size between defaulters and non-defaulters. This result agrees with the findings of Retta (2000) and Abafita (2003). However, it is inconsistent with the study made by Berhanu (2005) and Sileshi (2010).

Number of dependents in the household

The study showed 27.8 and 74.2% of the sample borrowers were dependent and non-dependent respectively. The household that have dependent’ family sizes are less percents than the non-dependent family sizes. Household dependents, which can determine the amount of the labor force in the household, are expected to bring about variation in decision behavior of households as to which repayment performances are increased (Semgalawe, 1998). The household size of the total sampled households ranges from 2 to 13 persons with mean and standard deviation of 6.3 and 4.2 persons respectively. Out of the total sampled households, 65.7% of them have a household size of above 6 people per household.

Number of economically active household members who live and work for the household also determines the labor available in the household which in turn determines the loan repayment performance of households. Households with more economic status may decide to use the loan which is effective and efficient in loan repayment performance. As the number of dependents increases, the borrower needs more money to fulfill their requirements in addition to the obligation of loan repayment. As a result he/she may divert the loan to meet the needs of those dependents families. This result is in agreement with the findings of Retta (2000). However, it is inconsistent with the study made by Abafita (2003).

Marital status of respondents

The study showed that 67.5% married household heads, while only 5.8% of them were unmarried/single. The rest of household heads were widowed and divorced, 8.3 and 18.3% respectively. Marital status of the households also determines household’s access to information and resource and hence on the use of loan received from office. This result was in agreement with the findings of Retta (2000) and Abafita (2003). However, it is inconsistent with the study made by Belay (1998) and Sileshi (2010).

Saving purpose of sample

The study showed that as regards saving purpose of the clients, about 42.5% of the respondent saved their money for future use, 43.3% of the respondents saved their money for the emergency, 2.5% of the respondents saved their money for consumption, 2.5% saved their money for repayments of the loan and 9.2% saved their money for personal. Regarding its relationship with loan, correlation test using Pearson chi-square, statistically there was a significant mean difference (t=3.052) at less than 5% probability level on their saving purpose of defaulters and non-defaulters. This result is in agreement with the findings of Retta (2000) and Abafita (2003). However, it was inconsistent with the study made by Belay (1998).

Savings habit of sample respondents

Results of the study showed that 80.8% of the beneficiaries reported that it had a positive effect (save), while 19.2% no effect (not save) reported that it had a discouraging effect on their loan repayment performance. Statistically there was a significant mean difference (t=19.417) at less than 1% probability level on their saving habit of defaulters and non-defaulters. This result is in agreement with the findings of Retta (2000), Abafita (2003) and Zeller (1996).

Lack of training and follow up

In order to effectively implement what the members of microfinance planned, training and follow up play a significant role. The informants, however, indicated that they were having two days training when they got the money, but after that nobody came to them to give any kind of support including training. There were also discussants (members) in a focus group discussion that indicated they were given training once. It was stated that ‘They- officials of microfinance institutions” gave us training once at the beginning, after that nobody appeared to see what we have done’. In support of this, another participant in a discussion said that, ‘At the beginning we were promised to get continuous training and support, but nothing was done’. Studies also showed that paying less attention to training was taken as one of the drawbacks of microfinance institutions. Jaffari et al. (2011) indicated that low attention given to client’s skill development as a weakness of microfinance institutions.

Lack of follow up was also among the reasons that became obstacle to the performance of members of microfinance institutions. The members in group discussion shared the same idea that at the beginning of their project, they started following them but immediately stopped it. The discussants argued that it was one of the limitations that led them not to be effective as expected. A woman who was member of MFI stated that, ‘There is nobody that followed us to see the improvements we made or the problems we faced’. In support of this, the other discussant also said that, ‘Let alone giving support, they did not ask us how we used the money’. A 35 year old woman who was a member explained the situation as, ‘Giving loan does not have any meaning unless they follow, encourage and support us when we need it. This situation makes us feel that the money is simply given as a gift’.

The lack of follow up of microfinance institutions were also manifested in a way that debts were not collected from members regularly and they did not have enforcing mechanisms of collecting the money lent. There were discussants who said that they were never requested to repay the debt so that they spent the money they prepared for other purposes. ‘My life has been changed for better. However, I am not happy because I wanted to repay my debt and take more but nobody requested me to repay’ as mentioned by a woman from a microfinance institution in the study area.

A participant in a focus group discussion also indicated that she did not pay because she felt that as there was no interest that it did not matter whether she paid it or not, but she was paying the saving money. Most informants mentioned that they were not requested to settle their debt, but nevertheless some members had already repaid their debts. This showed that the microfinance institutions in the study area did not have organized schedule to collect the debt from the clients. Moreover, from the information collected it could be concluded that continuous training was not given to clients so that they were constrained to effectively run their business.

Perceptions of borrowers on repayment period

The study showed 51(42.5%) of the sample respondents are of the opinion that the repayment period is not suitable. Of these borrowers, 69(57.5%) recommended a repayment period that is longer than a year while the rest recommended a repayment period that is less than a year, as suitable, which is a significant difference at less than 1% significance level  = 39.231). This result was in agreement with the findings of Berhanu (1999) and Abafita (2000).

= 39.231). This result was in agreement with the findings of Berhanu (1999) and Abafita (2000).

According to non-defaulters, they benefited by fully and timely paying their loans. Some of the benefits are: freedom from penalty, building of good relationship with the loan provider, access to the next higher loan and to make family stable. On the other hand, according to defaulters the reasons for not repaying their loans are; shortage of working capital and problem in workplace and improved use of loan, which is also another reason for default (Norell, 2001). Low supervision by the loan officers of the institution and personal problems of borrowers like illness were also stated in Norell (2001) as one of the reasons for default.

Business experience of borrowers

The study showed that the average business experience of non-defaulters was about 6.5 with maximum and minimum of 12 and 1 years respectively. On the other hand, the average business experience of defaulters was 2.5333 years with maximum and minimum years of 6 and 1 in that order. This study has identified about 11.3% of the respondents have less than 10 years of business experience, whereas around 3.3% of them had more than 40 years experience. Therefore, non-defaulters had more years of business experience than defaulters. This variable has significant impact at less than 1% significance level (t-test -4.216) between defaulters and non-defaulters. This result was in agreement with the findings of Berhanu (2005), Berhanu (2008) Berhanu and Fufa (2008).

Business information

The study showed that 69(57.5%) of borrowers had got information, whereas 51(42.5%) were not, which is a significant difference at less than 5% significance level  = 7.673). In fact, information is one of the most important parameters which help borrowers become aware of a microfinance enterprise. It plays a vital role in the success of business. Through this, borrowers can understand the advantages and disadvantages of the information on microfinance. It can initiate borrowers to try the new practice on their own business place. Borrowers can get information either formally or informally (such as from neighboring farmers, friends, relatives, elders, etc). This study agrees with Sileshi (2010).

= 7.673). In fact, information is one of the most important parameters which help borrowers become aware of a microfinance enterprise. It plays a vital role in the success of business. Through this, borrowers can understand the advantages and disadvantages of the information on microfinance. It can initiate borrowers to try the new practice on their own business place. Borrowers can get information either formally or informally (such as from neighboring farmers, friends, relatives, elders, etc). This study agrees with Sileshi (2010).

Business types

The result of the study showed that the sample respondents were engaged in various business activities. Out of the valid cases, 9.2, 6.7, 3.3, 33.3, 4.2 ,6.7, and 36.7% participate in service providers, shop and kiosk, tailoring, food processing, metal work, charcoal and groundnut trade, baltina and petty, respectively. From this, one can understand that the most important business activities on which borrowers of the area participated were food processing, petty trade and baltina, which is a significant difference at less than 5%significance level (t= 16.309). This result agrees with the findings of Fikirte (2011) and Abafita (2003). However, it is inconsistent with the study made by Belay (1998).

Other source of income

According to the survey results, about 46.7% of the total respondents had only one source of income which is from the business financed by the loan. Household’s source of income position and resource ownership was found to be important in loan repayment performance. The average source of income of the sample households was 2752.07 Ethiopian birr. The maximum annual source of income was 7000 Ethiopian birr while the minimum was 200. On average, non-defaulters had higher monthly source of income (about 3277.19 Ethiopian birr) as compared to defaulters who on average had only 1701.83 Ethiopian birr. Analysis of mean monthly source of income between defaulters and non defaulters had also indicated that there was significant mean difference (t =-3.581) at 1% significance level. Concerning this variable, most empirical study shows that the effect of additional income on household’s repayment decision is positive and significant. To mention some, for example, Norell (2001) and Fikirte (2011) reported positive influence of household’s income on loan repayment performance. This result does agree with the findings of Jama and Kulundu (1992).

Business status of borrowers

According to the survey, results showed that about 33.3% of defaulters business was successful but due to many reasons they were not willing to pay their loans on time. In contrast, 33.3% of non-defaulters’ business were not successful; however, they were paying their loans from other income sources (Table 1). There was significant difference ( =12.958**) at 5% probability level on business status of borrowers. This result agrees with the findings of Retta (2000) and Amare (2005).

=12.958**) at 5% probability level on business status of borrowers. This result agrees with the findings of Retta (2000) and Amare (2005).

Qualitative data were collected through Focus Group Discussions (FGDs) and informal discussions with households, loan officers and key informants during transect walk within sample Kebele Association.

Econometrics result

Here, econometric analysis was carried out in order to identify factors that affect the loan repayment performance of Harari microfinance institutions. As previously explained, binary logit models were employed to estimate the effects of hypothesized explanatory variables on the loan repayment performance of beneficiaries in the Harari microfinance institutions.

Analysis of factors influencing loan repayment performance

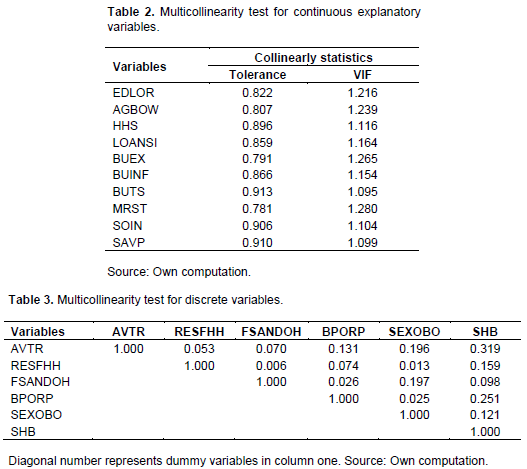

As discussed previously, the binary logit econometric model was selected for analyzing the factors influencing the loan repayment performance of the borrowers. Prior to running the logistic regression analysis, both the continuous and discrete explanatory variables were checked for the existence of multicollinearity and high degree of association using variance inflation factor (VIF) and contingency coefficients, respectively. The VIF values for continuous variables were found to be very small (much less than 10) indicating absence of multicollinearity between them (Table 2). Likewise, the results of the computation of contingency coefficients reveal that there was no serious problem of association among discrete variables (Table 3). For this reason, all of the explanatory variables were included in the final analysis. More specifically, nine (9) continuous and six discrete explanatory variables were used to estimate the binary logit model.

Contingency coefficient values ranges between 0 and 1, and as a result chi-square variable with contingency coefficient below 0.75 shows weak association and the value above it indicates strong association of variables. The contingency coefficient for the dummy variables included in the model was less than 0.75; thus did not suggest multicollinearity to be a series concern depicted in Table 3. The results of VIF and contingency coefficient computed from the survey data are presented in Tables 2 and 3 respectively.

Logit model

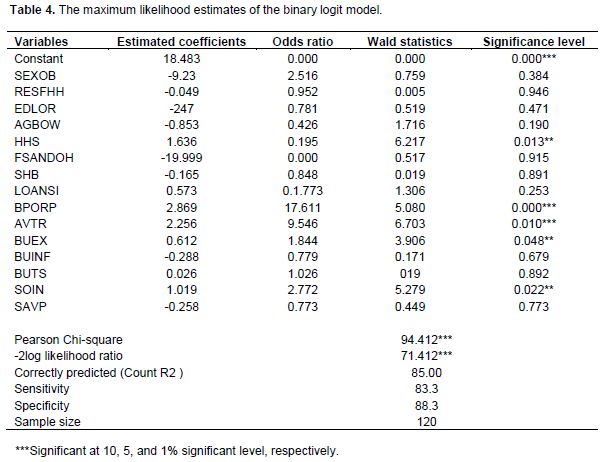

Logistic regression model was used to satisfy second objective of the study’ to assess the factors that affect the loan repayment performance’ in the study area’. Based on the result of multicollinearity diagnostics’ tests for both continuous and dummy explanatory variables, no variable was found to be highly correlated or associated with one of other variables. The likelihood ratio test statistic exceeds the Chi-square critical value with 12 degrees of freedom. The result is significant at less than 0.01 probabilities indicating that the hypothesis that all the coefficients except the intercept are equal to zero is not tenable. Likewise, the log likelihood value was significant at 1% level of significance.

Another measure of goodness of fit used in logistic regression analysis is the Count R2, which indicates the number of sample observations correctly predicted by the model. The Count R2 is based on the principle that if the estimated probability of the event is less than 0.5, the event will not occur and if it is greater than 0.5 the event will occur (Maddala, 1983, cited as Sileshi, 2011). In other words, the ith observation is grouped as a non-defaulter if the computed probability is greater than or equal to 0.5, and as a defaulter otherwise. The model results show that the logistic regression model correctly predicted 71.5 of 120, or 84.8% of the sample borrowers. The sensitivity (correctly predicted non-defaulters) and the specificity (correctly predicted defaulters) of the logit model are 83.3 and 88.3%, respectively. Thus the model predicts groups, defaulters and non-defaulters fairly accurately.

Out of the fifteen variables hypothesized to affect the loan repayment performance of borrowers, five were found to be statistically significant. The maximum likelihood estimates of the logistic regression model shows that family size (HHS), Borrowers perception on repayment period (BPORP), Availability of training (AVTR), Business experience (BUEX) and Source of income (SOIN) were factors affecting the loan repayment performance of borrowers in the study area. More specifically, the coefficients of borrowers perception, availability of training, source of incomes are statistically significant at less than or equal to 1% significance level. The variables, family sizes, business experience were statistically significant at 5% level of significance. On the other hand, the coefficients of ten explanatory variables, namely, sex of borrowers (SEXOBO), distance of household (RESFHH)), age of borrowers (AGBOW), dependent family sizes (FSANDOH), loan sizes (LOANSI), Business information (BUINF), Business types (BUTS) and Marital status (MRST) of borrowers were less powerful in explaining loan repayment performance of the sample borrowers. Regarding the signs of the coefficients of non-significant variables, all but business information have the expected signs. In what follows, the results of the model estimates are interpreted in relation to each of the statistically significant variables.

In total, fifteen independent variables were used for estimation. To analyze factors influencing the loan repayment performance of the borrowers, binary logit model was estimated using a statistical package known as SPSS version 16.0 (Table 4).

Family sizes (HHS)

The coefficients of this variable were hypothesized to influence loan repayment performance negatively. The result of this model estimates was contrary to prior expectation that the family sizes have a significant and positive impact on loan repayment performance. The variable was significant at 1% probability level, possibly due to one of their family members being engaged in source of other income activities, which might help them earn additional income. Besides, engaging in diversified ‘economic activities might reduce family dependency ratio, which is defined to be the ratio of economically dependent members to economically active members. Other things being constant, the odds ratio in favor of non-defaulting increases by a factor of 0.195 for those borrowers who has active age family. This result of the study is completely in agreement with the study conducted by Abafita (2005), Berhanu (2005) and Sileshi (2010).

Borrower’s perception on repayment period (BPORP)

The coefficient of this variable is hypothesized to influence loan repayment performance either positively or negatively. If repayment period is suitable, the client should perform better. The model results show that contrary to the a priori expectation, this variable has a significant positive impact on loan repayment performance. The variables are significant at less than 1% probability level. This might be due to the fact that those borrowers have positive perception for repayment period tend to develop repayment and become friendly with the lender, which results in reluctance to fulfill their loan repayment obligation. Hence, they do not bother about the consequences arising from the dalliance in loan repayment. On the other hand, those have not positive perception towards repayment period, the more dalliance for repayment of loan and become defaulters. Other factors being kept constant, the odds ratio favoring loan repayment performance increase by a factor of 17.611 for borrowers who had positive perception on repayment period. This result does agreement with the findings of Retta (2000) and Abafita (2003). However, it is inconsistent with the study made by Belay (1998).

Availability of training (AVTR)

The coefficient of this variable is hypothesized to influence loan repayment performance positively. It is one of the important requirements for the success of microfinance institution (Assefa et al., 2005).

If the lender provides various training, the clients will able to understand the rule and regulation easily. They also develop skill on how to do business and money utilization. Training is needed not only for clients but also for loan officers. In both cases, it has a positive contribution to the repayment rate. Norell (2001) also agree on the importance of training due to decreasing default rate. The model results show that to the a priori expectation, this variable has a significant positive impact on loan repayment performance. This might be due to the fact that those borrowers take trainings that have hints on the activities that should be performed and become friendly with the lender, which results in reluctance to fulfill their loan repayment obligation. Moreover, borrowers who do not take trainings were not successful. Hence, they do not bother about the consequences arising from the dalliance in loan repayment. Other things being kept constant, the odds ratio favoring loan repayment performance increase by a factor of 9.546 for borrowers who were trained. This result does agree with the findings of Assefa et al. (2005) and Norell (2001). However, it is inconsistent with the study made by Fikirte (2011).

Business experience (BUEX)

The coefficient of this variable was hypothesized to influence loan repayment performance positively. The result of this model has positively influenced loan repayment performance as sign of consistency with the priori expectation. Positive relation shows that longer experience in business, better knowledge, attitude and skill is developed on the operation and conduct of using microfinance enterprise as source of poverty reduction and methods of production. Additionally, micro entrepreneurs who have been in business longer are expected to have more stable sales and cash flows than those who have just started. Thus, those who have run their businesses longer may have higher debt capacity. The variable is significant at 5% levels. The odds ratio in favor of practicing business increases the non-defaulters by a factor of 1.844 for an increase in business experience by one year. This result completely agrees with the studies conducted by Berhanu and Fufa (2008) and Zeller (1998).

Source of income (SOIN)

The coefficient of this variable was hypothesized to influence loan repayment performance either positively. This is consistent with the priori expectation. The result of the logit model reveals that this Variable affects loan repayment performance positively at less than 1% level of significance. The possible explanation is that borrowers may use such cash flows from non-business activities and sources-such as income from other members-to make loan repayments. Thus borrowers with higher household incomes may have a higher chance of repaying their loans. The odds ratio favoring loan repayment performance increase by a factor of 2.772 for borrowers who had other sources of income. This result was in complete agreement with the studies conducted by Berhanu (2005) and Abraham (2002).

CONCLUSION

CONFLICT OF INTEREST

REFERENCES

| Abafita J (2003). Microfinance and Loan Repayment Performance: A Case Study of the Oromia Credit and Savings Share company (OCSSCO) in Kuyu', M.Sc thesis, Addis Ababa University, Addis Ababa. | ||||

| Abraham G (2002). Loan Repayment and it is Determinants in Small –Scale Enterprises financing in Ethiopia: Case of private borrowers Around Zeway Area', MSc, Thesis, AAU. | ||||

| Alemayew Y (2008). Research Paper Submitted To Addis Ababa University in Partial Fulfillment of the Requirement for the Degree in M.Sc. Program In Accounting And Finance. | ||||

| Amare B (2005). Determinants of Formal source of credit loan repayment performance of small holder farmers: the case of north western Ethiopia, North Gonder', MSc. Thesis, Alemaya University, Ethiopia. | ||||

| Assefa BA (2002). Factors influencing loan repayment of rural women in Eastern Ethiopia: the case of Dire Dawa Area', A Thesis presented to the school of graduate studies, Alemaya University, Ethiopia. | ||||

| Asian Development Bank (ADB) (2002). 'Finance for the poor: Microfinance development Strategy', Rural Asia study: beyond the Green revolution. Manila. | ||||

| Basu A, Blavy R, Yulek M (2004). 'The role of Donors and NGOs: Microfinance in Africa Experience and lessons from Selected African Countries. IMF Working Paper. | ||||

| Beckman TN, Foster RS (1969). Credits and Collections: Management and Theory, 8th Edition. McGraw-Hill Book Company, New York, U.S.A. | ||||

| Belay A (2002). Factors influencing loan repayment of rural women in Eastern Ethiopia: The Case of Dire Dawa area. M.Sc. Thesis, Alemaya University, Ethiopia. P 19. | ||||

| Belay K (1998). Structural Problem of Peasant Agriculture in Ethiopia. Research Report, Alemaya University of Agriculture. Ethiopia. | ||||

|

Berhanu A, Fufa B (2008). Repayment rate of loans from semi-formal financial institutions among small-scale farmers in Ethiopia: Two-limit Tobit analysis. J. Soc. Econ. 37:2221-2230. Crossref |

||||

| Bekele H (2001). Factors influencing the loan repayment performance of Smallholders in Ethiopia.M.Sc.Thesis, Haramaya University. | ||||

| Drake DR (2002). The Commercialization of Microfinance: Balancing Business and Development', Bloom field, CT: Kumarian Press. | ||||

| Fikirte K (2011). Determinant of loan repayment Performance' A case Study in Addis Ababa Credit and Saving Institution. Wegeningen University: Netherlands. | ||||

| Kashulaliza A (1993). Loan Repayment and it is determinants in Smallholder agriculture: A Case study in the Southern highlands of Tanzania'. East Afr. Econ. Rev. 9:1. | ||||

|

Maddala GS (1983). Limited-dependent and qualitative variables in econometrics: Cambridge University Press. Crossref |

||||

| Mengistu Bediye, 1997. Determinants of Micro-enterprise Loan Repayment and Efficiency of Screening Mechanism in Urban Ethiopia: The case of Bahir Dar and Awassa Towns, Addis Ababa, p. 20 | ||||

| National Bank of Ethiopia (2008). Monitory Development in Ethiopia', National Bank of Ethiopia Quarterly Bulletin, First Quarter 2008/09. | ||||

| National Bank of Ethiopia (NBE) (2010). Directive No.MFI/01/96 (Minimum Paid-up capital) and directive No.MFI/16/2002 (Minimum Capital Ratio Requirement), Draft background paper, Addis Ababa, Ethiopia. | ||||

| Norell D (2001) 'How To Reduce Arrears In Microï¬nance Institutions. J. Microfinan. 3(1):115-130. | ||||

| Ramesh R (2013). Financial Access for Everyone: A Review. Paper presented at the national conference on Loan and Savings: The Role in Ethiopian Socioeconomic Development' organized by Haramaya University, 15-16 February 2013. | ||||

| Retta G (2000). Women and Microfinance: The Case of Women Fuel Wood Carries in Addis Ababa'. M.Sc. Thesis, AAU. | ||||

| Semgalawe (1998). Group credit: A Means to Improve Information Transfer and Loan Repayment Performance. J. Develop. Stud. 32(2):263-281. | ||||

| Sandgrove K (2005). The complete guide to business risk management'. Gower publishing, Ltd. England. | ||||

| Sengupta R, Aubuchon CP (2008). The Microfinance Revolution: An Overview. Federal Reserve Bank of St. Louis Review, January/February 2008, 90(1), pp. 9-30. Available at: https://research.stlouisfed.org/publications/review/08/01/Sengupta.pdf | ||||

| Sileshi M (2010). 'Factors Affecting Loan Repayment Performance: The Case of small holder farmers in Hararghe, Ethiopia. M.Sc. Thesis, University of Nairobi, Kenya. | ||||

| Stiglitz JE, Weiss A (1999). Credit rationing in Markets with Imperfect Information'. Am. Econ. Rev. 71(3):393-410 | ||||

| Tesfaye GB (2009). Econometric Analysis of Microfinance Credit group formation, contractual risks and welfare in Northern Ethiopia', PhD thesis, Wageningen University. Wageningen, the Netherland. P. 21. | ||||

| Zinman (2006). Observing Unobservable: Identifying Information Asymmetries with a Consumer's Credit Field Experiment. Yale University and Dartmouth College. P. 21. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0