Review

ABSTRACT

This work, part of a broader research project on the role of store brand in the competitive development of Large Scale Distribution retailers, proposes an analysis of the current situation of commercial enterprises that implement complex strategies of store brand as a strategic leverage for marketing and synthesis of a corporate philosophy based on a real brand architecture. It aims to achieve increasing levels of competitive differentiation of a horizontal nature. Today, an increasing number of distributors transfer the knowledge and trust built over many years of activity, making it a private label for strategic decisions of the enterprise.

Key words: Store brand, retail marketing, MDD, differentiation, retail management, private label, retailer.

INTRODUCTION

The increasing tendency of some Large Scale Distribution retailers to transfer the assets of the trust and loyalty built up over the years on a private label elevating it to a strategic driver of competitive horizontal differentiation, originates from the evolution of the relationship between store, brand, and customer and from increase of the penetration rate of the store brand.

The implication of these assumptions guides the present contribution to the analysis of the marketing skills of the retailer that takes the declination of the store brand as the lynchpin of the differentiation strategy, with the aim of increasing the level of partnerships with selected suppliers to direct the choices of consumers and to strengthen the ability to generate added value in the trading system.

The first part of the work highlights, [S1] through a brief review of the relevant literature, the evolution of the concept of private label in recent decades. Then, on the base of the literature reviewed, it exposes the more intelligible data about the current state of the private label in Italy and the implications that these data have on companies adopting strategies of store branding. The impact of these decisions on the balance of the vertical chain and competition between retailers is high lighted.[S2]

The limitations of the paper are related to a prevalent finding and describing structure of the current situation.

However, it is the source of a research project that will make benchmark between retailers and will analyze [S3] the degree of perception of value delivered by customers/ consumers through questionnaires and interviews.

[S1]The firts part of the work highlights,

[S2]devide this long paragraph in 3 sentences:

...in recetnt decades.

Then, on the base... on companies adopting strategies of stoe branding.

The impact of these decisions on... is highlighted.

[S3]Of the current situation.

However, ...

THE DEVELOPMENT OF PRIVATE LABELS: LITERATURE REVIEW AND THEORETICAL IMPLICATIONS

Sharoff B., the president of PLMA (Private Label Manufacturers Association), underlines that the concept of private label is not a "new" concept and is even older than the industrial brands. In fact, more than two centuries ago, retailers developed awareness of the need to sell quality products, and they had to pack them with their name, in order to generate customer loyalty. For this reason, the first case of private label can be considered one of the names that the dealer puts on the card that physically packaged sugar, salt and other products.

The first examples of private labels, as we know it today, date back to some of the initiatives already taken place in the twenties in the United States, where it witnessed the start of a process of modernization in the industrial and commercial markets.

Since 1967, with the help of Myers, the international reference has shown increasing attention to the issue of the store brand, going gradually from one side to justify the increase of the market share developed by private label and the impact that the modern distribution has on upstream and downstream relationships and on the other [S1] the motivations that drive consumers to buy branded products distributor.

Myers, in particular, focuses on the relationship between disposable income and level of purchase of private label, resulting in a series of studies in the '70s and '80s investigated the socio economic variables income, age, education, number of family members as determinants for purchase.

An important essay in respect of the key variables for the purchase of private label products was given by Bettman (1984); in particular, the author focuses on three aspects: the quality perceived by consumers in respect of private label products, the risk in terms of differential warranty with industrial brands, and familiarity that consumers attach to private label products.

Richardson (1996) summarizes in a single model the contributions previously developed in order to create a single model to interpret the needs and motivations of private label purchase, identifying different classes of variables that may encourage consumers to opt for the products of retailers.

For a long time the reference literature has identified the "convenience" as the key factor in the sales of private label: the competitiveness of the private label is mainly due to the low price which is offered to the market, since retailers typically take strategies to streamline production, packaging and communication costs (Cunningham et al., 1982; Baltras, 1997; Putsis and Dhar, 2001).

Therefore, from the point of view of demand, consumers tend to associate a poor quality or a quality still lower than the big industrial brands to low price (Richardson et al., 1994; Sprott and Shimp, 2004). Through repositioning policies made by retailers, the consumer behaviour is gradually changing and tends more and more to recognize in private label, as well as price advantages, also benefits in terms of expansion of assortment and intensified promotional activity (Pauwels and Srinivasan, 2004).

In this regard, significant essays aimed to investigate the optimal level of private label products ( Winningham, 1999; Apelbaum et al., 2003) and the factors that can convince the consumer to purchase it (Shimp Sprott, 2004; De Wulf et al, 2005), in order to the retailers better exploit the potential benefits of private label.

Contrary to what has been thought and said for a long time, Apelbaum et al. (2003) point out in their research work that it is necessary [S2] to propose a high level of quality, combined with a lower price than the large industrial brands, in order to increase the level of differentiation and competitiveness of retailers. Not withstanding the importance of "convenience" to the end users, other auth[S3] ors analyze different tools to support the development of the private label. Among these Ceccacci (2013) stresses the importance of the development of the packaging in order to facilitate the communicative relationship between retailers and consumers, ensure the visibility of the product and improving brand recognition, with effects on the degree of vertical and horizontal differentiation. The packaging has a high communicative value and is an expression of the position chosen by the commercial (Cristini, 1994).

Sprott and Shimp (2004) stress the importance of in store promotion especially the sampling- to launch and consolidate the brand names, and compensate for the imbalance created by the advertising campaigns, which, for a long time, benefited only the industrial brands. The store itself, in recreational, emotional and social[S4] terms, has a strong motivation in encouraging the purchase by the final consumer, and greater interest in the products of the brand name (De Wulf et al., 2005).

In subsequent years, researchers [S5] start to give importance to other factors such as perception of promotional offers (Burton et al., 1998) and the role of product categories (Batra and Sinha, 1999). More recently, personality traits of consumers are taken into account and the different [S6] reactions to marketing stimuli resulting from them (Dalli and Romani, 2003), as well as ludic and hedonistic aspects related to consumption (Ailawadi et al., 2001).

In this regard, are important essays aimed at analyzing the relationship between the industrial and commercial brands: Quelch and Harding (1996) have a competitive perspective with regard to this report, pointing out that private labels can pose a serious threat to the 'manufacturing industry, due to several factors, including the strategic importance with the increasing quality of private label products; also the development of new innovative channels - mass merchandisers and warehouse Clubsable to launch new brands and new product categories potentially conquerable by retailers is likewise important.

Based on the growing success of private label brands in terms of market share, it is considered appropriate that the big companies put in place efficient strategies to engage the problem: the first of these is definitely the selling price, variable on which retailers are able to have a greater competitive advantage, because generally support lower cost, by contacting co-packer that need to dispose of excess production capacity, not incurring costs of advertising, can therefore offer the most competitive prices (Kotler, 1994). The progressive increase in the quality of private label products and the continued commitment of retailers to perceive the value of the products pose a serious threat to the major manufacturing industries.

Another area of strong competition is promotional, as commercial enterprises serving mainly the in-store promotions to increase sales of private label products and, consequently, the industrial brands tend to develop more and more such initiatives in order to compete directly and not to lose confidence on the part of consumers (Manzur et al., 2009). In contrast, the manufacturing industry maintains a communicative advantage through advertising, which remains a powerful tool for brand image and brand loyalty at the expense of business competition.

The tool of advertising, however, has a positive effect on the relationship between industry and distribution, with beneficial implications for both parties, as it may be practical to limit the entry of new competitors and to facilitate communication in the industrial distribution channel (Parker and Kim, 1997). In addition, the advertising differentiates a product from the competition, but at the same time draws attention to a specific category, generating indirect benefits on the store and on other brands and generating higher revenues upstream and downstream; so industrial and commercial enterprises have in common the process of co-packing: private label products, however, come from a manufacturing industry, with mutual benefits for the industry and the retailers (Dunne and Narasimhan, 1999) and with the ability to develop a cooperative viewpoint largest, towards forms of real co-marketing (Dioletta and Sansone, 2000).

In order to identify the characteristics of the markets in which it would be introduced private label distributor and the determinants of the different market shares achieved by different retailers in different categories, it may be made reference in search of Raju, Sethuraman and Dhar (1995). These authors show that the traditional idea why the store brand has more success in such price sensitive markets has to be revised, because in that way we can talk about two types of price competition, one between industrial brands instead on brands as an alternative to commercial producers.

In this regard, Rubio and Yague (2009) propose a synthesis model of the determinants of the market share of the store brand, delineating between the macro classes variables market structure, the demand charac-teristics, the financial objectives and competitive strategy.

Other factors affect the choice of the brand's distributor and can be classified in three dimensions: size qualifying - intrinsic quality, value, safety size of consolidation - perceived quality, diversity, ethics dimensions differentiating exclusive image, innovation, emotion (Cristini, 2014).

Many authors have also analyzed the benefits that the adoption of store branding strategies can bring to retailers. A number of studies [S7] have highlighted the contribution to the profitability of retailers and the effect on the relative distribution of power between retailers and producers (Meza, Sudhir, 2003; Harlam, 2004). Others [S8] have considered the contribution of the private label to differentiation of signs (Sudhir, Talukdar, 2004) and store loyalty (Corstjens Lal, 2000; Ailawadi et al., 2008).

The evolutionary dynamics of the determinants subject of research for a long time will inevitably have an impact on the very concept of store brands, generating the need to identify the different strategies implemented by commercial distributors as a result of socio economic motivations changing, of purchase and consumer proposition used in competitive dynamics and, therefore, the different levels of variation of a private label: products that focus on price competition generic private label and copycat brands those that compete in terms of quality premium brand and ultimately representative products of value and of strategic positioning of the retailers store brand (Kumar and Steenkamp, 2007).

The strategic choice of store branding adopted is therefore affected by a combination of different factors - the positioning of the product - resulting in the value defined by the distributor - the integration of the levers of retail marketing and increased reliability and guarantees of quality of retailer’s private label (Lugli, 2003; Cristini, 2006).

Confirming the development strategies of store branding, in January 2014 ADM showed the choice of words to replace the term Private Label by Brand Distributor (MDD), with the aim of emphasizing the real value of store brand product, and the ability to compete in this - both from the point of view of both tangible characteristics in the image - with the private label industry, in order to strengthen the competitive position of the retailer and to redesign the strategic balance in the supply chain.

The life cycle of private label

Since its origin, the store brand has evolved into several stages that represent the historical and strategic phases of management of private labels by retailers; in particular the life cycle of the store brand is divided into four generations.

The first phase is characterized by policies of retailers that aim to increase margins and reduce the price competitiveness in the store, through generic brands, primarily in commodity products, focusing then on the lever of the price convenience offered to customers through space large enough but little care in the packaging and packaging.

Over time, the need of commercial enterprises to differentiate their offerings from competitors increases, they did not directly employ the image of the store, but they use brands of fantasy not related to retailers: the second generation of the life cycle of store brand is characterized by an expansion of both categories manned, and the number of products for each category. In general, from the point of view of quality, private label products are better than the first generation of store brand, but the main competitive edge is still the price.

The success and increasing market share of store brand begin to explain to retailers that the products of private label can have a more strategic role beyond that of a mere increase in margins and profit, by acting as a lever to vertical competition useful for increasing the bargaining power and reduce the market share of the big brands: we thus move to the third generation of private label, which provides a direct involvement of the retailers in the products offered and culminates with the using of retailer name. In this phase [S9] the quality of products increases, because of the direct involvement of the retailer, but the price is lower than the industrial market leader: this is one of the key success factors of private labels that leads retailers to expand the range of products and to introduce new segments.

At this stage of development of the private label it lacks specific marketing skills of retailers and a conscious branding strategy: for example, the packaging is still not very detailed and the price is not uniform in the various markets served. During the fourth step of private label evolution, retailers acquire marketing skills in order to manage their products as a real industrial brand.

At this stage companies use all the levers of the marketing mix to position and support the products, strategic planning is shared and effective, the quality of the products tends more than that of the market leader, the packaging is accurate in every detail, it also increases the use of advertising.

The knowledge attained by retailers is also evident inside the store, in which they take a lot of promotion not just price promotion and much shelf space is reserved for private label products, strategically positioned in the layout of the store: the brand name becomes as drivers of the development of the retailer and competitive differentiator for vertical and horizontal level.

[S1]and on the other...

you mean “ [S2]that it is”?

[S3]“authors” why “Authors”?

[S4]In recreational, emotional and social terms.

[S5]Researchers/ or studies...

[S6]Inverse the sentence!!!

[S7]. A number...

[S8]2005). Others ...

[S9]You mean “this phase”?

EVOLUTIONARY TRENDS OF STORE BRAND IN ITALY: RESULTS AND DISCUSSION OF SECONDARY DATA ANALYSIS

In order to analyze the marketing skills of retailers and hypothesize possible future scenarios of store branding strategies, it is appropriate to briefly describe the current status of private label in Italy, through the analysis of the main data in this regard.

The general stagnation in consumption, in recent years, facilitates the penetration of private label products that have the name of the retailers: it is now customary to find private label products in the shopping cart of Italian consumer. The trend that for years has been recorded in other countries such as the UK, Spain or Germany, is now developing also in Italy (Symphony IRI): the report “Marca” by AdemLab shows that on average 93% of Italians buy at least one private label product.

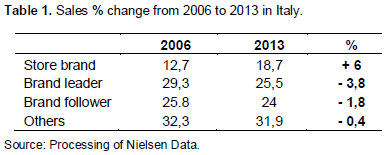

Considering the channels Hypermarket and Super market, the store brand has grown by 0.8% in value market share and now accounts for 18.4% of sales; unit market share grew by 0.5 to 22.4% (Symphony IRI, 2013).

Sales of the main retailers on the Italian market - Conad, Coop, Esselunga, Carrefour are overseen by 60% from private label products, that means in terms of units, one out of four of sold products are by private label.

The obvious relevance of these data (Table 1) leads to investigate the reasons why the sales of private label grow despite the general decline in consumption, in 2012 they even managed to buck the trend of total food sales, which remained positive thanks to the development of store brand development (Symphony IRI). One of the main reasons is certainly due to the phenomenon of trading down -which currently characterizes all categories of products- and always looking for convenience of consumers, factors that undoubtedly promote private labels.

The increasing sensitivity of consumers to price leverage is an important variable, but it is not enough to justify the above trends, so it has to refer to the totality of what motivates Italian consumers to purchase store brand products. In 2013, the price gap between private label and industrial brand has even reduced: against the increasing of promotional pressure of industrial brands, there was a reduction in the percentage volume of private label discount from 16, 5% to 16.2%.

In Europe, the store brand is on average cheaper by 29.9% compared to the same industrial brand products, with the greater price difference in France and Germany and lowest in the Netherlands, Great Britain and Italy (Symphony IRI).

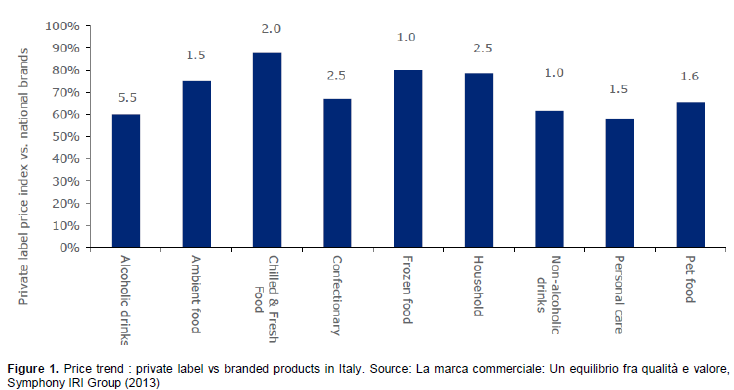

On the other hand, a growing number of investments by retailers aim to improve product quality and the consumer perception. This is done to expand market share and penetrate more segments; for example the certification and quality control of private label are increasing (Figure 1). [S1]

[S1]Need to restructure this sentence.

In particular, the retailers address the business strategies of store branding in six segments: biological / ecological, regional, functional foods, baby products, ready meals and premium products (Marca Report July 2014). This trend aims to further reduce the price gap and move the increasingly competitions between industry and distribution on the lever of quality. According to data from Symphony IRI investment by European retailers on premium products has generated retailer’s revenue growth of 0.4% and it has contributed to the quality perceived by the consumer.

The initiatives of retailers in terms of extension of lines and references are clearly feedback in consumer behaviour, finding supported by the numbers: the AdemLab Report shows that from 2012 to 2013 the premium brands have registered an increase of 14.7% in value and 13.2% in volume, while the private label biological products grew by 8.9% in volume and 5.9% in value, compared to an average growth of the private label 4% by volume and 1.2% in value;[S1] since once again confirms the growing trust of consumers towards private label products.

Therefore, from the analysis of the data it is possible to highlight the growing trend of commercial enterprises to manage strategically the store brand: an approach finalised to have just increasing income through private label is overcome. The new approach of retailer requires increasing marketing skills by retailers.[S2]

CONCLUSION AND MANAGERIAL IMPLICATIONS

The store branding strategy is characterized by the use by retailers of brand name in a growing range of products in order to increase its attractiveness in the market and pursue increasing levels of competitive differentiation of a horizontal nature, through processes and levers that influence the horizontal and vertical relationships in the supply chain.

The analysis highlights the new challenges of organizational and managerial skills and the need of marketing planning that involves all retail management, with the objective to develop, organize and manage an effective strategy for private label. It configures such a device evolving from the tactical to the strategic level whose contribution is manifested in a tangible way with the improvement of the competitive potential, with the overall development of a commercial firm, and monetary benefits in terms of profitability. This makes it possible, at this stage of the life cycle of the development of store brand, to verify specific skills of retail management in order to increase the total economic and relational value of retailers.

CONFLICT OF INTERESTS

The author has not declared any conflict of interests

REFERENCES

|

Ailawadi KL, Harlam B (2004). An empirical analysis of the determinants of retail margins: the role of store brand share, J. Market. 68. http://dx.doi.org/10.1509/jmkg.68.1.147.24027 Crossref |

||||

|

Ailawadi KL, Pauwels K, Steenkamp EM (2008). Private Label use and store loyalty, J. Market. 72. http://dx.doi.org/10.1509/jmkg.72.6.19 Crossref |

||||

|

Baltras G (1997). "Determinants of store brand choice: a behavioral analysis", J. Prod. Brand Manage. 6(5):315-324. http://dx.doi.org/10.1108/10610429710179480 Crossref |

||||

|

Bettman J (1984). Relationship of information-processing attitude structures to private brand purchasing behaviour, J. Appl. Psychol. 59(1):79-83. http://dx.doi.org/10.1037/h0035817 Crossref |

||||

|

Corstjens M, Lal R (2000). Building store loyalty through store brands, J. Market. Res. 37. http://dx.doi.org/10.1509/jmkr.37.3.281.18781 Crossref |

||||

| Cristini G(2006). Marketing d'insegna e marca private. Strategie e implicazioni operative per distributor e copackers. Milano, Il Sole24ore. | ||||

| Cunningham ICM, Hardy AP, Imperia G (1982). "Generic brands versus national brands and store brands", J. Advert. Res. 22(5): 25-32. | ||||

| Kumar N, Steenkamp JE (2007). Private Label Strategy: How to Meet the Store Brand Challenge, Harvard Business School Pr. | ||||

| Lugli G (2003). Branding distributivo: dalla marca di prodotto alla marca di categoria. Milano: Egea. | ||||

| Lugli G, Pellegrini L, (2003). Marketing distributivo, Torino: Utet. | ||||

| Marca (2014), X Report annuale sulla marca commerciale, Adem Lab. | ||||

| Meza S, Sudhir K (2003). The role of strategic pricing by retailers in the success of store brands, Quantitative Marketing and Economics. | ||||

|

Myers JG (1967). Determinants of private brand attitude. J. Market. Res. 4(1):73-81. Crossref |

||||

|

Putsis Jr. WP, Dhar R (2001). An empirical analysis of the determinants of category expenditure, J. Bus. Res. 52(3):277-291. http://dx.doi.org/10.2307/3150168 Crossref |

||||

|

Raju JS, Sethuraman R, Dhar SK (1995). The introduction and performance of store brands. Manage. Sci. 41(6). Crossref |

||||

|

Richardson PS, Jain AL,Dick A(1996). The influence if store aesthetics on evaluation of private label brands. J. Prod. Brand Manage, 5(1),19-28. http://dx.doi.org/10.1108/10610429610113384 Crossref |

||||

|

Rubio N, Jague MJ (2009). The determinants of store brand market share.A temporal and cross-sectional analysis. International J. Market Res. 51. http://dx.doi.org/10.2501/s1470785309200700 Crossref |

||||

|

Sudhir K, Talukdar D (2004). Does Store Brand patronage improve store patronage? Review of Industrial Organization, 24. http://dx.doi.org/10.1023/b:reio.0000033353.52208.ba Crossref |

||||

| Symphony IRI group (2012). Le Private Label in Europa- 2012. Esiste un limite alla crescita. | ||||

| Symphony IRI group (2013). La marca commerciale: un equilibrio fra qualità e valore. | ||||

Copyright © 2024 Author(s) retain the copyright of this article.

This article is published under the terms of the Creative Commons Attribution License 4.0