Full Length Research Paper

ABSTRACT

This paper aims to analyze the value relevance of financial statements prepared according to International Accounting Standards (IAS)/International Financial Reporting Standards (IFRS). The study focuses on two of the different sets of accounts presented by companies: the parent company financial statement and the consolidated version. We have developed a panel data from a sample of Italian listed companies by collecting accounting figures from consolidated and separate financial statements, since Italy mandates listed companies to prepare both reports according to IAS/IFRS. Using an Ohlson price model, we have tested our hypotheses, performing regressions of share price or market capitalization on book value and earning. Firstly, we compared the consolidated financial reports’ value relevance with that of the separate financial statements. The evidence suggests that, although the separate reports also have a high value relevance, this does not provide investors with additional information. Secondly, we investigated the value relevance of the consolidated financial statements alone, by focusing on the specific nature of the group’s equity book value and net income. Both are made up of two components: one referring to the parent company and the other attributable to non-controlling interests (NCI) as a consequence of the presence of minority shareholders within the group. We analyzed the value relevance of group financial statements, taking into account the presence/absence of minority shareholders and their portion of equity and net income. By dividing groups with minority shareholders from groups without these, we verified whether the presence of non-controlling interests can affect the value relevance of consolidated reports, and whether NCI equity and net income are value-relevant. In fact, all modes used to test value relevance are based only on the parent company equity and net income, leaving aside that group equity and net income are divided into two parts. The evidence suggests that NCI financial values slightly increase the fit of the model, and that NCI equity and net income are statistically significant in affecting the market capitalization of companies.

Key words: International Accounting Standards (IAS)/International Financial Reporting Standards (IFRS), value relevance, equity, accounting.

INTRODUCTION

Value relevance is one of the most important attributes of accounting quality (Francis et al., 2004), since investors rely on accounting information for their investment decisions. Given that the main purpose of accounting reports is to provide reliable information regarding the financial position, performance and cash flow of the reporting entity, value relevance determines whether accounting numbers are useful to financial statement users in making their choices.

The objective of financial statements for general purposes is also highlighted by the International Accounting Standards (IAS)/International Financial Reporting Standards (IFRS) framework (in addition to that of FASB), which states, among other qualitative characteristics of financial information, that “the objective of general purpose financial reporting is to provide financial information about the reporting entity that is useful to existing and potential investors…” and “decisions by existing and potential investors about buying, selling or holding equity and debt instruments depend on the returns that they expect from an investment in those instruments, for example dividends, principal and interest payments or market price increases” (The Conceptual Framework for Financial Reporting, OB2 and OB3).

Empirically, research on value relevance has found a fertile environment in the capital market and in publicly available financial statements. In fact, many models used to test for value relevance assume share price as a measure of investors’ decisions (Francis and Schipper, 1999) and accounting values from annual reports as a proxy for financial information. According to the authors, value relevance of financial statements exists when there is a statistical correlation or association between prices or returns and specific financial information. The value relevance studies carried out in this research stream are based on the financial figures reported in annual reports, such as equity book value and net income. These values are then matched with stock prices to analyze the ability of financial reports to capture or summarize information that influences share prices. Almost all analyses developed in this direction have considered the market value or the share price of listed companies and their publicly available financial statements as the source of accounting figures. Although many studies seem to ignore this, it is important to reinforce that the financial statements taken as the source of data are prepared on a consolidated basis.

Two main reasons drive this approach. First, consolidated reports are the actual financial statements of the economic entity. Second, in most countries, particularly for non-listed companies, only consolidated financial statements are publicly available, therefore all research is carried out on consolidated data. In the European Union, listed companies’ financial statements are addressed by Regulation 1606/2002 that mandates IFRS for consolidated reports and introduces a member state option to apply IFRS to other entities and to separate financial statements. In relation to this, few countries have adopted IFRS for separate financial statements and, among the main European economies, only Italy has done it.

IFRS adoption for separate financial statements has been fiercely debated. In fact, in many countries, the tax laws are so closely linked to domestic generally accepted accounting principles (GAAP) that the adoption of IFRS for separate reports would been very burdensome for companies (Choi and Mueller, 1992; Delvaille et al., 2005; Lamb et al., 1998; Macías and Muiño, 2011; Nobes, 1998; Oliveras and Puig, 2005; Whittington, 2005).

There are also obstacles to the preparation of a separate financial statement according to IFRS, since they are primarily viewed as being for consolidated reports. In 2015, The European Financial Reporting Advisory Group (EFRAG) developed a project to consider how financial statements (other than consolidated financial statements) are used in Europe for economic decision-making and analyzing the technical financial reporting issues that arise when preparing such financial statements under IFRS. Respondents to the discussion paper have agreed that it would be useful if the IASB reviewed existing requirements, with a view to developing a specific set of general principles for separate financial statements.

The purpose of this paper is to investigate the value relevance of Italian financial reports prepared according to IFRS by considering both sets of publicly available accounts. The analysis firstly aims to measure the value relevance of both separate and consolidated financial statements when prepared according to the same GAAPs. Second, this study evaluates which set of accounts might be more useful in making investment choices. Thirdly, we investigate the relevance of accounting figures related to minority interests.

The contribution made by this paper is innovative because of the limited adoption of IFRS in separate reports: only a few studies address this issue. Moreover, no studies have dealt with the NCI portion of equity and net income reported in consolidated financial statements.

LITERATURE REVIEW

There are few studies that deal with the value relevance of separate financial statements in absolute terms or compare these with consolidated reports. The international literature related to separate reports neglects U.S. studies due to the lack of public availability of parent companies’ reports, whilst more comparative analyses have been carried out in particular after the adoption of IAS/IFRS by European listed companies for their consolidated financial statements, and in some cases, also for separate statements.

Evidence discovered by scholars suggests that group reports are more value relevant than parent company accounts, even though these results are weak or limited. Darrough and Harris (1991) developed a research project on Japanese firms and the effects of consolidation on financial statements. Even though the results show a small incremental value relevance concerning consolidated data, the specific institutional environment of Japan and the inter-firm ownership relationship make the findings not generally applicable.

Some scholars (Abad et al., 2000; Harris et al., 1994; Niskanen et al., 1998) claim the superior value relevance of consolidated financial statements, while others (Goncharov et al., 2009; Niskanen et al., 1998) affirm that parent companies’ financial statements do not show incremental value relevance. According to several authors, the lower value relevance of single accounts is due to companies preparing and using their reports for a range of taxation or regulation purposes (Choi and Mueller, 1992; Delvaille et al., 2005; Lamb et al., 1998; Macías and Muiño, 2011; Nobes, 1998; Oliveras and Puig, 2005). This use of separate financial statements as the basis for tax computation has also been verified by some scholars (Nobes, 2004; Pfaff and Schröer, 1996) who have observed that it might vary between countries and time periods, and that it depends on the role given to financial statements by policymakers.

In contrast, a broad range of literature related to the value relevance of consolidated financial statements developed following the adoption of IFRS by European listed companies. Empirical research on value relevance has found a fertile environment for study after the mandatory adoption of IFRS by listed companies in the European Union. Since the first adoption of IFRS regarding the preparation of consolidated financial statements, in 2005, most studies have concentrated on the value relevance of group accounts prepared according to the new standards. Additionally, within this recent research stream, the results are not straightforward or unequivocal.

Two authors (Aubert and Grudnitski, 2011) carried out research on 13 European countries and 20 industries, examining the effects of the first adoption of IFRS. Their findings failed to prove that consolidated reports have had incremental value relevance after the adoption of IFRS. Other scholars (Daske et al., 2008) analyzed IFRS adoption in 26 countries worldwide and found modest, although statistically significant, capital market benefits related to the introduction of mandatory IFRS reporting. However, these benefits occurred only in countries with strict enforcement regimes and where firms were given inducements to encourage transparency. The importances of enforcement regimes and reporting incentives on the effects, subsequent to the mandatory adoption of IFRS, have also been highlighted by Barth et al. (2012), Byard et al. (2011) and Horton et al. (2013).

In addition to these cross-country studies, some analyses have been developed in relation to the individual country effects of IFRS adoption. Callao et al. (2007) carried out an analysis on IFRS adoption by Spanish listed companies and did not identify any incremental value relevance for financial statements prepared according to the new standards when compared with the previously adopted local GAAPs. The UK stock market has been investigated by Horton et al. (2013); this analysis evidenced diminishing forecast errors for firms adopting mandatory IFRS. Christensen, Lee, & Walker (2007)also examined the mandatory adoption of IFRS for the UK and concluded that the resultant benefits do not affect firms in a unique way.

Gjerde et al. (2008) found mixed results for Norwegian listed companies, investigating the effects of changes in accounting figures from local GAAPs to IFRS. The value relevance of key accounting figures in IFRS financial statements is not superior to the corresponding figures presented in NGAAP reports when these are evaluated unconditionally and conservatively as two independent samples. On the contrary, IFRS are marginally more value-relevant than NGAAP only for some firms with a high degree of intangibles. In the Greek context, Iatridis and Rouvolis (2010) found evidence that the transition to IFRS provided more value-relevant accounting figures.

Beyond such studies about the value relevance of IFRS financial statements, there are only a few analyses directly referring to separate financial statements. Harris et al. (1994) produced a comparison of the value relevance of accounting measures between U.S. and German firms within similar industries and of comparable size, concluding that the explanatory power of accounting numbers increases at the level of consolidation: unconsolidated data evidence has lower value relevance when compared with the data for separate accounting.

Abad et al. (2000) compared, in terms of value relevance, the consolidated financial statements of Spanish listed companies with the parent companies’ separate reports and concluded that group accounts were more value relevant than individual accounts. Goncharov et al. (2009) extended their analysis to different functions of sets of accounts prepared by holding companies in Germany and did not find that single accounts provided more useful information. On the contrary, they verified that the role of providing useful information is better fulfilled by group accounts.

METHODOLOGY

Ohlson model

The main objective of this paper is to investigate the value relevance of separate and consolidated financial statements of Italian listed companies. To provide a clear indication of financial statements and their value relevance, the paper defines value relevance, specifies the significance of consolidated financial statements, describes a widespread and well-known value relevance model, provides details on the data for the regression analysis and documents the empirical results.

Employing a definition of value relevance as the ability of financial statement information to capture or summarize information that affects share value (Hellström, 2006), studies of this issue have tested it empirically, calculating the statistical association between market value and accounting figures. In a nutshell, value relevance research tries to measure to what extent accounting information might be useful to readers of financial statements when making investment decisions; consequently, an amount is defined as value-relevant if it is significantly associated with share prices (Barth et al., 2001).

Among some models developed to test for value relevance, the Ohlson model (OM) is one of the most successful research schemes from recent decades. Even though this model was initially conceived for a different purpose, it has been adapted to fit with value relevance analyses. According to the OM, the market value of the company is a linear function of the level of capital invested in the company, the abnormal results generated by the company and variables other than the financial information. The main advantage of the model is that it defines a solid conceptual framework, according to which the market value of the company is in a relationship with the past and the future financial information of the company. In accounting terms, the market value of a company is related to current and future expected net income, or to the book value of equity or to dividends. The original version of the model expresses firm value as a linear function of the book value of equity and the present value of expected future abnormal earnings. It assumes a strong hypothesis as to the existence of perfect capital markets, but with additional assumptions it can re-express the firm value as a linear function of equity book value, net income, dividends and other information (Feltham and Ohlson, 1995; Feltham and Ohlson, 1996).

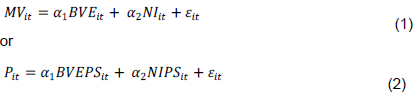

We have utilized an Ohlson modified price model, in which two major items from financial accounts (balance sheet and income statement) are used to test the value relevance of consolidated financial statements. Moving on from the original assumption of the model, we have adopted an extension that allows us to explore the relationships between equity market value and two main financial accounting figures. The equation used in the OM identifies market capitalization as a proxy of the market value of a firm, whilst the equity book value and the net income are assumed as proxies for the financial information supplied by financial statements. To avoid a scale effect due to the presence of firms with significant differences in terms of financial numbers, we also considered variables on a per-share basis. Consequently, the OM used in our analysis assumes these forms:

Where:

ð‘€ð‘‰ð‘–ð‘¡ is the market value of firm i at time t (fiscal year-end) and is designed as the dependent variable in model (1);

Pit is the share-price of firm i at time t (fiscal year-end) and is designed as the dependent variable in model (2);

ðµð‘‰Eð‘–ð‘¡ is the book value of the equity of firm i at year t; this is the first independent variable in model (1);

NIð‘–ð‘¡ is the reported net income of firm i at time t; this is the second independent variable in model (1);

ðµð‘‰Eð‘ƒð‘†ð‘–ð‘¡ is the book value of equity per share of firm i at year t; this is the first independent variable in model (2);

ð¸ð‘ƒð‘†ð‘–ð‘¡ is the reported accounting earnings of firm i at time t; this is the second independent variable in model (2);

εit is the residual value (error term) for company i in year t.

Using these two versions of OM, we applied and adapted them to consider the main features of the two sets of accounts we considered in our analyses: consolidated financial statements and parent companies’ separate annual reports. Applying OM on consolidated or individual accounting numbers differs, above all, in relation to the independent variables assumed as the proxies of the equity and net income of the firm/group.

Independent variables

In many implemented regression models based on Ohlson theory, independent variables, or regressors, are accounting numbers such as equity book value and net income reported in various sets of accounts presented by firms. We have followed this approach, but we have also introduced some changes in order to adapt the price models to the specific features of consolidated and separate financial statements and to the specific components of group equity and net income.

By gathering data from consolidated financial statements, we were able to observe how different values compose the group equity and net income. For both the equity and net income reported in consolidated accounts, we can distinguish the part attributable to the parent company and that attributable to the non-controlling interests, if they exist. In fact, almost all studies on value relevance assume, as independent variables, consolidated numbers attributable only to the parent company, such as parent company shareholders’ equity and net income/profit, and often these are considered on per-share base, to avoid scale effects.

In contrast, when defining independent variables, we have taken into account the real role of group accounts. Consolidated reports are the actual financial statements of an economic entity and it is evident within the modern economy that the most important firms have a group pattern created by a parent undertaking and its subsidiaries. Even though the parent company and its subsidiaries are legally and formally independent, they are still a single economic entity. Moreover, a subsidiary can be partially owned, resulting in the presence of non-controlling interests to be recognized on the balance sheet and in the income statement. Since non-controlling interests are relevant values within the group equity and net income, we have decided to consider this issue in our analysis. We have taken into consideration the assuming, as independent variables, of equity book value and net income attributable to non-controlling interests (NCI) other than those of the parent company. In other words, we have added – in our regression model – figures related to NCI.

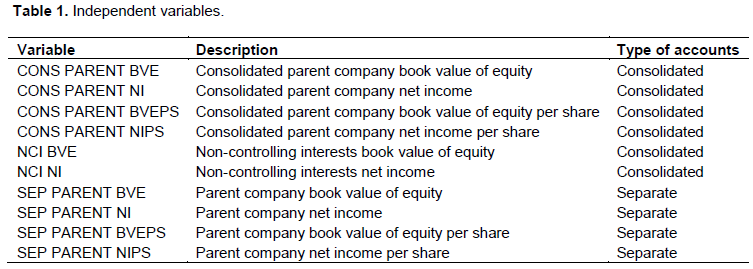

Unfortunately, in operationalizing the accounting values related to NCI, we encountered some obstacles. Because of the assumption of values on per-share base, we would have to do the same for NCI, which would have required a large amount of information. In fact, the amount of NCI recognized in the income statement and in the balance sheet is made up of the sum of single NCI related to each subsidiary controlled directly or indirectly by the parent, after eliminations for intra-group transactions. Hence, we should have discomposed NCI into as many components as the number of subsidiaries and expressed these on a per-share base. Due to these issues, we have considered the variables representing NCI in their total amount, and consequently only in model (1). Therefore, in our models, we have considered the following independent variables.

The consolidated parent company book value of equity (CONS PARENT BVE) represents a measure of the group equity attributable to the parent, often referred to as “Parent company shareholder equity” or “Equity attributable to the shareholders of a parent company”. The consolidated parent company net income (CONS PARENT NI) functions as an indicator of company profitability. These two variables are used in almost all studies based on price models and can also be expressed on a per-share basis.

The non-controlling interests book value of equity (NCI BVE) and net income (NCI NI) are the share of group equity and net profit attributable to shareholders that do not control the subsidiaries. Whilst these four variables are collected directly from consolidated financial statements, in separate financial reports we have found equity (SEP PARENT BVE) and net income (SEP PARENT NI) from the parent company. In addition, these variables can be easily expressed on per-share basis. The following table summarizes the labels, descriptions and account type of all the independent variables used in our analysis (Table 1).

Dependent variables

In this study, we have assumed dependent variables or regress and values that are expressions of a firm’s or a share market price. Many studies assume market capitalization or share price as dependent variables. To test for the relationship between share price or market value and particular accounting values, we looked for a dependent value that could reflect the effects of accounting information on investors’ choices. Whereas share price or market capitalization are a good value to represent these, we have assumed as dependent variables the share price (P) and the market capitalization (MKT CAP) four months after the end of the fiscal period. In our sample, we collected the share price of firms reported up to April 31st. For many companies, the fiscal year end occurs on December 31st, so in our opinion four months is a fair period for observing the effects of accounting information on investors’ choices. Moreover, to produce a deeper analysis, we collected, for each firm within the sample, the share price on 31st April for four years, from 2012 to 2015, and accounting numbers from the 2011 to 2014 financial statements.

Sample selection and data sources

By gathering quantitative data from annual reports prepared by Italian listed groups, we have developed a proprietary database composed of secondary data and consistent with the purpose of our survey. In preparing this, we have taken into account the annual reports from listed companies on the Italian Stock Exchange, since IAS/IFRS have been compulsory since 2005 for the preparation of consolidated financial statement, and since 2006 for the preparation of parent company statements. AIDA – a Bureau van Dijk database on Italian firms – has been used to collect data on 301 listed companies preparing separate and consolidated financial statements according to IAS/IFRS. Beginning from this initial sample, we have made several refinements in order to obtain a complete and homogeneous database with no missing data from the 2012 to 2015 financial statements. Initially, we excluded banks and assurance companies due to their specific industry and reporting activity, companies for which data was not available over the entire period because of delisting or unusual operations and companies with a fiscal year not beginning on January 1st. Thus, we have built a database from companies with available financial data over the period 2012 to 2015, with the share price available and market capitalization at the end of April for 2013 to 2016. As a result of these refinements, our database is strongly balanced and constitutes 144 companies presenting consolidated and financial statements with their fiscal year beginning on January 1st, incorporating 576 total observations.

Hypotheses development

Our empirical analysis is based on regression models used to test different hypotheses related to the value relevance of financial reports. To test these hypotheses, we ran ordinary least square (OLS) regressions using STATA 13.

H1: Information supplied by consolidated financial statements is value relevant.

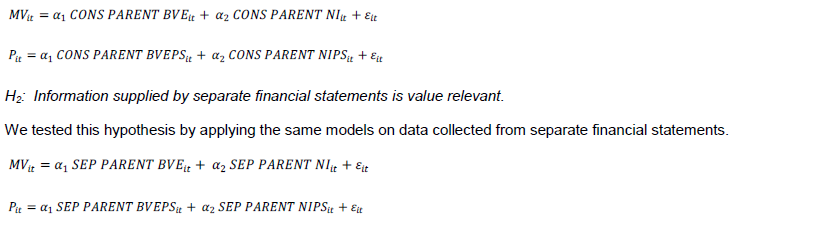

Naturally, for this development, we considered the empirical results of previous research that supports the thesis of consolidated financial statement relevance (Harris et al., 1994; Niskanen et al., 1998; Abad et al., 2000; Goncharov et al., 2009) and took into account the role of consolidated financial statements. Since group accounts are the actual accounts of an entity structured on a group pattern, we expected that consolidated financial statements would better provide useful financial information. Moving on from the basic models presented earlier, we applied these to consolidated data:

H3: Value relevance of consolidated financial statements is higher than separate financial reports.

By comparing the empirical results relating to H1 and H2, we were able to evaluate the different value relevance of group and parent company accounts.

H4: Accounting amounts related to NCI equity and net income are value relevant.

We tested this hypothesis by adding NCI-related variables to basic model (1) and by running regression on the consolidated data of groups with minority shareholders.

REGRESSION ANALYSIS AND DISCUSSION OF FINDINGS

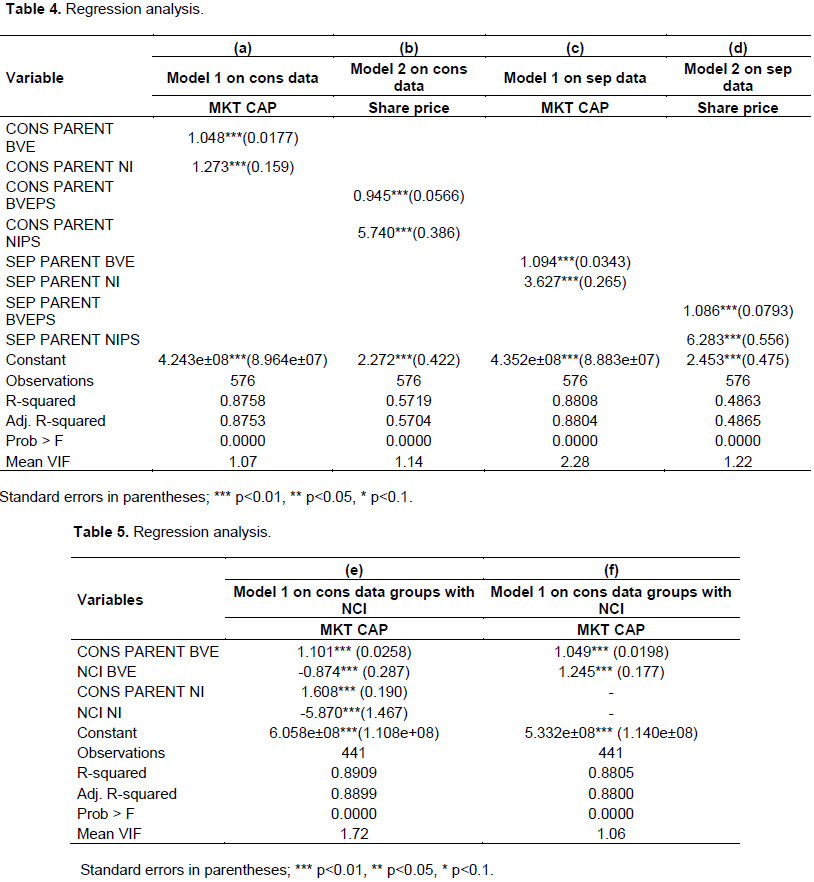

Tables 2 and 3 show some preliminary data about descriptive statistics and correlations. In relation to the existing associations between the variables employed in the econometric model, we observe that there are strong correlations between the independent variables (market capitalization and share price) and the explanatory variables. The correlation is slightly higher when the explanatory variables are reported from consolidated financial statements, which suggests that consolidated numbers have a higher explanatory power than those of the parent company.

The analysis of correlations also evidences a strong association between the dependent variables used in the model, possibly indicating multicollinearity between variables. This issue is common to empirical studies concerning value relevance (Abad et al., 2000; Collins et al., 1997). However, the variance inflation factor (VIF) of regressors is close to 1 and below the rule of thumb 4, making further investigation necessary. When it exceeds 10, this is a sign of serious multicollinearity requiring correction. Table 4 summarizes the results of regressions of model 1 and 2 run on consolidated and separate data in order to test hypotheses 1 and 2. Table 5 summarizes the results of regressions of model 1 on companies with and without non-controlling interest.

The results from the regressions run on consolidated separate and parent company data clearly verify H1 and H2. In the regressions with consolidated numbers only (regressions a and b) all the coefficients are statistically significant at the 1% level (p-value < 0.01) and the R2 is 0.8758 for regression on market capitalization and 0.5719 for regression on share price. The p-value for the F-test for overall significance confirms that the model offers a good fit. These conclusions are also valid for regressions run on separate data, where R2 is 0.8808 for regression on market capitalization and 0.4863 for regression on share price. The statistical significance of the variables coefficients, the amount of variance explained (R2) and the general suitability of the models tested (F-test) suggest to us that both consolidated and separate financial statements prepared according to IAS/IFRS are value relevant and verify H0 and H1. As predicted, the coefficients of equity and net income are strongly significant and positively associated with firm market value. Net income always has a higher coefficient than equity and this suggests that investors rely more on a company’s profit than its capital.

These findings also evidence differences in value relevance beetween consolidated and separate financial statements, confirming H3. While there are no significant differences in value relevance when regressions are developed on market capitalization (difference in R2 is 0.005), analysis carried out by measuring the degree of association between share price and equity and net income per share demonstrates that consolidated financial statements (R2 = 0.5719) are more value relevant than separate statements (R2 = 0.4863).

Interesting findings have been achieved by means of regressions on consolidated data that consider the existence of non-controlling interests and their portion equity and net income reported in consolidated accounts. Regression analysis evidences the statistical significance of variables (p-value < 0.01) and the appropriateness of all the models tested. This also introduces some novelties concerning accounting numbers that can be associated with investors’ choices. We ran a regression (e) on the consolidated data of groups with NCI, assuming as independent variables the share of equity and net income owned by minority shareholders in addition to the consolidated equity and net income of the parent. In a second regression (f), we removed the variables related to NCI in order to verify the effect of this omission on testing for value relevance.

The study findings suggest that NCI equity (coeff. = -0.874) and net income (coeff. = -5.870) are statistically significant at 0.01 level (p-value < 0.01) and are negatively associated with the regressand. The addition of these variables increases the explanatory power of the basic model (1). In fact, model (1) applied to parent company values evidences only R2 = 0.8805, while the same model with two additional variables shows R2 = 0.8909). This suggests that H4 has been verified. We can also claim that NCI equity and net income are negatively associated with share prices and market capitalization because they are considered by investors as claims on their ownership interests.

CONCLUSIONS

In this study, we investigated the value relevance of financial statements prepared by a cluster of Italian listed companies. Using econometric models, we tested how the financial information reported in annual reports is useful for investors in making decisions. Since Italian listed companies prepare both consolidated and separate financial statements according to IAS/IFRS, we tested the value relevance of these two sets of accounts in order to evaluate whether the parent company annual report could provide useful information to investors. As expected, consolidated and individual financial statements resulted in value relevance and our findings have demonstrated a certain superiority of group accounts when compared with parent company reports. These findings are consistent with previous literature about value relevance and introduce new evidence that parent company accounts are value relevant, in addition to as group accounts.

While most previous studies have dealt with parent company group and net income only, we decided to also investigate the NCI share of capital and profit as reported in the consolidated financial statements. As long as these values are measures of group capitalization and profitability for minority shareholders, how they affect value relevance of consolidated financial statements according to parent company perspective. As expected, our findings suggest that NCI equity and net income are statistically relevant and negatively associated with assessing firm market value. This conclusion is coherent with the role of NCI within a group, since they are constraints for the parent company.

Although these results confirm our expectations in terms of value relevance and the significance of NCI, it is vital to address the potential limitations and future developments of the study. We have based our analysis on Italian listed companies, for the aforementioned reasons, and the sample could be extended in order to increase its representativeness. For example, other European countries that have made IAS/IFRS mandatory for parent companies’ accounts could be included in the sample. Moreover, our study has been conducted from a controlling shareholding perspective, since most studies on value relevance deal only with the investors point of view. However, there are other potential perspectives to be analyzed; for example, creditors, financial institutions and minority shareholders might be studied. Finally, future studies could adopt nonlinear regression models or logarithmic or returns models.

CONFLICT OF INTERESTS

The author has not declared any conflict of interests.

REFERENCES

|

Abad C, Laffarga J, García-Borbolla A, Larrán M, Pi-ero JM, Garrod N (2000). An evaluation of the value relevance of consolidated versus unconsolidated accounting information: Evidence from quoted Spanish firms. Journal of International Financial Management and Accounting 11(3):156-177. |

|

|

Aubert F, Grudnitski G (2011). The impact and importance of mandatory adoption of international financial reporting standards in Europe. Journal of International Financial Management and Accounting 22(1):1-26. |

|

|

Barth ME, Beaver WH, Landsman WR (2001). The relevance of the value relevance literature for financial accounting standard setting: another view. Journal of Accounting and Economics 31(1-3):77-104. |

|

|

Barth ME, Landsman WR, Lang M, Williams C (2012). Are IFRS-based and US GAAP-based accounting amounts comparable? Journal of Accounting and Economics 54(1):68-93. |

|

|

Byard D, Li Y, Yu Y (2011). The Effect of Mandatory IFRS Adoption on Financial Analysts' Information Environment. Journal of Accounting Research 49(1):69-96. |

|

|

Callao S, Jarne JI, Laínez JA (2007). Adoption of IFRS in Spain: Effect on the comparability and relevance of financial reporting. Journal of International Accounting, Auditing and Taxation 16(2):148-178. |

|

|

Choi FDS, Mueller GG (1992). International accounting. Prentice-Hall. |

|

|

Christensen HB, Lee E, Walker M (2007). Cross-sectional variation in the economic consequences of international accounting harmonization: The case of mandatory IFRS adoption in the UK. International Journal of Accounting 42(4):341-379. |

|

|

Collins DW, Maydew EL, Weiss IS (1997). Changes in the value-relevance of earnings and book values over the past forty years. Journal of Accounting and Economics 24(1):39-67. |

|

|

Darrough MN, Harris TS (1991). Do Management Forecasts of Earnings Affect Stock Prices in Japan? Accounting and Financial Globalization, 119–154. |

|

|

Daske H, Hail L, Leuz C, Verdi R (2008). Mandatory IFRS reporting around the world: Early evidence on the economic consequences. Journal of Accounting Research 46(5):1085-1142. |

|

|

Delvaille P, Ebbers G, Saccon C (2005). International Financial Reporting Convergence: Evidence from Three Continental European Countries. Accounting in Europe 2(1):137-164. |

|

|

Feltham GA, Ohlson JA (1995). Valuation and Clean Surplus Accounting for Operating and Financial Activities. Contemporary Accounting Research 11(2):689-731. |

|

|

Feltham GA, Ohlson JA (1996). Uncertainty Resolution and the Theory of Depreciation Measurement. Journal of Accounting Research 34(2):209-234. |

|

|

Francis J, LaFond R, Olsson PM, Schipper K (2004). Costs of equity and earnings attributes. Accounting Review 79(4):967-1010. |

|

|

Francis J, Schipper K (1999). Have Financial Statements Lost Their Relevance? Journal of Accounting Research 37(2):319-352. |

|

|

Gjerde Ø, Knivsflå K, Sættem F (2008). The value-relevance of adopting IFRS: Evidence from 145 NGAAP restatements. Journal of International Accounting, Auditing and Taxation 17(2):92-112. |

|

|

Goncharov I, Werner JR, Zimmermann J (2009). Legislative demands and economic realities: Company and group accounts compared. International Journal of Accounting 44(4):334-362. |

|

|

Harris TS, Lang M, Moller HP (1994). The Value Relevance of German Accounting Measures: An Empirical Analysis. Journal of Accounting Research 32(2):187-209. |

|

|

Hellström K (2006). The Value Relevance of Financial Accounting Information in a Transition Economy: The Case of the Czech Republic. European Accounting Review 15(3):325-349. |

|

|

Horton J, Serafeim G, Serafeim I (2013). Does mandatory IFRS adoption improve the information environment? Contemporary Accounting Research 30(1):388-423. |

|

|

Iatridis G, Rouvolis S (2010). The post-adoption effects of the implementation of International Financial Reporting Standards in Greece. Journal of International Accounting, Auditing and Taxation 19(1):55-65. |

|

|

Lamb M, Nobes C, Roberts A (1998). International Variations in the Connection Between Tax and Financial Reporting. Accounting and Business Research 28(3):173-188. |

|

|

Macías M, Mui-o F (2011). Examining dual accounting systems in Europe. International Journal of Accounting 46(1):51-78. |

|

|

Niskanen J, Kinnunen J, Kasanen E (1998). A note on the information content of parent company versus consolidated earnings in Finland. European Accounting Review 7(1):31-40. |

|

|

Nobes C (1998). Towards a general model of the reasons for international differences in financial reporting. Abacus 34(2):162-187. |

|

|

Nobes CW (2004). A Conceptual Framework for the Taxable Income of Businesses, and How to Apply it under IFRS. Report. Association of Charted Certified Accountants, P 74. |

|

|

Oliveras E, Puig X (2005). The Changing Relationship between Tax and Financial Reporting in Spain: EBSCOhost. Accounting in Europe 2(1997):195-207. |

|

|

Pfaff D, Schröer T (1996). The relationship between financial and tax accounting in Germany-the authoritativeness and reverse authoritativeness principle. European Accounting Review 5(sup1):963-979. |

|

|

Whittington G (2005). The adoption of International Accounting Standards in the European Union. European Accounting Review 14(1):127-153. |

|

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0