Full Length Research Paper

ABSTRACT

Agricultural cooperatives are autonomous associations of individuals formed to augment production, marketing and financial needs of members. In Uganda, performance of cooperatives is largely constrained by weak organizational structures, market failures, and policy weaknesses. An integrated cooperative model (ICM) was introduced to improve performance of cooperatives but the effect of ICM on institutional performance has not been evaluated. This study examined the effect of cooperative integration on bulk production and credit provision to smallholder farmers. A multi-stage sampling technique was employed to select 40 cooperatives for the study. Primary qualitative and secondary quantitative data were collected from 16 focus group discussions and cooperatives’ performance reports respectively. Data was analyzed using thematic content analysis, t-test and censored tobit regression model to assess performance of the studied cooperatives. The results showed that integrated cooperatives bulk larger proportions of produce and disburse bigger loan proportions than single cooperatives. Tobit model revealed that integration has a positive significant (p< 0.05) influence on cooperatives’ performance in bulk production and providing credit. In conclusion, the results demonstrate that adoption of ICM improves performance of cooperatives and benefits to small holder farmers.

Keywords: Bulk production, credit provision, cooperatives, smallholder farmers

INTRODUCTION

A cooperative is an autonomous association of individuals who voluntarily unite to meet their common economic, social and cultural needs, and aspirations through a jointly-owned and democratically-controlled initiative (Adrian and Green, 2001). Cooperatives emerge from the main drivers of cooperation including; financial savings, credit access, risk sharing, perceived discount rates of future returns, joint production and marketing (Adrian and Green, 2001). Agricultural cooperatives play a vital role in meeting member needs (Gashaw and Kibret, 2018; Orr et al., 2017). However, such cooperatives are challenged by market volatility, global and public policy alterations (Hendrikse, 2006). These challenges complicate the cooperatives operational environments that call for innovative interventions to augment cooperative responsiveness to the changing needs of members. In wealthy countries such as Canada, multiple cooperative models such as the Arctic Cooperatives have emerged to facilitate contribution of cooperatives to community development by meeting the diverse needs of members (Hammond and MacPherson, 2001).

In the Ugandan context, cooperatives have been in existence since 1913, initially established to minimize exploitation of smallholder farmers by monopolistic traders, largely organized in a vertical- top-down structure as single entities heavily supported by state systems (Bazaara, 2001). These cooperatives crumbled under the weight of economic liberalization in 1987, leading to dynamic processes of restructuring and adjustment to the conditions of a liberalized economy (Kwapong, 2012). In the late 1990s, the Uganda Cooperative Alliance brought together diverse Rural Producer Organizations (RPOs) to develop Area Cooperative Enterprises (ACEs) under a new marketing model premised to serve farmers’ needs better in the new economic context (Kwapong, 2012).

Further adjustment was introduced by the Canadian Cooperative Association (CCA) in a form of an integrated cooperative model, encompassing the RPOs, ACEs, and Savings and Credit Cooperative societies (SACCOs) (Kwapong, 2012). Despite the introduction of the integrated cooperative model, some cooperatives still exist as single independent entities (Kwapong and Hanisch, 2013). The institutional performance of cooperatives under this mixed cooperative model environment in Uganda has not been previously studied. This study investigated the effect of integration on the performance of cooperatives among smallholder farmers through two objectives: to evaluate the performance of integrated and single cooperatives in terms of bulk production and credit provision to smallholder farmers; and to examine the effect of integration on performance of cooperatives in meeting the needs of members. The study tested one hypothesis, that integration significantly improves performance of cooperatives via increased bulk production and credit provision among other benefits to smallholder farmers.

Theoretical frame work of cooperative integration and performance

Cooperative integration

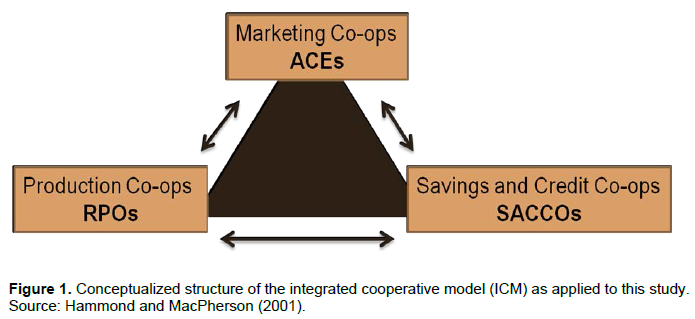

Hammond and MacPherson (2001) define cooperative integration as the legal linkage among cooperatives of similar (horizontal integration) or different (vertical integration) functions. The Hammond’s theory identifies an example of horizontal integration as a group of diverse producer organizations (RPOs) coming together to offer common services such as bulk production for collective marketing. An example of vertical cooperative integration involves a group of RPOs linking with SACCOs and Area Cooperative Enterprises (ACE) for diverse functions such as financial access and collective marketing among others. The vertical integration was theorized to be a three stage triangular shaped model referred to as the integrated cooperative model (ICM) (Figure 1). Fici (2015) argues that a study that regards a cooperative as an isolated economic unit, without any relations with other cooperatives, would provide only an incomplete view and an inaccurate concept of the operations of such a cooperative. Cooperatives often establish economic and socio-political forms of inter-cooperative integration, which contribute to their success as distinct legal enterprises. This theory by Fici (2015) recommends that there should be cooperation among cooperatives for maximum benefit to stakeholders. Linking the above theories, this study conceptualized the ICM as a perfect explanation for cooperative function and performance of diverse cooperatives in Uganda. The ICM supports the joint development of three distinct but inter-connected, cooperatives (ACEs, RPOs, and SACCOs), for holistic benefit to smallholder farmers (Figure 1).

In the integrated cooperative model, different cooperatives play distinct but related roles of production, marketing support and financial services for holistic benefits to members (Hammond and MacPherson, 2001). According to Anastase et al. (2016), RPOs are made up of individual smallholder farmers, who join together to increase their agricultural production and productivity, and to bulk their production for sale. On the other hand, ACEs are second-tier cooperatives focused on marketing, typically made up of six to ten production cooperatives working together to take advantage of economies of scale. The ACEs provide market information, source agricultural inputs in bulk, assist with strengthening of market linkages, offer training to members, and help to negotiate bulk sales at good prices. SACCOs are a vital third element of integrated cooperative model, acting as financial engines for the development and growth of the RPOs and ACEs in the integration. The SACCOs are in fact referred to as the life blood of the other cooperative enterprises (Hammond and MacPherson, 2001). This is because, SACCOs provide finance to farmers that enhance agricultural production and productivity, and run sustainable farm businesses. Working within the integrated model, cooperative members identify opportunities and make choices to attain both individual and collective goals for increased food production and productivity, linkages to larger markets, access to better prices, and access to affordable financial services. The integrated cooperative model in a theory proposed by Hammond and MacPherson (2001) was adopted for this study to explain the multidimensional integration of cooperatives in Uganda.

Performance of cooperatives

Chibanda et al. (2009) reported that performance of cooperatives is difficult to measure and interpret, because their prime objective is to pay their members the best price for the products received and or charge the lowest possible price for the inputs and services. However, Lerman and Parliament (1990) argued that performance of cooperatives can be measured in financial terms. Staatz (1994) defines performance of cooperatives as the optimized joined benefit of the coalition, while bargaining among heterogeneous members about how to distribute the net benefit. The theory of Staatz (1994) opines that cooperatives aim to optimize the objective for which they were formed for the joint benefit of association. Soboh (2009) and Persson (2010) further argued that measuring performance of a cooperative entails assessing progress towards achieving predetermined objectives by evaluating the extent to which basic interests considered by members to join the cooperative are satisfied.

Kyriakopoulos et al. (2004) defines performance as improved product quality, productivity, technical efficiency, service capabilities of a firm, and logistical performance (which include an organization’s ability to meet promised delivery dates), that leads to sustainable profits. “The choice of criteria for organizational performance is a contextual issue that depends on the nature of the organization in question” (Persson, 2010). Persson (2010) reported that evaluation of cooperative performance starts with discussing what cooperatives can and cannot do in consideration of the cooperative goals. On the other hand, Okello (2013) reveals that understanding cooperative principles is the only viable benchmark for performance following the tendency to measure every success and failure, against consistency or deviation from the principles written down. Performance of cooperatives is different compared to investor firms which relay on financial performance indicators like profitability, debt, operational efficiency, equity growth and size.

According to Chibanda et al. (2009), there are two popular measures of economic performance of cooperatives including, return on assets and growth in sales. Other key variables to assess cooperative performance include, training of members, loss of membership, market arrangements, levels of asset growth, levels of equitable capital, cooperative financing, net surplus generation and or price advantage to members (Chibanda et al., 2009). In assessing the performance of integrated and single cooperatives, this study considered objective based indicators such as; bulk production, farmer mobilization, credit provision and service to non-members (community service) as proposed by several authors (Chibanda et al., 2009; Soboh, 2009 and Persson, 2010).

Conceptual frame work of cooperative integration and performance

Desrochers and Fischer (2005) reported that integration reduces volatility in efficiency and performance of cooperatives. Despite the high costs of running hub?like organizations in highly integrated systems, these systems economize in bounded rationality and operate at lower costs than less integrated systems (Desrochers and Fischer, 2005). Bijman (2010) showed that small holder farmers acting alone do not always benefit from higher market prices, those acting collectively in strong producer organizations and cooperatives are more able to take advantage of market opportunities. The above concepts informed the hypothesis of this study, that among other factors, the integration of cooperatives significantly improves performance of cooperatives in meeting objectives for which they were formed and meeting the needs of small holder farmers. Using the censored Tobit regression model, the performance of SACCOs in terms of loan portfolios, and the performance of RPOs in terms of bulk production as affected by the type of cooperative model and associated factors were studied.

METHODOLOGY

Sampling procedure and data collection

The study was conducted in Ntungamo and Nebbi districts located in South Western and North Western Uganda respectively. The two districts were purposively selected from varying geographical locations given the existence of functioning integrated and single cooperative models in these localities. A multi-stage sampling procedure was employed by considering the model of cooperation as either integrated or single in the 1st stage followed by the type of cooperative as either RPO or SACCO in the 2nd stage. A total of 40 cooperatives were studied including 32 RPOs and 8 SACCOs with equal representation of respondents from either district. Some of the cooperatives studied in Ntungamo District include: Nyakyera Cooperative Union, Bujuzya Farmers Dairy Cooperative Society, Ruhara Diary, Kajara Youth, Kashanda Credit and Savings Farmers’ Cooperative, Katojo Society, Rwentobo SACCO, Obuyora Farmers Dairy Cooperative Society, Nyabihoko SACCO and Rugarama Financial Services while from Nebbi District, some of the cooperatives studied included; Pakwach Nam SACCO, Panyamur SACCO, Wadelai SACCO, Zeu SACCO, Erussi RPO, Kuchwinyi RPO, Panyango RPO, Zeu RPO, Kango RPO, Nyaravur RPO, Pakwinyo North RPO, Pakwinyo Central RPO, Wadelai Farmers Union, and Ochayo Waribtam RPO.

Quantitative secondary data was collected from seasonal and monthly performance reports of cooperatives covering a period of two years (2013 and 2014). This secondary data include number of cooperative members and non-members served by cooperatives, volumes of produce bulked from members and non-members, targeted and actual volumes of bulk production, proportion of loans disbursed to disbursed to members and non-members, and interest rates.

Qualitative data was collected through 16 focus group discussions (FGDs) involving cooperative members of integrated and single cooperative models, non-cooperative members who receive services from cooperatives and local governmental officials involved in cooperative development across the two districts. The data collected from FGDs included cooperative history, mode of establishment, location of cooperative, model type, months of operation, and cooperative governance system among others.

Data analysis

While qualitative data was analyzed using thematic content analysis, quantitative data was statistically analyzed using STATA software version 14 (Stata Corp, 2015). The t-test inferential analysis was used to determine the difference between the mean performance of integrated and single cooperatives in terms of bulk production and credit provision. Proportion of produce bulked and loans disbursed were used to represent performance of RPOs and SACCOs respectively. Proportions were used and not actual volumes because different cooperatives specialize in different enterprises which couldn’t be directly compared using actual volumes. For example, comparing coffee volumes and banana volumes at RPO level would be misleading since coffee is measured in kilograms but bananas are measured by number of bunches. The proportions of volumes of produce bulked by RPOs were calculated as the ratio of expected to actual volumes of produce bulked. Similarly, SACCOs have different targets of loan sizes for disbursement which makes proportions suitable for measuring performance rather than actual loan values. The performance of SACCOs was determined as proportions of sizes of loans disbursed to expected sizes of loans for disbursement. The model specification in equation 1 was used for determining proportions of bulk production by RPOs and loan sizes by SACCOs:

Yi (t) =  where ∈≠0………………………. (1)

where ∈≠0………………………. (1)

Where, y represents the proportional outcome, subscript i represents variables such as loan disbursed, bulk production, loan given to non-members, bulk production from non-members, trainings organized, size of loan borrowed from SACCOs, savings and farmers mobilized, t represents the time factor measured as season for RPOs and months for SACCOs, A is the actual value obtained and ∈ is the expected value.

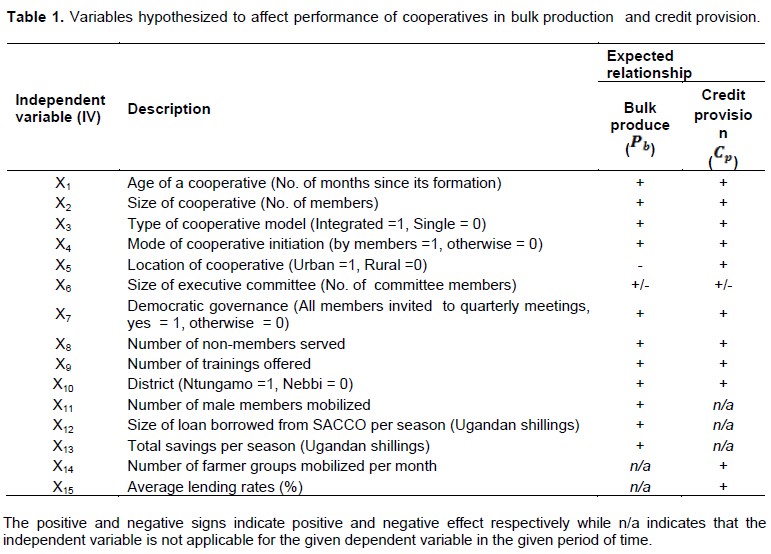

A censored tobit regression model was used to examine the effect of integration on performance of cooperatives in terms of bulk production and credit provision. Several predictor variables were entered into the model to assess their relationship with integration and performance of cooperatives across the two regions of Uganda (Table 1).

Before censored tobit modeling, the predictor variables were subjected to multicollinearity and heteroscedasticity tests using variance inflating factor (VIF) and Breusch-Pagan test, respectively to ensure consistent results. The data was then censored between zero and a hundred to minimize errors from missing variables and incomplete data. During the tobit model analysis, the linear effect (coefficient values) of predictor variables was expected to impact the uncensored latent variables namely, bulk production and credit provision. The effect of the explanatory variables on the observed outcome (proportion of bulk production and proportion of loan disbursed) were represented by the marginal effects (dy/dx). The tobit model specification for bulk production and credit provision is represented in equations 2 and 3 respectively:

Pbit= α0t + α1X1t +….+ αnXnt+ ?it……………………………………… (2)

Cbit = α0t + α1X1t+….+ αnXnt + ?it……………………………………… (3)

The dependent variable, Pbit represents the proportion of bulk production, Cbit represents proportion of loan sizes disbursed, α is the regression coefficient for each variable entered into the model, i represents individual cooperative under consideration, t represents the time dimension, εi is the error term due to time specific invariant effect and other un observed factors, while X1 …X n represent the various independent variables (Table 1).

RESULTS AND DISCUSSION

Performance of RPO cooperatives under integrated and single cooperative models

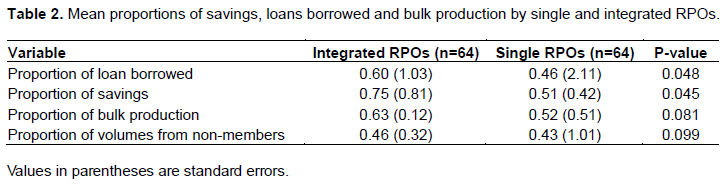

The proportions of bulk production from members and non-members, savings and amount of loans borrowed from SACCOs were significantly (p<0.05) higher in RPOs under integrated than single cooperative model (Table 2). The integrated RPOs also receive significantly (p<0.10) large contributions of produce from non-members than under the single cooperatives. This is because integrated cooperatives have high level of social responsibility that attracted large amounts of produce from non-cooperative members on seasonal basis. These results were corroborated by findings from the FGDs which affirmed that non-members who produce bulk with integrated cooperatives would consequently join as registered members enticed by the benefits that come with cooperation. The integration of RPOs and SACCOs strengthens access to credit, improves volumes produce bulked for sale. Wu et al. (2015) explained that integration of agricultural organizations enhances networking, and access to marketing services which are vital for organizational development leading to improved bulk production and sales.

Integrated RPOs benefit from engaging a large number of non-members that lead to increased capacity to pool large volumes of produce and attain targeted volumes augmenting their bargaining power in open competitive markets. Integration of cooperatives improves overall performance in terms of cost sharing unlike in single cooperatives where all costs are incurred by one cooperative entity (Kwapong and Hanisch, 2013). Single RPOs bulk less produce due to unreliable markets, less bargaining power, and over dependence on open marketing (Ampaire et al., 2013). The weakness of single cooperatives are due to structural limitations such as limited storage facilities and weak linkages to markets making them less competitive in open markets which in turn significantly results in less bulk production from non-members. For example, most of the single RPOs store produce in rented warehouses, which are normally associated with increased transaction costs that in the long run limit returns and participation of non-members.

The integrated RPOs borrow significantly (p<0.05) higher loan sizes compared to single cooperatives (Table 2), because of the need to invest huge resources in production of large amounts of produce to meet the set targets for bulk production and marketing. The loans borrowed by integrated RPOs are used to purchase inputs that improve production which attracts more revenues and profits from relatively higher prices in booked markets. Integrated RPOs benefit from running accounts with SACCOs making them legible borrowers of larger loans at lower rates than single RPOs. Nuwagaba (2012) reported that single RPOs enjoy limited privileges of running accounts with SACCOs because of small saving portfolios which exposes them to high interest rates from SACCOs. According to Abebe et al. (2010), high profits from bulk sales and reduced transaction costs are realized under cooperation and more so under integrated cooperatives which increase the chances of high savings and strengthens the borrowing powers and loan paying capabilities of such rural producer cooperatives. The institutional policy of saving from every season’s sales by integrated cooperatives boosts the savings of integrated RPOs compared to single RPOs which are not obligated to make seasonal savings with SACCOs because they are not formal members and not bound by SACCO rules.

Performance of integrated and single SACCOs

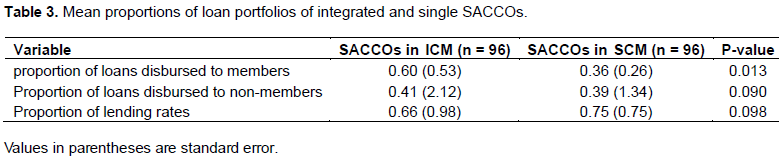

The performance differences between integrated and single SACCOs in providing credit are presented as proportions of total loans disbursed (actual loan sizes disbursed versus targeted amount of loans for disbursement), proportions of loans disbursed to non-members (actual loans to non-members versus targeted loans to non-members) and the average lending rates (Table 3). The results show significant (p<0.05) differences in loan portfolios between integrated and single SACCOs. The differences in proportion of loans disbursed by integrated and single SACCOs is attributed to large membership of farmer groups in integrated SACCOs compared to single SACCOs where membership is mainly of individual farmers. Farmers groups are more likely to obtain large loan facilities from SACCOs than single farmers with limited credit worthiness. Wambugu et al. (2009) argued that social networks with other financial institutions like the network between integrated SACCOs and Microfinance Support Centre Limited strengthens the capacity of such integrated SACCOs to disburse large loan sizes to members.

The results further indicated that integrated cooperatives disburse more proportions of loans to non-members than single cooperatives (Table 3). This might be explained by the holistic approach taken by integrated cooperatives to community development by seeking to attract non-members who then appreciate the benefits of the integrated cooperative model and join as legal members. Ketilson and MacPherson (2001) reported that the strong institutional value of social responsibility by integrated cooperatives promotes participation in community service involving both members and non-members. The integrated SACCOs have increased capacity to disburse large loan sizes which explains their capacity to disburse loans even to non-members. Williams (2016) and Yamko (2008) argued that proper financing and full participation of different members in cooperatives is one of the most important factors for cooperative development and success in achieving its objectives. Integrated cooperatives tend to charge significantly (p<0.10) lower lending rates to attract as many members as possible. The cost of financing is a major factor influencing decision making to seek credit for agricultural investment. Research shows that lower lending rates present a competitive edge that attracts many clients which increases chances of disbursing large loan sizes (Awoyemi and Jabar, 2014).

Effect of integration and other factors on bulk production by Rural Producer Organizations

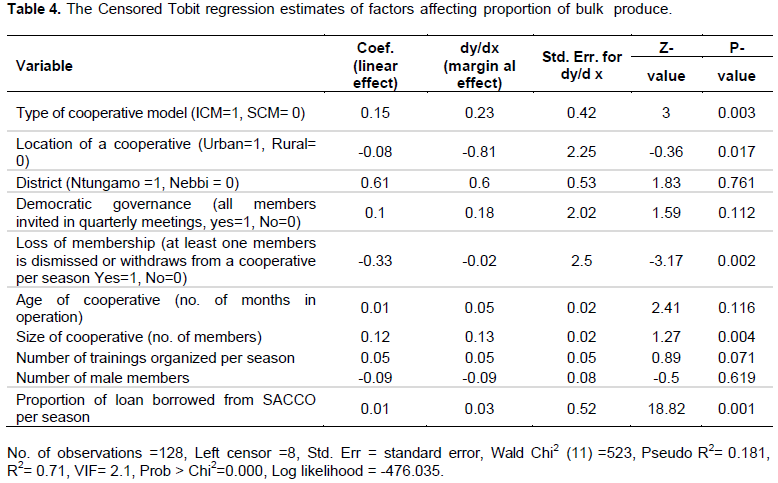

The effect of integration and other factors on performance of RPOs in bulk production were evaluated using a censored tobit regression model and the results are indicated in Table 4. The results revealed that the type of cooperative model, location, loss of membership, size of cooperative, proportion of loans borrowed from SACCO per season had significant effects (p<0.01) on the performance of cooperatives in bulk production. Integration of RPOs had a significantly positive effect on performance in bulk production. The results further indicated that the integrated cooperative model linearly increases bulk production by 15%. This is because cooperative integration yields multiple opportunities such as reliable access to finances, bulk inputs, assurance of market services, trainings on good agronomic practices and transport facilities that lead to better performance for bulk produce and related functions. Wu et al. (2015) reported similar findings which showed that integration of cooperatives increases social networking in form of linkages between individuals and groups and enhances access to technical, financial and market information that act as incentives for bulk produce by members.

The effect of number of trainings on performance of cooperatives in bulk production hinged on the fact that trainings enlighten the members on the benefits of bulk sales and improves trust and commitment of members to contribute their produce to the cooperative produce targets. Matthews-Njoku et al. (2003) explained that training is positively correlated with the rate of technology adoption which improves production and productivity and consequently results in increased bulk production. Wu et al. (2015) reported that training enriches the knowledge of members to take informed decisions regarding performance of their cooperatives. This is because training empowers members to have a better understanding of cooperative’s operations and obligations which strengthens ownership leading to better performance and sustainability (Chibanda et al., 2009).

Results further revealed that increasing the proportion of loans that RPOs borrow from SACCOs positively and significant (p<0.01) affects bulk production (Table 4). The significant positive relationship of sizes of loans borrowed and bulk production is because credit empowers members to access inputs timely and afford transport for produce to the bulk centers. Similar findings have been reported by Ton et al. (2010), showing that loans motivate farmers to invest more in production so as to realize better returns for bulk production and payment of the loan obligations after sales. The positive and significant effect of size of a cooperative on proportions of bulk production was linked to direct increase in the pool of produce for example: Nyakyera Cooperative Union (a maize bulking RPO), Abateganda Ntungamo Coffee Growers and Wadelai Farmers Union (RPO rice bulk) had over 100 members bulking over 200MT compared to Kajara Youth Group and Erussi RPO which with less than 30 members, had about 60MT of bulk production. The increase in the pool of bulk production comes with advantages of economies of scale such as negotiating for higher price margins in addition to reduced transaction costs (Ampaire et al., 2013). Cazzuffi and Moradi (2012) reported that increasing size of a cooperative membership improves the chances of cooperative sustainability and promotes cooperative performance. Besides, these results show that when a cooperative loses a member by withdrawal, dismissal or natural death, bulk production reduces. This observation is associated with direct reduction on the pool of produce previously contributed by the lost member. Chibanda et al. (2009) further argued that loss of membership leads to low morale and poor image of cooperative which makes members renege on their contracts. Low confidence in the cooperative makes famers individually start searching for alternative market opportunities; thus, dwindling the volumes of produce bulked with the cooperative. Such acts usually threaten the development and sustainability of the cooperatives.

Inclusion of proportion of produce from non-members significantly (p<0.05) increased the overall performance of cooperatives in bulk production such as Nyakyera Cooperative Union dealing in bulk maize production showed a 10% increment in maize produce bulked, due to over 10MT of maize received from non-members. This positive influence is attributed to the fact that volumes of produce from non-members are not always projected in target volumes for bulk production yet it directly increases the pool of actual volume of bulk production. Conversely, urban location of a cooperative had significant negative (p<0.05) effect on volumes of bulk production. It is because long distances and higher costs of transporting produce from the village farms to the bulk centers tend to hinder compliance by farmers (Fafchamps and Hill, 2005). Unfortunately, farmers in urban locations are sometimes offered quick cash by open market traders, which seduce these farmers to sell off some of the produce resulting in reduced volumes of bulk produce available with the RPOs.

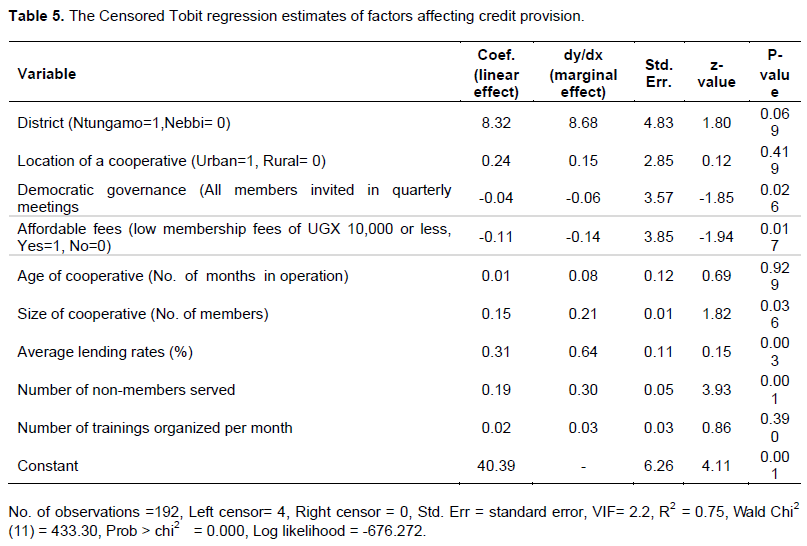

Factors affecting credit provision by integrated and single SACCOs

The results in Table 5 revealed that among other factors, integration of cooperatives had a positive effect on performance of SACCOs in terms of providing credit to cooperative members. The effect of the type of cooperative model on the proportion of credit disbursed was significant indicating that cooperative integration improves the likelihood of more credit disbursement. The censored tobit regression model revealed that integration of cooperatives boosts credit provision. The positive effect of integration on credit provision could be explained by the fact that integration attracts membership and lowers effective costs due to cost sharing and spreads the liabilities hence reducing unit risks per funds disbursed. This argument is supported by reports from Wu et al. (2015), that integration of cooperatives increases social networking in form of linkages between individuals and groups which enhance access to technical, financial and market information regarding credit access.

The effect of size of a cooperative on credit provision was also positive and significant (p<0.05) indicating that increasing cooperative membership increases credit provision probably because of the improvement in resources from new membership fees. Previously, Jones and Kalmi (2015) reported similar findings showing that increase in cooperative membership increases the number of legible credit borrowers resulting in proportionate increase in the sizes of loans disbursed. Large cooperative numbers increase resources available for cooperatives to disburse large loan sizes (Verhofstadt and Maertens, 2013).

Whereas non-members do not pay membership fees, they benefit from credit facilities offered by SACCOS, which significantly increases SACCOs’ credit provision portfolio. The findings of focus group discussions showed that non-members are offered loans but at relatively higher interest rates than that of members according to the policy of a given cooperative. The high interest rates earned from non-member clients influence cooperatives to disburse more loans for such high returns. This finding corresponds with the observation that average lending rates positively and significantly (p<0.05) affect performance of cooperatives in providing credit because increase in credit provision especially to non-members results in higher returns from interest rate (Table 5). The results from the FGDs further showed that SACCOs normally disburse large sums of loans to businessmen at relatively higher interest rates than that offered to members based on agreed membership terms and conditions. The discussions revealed that businessmen possess high payment ability which propels cooperatives to disburse large sums of money to such high return clients. However, this finding contradicts the demand theory whose premise is that such high lending rates would scare away potential clients for alternative sources of credit that offer lower interest rates. Awoyemi and Jabar (2014) reported that lower lending rates attract many clients which prompts cooperatives to increase the lending rates and at times practice price discrimination.

The democratic governance represented by participation of all members in quarterly meetings significantly (p<0.05) lowers credit provision. This is based on the fact that these meetings result in delayed loan processes because of lengthy negotiations and delayed decision making by management and all members. Kyriakopoulos et al. (2004) observed that meetings by all members increase workloads of loan officers who must await decisions from meetings by all members before sanctioning loan disbursement thus delaying and consequently reducing the number of loans paid out in a specific period. Such reduction in loan disbursements results in low capital investment and less returns from the few loans disbursed which constrains financial capability of SACCOs to lend to future clients. Similarly, low averages of membership fees (2.74 USD or less) accounted by 62.5% of cooperatives studied had significant (p<0.05) negative effects on performance of SACCOs in providing credit. This is because the limited pool of financial resources from members’ contributions reduces the overall amount of funds available for disbursement. This observation is supported by Verhofstadt and Maertens (2013) who argued that low membership fees reduce the gross cooperative revenue which gradually reduces the surplus funds for disbursement. However, district, location of a cooperative, age of a cooperative and number of trainings organized per month showed a positive effect on credit provision by a cooperative although the effect was not significant.

CONCLUSIONS

The integration of cooperatives improves performance in terms of bulk production, and providing affordable and timely credit leading to improved production, access to finances and marketing options. The integrated cooperative model plays a positive significant role on performance of cooperatives in production, produce bulking, financial access and marketing functions among linked RPOs and SACCOs. The knowledge generated from this study will boost the integration efforts of linked cooperatives and encourage single cooperatives to upgrade to integrated model to tap the immense benefits to their stakeholders. Nevertheless, further studies should be conducted to investigate what fosters continued existence of single cooperatives, and the effect integration on other variables such as, returns to investment, profit maximization and competitiveness in liberalized markets to provide holistic information for decision making concerning sustainability and attractiveness of such cooperatives in the face of cut-throat competition from traders and middle men dealers in open markets.

CONFLICT OF INTERESTS

The author has not declared any conflict of interest.

ACKNOWLEDGEMENT

The author is grateful for the financial support given by the Canadian Cooperative Association through the International Development Research Corporation. The author also appreciates the cooperation and willingness of leaders of different cooperatives to participate in this study and the coordination role performed by the Uganda Cooperative Alliance.

REFERENCES

|

Abebe G K, Bijman J, Ruben R, Omta S, Tsegaye A (2010). The role of agricultural cooperatives in improving quality and reducing transaction costs in the Ethiopian potato chain. Paper presented at the Proceedings of the 9th Wageningen International Conference on Chain and Network Management (WICaNeM), Wageningen, The Netherlands, 26-28 May 2010. |

|

|

Adrian Jr JL, Green TW (2001). Agricultural Cooperative Managers and the Business Environment. Journal of Agribusiness 19(1):17-33. |

|

|

Ampaire EL, Machethe CL, Birach E (2013). The role of rural producer organizations in enhancing market participation of smallholder farmers in Uganda: Enabling and disabling factors. African Journal of Agricultural Research 8(11):963-970. doi: 10.5897/AJAR12.1732. http://www.academicjournals.org/AJAR |

|

|

Anastase B, Chambo S, Jaffe J, Javan S, Hanson C, Habiyameye G, Ketilson LH, Mchopa A, Mugisha J, Namwanje D, Nimusiima M (2016). Examining Success Factors for Sustainable Rural Development through the Integrated Co-operative Model: International Development Research Centre Final Research Report. |

|

|

Awoyemi BO, Jabar AA (2014). Prime lending rates and the performance of microfinance banks in Nigeria. European Journal of Business and Management, 6(12):131-136. |

|

|

Bazaara N (2001). Structural Adjustment Participatory Review Initiative (SAPRI) Uganda: impact of liberalization on agriculture and food security in Uganda. Research Report, Centre for Basic Research, Kampala. |

|

|

Bijman J (2010). Agricultural cooperatives and market orientation: A challenging combination. Market orientation: transforming food and agribusiness around the customer pp. 119-136. |

|

|

Cazzuffi C, Moradi A (2012). Membership Size and Cooperative Performance: Evidence from Ghanaian Cocoa Producers' Societies, 1930-36. Economic History of Developing Regions, 27(1):67-92. |

|

|

Chibanda M, Ortmann GF, Lyne MC (2009). Institutional and governance factors influencing the performance of selected smallholder agricultural cooperatives in KwaZulu-Natal. Agrekon 48(3):293-315. |

|

|

Desrochers M, Fischer KP (2005). The power of networks: integration and financial cooperative performance. Annals of public and cooperative economics 76(3):307-354. |

|

|

Fafchamps M, Hill RV (2005). Selling at the farm gate or traveling to market. American journal of agricultural economics 87(3):717-734. |

|

|

Fici A (2015). Cooperation among cooperatives in Italian and comparative law. Journal of Entrepreneurial and Organizational Diversity 4(2):64-97. |

|

|

Gashaw BA, Kibret SM (2018). Factors Influencing Farmers' Membership Preferences in Agricultural Cooperatives in Ethiopia. American Journal of Rural Development 6(3):94-103. |

|

|

Hammond KL, MacPherson I (2001). Aboriginal co-operatives in Canada: Case studies. Otawa: Research and Analysis Directorate, Indian and Northern Affairs Canada. |

|

|

Hendrikse G (2006). Challenges facing agricultural cooperatives: Heterogeneity and Consolidation. Proceedings "Schriften der Gesellschaft für Wirtschafts-und Sozialwissenschaften des Landbaues eV" 41(874-2017-845):31-41. |

|

|

Jones D, Kalmi P (2015). Membership and performance in Finnish financial cooperatives: a new view of cooperatives. Review of Social Economy 73(3):283-309. |

|

|

Kwapong AN (2012). Making rural services work for the poor: The role of Uganda's service reforms in marketing and agricultural extension. Humboldt-Universität zu Berlin. |

|

|

Kwapong AN, Hanisch M (2013). Cooperatives and poverty reduction: a literature review. Journal of Rural Cooperation 41(886-2016-64714):114-146. |

|

|

Kyriakopoulos K, Meulenberg M, Nilsson J (2004). The Impact of Cooperative Structure and Firm Culture on Market Orientation and Performance. Journal of Agribusiness 20(4):379-396. |

|

|

Lerman Z, Parliament C (1990). Comparative performance of cooperatives and investor?owned firms in US food industries. Agribusiness 6(6):527-540. |

|

|

Matthews-Njoku EC Ugochukwu AI, Ben-Chendo NG (2003). Performance evaluation of women farmer cooperative societies in Owerri agricultural zone of Imo State, Nigeria. Journal of Agriculture and Social Research 3(2):97-107. |

|

|

Orr A, Amede T, Tsusaka T, Tiba Z, Dejen A, Deneke TT, Phiri A (2017) . Smallholder Risk Management Solutions (SRMS) in Malawi and Ethiopia. |

|

|

Persson S (2010). Organisational Constraints in Rural Development: Causes of Different Performance among Ugandan Cooperatives. |

|

|

Soboh RA, Lansink AO, Giesen G, Van Dijk G (2009). Performance measurement of the agricultural marketing cooperatives: the gap between theory and practice. Review of Agricultural Economics, 31(3):446-469. |

|

|

Staatz JM (1994). A Comment on Phillips "Economic Nature of the Cooperative Association". Journal of Agricultural Cooperation 9(1141-2016-92524):80-85. |

|

|

Stata Corp (2015). Stata Statistical Software: Release 14. College Station, TX: StataCorp LP. |

|

|

Ton Z, Raman A (2010). The effect of product variety and inventory levels on retail store sales: A longitudinal study. Production and Operations Management 19(5):546-560. |

|

|

Verhofstadt E, Maertens M (2013). Cooperative membership and agricultural performance: Evidence from Rwanda (1067):2016-86824 |

|

|

Wambugu SN, Okello JJ, Nyikal RA, Bekele S (2009). Effect of social capital on performance of smallholder producer organizations: The case of groundnut growers in Western Kenya. |

|

|

Williams RC (2016). The cooperative movement: Globalization from below: Routledge. |

|

|

Wu SPJ, Straub DW, Liang TP (2015). How information technology governance mechanisms and strategic alignment influence organizational performance: Insights from a matched survey of business and IT managers. Mis Quarterly 39(2):497-518. |

|

|

Yamko Y (2008). The Organization of Project Financing and Management as a Needed Condition for the Intensification of Ukrainian-Polish Co-operation. Journal of International Studies 1(1). |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0