The Sunday opening of shops is a very debated topic on both international and national levels. On a European level, the regulation of Sunday work is varied, with most Member States that, like Italy, do not impose restrictions on openings and working hours. The present work aims to analyze the European reference framework of Sunday openings, focusing on the Italian situation, which is currently experiencing proposals for change. Moreover, from the statistical analysis of the purchase data made in the main Italian stores of a multinational company, the "profile of the Sunday consumer" is highlighted, analyzing the characteristics and peculiarities that orient Sunday shopping. The Two Step cluster analysis provides different profiles, among which emerges the consumer profile of Sunday, which assumes peculiar characteristics and different from those of consumers of the other days of the week.

The regulation of Sunday work is a subject that has long divided and has been long discussed by public opinion. The arguments against liberalization policies of the sector are numerous: religious organizations defend the uniqueness of Sunday as a day of rest, the trade unions highlight the right of workers to stay with the family, while small and medium-sized enterprises seek prohibiting openings Sunday a protection against the competition of modern retailers (Kim, 2016; Danchev and Genakos, 2015; Skuterud, 2005; Gruber and Hungerman, 2008; Tanguay et al., 1995).

In Europe, the regulatory model of working hours and Sunday openings is the most varied. In some EU Member States there is no restriction on timetable nor Sunday opening. Italy, therefore, belongs to the group of countries with a more competitive discipline, but certainly it is not an exception in the European panorama (Kovács and Sikos, 2016; Choi and Jeong, 2016; Clemenz, 1990; Ingene, 1986; Kay and Morris, 1987; Price and Yandle, 1987; Tanguay and Upton, 1986).

The present work aims to frame the European situation of Sunday openings, focusing attention on the current Italian situation. Moreover, from the analysis of the data carried out on the main Italian stores of a well-known Swedish multinational, the profile of the Sunday consumer is highlighted, analyzing in detail his personal characteristics, spending preferences and the motivations that drive him to Sunday shopping.

The analysis contained in this work involves both the "quality" of the law and its actual innovative charge;

moreover it analyzes the verification of the implementation of the new law and therefore the real interest shown by the local and regional autonomies in pursuing an opening policy of a very crucial sector, as it is undervalued for the productivity of the entire economy and for the overall efficiency of the Italian economic system.

This last statement becomes even more significant if it is inserted in the framework of the enormous transfer of competences envisaged by constitutional federalism, including the passage of exclusive legislative power to the regions in matters of trade. The evaluation of the "Bersani Law" becomes, therefore, a first litmus test of the institutional structure of the overall economic policy and of the sectoral policies. A structure that responds, on one hand, to the traditional principles of decentralization efficiency, on the other hand, raises numerous questions in relation to the possible disincentive towards liberalizations and market (more direct lobbying by some categories; more possible conditioning).

The result of the law on trade, therefore, can be very useful to understand more clearly not only the advantages, but also the risks and potential problems that may arise in the process of complete implementation of federalism.

The Italian retail trade presents a series of peculiarities that differentiate it markedly from that of the major European countries. For the most part, these are the same anomalies that make the national industrial system a case study in the European Union: average size per employee and very low turnover, bordering on the pulverization of the company, and very low weight of the largest companies’ size. All of this with the well-known corollaries of obvious income positions, managerial inefficiencies and limited levels of research and development.

Italy is the country with a far lower market share of the top ten distributors - below 40% - compared to all other European countries and to a European average of 80%. In analogy to other indicators of the structure of our economy, the very low level of concentration in the retail trade hides very marked differences on a territorial level. Unlike the central-northern Italian regions where the presence of large retailers was greater, especially in the past decade, the South tends to have fewer large retailers on average. For example, where the regional structure appears to be unbalanced on small typologies of commercial establishments, the degree of presence of the large company is more limited. This is a circumstance that will help to understand better the regional market dynamics and, above all, the resistance to a greater opening of the local areas to the larger commercial enterprises.

The Added Value of the entire trade sector (wholesale and retail) accounts for figures close to 13% of GDP. These are high figures, even if not in a resounding way if we consider that - based on a comparison of an OECD source (Pilat, 1997) with data from some years ago - the added value of trade is equal in the USA to 16.8% of GDP and higher than that of the other southern European countries (Greece, Spain, Portugal).

The data on the Added Value of the trade are sometimes placed in relation to the degree of efficiency of the distribution sector: the greater the economic weight of the phase of forwarding of the goods to the final markets - therefore greater the resources "designated" outside the time of production - the lower the capacity of the sector to manage the intermediation activity at low cost in the national economy as a whole is lower. Similar considerations can be made regarding the share of employment attributable to the sector: the figure for Italy (17.3% of total employment) is compared with 25.8% in the United States, 16.4% of the United Kingdom, 22.3% of Spain. It is very difficult, in our opinion, to develop a criterion of "sectoral efficiency" only on the basis of the share of added value and employment; it could be argued that the high weight of commercial intermediation is a sign of an advanced tertiarization of the economy, as demonstrated, moreover, by US data.

In the Italian case the only statistics available relating to the added value of retail trade alone are surprising for their size: our country would in fact have the lowest weight of added value on total GDP against systems such as the French, German, and Dutch showing much higher measures. We should deduce from this that our retail trade is the most efficient and best organized in the West, but this consideration is hasty.

Tracing the origins of such a market structure goes far beyond the objectives of this work. Moreover, it is the entire history of the Italian company that is included in "a world from its origins determined by the fragmented physiognomy of the national market, that is, by the presence of production and consumption circuits closed in very narrow local areas". A story made up of small markets in which it seems, at times, that it was precisely the precocity of national commercial development with respect to other countries that defined salient features of the quality of our business system, regardless of the sector in which they operate and therefore included the trade segment.

At the same time, however, there is no doubt that the persistence of the phenomena of pulverization of the commercial sector and resistance to a more massive entrance of the large-scale retail trade can be justified by particularly rigid regulatory arrangements, marked by high barriers to entry and the establishment of anticompetitive practices within the sector itself. It is the role played by the heavy regulation of the commercial sector that this work intends to explore. In international comparison, Italy shows the lowest number of commercial establishments in each of the types considered.

Ultimately, the ratio of public intervention in the commercial sector cannot be traced to any market failure. The public authorities, although not directly exercising business activities, make use of a very penetrating indirect intervention. In fact, they reach a sort of "defense against the competition" of the sector, both internal and external. This function of controlling the possible increase in the competitiveness of the sector has been carried out by the public authorities for a long time with great effectiveness and has involved: a poor market contestability, a division for territorial areas and commercial types of sales very precise and even, in some stages, a check on pricing decisions.

RETAIL CONCENTRATION

Retail and brands represent the key success factors to compete in the international arena. Stores become the place where the marketing strategies of a firm come to life; in them firms communicate, foster the loyal relationship with their customers and constantly monitors market tastes and needs. The store is a determining factor in the brand image and brand identity building processes, since it is the first place to contact the consumer. Store interactivity must be boosted in order to collect more information on consumer needs and shopping behavior.

To date, retail caters to a wider specialization, serving specific target markets with different lifestyles and transmitting images, symbols and emotions. On the other hand, it presents deep fragmentation, limited efficiency in the distribution network and the high presence of small independent shops. This structure derives from the sector’s need for differentiation, since the point of sale increases the product added value (Ravazzoni and Panciroli, 2002). Store is no longer only a logistic-operative thrust but also a more complete marketing one, especially from a relational point of view.

Location and consequently the point of sale have two dimensions: the firm one and the consumer one. They should be combined in the search for a store loyalty that matches the brand one. So far stores are physically structured in relation to the spatial position and the products sold, in order to attract consumers and create an ambience (Kotler, 1972) in which to live an experience. In order to enter the consumer evocative set, the store must make such an impression as to be positively remembered in the decision-making process while choosing products and brands (Skinner, 2008). Empirical studies (Paparelli and Del Duca, 2010) found location, service, assortment depth, price strategies, quality, and store ambience to be discriminatory factors in the relation between retail and customers. In particular, the physical features such as layout, colors, music and crowding, result as strongly affecting shopping behavior and store choice (Babin et al., 2006). For example, overcrowded stores can inhibit the shopping behavior and cause various reactions, that range from reducing the store visit frequency to postponing the scheduled purchases or giving up the shopping expedition entirely (Carmona et al., 2010).

Moreover, store positioning proves to have a strong correlation not only with product features, such as quantity, quality and services, but also with marketing ones, namely price strategies, store format, time factors, benefit sought, consumer’s perception and shopping behavior. All these elements are summarized in the store image, that is strictly correlated to the quality and reputation of the brands sold in it. The store ambience features strongly affect the consumption volume and nature.

This phenomenon is obvious especially for fashion products, in which brand notoriety is combined with locations. Firms try to create a glamour context around brands in order to realize an unforgettable experience not only in buying and consuming the product but also in the time spent choosing it within a stylish environment.

In this scenario retail is spatially redefining social spaces and the relations within the city, through the traffic flows it causes. The complex functions of selling require specific locations; from city centers, suburbs, high streets, stations, airports, and so on; while globalization and the consequent enlargement of space and time relations, necessitate easy access, no separation of the street by huge windows, and free service. Therefore, a new relation between consumers and retailers is created, based exclusively on psychological and emotional factors; image and the consumers perception of it play an important role.

Consumption, and its display – shopping-, are shaping city’s identities and functions in relation to consumers’ needs. The so-called “percorsi degli elefanti” (Zukin, 2012) creates a network that assigns new vitality and dynamism to goods and people flows.

Therefore, location strategies tend towards concentration in order to follow the evolution of consumer needs: for convenience goods concentration results in purchases in a single store; while for shopping goods concentration is the solution to the issue of minimizing search costs. On one hand, consumers look for detailed information on product prices, quality and variety, and on the other hand for entertainment and fun while shopping. To match consumer needs firms are forced to locate their stores near their competitors in the so-called shopping districts/streets.

Such a concentration derives from belonging to complementary sectors and from the presence of magnet stores that modify shopper traffic and mobility, given also the customer exchange among nearby similar commercial types. So, agglomeration is demand pull; it is possible to offer a complete set of products, that can be bought in the same shopping expedition, granting savings of time and space. At present, distance is no longer the main discriminating factor, it becomes a marketing factor rather than a geographical one. Nowadays, accessibility results as the key “shopping” criterion. To be in the city center does not assure success in itself; it is the “accessibility image” that counts. So far, the trade-off between distance and dimension is influenced by consumers’ perception of the specific store image and of the store network one (Lowe, 2005).

Urban areas seem to be the best locations for shopping agglomerations by nature. They offer visibility and direct contact as near as possible to consumers, both potential and actual. On the other hand, firms are searching for larger spaces to locate their activity and create an ambience in which consumers can experience more fun and entertainment while shopping. Unfortunately, these requirements match higher location costs and are suitable only for certain products, such as fashion ones. However, spatially they stimulate a repositioning process of city centers and their streets. Throughout all the Italian cities, Bari has been chosen for its long-established commercial tradition. As it can be observed in most of Europe, the city is repositioning its image, having lost its regional and provincial commercial leadership. Within its structure, the city center is suffering from strong competition from the suburbs where shopping malls are able to attract many consumers from different areas due to price strategies, the worsening of urban accessibility and the lack of “entrepreneurship” collaboration among central retailers (Reimers and Clulow, 2009).

THE ITALIAN ECONOMIC MODEL

The evolution of the post-crisis international economic model

As known, the international economic crisis of 2008 has affected many countries, including Italy; among its effects there is the re-opening of the long-standing debate on which the most appropriate economic policies to deal with the recession are; on one hand, the need to identify the correct strategies to be put in place to use the increasingly scarce public resources (a continuous object of spending review policies) has become increasingly incumbent; on the other hand, the use of private ones has become equally crucial (De Benedetto, 2014).

In the case, in point one of the most discussed issues was the question whether the right degree of market opening was open to competition or, in other words, what was the most suitable model of capitalism to cope with the effects of the economic crisis (Somma, 2013). According to some, in fact, in the midst of the economic crisis, the state must intervene more and more directly on the markets, until it reaches the main companies of the country - the so-called "national champions" - from excessive competition with other foreign companies (Mazzucato, 2018); according to others, on the other hand, it is only by opening the markets to greater competition that the degree of competitiveness of the country system can be increased and the national economy can be boosted, improving the performance of companies, "economic liberalization" therefore understood as the abolition of limits to entry into particular economic sectors.

Indeed, it can be summarized that the first strategic evaluation prevailed in the period 2008-2011, perhaps finding its sublimation in the decree law no. 134 of 2008 (the so-called "Alitalia - CAI" decree), later converted into law no. 166 of 2008, which suspended for three years the powers of control of the Antitrust Authority on mergers between companies that are in certain conditions.

The second strategic assessment has instead characterized (Giulietti, 2012) the economic policy of the period 2011-2012, especially during the establishment of the technical government that, in November 2011 dedicated a whole provision to the liberalizations, the so called "Cresci Italia" decree (Decree Law No. 1 of 2012), and included other individual articles and provisions in other decrees, starting from "Salva Italia" decree (Decree Law No. 201 of 2011); which provided for the full liberalization of the days and opening hours of the shops. A national law, based on the basic idea that the question of working hours was relevant to the protection and promotion of competition and that establishes the freedom of the entrepreneur to better manage his business, in compliance with the laws and collective national agreements. Moreover, over 3.4 million employees work on Sundays in Italy (20% of total employees), of whom approximately 2.2 million in "non-essential" services.

This provision was issued at a time when the country was going through its worst post-war crisis. In this context there were more days of work and therefore a greater number of hours worked, exactly 24.5 million more hours worked, consequently more than 400 million higher salaries were paid each year, equivalent to 16,000 jobs of work; and again, consumption was supported, which would have fallen more than what occurred. The estimates define a support for consumption dynamics of +2% for non-food goods and +1% for food products.

Advantages and disadvantages of Sunday openings

Six years after the coming into force (year 2012) of the decree-law no. 214/2011, the “Salva Italia” conclusions can be drawn and express the first considerations on the possible advantages or disadvantages that the decree has brought.

According to Federdistribuzione (2019), the federation that represents the GDO (large-scale retail trade) in Italy, certainly the introduction of the decree has brought advantages that are immediately apparent from the rereading of the ISTAT data (National Institute of Italian Statistics).

Indeed, there are 19.5 million consumers who shop on Sundays (75% of those for family purchases) and for 58% of citizens (15 million) Sunday shopping has become a consolidated habit. In the large-scale retail trade (GDO) there are 12 million consumers who shop every Sunday (GFK, 2018). When the stores remain open 7 days a week, Sunday is the second day by turnover, representing almost 15% of the weekly turnover.

Another proof is that there was no liberalization. Indeed, on Sundays and public holidays, only outlets remain open for which the entrepreneur is convinced to provide a service to consumers while maintaining a correct budget. According to the Trade Observatory of the Ministry of Economic Development between 2012 (year of entry into force of liberalization) and 2017, the number of outlets, even with the crisis, fell only 1.4%, consequently not a collapse of the number of shops.

The Sunday and festive openings follow the needs of the consumer and with the change of the lifestyles and purchase habits of the families, that ask for more opportunities and alternatives for their free time (Dalli and Romani, 2011).

According to the CCT, the consumer of the new millennium is increasingly an Internet user (Arnould and Thompson, 2005) and approaches consumption in a multi-channel mode (Carrù and Cova, 2012), giving an objective boost to online commerce; but the growth of e-commerce, has further introduced complexity in the activities of physical commerce, which sees its perimeter shrinking both due to the crisis, which has subtracted sales, and the action of digital market places.

In light of this data, again according to Federdistribuzione, compared to the current situation, to go back would cause a worsening of the service offered to the Italian population, whose approval is shown by the 19.5 million people who shop on Sunday and an undoubted advantage to the e-commerce, which could accelerate its growth, thus exacerbating the situation for physical commerce, which invests in territories, creating employment and local development.

Furthermore, it could generate a decrease in sales at a very complex time for trade, with a consequent slowdown in investments and a reduction in the positive impact in terms of development and employment; the fewer opening days and hours worked in outlets (and therefore lower sales) would be added to the employment tensions generated by the growth of e-commerce. Reporting the regulatory situation to the "Salva Italia" could generate lower distributed wages and an employment loss at least equal to the benefits generated since 2012 (between new jobs and protected jobs), without considering the related industries. This is also the case, as some have suggested, if sales were to spread over six days instead of seven.

Different evaluations can arise from the analysis of consumer data. In fact, the retail sales measured by ISTAT for the first 5 months of 2018 are down by -0.2%.

The decrease in consumption, in the years following 2011, is demonstrated by the ISTAT charts: retail trade declines until 2014, stabilizes in the following two years and resumes growth in 2017, while wholesale trade stabilizes in 2013 then grows from 2016. But according to Federdistribuzione such a decrease would depend precisely on the economic crisis and on the spread of online purchases "every day and at any time of the day", not from liberalization but this assumption is not verifiable, in fact if considered in the years after 2011 the crisis has continued to hit the Italian economy hard, there is no way of verifying if in the absence of liberalization sales and turnover of the shops would have gone even worse, in an equal or even better way.

So, without the advent of e-commerce and without the economic crisis, liberalization would have led to a jump in sales, as Federdistribuzione implies? Or would nothing has changed, as the political representation of the current Italian government affirms?

Data analysis on Sunday shopping in Italy

The debate on Sunday work is part of a context that has seen, in recent years, the retail sector characterized by a moderate sales dynamics, with a gap between the large distribution sector that has a positive sign (+1.2%) and the small one that faces obvious difficulties with a 0.3% decline. Overall, the large distribution increased by over 4% points in the period 2010-2015; its contribution to the total turnover of fixed retail trade in Italy, reaching a share close to 50% (Istat, 2018).

The territorial reading of Sunday purchases shows that the residents of Central Italy, with 25.6%, are above the national average, while the percentage falls to 23.1% for the inhabitants of Southern Italy (Table 1). On the other hand, by observing the urban areas, the residents in the center of metropolitan areas (25.6%) are more likely to make Sunday purchases than those living in the suburbs (23.6%).

Further details allow us to grasp the specificities related to the position in the family nucleus and gender. The highest incidences are observed on Sundays within family units made up of partners in pairs with or without children (Table 2). It is mainly men, both in couples with children (33.2%) and in those without (31.4%), to make purchases; high percentages are also found in the case of "single" men (27.7%).

ISTAT also has sample information referring to the complex of the different sectors of the trade obtained from the data of the Labor Force Survey of 2017. Workers employed on Sunday represent 21.1% employment, slightly share below the EU average (22.5%) and higher than in other countries: in France this share is equal to 20.1%, followed by Spain (19.8%) and Germany (18.4%).

Mainly women work on Sundays (Table 3), who represent 61.1% of Sunday workers, compared to an average share of the total employed of 47.8%. Sunday workers are relatively younger: 42.9% are under 35 years of age, 41.7% are between 35 and 49 years old. Sunday work mainly involves workers with upper secondary education (58.5%).

The descriptive results of a large distribution survey

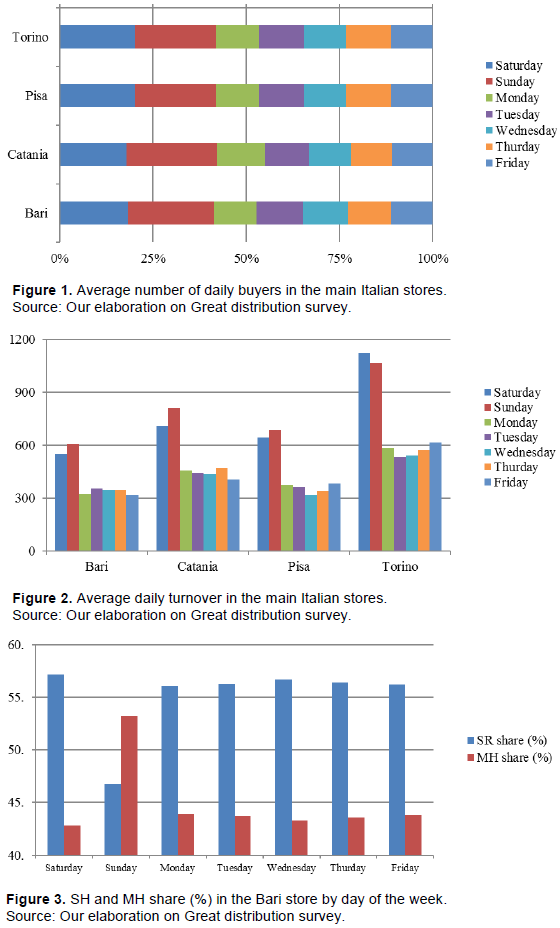

The study starts from the analysis of the data of a well-known Swedish multinational, world leader in furniture. The choice, for the elaboration of the case study, has fallen on the "Swedish giant" because it owns 21 stores distributed all over the national territory; moreover, always in the business strategy, is previewed the Sunday opening to support of the business. From the analysis of the data on the main Italian stores of a Swedish multinational, in all the Italian cities studied the number of visitors is higher both on Saturdays and Sundays; this figure also combines the largest number of buyers (Figure 1). In the stores observed we found that 42% of buyers are concentrated between Saturday (19%) and Sunday (23%). In the remaining 5 days, 48% of buyers are concentrated with percentages between 11 and 12%.

In the same way on Sunday there is an increase in turnover (+50% compared to the weekly average) in all the stores analyzed. In particular, in the Turin store the daily turnover on Sunday is equal to 1,124 euros compared to the average 718 euros per week (Figure 2).

Sunday consumer behavior

Sunday opening seems to have a genuine positive effect on spending, but not on all products, because it is only partly attributed to attracting expenses from other segments.

In the case of the Bari store it emerges that on Sunday there was a decline in the share of "furniture sector (SH)" (46.8%) and a peak in the share of "accessories sector (MH)” (53.2%). This means that the Sunday consumer focuses more on accessory products, considering Sunday shopping as a leisure time to spend with the family (Figure 3).

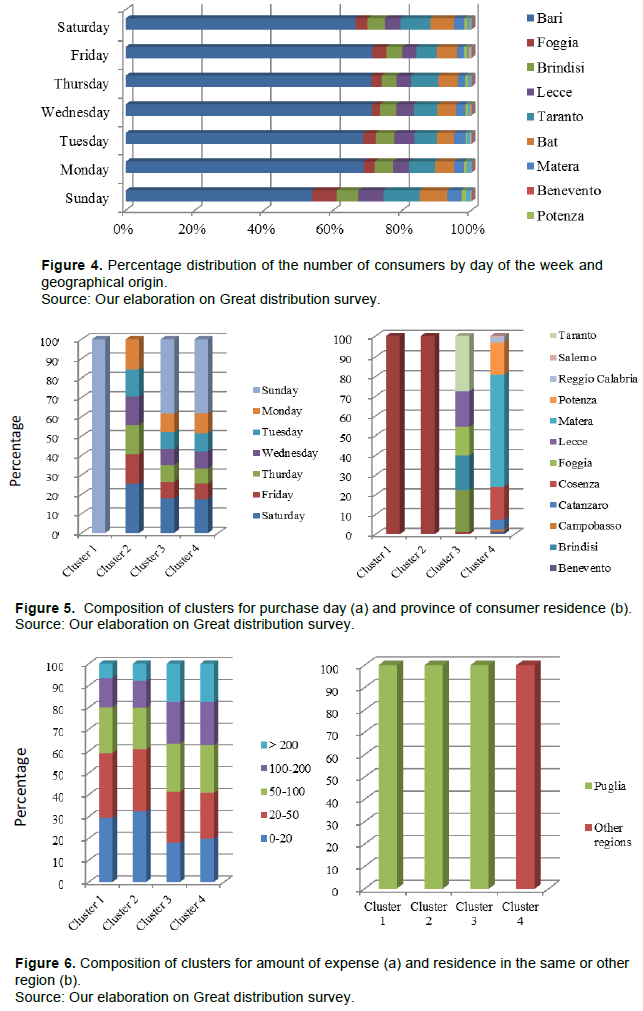

A further characteristic of the profile of the Sunday consumer concerns the territorial origin. In fact, while on all days of the week consumers from Bari and the province are about 70%, on Sunday this percentage drops to 54%, leaving room for consumers from other provinces of the Puglia region or even from other regions (Figure 4). 10.6% of Sunday's consumers come from the province of Taranto, while 8% from the province of Barletta Andria Trani (BAT). But there is also a 5.3% of consumers coming from Basilicata (4.2% from the province of Matera, European capital of culture 2019, and 1.2% from the province of Potenza).

Cluster analysis on Sunday consumer behavior

The cluster analysis technique is very advantageous since it provides "relatively distinct" clusters between them (that is heterogeneous), each consisting of units (families) with a high degree of "natural association". The different approaches to cluster analysis are united by the need to define a matrix of dissimilarity or distance between the n pairs of observations, which represents the point from which each algorithm is generated.

The chosen cluster analysis technique is "TwoStep". This is an extension of the distance measures used by Banfield and Raftery (1993) based on the model, introduced for data with continuous attributes. The TwoStep algorithm has two advantages: it treats mixed-type variables and automatically determines the optimal number of clusters, although it allows to set the desired number of clusters. The TwoStep, very efficient for large data sets, is a scalar cluster analysis algorithm and can deal simultaneously with continuous and categorical variables or attributes.

It is achieved through two steps: in a first step, defined as pre-cluster, the records are pre-classified in many small sub-clusters; in a second step the sub-clusters (generated in the first step) are grouped into a number of clusters that optimizes the Bayesian Information Criterion (BIC) defined as: