ABSTRACT

The purpose of this study is to investigate the factors affecting customers’ satisfaction towards the use of Automated Teller Machines (ATMs). To address the research objectives, 200 questionnaires were distributed to respondents. A total of 176 were returned which is equivalent to 88% of the total response rate. Data were collected using semi-structured questionnaires and they were organized, coded and analyzed using Minitab18 software. The collected data were analyzed using descriptive Statistics, correlation and multiple regression model. Descriptive analysis showed half of the respondents (50%) agreed that time saving is the main reason to use ATM services. Majority of customers use ATM Banking for Cash withdrawal services and majority of the CBE customers were satisfied by the ATM services provided to them. However, customers were facing different problems associated with ATM service. Some of the problems were the unreliable network for ATM services, limited amount of money to be withdrawn per day, reduction in balance without cash payment, bank charges for ATM services, machine out of cash, card gets blocked or locked up and waiting in line to use ATM Machines. The multiple regression findings also revealed that responsiveness, efficiency, appearance, reliability and convenience of ATM have a significant and positive influence on customers’ satisfaction.

Key words: Commercial Bank of Ethiopia (CBE), automated teller machine (ATM), customer satisfaction, service quality.

In modern economics, service sector plays a significant role side by side with manufacturing and other sectors. According to Agbor (2011), banking sector does its activities socially and economically in a country. Service personnel of such service industries are concerned about their service quality and client satisfaction. This calls for the application of more efficient method of service delivery that makes it possible for the clientele to meet their service expectations.

In the age of modern technology, the banking sector is considered as life blood of global business. Innovation in technology increases the efficiency of banking operations and system to increase the competitive market share. Banking industry is fast growing with the use of technology. In the last few decades, information technologies have changed the banking industry and have provided a way for the banks to offer differentiated products and services to their customers (Barun et al., 2014). Electronic based business models are replacing conventional banking system and most banks are rethinking business process designs and customer relationship management strategies. It is also known as e-banking, online banking which provides various alternative e-channels to using banking services, that is ATM, credit card, debit card, internet banking, mobile banking, electronic fund transfer, electronic clearing services etc. (Singh and Komal, 2009).

Automated Teller Machine (ATM), is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller (Adepoju and Alhassan, 1970). Automated Teller Machine (ATM) has been seen by both scholars and practitioners as one of the most innovative techniques that have been introduced into the banking system. This technique enables banks to provide customers with quality and satisfactory services. The increasing numbers of bank customers preferring this technique do so not only because of its self-service delivery attribute and increased autonomy in executing transactions but also due to diversified financial services it offers (Akpan, 2016). ATMs save time and provide convenience to the customers due to the fact that the card holders do not need to go to bank branches to withdraw money, and the card holder is able to make shopping, travelling etc. ATMs offer a 24 h banking service to the bank customer like cash withdrawal, fund transfer, balance inquiry, card to card transfer, bill payment, accept deposit etc (Kumbhar, 2011).

An ATM allows a bank customer to conduct their banking transactions from almost every other ATM in the world. The developments of technologies have enabled organizations to provide superior services for customers’ satisfaction (Surjadjaja et al., 2003). The availability of several ATMs country wide has greatly improved the quality and convenience of service delivery; however, some researchers have stated that users’ satisfaction is an essential determinant of success of the technology-based delivery channels (Tong, 2009). According to Singh and Komal (2009), ATM services enhance operations and customer satisfaction in terms of flexibility of time, add value in terms of speedy handling of voluminous transactions which traditional services were unable to handle efficiently and expediently. Moreover, today customers of any service including banking are interested in the ease, reliability and faster service. They want autonomy in transacting and so that they prefer self- service delivery system (Khan, 2010).

In Ethiopia, banking services offer different services like mobile banking, internet banking, SME banking, credit card, Short Message Service (SMS) banking, foreign currency account, Automated Teller Machine services, locker service, and loan and advances. They also offer corporate banking, loan syndication, real-time online banking for corporate clients. Service charges, quality of service, perceived value and customer‘s satisfaction are the main sources of success in any service factory. Commercial Bank of Ethiopia (CBE) is the first bank in Ethiopia to introduce ATM service for local users. Currently, CBE has more than 20 million account holders and the number of Mobile and Internet Banking users also reached more than 1,736,768 as of June 30th, 2018. Active ATM card holders reached more than 5.2 million. As of December 31, 2018, 2361 ATM machines and 12,057 POS machines were available (CBE, 2018). However, despite the fact that the ATMs are strategically installed in branches, hotels, universities, malls and other public places, only 22.5% of the total CBE’s customer were using ATM at the end of 2016. Moreover, due to lack of appropriate infrastructure and related problems (frequent breakdown of ATM service, ATM machines being out of cash, cards being blocked, unreliability of ATM service, lack of sufficient technicians who solve breakdown of ATM machine in all bank). It failed to increase customer satisfaction and profitability. Therefore, the researchers prompted to investigate and find out the factors affecting customer satisfaction towards the use of ATMs cards at state owned Commercial Banks in Chiro Twon.

ATM and ATM services

ATM is a computerized machine that provides the customers of banks the facility of accessing their accounts for dispensing cash and carrying out other financial transactions without the need of actually visiting a Bank Branch. ATM is an Electronic Fund Transfer terminal capable of handling cash deposits, transfer between accounts, balance enquiries, cash withdrawals and pay bills (Hood, 1976). ATM refers to a machine that acts as a bank teller by receiving and issuing money to and from the ATM account holders/users. The features of ATM include a computer terminal, record keeping system and cash vault in one unit. It permits customers to enter a financial firm’s bookkeeping system with either a plastic card containing a personal identification number by punching a special code number into a computer terminal linked to the financial firm’s computerized records (Peter and Sylkia, 2008). Worldwide, ATMs have made it easy for ATM users to get some bank services out of bank offices which inter alia include provision of mini bank statement, cash withdrawal, cash deposit, transfer of funds from one account to another, balance enquiry, purchase of some utilities like electritown and air time, bill payments, and tax payments (Tillya, 2013). According to Lovelock (2000), today ATM machine gives convenience to bank`s customers. This means that nowadays, ATMs are located at convenient places, such as at the universities, air ports, railway stations, hotels, bus stands, supermarkets, petrol stations, and not necessarily at the bank`s premises. ATM provides 24 h service, meaning that ATMs provide service around the clock. The customer can withdraw cash up to a certain limit during any time of the day or night (Akrani, 2011).

ATM service quality and customer satisfaction

Akinmayowa and Ogbeide (2014) found that convenience, efficient operations, security and privacy, reliability and responsiveness are significance dimensions of ATM service quality, adding that ATM service quality has a significant positive relationship with customer satisfaction. Salami and Olannye (2013) investigated customer perception about the service quality in selected banks in Asaba Delta State. The study found that the dimensions of empathy, tangibility, assurance and responsiveness significantly affect customers’ perception of service quality. Khan (2010) identified that the key dimensions of automated banking service quality include convenience, reliability, privacy, ease of use, and responsiveness. Ebere et al. (2015) further argued that efficient operation, convenience, security and privacy, responsiveness and reliability influence customers’ satisfaction. Lovelock (2000) identified that adequate number of ATMs, secured and convenient location; user-friendly system, and functionality of ATM are the important factors for the customer satisfaction. Moreover, Al-Hawari and Ward (2006) compiled a list of five major items about ATM service quality that include convenient and secured locations, functions of ATM, adequate number of machines and user-friendliness of the systems and procedures.

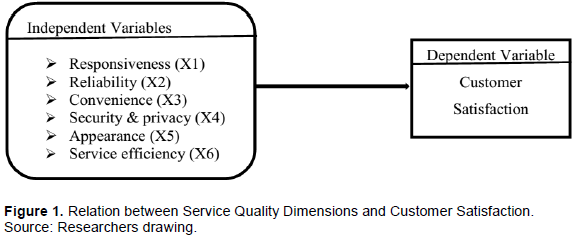

Conceptual frame work

This conceptual frame work describes the relationship between dependent variable (customer satisfaction) and independent variables (dimensions of service quality). The model identifies responsiveness, reliability, convenience, security and privacy, appearance and operation efficiency as the main dimensions of service quality (Figure 1).

Research design

This empirical study was based on primary data that were obtained from ATM users of the selected commercial banks in Chiro town. Descriptive, Correlation and Multiple regression analysis were employed for the study. Descriptive statistics was applied to give a clear picture of respondents’ demographic profiles and to answer some research questions like reasons to prefer ATM, degree of satisfaction, challenges using ATM services, purposes of using ATM, how long respondents had owned an ATM card and how often respondents use ATMs cards etc. The correlation analysis was conducted to assess the relationship between independent variables and dependent variable. Multiple regression method was used to examine the simultaneous effects of several independent variables on a dependent variable

Data collection

The study used mainly the data obtained from primary sources. Primary data were collected from customers who were using ATM services in different branches of CBE in Chiro Town. Primary data were collected using semi-structured questionnaires. 200 Questionnaires were distributed by using convenience sampling techniques in different branches of CBE and 176 questionnaires were completed and used for the analysis.

Population and sampling size determination

The study targeted only ATM users of Commercial Bank of Ethiopia in Chiro town. A non-probability sampling system specifically, convenience sampling technique was used during the study. This is because the total number of population from which the sample was drawn was not known to the researcher. In this study a sample of 200 ATM users of CBE in Chiro town were selected. To get each respondent, convenience sampling method was used where customers were intercepted at the branches of the banks until the required sample size was reached.

Data analysis

Descriptive, Correlation and Multiple regression analysis were employed for the study. Descriptive statistics was applied to give clear picture of the respondents’ profiles. To determine the relationship between dependent and independent variables Pearson correlation was used. Furthermore, the regression analysis was applied to measure the contribution of the independent variable to the dependent variable. Data were processed with the help of Mintab18 software.

Model specification

According to Sekaran (2003), multiple regression analysis is done to examine the simultaneous effects of several independent variables on a dependent variable using interval scale. In other words, multiple regression analysis aids in understanding how much of the variance in the dependent variable is explained by a set of predictors. To assess the determinant factors of customer satisfaction, the model proposed six predictors. These six predictors are Responsiveness (X1), Reliability (X2), Convenience (X3), Security and privacy (X4), Appearance (X5) and Service efficiency (X6). For the analysis, the following MLR model was developed as follows:

Y = β0 + β1(x1) + β2(x2) + β1(x3) + β2(x4) + β1(x5) + β2(x6) + ε

Where,

(i) Y - is the value of the dependent variable (in the case of this study Customer satisfaction).

(ii) β0 - the regression constant

(iii) The parameters βj, j = 1, 2 … k are called the regression coefficients of parameters

(iv) ε - is the total error of prediction (residual).

EMPIRICAL RESULTS AND DISCUSSION

Descriptive analysis

Sex of respondents

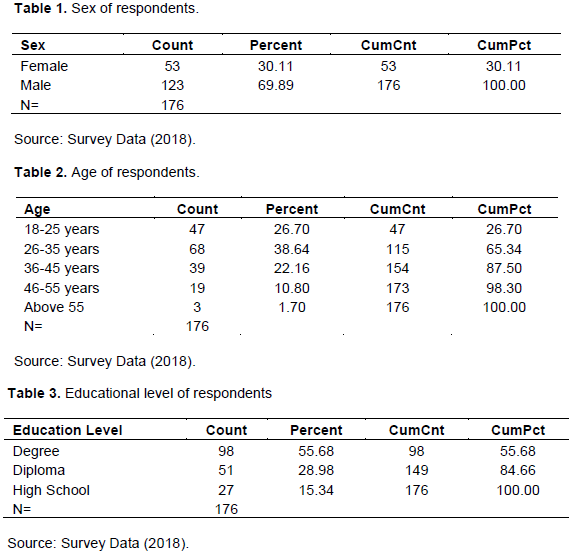

Table 1 revels that out of 176 respondents, 123 (70%) were males and 53(30%) were females. This implies that males make use of ATM services than the females in Chiro town.

Age of respondents

Table 2 reveals that 47(26.70%) of respondents were between 18 and 25 years; 68 (38.6%) respondents were between 26 and 35 years. Another 39 (22.16%) were between 36 and 45 years, 19 (10.8%) respondents were between 46 to 55 years, while 3 respondents, representing about 1.7% were above 55 years. The result implies that majority of the customers that patronize banks were 26-35 age groups

Education level of respondents

The academic attainment of the respondents shows that more than half of the users of ATMs (56%) were degree holders, 30% of the users were Diploma holders and 15.3% of the users completed high school. This implies that most of ATM Services customers were educated (Table 3).

Occupational distribution

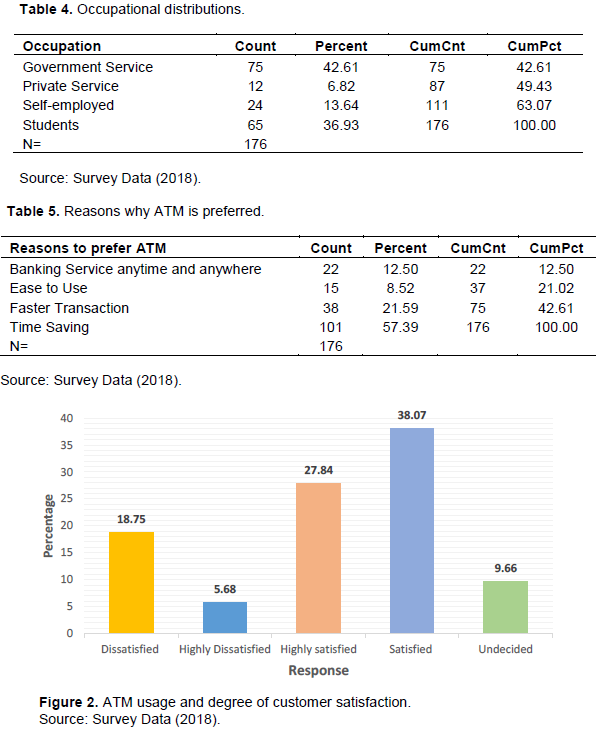

Occupational distributions of the respondents are shown in Table 4. The results reveal that out of the total respondents 42.6% were civil servants, 36.9% were students, 13% were self -employed customers and about 6.8% were private services employed. The result showed that civil servants form the larger percentage of banks’ customers and as well as active users of ATMs in Chiro town.

Reasons why customers prefer to use ATM services

Table 5 reflects that 12.50% respondents were using ATM to get banking service at anytime and anywhere, 8.52 % respondents preferred it as it is easy for them to use, 21.59 % preferred ATM banking for its faster transaction, 57.39 % used it since it saves time. This is to mean, it is manly used in order to avoid long queues in banks.

Degree of satisfaction

Figure 2 shows that only about 33 (18.75%) and 10 (5.6%) of the respondents were dissatisfied and highly dissatisfied respectively with the ATM service of their banks. However, 67(38%) and 49(27.8%) indicated being satisfied and highly satisfied respectively and while 17 (10%) were undecided This implies that larger proportion of banks’ customers in Chiro town were satisfied with ATM services of their banks.

Purpose of using ATM

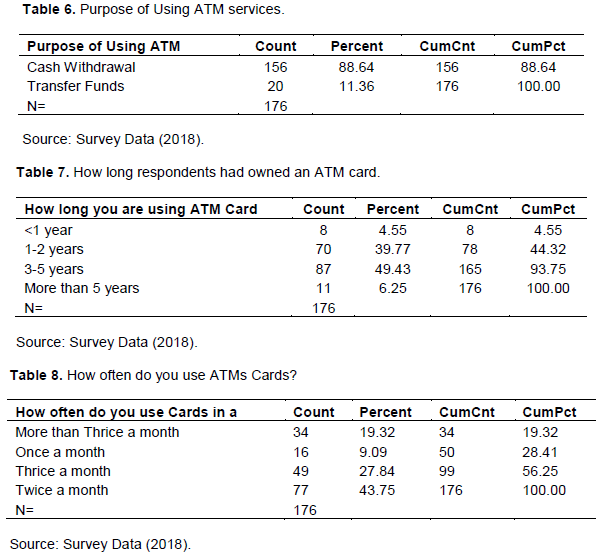

With reference to Table 6, the study reveals that majority of the respondents 156 (88.64%) were using ATM Banking for Cash withdrawal and 20 (11.36%) of respondents were using ATM Banking for transfer funds. However, the study reveals that none of the respondents performed ATM banking transactions involving bill payments, balance enquiry, recharging of prepaid cards and cash deposit to their own accounts and different accounts.

Reponses on how long respondents owned an ATM card

The results in Table 7 shows that majority of the

respondents 87 (49.4%) had owned an ATM card for 3-5 years, 70 (39.7%) of respondents had owned an ATM card for 1-2 years. 11 (6.25%) of the respondents had owned an ATM card for more than 5 years and 8 (4.5%) of the respondents had owned an ATM card for less than 1 year.

Responses on ATM banking frequency

With reference to Table 8, the majority of the respondents 77 (43.7%) engaged in ATM Banking twice a month, 49 (27.8%) engaged in using ATM Banking 3 times a month, 34 (19.3%) of the respondents engaged in using ATM Banking more than thrice a month, while 16 (9%) of the respondents engaged in using ATM Banking once in a month.

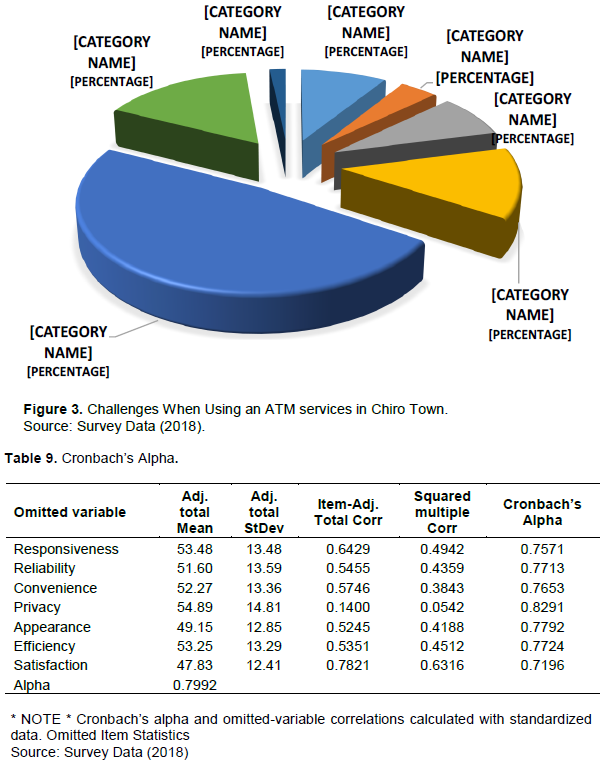

Responses on challenges when using an ATM in Chiro Town

Figure 3 presents the problems associated with ATM transaction in the selected banks. It reveals that 16 (9.09%) of the respondents considered the problem of ATM of their bank branch to be bank charges for ATM services, 7 (4%) of the respondents perceived the problem to be card got blocked or locked up, 14 (7.95%) indicated the problem to be machine out of cash, 85 (48.30%) perceived the problem was unreliable network for ATM services, 23 (13.07%) perceived the problem to be reduction in balance without cash payment, 28 (16%) believed it is limited amount of money to be withdrawn per day. Finally, waiting in line to use ATM Machines was stated by just 3 (1.70%) of the respondents. The conclusion here is that unreliable Network for ATM services ranks the first of the problems of ATMs in Chiro Town.

Reliability test

Table 9 indicates that all the reliability values of each construct are greater than the benchmark of 0.70 which was recommended by Hair et al. (2014). Therefore, all variables have crossed this acceptable level as Cronbach

Alpha of responsiveness, reliability, convenience, privacy, appearance, efficiency and satisfaction are 0.7571, 0.7713, 0.7653, 0.8291, 0.7792, 0.7724 and 0.7196 respectively. Since all the Cronbach’s Alpha coefficients were greater than 0.7, the conclusion is drawn that the instrument had a good internal consistency of the items in the scale and was appropriate for the study.

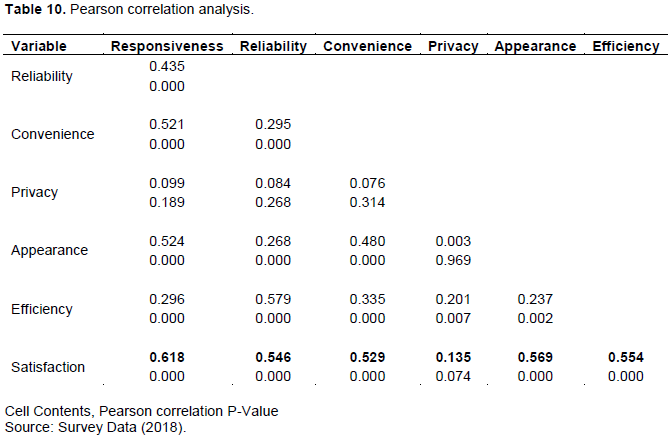

Correlation analysis

Table 10 indicates Pearson correlation. The Pearson shows the relationship between responsiveness, reliability, convenience, privacy, appearance, efficiency and customer satisfaction.

The results indicate that there is positive and significant relationship between responsiveness and customer satisfaction (r = 0.618, p < 0.000), reliability and customer satisfaction (r = 0.546, p < 0.000), convenience and customer satisfaction (r = 0.529, p <0.000), appearance and customer satisfaction (r = 0.569, p < 0.000) and operations Efficiency and customer satisfaction (r = 0.554, p < 0.000). Similarly, there is a moderate positive correlation between privacy and customer satisfaction (r = 0.135, p < 0.074). The finding indicates that the highest relationship is found between responsiveness and customer satisfaction (r = 0.618, p < 0.000). Unlike privacy, four service quality dimensions (reliability, convenience, appearance, and operations efficiency) have a strong positive and significant relationship with customer satisfaction.

Regression analysis

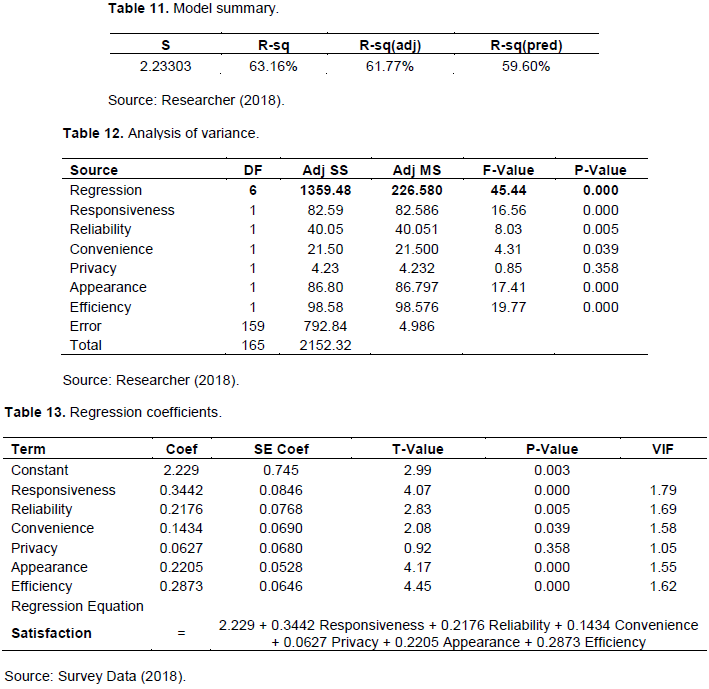

Model summary (Table 11) shows the results of entering six independent variables against customer satisfaction (dependent variable). The model described the overall relationships between dependent and independent variables (R), goodness of fit (R square) and the standard error of estimate. The value of (R) is (0.63); it determines the strength of the relationship between all independent variables and dependent variable. The results have shown that 63.16% variations are caused by independent variables.

The coefficient of determination (R2) is (0.617); the value R square shows how close the data are to the fitted regression line. The R2 value of 0.617 indicates that the model explains 61% of the attributes were responsible for overall customer satisfaction of ATM users. It means that there is a positive relationship between all independent variables and a dependent variable (customer Satisfaction). The independent variables represented in the responsiveness, reliability, convenience, privacy, appearance and operations efficiency amounted to the impact of these variables combined on the dependent variable through the Adjusted R Square of 0. 596. This indicates that the model explains roughly about 59% of the factors are responsible for customer satisfaction.

The ANOVA output was examined to check whether the proposed model was viable. Therefore, Analysis of variance in Table 12 indicated that responsiveness, reliability, convenience, privacy, appearance and efficiency were statistically significant in explaining customer satisfactions. The results showed that the overall model was significant (F=45.44, P value =0.000). Table 13 shows the VIF value <10. Thus the model does not have the phenomenon of multi-collinearity between the independent variables.

The unstandardized Beta Coefficients that represent the contributions of each variable to the model are presented in Table 13. The Beta Coefficients and p-values showed the impact of the independent variables on the dependent variable. The regression results confirmed that responsiveness, operations efficiency, appearance, reliability and convenience of ATM have a significant and positive influence on customer satisfaction. Their magnitudes are as follows: Responsiveness (β = 0.3442, p = 0.000) was found to have a significant effect on customers’ satisfaction towards ATM service. The result is in support of the conclusion made by Akinmayowa and Ogbeide (2014), Ebere et al. (2015) and Adeleye and Samson (2015). Operations efficiency (β = 0.2873, p = 0.000) had the major effect on customers’ satisfaction towards ATM service. This finding was supported by Akinmayowa and Ogbeide (2014) and Ebere et al. (2015). Appearance (β = 0.2205, p = 0.000) had a positive and significant effect on customer satisfaction. The finding of this study supported the conclusion made by Lovelock (2000). Reliability (β = 0.2176, p = 0.005) had significant effect on customers’ satisfaction. The finding of this study is consistent with Naeem and Arif (2011), Akinmayowa and Ogbeide (2014), Narteh (2013) and Adeleye and Samson (2015). Moreover, convenience (β = 0.1434, p = 0.039) had a positive and significant effect on customers’ satisfaction. The result of the study supports the previous research by Akinmayowa and Ogbeide (2014), Ebere et al. (2015) and Narteh (2013). Finally, the results found that privacy (β = 2.906, p = 0.358) had a positive and insignificant effect on customers satisfaction.

In general, the results indicate that increasing the quality of service efficiency, responsiveness, appearance, reliability and convenience will inherently increase customers’ satisfaction towards ATM service quality.

Based on the descriptive results, out of total respondents more than 50% agree that time saving is the reason to use ATM services, followed by faster transaction; banking service at anytime and anywhere is another significant reason to use ATM services. The study has revealed that majority of customers were using ATM Banking for cash withdrawal while second preference was to use ATM banking for transfer funds. The findings also lead us to conclude that, majority of the CBE customers were satisfied by the ATM services provided to them. However, customers faced different problems associated with ATM services. Some of the problems that customers indicated were unreliable network for ATM services, limited amount of money to be withdrawn per day, reduction in balance without cash payment, bank charges for ATM services, machine out of cash, card gets blocked or locked up and waiting in line to use ATM Machines.

Moreover, the regression analysis supported that responsiveness, efficiency, appearance, reliability and convenience of ATMs have positive and significant effect on customer satisfaction. The study findings further indicated that responsiveness were regarded as the most important factors by the customers and it has a significant impact upon customer satisfaction followed by Service efficiency, appearance and reliability.

Based on the findings of the study, the following recommendations were forwarded;

(i) The respondents ranked the major problems that encountered while using the ATM services. Therefore, the bank should improve its service quality by solving problem of network failure, shortage of cash in ATM machines, limited amount of money to be withdrawn per day, reduction in balance without cash payment, bank charges for ATM services and machine out of cash by using different mechanisms. That is upgrading network system, periodic maintenance of machine, availing power supply, increasing the amount of money to be withdrawn and close follow up on cash availability in ATM) to resolve existing problems and improve satisfaction on ATM services.

(ii) The amount of money to be withdrawn from the bank using ATM machine should be increased more than it is now. This will help reduce congestion at the counter.

(iii) The banks should frequently and consistently inspect the ATM machines in order to avoid network failure, shortage of cash in ATM machine and machine breakdowns that may lead to inconvenience to the customers

(iv) The bank management should increase the number of ATM machine accessible in every branch and some selected areas like universities/colleges, hotels and hospital.

(v) The bank management should give training to employees how to treat customers and how to solve the ATM banking service problems.

(vi) Commercial bank of Ethiopia should enhance and diversify their services through ATMs. Banks should also improve ATM features to suit customers and use this medium to build a strong and sustainable relationship with customers

(vii) Finally, commercial bank of Ethiopia should raise customer awareness on usage of ATMs by using mass media such as, television, radio and bill board as well as paste directive posters at every ATM centers. These will ensure that the services are easy and clear to enhance effective interaction for maximum customer satisfaction.

The authors have not declared any conflict of interests.

REFERENCES

|

Akrani G (2011). Automated Teller Machine ATM - Advantages of ATM.

|

|

|

|

Adeleye OI, Samson OF (2015). An empirical study of automated teller machine service quality on customer satisfaction (A case study of United Bank of Africa [UBA]). International Journal of Scientific Research in Information Systems and Engineering 1(1):61-68.

|

|

|

|

|

Adepoju AS, Alhassan ME (1970). Challenges of Automated Teller Machine (ATM) Usage and Fraud Occurrences in Nigeria â   A Case Study of Selected Banks in Minna Metropolis. The Journal of Internet Banking and Commerce 15(2):1-10.

|

|

|

|

|

Agbor JM (2011). The Relationship between Customer Satisfaction and Service Quality: a study of three Service sectors in Umeå. Available at: View

|

|

|

|

|

Akinmayowa JT, Ogbeide DO (2014). Automated Teller Machine Service Quality and Customer Satisfaction in the Nigeria Banking Sector. Journal of Business and Social Science 65(1):52-72.

|

|

|

|

|

Akpan SJ (2016). The influence of atm service quality on customer Satisfaction in the banking sector of Nigeria. Global Journal of Human Resource Management 4(5):65-79. Available at:

View

|

|

|

|

|

Al-Hawari M, Ward T (2006). The effect of automated service quality on Australian banks' financial performance and the mediating role of customer satisfaction. Marketing Intelligence and Planning 24(2):127-147.

Crossref

|

|

|

|

|

Barun KJ, Shilpa S, Shitika (2014). Customer'sSatisfaction For ATM Services In Bihar, India. International Journal of Interdisciplinary and Multidisciplinary Studies 1(4):42-49. Available at:

View

|

|

|

|

|

Commercial Bank of Ethiopia (CBE) (2018). Annual Report, 2018. Available at:

View

|

|

|

|

|

Ebere AK, Udoka EF, Gloria EN (2015). Gap Analysis of Automatic Teller machine (ATM) Service Quality and Customer Satisfaction. Journal of Electronics and Computer Science 2(3):1-8.

|

|

|

|

|

Hood JM (1979). Demographics of ATMs. Banker's Magazine, November-December. pp. 68-71.

|

|

|

|

|

Khan MA (2010). An empirical study of automated teller machine service quality and customer satisfaction in Pakistani banks. European Journal of Social Sciences 13(3):333-344.

|

|

|

|

|

Kumbhar V (2011). Factors affecting on customers' satisfaction an empirical investigation of ATM service. International Journal of Business Economics and Management Research 2(3):144-156.

|

|

|

|

|

Lovelock C (2000). Functional integration in services. Handbook of Services Marketing and Management', Sage, Thousand Oaks pp. 421-437.

|

|

|

|

|

Naeem BA, Arif ZO (2011). How do service quality perceptions contribute in satisfying banking customers? Interdisciplinary Journal of Contemporary Research in Business 3(8):646-653.

|

|

|

|

|

Narteh B (2013). Service quality in automated teller machines: an empirical investigation. Managing Service Quality: An International Journal 23(1):62-89.

Crossref

|

|

|

|

|

Peter SR, Sylvia CH (2008). Bank Management and Financial Services. New York: McGraw Hill/Irwin.

|

|

|

|

|

Salami CG, Olannye AP (2013). Customer Perception about the Service Quality in Selected Banks in Asaba. Journal of Research in International Business and Management 3(3):119-127.

|

|

|

|

|

Sekaran U (2003). Research Methods for Business: A Skill-Building Approach. New York: Hermitage Publishing Services and printed and bound by Malloy Lithographing, Inc.

|

|

|

|

|

Singh S, Komal M (2009). Impact of ATM on customer satisfaction (A comparative study of SBI, ICICI & HDFC bank). Business Intelligence Journal 2(2):276-287.

|

|

|

|

|

Surjadjaja H, Ghosh S, Antony J (2003). Determining and assessing the determinants of e-service operations. Managing Service Quality: An International Journal 13(1):39-53.

Crossref

|

|

|

|

|

Tillya JJ (2013). The effect of automated teller machine (ATM) service on customer satisfaction in the Tanzanian banking sector: the case study of national microfinance bank (NMB), Ifakara branch (Doctoral dissertation, Mzumbe University).

|

|

|

|

|

Tong DYK (2009). A study of e-recruitment technology adoption in Malaysia. Industrial Management and Data Systems 109(2):281-300.

Crossref

|

|