Cross border trade involves a greater number of female than male entrepreneurs, thus promoting the empowerment of women in the Southern Africa Development Community. Most of the women cross-border traders are aged between 25 and 35 years. This trade has been going on for several years but under very difficult circumstances (Peberdy, 2000).

The role that SMEs play worldwide

Small business sector is a major source of job creation (Schreyer, 1996). MSEs have a propensity to employ more labour intensive production processes than large enterprises. Consequently, they contribute significantly to the provision of productive employment opportunities, generation of income and equality and the reduction of poverty (Kongolo, 2010).

There is growing recognition of the important role that the small and medium scale enterprises (SMEs) play in economic development. They are often described as efficient and prolific job creators, the seeds for big businesses and the fuel of national economic engines. Even in the developed industrial economies, the SMEs sector is the largest employer of people. Interestingly, the role of SMEs in the development process continues to be in the forefront of policy debates in the country. Governments at all levels have undertaken initiatives to promote the growth of SMEs. More generally, the development of SMEs is seen as accelerating the achievement of wider socio-economic objectives, including poverty alleviation. Thus, governments throughout the world focus on the development of the SMEs sector to promote economic growth.

It is therefore imperative that governments need to pay increased attention to the SMEs and try to create a business environment that will be beneficial to SMEs development. The lack of skills, lack of credit facilities in general and export credit in particular, and as most credit requires collateral this also limits if not prevents access to finance, lack of information on export markets, lack of technology to produce quality goods and achieve high productivity (MSME, 2012).

Collateral are the assets that are pledged by a borrower to a lender as a security for the re-payment of debt. Collateral requirement is seen as an obstacle to SME’s growth. Lack of collateral is ranked as obstacle number two from lack of finance. The lack of collateral is probably the most widely cited obstacle encountered by MSEs accessing finance (Kihimbo et al., 2012). The enterprise may be unable to provide sufficient collateral because it is too new or is not firmly enough established (Olawale and Garwe, 2010).

Lending to MSEs is seen as high-risk business since most of these enterprises lack collateral. The problem does not appear to be lack of funds but rather how to make them accessible to MSEs (Kihimbo et al., 2012). There are institutions such as banks and non-bank financial institutions that are willing to provide funds to MSEs but are not able to meet the requirements of these financial institutions and among these requirements is the issue of collateral, which most MSEs cannot provide (Ackah and Vulvor, 2011).

The demand for collateral by banks and other financial institutions stifle the growth of MSEs (Kunateh, 2009). Lending to MSEs is more likely to be based on collateral than is the case for loans for large firms. This may lead to situations in which lending is not based on expected return but rather upon access to collateral. Many MSEs lacking access to ‘good collateral’ suffer from credit rationing (Nonso, 2013).

Collateral matters because of three essential features of formal credit markets. First, borrowers face requirements for collateral in the formal financial sector of most countries, regardless of the size of the economy. It is argued that loans secured by collateral have more favorable terms than unsecured loans do, for any given borrower or size of the loan. A borrower who is able to offer collateral can obtain a larger loan relative to the borrower’s income, with a larger payment period and a lower interest rate. Conversely, a borrower who cannot provide the type of assets lenders require as collateral often gets worse loan terms than an otherwise similar borrower who can do so, or gets no loan at all. Secondly, it is argued that in most low- and middle-income countries, most firms receive none of the benefits of collateral despite having a wide array of productive assets because their assets cannot serve as collateral. This limitation arises entirely from the legal framework for secured transactions. It can, therefore, be concluded that secured loans are the most common loans in the formal financial sector. In low- and middle-income countries, between 70% and 80% of firms applying for a loan are required to pledge some form of collateral (Fleisig et al., 2006).

In Kenya, there are many MSEs which despite their high potential have been unable to access financing from existing institution in the financial sector. Such situations may be due to the inability of the MSE to offer sufficient loan collateral. In a study in four East Africa countries it was established that 94% of the banks in the sample demanded collateral from their MSE borrowers. They found that collateral requirements for MSE loans are higher than consumer loans because SMEs’ credit risk is usually more difficult to evaluate. Informality of MSEs came out as the main reason why banks in the region require that MSEs in the region lodge security relative to corporate clients.

Despite the potential role of SMEs in accelerating economic growth and job creation in developing countries, a number of bottlenecks affect their ability to realize their full potential. SME development is hampered by a number of factors including finance, lack of managerial skills, equipment and technology, regulatory issues, and access to international markets. The lack of managerial know-how places significant constraints on SME development. Even though SMEs tend to attract motivated managers, they can hardly compete with larger firms. The scarcity of management talent prevalent in most countries in the region has a magnified impact on SMEs (Aryeetey, 1994). The lack of support services or their relatively higher unit cost can hamper SMEs’ efforts to improve their management because consulting firms are often not equipped with appropriate cost-effective management solutions for SMEs. Besides, despite the numerous institutions providing training and advisory services, there is still a skills gap in the SME sector as a whole (Dalitso and Peter, 2000). This is because entrepreneurs cannot afford the high cost of training and advisory services while others do not see the need to upgrade their skills due to complacency. In terms of technology, SMEs often have difficulties in gaining access to appropriate technologies and information on available techniques (Aryeetey, 1994). In most cases, SMEs utilize foreign technology with a scarce percentage of shared ownership or leasing. They usually acquire foreign licenses because local patents are difficult to obtain.

An analysis of survey and research results of SMEs in South Africa, for instance, reveals common reactions from SME owners interviewed. When asked what they perceive as constraints in their businesses and especially in establishing or expanding their businesses, they answered that access to funds is a major constraint. This is reflected in perception questions answered by SME owners in many surveys (Gockel and Akoena, 2002). This situation is not different in the case of Malawi according to survey done by Finscope (MSME, 2012).

The role that cross-border SME’S play

Cross border traders supported on average 3.2 children as well as 3.1 dependents who were not children or spouses (Peberdy and Rogerson, 2000). Informal cross-border traders are playing an important role in the circulation of goods from areas with excess supplies to those deficit areas. In this period, informal cross-border traders serving rural areas provided agriculture inputs and industrial consumer goods to farmers and contributed in the commercialization of the farmer’s produce (Justice, 2010).

Challenges that cross-border SME’s face

Despite their significant contributions, Informal Cross Border Traders (ICBT) faces significant constraints when doing business. Women ICBTs in particular still suffer stigmatization, violence, harassment, poor working conditions and lack of recognition of their economic contribution. Some of the challenges identified by the UNIFEM 2007–2009 research include cumbersome border processes, bribery and corruption at border posts, lack of policy recognition of ICBTs at national and regional levels, weak organization of ICBTs at national and regional levels, poor dissemination of information on the SADC trade protocol and other customs rules and regulations, poor infrastructure at border posts, ranging from lack of clean toilets to lack of storage space; import restrictions, sexual coercion in some places, vulnerability to HIV and AIDS, inability to meet certain health, sanitary, and environmental requirements, harassment of women ICBTs, including unwarranted impounding of goods and humiliating body searches, and excessive, arbitrary, or inconsistent customs charges, often as part of bribe-seeking. There is also the danger entailed in using risky informal border crossing points, including wild animal corridors, as found by researchers in Botswana (Blumberg, Meyers and Malaba, 2016).

Despite the growth of intraregional and total trade in the region, opportunities for expansion of trade through greater integration in COMESA and SADC appear limited since product complementarities and levels of intraregional trade are low, and there is a risk of polarization. Factors that hinder African trade include distorted trade regimes, high transaction costs due to high transportation costs, as in the case of Malawi, inadequate information and communication infrastructure, lack of political will, policy reversals, difficulties in implementing harmonization provisions, multiple and conflicting objectives of overlapping regional arrangements and limited human capacity (UNCTAD, 2006).

The lack of convergence in SADC Member States’ external tariff and trade policies is also a threat to mutual cooperation and becomes unnecessarily unwieldy for informal cross border traders. What further complicates the situation is the fact that most SADC countries belong to more than one regional trade block. SADC countries are members of five overlapping economic groups that include SADC, COMESA, East African Community (EAC), Southern African Customs Union (SACU) and Indian Ocean Community (IOC). These regional trade blocs do not necessarily have similar aims and their over-lapping membership makes life difficult for informal cross border traders who would prefer harmonization in the trading regime (Makombe, 2011). Many border officials ask for bribes to make a smooth clearance. If the trader does not pay, it will cost a lot and may take several extra days to cross the border. The cases are reported to the authorities but the authorities ask for receipts. Of course, nobody gives receipts for bribes! It is also very difficult for a cross border trader to access low interest loans from national banks (Justice, 2010).

There is vulnerability of traders to corruption by customs officials. They may take advantage of their lack of knowledge of certain customs procedures, and harass them with the aim of extorting money from them (Justice, 2010).

There is also limited knowledge of procedures. These include customs and related charges and taxes. This is particularly relevant for importing the goods on which informal traders rely. Where knowledge does exist, the procedures are cumbersome (Network Economic Justice, 2010).

The role that women owned cross-border SMEs play

Small and medium enterprises operated by women in Malawi are believed to contribute significantly to the country’s Gross Domestic Product (GDP) and account for an increase of businesses in Malawi. SMEs therefore have a crucial role to play in stimulating growth, generating employment and contributing to poverty alleviation, given their economic importance in the country.

Cross-border trading is one type of the SMEs and is often one of the few employment options available to women, especially with limited or no education who have families to support. For many women, it may be the only source of household income in many families (Africa Regional Empowerment and Accountability Programme, 2015).

SMEs owned by the women also improve the efficiency of domestic markets and make productive use of scarce resources, thus facilitating long-term economic growth. SMEs also seem to have advantages over their large-scale competitors in that they are able to adapt more easily to market conditions changes. They are able to withstand adverse economic conditions because of their flexible nature. The sector has the potential to contribute towards reducing poverty among both rural and urban cities.

Women comprise 70-80% of informal cross border traders in the southern Africa region and that ICBT contributes to women’s livelihoods – both at the individual and household level- as well as food security and national and regional economic growth and trade (USAID, 2017).

The Informal Cross Border Trades (ICBT) done by women accounts for some 30 to 40% of intra-SADC trade and they contribute to economic growth by increasing business activity through their import and export of goods and employment creation at the national and regional level (UNCTAD, 2010). They also contribute to governments’ revenues via duty, license, and passport fees. According to key informants from the Mwanza Land Border of the Malawi Revenue Authority (MRA), Malawi’s trade policy recognizes ICBT and its impact on easing unemployment.

Challenges faced by women-owned SMEs

There are four areas of financing that previous research has noted can pose particular problems for women. Firstly, women may be disadvantaged in their ability to raise start-up finance. Secondly, guarantees required for external finance may be beyond scope of most women’s personal assets and credit track record. Thirdly, once business is established, finance may be more difficult for female entrepreneurs to rise than for their male counterparts because of the greater difficulties that women face in penetrating informal financial networks. Finally, the relationship between female entrepreneurs and bankers may suffer from sexual stereotyping and discrimination (Carter, 2000).

The research carried out by the United Nations Conference on Trade and Development and the United Nations Industrial Development Organization in Zambia in 2000 based on 35 women entrepreneurs revealed that women’s full economic potential is not being tapped. The main obstacles for women entrepreneurs in this study include lack of capital, lack of infrastructure for business, as well as lack of training, lack of innovation, networking and assistance from government agencies.

The research from the State University in Kenya on the constraints faced by SME’s in Kenya revealed that business financing in terms of start-up and capital for continued operations is cited as the greatest problem for small women’s business development (Cooley and Lutabwinga, 2001).

There are also several key constraints for Informal Cross Border Traders. While free trade area has helped ease border taxes in Common Market for Eastern and Southern Africa region, there are still a range of taxes and charges, many which are quite costly for traders. Additionally, inadequate access to finance and financial resources is a chronic problem for women ICBTs; 80% of ICBTs obtain capital from informal sources and rotating savings clubs are highly popular. A key finding from field research is the enormous information gap between ICBTs and border agents. Many Malawian revenue authorities insisted that customs rules are clear, but ICBTs disagree and expressed concerns about being harassed, cheated and overcharged by the MRAs. Many ICBT’s also complained of high rates of GBV to, from, and at borders (USAID, 2017).

The legal situation of African women in business is improving. Nevertheless, women still have inadequate access to finance in general and, more specifically, to working capital for their businesses. Limited access to financial resources for doing business is a chronic problem for women ICBTs. According to COMESA (2012), nearly 80% of ICBTs obtain their capital from informal sources while about half used their own savings. Financial support from family and friends are particularly important sources of finance for up to 68% of women. Only one-fifth of traders have access to bank loans, and 62% of these are men, mostly in Ugandan border towns (Blumberg et al., 2016).

A key finding from the field research is the enormous information gap between the ICBTs, especially women ICBTS and customs officials, both high-level and “front-line” (Blumberg et al., 2016). The situation is exacerbated by the lack of posted customs rules and regulations at all the borders visited by the researchers. Researchers asked representatives of all the major border agencies, “Would you be in favor of a large, laminated poster that contains all the latest rules and regulations about [customs duties, immigration rules about length of stay, etc…] being mounted on the wall in a high-traffic area of your office, where it would be visible to all?” All of the agencies agreed that this would be a good idea. In some cases, a follow-up question was asked, “Should a complete, printed set of the rules and regulations be available to those who pass through their border agency?” Here too, the response was very positive. This is an initiative that can be followed up and easily monitored.

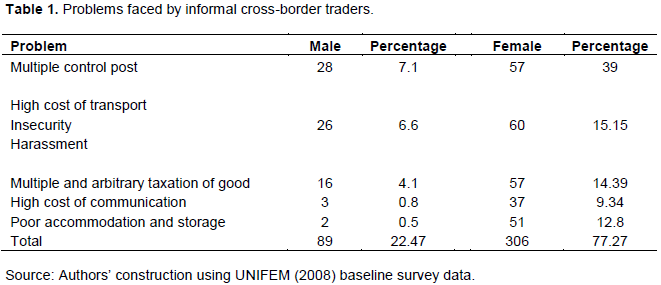

As with other sectors, gender inequalities also manifest themselves in informal trade and affect the way in which women make their living. According to International Labour Office (1991), informal trade is the most important source of employment among self-employed women in sub-Saharan Africa. Women therefore play a critical role in addressing vital issues of livelihoods such as food and income security. The SADC Gender Protocol is also critical for women in informal cross -border trading, especially Article 17 on economic empowerment which states that State Parties shall, by 2015, adopt policies and enact laws which ensure equal access, benefit and opportunities for women and men in trade and entrepreneurship, taking into account the contribution of women in the formal and informal sectors (Makombe, 2011). Table 1 shows challenges faced by women face in Central Africa (Njikam, 2011).

By looking at the earlier discussed, it can be noted few mentioned challenges (especially customs challenges) that are faced by cross-border women and one would conclude that cross border entrepreneurs are not much recognized or not much has been done to assist the cross-border entrepreneurs, hence, the aim of this research to fill that gap which other researchers did not do.