Full Length Research Paper

ABSTRACT

The investigation considered farmers’ readiness to take part in crop insurance in the Dormaa municipality of the Bono Region, Ghana. Essential information from 167 respondents who were chosen through a multi-stage sampling method for the study was collected through a structured questionnaire. Elements influencing readiness to participate in crop protection by cocoa farmers was evaluated using probit regression model and lastly constraints of cocoa farmers were assessed utilizing Kendall’s coefficient of concordance. The study found that the average amount farmers were eager to pay was GH₵215.59 per year for crop insurance. Majority 96.7% of the respondents were eager to participate in crop insurance but 3.3% of the respondents were not willing to take part. The important factors influencing readiness to join crop insurance by the farmers were age, marital status, access to extension service and experience in cocoa farming. Again, the foremost constraint affecting the farmers was pests and diseases. The study therefore recommends that agricultural extension agents and other agricultural insurance stakeholders should sensitize crop farmers on the significance of crop insurance policy. Insurance companies ought to give crop insurance to farmers at moderate rates of GH¢ 215.59 per year to encourage their participation.

Key words: Crop insurance, cocoa, probit regression, Dormaa Municipal assembly, Ghana.

INTRODUCTION

Agriculture is critical to the economy of each emerging nation including Ghana since it utilizes around 66% of the labour force in Ghana; both formal and casual. The agriculture subsector grew by 4.8% in 2018 contrasted with a development pace of 6.1% in 2017. Agriculture’s portion of gross domestic product dropped from 21.1% in 2017 to 19.7% in 2018. Crops are another major engagement in Ghana with a portion of 14.5% of gross domestic product (Ghana Statistical Service, 2019). Despite the fact that the contribution of farming to Ghana's Gross domestic product has dropped over the years, it continues to be a powerful force in the economy (ISSER, 2011). A fundamental profitable area and a significant source of export income for Ghana over the past years have been cocoa. Briesinger et al. (2011) showed the portion of cocoa in agrarian gross domestic product surge from 13.7% in 2000 to 2004 to 18.9% in 2005/2006. The momentous role of cocoa to Ghana's income in addition to the reality it helps as a key wellspring of work for many Ghanaian farmers implies its future against any unexpected conditions should be secured. This is on the grounds that any significant disaster in this sector will negatively affect both the macroeconomic and the microeconomic areas of the economy. Despite the fact that danger in the agricultural sector is inevitable, it can be managed.

Cocoa production differ markedly on yearly basis because of unpredicted climate conditions, pests and disease invasions and sporadic economic situations triggering harvests and prices to sway widely. Cocoa production ought to be given more consideration to enlarge Ghana's income and in addition to assist with settling the food security challenges in parts of the nation.

As per Oluyole and Sanusi (2009) prior investigations recognized some significant explanations behind differences in cocoa output which include low harvest, impulses of environment, extreme climate situations, infection occurrence, pest invasion, and regular dangers like heavy downpour, erosion and long dry seasons. High risks and uncertainties related with agricultural production has been ascribed to the decline in production of cocoa (Aderinola and Abdulkadri, 2007). This is due to the fact that similar to other crops, cocoa needs extensive uninterrupted and incessant interaction with the forces of nature. These threats and vulnerabilities are unpredicted and they are outside the capability of the farming households, subsequently, the farmers can just cope with them. Cocoa farmers incur huge losses on savings and income due to the losses suffered from these hazards and uncertainties. In the light of this, Ajakaiye and Adeyeye (2001) discovered that smallholder-farming households in many emerging nations of the world with no exception to Ghana are ensnared in the rancorous pattern of insufficiency. This succession is portrayed by low output and low returns from the farm, occasioning in practically no sparing funds, necessary for the revolution of their farming expedition, accordingly adding to the low position conferred on farmers within the populace. Conversely, Quagrainie (2006) prescribed that insurance could be utilized to abate financial expenses of numerous hostile events, for example, deaths, accidents, burglary and weather damages. Insurance is defined as an agreement between two parties where one party called the insurer agrees to an exchange called premium to pay the other party a fixed measure of money in the event of sudden incident (Adams 1995). As indicated by Sarris (2002), insurance warrants a base cost for an explicit amount over a determined duration for which the safety net provider pays a forthright premium. Nevertheless, insurance affords the prospect for societies to substitute risk with known rate. Individuals procure insurance coverage hoping to receive a sum, anytime the policyholder encounters protection secured misfortune (Nimo et al., 2011). As indicated by Aidoo et al. (2014), a large portion of the insurance agencies in Ghana offer numerous protection plans (for example accident coverage, life and medical coverage, fire protection and burglary) apart from crop insurance scheme.

As indicated by Ray (2001), crop insurance can provide a cushion for yield damages in an awful time and assist guarantee a significant level of protection in farm returns in the long term. Agricultural protection considers how vulnerabilities can be dealt with efficiently to the benefit of the farming households presently and later on. This can assist to safeguard agriculture and the bigger economy. Agricultural insurance is thus an indispensable aspect of the institutional arrangement crucial for the growth of food production; generally a high-hazard endeavour. One of Ghana’s main national export produce is cocoa (Anang, 2011). At the national level, cocoa’s contribution to trade balance is in excess of over 20% of the total annual export revenue. The cocoa sector in Ghana has been pronounced as an African success story for the reason that over the years, the country has continued its status as one of the worlds’ foremost suppliers of the crop (Williams et al., 2015).

From 1911 to 1960, Ghana led in the supply of cocoa beans, exporting about 40% of the total world output. Ghana went through two significant cataclysmic events over the past three decades affecting agricultural activities (Nimoh et. al., 2011). These debacles were prolong dry season and flooding. These hostile situations prompted inescapable decimation of farmland and deaths in the pretentious zones (Agyemang, 2010). In 1983, there occurred a mass decimation of cocoa seedlings in the nation as a result of the cocoa swollen shoot infections and shrubbery fire (Nimoh et. al., 2011). Cocoa farmers lost almost all their funds. In situations like this crop insurance is the only option to mitigate such problems that may arise from natural causes. Lately, interest has increased in introducing weather-based crop insurance contracts to farmers as a means to help them break out of their vicious cycle of poverty (Barrett et al., 2008).

Insurance decreases the effect of yield destruction and damages; offer farmers earnings and production cushioning (ILO, 2011). Advantages of this nature give impetus to crop insurance as an avenue that diminishes the effect of output risk. Insurance assists farmers to stabilize their income and savings and prevent devastating effects of losses due to natural vulnerabilities or low market prices. Notwithstanding, if farmers are eager to partake in insurance and the amount they are ready to pay just as the determinants of their readiness to pay for a minimum price of insurance remain an open inquiry. According to Okoffo et al. (2016), there is diminutive evidence on cocoa farmers' eagerness to protect their produce, premium prepared to pay and the readiness of protection agencies to deliver crop protection scheme to farming households. This has been a challenge affecting the introduction of insurance schemes to cocoa farmers in cocoa farming communities. This situation is not different from what persist in the Dormaa Municipality. Therefore, the question as to whether farmers are prepared to partake in crop insurance in the Dormaa municipality still remains a mystery and the study intends to investigate this gap.

METHODOLOGY

Description of the study area

The investigation was carried out in the Dormaa municipality. The Dormaa Municipal is situated at the Western part of the Bono Region. It exists on longitudes 3o West and 3o 30’ West and latitudes 7o North and 7o 30’ North. Jaman and Berekum Districts bound the district on the north, on the east by the Sunyani Municipal, in the South and southeast by Asunafo and Asutifi Districts respectively, in the southwest by Western Region and in the West and northwest by la Cote d’Ivoire. The Municipal Capital is Dormaa Ahenkro, situated about 80 km west of the regional capital, Sunyani (GSS, 2012), Figure 1.

Population, sample size and sampling technique

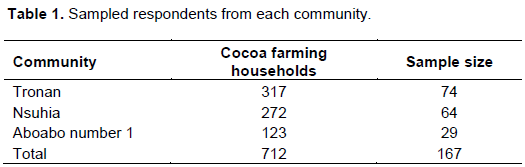

The population for the study was 920 cocoa farming households. Multi-stage sampling method was utilised for the selection of 167 respondents for the investigation. To begin with, purposive sampling was utilised to choose Dormaa Municipality in the Bono region of Ghana for its high emergence of cocoa farmers. Second, purposive sampling was utilised to choose three different communities that is Aboabo number 1, Tronan, and Nsuhia in the district because of their intensive cocoa production.

Thirdly, systematic random sampling procedure was utilised for the choice of the cocoa farming households from the three different communities in the district to form the sample size. The systematic random sampling was accomplished by picking each subsequent cocoa cultivating family unit in a community, beginning with the first randomly interviewed cocoa cultivating family unit. The number of cocoa family units questioned from the three communities picked for the present study is presented in Table 1. The number of respondents for this investigation was computed which dependent on the accompanying equation is given by Yamane (1967):

Where n = sample size, N = population size and e = level of precision.

Method of data collection

Primary data and auxiliary information were sourced for the current study. Auxiliary information was gotten from several sources including journals articles, Ghana Statistical Services, Ministry of Food and Agriculture, relevant books and online sources. Primary data was zeroed in on respondents’ personal and household attributes, factors influencing readiness to partake in insurance and constraints affecting cocoa production. The data was obtained from the 167 randomly selected respondents using structured questionnaires.

Data analysis

The data collected were analyzed utilizing the probit regression model and Kendall’s coefficient of concordance. Graphic statistics such as, tabular description and summary statistics like percentages and frequencies were also used to summarize the data. In this study, the probit regression model was utilized to measure the elements that control the readiness of farming households to partake in crop insurance due to the contrast feature of the contingent characteristic. The significance for using of the probit model over the logit model is because of its capacity to restrict the utility value of the choice to join variable to exist in 0 and 1, in addition to its capability to determine the issue of heteroscedasticity (Asante et al., 2011). Disposition to partake in crop insurance (Y) was represented as a dummy characteristic with the value of 1 given to a farming household who is eager to partake in crop insurance and 0 for otherwise. The probit model is a likelihood model with binary classes in the dependent characteristic (Liao, 1984). The probit analysis provides statistically significant findings of which socio economic elements influence farmer’s readiness to partake in crop insurance and measure whether it increase or decrease the likelihood of participating in crop insurance.

The probit model postulates existence of an underlying latent variable  for which dichotomous realization is observed (Gujarati and Madsen, 1998). The model is expressed as:

for which dichotomous realization is observed (Gujarati and Madsen, 1998). The model is expressed as:

Where Z represents a vector of explanatory variables (socio-economic factors), f indicates α standard normal cumulative distribution function, α signifies a vector of unknown parameters, j designates jth socio-economic factor, µ denotes the error term and i represents the ith farmer.

In the equation, y* denotes the unobserved variable termed as a latent variable. The decision or intention to partake in crop insurance is measured by the latent variable. The observed dichotomous variable is represented as:

Since is unobserved, it is believed to relate to the observed characteristics of the individual farmer, which provides the empirical mode given by the relation:

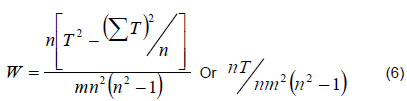

Constraints affecting cocoa farming households in the study area were evaluated using Kendall’s coefficient of concordance. It is a nonparametric statistical approach proposed by Maurice G. Kendall and Bernard Babington Smith, used to estimate the strength as well as bearing of association that exist between two variables and ranks the variables from the outmost important to the least important using an ordinal scale, and then estimates the level (Kendall, 1962).

Empirical specification of Kendall`s coefficient of concordance is given as follows:

Where T denotes the sum of ranks for the factors ranked; m = number of respondents; and n = number of factors ranked.

The index W estimates the proportion observed variance of the sum of ranks and the maximum possible variance of the sum of ranks.

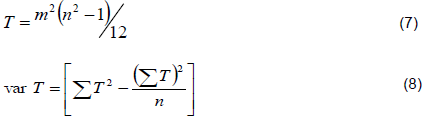

The maximum variance (T) is specified as:

Coefficient of Concordance (W), which estimates the level of concordance, is calculated using the aggregate rank score. The limits of W are specified as  It is 1.00 and 0.00 if there is maximum agreement and maximum disagreement among the respondents respective.

It is 1.00 and 0.00 if there is maximum agreement and maximum disagreement among the respondents respective.

RESULTS AND DISCUSSION

Socio-economic characteristics of the respondents

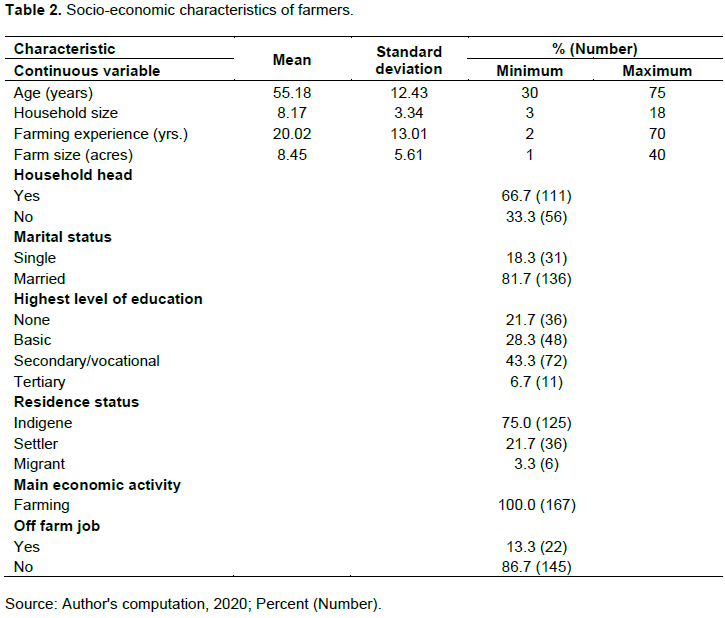

Features that assist to develop the effectiveness of farmers to embrace practices that can increase their production are their socio-economic features. These features assist to modify the entrepreneurial capabilities of farmers in decision-making, particularly those involving farming venture systems (Haruna et al., 2010). In view of this, the pertinent socio-economic characteristics of the farmers were explored to establish their importance to the capacity of the farming households to accept crop protection.

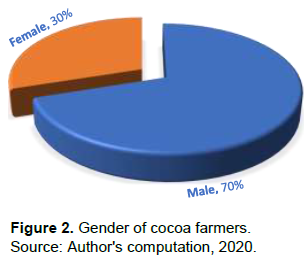

Majority (70.0%) out of the 167 respondents were males while just 30.0% were females as shown in Figure 2. This is in accordance with the results of Aneani et al. (2012) who also established 80% of sampled farmers were males and 20% being females in the Ghanaian cocoa sector in their study. This might be because cocoa production is an energy intensive activity and males are fit for undertaking energetic actions compared to females.

From Table 2, the results indicated the mean age of cocoa farmers in the study zones was 55 years with minimum and maximum age of 30 years and 75 years respectively. This implied that the average cocoa farmer was 55 years old. This showed that cocoa farmers in the study area were largely old farmers with few young ones getting into cocoa production. The finding is in accordance with Baffoe-Asare et al. (2013) who recorded an older cocoa farming population. From the study, all the farmers had been farming cocoa for a minimum of 2 years, with a mean farming experience of 20 years. This implied that respondents had some experience in cocoa farming. Previous experience in farming enabled farmers to make informed decisions on adoption (Egyir, 2008).

The average household size was about 8 members according to the study. This figure was higher than the national average household size of 4.4 and that of the Bono and Ahafo regions, which recorded a household size of 4.6 per the 2010 Population and Housing Census (GSS, 2012). The average size of cocoa farms in the three communities was 8.45 acres, translating into 3.3 ha, which implied that farmers in the community were having medium size farms.

Moreover, from Table 2, out of the total number of cocoa farmers, 66.7% of the respondents were household heads and 33.3% were not, meaning a majority of them were males because male household heads had better access to inputs such as land compared to their female counterparts who only assisted their husbands. This study is consistent with reports by the GSS (2012), which reported male-headed households as being the majority. About 81.7% of the farmers were married with just 18.3% being single. The finding submits that cocoa farming was an avenue of providing for households in the study zone. Half of the farming households, 50% had further education, 28.3% had only basic education and 21.7% had no formal education which was in disagreement with Anim-Kwapong and Frimpong (2004) who established that many cocoa farmers have elementary education particularly up to the junior high school level. This effect should make them amenable to participate in crop insurance.

Again majority (125) of cocoa producers interviewed representing 75.0% were indigenes (native) in the residency status distribution. Moreover, 36 of the cocoa producers representing 21.7% were settlers (permanent) while 6 of the cocoa producers representing 3.3% were migrant (temporary settlers). All the respondents (100%) in the study area reported cocoa farming as the central commercial activity engaged in, meaning, farmers in the study area were predominantly into cocoa farming. Again, 86.7% were not in any off-farm jobs but only 22 representing 13.3% were in an off-farm job, which enabled them to earn additional income aside the cocoa farming business.

Average price that farmers were willing to pay for crop insurance

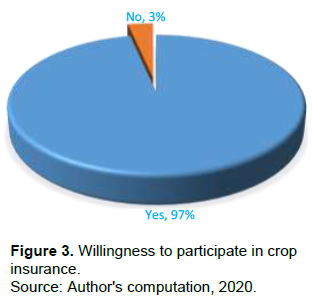

From Figure 3, out of the 167 sampled farmers, 162 farmers representing 97% were eager to partake in crop insurance and 5 representing 3% not ready to participate. This meant high proportion of the farming households in the study area were eager to patronize crop insurance, as they were more probable to secure their ventures from vulnerabilities. This is in accordance with the findings of Kwadzo et al. (2013) who reported readiness to partake in crop insurance among farming households within the Kintampo north municipality of Ghana.

From Table 3, the average price for those enthusiastic to take crop insurance was GH¢ 215.59 per year with a minimum of GH¢5 and a maximum of GH¢2000, so there was a disagreement with Okoffo et al. (2016) who established cocoa farmers in Ghana were eager to pay a mean of GH¢49.32 per year. There was a wide difference between this study and Okoffo et al. (2016) because an average price of GH¢49.32 was very low and farmers were adamant to insure their crop compared to GH¢ 215.59, which was high and a high percentage of 96.7% were willing to participate in insurance at that premium due to the perceive benefit they would derive at that price.

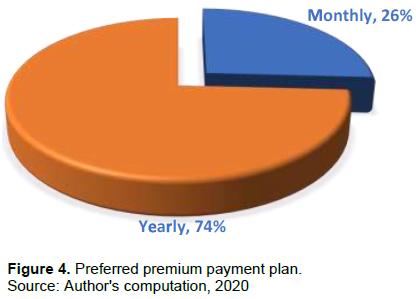

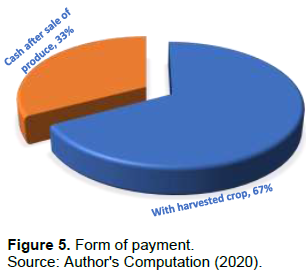

As should in Figure 4, regarding the payment plan, for those who were eager to participate in crop insurance, 74.0% were prepared to pay yearly and 26.0% were willing to pay monthly. In addition, on the form they wanted to do the payment, 67.0% were going to pay with harvested crop after harvesting and 33.0% were going to pay with cash after the sale of produce as indicated in Figure 5.

Factors affecting farmers’ willingness to participate in crop insurance

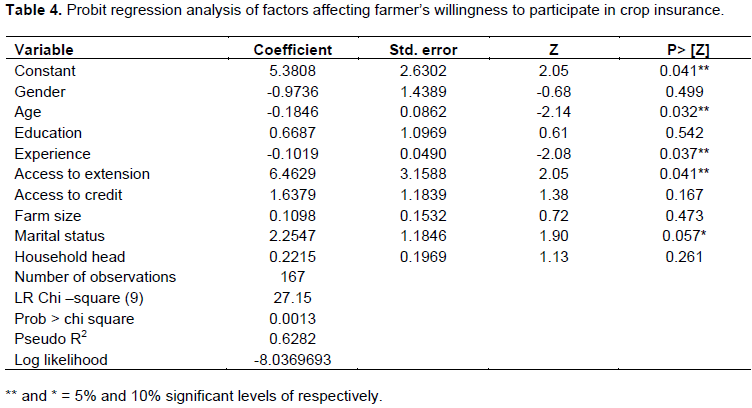

From Table 4, the coefficients of gender and access to credit were –0.9736 and 1.6379, respectively. Even though the coefficient of access to credit carried the positive sign, it did not statistically influence farmers’ willingness to partake in crop insurance significantly. One would have thought that the level of participation of males would be higher paralleled to their female colleagues owing to the fact that males were thought to have better access to resources including credit. Wiredu et al. (2011) report no significant relationship between gender and cocoa technology adoption. Again, the positive sign on the coefficient for access to credit means that credit does not act as a cushion against threats but affect the choice of buying insurance.

Again, marital status and household head with coefficients, 2.2547 and 0.2215, respectively had a positive relationship with readiness to participate in crop insurance but only marital status was statistically significant at the 10% confidence level. This is also comparable to Danso-Abbeam et al. (2014) who reported a positive relationship between household head status and readiness to partake in crop protection. Married farmers have the obligation of decreasing their household’s threats and subsequent deleterious effects thus, bound to participate in crop insurance. Farmers who are single will be additionally ready to buy insurance, which could be on the grounds that with restricted duty of providing for others, these farmers are bound to put aside cash to participate in insurance. This was reliable with the results of Munkaila (2015) among cereal farming households in Ghana. This finding accordingly establishes that both statuses had a positive and significant effect on insurance grounded on various potential explanations.

The age of the farmer was statistically significant at 5% significance level with a coefficient (-0.1846) which showed an inverse association between age and farmers willingness to partake in crop protection. This means an additional increment in age will lead to 0.1846 units reduction in the readiness to participate in crop insurance. This suggests that the aged would be more hesitant in using innovations such as agricultural insurance (Falola et al., 2013), and comparatively, illiterate with less understanding of insurance policies and products (Kakumanu et al., 2012) than younger farmers, hence less probable to participate in crop insurance. Besides what had been said, adult farmers may have acquired enough experience and knowledge in farming, therefore, could predict future weather occurrences (Abebe and Bogale, 2014), accept risk (risk-loving) (Aidoo et al., 2014) or devise a means to manage certain risks since they were aware of them (Wairimu et al., 2016) than younger farmers with less experience, hence, were less probable to partake in crop insurance.

The coefficients of years of experience (-0.1019) and access to extension (6.4629) were statistically significant at 5% significance levels with access to extension having a positive sign suggesting a positive relationship with willingness to participate in crop insurance. Extension services make available to farmers essential knowledge regarding husbandry practices, contemporary tools, management approaches and thus affect farmers buying decision positively. The coefficient of access to extension services is 6.4629, which suggests that an additional increment in access to extension services will result in 6.4629 units increase in willingness to partake in crop protection. In accord with many types of research, the more farmers accessed these services, the greater the likelihood of participating in crop insurance, which educate them on how to manage risk. This outcome is in accordance with Falola et al. (2013) who testified affirmative correlation between extension services and the readiness to buy insurance among farming households.

Years of experience had a negative sign suggesting an inverse relationship with readiness to partake in crop insurance. Years of experience was expected to affect participation positively (Danso-Abbeam et al., 2014; Jin et al., 2016). In this case, it did not. Experience in farming enhances human capital so that information accumulated through years of farming is channeled into decision-making about farming and farmers with considerable experience in farming would probably be more assertive and satisfied with their current husbandry practices and would be more probable to accept an innovation. It was expected that experienced farmers would have more knowledge about the benefits of insurance and therefore prepared to pay greater insurance premium relative to farmers with low years of farming but years of experience affected it negatively because farmers may have encountered these risks previously and probably devised ways of coping with the risks and associated consequences (Wairimu et al., 2016).

The coefficient of education is 0.6687 and carries a positive sign as expected, depicting a positive connection between education and readiness to partake in crop protection. This was however not statistically significant. This suggests that as education increases by 1 unit, willingness to partake in crop protection increases by 0.6687 units. This is because as farmers’ level of education increases, it increases their ability to appreciate insurance products. This is particularly different from less-educated farmers who sometimes find it difficult to accept insurance. Such farmers may participate but later. This result is similar to that of Agyekum et al. (2014) and Tiamiyu et al. (2009) who establish a huge connection between farmers’ education and reception of new technology such as crop insurance.

Finally, farm size with coefficient (0.1098) carried a positive sign, but did not statistically affect farmers’ readiness to partake in crop protection significantly, which is in line with Tiamiyu et al. (2009) who detailed no critical connection between farm size and willingness to embrace innovation.

Constraints affecting cocoa production

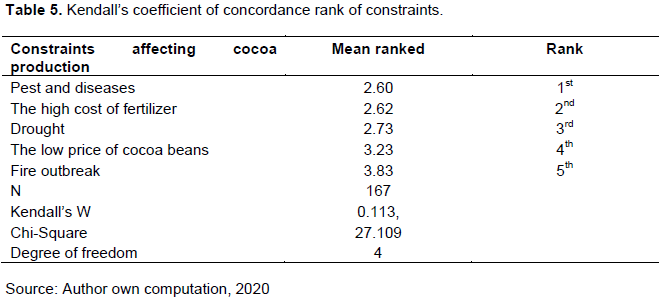

The calculated chi-square value was 27.109. At a significance level of 5% with a degree of freedom of 4, the critical chi-squared value was 9.49. The null hypothesis was rejected since chi-square calculated was greater than chi-square critical.

As shown in Table 5, respondents ranked constraints they faced as farmers, from the highest to the least. The rankings are as follows: Pest and diseases, high cost of fertilizer, drought, low price of cocoa beans and fire outbreak.

Farmers ranked pest and diseases as their major constraint. As indicated by Dormon et al. (2004), the prevalence of pests and diseases is a key problem in cocoa farming in Ghana and has occasioned low harvests because of deficient husbandry practices. Dormon et al. (2007) approximate damages by pests and diseases to be 30% percent of worldwide harvests of the crop every year.

The high occurrence of cocoa pests and infections leads to increased use of pesticides and fertilizers by farming households in the investigation zone. Nonetheless, the farming households pointed that the administration supplied fertilizers, which were woefully inadequate to fertilize their cocoa trees. For example, the farmers pointed out that cocoa plantation within the municipality were to be sprayed four times each year, around July and November with Ghana Cocoa Board (COCOBOD) approved pesticides. As indicated by Aneani et al. (2012) and Danso-Abbeam et al. (2014), spraying rate of the ‘mass spraying exercise’ is not sufficient and cocoa farming households are required to perform extra spraying. This condition rendered farm families in the investigation zone purchased insecticides from the open market, which they complained were costly.

Cocoa is exceptionally vulnerable to dry spells and the trend of planting of cocoa is linked to precipitation circulation. Substantial relationships between cocoa output and precipitation over erratic intervals before harvest have been recounted (Anim-Kwapong and Frimpong, 2004).

The low price of the cocoa bean and fire outbreaks are constraints in cocoa production that influence the revenue of smallholder farmers, accordingly compounding job losses and poverty just as the export earnings of the nation. A greater number of the farmers depend on revenue from the selling of cocoa to pay for their ward’s education, health expenses and daily expenditures. Crop disaster brings about wards of farmers dropping out of school, poor health and poor nourishment of the family overall. The requirement for farming households to prevent these constraints of crop disaster is therefore supreme.

CONCLUSION AND RECOMMENDATIONS

The study assessed the willingness of cocoa farmers to partake in crop insurance in the Dormaa Municipality. The results had established that a greater number of cocoa farmers were eager to participate in crop protection. The study further showed that farmers typically were eager to take insurance if the premium was not more than GH¢ 215.59 yearly, which was quite low. Even though majority of the respondents agreed that crop insurance was important to protect against catastrophic losses, they were eager to pay only a little amount to insure their crops. Thus, either farmers perceived themselves too poor to pay for insurance or they do not fully understand the benefits of crop protection. The outcome of the probit regression showed that significant factors affecting readiness to participate in crop protection were marital status, access to extension, age and years of experience. The results showed that insurance premium paid with harvested crop was the most preferred by the farmers. The next preferred insurance option was where the premium was paid in cash after sale of produce. Thus, the payment of insurance premium with harvested crop was preferred to payment in cash after sale of produce. This was because the use of harvested crop was perceived as an easier option for premium payment. In addition, farmers preferred to pay premium yearly and not monthly. This was because for smallholder farmers, linking harvested crop to their cash after sale of produce seems like double risk. The study discovered respondents faced some constraints regarding cocoa farming. The results of the Kendall’s coefficient of concordance utilized to rank the limitations revealed that the main ranked constraint the farmers faced was pest and diseases, followed by high cost of fertilizer, drought and the least constraint was low price of cocoa beans.

The study recommends that extension agents and other agricultural insurance stakeholders should be able to sensitize crop farmers on the importance of crop insurance policy, as this would help to improve their level of participation in insurance. In addition, agricultural insurance centers should be located in each extension block in the study area; this will ensure easy access to insurance experts and the rate of insurance uptake. Again, farmers should be encouraged to further their education as it has a significant consequence on their acceptance of crop insurance. Insurance enterprises should deliver crop insurance to farmers at reasonable amounts to embolden them to participate. From the study, an average premium of GH¢ 215.59 which was to be paid yearly was estimated. Having this in view, GAIP (Ghana agricultural insurance program) should consider this price tag accepted by the crop farmers and reach a conclusion below or equal to this premium.

CONFLICT OF INTERESTS

The authors have not declared any conflict of interests.

REFERENCES

|

Abebe TH, Bogale A (2014). Willingness to pay for Rainfall based Insurance by Smallholder Farmers in Central Rift Valley of Ethiopia: The Case of Dugda and Mieso Woredas. Asia Pacific Journal of Energy and Environment 1(2):121-155. |

|

|

Adams A (1995). Banking and Finance Series Investment. Kluwer Law International, London. |

|

|

Aderinola EA, Abdulkadri AO (2007). Resource Productivity of Mechanised Food Crop Farm in Kwara State, Nigeria. Delta Agriculturist 2:59-71 |

|

|

Agyekum EO, Ohene-Yankyera K, Keraita B, Fialor SC, Abaidoo RC (2014). Willingness to Pay for Faecal Compost by Farmers in Southern Ghana. Journal of Economics and Sustainable Development 5(2):18-25. |

|

|

Agyemang M (2010). The Determinants of Cocoa Output: A Case Study of the Aowin Suaman District. American Journal of Environmental Sciences 1(3):194-201. |

|

|

Aidoo R, Mensah JO, Wie P, Awunyo-vitor D (2014). Prospect of Crop Insurance as a Risk Management Tool among Arable Crop Farmers in Ghana. Asian Economic and Financial Review 4(3):341-354 |

|

|

Ajakaiye DO, Adeyeye VA (2001). The Nature of Poverty in Nigeria. NISER Monograph Series: No. 13, 2001, 1badan NISER. |

|

|

Anang BT (2011). Market structure and competition in the Ghanaian cocoa sector after Partial liberalization. Current Research Journal of Social Sciences 3(6):465-470. |

|

|

Anim-Kwapong GJ, Frimpong EB (2004). Vulnerability and adaptation assessment under the Netherlands climate change studies assistance programme phase 2 (NCCSAP2): vulnerability of agriculture to climate change-impact of climate on cocoa production. Cocoa Research Institute of Ghana, Ghana. |

|

|

Asante KP, Zandoh C, Dery DB, Brown C, Adjei G, Antwi-Dadzie Y, Adjuik M, Tchum K, Dosoo D, Amenga-Etego S, Mensah C, Owusu-Sekyere KB, Anderson C, Krieger G, Owusu-Agyei S (2011). Malaria epidemiology in the Ahafo area of Ghana. Malaria Journal 10(211):1-14. |

|

|

Baffoe-Asare R, Danquah JA, Annor-Frimpong F (2013). Socioeconomic Factors Influencing Adoption of Codapec and Cocoa High-tech Technologies among Smallholder Farmers in Central Region of Ghana. American Journal of Experimental Agriculture 3(2):277-292. |

|

|

Barrett CB, Barnett B, Carter M, Chantarat S, Hansen L, Mude A, Osgood D, Skees TC, Ward M (2008). Poverty Traps and Climate and Weather Risk: Limitations and Opportunities of Index-based Risk Financing. IRI Technical Report 070, International Research Institute for Climate and Society, Columbia University, New York, NY. |

|

|

Briesinger C, Diao Z, Kolavalli S, Al Hassan R, Thurlow J (2011). A new era of transformation in Ghana: Lessons from the past and scenarios for the future. IFPRI Research Monograph, IFPRI, Ghana. |

|

|

Danso-Abbeam G, Addai KN, Ehiakpor D (2014). Willingness to Pay for Farm Insurance by Smallholder Cocoa Farmers in Ghana. Journal of Social Science for Policy Implications 2(1):163-183. |

|

|

Dormon ENA, Huis AV, Leeuwis C (2007). Effectiveness and profitability of pest management for improving yield on small holder cocoa farms in Ghana. International Journal of Tropical Insect Science 27(1):27-39. |

|

|

Dormon ENA, Van Huis A, Leeuwis C, Obeng-Ofori D, Sakyi-Dawson O (2004). Causes of Low Productivity of Cocoa in Ghana: Farmers' Perspectives and Insights from Research and the Socio-political Establishment. NJAS - Wageningen Journal of Life Sciences 52(3-4):237-259. |

|

|

Egyir IS (2008). Assessing the Factors of Adoption of Agro-chemicals by Plantain Farmers in Ghana Using the ASTI Analytical Framework. |

|

|

Falola A, Ayinde AE, Agboola BO (2013). Willingness to Take Agricultural Insurance by Cocoa Farmers in Nigeria. International Journal of Food and Agricultural Economics 1(1):97-107. |

|

|

Ghana Statistical Service (2012). 2010 Population and Housing Census: Summary Report of Final Results. Accra, Ghana: Ghana Statistical Service. |

|

|

Ghana Statistical Service (2019). Revised 2013 to 2018 annual gross domestic product. Accra, Ghana: Ghana Statistical Service. |

|

|

Gujarati DN, Madsen JB (1998). Basic econometrics. Journal of Applied Econometrics 13(2):209-212. |

|

|

Haruna U, Garba M, Nasiru M, Sani MH (2010). Economics of Sweet Potato Production in Toro Local Government Area of Bauchi State, Nigeria. Proceedings of 11th Annual National Conference of National Association of Agricultural Economists (NAAE). |

|

|

ILO (2011). Social protection floor for a fair and inclusive globalization, Report of the Social Protection Floor Advisory Group. International Labor Office, Geneva. |

|

|

ISSER (2011). The State of the Ghanaian Economy, Accra, Ghana: Institute of Statistical Social and Economic Research, University of Ghana, Legon. |

|

|

Jin J, Wang W, Wang X (2016). Farmers' risk preferences and agricultural weather index insurance uptake in rural China. International Journal of Disaster Risk Science 7(4):366-373. |

|

|

Kakumanu KR, Palanisami K, Nagothu U, Xenarios S, Reddy K, Ashok B, Tirupataiah T (2012). An insight on farmers' willingness to pay for insurance premium in South India: Hindrances and challenges. Paper presented at the challenges of index-based insurance for food security in developing countries: Proceedings of a technical workshop organized by the EC (European Union) Joint Research Centre (JRC) and the International Research Institute for Climate and Society (IRI), 2-3 May 2012, Luxembourg. |

|

|

Kendall MG (1962). Rank Correlation Methods: 3d Ed. C. Griffin. |

|

|

Kwadzo TMG, Kuwornu JKM, Amadu ISB (2013). Food Crop Farmers' Willingness to Participate in Market-Based Crop Insurance Scheme: Evidence from Ghana. Research in Applied Economics 5(1):1-21. |

|

|

Liao TF (1984). Logit, Probit and Other Generalized Linear Models. Sage Publications, USA. |

|

|

Munkaila HF (2015). Cereal Farmers Willingness to pay for Weather- Based Index Insurance (WII) Product as a Risk Management Tool in the Eastern Region of Ghana. Master Thesis. Department of Agricultural Economics and Agribusiness, University of Ghana. |

|

|

Nimo F, Baah K, Tham-Agyekum EK (2011). Investigating the Interest of Farmers and Insurance Companies in Farm Insurance: The Case of Cocoa Farmers in Sekyere West Municipal of Ghana. Journal of Agricultural Science 3:4. |

|

|

Okoffo ED, Denkyirah EK, Adu DT, Fosu-Mensah BY (2016). A double-hurdle model estimation of cocoa farmers' willingness to pay for crop insurance in Ghana. Springer Plus 5(1):873. |

|

|

Oluyole KA, Sanusi RA (2009). Socioeconomic Variables and Cocoa Production in Cross River State, Nigeria. Journal of Human Ecology 25(1):5-8. |

|

|

Quagrainie K (2006). IQF Catfish Retail Pack: A Study of Consumers' Willingness to Pay. International Food and Agribusiness Management Review 9:2. |

|

|

Ray PK (2001). Agricultural Insurance: Theory and practice and application to Developing countries. 2nd edition, Oxford: Pergamon Press. |

|

|

Sarris A (2002). Market based Commodity Price Insurance for Developing Countries: Towards a New Approach, paper presented at the XXIV International Conference of Agricultural Economists, August 13-19, 2000. Berlin, forthcoming in Revue D'Economie du Development. |

|

|

Tiamiyu SA, Akintola JO, Rahji MAY (2009). Technology Adoption and Productivity Difference among Growers of New Rice for Africa in Savanna Zone of Nigeria. Tropicultura 27(4):193-197. |

|

|

Wairimu E, Obare G, Odendo M (2016). Factors affecting weather index-based crop insurance in Laikipia County, Kenya. Journal of Agricultural Extension and Rural Development 8(7):111-121. |

|

|

Williams C, Fenton A, Huq S (2015). Knowledge and adaptive capacity. Nature Publishing Group 5(2):82-83. |

|

|

Wiredu AN, Mensah-Bonsu A, Andah EK, Fosu KY (2011). Hybrid Cocoa and Land Productivity of Cocoa Farmers in Ashanti Region of Ghana. World Journal Agricultural Sciences 7(2):172-178. |

|

|

Yamane T (1967). Statistics: An Introductory Analysis, 2nd edition, New York: Harper and Row. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0